Embed Size (px)

Citation preview

1

Krause Fund Research Spring 2021

Stock Performance Highlights

Source: Krause Fund Model

FEDEX CORPORATION (NYSE: FDX) INDUSTRIALS RATING: BUY

Analysts: Carson Steffen Drake Evans Dee Le Target Price: $342-$389

March 26th, 2021

[email protected] [email protected] [email protected]

Investment Thesis

March 26th, 2021

We recommend a BUY rating for FedEx Corporation.

Drivers of Thesis:

❖ Currently monopolizing the Sundays and holiday

shipments.

❖ Strong e-commerce growth during and after the

COVID-19 pandemic elevates the demands for

shipping delivery services.

❖ Loosening of trade restrictions post-pandemic

increases revenue generated from international

transactions.

❖ Replacing old aircrafts and increasing uses of new

technology to optimize the Express and Ground

operations while reducing their costs.

Risks of Thesis:

❖ Low senior unsecured debt credit ratings potentially

decrease future access to capitals.

❖ Corporate tax hike adds more income tax expenses,

lowering profitability.

❖ Competition threats imposed by Amazon in the long

term.

Stock Performance Highlights

Current Price $281.34

52wk Range $103.40 - $305.66

Beta 1.032

Average Daily Volume 2.27 M

Share Highlights

Market Capitalization $75.16 B

Shares Outstanding 265.34 M

EPS (TTM) $11.36

P/E Ratio (TTM) 24.94

Dividend Yield 0.92%

Dividend Payout Ratio (most recent) 23.05%

Financial Ratios (2020)

Cash Ratio 0.47

Asset Turnover 0.27

Debt/Equity 2.06

ROE 7.03%

Operating Profit Margin 3.49%

ROA 1.75%

Dividend Payout Ratio 23.05%

Company Overview

FedEx Corp. is a global leader in providing integrated

freight & logistics services, based in Memphis,

Tennessee. They operate under four main segments:

FedEx Express, FedEx Ground, FedEx Freight, and

FedEx Services. Their FedEx Express unit is the world

largest transportation provider to 220 countries and

territories. FedEx maintains a fleet of over 680 aircrafts

and 183,000 vehicles. About 70% of their revenue is

generated in the United States.

EPS Forecasts

12 Months FDX Stock Performance VS. S&P500

2

Our group of analysts recommends a BUY rating for shares

of FedEx. Our predictions show an upside of 20% over the

next five years due to higher online consumption. Moving

forward, we believe that FedEx will become upgrade their

technology and become one of the most efficient package

service providers. The recent merger with TNT Express in

Europe will also make them a global leader in parcel delivery

services in the years to come. FedEx managed to keep their

delivery percentage higher than expected at the beginning of

the pandemic and we predict their revenue to get stronger.

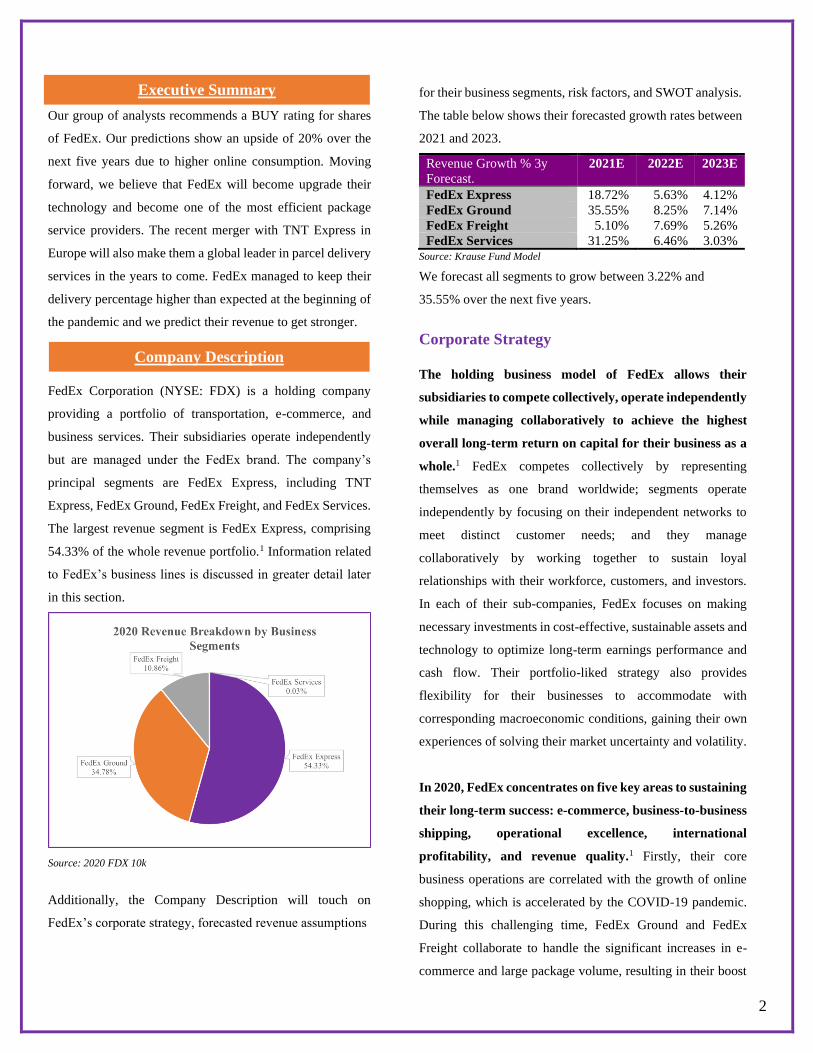

FedEx Corporation (NYSE: FDX) is a holding company

providing a portfolio of transportation, e-commerce, and

business services. Their subsidiaries operate independently

but are managed under the FedEx brand. The company’s

principal segments are FedEx Express, including TNT

Express, FedEx Ground, FedEx Freight, and FedEx Services.

The largest revenue segment is FedEx Express, comprising

54.33% of the whole revenue portfolio.1 Information related

to FedEx’s business lines is discussed in greater detail later

in this section.

Source: 2020 FDX 10k

Additionally, the Company Description will touch on

FedEx’s corporate strategy, forecasted revenue assumptions

for their business segments, risk factors, and SWOT analysis.

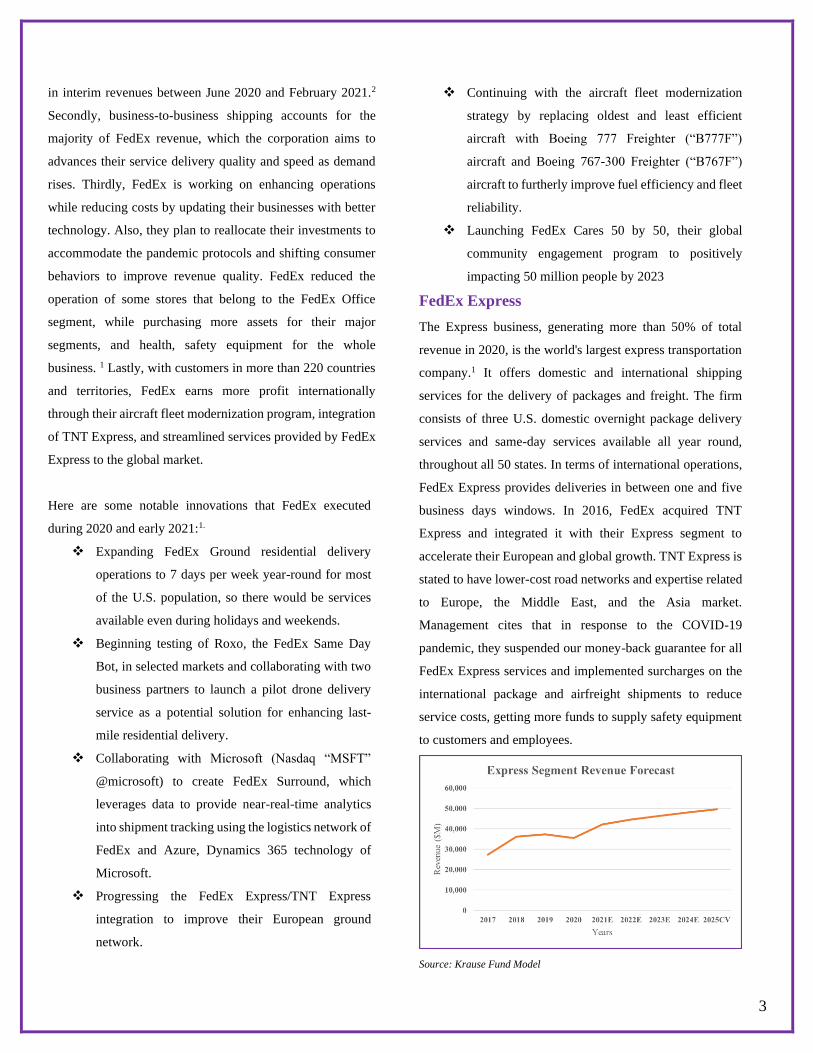

The table below shows their forecasted growth rates between

2021 and 2023.

Revenue Growth % 3y

Forecast.

2021E 2022E 2023E

FedEx Express 18.72% 5.63% 4.12%

FedEx Ground 35.55% 8.25% 7.14%

FedEx Freight 5.10% 7.69% 5.26%

FedEx Services 31.25% 6.46% 3.03% Source: Krause Fund Model

We forecast all segments to grow between 3.22% and

35.55% over the next five years.

Corporate Strategy

The holding business model of FedEx allows their

subsidiaries to compete collectively, operate independently

while managing collaboratively to achieve the highest

overall long-term return on capital for their business as a

whole.1 FedEx competes collectively by representing

themselves as one brand worldwide; segments operate

independently by focusing on their independent networks to

meet distinct customer needs; and they manage

collaboratively by working together to sustain loyal

relationships with their workforce, customers, and investors.

In each of their sub-companies, FedEx focuses on making

necessary investments in cost-effective, sustainable assets and

technology to optimize long-term earnings performance and

cash flow. Their portfolio-liked strategy also provides

flexibility for their businesses to accommodate with

corresponding macroeconomic conditions, gaining their own

experiences of solving their market uncertainty and volatility.

In 2020, FedEx concentrates on five key areas to sustaining

their long-term success: e-commerce, business-to-business

shipping, operational excellence, international

profitability, and revenue quality.1 Firstly, their core

business operations are correlated with the growth of online

shopping, which is accelerated by the COVID-19 pandemic.

During this challenging time, FedEx Ground and FedEx

Freight collaborate to handle the significant increases in e-

commerce and large package volume, resulting in their boost

Executive Summary

Company Description

3

in interim revenues between June 2020 and February 2021.2

Secondly, business-to-business shipping accounts for the

majority of FedEx revenue, which the corporation aims to

advances their service delivery quality and speed as demand

rises. Thirdly, FedEx is working on enhancing operations

while reducing costs by updating their businesses with better

technology. Also, they plan to reallocate their investments to

accommodate the pandemic protocols and shifting consumer

behaviors to improve revenue quality. FedEx reduced the

operation of some stores that belong to the FedEx Office

segment, while purchasing more assets for their major

segments, and health, safety equipment for the whole

business. 1 Lastly, with customers in more than 220 countries

and territories, FedEx earns more profit internationally

through their aircraft fleet modernization program, integration

of TNT Express, and streamlined services provided by FedEx

Express to the global market.

Here are some notable innovations that FedEx executed

during 2020 and early 2021:1.

❖ Expanding FedEx Ground residential delivery

operations to 7 days per week year-round for most

of the U.S. population, so there would be services

available even during holidays and weekends.

❖ Beginning testing of Roxo, the FedEx Same Day

Bot, in selected markets and collaborating with two

business partners to launch a pilot drone delivery

service as a potential solution for enhancing last-

mile residential delivery.

❖ Collaborating with Microsoft (Nasdaq “MSFT”

@microsoft) to create FedEx Surround, which

leverages data to provide near-real-time analytics

into shipment tracking using the logistics network of

FedEx and Azure, Dynamics 365 technology of

Microsoft.

❖ Progressing the FedEx Express/TNT Express

integration to improve their European ground

network.

❖ Continuing with the aircraft fleet modernization

strategy by replacing oldest and least efficient

aircraft with Boeing 777 Freighter (“B777F”)

aircraft and Boeing 767-300 Freighter (“B767F”)

aircraft to furtherly improve fuel efficiency and fleet

reliability.

❖ Launching FedEx Cares 50 by 50, their global

community engagement program to positively

impacting 50 million people by 2023

FedEx Express

The Express business, generating more than 50% of total

revenue in 2020, is the world's largest express transportation

company.1 It offers domestic and international shipping

services for the delivery of packages and freight. The firm

consists of three U.S. domestic overnight package delivery

services and same-day services available all year round,

throughout all 50 states. In terms of international operations,

FedEx Express provides deliveries in between one and five

business days windows. In 2016, FedEx acquired TNT

Express and integrated it with their Express segment to

accelerate their European and global growth. TNT Express is

stated to have lower-cost road networks and expertise related

to Europe, the Middle East, and the Asia market.

Management cites that in response to the COVID-19

pandemic, they suspended our money-back guarantee for all

FedEx Express services and implemented surcharges on the

international package and airfreight shipments to reduce

service costs, getting more funds to supply safety equipment

to customers and employees.

Source: Krause Fund Model

4

Our team projects a growth period for Express’s revenue

between 2021 and 2025, based on the booming of e-

commerce, TNT acquisitions, and FedEx’s aircraft fleet

modernization strategy. Our prediction of an 18.72% increase

in sales of this segment is deduced from the positive financial

results of the previous quarters of 2021.2 The pandemic

drives the demands for Express services as well as results in

favorable exchange rates for FedEx international business.

We believe the recovery from COVID-19 from the second

half of 2021 and loosening travel restrictions will lead to a

healthy rise of 5.63% in revenue. As FedEx continues with

their aircraft upgrade scheme and Indianapolis and Memphis

hub modernization, expansion programs that increase

productivity while lowering expenses,1 Express segment

would continue generating higher earnings.

FedEx Ground

The Ground segment generates more than 30% of total

revenue in 2020 from providing low-cost small-package

ground delivery services primarily in North America. 1 The

company recently integrated FedEx SmartPost, a business-to-

consumer package business that uses US Postal Service for

the final mile delivery, into this segment to keep pace with

higher demands for residential services. Management invests

more business resources into this segment during the

pandemic, increases hiring at FedEx Ground whilst making

temporary reductions in other workforces.

Source: Krause Fund Model

Historically, the Ground segment has higher annual growth

rates than the Express segment as it is less exposed to the

complex uncertainty and interconnectedness of the global

market. The 2021 interim reports show their strong earnings

performance due to large domestic package volumes and

safety supplies, vaccine distributions.2 From 2022, we

predict this segment’s revenue will grow between 7-8%.

Online shopping trends in North America will continue to

rise, sustaining the demands for Ground services.

FedEx Freight

FedEx Freight Segment offers less-than-truckload freight

services across all lengths of haul, including FedEx Freight

Priority and Economy services. 1 They contribute 10% of the

aggregate revenue. This business line is directly involved the

Express and Ground segments; hence, their revenue growth

rate is positively correlated with other major subsidiaries.

Management recently introduced FedEx Freight Direct,

which makes deliveries straight into homes to address the

needs for delivery of heavy, bulky products to residences and

businesses during the COVID-19 pandemic. The 2021

quarterly results of the Freight subsidiary emphasize the

increasing demands.2

We project the Freight segment revenue to rise steadily in the

next five years, resulting from comparable sales trend of

Express and Ground segments.

Source: Krause Fund Model

FedEx Services

Finally, the FedEx Services subsidiary offers sales,

marketing, technology supports, and other back-office

5

functions that support their transportation segments.1 This

unit includes FedEx Office and Print Services, providing

document and business services. The plummeting drop in

revenue between 2020 and 2021 is due to their accounting

approach alteration. Management allocates revenue and

operating expenses from the Services segment to other

respective operating segments to reflect their costs’ utility.

Source: Krause Fund Model

Again, the sales of this segment change accordingly with the

transportation businesses' revenue. Therefore, they are

predicted to rise slowly around 5% yearly, sharing the same

increasing trends with other subsidiaries.

Risk Factors

While FedEx expresses strong earnings performances

during the COVID-19 pandemic, they still face negative

impacts due to uncertainty and volatile conditions of the

domestic and global markets. One of the noted risks is the

disruption of global supply chains, interruption in economic

activity, and preventative measures that reduce international

sales and make it difficult for the company to predict

services’ demands.1 Additionally, the pandemic delays their

facility expansions, information technology initiatives, and

the TNT Express integration, postponing cost reduction and

revenue-boosting schemes that FedEx aims to implement.

Remote work arrangements also increase the enterprise

transporting hubs’ exposure to cyber risks and security

collapses, which lead to loss of critical confidential

information, adversely affecting their business reputation and

competitive advantages. When approaching the recovery

phase from the pandemic, FedEx’s financial results may

suffer due to challenges on tax positions from the Biden

administration, increasingly intensive competition, rising

fuel and vehicle prices, and volatility of costs and funding

requirements for employee benefits, especially pension and

healthcare benefit. These factors would incur more expenses,

reducing their net income in the future.

SWOT Analysis

Strengths

One of FedEx’s competitive advantages is their strong brand

recognition for their Express and Ground segments’

reliability, speed, and high-quality service. 1 Notably

speaking, FedEx Express is recognized as the largest express

provider in the world. Their Ground service is distinguishing

itself from its competitors due to their Sundays and holidays

residential deliveries to much of the domestic population.

FedEx’s holding strategy allows their sub-businesses to

utilize their market-specific expertise to cope with varying

economic conditions and meet distinct customers’ demands.

It also brings more flexibility in terms of reallocating capitals

among subsidiaries, based on their quick business

restructures in response to COVID-19. Additionally,

management emphasizes their technology-orientated goals,

including the utilization of drones, robots, as well as aircraft

fleets, and facilities modernizations. These improve FedEx’s

efficiency and decrease costs in the long run.

Weaknesses

Though the significant increase in the volumes of shipments

transported during the COVID-19 pandemic boosts the

demand for FedEx’s services, it can severely affect the

company’s profitability if capacity-demand is managed

poorly, as FedEx has high operating leverage due to heavy

investment in fixed assets. Other key weaknesses are their

liquidation problems as well as lower debt credit rating

compared to its strong rivals Amazon and UPS. Standard &

Poor’s has assigned them a senior unsecured debt credit

rating of BBB with an outlook of “negative,” while Moody’s

6

Investors Service has given a “negative” rating of Baa2. 1 The

company routinely grants credit to customers without

collateral, leading to high bad debt expense and hazardous

credit risk. Also, a lot of their debts have floating interest rate,

which is adversely impacted during volatile economic

conditions. If their credit ratings drop, they may have

difficulty utilizing the commercial paper market, resulting in

limitations to access to capital.

Opportunities

The continuing impacts of the COVID-19 pandemic drive e-

commerce sales, which increases the demand for FedEx

services, resulting in improved year-over-year revenue and

operating income for the remainder of 2021. The positive

e-commerce trend is projected to sustain even after post-

COVID-19, as the internet utilization rate increases during

shelters in places or work from home scenarios, leading to

people becoming more adjusted to the amenities provided by

technology. Additionally, the pandemic economic situation

makes the exchange rates more favorable for FedEx’s

international transactions. With the loosening of preventive

measures as well as global trading restrictions due to vaccine

recess, international sales are expected to boost. Moreover, if

FedEx successfully integrates the businesses and operations

of FedEx Express and TNT Express in the expected period

and cost, they will receive more demand from the European

markets; hence expanding their profitability.

Threats

To begin with, in the short run, rising variable accruals, labor

costs, and other costs related to the COVID-19 pandemic

would continue incurring in the remainder of 2021. Besides,

there will be headwinds related to the December 31, 2020,

expiration of the aviation excise tax holiday created by the

CARES Act and a higher effective income tax rate for the

second half of 2021. In March 2021, the Biden administration

was eyeing a major corporate tax hike to 28% from 21%,

which might lead to higher income tax expenses for FedEx.3

Secondly, the current government-related travel restrictions

make any expectations for the second half of 2021 to be

inherently less certain. Thirdly, as mentioned in our Risk

Factors section, cyber risk exposure during the pandemic

might harm their reputation, deteriorating their competitive

advantages. Overall, the company’s most prominent threat is

intense competition, posing by Amazon’s own shipping

delivery services. Amazon is aiming to expand its logistic

network and developing drone technology, which might

undermine FedEx in terms of pricing and speedy services.

World GDP

Source: International Monetary Fund (shown bigger in Appendix 1)

The global GDP has made significant rebounds since the

beginning of the COVID-19 pandemic. This heat map shows

first-quarter GDP changes by country around the world. The

dark green colors show higher growth change in GDP while

red stands for loss. This is an incredibly positive sign for all

business and economic sectors because it shows that the

world's economy is growing which will lead to business-to-

business growth all around the world.

U.S. GDP

Source: Bureau of Economic Analysis

Economic Outlook

7

This chart shows RGDP percentage change each quarter for

the last four years and into 2021. The US shows an increase

in Real GDP of 4.6% after the first quarter of 2021 while we

still work our way through the pandemic. With a vaccine now

being vastly distributed and implemented throughout the

country capital markets and economies are slowly moving

back to full functionality which we assume will lead to even

further GDP growth throughout the rest of the year.

COVID-19 Impacts

While economies and global GDP have rebounded from the

pandemic there is still concern as to variants in COVID and

the lasting effects of the vaccine. One of which has just been

recalled for a rare blood clotting. If there was a variant that

was not susceptible to the antibodies being administered right

now, we could be heading for another shut down or the

slowing of production for business and reversing the progress

the world has been making over the past 6 months.

Consumer Spending

Consumer spending has been down throughout the pandemic

as people have been prepared for the worst. However, these

numbers have increased as stimulus has been distributed

throughout the country and people have been spending the

stimulus money if they did not exactly need it to cover living

expenses.

Interest Rates

A big concern with the cost of borrowing and interest rates

has resurfaced as the stimulus brought into the economy is

going to have to be paid and stopped sometime in the future.

While we do not know exactly when this is coming, it will

certainly have an impact on most companies and the

economies of the world. The 10yr, 20yr, and 30yr Treasury

yields have already slightly from the beginning of the

pandemic and will continue to rise going forward. This will

increase the cost of borrowing for many companies, such as

FedEx who borrows a large amount of money for the

allocation of new airplanes and other vehicles for their air and

express cargo.

Industry Description

FedEx is a part of the Integrated Freight & Logistics industry

within the Industrials sector. Integrated Freight & Logistics can

be broken down into 5 subcategories: Logistics Services, Air and

Express Delivery Services, Freight Rail, Maritime, and Trucking.

FedEx is a part of all subcategories excluding maritime.

Source: Fred Economic Data (Shown larger in Appendix 2)

Producer Price Index: Air and Express Delivery

Services

This graph is the average production price for the air and

express delivery services industry from 1994 to 2020.11 There

has been 320% growth in the price of these services over the

past 25 years. This shows that industry has steadily grown

with the economy and inflation and the companies that

deliver these services are healthy. FedEx was the North

American Leader for both freight cargo deliveries and air

cargo deliveries in 2020.

Industry Lifecycle

The main subcategories that FedEx falls under in the Air &

Freight Logistics industry are very cyclical. This is because

this industry requires the demand for consumers and

businesses to be buying and shipping products. If the

economy is in a recession or is consumer spending is lower

than this lowers the potential revenue for companies like

FedEx in this industry.

Industry Analysis

8

Industry Trends

Technology

There are many ways that FedEx and its competitors must

look at to outpace the competition in delivering product faster

and more efficient. Drone technology has been the biggest

advancement for ground and expedited delivery services that

has been in the works for years now. The freight industry has

been looking to convert their coal emitting rails into hydrogen

fuel cell rails making the deliveries more efficient and better

for the environment. Another leading technology that is not

too far from being put into use is the use of biofuels instead

of rocket fuels for jet engines. This would significantly

reduce the cost of air delivery companies like FedEx and

leave a lot of capital to buy more planes with the same

capabilities. Another advancement being made is the use of

electric or hydrogen powered trucks that could one day be

self-driving which would also significantly reduce the cost of

companies that have primary expenses being the amount of

employees that they have.

Social Changes

Consumers and Investors have become increasingly

concerned with the use of sustainable component in all

aspects of the business model. Going forward, we will see a

lot of these logistics companies pushing for advancements in

the efficiency in the vehicles that they use along with the

environmental impact that the vehicles they use have. The

companies that can become the most sustainable will be the

ones that people lean toward using. Not only will this lead to

more business, but also to lower costs if there are

governmental changes that require these companies to have

lower emissions or are subsidized for being ahead of the

competition when it comes to the use of renewable energy.

Government

As mentioned above, Government could have a lasting

impact on how companies in this industry are allowed to

operate. Depending on trade policies with foreign countries

the demand for international package transportation services

could be highly volatile which could both positively and

negatively impact potential revenue for FedEx. More

regulation that will be coming into effect in the future will

drone policy. California recently became the first state to

allow the use of drones for delivery. If many other states,

follow, or federal policy was put in place to allow the use of

drones for delivery FedEx could potentially see exceedingly

high revenue numbers if they were able to implement drones

into their services. However, if big competitors like Amazon

implement these services before FedEx this could lead to an

exceptionally large decrease in market share for the FedEx

segment all around.

Demographics

The demand for truck driver for FedEx’s ground delivery

have increased in recent years as the amount of truck drivers

in the United States has begun to decrease. This will lead to

a higher pay for the retained driver and higher operating

expenses for the company. The idea of self-driving electric

vehicles has also become more relevant with the emergence

of companies like Tesla and Nikola who forecast there will

be fully self-automated trucking available to service

companies like FedEx by the year 2024. While this would

help in no longer needing as many drivers as possible or

employees and effectively lowering the cost of operating

expenses, FedEx would now have to invest in more Property,

Plant, and Equipment which may be more costly for the

company and create liquidity issues.

Porter’s Five Forces

Degree of Rivalry/Competition: High

There is a remarkably elevated level of competition in the Air

& Freight Logistics industry. UPS and Amazon have

extremely high market capitalizations and large market

shares as well. The Unites States Postal Service is also a key

competitor however, they rely on FedEx to transport most of

their air and freight deliveries. However, those two

subcategories are FedEx’s strongholds where they are the

North American leader for both Air and Freight delivery.

9

UPS and Amazon pose the most threat to FedEx’s ground

deliveries.

Bargaining Power of Customers: Low

The bargaining powers of customers in the industry is low

since there are only a few substitutes usually offering the

same prices for the same service. What also needs to be

considered is that when consumers are buying product from

businesses, they are only usually offered one or two

companies for their potential delivery service providers.

Bargaining Power of Suppliers: Medium

Boeing, Cessna, and Airbus are the three suppliers of air

couriers for FedEx. While Freightliner, Dodge, Mercedes-

Benz, and Volkswagen make up its suppliers of trucks for

ground services. This shows that FedEx has some options

when it comes to choosing a supplier for its ground services

and may be able to lower cost for capital expenditures in that

business segment. However, there a limited aerospace

manufacturing companies in the market which means FedEx

must spend large amount of capital or take on debt at the

amount the suppliers want for their vehicles.

Threats of Substitutes: High

There is a prominent level of threat for substitutes in this

industry mostly coming from FedEx’s largest competitors in

UPS and the rise of Amazon. These companies are constantly

competing for business are always looking to lower rates for

companies and speed up shipping times where they can.

These companies also offer the similar rates and delivery

times.

Threats of New Entrants: Low

While the emergence of Amazon is a prime example of a new

entrant to the delivery service market this is a rare occurrence

because of the other services that Amazon already offers. It

would be difficult for a new company to emerge in this

already highly competitive and saturated market. The amount

of PPE and infrastructure needed to compete with FedEx,

UPS, and Amazon would be hard for a new company to

acquire and be able to offer the same delivery speeds and

pricing.

Source: FactSet

*Note: Amazon market cap ($1.7T) too large to include.

Source: FactSet

In the freight and logistics sub-industry, Property, Plant, and

Equipment is incredibly significant. Machinery and

equipment take up an exceptionally sizable percentage of

capital expenditures (47% for FedEx in 2020).2 This sub-

industry also saw a 56% increase in Net PP&E from 2019 to

2020. We included the graphs above to show FedEx in

comparison to its competitors to help forecast the future.

PP&E as a percent of total assets help display which

companies can expand domestically and internationally due

to machinery and equipment making up a large amount of

these companies PP&E. Also, this is a great indication of

which companies would be able to satisfy drastic increases in

Comparative Analysis

10

deliveries/services. As far as market capitalization, FedEx is

second largest in the industry with UPS being the largest.

Although Amazon is in a different industry, we included it in

the second chart above because many segments of their

business overlap into the same sub-industry. FedEx differs

itself from its competitors with their air fleet. They have

nearly double the air fleet of UPS leading their pricing to be

cheaper in time-sensitive delivery. FedEx also operates under

multiple networks (Express, Ground, Services, etc.) while

UPS and many of the other competitors operate as one. FedEx

also uses independent contractors for a substantial part of its

ground transportation. FedEx’s large air freight footprint is

allowing them to grow a lot faster than many of its

competitors internationally.

United Parcel Service (UPS)

UPS engages in the transportation, distribution, ground

freight, air freight, ocean freight and other logistics services.

UPS is mostly known for its specialization in ground

delivery services. UPS is the world leader in logistics with

FedEx as a close second. As opposed to FedEx, UPS uses

its own employees for all deliveries and no independent

contractors.7 UPS is a direct competitor to FedEx, and we

forecast it to continue to be. UPS is currently focusing in on

small/medium sized businesses, international markets, and

health care.5 Like FedEx, UPS currently services over 220

countries and territories.

Expeditors International of Washington (EXPD)

EXPD engages in air and air freight services as well as

temperature-controlled transit, cargo insurance, and other

logistics services. EXPD had a 2020 quarter of 55% revenue

growth compared to that of the same quarter of the previous

year.8 With this growth it is possible for EXPD to become a

bigger competitor of FedEx in coming years.

J.B. Hunt Transport Services (JBHT)

JBHT offers logistical services such as intermodal freight

operations for rail carriers as well as private fleet conversion

and final-mile delivery services.

XPO Logistics (XPO)

XPO is a trucking company that operates in two segments.

Their transportation segment engages in freight brokerage,

full truckload, less-than-truckload, last mile, and global

forwarding services. The logistics segment engages in

warehousing and distribution, inventory solutions, and other

contract logistics services.

C.H. Robinson Worldwide (CHRW)

CHRW engages in freight transporting services through

their two segments: North American Surface Transportation

and Global Forwarding.

Amazon (AMZN)

Amazon is known worldwide for their online retail shopping

services. Increasingly, Amazon is taking market share in the

logistics industry. In this recent month, “Amazon added 15

cargo planes totaling 70 in the air by mid-2021.”

Comparingly, FedEx has 680 cargo planes ten times that of

Amazon. However, Amazon has an average “click-to-door"

time of 3.2 days while the average of the freight and logistics

industry is 4.3 days.6 In response to Amazon’s insane growth,

in mid-2019 FedEx ended its service contract with Amazon.

With FedEx working on autonomous delivery robots and

Amazon working on their autonomous delivery drones, it is

going to be increasingly competitive in this industry.

Revenue

As addressed in the Company Description, we anticipate that

all FedEx’s main segments’ revenues will increase

throughout five years, leading to an overall rise in total sales

from $65,370 million in 2020 to $100,385 million in 2025.

Valuation Analysis

11

The bar chart below depicts our forecasted numbers,

portraying a steady rise in the future. The most prominent

revenue growth will occur between 2020 and 2021, because

of the major boost in online shopping in the domestic

markets. FedEx will continue with its growth, if they keep

pursuing the TNT Express integration, upgrading their fixed

assets, and implementing innovations into their operations.

Their growth rates may face declining threats due to the

Biden administration’s tax hike scheme, 3 additional

competition, and capital-intensive investments in technology.

Source: Krause Fund Model

Operating Expense

Except for 2021, we project the 2022-2024 operating

expenses as 94% of their corresponding total revenues. We

computed this percentage from taking the historical average

of the prior ten years' operating expenses as proportions of

the total revenues. The sales and operating expenses are

positively correlated with each other, as FedEx’s strategy

demands them to immediately pay for their costs incurred by

the fixed assets and reinvest their earnings into modernizing

and purchasing new machinery. In 2021, the quarterly results

suggest that there was a substantial rise in the operating

expense due to the extra costs for compensating employees,

buying medical supplies, and losses caused by the COVID-

19 pandemic. We assume the average of 2021 first three

quarters operating expenses to be the figure for the last

interim, then sum them together to get the 2021 number.

Therefore the 2021 operating expense equals 98.44% of total

sales instead of 94%.

Cost of Equity

Risk-Free Rate 1.67%

Beta 1.032

Equity Risk Premium 4.26%

Cost of Equity 6.07%

Source: Krause Fund Model

We use the CAPM model to calculate the cost of equity. Our

risk-free rate is from the 10-year US Treasury Note rate. The

beta value is taken from the Bloomberg Terminal's 2-year

raw figure, plotted weekly. Finally, the equity risk premium

is referred from professor Damodaran’s spreadsheets, which

include the implied, COVID-19 adjusted rate as of April

2021. Together, we derive a cost of the equity value of 6.07%.

Cost of Debt

Risk-Free Rate 1.67%

Implied Default Premium 0.74%

Pre-Tax Cost of Debt 2.41%

Marginal Tax Rate 25.82%

After-Tax Cost of Debt 1.79%

Source: Krause Fund Model

The pre-tax cost of debt is pulled from the FINRA website,

which lists out most of FedEx bonds. We select a contract

that expires in 2030, the one that has the closest horizon to 10

years and use its yield as our pre-tax cost of debt. Our

marginal tax rate is computed as the sum of FedEx’s

Statutory tax, state and local tax, and foreign income tax, then

dividing it by the corresponding income before tax. We then

anticipate that the future tax rates will be the same as the 2020

rate. Finally, we get an after-tax cost of debt of 1.79%.

WACC

To derive the WACC, we first calculate the equity and debt

weights. The market value of FedEx’s equity is computed by

multiplying the total number of shares outstanding by the

current stock price, which gives us $73.430 B. By adding all

the interest-bearing debts with the PV of operating leases, we

have a market value of debt figure of $37.522 B. These lead

12

to the weights of equity and debt being 66.18% and 33.82%

respectively. Finally, we get a WACC of 4.62%.

Models

Models Price

DCF/EP $388.70

DDM $342.18

P/E (Rel_EPS) $286.91

PEG (Rel_EPS) $363.93

Source: Krause Fund Model

The P/E relative valuation model has the price that is closest

to the current price of $281.34. All the peers used in the

model have a lower price than FedEx; however, their average

P/E is higher, which makes the overall estimate more

consistent. Both DCF/EP and DMM show the higher price

than FedEx’s market price, showing that the company’s

fundamental values have been underestimated by the market.

This would suggest a buy signal for contrarian investors.

Beta vs Equity Risk Premium

We compared our two year weekly average beta against

Damodaran’s equity risk premium calculation to test for

sensitivity in FedEx’s stock price from factors compared to the

overall stock market. We chose a two-year average weekly

beta instead of a five-year because we felt the five year was

not a correct representation of the average beta due to

volatility after changing corporate strategy and the acquisition

TNT. As you can see in the table above, changes in both the

beta and the equity risk premium do not cause a substantial

change in stock price. We find this to be a sign of how stable

FedEx is as a company.

CV Growth % of NOPLAT vs. Marginal Tax Rate

We next compared the CV growth % of NOPLAT against the

marginal tax rate to see how the stock price would respond in

times of change in tax. This is especially important because

with there being a new party in office, there could be a

tremendous change in marginal taxes affecting FedEx. We

tested this against CV % of growth to also see how much the

price would be affected when growing NOPLAT with

different tax levels. We forecasted conservatively in our

NOPLAT CV growth, using GDP growth of 3.1%, so this

testing will example prices at higher NOPLAT growth.

Pre-tax cost of Debt vs. Risk-free Rate

We then compared the pre-tax cost of debt calculated by

taking the rate of a 10-year FedEx bond against the risk-free

rate calculated from the rate on a 10-year US Treasury bond.

We chose these two variables due to the enormous impact they

have in the WACC which the changes of lead onto our DCF

and EP models. As portrayed in the chart above, a change in

the risk-free rate minimally affects the forecasted price.

However, a change in the pre-tax cost of debt causes a drastic

change in stock price. This is because FedEx holds 34%

market value of debt.

CV Growth of EPS vs. CV ROE

We compared CV Growth of EPS to CV ROE to test

sensitivity in our DDM model. We felt that these two variables

would be the most significant to test against each other since

they are massive parts of the DDM calculation. As expected,

changes in growth of EPS cause large price changes in the

forecasted stock price while changes in ROE cause only slight

changes in stock price.

WACC vs. CV ROIC

Lastly, we compared the WACC against the CV ROIC due to

their significant impact in our valuations. The WACC as well

as the CV ROIC are used to calculate the DCF and the EP

valuation methods. As shown in the chart above, the WACC

effects the stock price about three times more than the CV

ROIC when increasing/decreasing it by .1%. The highest price

was yielded from the lowest WACC with the highest ROIC as

we expected. We specifically wanted to test these two

variables because we believe it is quite possible for the WACC

to change due interest rates rising and the CV ROIC to change

due to the many ways Invested Capital or NOPLAT can

fluctuate.

Sensitivity Analysis

University of Iowa Krause Fund 13

1. FedEx 10K 2020

2. FactSet - FedEx

3. Bloomberg – Biden Administration tax hike

4. Thomson Reuters - XPO Logistics Inc Profile

5. UPS – Investors Relations

6. GeekWire - the next AWS

7. Diffen - FedEx vs UPS

8. CSIMarket - EXPD Growth Comparisons

9. Bureau of Economic Analysis – GDP

10. IMF – Real GDP Growth % Change

11. Fred Economic Data - Producer Price Index by

Industry

12. Bureau of Economic analysis – Personal Income and

Outlays, Feb. 2021

13. Data Source

a) FactSet – Model

b) Damodaran – Model

c) Bloomberg Terminal – Model

d) FINRA Bond Data - Model

c) Yahoo! Finance – Tear Sheet Chart and data

References

University of Iowa Krause Fund 14

Appendix 1. Bureau of Economic Analysis – GDP

Appendix 2. Fred Economic Data - Producer Price Index by Industry

Appendix

University of Iowa Krause Fund 15

Important Disclaimer

This report was created by students enrolled in the Security

Analysis (6F:112) class at the University of Iowa. The report

was originally created to offer an internal investment

recommendation for the University of Iowa Krause Fund and

its advisory board. The report also provides potential

employers and other interested parties an example of the

students’ skills, knowledge, and abilities. Members of the

Krause Fund are not registered investment advisors, brokers

or officially licensed financial professionals. The investment

advice contained in this report does not represent an offer or

solicitation to buy or sell any of the securities mentioned.

Unless otherwise noted, facts and figures included in this

report are from publicly available sources. This report is not a

complete compilation of data, and its accuracy is not

guaranteed. From time to time, the University of Iowa, its

faculty, staff, students, or the Krause Fund may hold a

financial interest in the companies mentioned in this report.

FedEx CorporationSensitivity Tables

388.70 0.43 0.63 0.83 1.03 1.23 1.43 1.63 342.18 2.20% 2.40% 2.60% 2.80% 3.00% 3.20% 3.40%3.36% 379.74 381.79 383.83 385.89 387.90 389.94 391.97 13.45% 284.33 294.12 305.05 317.32 331.18 346.98 365.15 3.66% 380.13 382.36 384.58 386.83 389.02 391.24 393.45 15.45% 291.25 302.09 314.18 327.75 343.09 360.57 380.68 3.96% 380.53 382.93 385.34 387.76 390.14 392.53 394.93 17.45% 296.59 308.23 321.22 335.79 352.27 371.05 392.64 4.26% 380.92 383.51 386.09 388.70 391.26 393.83 396.40 19.45% 300.83 313.11 326.81 342.18 359.56 379.37 402.14 4.56% 381.31 384.08 386.85 389.64 392.37 395.12 397.87 21.45% 304.28 317.08 331.36 347.38 365.50 386.14 409.88 4.86% 381.70 384.66 387.60 390.58 393.49 396.42 399.35 23.45% 307.14 320.37 335.13 351.69 370.42 391.75 416.29 5.16% 382.10 385.23 388.36 391.51 394.60 397.71 400.82 25.45% 309.56 323.15 338.31 355.33 374.56 396.48 421.69

388.70 2.80% 2.90% 3.00% 3.10% 3.20% 3.30% 3.40% 388.70 4.32% 4.42% 4.52% 4.62% 4.72% 4.82% 4.92%22.82% 339.46 354.14 370.63 389.29 410.58 435.10 463.63 6.04% 502.60 448.49 402.01 361.67 326.32 295.09 267.30 23.82% 339.28 353.96 370.44 389.10 410.38 434.89 463.41 6.14% 514.33 459.29 412.01 370.97 335.01 303.25 274.99 24.82% 339.10 353.77 370.25 388.90 410.17 434.67 463.19 6.24% 525.68 469.74 421.69 379.98 343.43 311.15 282.42 25.82% 338.92 353.59 370.06 388.70 409.97 434.46 462.96 6.34% 536.67 479.86 431.06 388.70 351.59 318.80 289.62 26.82% 338.75 353.40 369.87 388.51 409.77 434.25 462.74 6.44% 547.32 489.67 440.14 397.15 359.49 326.21 296.60 27.82% 338.57 353.22 369.68 388.31 409.56 434.03 462.52 6.54% 557.65 499.17 448.95 405.35 367.14 333.40 303.37 28.82% 338.39 353.04 369.49 388.11 409.36 433.82 462.29 6.64% 567.67 508.39 457.49 413.29 374.57 340.36 309.93

388.70 1.81% 2.01% 2.21% 2.41% 2.61% 2.81% 3.01%0.77% 367.20 373.55 379.90 386.31 392.60 398.95 405.30 1.07% 367.95 374.32 380.68 387.11 393.41 399.78 406.14 1.37% 368.70 375.08 381.46 387.91 394.22 400.60 406.98 1.67% 369.45 375.85 382.24 388.70 395.03 401.43 407.82 1.97% 370.20 376.61 383.02 389.50 395.84 402.25 408.66 2.27% 370.95 377.38 383.80 390.29 396.65 403.08 409.50 2.57% 371.70 378.14 384.58 391.09 397.46 403.90 410.34

Ris

k-F

ree

Ra

te

Beta CV Growth of EPS

Eq

uity

Ris

k P

rem

ium

CV

Ye

ar

RO

E

WACC

Ma

rgin

al T

ax

Ra

te

CV

RO

IC

CV Growth % of NOPLAT

Pre-Tax Cost of Debt

FedEx CorporationRevenue Decompositionin $ million / millions of packagesFiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

Express Segment Average Daily Package Volume (Domestic) 2.726 2.729 2.901 2.808 3.910 4.164 4.260 4.459 4.553

Package Volume (Domestic) 994.990 996.085 1,058.865 1,027.728 1,427.150 1,519.915 1,554.873 1,631.944 1,661.663

Average Daily Package Volume (International) 2.424 2.454 2.471 2.337 2.429 2.475 2.492 2.545 2.563

Package Volume (International) 884.760 895.710 901.915 855.342 886.585 903.430 909.483 931.400 935.338

Total Net Sales 27,358 36,172 37,331 35,513 42,162 44,536 46,371 48,017 49,563

% Growth 3.43% 32.22% 3.20% -4.87% 18.72% 5.63% 4.12% 3.55% 3.22%

Ground Segment Average Daily Package Volume 7.896 8.336 8.952 9.997 11.810 12.572 13.381 14.594 15.222

Package Volume 2,882.040 3,042.640 3,267.480 3,648.905 4,310.816 4,588.864 4,883.928 5,326.900 5,555.957 Total Net Sales 18,075 18,395 20,522 22,733 30,814 33,356 35,738 38,700 41,541 % Growth 9.06% 1.77% 11.56% 10.77% 35.55% 8.25% 7.14% 8.29% 7.34%Freight Segment Total Net Sales 6,443 6,812 7,582 7,102 7,464 8,038 8,461 8,867 9,244

% Growth 3.92% 5.73% 11.30% -6.33% 5.10% 7.69% 5.26% 4.80% 4.25%

Services Segment Total Net Sales 1,621 1,650 1,691 22 32 34 35 36 37 % Growth 1.76% 1.79% 2.48% -98.70% 31.25% 6.46% 3.03% 3.54% 3.16%

Total Business Segment Sales 60,898 63,029 67,126 65,370 80,472 85,964 90,604 95,620 100,385

% Growth 19.84% 3.50% 6.50% -2.62% 18.77% 6.39% 5.12% 5.25% 4.75%

FedEx CorporationIncome Statementin $millionsFiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

Total revenue 60,319 65,450 69,693 69,217 80,472 85,964 90,604 95,620 100,385

Total operating expenses -55,753 -61,178 -65,227 -66,800 -79,213 -81,081 -85,463 -90,265 -94,844

Salaries and employee benefits -21,989 -23,795 -24,776 -25,031 -30,894 -31,549 -33,252 -35,093 -36,841

Purchased transportation -13,630 -15,101 -16,654 -17,466 -22,046 -20,545 -21,564 -22,758 -23,892

Rentals and landing fees -3,240 -3,361 -3,360 -3,712 -4,302 -4,212 -4,440 -4,685 -4,919

Depreciation and amortization -2,995 -3,095 -3,353 -3,615 -3,789 -4,401 -4,734 -5,068 -5,401

Fuel -2,773 -3,374 -3,889 -3,156 -2,798 -3,954 -4,168 -4,399 -4,618

Maintenance and repairs -2,374 -2,622 -2,834 -2,893 -3,273 -3,782 -3,987 -4,207 -4,417

Asset impairment charges 0 -380 0 -435 0 0 0 0 0

Business realignment costs 0 0 -320 0 -10 0 0 0 0Other -8,752 -9,450 -10,041 -10,492 -12,101 -12,637 -13,319 -14,056 -14,757

Total operating income / loss 4,566 4,272 4,466 2,417 1,259 4,883 5,142 5,355 5,541

Total other expense / income 13 -517 -3,811 -748 229 -521 -577 -639 -693

Interest, net -479 -510 -529 -617 -508 -521 -577 -639 -693

Interest expense -512 -558 -588 -672 -572 -603 -643 -689 -737

Interest income 33 48 59 55 64 82 65 50 44

Other retirement plans income 471 598 -3,251 -122 737 0 0 0 0

Other, net 21 -7 -31 -9 0 0 0 0 0

Income before income taxes 4,579 4,353 655 1,669 1,488 4,362 4,564 4,716 4,848Provision for income taxes -1,582 219 -115 -383 -342 -1,003 -1,050 -1,085 -1,115

Net income / loss 2,997 4,572 540 1,286 1,146 3,359 3,515 3,631 3,733

Per ShareEPS 11.07 16.79 2.03 4.90 4.35 13.15 14.09 14.95 15.36

Basic Shares Outstanding 266 267 262 261 267.67 263.17 255.45 249.49 242.96

Dividends per Share 1.60 2.00 2.60 2.60 2.62 2.87 3.16 3.28 3.58

FedEx CorporationCommon Size Income Statement% of sales Fiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

Total revenue 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Total operating expenses -92.43% -93.47% -93.59% -96.51% -98.44% -94.32% -94.33% -94.40% -94.48%

Salaries and employee benefits -36.45% -36.36% -35.55% -36.16% -38.39% -36.70% -36.70% -36.70% -36.70%

Purchased transportation -22.60% -23.07% -23.90% -25.23% -27.40% -23.90% -23.80% -23.80% -23.80%

Rentals and landing fees -5.37% -5.14% -4.82% -5.36% -5.35% -4.90% -4.90% -4.90% -4.90%

Depreciation and amortization -4.97% -4.73% -4.81% -5.22% -4.71% -5.12% -5.23% -5.30% -5.38%

Fuel -4.60% -5.16% -5.58% -4.56% -3.48% -4.60% -4.60% -4.60% -4.60%

Maintenance and repairs -3.94% -4.01% -4.07% -4.18% -4.07% -4.40% -4.40% -4.40% -4.40%

Asset impairment charges 0.00% -0.58% 0.00% -0.63% 0.00% 0.00% 0.00% 0.00% 0.00%

Business realignment costs 0.00% 0.00% -0.46% 0.00% -0.01% 0.00% 0.00% 0.00% 0.00%Other -14.51% -14.44% -14.41% -15.16% -15.04% -14.70% -14.70% -14.70% -14.70%

Total operating income / loss 7.57% 6.53% 6.41% 3.49% 1.56% 5.68% 5.67% 5.60% 5.52%

Total other expense / income 0.02% -0.79% -5.47% -1.08% 0.28% -0.61% -0.64% -0.67% -0.69%

Interest, net -0.79% -0.78% -0.76% -0.89% -0.63% -0.61% -0.64% -0.67% -0.69%

Interest expense -0.85% -0.85% -0.84% -0.97% -0.71% -0.70% -0.71% -0.72% -0.73%

Interest income 0.05% 0.07% 0.08% 0.08% 0.08% 0.10% 0.07% 0.05% 0.04%

Other retirement plans income 0.78% 0.91% -4.66% -0.18% 0.92% 0.00% 0.00% 0.00% 0.00%

Other, net 0.03% -0.01% -0.04% -0.01% 0.00% 0.00% 0.00% 0.00% 0.00%

Income before income taxes 7.59% 6.65% 0.94% 2.41% 1.85% 5.07% 5.04% 4.93% 4.83%Provision for income taxes -2.62% 0.33% -0.17% -0.55% -0.43% -1.17% -1.16% -1.13% -1.11%

Net income / loss 4.97% 6.99% 0.77% 1.86% 1.42% 3.91% 3.88% 3.80% 3.72%

FedEx CorporationBalance Sheetin $millionsFiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

AssetsCurrent AssetsCash & Short-Term Investments 3,969 3,265 2,319 4,881 6,233 4,955 3,786 3,300 2,418

Accounts Receivables, Net 7,599 8,481 9,116 10,558 11,968 11,605 12,232 12,909 13,552

Accounts Receivables, Gross 7,851 8,882 9,416 10,948 12,771 12,035 12,685 13,387 14,054

Bad Debt/Doubtful Accounts -252 -401 -300 -390 -803 -430 -453 -478 -502

Spare parts, supplies and fuel, Net 514 525 553 572 577 705 743 784 823

Spare parts, supplies and fuel, Gross 751 793 888 907 926 1,118 1,178 1,243 1,305

Inventory Valuation Allowance -237 -268 -335 -335 -349 -413 -435 -459 -482Prepaid expenses and other 546 1,070 1,098 372 853 860 906 956 1,004

Total Current Assets 12,628 13,341 13,086 16,383 19,631 18,125 17,667 17,949 17,797

Long-Term AssetsNet Property, Plant & Equipment 25,981 28,154 30,429 33,608 35,277 37,684 40,221 42,899 45,710

Property, Plant & Equipment - Gross 51,355 55,121 59,511 65,024 69,590 75,092 80,891 87,011 93,435

Aircraft and related equipment 18,833 20,749 22,793 24,518 26,691 29,012 31,458 34,040 36,750

Package handling and ground support equipment 8,989 9,727 10,409 11,382 12,227 13,130 14,081 15,085 16,139

Computer and Electronic Equipment 5,396 5,794 6,268 6,884 7,407 7,966 8,555 9,176 9,829

Vehicles and Trailers 6,961 7,708 8,339 9,101 9,906 10,765 11,671 12,628 13,631

Facilities and other 10,447 11,143 11,702 13,139 13,360 14,220 15,126 16,082 17,086

Accumulated Depreciation -24,645 -26,967 -29,082 -31,416 -34,313 -37,408 -40,669 -44,112 -47,726

Total Other Long-term Assets 10,198 10,835 10,888 23,546 26,898 29,500 30,706 32,010 33,249

Operating Lease Right-of-Use Assets 0 0 0 13,917 15,198 18,052 19,027 20,080 21,081

Goodwill 7,154 6,973 6,884 6,372 7,149 7,149 7,149 7,149 7,149Other Assets 3,044 3,862 4,004 3,257 4,551 4,298 4,530 4,781 5,019

Total Assets 48,807 52,330 54,403 73,537 81,806 85,309 88,595 92,858 96,756

Liabilities & Shareholders' EquityCurrent LiabilitiesST Debt & Curr. Portion LT Debt 22 1,342 964 51 656 538 574 615 658

Accounts Payable 2,752 2,977 3,030 3,269 4,316 3,868 4,077 4,303 4,517

Other Current Liabilities 5,144 5,308 5,019 7,024 9,512 9,026 9,513 10,040 10,540

Accrued salaries and employee benefits 1,914 2,177 1,741 1,569 2,604 2,321 2,446 2,582 2,710

Acrued expenses 3,230 3,131 3,278 3,532 4,720 4,298 4,530 4,781 5,019

Operating Lease Liabilities 0 0 0 1,923 2,188 2,407 2,537 2,677 2,811

Total Current Liabilities 7,918 9,627 9,013 10,344 14,484 13,433 14,164 14,958 15,715

Long-Term LiabilitiesLong-term debt, less current portion 14,909 15,243 16,617 21,952 23,074 24,470 26,073 27,959 29,895

Other Long-Term Liabilities 9,652 8,044 11,016 22,946 24,857 27,479 28,917 30,472 31,949

Deferred Lease Obligations 531 551 531 0 0 0 0 0 0

Operating Lease Liabilities 0 0 0 12,195 12,904 14,614 15,403 16,255 17,065

Deferred Income Taxes 2,485 2,867 2,821 3,162 3,759 3,439 3,624 3,825 4,015

Pension, postretirement healthcare, and other benefit obligations 4,487 2,187 5,095 5,019 4,966 6,017 6,342 6,693 7,027

Self-insurance accruals 1,494 1,784 1,899 2,104 2,398 2,579 2,718 2,869 3,012Other Liabilities 655 655 670 466 830 830 830 830 830

Total Liabilities 32,479 32,914 36,646 55,242 62,415 65,382 69,155 73,389 77,560

EquityCommon Stock 32 32 32 32 32 32 32 32 32

Additional paid-in capital 3,005 3,117 3,231 3,356 3,480 3,602 3,728 3,858 3,993

Retained Earnings 20,833 24,823 24,648 25,216 25,677 28,268 30,951 33,744 36,583

Accumulated Other Comprehensive Loss / Income -415 -578 -865 -1,147 -636 -712 -798 -894 -1,001

Treasury Stock -7,382 -7,978 -9,289 -9,162 -9,162 -11,262 -14,472 -17,272 -20,412Total common stockholders' investment 16,073 19,416 17,757 18,295 19,391 19,927 19,441 19,469 19,196

Total Liabilities & Shareholders' Equity 48,807 52,330 54,403 73,537 81,806 85,309 88,595 92,858 96,756

FedEx CorporationBalance Sheetin $millionsFiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

AssetsCurrent AssetsCash & Short-Term Investments 8.13% 6.24% 4.26% 6.64% 7.62% 5.81% 4.27% 3.55% 2.50%

Accounts Receivables, Net 15.57% 16.21% 16.76% 14.36% 14.63% 13.60% 13.81% 13.90% 14.01%

Accounts Receivables, Gross 16.09% 16.97% 17.31% 14.89% 15.61% 14.11% 14.32% 14.42% 14.53%

Bad Debt/Doubtful Accounts -0.52% -0.77% -0.55% -0.53% -0.98% -0.50% -0.51% -0.51% -0.52%

Spare parts, supplies and fuel, Net 1.05% 1.00% 1.02% 0.78% 0.71% 0.83% 0.84% 0.84% 0.85%

Spare parts, supplies and fuel, Gross 1.54% 1.52% 1.63% 1.23% 1.13% 1.31% 1.33% 1.34% 1.35%

Bad Debt/Doubtful Accounts -0.49% -0.51% -0.62% -0.46% -0.43% -0.48% -0.49% -0.49% -0.50%Prepaid expenses and other 1.12% 2.04% 2.02% 0.51% 1.04% 1.01% 1.02% 1.03% 1.04%

Total Current Assets 25.87% 25.49% 24.05% 22.28% 24.00% 21.25% 19.94% 19.33% 18.39%

Long-Term AssetsNet Property, Plant & Equipment 53.23% 53.80% 55.93% 45.70% 43.12% 44.17% 45.40% 46.20% 47.24%

Property, Plant & Equipment - Gross 105.22% 105.33% 109.39% 88.42% 85.07% 88.02% 91.30% 93.70% 96.57%

Aircraft and related equipment 38.59% 39.65% 41.90% 33.34% 32.63% 34.01% 35.51% 36.66% 37.98%

Package handling and ground support equipment 18.42% 18.59% 19.13% 15.48% 14.95% 15.39% 15.89% 16.25% 16.68%

Computer and Electronic Equipment 11.06% 11.07% 11.52% 9.36% 9.05% 9.34% 9.66% 9.88% 10.16%

Vehicles and Trailers 14.26% 14.73% 15.33% 12.38% 12.11% 12.62% 13.17% 13.60% 14.09%

Facilities and other 21.40% 21.29% 21.51% 17.87% 16.33% 16.67% 17.07% 17.32% 17.66%

Accumulated Depreciation -50.49% -51.53% -53.46% -42.72% -41.94% -43.85% -45.91% -47.50% -49.33%

Total Other Long-term Assets 20.89% 20.71% 20.01% 32.02% 32.88% 34.58% 34.66% 34.47% 34.36%

Operating Lease Right-of-Use Assets 0.00% 0.00% 0.00% 18.93% 18.58% 21.16% 21.48% 21.62% 21.79%

Goodwill 14.66% 13.33% 12.65% 8.67% 8.74% 8.38% 8.07% 7.70% 7.39%Other Assets 6.24% 7.38% 7.36% 4.43% 5.56% 5.04% 5.11% 5.15% 5.19%

Total Assets 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Liabilities & Shareholders' EquityCurrent LiabilitiesST Debt & Curr. Portion LT Debt 0.05% 2.56% 1.77% 0.07% 0.80% 0.63% 0.65% 0.66% 0.68%

Accounts Payable 5.64% 5.69% 5.57% 4.45% 5.28% 4.53% 4.60% 4.63% 4.67%

Other Current Liabilities 10.54% 10.14% 9.23% 9.55% 11.63% 10.58% 10.74% 10.81% 10.89%

Accrued salaries and employee benefits 3.92% 4.16% 3.20% 2.13% 3.18% 2.72% 2.76% 2.78% 2.80%

Acrued expenses 6.62% 5.98% 6.03% 4.80% 5.77% 5.04% 5.11% 5.15% 5.19%Operating Lease Liabilities 0.00% 0.00% 0.00% 2.62% 2.67% 2.82% 2.86% 2.88% 2.91%

Total Current Liabilities 16.22% 18.40% 16.57% 14.07% 17.71% 15.75% 15.99% 16.11% 16.24%

Long-Term LiabilitiesLong-term debt, less current portion 30.55% 29.13% 30.54% 29.85% 28.21% 28.68% 29.43% 30.11% 30.90%

Other Long-Term Liabilities 19.78% 15.37% 20.25% 31.20% 30.39% 32.21% 32.64% 32.82% 33.02%

Deferred Lease Obligations 1.09% 1.05% 0.98% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Operating Lease Obligations 0.00% 0.00% 0.00% 16.58% 15.77% 17.13% 17.39% 17.51% 17.64%

Deferred Income Taxes 5.09% 5.48% 5.19% 4.30% 4.60% 4.03% 4.09% 4.12% 4.15%

Pension, postretirement healthcare, and other benefit obligations 9.19% 4.18% 9.37% 6.83% 6.07% 7.05% 7.16% 7.21% 7.26%

Self-insurance accruals 3.06% 3.41% 3.49% 2.86% 2.93% 3.02% 3.07% 3.09% 3.11%Other Liabilities 1.34% 1.25% 1.23% 0.63% 1.01% 0.97% 0.94% 0.89% 0.86%

Total Liabilities 66.55% 62.90% 67.36% 75.12% 76.30% 76.64% 78.06% 79.03% 80.16%

EquityCommon Stock 0.07% 0.06% 0.06% 0.04% 0.04% 0.04% 0.04% 0.03% 0.03%

Additional paid-in capital 6.16% 5.96% 5.94% 4.56% 4.25% 4.22% 4.21% 4.16% 4.13%

Retained Earnings 42.68% 47.44% 45.31% 34.29% 31.39% 33.14% 34.94% 36.34% 37.81%

Accumulated Other Comprehensive Loss / Income -0.85% -1.10% -1.59% -1.56% -0.78% -0.83% -0.90% -0.96% -1.03%

Treasury Stock -15.12% -15.25% -17.07% -12.46% -11.20% -13.20% -16.34% -18.60% -21.10%Total Common Stockholders' Investment 32.93% 37.10% 32.64% 24.88% 23.70% 23.36% 21.94% 20.97% 19.84%

Total Liabilities & Shareholders' Equity 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

FedEx CorporationHistorical Cash Flow Statementin $millionsFiscal Years Ending May.31 2017 2018 2019 2020Operating ActivitiesNet income 2,997 4,572 540 1,286

Adjustments to reconcile net income to cash provided by operating activities 1,933 102 5,073 3,811

Depreciation and amortization 2,995 3,095 3,353 3,615

Other, net 1,199 477 228 3,494

Provision for uncollectible accounts 136 246 295 442

Deferred income taxes and other noncash items 909 -231 -233 2,449

Stock-based compensation 154 167 174 168

Gain from sale of business 0 -85 -8 0

Impairment charges 0 380 0 435

Retirement plans mark-to-market adjustment -24 -10 3,882 794

Gain from sale of an investment -35 0 0 0

Business realignment costs 0 0 101 0

Changes in operating assets and liabilities, net -2,202 -3,460 -2,491 -4,092

Receivables -556 -1,049 -873 -1,331

Other assets 78 -135 -25 -59

Pension and postretirement healthcare assets and liabilities, net -1,688 -2,345 -909 -908

Accounts payable and other liabilities 103 141 -571 -1,787Other, net -139 -72 -113 -7

Net Operating Cash Flow 4,930 4,674 5,613 5,097

Investing ActivitiesCapital expenditures -5,116 -5,663 -5,490 -5,868

Proceeds from asset dispositions and other 135 -14 17 22

Business acquisitions, net of cash acquired 0 -179 -66 0

Proceeds from sale of business 0 123 0 0Proceeds from asset dispositions and other excluding business acquisitions, net of cash acquired and proceeds from sale of 135 42 83 22

Net Investing Cash Flow -4,981 -5,677 -5,473 -5,846

Financing ActivitiesProceeds from short-term borrowings, net 0 0 0 0

Principal payments on debt -82 -38 -1,436 -2,548

Proceeds from debt issuances 1,190 1,480 2,463 6,556

Proceeds from stock issuances 337 327 101 64

Dividend Paid -426 -535 -683 -679

Purchase of Treasury Stock -509 -1,017 -1,480 -3Other, net 18 10 -4 -9

Net Financing Cash Flow 528 227 -1,039 3,381

Effect of exchange rate changes on cash -42 72 -47 -70Net increase / decrease in cash and cash equivalents 435 -704 -946 2,562

Beginning Cash Balance 3,534 3,969 3,265 2,319Ending Cash Balance 3,969 3,265 2,319 4,881

FedEx CorporationForecasted Cash Flow Statement

Fiscal Years Ending May.31 2021E 2022E 2023E 2024E 2025CV

Operating ActivitiesNet income 1,146 3,359 3,515 3,631 3,733

Adjustments to reconcile net income to cash provided by operating activitiesDepreciation and amortization 3789 4401 4734 5068 5401

Allowance for doubtful accounts 803 430 453 478 502

Stock-based compensation 216 221 233 246 258

Changes in operating assets and liabilities, netReceivables -413 373 -23 -25 -24

Spare parts, supplies and fuel -14 -64 -22 -24 -23

Prepaid expenses and other -481 -7 -46 -50 -48

Operating Lease Right-of-Use Assets -1281 -2854 -974 -1053 -1001

Accounts payable 1047 -448 209 226 214

Accrued salaries and employee benefits 1035 -283 125 135 129

Acrued expenses 1188 -422 232 251 238

Operating Lease Liabilities 974 1929 919 993 943

Pension and postretirement healthcare assets and liabilities, net -53 1051 325 351 334

Deferred Income Taxes 597 -320 186 201 191

Self-insurance accruals 294 181 139 150 143

Other Long-term Liabilities 364 0 0 0 0

Net Operating Cash Flow 8553 7366 9864 10427 10847

Investing ActivitiesCapital expenditures -4566 -5502 -5799 -6120 -6425

Change in Short-term Investments -1663 -48 -594 -1615 -751

Business Acquisitions (Change in Goodwill) -777 0 0 0 0

Change in Other Long-term Assets -1294 253 -232 -251 -238

Net Investing Cash Flow -8300 -5297 -6625 -7986 -7414

Financing ActivitiesProceeds from issuance of long-term debt 1,727 1,278 1,638 1,927 1,979

Principal payments on debt 0 -1,853 -2,105 -1,324 -2,315

Payment of Finance Lease -67 -26 -25 -24 -81

Proceeds from issuance of Common Stock 124 122 126 130 135

Dividend Paid -685 -768 -832 -838 -893Repurchase of Treasury Stock 0 -2,100 -3,210 -2,800 -3,140

Net Financing Cash Flow 1,099 -3,347 -4,408 -2,928 -4,316

Beginning Cash Balance 4,881 6,233 4,955 3,786 3,300Ending Balance of Cash 6,233 4,955 3,786 3,300 2,418

Net increase / decrease in cash and cash equivalents 1,352 -1,277 -1,169 -486 -882

FedEx CorporationValue Driver Estimation

Fiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

NOPLAT:Net Sales 60,319 65,450 69,693 69,217 80,472 85,964 90,604 95,620 100,385

Less: Operating Expense -55,753 -61,178 -65,227 -66,800 -79,213 -81,081 -85,463 -90,265 -94,844

Salaries and employee benefits -21,989 -23,795 -24,776 -25,031 -30,894 -31,549 -33,252 -35,093 -36,841

Purchased transportation -13,630 -15,101 -16,654 -17,466 -22,046 -20,545 -21,564 -22,758 -23,892

Rentals and landing fees -3,240 -3,361 -3,360 -3,712 -4,302 -4,212 -4,440 -4,685 -4,919

Depreciation and amortization -2,995 -3,095 -3,353 -3,615 -3,789 -4,401 -4,734 -5,068 -5,401

Fuel -2,773 -3,374 -3,889 -3,156 -2,798 -3,954 -4,168 -4,399 -4,618

Maintenance and repairs -2,374 -2,622 -2,834 -2,893 -3,273 -3,782 -3,987 -4,207 -4,417

Asset impairment charges 0 -380 0 -435 0 0 0 0 0

Business realignment costs 0 0 -320 0 -10 0 0 0 0

Add: Implied Interest on Operating Leases 380.40 382.22 386.70 387.21 366.58 435.42 458.93 484.34 508.47EBITA 4,946 4,654 4,853 2,804 1,626 5,319 5,601 5,839 6,050

Adjusted TaxesMarginal Tax Rate 36.75% 27.89% 34.05% 25.82% 25.82% 25.82% 25.82% 25.82% 25.82%Income Tax Provision 1582.00 -219.00 115.00 383.00 342.25 1003.33 1049.80 1084.64 1114.98

Tax Shield on Interest Expense (+) 188.18 155.62 200.19 173.54 147.79 155.75 165.95 177.95 190.28

Tax on Interest on Operating Leases (-) -139.81 -106.60 -131.65 -99.99 -94.65 -112.43 -118.50 -125.06 -131.29

Tax on interest income (-) -12.13 -13.39 -20.09 -14.20 -16.64 -21.24 -16.89 -12.91 -11.25

Tax shield on Other retirement plans income (+) -173.11 -166.78 1106.83 31.51 -190.29 0.00 0.00 0.00 0.00

Tax shield on other non-operating income (+) -7.72 1.95 10.55 2.32 0.00 0.00 0.00 0.00 0.00

Total adjusted taxes (subtract from EBITDA) 1437.41 -348.19 1280.83 476.17 188.46 1025.40 1080.36 1124.64 1162.72

Change in Deferred Taxes (plus, cash basis vs GAAP) 918 382 -46 341 597 -320 186 201 191

NOPLAT 4,427 5,384 3,526 2,669 2,034 3,973 4,706 4,915 5,077

Invested Capital (IC):Operating Current Assets

Normal Cash (3.33% of sales) (+) 2,007 2,178 2,319 2,303 2,678 2,860 3,015 3,182 3,340

Account Receivables (+) 7,599 8,481 9,116 10,558 11,968 11,605 12,232 12,909 13,552

Spare parts, supplies and fuel (+) 514 525 553 572 577 705 743 784 823

Prepaid expenses and other (+) 546 1,070 1,098 372 853 860 906 956 1,004

Non Interest-Bearning Current Liabilities Accounts Payable 2,752 2,977 3,030 3,269 4,316 3,868 4,077 4,303 4,517

Other Current Liabilities 5,144 5,308 5,019 7,024 9,512 9,026 9,513 10,040 10,540

Net Operating Working Capital 2,770 3,969 5,037 3,512 2,248 3,135 3,305 3,488 3,661

Net Property, Plant, and Equipment (+) 51,355 55,121 59,511 65,024 69,590 75,092 80,891 87,011 93,435

Net Other Operating Assets (+) 15,847 16,032 16,053 15,519 15,198 18,052 19,027 20,080 21,081

Net Other Operating Liabilities (-) 9,652 8,044 11,016 22,946 24,857 27,479 28,917 30,472 31,949

Invested Capital 60,320 67,078 69,585 61,109 62,179 68,801 74,305 80,106 86,228

Free Cash Flow (FCF):NOPLAT 4,427 5,384 3,526 2,669 2,034 3,973 4,706 4,915 5,077Change in IC 6,022 6,758 2,507 -8,477 1,070 6,622 5,504 5,801 6,122

FCF -1,595 -1,374 1,018 11,146 964 -2,649 -798 -886 -1,045

Return on Invested Capital (ROIC):NOPLAT 4,427 5,384 3,526 2,669 2,034 3,973 4,706 4,915 5,077Beginning IC 54,297 60,320 67,078 69,585 61,109 62,179 68,801 74,305 80,106

ROIC 8.15% 8.93% 5.26% 3.84% 3.33% 6.39% 6.84% 6.62% 6.34%

Economic Profit (EP):Beginning IC * (ROIC-WACC)

Economic Profit (Total) 1,918 2,598 427 -546 -789 1,100 1,527 1,483 1,377

FedEx CorporationDiscounted Cash Flow (DCF) and Economic Profit (EP) Valuation Models

Key Inputs: CV Growth of NOPLAT 3.10% CV Year ROIC 6.34% WACC 4.62% Cost of Equity 6.07%

Fiscal Years Ending May.31 2021E 2022E 2023E 2024E 2025CV

DCF Model:Free Cash Flow (FCF) 963.8 -2649.3 -798.1 -885.6 -1044.5Continuing Value (CV) 170709.2PV of FCF 921.2 -2420.5 -696.9 -739.3 142494.5

Value of Operating Assets: 139559.0Non-Operating Adjustments(+)Excess Cash 2577.8- ESOP -2185.7(-) MV of Total Debt -37521.7(-) Underfunded Pension -5064.0

Value of Equity 97365.5Shares Outstanding 261.0

Intrinsic Value of Last FYE 373.05$ Implied Price as of Today 388.70$

EP Model:Economic Profit (EP) -789.1 1100.1 1527.2 1482.5 1376.5Continuing Value (CV) 90602.9PV of EP -754.3 1005.1 1333.7 1237.5 75628.1

Total PV of EP 78450.1Invested Capital (last FYE) 61108.8Value of Operating Assets: 139559.0

Non-Operating Adjustments(+)Excess Cash 2577.8- ESOP -2185.7(-) MV of Total Debt -37521.7(-) Underfunded Pension -5064.0

Value of Equity 97365.5Shares Outstanding 261.0

Intrinsic Value of Last FYE 373.05$ Implied Price as of Today 388.70$

FedEx CorporationDividend Discount Model (DDM) or Fundamental P/E Valuation Model

Fiscal Years Ending 2021E 2022E 2023E 2024E 2025CV

EPS 4.35$ 13.15$ 14.09$ 14.95$ 15.36$

Key Assumptions CV growth of EPS 2.80% CV Year ROE 19.45% Cost of Equity 6.07%

Future Cash Flows P/E Multiple (CV Year) 26.21 EPS (CV Year) 15.36$ Future Stock Price 402.65$ Dividends Per Share 2.62 2.87 3.16 3.28 Discounted Cash Flows 2.47 2.55 2.65 2.59 318.14$

Intrinsic Value as of Last FYE 328.40$ Implied Price as of Today 342.18$

FedEx CorporationRelative Valuation Models Prices as of 3/26/21

EPS EPS Est. 5yrTicker Company Price 2021E 2022E P/E 21 P/E 22 EPS gr. PEG 21 PEG 22UPS United Parcel Service (UPS) $167.98 $8.88 $9.63 19.60 18.30 10.06 1.95 1.82 EXPD Expeditors International of Washington, Inc. $107.80 $4.26 $4.39 25.60 25.10 4.20 6.10 5.98 JBHT J.B. Hunt Transport Services, Inc. $166.90 $6.19 $7.63 27.70 23.30 20.73 1.34 1.12 XPO XPO Logisitics, Inc. $123.21 $5.07 $5.92 24.90 21.50 10.14 2.46 2.12 CHRW C.H. Robinson Worldwide, Inc. $97.70 $4.43 $4.69 22.50 20.90 9.94 2.26 2.10

Average 24.06 21.82 2.82 2.63

FDX FedEx Corporation $281.34 $4.35 $13.15 16.1 14.5 10.5 1.5 1.4

Implied Relative Value: P/E (EPS20) $ 104.75

P/E (EPS21) 286.91$ PEG (EPS20) 129.28$ PEG (EPS21) 363.93$

FedEx CorporationWeighted Average Cost of Capital (WACC) Estimation

Cost of Equity: ASSUMPTIONS:Risk-Free Rate 1.67% 10-year Treasury Note used Beta 1.032 2 year weekly raw beta from BloombergEquity Risk Premium 4.26% Damodaran implied COVID-19-adjusted ERP as of 1-Apr-2021Cost of Equity 6.07%

Cost of Debt:Risk-Free Rate 1.67% 10-year Treasury Note used Implied Default Premium 0.74%Pre-Tax Cost of Debt 2.41% YTM on company's 9-year corporate bondMarginal Tax Rate 25.82%After-Tax Cost of Debt 1.79%

Market Value of Common Equity: MV Weights

Total Shares Outstanding 261Current Stock Price $281.34MV of Equity 73,429.74 66.18%

Market Value of Debt:Short-Term Debt 0Current Portion of LTD 51Long-Term Debt 21,952PV of Operating Leases 15,519 MV of Total Debt 37,521.67 33.82%

Market Value of the Firm 110,951.41 100.00%

Estimated WACC 4.62%

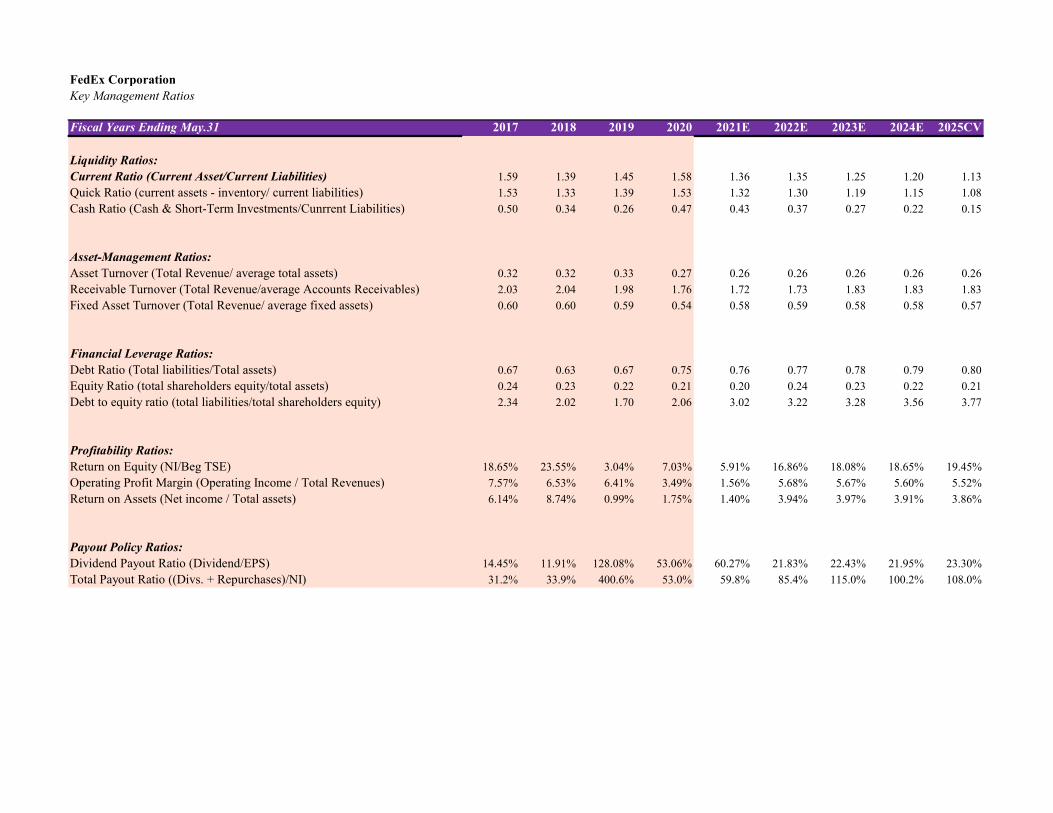

FedEx CorporationKey Management Ratios

Fiscal Years Ending May.31 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025CV

Liquidity Ratios:Current Ratio (Current Asset/Current Liabilities) 1.59 1.39 1.45 1.58 1.36 1.35 1.25 1.20 1.13

Quick Ratio (current assets - inventory/ current liabilities) 1.53 1.33 1.39 1.53 1.32 1.30 1.19 1.15 1.08

Cash Ratio (Cash & Short-Term Investments/Cunrrent Liabilities) 0.50 0.34 0.26 0.47 0.43 0.37 0.27 0.22 0.15

Asset-Management Ratios:Asset Turnover (Total Revenue/ average total assets) 0.32 0.32 0.33 0.27 0.26 0.26 0.26 0.26 0.26

Receivable Turnover (Total Revenue/average Accounts Receivables) 2.03 2.04 1.98 1.76 1.72 1.73 1.83 1.83 1.83

Fixed Asset Turnover (Total Revenue/ average fixed assets) 0.60 0.60 0.59 0.54 0.58 0.59 0.58 0.58 0.57

Financial Leverage Ratios:Debt Ratio (Total liabilities/Total assets) 0.67 0.63 0.67 0.75 0.76 0.77 0.78 0.79 0.80

Equity Ratio (total shareholders equity/total assets) 0.24 0.23 0.22 0.21 0.20 0.24 0.23 0.22 0.21

Debt to equity ratio (total liabilities/total shareholders equity) 2.34 2.02 1.70 2.06 3.02 3.22 3.28 3.56 3.77

Profitability Ratios:Return on Equity (NI/Beg TSE) 18.65% 23.55% 3.04% 7.03% 5.91% 16.86% 18.08% 18.65% 19.45%

Operating Profit Margin (Operating Income / Total Revenues) 7.57% 6.53% 6.41% 3.49% 1.56% 5.68% 5.67% 5.60% 5.52%

Return on Assets (Net income / Total assets) 6.14% 8.74% 0.99% 1.75% 1.40% 3.94% 3.97% 3.91% 3.86%

Payout Policy Ratios:Dividend Payout Ratio (Dividend/EPS) 14.45% 11.91% 128.08% 53.06% 60.27% 21.83% 22.43% 21.95% 23.30%

Total Payout Ratio ((Divs. + Repurchases)/NI) 31.2% 33.9% 400.6% 53.0% 59.8% 85.4% 115.0% 100.2% 108.0%

FedEx CorporationPresent Value of Operating Lease Obligations

Fiscal Years Ending May.31 2017 2018 2019 2020Year 1 2,445 2,471 2,497 2,416Year 2 2,230 2,177 2,263 2,266Year 3 1,931 1,951 2,028 2,012Year 4 1,709 1,762 1,779 1,689Year 5 1,540 1,548 1,486 1,515Thereafter 8,019 8,193 8,062 7,552Total Minimum Payments 17874.0 18102.0 18115.0 17450.0Less: Cumulative Interest 2027.4 2069.8 2061.5 1931.3PV of Minimum Payments 15846.6 16032.2 16053.5 15518.7

Implied Interest in Year 1 Payment 380.4 382.2 386.7 387.2

Pre-Tax Cost of Debt 2.41% 2.41% 2.41% 2.41%Years Implied by Year 6 Payment 5.2 5.3 5.4 5.0Expected Obligation in Year 6 & Beyond 1540 1548 1486 1515

Present Value of Lease PaymentsPV of Year 1 2387.4 2412.8 2438.2 2359.1PV of Year 2 2126.2 2075.7 2157.7 2160.5PV of Year 3 1797.8 1816.4 1888.1 1873.2PV of Year 4 1553.6 1601.8 1617.2 1535.4PV of Year 5 1367.0 1374.1 1319.1 1344.8PV of 6 & beyond 6614.7 6751.5 6633.3 6245.7Capitalized PV of Payments 15846.6 16032.2 16053.5 15518.7

FedEx CorporationEffects of ESOP Exercise and Share Repurchases on Common Stock Account and Number of Shares Outstanding

Number of Options Outstanding (shares): 16,124,745

Average Time to Maturity (years): 6.20

Expected Annual Number of Options Exercised: 2,600,765

Current Average Strike Price: 167.79$

Cost of Equity: 6.07%

Current Stock Price: $281.34

Fiscal Years Ending May.31 2021E 2022E 2023E 2024E 2025CV

Increase in Shares Outstanding: 2,600,765 2,600,765 2,600,765 2,600,765 2,600,765

Average Strike Price: 167.79$ 167.79$ 167.79$ 167.79$ 167.79$

Increase in Common Stock Account: 436,382,413 436,382,413 436,382,413 436,382,413 436,382,413

Share Repurchases ($) 0 2,100,000,000 3,210,000,000 2,800,000,000 3,140,000,000

Expected Price of Repurchased Shares: 281.34$ 295.82$ 311.04$ 327.05$ 343.88$

Number of Shares Repurchased: 0.00 7,098,943.74 10,320,135.38 8,561,390.68 9,131,073.84

Shares Outstanding (beginning of the year) 265,070,592 267,671,357 263,173,179 255,453,809 249,493,183

Plus: Shares Issued Through ESOP 2,600,765 2,600,765 2,600,765 2,600,765 2,600,765

Less: Shares Repurchased in Treasury - 7,098,944 10,320,135 8,561,391 9,131,074

Shares Outstanding (end of the year) 267,671,357 263,173,179 255,453,809 249,493,183 242,962,875

FedEx CorporationValuation of Options Granted under ESOP

Current Stock Price $281.34Risk Free Rate 1.67%Current Dividend Yield 0.92%Annualized St. Dev. of Stock Returns 31.67%

Average Average B-S ValueRange of Number Exercise Remaining Option of OptionsOutstanding Options of Shares Price Life (yrs) Price GrantedRange 1 16,124,745 167.79 6.20 135.55$ 2,185,689,830$ Total 16,124,745 167.79$ 6.20 149.06$ 2,185,689,830$