Embed Size (px)

Citation preview

Kogut, BruceJoint Ventures and the Option to Expand and AcquireManagement Science, 1991

Eva Herbolzheimer University of Illinois at Urbana-

Champaign

Objective Applying the Real Options Theory on Joint Venture decisions Firm’s problem when deciding whether to invest and expand

into new market: uncertainty of demand Firm’s initial investment in new market: can be considered as

right to expand in the future Right to expand is a “real option”

(need not be exercised!!) Joint Venture does not only share risk, but

might also decrease investment

Joint Ventures and the Option to Expand and Acquire

Introduction

Buying conditions : The net value of purchasing the JV must be at least equal to the value of purchasing comparable assets on the market

To exercise the option to expand requires further commitment of capital, thus requiring renegotiation among the partners One possible outcome is that the party placing a higher value on this new capital commitment buys out the other

Distinction between option perspective on acquisitions motivated by industry or growth conditions

Joint Ventures and the Option to Expand and Acquire

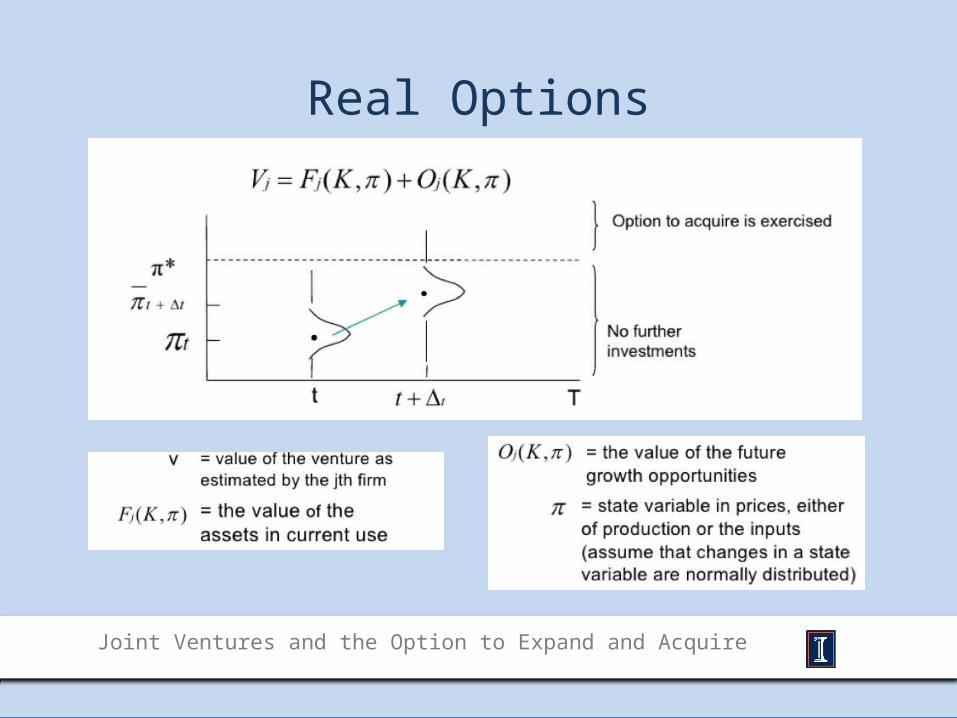

Real Options

Joint Ventures and the Option to Expand and Acquire

Joint Ventures as Real Options

Why are joint ventures analogues? (two polar types)1) Waiting to invest, whereby it pays to wait before committing

resources 2) Option of expanding production, where investment is necessary

to have the right to expand in the future JV bridges these options through pooling resources of two or

more firms The divesting firm is willing to sell if it realizes capital gains or it

does not have the downstream assets to bring the technology to market

Joint Ventures and the Option to Expand and Acquire

Timing of Exercise

The exercise of option to acquire the joint venture is likely to be immediate for two reasons:

1) the value of the real option is only recognized by making the investment and realizing the incremental cash flows. If the investment in new capacity is not made in a period, the cash flows may be lost

2) The necessity to increase the capitalization of the venture invariably requires a renegotiation of the agreement, which often leads to its termination.

The option to expand the investment is likely to coincide with exercising the option to acquire the joint venture.

Joint Ventures and the Option to Expand and Acquire

Selective Cues and Market Valuation

There is little guidance for establishing the base rates that might be used for irregular decisions, such as the acquisition of a joint venture

Camerer (1981): individuals rely upon only a few cues of those available

Experiment with two time-varying specifications of the market cues relevant to the acquisition decision

1) The short-term annual growth rate (value of product shipment) = Changes in the value of PS for the industries over an annual interval

2) The residual error (derived from an estimated regression of the time trend in shipment growth)

Joint Ventures and the Option to Expand and Acquire

Data Collection

Questionnaires: Samples included only ventures in the manufacturing industry located in the U.S. with at least one American firms in the joint venture. 92 usable responses from the manufacturing industry

Bureau of census firm concentration ratio at the four-digit SIC level Department of Commerce Unpublished data on Annual shipments (at

the four digit in constant 1982 dollars for the years 1965-1986) Dummy variables (R&D, Production and Marketing) are created

from questionnaire data

Joint Ventures and the Option to Expand and Acquire

Results (I)

Joint Ventures and the Option to Expand and Acquire

Results (II)

Joint Ventures and the Option to Expand and Acquire

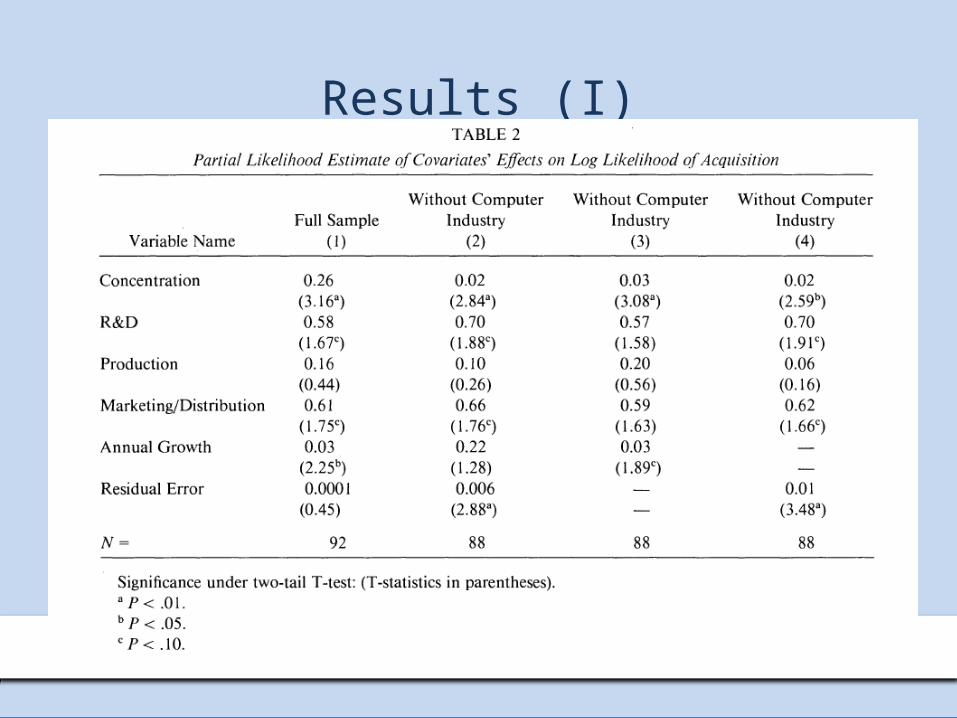

In concentrated industries, joint ventures appear to be used as an intermediary step towards a complete acquisition

Joint ventures are often part of the restructuring of mature industries, either due to new (foreign?) competition or to efforts to stabilize the degree of rivalry

By acquiring the assets, a shifting of ownership occurs without an increase in industry capacity

Ventures with R&D activities or marketing and distribution activities are more likely to be acquired

Results without the Computer Industry are kinder to the proposition that managers are sensitive to long-term intra-industry base rate Serves as standard by which to evaluate annual changes

Discussion of Market Signals

Joint Ventures and the Option to Expand and Acquire

The above findings indicate that increases in excess of the long term trend in shipment growth are significantly related to the timing of the acquisition of ventures. Managerial decisions are cued by market signals that the venture’s value has increased New variable “Change in Concentration”

BUT: No support that consolidation leads to an increase in acquisition Argument

Possible other interpretation: managers are myopic and fail to consider that short term deviations may be outliners Dissolve decision when market turns down? NO! Once the capital is committed, the downside risk is low

Strong support that JVs are designed as Options

Conclusion

Joint Ventures and the Option to Expand and Acquire

Joint ventures are designed as options that are exercised through a divestment and acquisition decision

Factors like unexpected increases in the value of the venture and the degree of concentration in the industry increases the likelihood of an acquisition

Though a signal that the venture’s value has increased should lead to an acquisition, a signal that it has decreased should not lead to dissolution, as long as further investment is not required and operating costs are modest

Firms may profit from uncertainty- more flexible production processes- platform for possible future development