Embed Size (px)

Citation preview

N,

UNITED STATES DISTRICT COURT FOR THE MIDDLE DISTRICT OF NORTH CA

_•\!%

EASTSIDE INVESTORS, Individually and On Behalf Of All Others Similarly Situated,

Plaintiff,

vs.

KPJSPY KREME DOUGHNUTS, INC., RANDY S. CASSTEVENS, SCOTT A. LIVEN000D, MICHAEL C. PHALEN, and JOHN W. TATE,

Defendants.

X Civil Action No.

CLASS ACTION COMPLAINT FOR VIOLATION OF THE SECURITIES EXCHANGE ACT OF 1934

1:04CV00416 X

Plaintiff has alleged the following based upon the investigation of plaintiff's counsel,

which included a review of United States Securities and Exchange Commission ("SEC") filings

by Krispy Kreme Doughnuts, Inc. ("Krispy Kreme" or the "Company"), as well as regulatory

filings and reports, securities analysts reports and advisories about the Company, press releases,

and media reports about the Company, and plaintiff believes that substantial additional

evidentiary support will exist for the allegations set forth herein after a reasonable opportunity

for discovery.

INTRODUCTION

1. This is a securities class action on behalf of all purchasers of the publicly

traded securities of Krispy Kreme between August 21, 2003 and May 7, 2004 inclusive (the

"Class Period") against Krispy Kreme and certain of its officers and directors for violations of

the Securities Exchange Act of 1934 (the "1934 Act ").

2. Krispy Kreme is a specialty retailer of doughnuts. The Company's

principal business is owning and franchising Krispy K.rerne doughnut stores, where it makes

more than 20 varieties of doughnuts. Under the terms of the franchise agreements, the licensed

operators paid royalties and fees in exchange for the use of the Krispy Kreme name. Each of

Krispy Kreme's franchises also is a doughnut factory with the capacity to produce from 4,000

dozen to over 10,000 dozen doughnuts daily for retail sale to store customers and for wholesale

to supermarkets and other outlets. The Company also accomplishes off-premises sales through

its direct store delivery system.

3. After its initial public offering in April 2000, the Company grew rapidly

and, throughout the Class Period, defendants touted the Company's growth and the expansion of

Krispy Kreme stores into new markets. An article published in The New York Times on May 8,

2004, the day after the Class Period, described Krispy Kreme's rapid ascent, and characterized

its apparently phenomenal performance as follows:

Until recently, the company appeared to be unstoppable. When the shares were first sold to the public in April 2000, during the boom in high-technology public offerings, Krispy I(reme was hailed as an old-economy growth story. The shares rose 76 percent on the first day of trading and did not look back.

Even as the high-technology issues lost most of their value, Krispy Kreme surged ahead, [Emphasis added.]

4. Unbeknownst to investors, the Company's class-period statements and

reported financial results were materially false and misleading because they failed to disclose

that:

a. as a result of the trend toward low-fat, low carbohydrate diets, such

as the South Beach and Atkins diets, Krispy Kreme had been suffering from increasingly poor

sales performance;

2

b. defendants knew or recklessly disregarded that the trend toward

low-fat, low-carbohydrate diets was not the sole reason for the Company's worsening financial

condition;

C. While the opening of new Krispy Kreme stores created initial

consumer excitement and a corresponding surge in sales, sales at those newly-opened stores

quickly tapered off. This was especially damaging to the Company in smaller markets with a

limited number of potential new customers. Rather than cultivate a steady customer based, the

Company instead attempted to capitalize on Krispy Kreme's "fad appeal" and adopted a business

model and strategy for increasing sales that was predicated on the perpetual addition of new

stores and the hyping of the Company's entry into new markets ---- a tactic that resulted in

unsustainable surges in sales that fell off once the hype ceased and the novelty of the new store

wore off. For example, according a Herb Greenberg column published by CBS

Marketwatch.com, Krispy Kreme opened a franchise in Newington, Connecticut in 2002. In

October 2002, the franchise recorded sales of $792,745. Within two months they were $540,229

and by February 2004 they had fallen to $152,704 per month;

d. the Company's strategy of offsetting slowing retail sales with

wholesale shipments to supermarkets was not working because:

i) the Company's wholesale business was more expensive to

operate and, therefore, resulted in a lower profit margin than in-store sales and

ii) the Company's wholesale business was saturating the

market with Krispy Kreme products, cannibalizing the company's retail operations, perhaps

undermining them as well, and decreasing the Company's overall profit margin; and

C. During the Class Period, the Company repurchased several

franchises, which might have been a sign of trouble but for the fact of the Company's materially

false and misleading statements that the repurchases were all part of its "acquisition strategy." In

fact, the Company was repurchasing franchises to prevent franchisees from closing the stores,

because this would damage Krispy Kreme's reputation for ever-increasing growth and as part of

a scheme to wipe franchisee accounts receivable off its books.

5. The truth was revealed early on the morning on May 7, 2004, before the

markets opened. On that date, defendants issued a news release over PRNewrwire in which they

announced that Krispy Kreine's expected fiscal 2005 diluted earnings per share from continuing

operations, excluding charges, to be 10% lower than previously announced, and that Krispy

Kreme was closing certain company-owned stores and reducing plans to open new ones, Krispy

Kreme also announced that it was closing its Montana Mills bread stores, an operation that it had

bought a year ago, and that it was going to write-off as much as $40 million on the venture; as

recently as mid-April, defendants had said they intended to refine and expand the operation.

6. On this news, shares of Krispy Kreme fell $9.29, or 29%, to close at

$22.5 1, a new 52-week low and more than 50% below Krispy Kreme's 52-week high of $49.74.

The trading volume was 20,5 million shares, the largest ever for Krispy Kreme and amounting to

a third of the shares outstanding.

7. During the Class Period, Krispy Kreme insiders sold in excess of 1.5

million shares for guaranteed proceeds of $50.1 million.

JURISDICTION AND VENUE

8, Jurisdiction is conferred by Section 27 of the Exchange Act. The claims

asserted herein arise under §10(b) and 20(a) of the 1934 Act and Rule lOb-5.

4

9, Venue is proper in this District pursuant to §27 of the 1934 Act. Many of

the false and misleading statements were made in or issued from this District.

THE PARTIES

10. Plaintiff Eastside Investors purchased publicly-traded Krispy Kreme

securities during the Class Period as described in the attached certification, incorporated herein

by reference, and was damaged thereby.

ii Defendant Krispy K.reme a specialty retailer of doughnuts. The Company's

principal business is owning and franchising Krispy Kreme doughnut stores, where it makes and

sells more than 20 varieties of doughnuts. It currently operates 374 factory stores in 44 U.S.

states, Australia, Canada and Mexico. Krispy Krernc is incorporated in North Carolina and its

principal place of business is located at 370 Knollwood Street, Winston-Salem, North Carolina.

Throughout the Class Period, Krispy Kreme's common stock traded in an efficient market on the

NYSE.

12. Defendant Randy S. Casstevens was at all relevant times Chief Financial

Officer of Krispy K.reme until his resignation effective December 23, 2003.

13. Defendant Scott A. Livengooci ("Livengood") was, at all relevant times,

Chairman and Chief Executive Officer of Krispy Kreme.

14. Defendant Michael C, Phalen ("Phalen") has been Chief Financial Officer

ot'Krispy Kreme since January 2004.

15. Defendant John W. Tate ("Tate") was at all relevant times Chief Operating

Officer of Krispy Kreme.

16. Defendants Casstevens, Livengood, Phalen and Tate are collectively

referred to herein as the "Individual Defendants," The Individual Defendants, because of their

5

positions with the Company, possessed the power and authority to control the contents of Krispy

Kreme's quarterly reports, press releases and presentations to securities analysts, money and

portfolio managers and institutional investors. Each defendant was provided with copies of the

Company's reports and press releases alleged herein to be misleading prior to or shortly after

their issuance and had the ability and opportunity to prevent their issuance or cause them to be

corrected.

17. Because of their positions and access to material non-public information,

each of the Individual Defendants knew that the adverse facts specified herein had not been

disclosed to and were being concealed from the public and that the positive representations

which were being made were then materially false and misleading. The Individual Defendants

are liable for the false statements pleaded herein, as those statements were each "group-

published" information, the result of the collective actions of the Individual Defendants,

SCIENTER

IS, Each Individual Defendant had knowledge of Krispy Kreme's problems

and was motivated to conceal such problems As Chief Executive Officer, defendant Livengood

reviewed or was responsible for the preparation of many of the internal reports showing Krispy

Kreme's forecasted and actual growth and thus defendant Livengood, as well as the other

Individual Defendants, were aware of the company's significant operational and financial

problems before these problems became known to the investing public. Defendants, as directors

and/or officers of Krispy Kreme were responsible for the financial results and press releases

issued by the Company. Each Individual Defendant sought to demonstrate that they could lead

the Company successfully and generate the growth expected by the market.

51

19. Defendants knew or deliberately disregarded that the materially false and

misleading statements and omissions complained of herein would adversely affect the integrity

of the market for the Company's securities and would artificially inflate the price of the

Company's publicly-traded securities. Defendants acted knowingly or with such deliberate

disregard of such facts as they should have known in such a manner as to constitute a fraud and

deceit upon plaintiff and other members of the Class,

20. Moreover, during the Class Period, insiders sold 1.5 million Krispy Kreme

shares for proceeds of $50.1 million. The sale was executed through Jubilee Investments

Limited Partnership, formerly McAleer Investments Limited Partnership ("Jubilee"), which is a

limited partnership established by Krispy Kreme insider John N McAleer ("McAleer") and

members of his family, McAleer is Vice Chairman of the I'Zrispy Kreme Board and Krispy

Kreme's Executive Vice President of "Concept Development." On August 26, 2004, when

Krispy Kreme was trading at approximately $43.50, Jubilee entered into a forward contract for

the sale of 1.5 million Krispy Kreme shares for delivery in two tranches in September 2007 and

March 2007 respectively, for an aggregate purchase price of $50,186,618

FRAUDULENT SCHEME AND COURSE OF BUSINESS

21. Each defendant is liable for: (i) making false statements; and (ii) failing to

disclose adverse facts known to him about Krispy Kreme. Defendants' fraudulent scheme and

course of business that operated as a fraud or deceit on purchasers of Krispy Kreme publicly

traded securities were a success, as they (i) deceived the investing public regarding Krispy

Kreme's prospects and business and (ii) artificially inflated the prices of Krispy Kreme's

publicly-traded securities; and (iii) sold 1.5 million shares of Krispy Kreme stock for proceeds of

$50.1 million.

7

DEFENDANTS FALSE AND MISLEADING STATEMENTS ISSUED DURING THE CLASS-PERIOD

22. The Class Period commences on August 21, 2003. On that date

defendants issued a release over the PRNewswire in which they reported Krispy Kreme' s

financial results for the three months ended August 3, 2003, the Company's second quarter of

Fiscal 2004. The release stated that income for the second quarter increased 46.8% to $13.0

million compared with $8.9 million in the second quarter of Fiscal 2003, and that diluted

earnings per share increased to $0.21 in the second quarter compared with $0.15 for the same

period in Fiscal 2003. Reported diluted earnings per share were $0.01 more than analysts'

forecasts. Defendants further reported that total Company revenues, which include sales from

company stores, franchise operations, Krispy Kreme Manufacturing and Distribution (KXM&D)

and Montana Mills, rose 41.1% to $161.8 million, compared with $114.6 million in the prior

year comparable period. On a comparable store basis, systemwide store sales purportedly

increased 11.3% and company store sales were up 15.6%.

23. In the release, defendants touted the Company's growth and bright

prospects without giving any indication that they had saturated the market with Krispy Kreme

products and that such saturation were having a deleterious effect on the Company's operating

performance and financial results. In this regard, the release stated, in relevant part, as follows:

"Krispy Kreme had an extremely exciting second quarter that included a number of significant events for the Company," said Scott Livengood, Chairman, President and Chief Executive Officer. "We experienced great success when we opened our first store outside North America in Sydney, Australia. We also set new opening day and opening week sales records in our first store in the Boston market, Finally, we served the first-ever Krispy Kreme doughnuts in a French-speaking environment in Montreal, Canada and were met with great excitement when we opened there in May.' [ ... ]

8

Further commenting on the Company's financial performance, Livengood added, "The results of the second quarter and the initiatives we have underway create a strong foundation for the balance of the year. Our broadening platform, which now includes both large and small US markets, combined with our international expansion plans will create growth opportunities for years to come."

In light of the operating performance during the first half of Fiscal 2004, the Company today is establishing new long-term operating margin targets. These three to five year targets are as follows: total Company operating income as a per cent of sales: 20% and Company store operations segment income as a per cent of sales: 25%. These are changes from the previous guidance of 15% and 20%, respectively. Also, the Company indicated that based on its second quarter performance, it now expects to earn $0.91 per fully diluted share or $002 above consensus for Fiscal Year 2004. Quarterly earnings guidance is as follows: Q3 - $0.22; Q4 - $0.26.

The Company affirmed its previously announced goals of systemwide comparable sales of 10% for the year with quarterly variations. Additionally, the Company reiterated its store development plans to open 77 new stores in 17 new markets and to open 10 other units, a combination of Doughnut and Coffee Shops and/or satellite stores during Fiscal 2004.

24. On September 22, 2003, the Company issued a release over the

FRNewswire in which it announced its intention to acquire a majority interest its Michigan

franchisee, Dough-Re-Mi Co., Ltd. Pursuant to the agreement, }(rispy Kreme would acquire five

of the seven Krispy Kreme stores in Michigan, and the franchisee would close the other two

prior to consummation of the acquisition. The release stated, in pertinent part, as follows:

Scott Livengood, the Company's Chairman, President and Chief Executive Officer said, "the success of previous market repurchases has validated our acquisition strategy. We will continue to acquire or expand our interest in markets where such an acquisition is mutually advantageous for Krispy Kreme, our franchisees and our customers. We believe there is tremendous opportunity for growth in Michigan, both in retail and off-premises channels."

25. On November 21, 2003, defendants issued a release over PRNewswirc in

which they announced that net income for the third quarter had increased 43.4% to $14.5 million

compared with $10.1 million in the third quarter of Fiscal 2003, and that diluted earnings per

share had increased to $0.2:3 in the third quarter compared with $0.17 for the same period in

Fiscal 2003. With respect to the reported financial results, the release stated as follows:

"Our business momentum continues and our third quarter results reflect our focus on opening new stores, establishing strong off-premises relationships and gaining greater market share," said Scott Livengood, Chairman, President and Chief Executive Officer. "Our fundamentals remain very strong and we delivered solid results in an active quarter. Despite weather related issues and the grocery store strike that impacted several of our markets, we produced systemwide sales of $253 million and grew net income by 43%. I am very pleased with these results."

During the quarter, 27 new Krispy Kreme factory stores were opened in ten new markets, The Company opened its first factory store in Europe, located in the world-renowned department store, Harrods of Knightsbridge, London. Other new markets entered included Lansing, MI, Evansville and South Bend, IN, Hattiesburg, MS, Chico and Visalia, CA, Boise, ID, and Lubbock and Laredo, TX. This brings the total number of stores at the end of the third quarter to 326. Additionally, during the quarter the Company opened eight satellite units consisting of six fresh shops and two doughnut and coffee shops.

Subsequent to quarter end, the Company opened six new Krispy Kreme factory stores and three satellite stores consisting of two fresh shops and one doughnut and coffee shop. Also, the Company opened its first commissary in Mexico City, Mexico. Kxispy Kreme Mexico, S. de R.L, de C. V., the Company's franchisee in Mexico, will develop 20 stores over the next six years throughout Mexico.

Commenting on the Company's outlook, Livengood said, "The momentum generated by store openings, our broadening platform and growth in both our stores and off-premises give me great confidence for this year and the years to come."

Based on its latest review of factory store and satellite development plans, the Company now expects Fiscal 2004 store openings will range between 92 and 97, exceeding the previous guidance of 87 that included 77 factory stores and 10 satellites, The Company expects to earn $0.26 per fully diluted share in the fourth quarter of Fiscal 2004 and $092 for all of Fiscal 2004, including the S0.01 positive impact of the arbitration settlement recorded in the first quarter of Fiscal 2004. Additionally, the Company affirmed its previously announced goal for systemwide comparable sales of 10% for the fiscal year; systemwide comp store sales in the fourth quarter are expected to be slightly above or below 10%.

Based on the performance in the first nine months of Fiscal 2004, the Company today established a new long-term operating margin target for its Franchise Operations segment The three to five year target for franchise operating income

10

as a percent of franchise revenue was increased from 70% to a range between 75% and 85%.

26. On November 21, 2003, Bloomberg News published an article about

reaction to Krispy Kreme's earnings announcement in which it quoted the remarks of Robert

Bender & Associates analyst Reed Bender. In reliance on Krispy Kreme's public statements,

Bender stated as follows;.

"This is clearly a growth story here and I think you are still at the early stage in terms of stores, "said Reed Bender, who helps manage $250 million in assets at Robert Bender & Associates, including about 130,000 Krispy Kreme shares. "I think people are really underestimating the amount of stores this company can have"

27. On February 17, 2004, defendants issued a release over the PRNewswire

in which they preliminarily reported on the Company's purportedly strong operating

performance and financial results in the fourth quarter of fiscal 2004 which ended February 1,

2004. The release stated, in pertinent part:

The Company indicated that business momentum and sales growth continued to be strong, driven by increases in comparable store sales and new store openings. Fourth quarter systemwide sales including sales of company and franchise stores grew 25.6%. Systemwide and company comparable store sales increased 9.1% and 10.7%, respectively, for the quarter. Sales momentum increased throughout the quarter, but sales were affected by the grocery Store strikes and unseasonably warm weather early in the fourth quarter. Systemwide sales including Krispy Kreme stores and Montana Mills increased 26.6% in the fourth quarter. The Company opened 35 new stores, including 31 factory stores and 4 satellites, during the quarter. In fiscal 2004, the Company opened 99 stores, comprised of 86 factory stores and 13 satellites.

Systemwide sales including sales of company and franchise stores advanced 26.6% for fiscal 2004. On a comparable store basis, systemwide store sales increased 10.2% for the year and company store sales advanced 13,6%. Systemwide sales including Krispy Kreme stores and Montana Mills increased 27.4% for the year. Commenting on these results, Scott Livengood, the Company's Chairman, President and Chief Executive Officer stated, "We are pleased to report record systemwide sales and store openings for both the quarter and fiscal year. We experienced strong comparable store sales performance across the system in fiscal 2004, driven by continued strength among company stores."

11

Additionally, the Company estimates that diluted earnings per share will be approximately $0.26 in the fourth quarter, consistent with previous guidance. The Company expects to earn approximately $0.92 per diluted share for fiscal 2004, including the $0.01 positive impact of the arbitration settlement recorded in the first quarter. Livengood commented further, "I am especially pleased with achieving our earnings guidance in a quarter in which we continued the accelerated development of company stores. We believe these investments in new company stores, including the related pre-opening costs, will provide substantial returns to shareholders."

The Company also Issued preliminary guidance for fiscal 2005. Mike Phalen, the Company's Chief Financial Officer commented, "The forward estimates were developed based on the continuing evolution of our business model. The primary growth drivers in fiscal 2005 will continue to be opening new factory stores and improving existing store productivity. There will be increased company store development, and the forecast anticipates higher pre- opening and operating costs associated with the new stores. We will continue to invest in our international operations as well as our emerging growth initiatives including our satellite concepts and store-in-store partnerships, which are designed to make the Krispy Kreme experience more convenient to customers."

The Company expects diluted earnings per share of $1.16 to $1.18 forfiscal 2005 and systemwide comparable store sales growth in the mid-to-high single digits. The Company estimates that systemwide sales will increase approximately 25% in fiscal 2005, while each quarter may be slightly above or below 25%. Additionally, the Conpan,v expects to open approximately 120 new stores systemwide, including 20 to 25 satellites, in fiscal 2005. Commenting on the Company's outlook, Livengood stated, "Our fundamentals remain strong, and we continue to focus on delivering results and creating value for shareholders. Our broadening platform will create significant long-term growth opportunities." (Emphasis added.)

28. On December 23, 2003, defendants issued a release over the PRNewswire

in which they announced that defendant Casstevens had resigned from Krispy Kreme "to pursue

personal interests," and that defendant Plialen would become Chief Financial Officer effective

January 5, 2004.

29. On February 4, 2004, defendants issued a release over the .PR.Ncwswire in

which they announced that the Company had acquired the remaining 33% minority interest in

Golden Gate Doughnuts, LLC and that the Company now owned 100% of the rights to develop

12

the Northern California market as well as existing stores and the associated assets. The

Company did not disclose the purchase price. Commenting on the acquisition the Company

stated in the release as follows:

Scott Livengood, the Company's Chairman, President and Chief Executive Officer, said this acquisition is consistent with other recent market acquisitions by the Company, "We are excited about owing 100 percent of the Northern California market. We believe there are tremendous growth opportunities in Northern California, both in retail and off-premises channels. As we have said previously, we will continue to acquire or expand our interest in markets where such an acquisition is mutually advantageous for Krispy Kremne, our franchisees and our customers."

30. On March 10, 2004, defendants issued a release over the PRNewswire in

which they reported financial results for the fourth quarter and the fiscal year ended February 1,

2004. In the release, defendants stated that fourth-quarter net income had increased to $16.4

million, or $0.26 per share, from $5.63 million, or $0.09 per share a year earlier. Defendants

stated that fourth-quarter revenues had increased 36% to $185.5 million compared with $136.7

million in the previous fiscal year's fourth quarter. With respect to the Company's operating

performance, defendants stated in the release as follows:

Fourth quarter systemwide sales including sales of company and franchise stores advanced 25.5%. Systemwide sales were driven by an increase in company store sales of 36.0% to $124.7 million. On a comparable store basis, company store sales advanced 10,7% and systemwide sales increased 9.1%. Systemwide sales including Krispy Kreme Stores and Montana Mills rose 26.6%.

"We are pleased with our record fourth quarter results," stated Scott Livengood, Chairman, President and Chief Executive Officer of Krispy Kreme Doughnuts, Inc. "During the quarter, we continued to execute on our core business model while investing in operating initiatives designed for future growth." [.. , J

Further commenting on the Company's financial performance, Livengood added, "Fiscal 2004 was a year of milestones and our fourth quarter results cap another year marked by strong execution of our growth strategy. We produced record earnings, opened 99 new stores - a record number - and grew systemwide sales 26 percent. We plan to leverage this momentum in fiscal 2005 as we continue to

13

develop factory stores and invest in international operations and emerging growth initiatives, including satellites and store-in- store partnerships."

The Company set a new record in the fourth quarter for unit growth by opening 35 new stores, including 31 factory stores and four satellites in nine new markets, The Company opened its first store in Mexico, located in Interlomas, a suburb of Mexico City. Other new markets entered included Altoona, PA, Youngstown, OH, Atlantic City, NJ, Syracuse, NY, Lexington, KY, Kahului, HI, Onalaska, WI and Florence, AL.

31. The statements set forth in ¶j22-25, 27 and 29were materially false and

misleading for the reasons set forth in ¶4.

THE TRUTH BEGINS TO RE

32. The truth began to emerge on May 7, 2004. On that date, defendants

issued a release over the PR Newswire in which they announced that they expected fiscal 2005

diluted earnings per share from continuing operations, excluding certain charges, to be 10%

lower than previously announced guidance and blamed the decrease on increased interest in low-

carbohydrate diets. In this regard, the release stated:

Scott Livengood, Chairman, President and Chief Executive Officer commented, 'For several months, there has been increasing consumer interest in low-carbohydrate diets, which has adversely impacted several flour-based food categories, including bread, cereal and pasta. This trend had little discernable effect on our business last year. However, recent market data suggests consumer interest in reduced carbohydrate consumption has heightened significantly following the beginning of the year and has accelerated in the last two to three months, This phenomenon has affected us most heavily in our off-premises sales channels, in particular sales of packaged doughnuts to grocery store customers."

33. Defendants also announced that the Company was closing its Montana

Mills bread stores, an operation that it had bought a year ago, and that it was going to write-off

as much as $40 million on the venture; as recently as mid-April, defendants had said they

intended to refine and expand the operation.

14

34. On this news, shares of Krispy Kreme fell $9.29, or 29%, to close at

$22.51, a new 52-week low and more than 50% below the 52-week high of $49.74. The trading

volume was 20.5 million shares, the largest ever for Krispy Kreme and amounting to a third of

the shares outstanding.

35. Many analysts did not accept the Company's claim that the Atkins/South

Beach low-carb diet phenomenon was the sole reason for the Company's unexpectedly poor

operating performance and its divesture of the Montana Bread stores but rather stated that a

myriad of company-specific, undisclosed factors were responsible for the dramatic change in the

Company's financial performance and prospects. In this regard, on May 7, 2004, Reuters

published an article on Krispy Kreme's announcement that stated, in relevant part, as follows:

In the face of growing consumer distaste for high-carb foods like bread and pasta, Krispy Kreme cut its full-year earnings forecast by 10 percent and said it would shut down or sell off operations of Montana Mills Bread Co., a gourmet bread and pastry chain it bought last year.

The company also said that it will restate prior and current financial statements to recategorize Montana Mills as a discontinued operation.

The Winston-Salem, North Carolina, company also plans to close six less- profitable stores and is working to make its delivery operations more efficient due to weakened sales at grocery stores and other retailers.

The popularity of such low-carb diets as Atkins and South Beach has taken a bite out of food companies in recent months, including Kraft Foods Inc. and Interstate Bakeries Corp..

But analysts were skeptical of Krispy Kreme's efforts to blame a diet for such a broad shift in strategy.

"We believe many issues are internal," J.P Morgan analyst John Ivankoe said in a note.

Krispy Krem&s "fad appeal" appears to be waning, Ivankoc said, and the company has become increasingly dependent on selling doughnuts in grocery stores and other retailers.

15

But on a conference call with investors, Krispy Krerne Chief Executive Scott Livengood insisted the low-carb diet trend was to blame for the company's woes.

"We have used the word phenomenal multiple times, but that's what it is," Livengood said. "It is the primary variable that is different from anything we have experienced since being a public company,"

U.S. doughnut sales volume fell 0.4 percent industrywide in the 12 weeks ended April 18 from a year earlier, Krispy Kreme said. In the previous 12 weeks it had risen 7.4 percent.

One food industry expert said the low-carb trend was likely a factor for Krispy Kreme, but added most Americans had not changed the way they eat.

"It's not as if a majority of Americans are changing their diets," said Harry Balzer, vice-president of market research firm The NPD Group. "About 6 to 7 percent of the population are on a low-carb diet"

36. Similarly, on May 7, 2004, The Street.com published an article which

stated, in pertinent part:

Certainly, Krispy Kreme is being affected by the Atkins, South Beach and other low-carb diets. But just like a company that blames the weather on poor sales, some companies are better than others at weathering a storm

One source who is short Krispy Kreme cited some company-specific issues working against Krispy Kreme, which go beyond the low-carb craze. First, the company's wholesale business is expensive to operate, requiring trucks and distribution channels (and the costs associated with that). Second, the wholesale business is cannibalizing the company's retail operations, and perhaps undermining them as well.

Krispy Kreme doughnuts bought at the wholesale level are often inferior to the doughnuts that customers can get at a company store. A consumer who is trying a Krispy Kreme doughnut may be underwhelmed by the ones that sell at a grocery store, which may prevent that consumer from ever going to a retail Krispy Kreme store, where doughnuts have higher margins

Third., those retail stores -- under pressure from both the company's wholesale business and the low-carb craze -- are expensive and uneconomical in smaller markets.

"Each Krispy Kreme store costs about $3 million to open. Its not economical in every location," said the short-seller, who requested anonymity. These stores tend to hit their peak in about 12-18 months, and if you don't have a fresh supply of consumers to snap up every doughnut that comes off the conveyor belt, you end

16

up having problems, he continued. So, the company won't be closing stores in places like Los Angeles or New York, where millions of people live, but it makes little economic sense to continue operating less profitable stores in smaller markets.

37. On May 7, 2004, Motley Fool published an item about Krispy Kreme

under the headline, "Krispy Kreme: Deep Fried?" The article stated in pertinent part, as follows:

Has it finally happened? Has the low-carb trend, which has plagued many a food company, finally hit Krispy Kreme Doughnuts (NYSE: KKD)? For the first time ever, the doughnut purveyor issued a profit warning today, pushing its stock price down nearly 25% in recent trading.

A Motley Fool Stock Advisor pick. Krispy Kreme said it now anticipates fiscal 2005 earnings to be 10% lower than its previous guidance. First-quarter earnings are now seen coming in at $0.23 per share, while fiscal 2005 earnings will be $1.04 to $1.06 per share; including charges, Krispy Kreme forecasts annual earnings of $0.93 to $095 per share.

There are ufew things to wonder about here, not least of which are sudden changes. After all, historically, Krispy K,eine has delivered steady revenue and earnings growth despite building interest in carb cutting over the last year [ ... ]

If investors really thought that this was the crux of the problem, though, they might have relaxed today. Krispy Kreme recently said it was working to develop a lower-carb, lower-fat doughnut (a move to which I played devil's advocate, wondering about undermining the almighty, decadent brand). Right now, though, if low-carb diets are indeed plaguing Krispy Kreme, I question why it didn't mention this development effort in its press release today. At the same time, the company did say it was among the initiatives its pursuing "urgently" in its conference call (transcript courtesy of CCBN StreetEvents).

The other aspect of today's press announcement that might warrant a critical eye, is the company's announcement that it will sell Montana Mills, a bread and pastry concept that Krispy Kreme bought for $40 million only a little over a year ago. While we love companies that focus, it seems like a rather sudden development.

When Krispy Kreme previously seemed insulated against the lowcarb trend, was there more going on than met the eye? While some might see Krispy Kreme as an exceptional bargain in the event that the low-cub craze ends up just another passing fad -- which, of course, would give credence to the idea that today's warning is only a temporary speed bump in the company's long-term

17

growth rate -- would-be Krispy Kreme shareholders have a lot of food for thought before gobbling up shares. (Emphasis added.]

38. As a result of the materially false and misleading statements and failures

to disclose as alleged herein, Krispy Kreme common stock traded at artificially inflated prices

during the Class Period, Plaintiff and other members of the Class purchased or otherwise

acquired Krispy Kxeme common stock relying upon the integrity of the market price of Krispy

Krcme shares and market information relating to Krispy Kreme and have been damaged thereby.

39. During the Class Period, defendants materially misled the investing public

as alleged herein, thereby inflating the price of Krispy Kreme stock, by publicly issuing false and

misleading statements and omitting to disclose material facts necessary to make defendants'

statements, as set forth herein not false and misleading. Defendants failed to disclose the

material facts alleged herein at the times they made their statements to the market as concerning

the Company's financial condition and operational results.

FIRST CLAIM FOR RELIEF

For Violation Of §10(b) 01 The 1934 Act And Rule 10b-5 Against All Defendants

40 Plaintiff repeats and realleges each and every allegation contained above

as if fully set forth herein.

41. During the Class Period, defendants disseminated or approved the false

statements specified above, which they knew or deliberately disregarded were misleading in that

they contained misrepresentations and failed to disclose material facts necessary in order to make

the statements made, in light of the circumstances under which they were made, not misleading.

42. Defendants violated §10(b) of the 1934 Act and Rule lOb-5 in that they:

a. Employed devices, schemes, and artifices to defraud;

18

b. Made untrue statements of material facts or omitted to state

material facts necessary in order to make the statements made, in light of the circumstances

under which they were made, not misleading; and/or

C. Engaged in acts, practices, and a course of business that operated

as a fraud or deceit upon plaintiff and others similarly situated in connection with their purchases

of Krispy Kreme publicly traded securities during the Class Period.

43. Plaintiff and the Class have suffered damages in that, in reliance on the

integrity of the market, they paid artificially inflated prices for Krispy Kreme publicly-traded

securities. Plaintiff and the Class would not have purchased Krispy Kreme publicly-traded

securities at the prices they paid, or at all, if they had been aware that the market prices had been

artificially and falsely inflated by defendants' misleading statements.

44 As a direct and proximate result of these defendants wrongful conduct,

plaintiff and the other members of the Class suffered damages in connection with their purchases

of Krispy Kreme publicly traded securities during the Class Period.

SECOND CLAIM FOR RELIEF

For Violation Of §20(a) Of The 1934 Act Against All Defendants

45. Plaintiff repeats and realleges each and every allegation contained above

as if filly set forth herein,

46. The Individual Defendants acted as controlling persons of Krispy Kreme

within the meaning of §20(a) of the 1934 Act. By reason of their positions as officers and/or

directors of Krispy Kreme, and their ownership of Krispy Kreme stock, the Individual

Defendants had the power and authority to cause Krispy Kreme to engage in the wrongful

conduct complained of herein. Krispy Kreme controlled each of the Individual Defendants and

19

all of its employees. By reason of such conduct, the Individual Defendants and Krispy Kreme

are liable pursuant to §20(a) of the 1934 Act.

CLASS ACTION ALLEGATIONS

47. Plaintiff brings this action as a class action pursuant to Rule 23 of the

Federal Rules of Civil Procedure on behalf of all persons who purchased Krispy Kreme publicly

traded securities (the "Class") on the open market during the Class Period. Excluded from the

Class are defendants, members of their immediate families and their legal representatives, heirs,

successors or assigns and any entity in which defendants have a controlling interest.

48. The members of the Class are so numerous that joinder of all members is

impracticable The disposition of their claims in a class action will provide substantial benefits

to the parties and the Court. During the Class Period, Krispy Kreme had more than 150 million

shares of stock outstanding, owned by hundreds if not thousands of persons.

49. There is a well-defined community of interest in the questions of law and

fact involved in this case. Questions of law and fact common to the members of the Class which

predominate over questions which may affect individual Class members include;

a. Whether the 1934 Act was violated by defendants;

b. Whether defendants omitted and/or misrepresented material facts;

C. Whether defendants' statements omitted material facts necessary to

make the statements made, in light of the circumstances under which they were made, not

misleading;

d. Whether defendants knew or deliberately disregarded that their

statements were false and misleading;

20

e. Whether the prices of Krispy Kreme's publicly traded securities

were artificially inflated; and

f. The extent of damage sustained by Class members and the

appropriate measure of damages.

50, Plaintiff's claims are typical of the claims of the members of the Class as

all members of the Class are similarly affected by defendants' wrongful conduct in violation of

federal law that is complained of herein.

51. Plaintiff will adequately protect the interests of the members of the Class

and has retained counsel competent and experienced in class action securities litigation.

(Plaintiff has no interests which may conflict with other members of the Class.

52. A class action is superior to other available methods for the fair and

efficient adjudication of this controversy since joinder of all members in impracticable

NO SAFE HARBOR

53 The statutory safe harbor provided for forward-looking statements under

certain circumstances does not apply to any of the allegedly false forward-looking statements

pleaded in this Complaint, The safe harbor does not apply to Krispy Kreme's allegedly false

statements made during the Class Period. None of the written forward-looking statements made

were identified as forward-looking statements, nor was it stated that actual results "could differ

materially from those projected." Nor did meaningful cautionary statements identifying

important factors that could cause actual results to differ materially from those in the forward-

looking statements accompany those forward-looking statements. Each of the forward-looking

statements alleged herein to be false was authorized by an executive officer of Krispy Kreme and

was actually known by each of the Individual Defendants to be false when made.

21

PRAYER FOR RELIEF

WHEREFORE, plaintiff prays for judgment as follows:

i) Determining that this action to be a proper class action

pursuant to Rule 23 of the Federal Rules of Civil Procedure;

ii) Awarding plaintiff and the members of the Class

compensatory damages;

iii) Awarding plaintiff and the members of the Class pre-

judgment and post-judgment interest, as well as their reasonable attorneys fees, expert witness

fees and other costs;

iv) Awarding extraordinary, equitable and/or injunctive relief

as permitted by law, equity and the federal statutory provisions sued hereunder, pursuant to

Rules 64 and 65 and any appropriate state law remedies to assure that the Class has an effective

remedy; and

v) Awarding such other relief as this Court may deem just and

proper.

JURY TRIAL DEMAND

Plaintiff hereby demands a trial by jury.

Dated: May 12, 2003

4-TmN eairney for Plaintiff

State Bar Number: 23446

FOR THE FIRM; DONALDSON & BLACK, P.A. 208 West Wendover Avenue Greensboro, North Carolina 27401 Phone: (336) 273-3812

22

MILBERG WEISS BERSHAD & SCHULMAN LLP Steven U. Schulman Peter F. Seidman One Pennsylvania Plaza New York NY 10119-0165 (212) 594-5300

LAW OFFICES OF RICHARD B. BRUALDI Richard B. Brualdi 29 Broadway Suite 1515 New York, NY 10006 (877) 495-1187

23

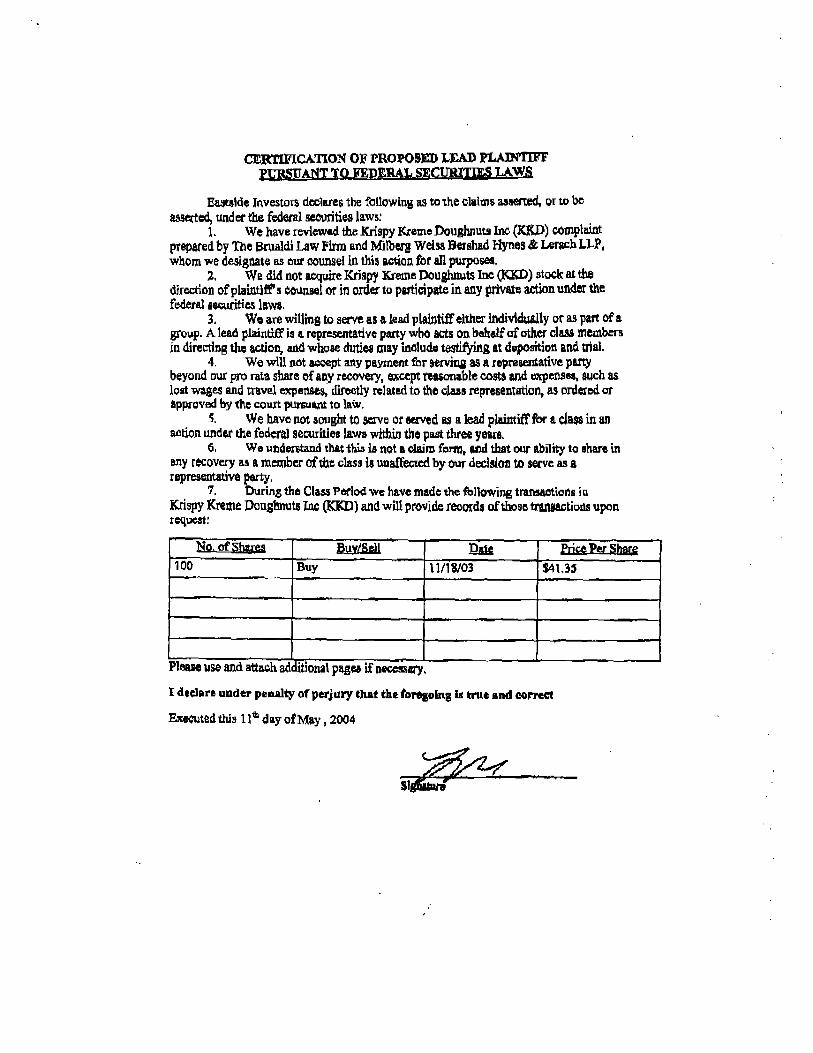

CtRTMCATION O PROPOSED LEAD PLAIN'UFT LAWS

Eaitslde Investors declares the following as to The claims asserted, or to be assetted) under the federal securities laws

I. We have reviewed the Krispy iCretne Doughnuts Inc (1(1(D) complaint prepared by The Brusidi Law Firm and Milberg Weiss Bershad Hynes & Lerach LLP, whom we designate as our counsel in this action for all purposes.

2. We did not acquire Krispy Xreme Doughnuts Inc (KXD) stock at the direction of plaintiff's cosneeI or in order to participate in any private action under the federal securities laws.

3. We are wilting to serve as a lead plaintiff either ndividuaJ.tyor as part of a group. A lead plaintiff is a representative party who acts on beheif of other class members in directing the action, and whose duties may include testng at deposition and trial.

4. We will not accept any payment for serving as a representative party beyond our pro rata share of any recovery, except reasonable costs and eipensaa, such as lost wages and travel expenses, directly related to the class representation, as ordered or approved by the court pUrSUI to law.

5. We have not sought to serve or sand as alead ptaintiffforaclassinan action under the federa' securities laws within the past three years.

6 We understand that this Is not a claias form, and that our ability to share in any recovery as a member of the class is unaffected by our decision to serve as a representative party.

7. During the Class Period We have made the fbllowing transactions in Krispy Kreme Doughnuts Inc (ICED) and will provide records of those transactions upon request

I declare under pna1ty of perjury that the foregoing k true and correct

Executed this lh day of May, 2004