Embed Size (px)

DESCRIPTION

Kuwait Energy Annual Report 2009

Citation preview

Laila Tower, 13th floor, Salem Mubarak St, Salmiya, KuwaitP.O Box 5614, Salmiya 22067 Tel.: (+ 965) 2575 5657 Fax: (+ 965) 2575 5679

Annual Report 2009

www.kec.com.kw

For queries, please contact:

Abbas Al-RasheedPublic Relations Advisor Kuwait Energy CompanyTel: (+965) 25755657 – 25755878 / Ext 314Fax: (+965) 25755679Mobile: (+965) 97298106Email: [email protected]

Kuwait Energy C

ompany

Energy in the Middle East

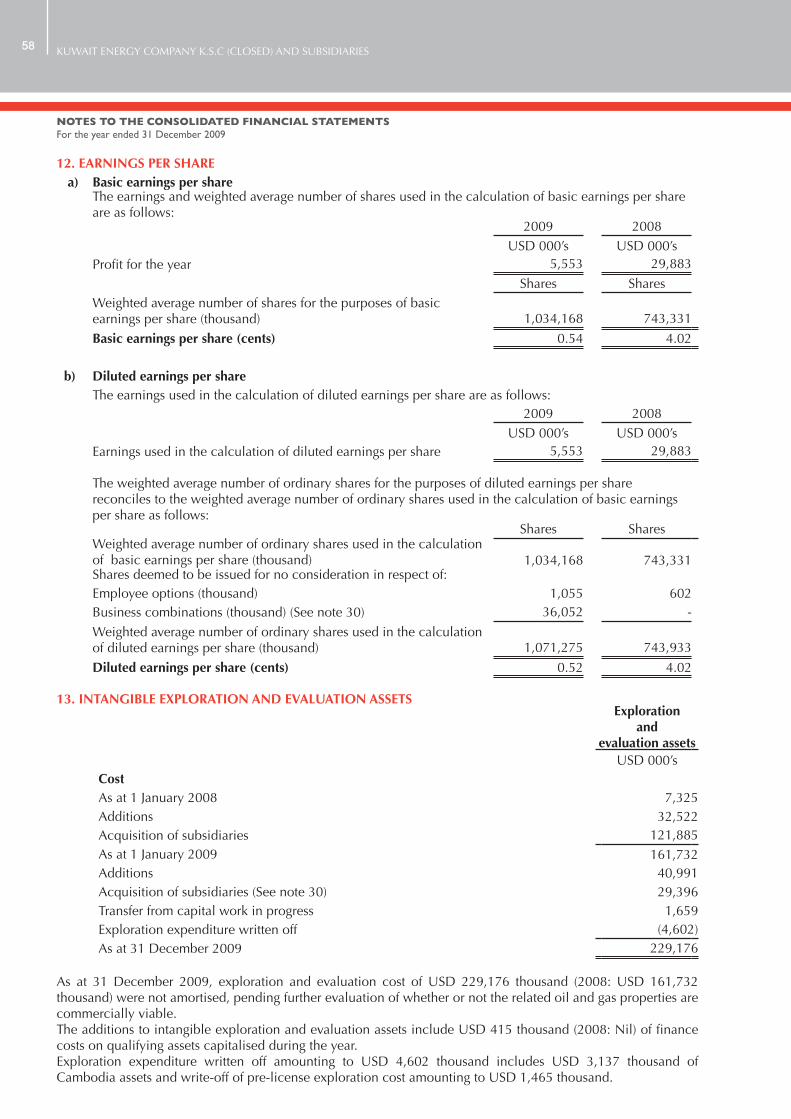

Annual Report 2009

On the cover:

Mahdy Kotb, Vice President Operations, Kuwait Energy

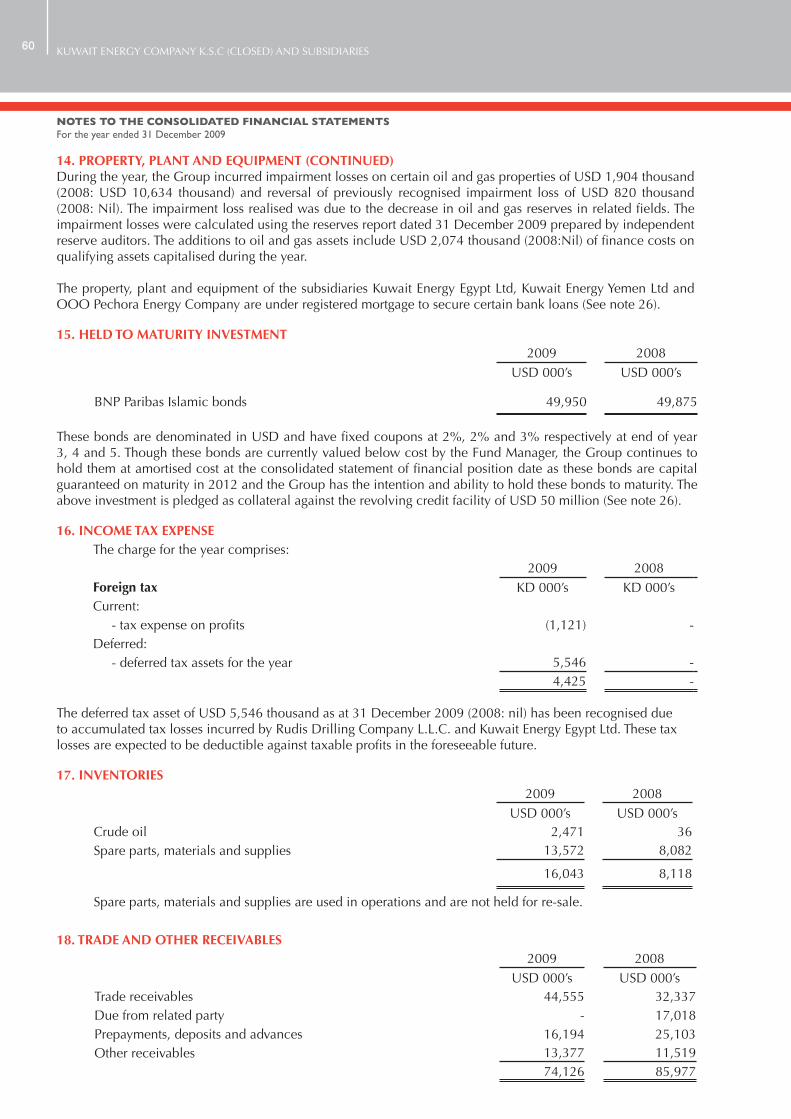

Egypt and Mohammad Al Timimy, Petroleum Engineer,

Kuwait Head Office in Burg El Arab Field, Egypt

operated by Kuwait Energy since October 2009

Laila Tower, 13th floor, Salem Mubarak St, Salmiya, KuwaitP.O Box 5614, Salmiya 22067 Tel.: (+ 965) 2575 5657 Fax: (+ 965) 2575 5679

Annu

al R

epor

t 200

9

www.kec.com.kw

For queries, please contact:

Abbas Al-RasheedPublic Relations Advisor Kuwait Energy CompanyTel: (+965) 25755657 – 25755878 / Ext 314Fax: (+965) 25755679Mobile: (+965) 97298106Email: [email protected]

Kuw

ait E

nerg

y C

ompa

ny

Energy in the Middle East

Annual Report 2009

H. H. Sheikh Nawaf Al-Ahmad Al-Jaber Al-SabahCrown Prince of the State of Kuwait

H. H. Sheikh Sabah Al-Ahmad Al-Jaber Al-Sabah

Amir of the State of Kuwait

2

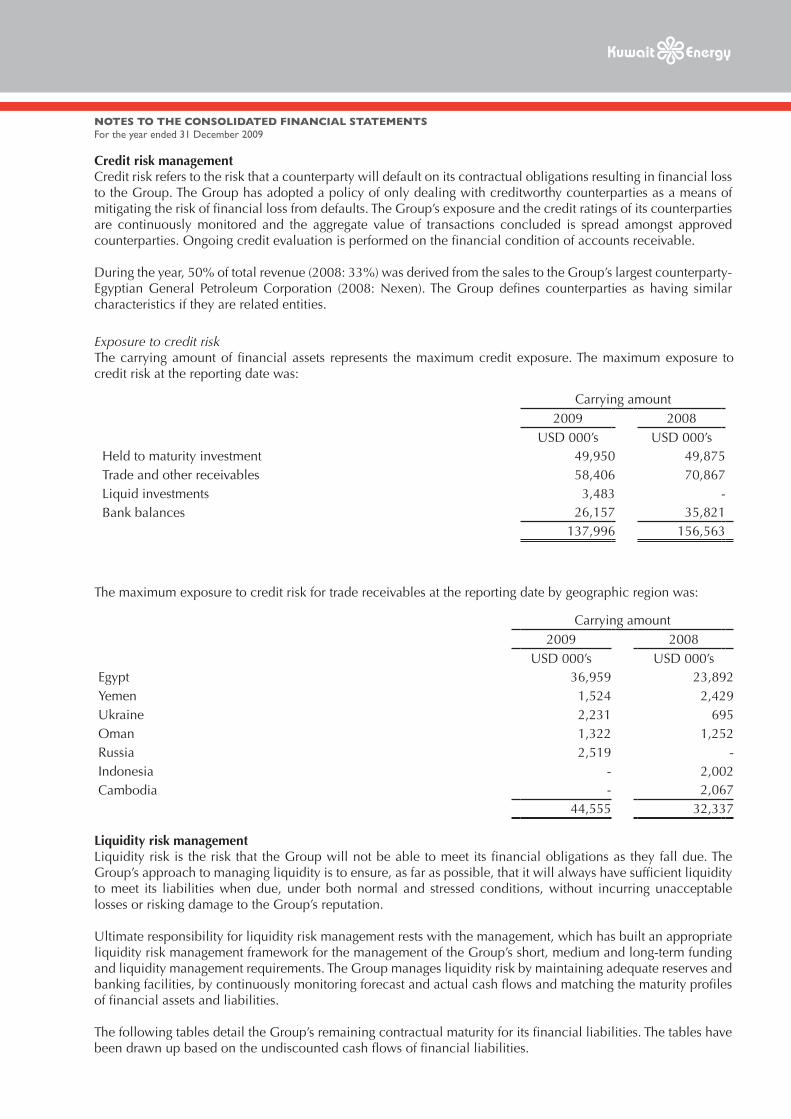

Kuwait Energy K. S. C. C. was established in 2005 and is one of the fastest growing, independent, oil and gas exploration and production companies in the Middle East.

Kuwait Energy has a high quality and diverse portfolio of oil and gas assets, and is focused on production, development and exploration of oil and gas reserves in the MENA and Eurasia regions.

Headquartered in Kuwait, the Company’s regional offices includeCairo, Sana’a, Baghdad, Moscow and Kiev overseeing operations in seven countries namely Egypt, Yemen, Oman, Ukraine, Latvia, Russia and Pakistan. Our participation interests range from 15% to 100% across our exploration and producing assets, providing a balance of risk diversification with significant upside exploration potential.

Who We Are

Executive Management Strategy Meeting - 29 October 2009, Kuwait

Energy in the Middle East

Contents

Message from the Chairman & Managing Director 06

Board of Directors 08

Kuwait Energy Assets 10

Financial and Operating Highlights 12

Chief Executive’s Report 15

Financial Performance 15

Acquisitions 15

Operations 16

Development Activities 18

Reserves 19

Exploration Activities 20

Business Development 21

Other Corporate Activities 22

Corporate Governance Report 25

Internal Management Controls 25

Corporate Governance Review by IFC 25

Board Performance 25

Board Committees 26

Remuneration Report 30

Remuneration Disclosures – Executive and Non-Executive Directors 30

Employee Incentive Scheme 31

Kuwait Energy Five Year Summary 33

Consolidated Financial Statements and Independent Auditors’ Report for the year ended 31 December 2009 34

Glossary & Definitions 75

4

2009 Milestones

Energy in the Middle East

Oil Storage Tanks, Burg El Arab, Egypt

6

On behalf of my colleagues on the Board of the Kuwait Energy Company, I have great pleasure in presenting the Annual Report for the fiscal year ending31 December 2009, which was another profitable year with an increase in reserves and production.

Financial OverviewKuwait Energy was able to secure an innovative, Sharia-compliant, Islamic reserve based financing of US$50 million from the International Finance Corporation (IFC) despite the global markets’ continued state of turmoil and volatility. This was the first time that the IFC had offered this type of financing in the oil and gas industry, to support a local private oil and gas company in the Middle East and North Africa (MENA) that is expanding regionally and providing valuable jobs and revenues to governments.

The US$50 million is being utilized for the development and exploration of our assets in Egypt and Yemen. The primary focus in 2009 was to consolidate the eight assets acquired from Oil Search in 2008, with our existing assets in these countries, to build upon our operational and technical expertise and enhance our reputation as an operator.

Kuwait Energy reported a net profit of US$5.6 million for 2009 which follows on from the company successfully reporting yearly net profits since its inception in August 2005. The year-end exit working interest production achieved for 2009 was 15,927 barrels of oil equivalent per day (boepd), a 68% increase on 2008. Revenue remained stable at US$88.3 million, down 3%

from 2008 due to a lower realised oil price in 2009, despite higher production.

OperationsKuwait Energy’s first exploration drilling program began in 2008 and yielded three exploration successes out of four wells in Egypt. This high success rate continued into 2009 with four exploration discoveries in Egypt from ten wells, with two of these discoveries coming from Kuwait Energy operated blocks.

Our exploration focus is on the MENA region, which is a prolific hydrocarbon bearing region with lower risk. Our exploration results to date reflect this lower risk.

In 2009, Kuwait Energy continued to move reserves from undeveloped to developed by the drilling of 35 development wells with four wells drilling at year-end. The majority of these development wells were drilled in the MENA region. Kuwait Energy’s year end 2009 proved and probable reserves increased by 18% to 51.2 million barrels of oil equivalent (mmboe).

Kuwait Energy’s exploration portfolio increased with the successful bid for the prospective North Block in Latvia.

Acquisition activity continued in 2009 with Kuwait Energy successfully acquiring additional working interests and operatorship of the following assets:· 25.00% in Burg El Arab, Egypt· 12.00% in Abu Sennan, Egypt · 63.44% in Luzskoye and Chikshina, Russia (subject to completion).

Message from the Chairman& Managing Director

Energy in the Middle East

Corporate DevelopmentWith an impressive growth record to date and the desire to fund further significant growth, Kuwait Energy was granted approval by its shareholders at the 2009 AGM to explore a possible listing on the London and/or Kuwait Stock Exchanges. The company has appointed the following Advisors to assist the Company in executing this significant event:

• JP Morgan as Financial Advisor • Deloitte as Reporting Accountant• Lovells as Legal Counsel• Pelham Bell Pottinger as Financial Public Relations Advisor

Corporate GovernanceKuwait Energy sought the IFC’s input on corporate governance best practices. The IFC assessed Kuwait Energy’s current corporate governance framework and provided recommendations for improvement, based on IFC’s corporate governance methodology. Kuwait Energy has committed to pursuing these improvements to bring its corporate governance framework in line with international practices and standards.

Health, Safety, Environment and Social ResponsibilityKuwait Energy gives Health, Safety and Environment and Social Responsibility (HSESR) high importance in its operational activities. Our Egypt operations recorded zero Lost Time Incident during 2009; an achievement of which all of us at Kuwait Energy are immensely proud. Additionally, some of our Eurasia operations recently achieved ISO 9001 (Quality Management System) and ISO 14001 (Environmental Management System) certifications.

Kuwait Energy is a founder member and co-sponsor of the Kuwait Science Fair together with ExxonMobil Exploration and Production Kuwait Limited and the Kuwait Scientific Centre. This is an initiative to develop and nurture interest in science in the youth of Kuwait. An inter-school quiz competition is held once a year that is well represented and attended by over 50 high schools in Kuwait.

As part of IFC’s requirements for the US$50 million Reserve Based Funding granted to Kuwait Energy, we are required to demonstrate Corporate Social Responsibility by way of contributions to sustainable economic development by working with our employees, their families, the local communities and the society at large. Kuwait Energy is working with the IFC to develop a detailed environmental and social action plan to enhance the Company’s operations as well as to contribute to the development of the countries in which it operates.

Board CompositionWalter Brandhuber, formerly Managing Director of Millennium Private Equity Energy Fund headquartered in Dubai, United Arab Emirates joined the Board of Directors, bringing 28 years of experience in the international oil and gas industry.

EmployeesKuwait Energy enjoys a multinational, multicultural workforce with its employees coming from over 22 countries. Kuwait Energy had 292 employees at the end of 2009, a growth of 27% in employee

strength over 2008. On behalf of the Directors, I would like to thank everyone at Kuwait Energy for their valuable contribution, energy and commitment in 2009 to advancing the interests of our shareholders.

OutlookKuwait Energy’s vision, since commencement in 2005, is to achieve production of 50,000 barrels of oil equivalent per day and reserves of 300 million barrels of oil equivalent by the end of 2010. The company remains focused on achieving these ambitious targets and acknowledges that these targets would in all likelihood be met through inorganic growth. The Board remains focused on ensuring that any growth transaction meets strict financial targets, is complementary to our existing asset base and operations and provides value to our shareholders.

There are outstanding opportunities for developing oil and gas assets in the Middle East as the region opens up to international oil companies. Kuwait Energy is uniquely placed to access these assets given its local knowledge, technical understanding, commercial ability and international experience in a team built up over the last four to five years.

Your company is working hard on capturing a number of the large scale projects available in Yemen, Iraq and Kuwait. For us, 2010 promises to be an exciting year and we expect to deliver enormous growth to our shareholders through one or more of these exceptional projects.

Dr. Manssour AboukhamseenChairman & Managing Director

8

Board of Directors

Dr. Manssour Aboukhamseen, Chairman & Managing Director

Dr. Manssour Aboukhamseen is a successful business entrepreneur and leader and the founder of several successful business enterprises.

He has over 23 years of experience in the oil and gas industry in Kuwait Oil Company (KOC), Zahra Group and Kuwait Energy.

He has a Ph.D. in Modern History from Berkeley University, California, USA

Board member and Chairman since June 2006.

Sara Akbar, Chief Executive Officer

Sara Akbar is a well known figure in the industry, both inKuwait and internationally.

She has over 28 years experience in the oil and gas industry having worked in several challenging senior positions in KOC and in Kuwait Foreign Petroleum Exploration Company (KUFPEC).

She has a B.Sc in Chemical Engineering from the Kuwait University.

Board member and Chief Executive Officer (CEO) sinceOctober 2005.

Dr. Manssour AboukhamseenSara Akbar

Jason SelchTareq Al Wazzan

Walter Brandhuber Mohammad Algharaballi

Ashour Habeeb

Energy in the Middle East

Jason Selch, Non-Executive Director

Jason Selch is the Managing Director of Equity Group Investments, a private investment firm based in Chicago,USA and since 2002 has been a member of the Board of Directors of MB Financial Bank, a Chicago based commercial bank with US$8 billion in assets.

He holds both a BA in Economics and MBA in Finance from the University of Chicago. He was awarded the Chartered Financial Analyst (CFA) designation in 1997.

Board member since January 2007.

Tareq Al Wazzan, Non-Executive Director

Tareq Al Wazzan is the CEO of Aref Energy Holding Company, a subsidiary of the Aref Investment Group, a leading investment group in Kuwait.

He has over 23 years experience in the oil & gas industry managing several strategic projects and has gathered an in depth understanding of the oil supply chain and international energy markets with Kuwait Petroleum Corporation (KPC).

He has a B.Sc in Business Administration from San Diego State University, USA.

Board member since March 2008.

Mohammad Algharaballi, Non-Executive Director

Mohammad Algharaballi heads the Business Development in Aref Energy Holding Company, a subsidiary of Aref Investment Group, a leading investment group in Kuwait.

Prior to joining Aref Energy Holding in 2007, Mohammad Algharaballi worked with KOC for over 14 years where he gained vast experience in the oil and gas production operations and corporate planning.

He has a B. Sc in Petroleum Engineering from Colorado School of Mines, USA.

Board member since March 2008.

Ashour Habeeb, Non-Executive Director Ashour Habeeb is Vice President – Corporate Affairs, Zahra Group Holding, Kuwait. He has over 35 years experience in the oil and gas industry where he has worked in various capacities in KPC and KOC as Manager of Sales & Administration, Manager of Bunker Sales and Manager of Crude Oil & LPG. He also worked for the Gulf Oil Corporation at Port Arthur Texas Refinery, USA for a year. He has a Diploma in Oil Handling, University of Pittsburgh, Pennsylvania, USA. Board member since October 2008.

Walter Brandhuber, Non-Executive Director

Walter Brandhuber is a founding Principal and CEO of Eastbridge Al Mal Investments Ltd. headquartered in Dubai, United Arab Emirates. Prior to joining Eastbridge, Walter was Managing Director of the Millennium Private Equity Energy Fund during which time the fund invested in Kuwait Energy among other transactions.

He holds a BA from Loyola University of Chicago, an MBA from the University of Notre Dame and a Doctor of Jurisprudence from the University of Oklahoma, USA.

Board member since May 2009.

10

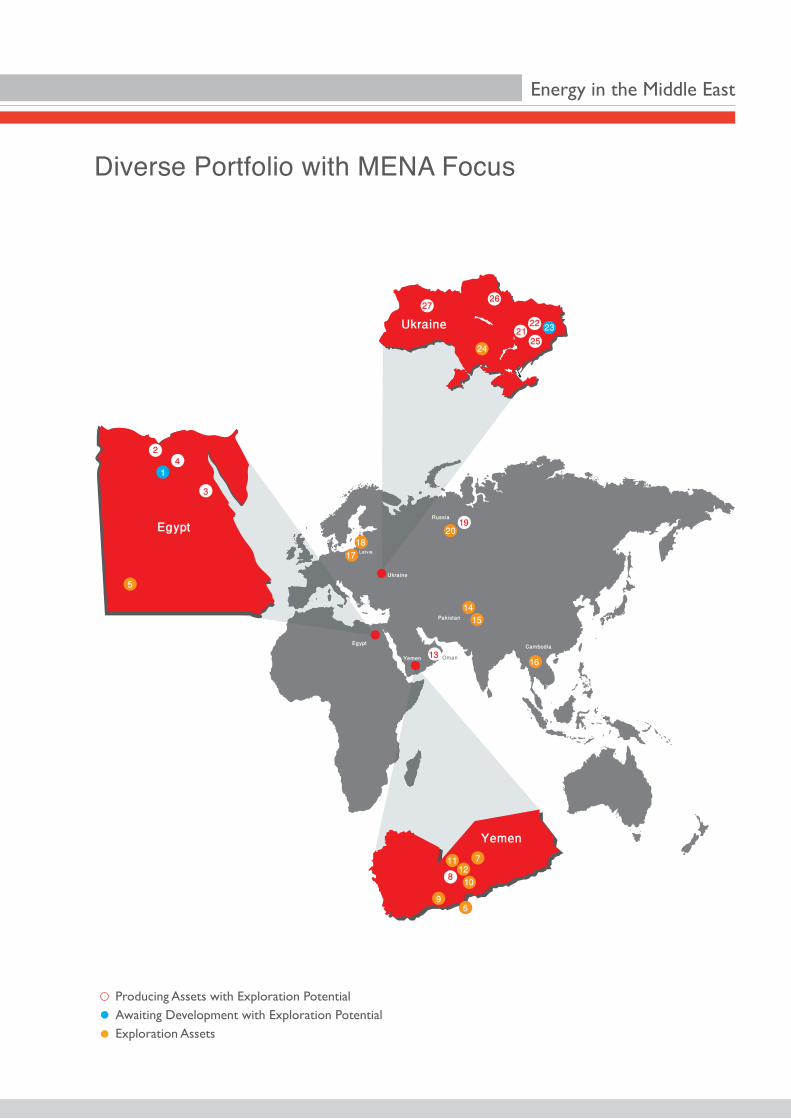

Kuwait Energy AssetsKuwait Energy Group Interests as at 31 March 2010

Country Ref Asset/Block/Field Revenue Interest Cost Interest Operator

% %

Egypt

1 Abu Sennan 72.0% 100.0% Kuwait Energy

2 Burg El Arab (BEA) 75.0% 75.0% Kuwait Energy

3 Area A 70.0% 70.0% Kuwait Energy

4 ERQ 49.5% 49.5% Sipetrol

5 Block 6 30.0% 30.0% Melrose Resources

Yemen

6 Block 15 41.6% 43.8% Kuwait Energy

7 Block 35 32.5% 34.2% Kuwait Energy

8 Block 43 28.3% 33.3% DNO International

9 Block 49 42.33% 49.8% Kuwait Energy

10 Block 74 34.0% 40.0% Kuwait Energy

11 Block 82 21.3% 25.0% Medco Energi

12 Block 83 21.3% 25.0% Medco Energi

Oman 13 Karim Small Fields 15.0% 15.0% Medco LLC

Pakistan14 Jherruck 40.0% 40.0% NHEPL

15 Kunri 40.0% 40.0% NHEPL

Cambodia 16 Block E 20.6% 20.6% Medco Energi

Latvia17 License 1 45.0% 50.0% Kuwait Energy

18 North Block 45.0% 50.0% Kuwait Energy

Russia19 Luzskoye 100.0% 100.0% Kuwait Energy

20 Chikshina 100.0% 100.0% Kuwait Energy

Ukraine

21 Bilousivska (B) 100.0% 100.0% Kuwait Energy

22 Chornukhynska (C) 100.0% 100.0% Kuwait Energy

23 North Yablunivska (NY) 100.0% 100.0% Kuwait Energy

24 Dubrivska 100.0% 100.0% Kuwait Energy

25Bilske & Kulichihinske

(JAA 429)25.0% 25.0% Ukragas

26Rudivsko-

Chervonozavodske (RC)14.9% 16.6% Ukranafta

27 Bytkiv-Babchenske 45.0% 45.0% UkrCarpat Oil

Energy in the Middle East

Diverse Portfolio with MENA Focus

Producing Assets with Exploration Potential Awaiting Development with Exploration PotentialExploration Assets

12

Sales Revenues US$ million 88.3 90.8

Cost of Sales US$ million 70.8 71.0

EBITDA US$ million 50.4 53.5

Net Income US$ million 5.6 29.9

Net Cash from Operating Activities US$ million 33.5 7.4

Property, Plant & Equipment US$ million 102.7 226.6

Exploration Evaluation Assets US$ million 72.0 154.4

Total Capital Expenditures US$ million 174.7 381.0

Total Assets US$ million 680.9 577.7

Net Debt (Non-Collateralised) US$ million 28.0 -

Shareholder Equity US$ million 580.1 525.7

Earnings Per Share US Cents 0.52 4.02

Exit WI Production BOEPD 15,927 9,478

Proven Plus Probable Reserves* MMBOE 51.2 43.4

Exploration Wells # 10 4

Development Wells # 39 44

Workovers # 44 46

Financial and Operating Highlights

2009 2008

* Excludes Oman where the Service Agreement does not allow external Reporting.

Energy in the Middle EastEnergy in the Middle East

Producing Well, Area A, Egypt

Drilling Operations at BC Fields, Ukraine

Energy in the Middle East

Chief Executive’s Report

On behalf of the management team of Kuwait Energy, I present this report on our activities in 2009:

Kuwait Energy continued on its growth path by increasing production, adding reserves, increasing the number of operated assets and building upon its employee strength. A financing facility of US$50million was obtained to enable future growth of our asset base and a net profit of US$5.6 million was achieved,despite the global financial crisis andlower oil prices. I am very proud to announce that Kuwait Energy has reported a profit every year since itsinception.

a. Financial Performance

Profits: Our financial performancebenefited from our increasedproduction, however lower realised oil prices resulted in a net profitdecrease from US$29.9 million in 2008 to US$5.6 million in 2009.

Cash Position: The Company generated an operating cash flow ofUS$33.5 million in 2009 compared to US$7.4 million in 2008. The cash position at the end of 2009 was US$29.6 million with US$30.0 million remaining to be withdrawn from the IFC financing facility. During the yearUS$23.6 million was raised from equity and we are currently in the process of raising further equity to support the Company’s growth.

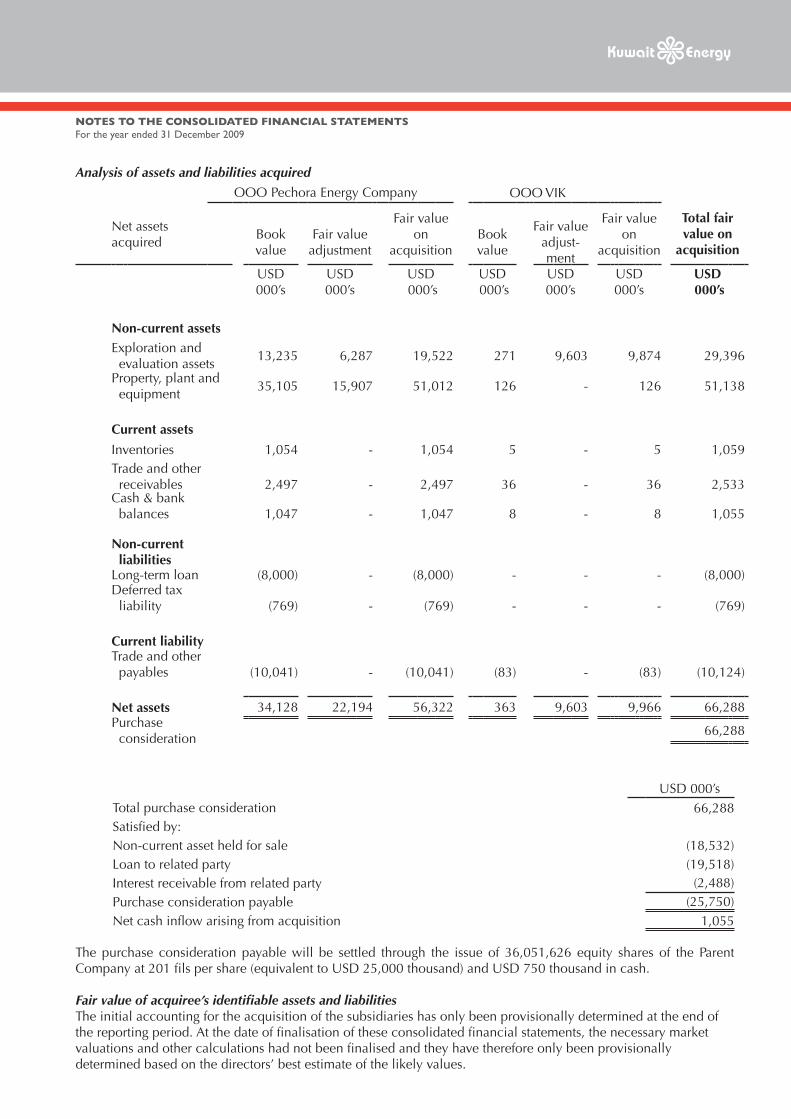

Capital Expenditure: US$174.7 million was spent on: • Payment for the purchases of additional interests in Abu Sennan and Burg El Arab Egypt; • Acquiring Russian assets of Pechora Energy Company and VIK;• Exploration and developing the existing assets of the Company, especially in Egypt and Ukraine.

Credit Rating: Kuwait Energy was credit rated by Capital Intelligence, Cyprus in July 2009 and was accredited with a long term rating of BBB-. The drivers of this rating include a well capitalized balance sheet, an increasing barrels per day production, a coherent strategy aided by very good management and a significant increase in projectedreserves.

b. Acquisitions

Acquisition of Russian assets from Pechora Energy Company and VIK: On 31 December 2009, Kuwait

Energy agreed to acquire (for shares) Pechora Energy Company and VIK (two wholly owned subsidiaries of Concorde Oil & Gas Plc), the owners of two assets Luzskoye and Chikshina in Russia. The transaction is expected to complete by June 2010. Prior to completion, Kuwait Energy has a 36.56% interest in the two subsidiaries.

Luzskoye is producing oil and is in the early stages of development whereas the Chikshina development is scheduled to commence in 2010. The year-end proved and probable reserves for these Russian assets were 18.1 million barrels of oil equivalent. Kuwait Energy is now the operator of these assets and is actively reducing overheads by shutting down the London, Moscow and Pechora offices and opening anoffice in Ukhta from where theseassets will be operated.

Acquisition of additional interests in existing Egyptian assets: Burg El Arab

On 14 July 2009, Kuwait Energy signed an agreement with Gharib Oil Fields to acquire an additional 25% interest in the Burg El Arab field inthe Western Desert, Egypt and to take over its operatorship. The year-end proved and probable reserves for Burg El Arab were 10.5 million barrels of oil equivalent in which Kuwait Energy has a 75% interest.

Since becoming the operator on 4 August 2009, Kuwait Energy has experienced exploration success with

16

its first well in BEA N-1X. The plan is to enhance further value by the acceleration of development and exploration drilling, both in the current producing horizons as well as in the deeper Jurassic formation. Four development wells and two exploration wells are scheduled for 2010.

Abu SennanIn 2009, Kuwait Energy completed the acquisition of an additional 3% interest from Tradewinds and 9% interest from Dover in Abu Sennan, which is located in the Western Desert, Egypt. Kuwait Energy is the operator of this asset which is scheduled to commence production in the second quarter of 2010. The year end proved and probable reserves for Abu Sennan are 1.0 million barrels of oil equivalent of which Kuwait Energy has a 72% interest. This block is viewed as one of Kuwait Energy’s most prospective blocks.

c. Operations

ProductionKuwait Energy’s production has continued to grow year on year with 2009 exit production of 15,927 boepd, a 68% increase in comparison to 2008. This increase was primarily due to the production from the development of exploration discoveries Shukheir North West in Area A and Al Zahraa in East Ras Qattara, the successful workover of Ch3a well in Ukraine and the increased interests in our Egyptian and Russian assets.

The ARD fields contract in Indonesia ended on 22 April 2009.

In the East Ras Qattara fields in Egypt, production operations were constrained in 2009 owing to transport facility limitations which are now resolved.

In 2009, Kuwait Energy became the operator of Burg El Arab asset in Egypt, Luzskoye and Chikshina assets in Russia and the North Block asset in Latvia increasing the number of assets operated to fourteen.

Energy in the Middle East

2009 Daily Average 2008 Daily Average % change

Country Asset BOEPD BOEPD

Egypt

BEA 193 212 -9%

Area A 4,008 1,729 132%

ERQ 2،092 798 162%

Total 6,293 2,738 130%

Ukraine

Rudis (BC & NY) 311 372 -16%

RC 284 284 0%

Bytkiv 40 37 8%

JAA 429 333 155 155%

Total 969 848 14%

Oman KSF 2,635 2,128 24%

Yemen Block 43 1,093 1,185 -8%

Russia Luzskoye 263 393 -33%

Indonesia ARD* 245 869 -72%

Kuwait Energy Total 11,499 8,160 41%

Production Summary

* ARD Fields Contract ended 22 April 2009

18

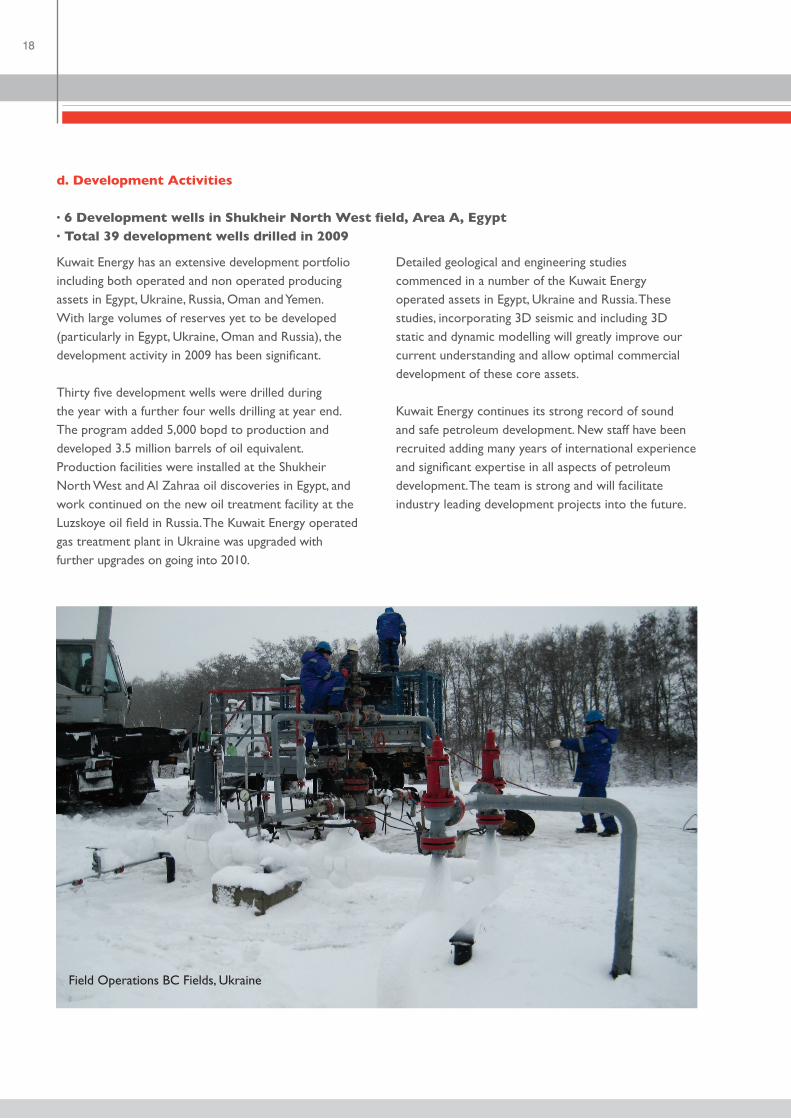

Kuwait Energy has an extensive development portfolio including both operated and non operated producing assets in Egypt, Ukraine, Russia, Oman and Yemen. With large volumes of reserves yet to be developed (particularly in Egypt, Ukraine, Oman and Russia), the development activity in 2009 has been significant.

Thirty five development wells were drilled duringthe year with a further four wells drilling at year end. The program added 5,000 bopd to production and developed 3.5 million barrels of oil equivalent. Production facilities were installed at the Shukheir North West and Al Zahraa oil discoveries in Egypt, and work continued on the new oil treatment facility at the Luzskoye oil field in Russia.The Kuwait Energy operatedgas treatment plant in Ukraine was upgraded with further upgrades on going into 2010.

Field Operations BC Fields, Ukraine

Detailed geological and engineering studies commenced in a number of the Kuwait Energy operated assets in Egypt, Ukraine and Russia. These studies, incorporating 3D seismic and including 3D static and dynamic modelling will greatly improve our current understanding and allow optimal commercial development of these core assets.

Kuwait Energy continues its strong record of sound and safe petroleum development. New staff have been recruited adding many years of international experience and significant expertise in all aspects of petroleumdevelopment. The team is strong and will facilitate industry leading development projects into the future.

d. Development Activities

· 6 Development wells in Shukheir North West field, Area A, Egypt· Total 39 development wells drilled in 2009

Energy in the Middle East

e. Reserves

Kuwait Energy Reserves and Resources SummaryAs at 31 December 2009

2P RRR = 340%

Classification

Reserves

Contingent &ProspectiveResources

Kuwait Energy Working Interest Reserves and Resources mboe

Category

2P

Mid Case

YE08

43,445

921,146

ExplorationAdds

2,394

.............

Acq/Divest &

Revisions

8,592

800,854

YE09(GCA/NSAI)

51,197

1,722,000

Production

3,235

.............

Notes 1. Estimates above are Kuwait Energy Working Interest and are unrisked.2. Estimates above exclude Karim Small Fields (Oman) which is covered by a Service Agreement which does not allow external reporting of reserve volumes.3. YE09 reserves were audited by Gaffney Cline & Associates (GCA) with the exception of Russia which was audited by Netherland Sewell & Associates (NSAI).

Reserves and Resources DefinitionReserves and resources have been estimated in accordance with the 2007 Society of Petroleum Engineers (SPE), World Petroleum Council (WPC), American Association of Petroleum Geologists (AAPG), Society of Petroleum Evaluation Engineers (SPEE), Petroleum Resources Management System (PRMS) – commonly referred to as the SPE PRMS.

Proven plus Probable Reserves (Kuwait Energy Working Interest)

Reserves year-end 2008

Production

Exploration Discoveries

Acquisition/Divestments & Revisions

Reserves year-end 2009

85,350

1,894

0

-25,545

57,912

Sales Gas(mmcf)

25,041

2,892

2,394

14,070

38,614

Crude Oil

(mbbl)

4,470

28

0

-1,307

3,135

Condensate

(mbbl)

43,445

3,235

2,394

8,592

51,197

Total

(mboe)

20

Exploration Drilling

Ten exploration wells were drilled in 2009 resulting in four discoveries, one appraisal success, four dry holes and one well in Block 43, Yemen is currently under evaluation. This yielded a 50% success rate and a three year average finding cost of US$6.84/boe for proved and probable reserves for Kuwait Energy. Exploration success in 2009 resulted in the addition of 2.4 million barrels of oil equivalent of proved and probable reserves and approximately 5,400 barrels of oil per day of additional production.

Kuwait Energy as an operator drilled three wells in 2009 based on high quality technical work in two concessions in Egypt, Area A and Burg El Arab (BEA) resulting in two discoveries, Shukheir NW in Area A and BEA North. The Shukheir NW well was Kuwait Energy’s first fully operated exploration well and was subsequently followed up with seven development wells and one sidetrack well. The three non-operated exploration discoveries were all in East Ras Qattara (Al Zahraa1and Diaa).

Geophysical and Geological Studies

During 2009, Kuwait Energy participated in acquiring, processing, reprocessing and the reinterpretation

of approximately 1,300 kilometres of seismic data in Yemen, Pakistan, Latvia and Ukraine. These efforts resulted in the identification of a number of prospects and leads.

Kuwait Energy entered into an agreement with Fugro Robertson Limited (FRL), United Kingdom to provide specialized geological and geophysical support related to the exploration function. During 2009, FRL became Kuwait Energy’s primary consultant to prepare geological studies and provide a detailed update for the Contingent and Prospective resource assessment in Kuwait Energy’s exploration portfolio. Kuwait Energy exploration staff worked as

f. Exploration Activities

• Five of the ten 2009 exploration wells were successful (50% success rate)• Four exploration discoveries; two of the discoveries were on Kuwait Energy operated blocks• Three year average finding cost of US$6.84/boe for proved and probable reserves• Technically defined 1.7 billion boe un-risked resource potential

part of the integrated team with FRL and closely managed the work for technical excellence. This study resulted in Kuwait Energy identifying and technically documenting 1.7 billion barrels of oil equivalent of un-risked resources and confirming the Company’s significant upside related to exploration potential.

New Exploration Asset

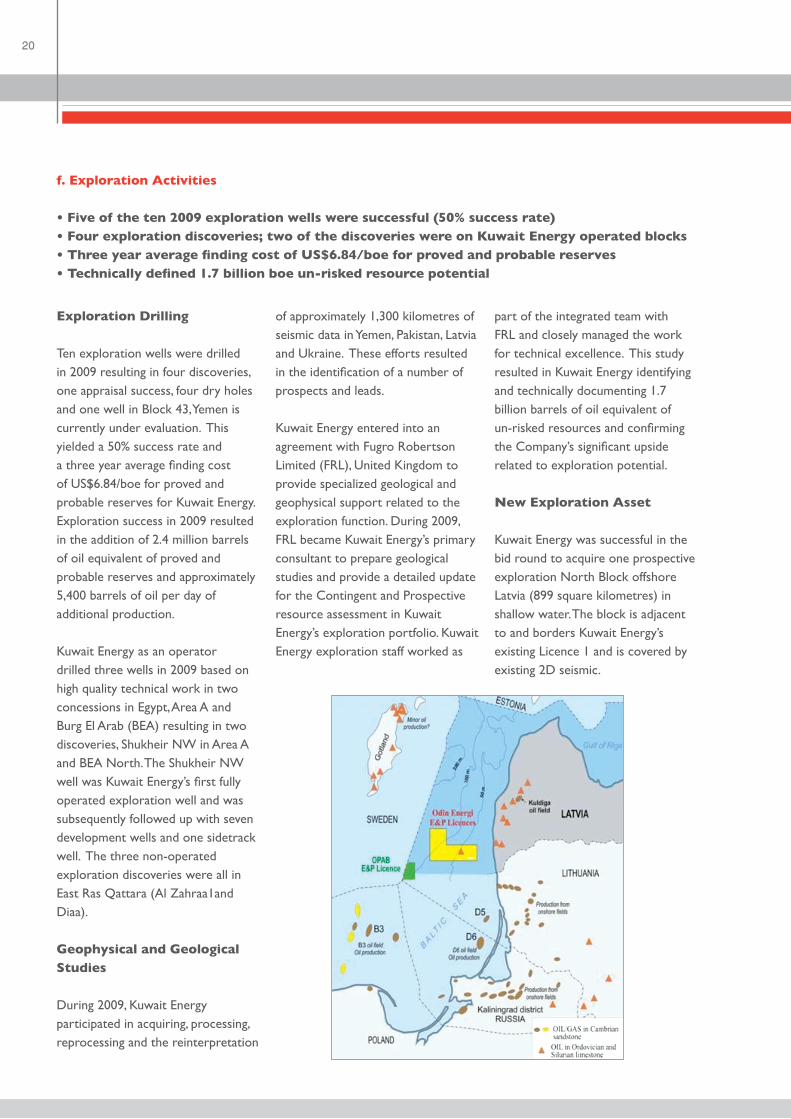

Kuwait Energy was successful in the bid round to acquire one prospective exploration North Block offshore Latvia (899 square kilometres) in shallow water. The block is adjacent to and borders Kuwait Energy’s existing Licence 1 and is covered by existing 2D seismic.

Energy in the Middle East

g. Business Development

Business development is a key focus for Kuwait Energy as it strives to meet its inception targets of 50,000 barrels of oil equivalent per day production and300 million barrels of oil equivalent reserves by the end of 2010. In addition to its Acquisition Department, a Projects Department was established in the fourth quarter of 2009 in order to develop business opportunities in the Gulf Region and surrounding countries, and to maintain the focus of Kuwait Energy on the Middle East region.

Kuwait Energy is positioning itself to capture future opportunities in Yemen, Iraq and Kuwait. Currently, Kuwait Energy has an office in Sana’a which overseesthe operations of our seven blocks in Yemen, where we are one of the largest holders of exploration acreage and enjoy good working relationships with the

Government and the Ministry. The Yemen gas sector has existing potential opportunities to supply power plants, industry and the domestic market which Kuwait Energy is investigating.

In September 2007, Kuwait Energy signed a Memorandum of Cooperation with the Ministry of Oil, Iraq and obtained available data and information on the Siba gas field inorder to propose a field development plan.A Siba fieldworkshop was held in early 2009 and was attended by representatives from the Ministry of Oil, Iraq and the South Oil Company, Iraq. Kuwait Energy continues to pursue opportunities in Iraq.

Kuwait Energy tendered a bid for Kuwait Oil Company’s new GC-16 Project in West Kuwait in mid 2009. The bid is being evaluated and the results are awaited.

Production Facilities, Burg El Arab, Egypt

22

h. Other Corporate Activities

Human Resources

Kuwait Energy has had to grow significantly in its staffing function in order to keep up with its rapid expansion in assets and operations. In 2009, over 60 new employees joined the Company.

Kuwait Energy has provided access to its employees to internet based learning tools such as International Petroleum Industry Multimedia System(IPIMS). This system is an award winning, extensive online training system which operates accredited learning courses on all topics involving upstream oil and gas.

Information Technology

During 2009, Kuwait Energy’s Information Technology department aimed to provide services through state-of-the-art tools and systems with an average uptime of 99.73%.

Kuwait Energy is equipped with a company-wide cost effective yet secure network infrastructure that uses a single network topology. Additionally, the Kuwait Energy data centre is modern and robust and allows for an automated and reliable back-up system.

Sara AkbarChief Executive Officer

Legal

Kuwait Energy is a Sharia compliant company and has appointed a Sharia auditor to regulate Kuwait Energy’s compliance with the Sharia Law. All legal documents and contracts are subject to approval by the Sharia auditor for compliance.

Commercial

During 2009, the Commercial department started providing efficient and cost effective tendering and procurement services to all the departments and divisions in the Company. As a result of which Kuwait Energy has implemented procurement, contracting and warehousing best practices in all its offices. The Materials Management System facilitates tracking and record keeping of commitment documents such as purchase orders and effective inventory management.

Open Day 2009, Failaka Island, Kuwait

Staff at Kuwait Head Office receiving seasonal flu vaccine

Energy in the Middle EastEnergy in the Middle East

Mud System on Rig EDC – 63, Area A, Egypt

Workover Operations, Area A, Egypt

Energy in the Middle East

Kuwait Energy’s Board and management recognise the importance of adhering to the best international practices and standards of corporate governance.

This report illustrates the main aspects of the Company’s Corporate Governance.

a. Internal Management Controls

Delegation of Authority Document: The Delegation of Authority provides the structure within which all aspects of Kuwait Energy’s business is conducted. It is mandatory and sets out the key policies and procedures that are to be adhered to across all of Kuwait Energy’s operations. It is essential for the Company’s managers to understand the principles and procedures outlined in the Delegation of Authority document.

b. Corporate Governance Review by IFC

The IFC is a member of the World Bank and is widely perceived to be a leader amongst multilateral financialinstitutions in the area of corporate governance in emerging markets.

Kuwait Energy engaged the IFC to conduct a corporate governance review in 2009 to assess Kuwait Energy’s current corporate governance framework and to provide recommendations for improvement.

The IFC Team conducted interviews with numerous individuals, including Board members and various executives. In addition, the IFC Team collected and analysed key company documents.

The IFC provided recommendations to improve Board performance and internal management control which Kuwait Energy is currently implementing.

c. Board Performance

Kuwait Energy’s Board of Directors comprises seven members.

The Chairman of the Board also performs an executive role as the Managing Director of the Company. The CEO and the other five (non-executive) Directors allrepresent (or represented at the time of appointment) significantshareholders.

There is a clear distinction in the roles of the Chairman and the CEO. The Chairman devotes approximately 40% of his time to engaging with shareholders; 30% to managing all other types of relationships, including the governance process; and 30% on the operations of the Company.

The Board functions in a spirit of teamwork and cooperative support. Every Board member is required:

• to attend scheduled board meetings of the Company’s Board of Directors; • to represent the shareholders and

the interests of the Company as a fiduciary in accordance with the Kuwait General Company Law; and • to participate as a full voting member of the Company’s Board of Directors in setting overall objectives, approving plans and programs of operations, formulating general policies, offering advice and counsel, serving on board committees and reviewing management performance.

The Chairman has the overall responsibility of communicating with Shareholders and keeping the board appraised in this regard. Additionally, the Company issues quarterly activity reports to its shareholders for periodic updates on the operations and activities of the Company.

Corporate Governance Report

26

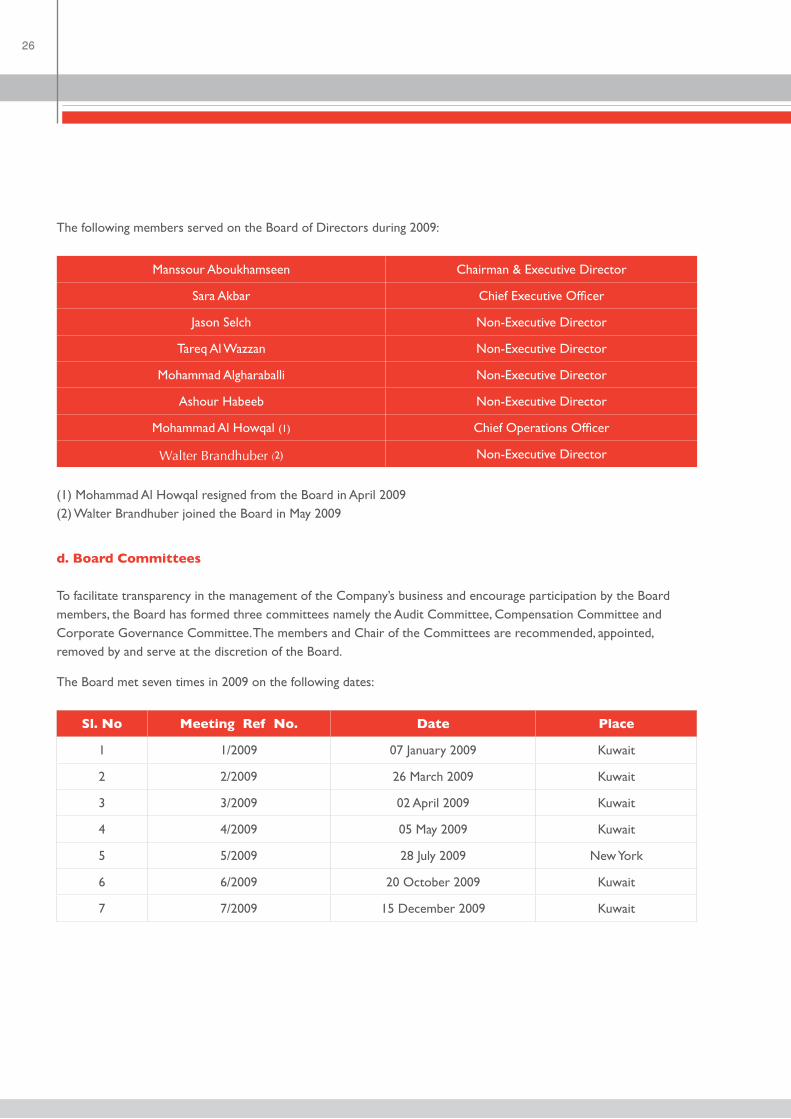

The following members served on the Board of Directors during 2009:

Manssour Aboukhamseen Chairman & Executive Director

Sara Akbar Chief Executive Officer

Jason Selch Non-Executive Director

Tareq Al Wazzan Non-Executive Director

Mohammad Algharaballi Non-Executive Director

Ashour Habeeb Non-Executive Director

Mohammad Al Howqal (1) Chief Operations Officer

Walter Brandhuber (2) Non-Executive Director

(1) Mohammad Al Howqal resigned from the Board in April 2009(2) Walter Brandhuber joined the Board in May 2009

d. Board Committees

To facilitate transparency in the management of the Company’s business and encourage participation by the Board members, the Board has formed three committees namely the Audit Committee, Compensation Committee and Corporate Governance Committee. The members and Chair of the Committees are recommended, appointed, removed by and serve at the discretion of the Board.

The Board met seven times in 2009 on the following dates:

Sl. No Meeting Ref No. Date Place

1 1/2009 07 January 2009 Kuwait

2 2/2009 26 March 2009 Kuwait

3 3/2009 02 April 2009 Kuwait

4 4/2009 05 May 2009 Kuwait

5 5/2009 28 July 2009 New York

6 6/2009 20 October 2009 Kuwait

7 7/2009 15 December 2009 Kuwait

Energy in the Middle East

Register of attendance of Board members and Committee members from 01 January 2009 to 31 December 2009:

Board(7 Meetings)

Audit Committee(5 Meetings)

Compensation Committee(3 Meetings)

Manssour Aboukhamseen 7/7 - -

Sara Akbar 7/7 - -

Jason Selch 7/7 5/5 3/3

Tareq Al Wazzan 3/7 3/5 -

Mohammad Algharaballi 6/7 - 3/3

Ashour Habeeb 7/7 5/5 3/3

Mohammad Al Howqal 2/3 - -

Walter Brandhuber 4/4 - -

The average Board members attendance at the Board meetings was 88%.

The Committees are made up of three members each, constituting of only the non-executive Directors on the Board.

Audit Committee Compensation CommitteeCorporate Governance

Committee

Chairman Chairman Chairman

Jason Selch Mohammad Algharaballi Walter Brandhuber

Members Members Members

Tareq Al Wazzan Jason Selch Tareq Al Wazzan

Ashour Habeeb Ashour Habeeb Ashour Habeeb

28

Audit Committee

The Board of Directors has established an Audit Committee, which is responsible for assisting the Board of Directors in fulfilling itsfiduciary responsibilities to provideoversight with respect to:

(a) the integrity of the Company's financial statements and otherfinancial information provided tostockholders and others;(b) the Company's system of internal controls;(c) the engagement and performance of the independent auditors;(d) the performance of the internal audit function; and(e) compliance with legal requirements and Company policies regarding ethical conduct.

In so doing, the Committee provides a focal point for free and open communications amongst the non-executive directors, the Company's management, the internal auditors and the independent auditors.

The Executive Directors do not attend the Audit Committee meetings.

The Audit Committee met five timesduring 2009. Some of the key items considered at these meetings were:

1. Review of 2009 Interim Accounts 2. Audit Plan for 2009 Accounts3. Mid-Year 2009 External Reserves Audit & Year-End 2009 Preliminary Reserves Forecast4. Proposed 2009 Reserves Process5. Economic Assumptions

6. Revisions to the Audit Committee Charter

In addition to the above the Board Audit Committee has been delegated with an internal control function, as follows:

a) Reviewing with the management and the independent auditors the adequacy of the Company's internal controls, including computerized information system controls and security. b) Reviewing with management the scope and results of management's evaluation of disclosure controls and assessment of internal controls over financial reporting, including therelated certifications to be includedin the Company's periodic reports. c) Reviewing with the independent auditors the scope and results of their review of management's assessment of internal controls over financial reporting.d) Review the Company’s overall Sharia compliance.e) Review and approve the Company’s financing/investmentproposals, as and when required.

Corporate Governance Committee

The Corporate Governance Committee was recently established to oversee and monitor matters of corporate governance. Some of the key responsibilities of the Corporate Governance Committee include: 1) Allocation of responsibilities among the Board and its various committees and the management;2) Review annually and make recommendations to the Board regarding Board & management performance, practices and procedures, and the Board’s meeting schedule in light of the operating requirements of the Company and existing social attitudes;3) Review the content of Board meetings and the adequacy of material provided to Directors and make recommendations to the Board related thereto;4) Formulate, recommend to the Board and oversee the implementation and administration of the Company's corporate governance structure and framework;5) Review annually and make recommendations for additional corporate governance matters as necessary or appropriate or as directed by the Company's Chairman or the Board;6) Review periodically, and approve changes to the Company's code of conduct and other policies with respect to legal compliance, conflictsof interest and ethical conduct;

Energy in the Middle East

7) Oversee the development and implementation of policies and management systems relating to environmental, social and governance issues in order to ensure compliance with applicable laws and best practices and monitor the Company’s performance against sustainability objectives set under those policies and systems.

8) Review annually and assess the adequacy of this Charter and the performance of the Committee, and recommending to the Board for approval any proposed changes to this Charter or the Committee.

In addition to the above responsibilities, the Committee will undertake such other duties as the Board delegates to it, and will report periodically to the Board regarding the Committee's examinations and recommendations.

3. Acting as administrator of the Company's compensation plans, including granting awards to executive officers and directors, reviewing aggregate awards for other eligible individuals and determining the terms and conditions of such awards. The Committee shall also make recommendations to the Board of Directors with respect to amendments to the plans and changes in the number of shares reserved for issuance under such plan;

4. Evaluating the performance of the Chairman and the Chief Executive Officer (and such other executive officers as the Committee deems appropriate) in light of the Company's current business environment and the Company's strategic objectives;

5. Reviewing with Company management and approving recommendations with regard to aggregate salary budget and guidelines for all Company employees;

6. Evaluating the need for, and provisions of, employment contracts or severance arrangements for the executive officers.

The Compensation Committee met three times during 2009. Some of the key items considered at these meetings were:

1. Performance Appraisal of Chairman, CEO and Vice Presidents ;2. Revisions to the Human Resources policy;3. Revisions to the Compensation Committee Charter.

The Executive Directors do not attend the Compensation Committee meetings.

Dr. Manssour AboukhamseenChairman & Managing Director

Compensation Committee

The Board of Directors has established a Compensation Committee to review and approve, on behalf of the Board of Directors, management recommendations regarding all forms of compensation to be provided to the executive officers and directors of the Company and bonus and stock compensation guidelines to all employees.

Some of the key responsibilities of the Compensation Committee include:

1. Reviewing with Company management and approving the compensation policy for executive officers and directors of the Company, and such other managers of the Company as directed by the Board;

2. Reviewing with Company management and approving all forms of compensation to be provided to the executive officers of the Company;

30

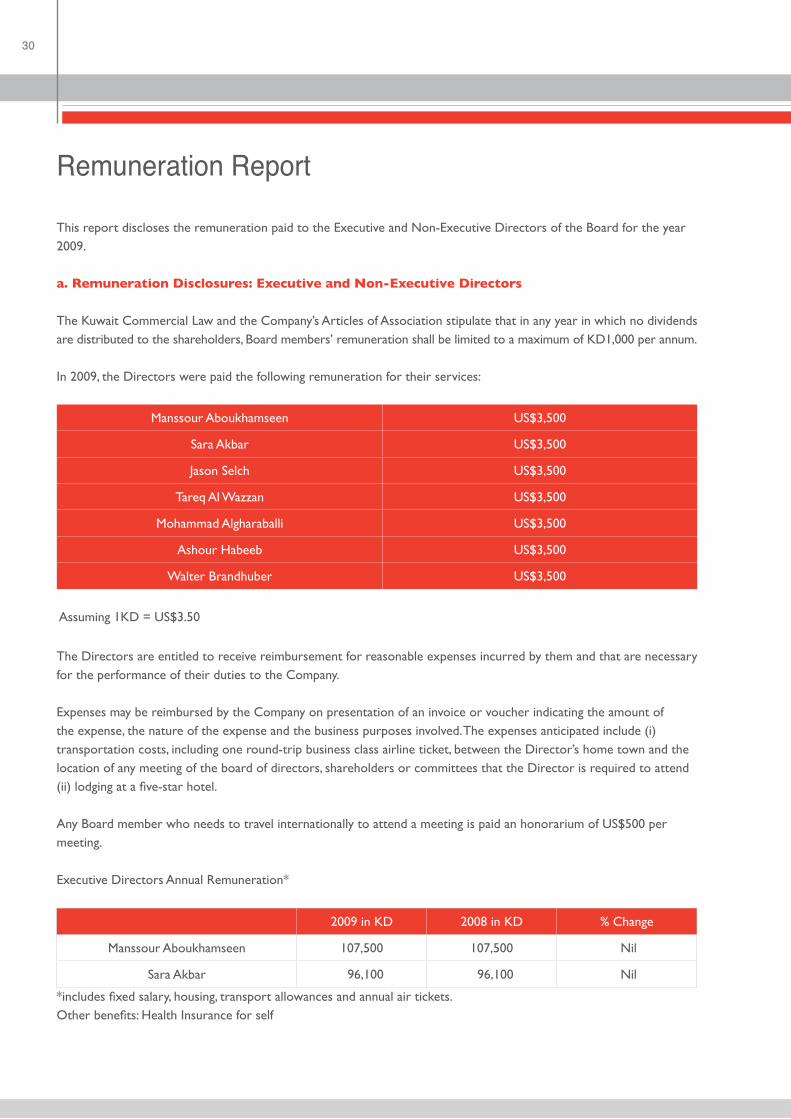

This report discloses the remuneration paid to the Executive and Non-Executive Directors of the Board for the year 2009.

a. Remuneration Disclosures: Executive and Non-Executive Directors

The Kuwait Commercial Law and the Company’s Articles of Association stipulate that in any year in which no dividends are distributed to the shareholders, Board members’ remuneration shall be limited to a maximum of KD1,000 per annum.

In 2009, the Directors were paid the following remuneration for their services:

Manssour Aboukhamseen US$3,500

Sara Akbar US$3,500

Jason Selch US$3,500

Tareq Al Wazzan US$3,500

Mohammad Algharaballi US$3,500

Ashour Habeeb US$3,500

Walter Brandhuber US$3,500

Assuming 1KD = US$3.50

The Directors are entitled to receive reimbursement for reasonable expenses incurred by them and that are necessary for the performance of their duties to the Company. Expenses may be reimbursed by the Company on presentation of an invoice or voucher indicating the amount of the expense, the nature of the expense and the business purposes involved. The expenses anticipated include (i) transportation costs, including one round-trip business class airline ticket, between the Director’s home town and the location of any meeting of the board of directors, shareholders or committees that the Director is required to attend (ii) lodging at a five-star hotel. Any Board member who needs to travel internationally to attend a meeting is paid an honorarium of US$500 per meeting.

Executive Directors Annual Remuneration*

2009 in KD 2008 in KD % Change

Manssour Aboukhamseen 107,500 107,500 Nil

Sara Akbar 96,100 96,100 Nil

*includes fixed salary, housing, transport allowances and annual air tickets.Other benefits: Health Insurance for self

Remuneration Report

Energy in the Middle East

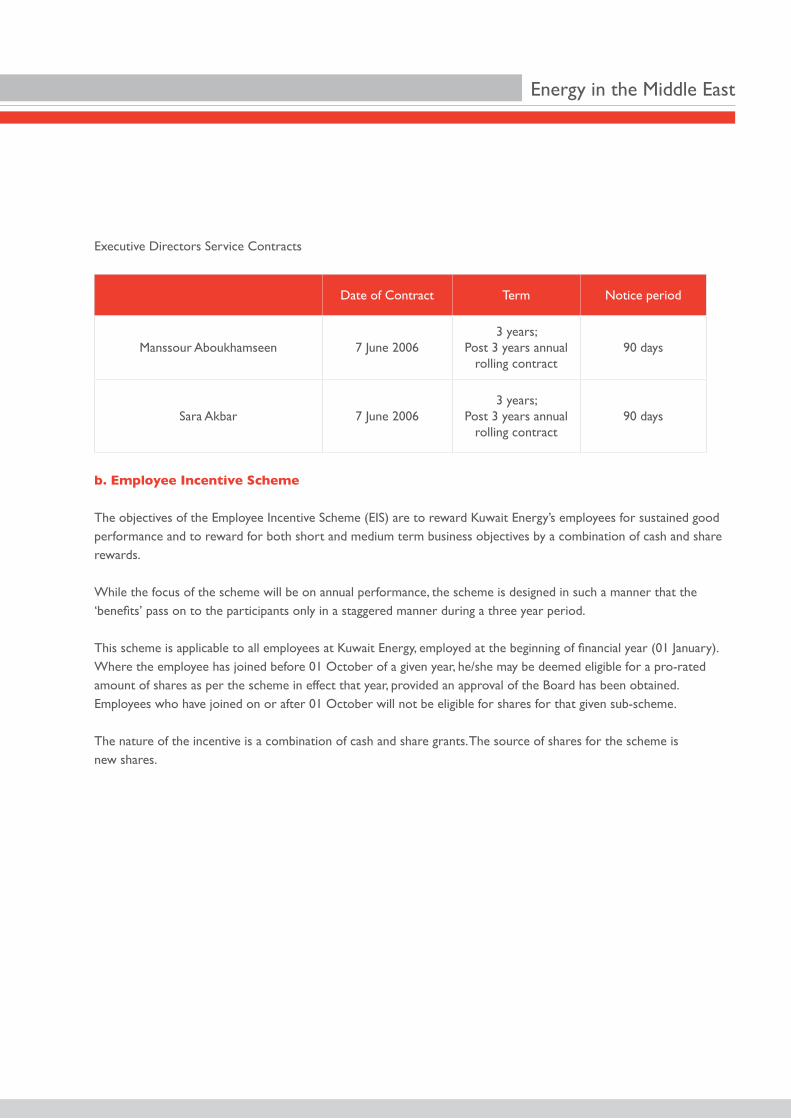

Executive Directors Service Contracts

Date of Contract Term Notice period

Manssour Aboukhamseen 7 June 20063 years;

Post 3 years annual rolling contract

90 days

Sara Akbar 7 June 20063 years;

Post 3 years annual rolling contract

90 days

b. Employee Incentive Scheme

The objectives of the Employee Incentive Scheme (EIS) are to reward Kuwait Energy’s employees for sustained good performance and to reward for both short and medium term business objectives by a combination of cash and share rewards.

While the focus of the scheme will be on annual performance, the scheme is designed in such a manner that the ‘benefits’ pass on to the participants only in a staggered manner during a three year period. This scheme is applicable to all employees at Kuwait Energy, employed at the beginning of financial year (01 January).Where the employee has joined before 01 October of a given year, he/she may be deemed eligible for a pro-rated amount of shares as per the scheme in effect that year, provided an approval of the Board has been obtained. Employees who have joined on or after 01 October will not be eligible for shares for that given sub-scheme.

The nature of the incentive is a combination of cash and share grants. The source of shares for the scheme is new shares.

32

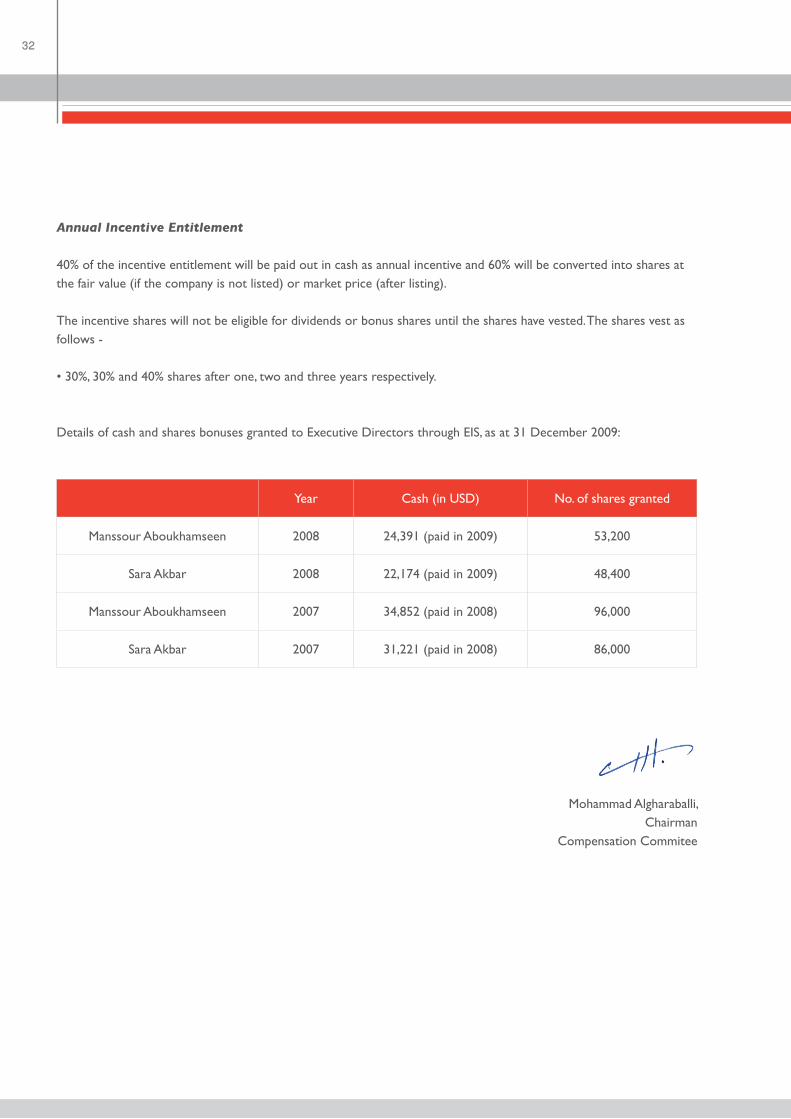

Annual Incentive Entitlement

40% of the incentive entitlement will be paid out in cash as annual incentive and 60% will be converted into shares at the fair value (if the company is not listed) or market price (after listing).

The incentive shares will not be eligible for dividends or bonus shares until the shares have vested. The shares vest as follows -

• 30%, 30% and 40% shares after one, two and three years respectively.

Details of cash and shares bonuses granted to Executive Directors through EIS, as at 31 December 2009:

Year Cash (in USD) No. of shares granted

Manssour Aboukhamseen 2008 24,391 (paid in 2009) 53,200

Sara Akbar 2008 22,174 (paid in 2009) 48,400

Manssour Aboukhamseen 2007 34,852 (paid in 2008) 96,000

Sara Akbar 2007 31,221 (paid in 2008) 86,000

Mohammad Algharaballi, Chairman

Compensation Commitee

Energy in the Middle East

Kuwait Energy Five Year Summary

As at 31 December Units 2005 2006 2007 2008 2009

Financial perfomance

Sales revenue US$ million - 2.4 25.9 90.8 88.3

Cost of sales US$ million - 1.7 10.1 71.0 70.8

EBITDA US$ million - 1.4 24.4 53.5 50.4

Net profit US$ million - 1.0 20.6 29.9 5.6

Cash flow from operating activities US$ million - 0.2 8.7 7.4 33.5

Financial position

Total assets US$ million 3.5 87.2 239.6 577.7 680.9

Net debt (Non Collateralised) US$ million - - - - 28.0

Total equity US$ million 3.5 84.9 193.7 525.7 580.1

Reserves and production

Proven plus Probable reserves mmboe - 10.7 34.1 43.4 51.2

Production mmboe - 0.2 1.2 3 4

Development Wells # - - 26 44 39

Workovers # - - 30 46 44

Exploration Wells # - - - 4 10

Exploration Expenditure US$ million - - 4.8 13.8 31.0

Kuwait Energy was established in August 2005, signing its first contract in March 2006, a Service Contract for the Karimfields in Oman.

Consolidated financialstatements and independent auditors’ report for the year ended 31 December 2009

INDEX

Independent auditors’ report 35-36 Consolidated statement of income for the year ended 31 December 2009 37

Consolidated statement of comprehensive income for the year ended 31 December 2009 38

Consolidated statement of financial position as at 31 December 2009 39

Consolidated statement of changes in equity for the year ended 31 December 2009 40-41

Consolidated statement of cash flows for the year ended 31 December 2009 42

Notes to the consolidated financial statements 43-74

MOORE STEPHENSPUBLIC ACCOUNTANTS

AL NISF & PARTNERS

Al Jawhara Tower, 6th floorKhaled Ben Al-Waleed Street, SharqP.O.Box: 25578, Safat 13116, Kuwait

Tel: 965 2426 999Fax: 965 2401 666

INDEPENDENT AUDITORS’ REPORT

The ShareholdersKuwait Energy Company K.S.C. (Closed)Kuwait

Report on the consolidated financial statements

We have audited the accompanying consolidated financial statements of Kuwait Energy Company K.S.C. (Closed), (“the Parent Company”) and subsidiaries (together referred to as “the Group”), which comprise the consolidated statement of financial position as at 31 December 2009, and the related consolidated statements of income, comprehensive income, changes in equity and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes.

Management’s responsibility for the consolidated financial statements

Management of the Parent Company is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the group preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the group internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Al-Fahad & Co. Salhia ComplexGate 2, 4th FloorP.O. Box 23049Safat 13091State of Kuwait

Tel: + (965) 22438060Tel: + (965) 22468934Fax: + (965) 22452080www.deloitte.com

P. O. Box 25578, Safat 13116, KuwaitAl Jawhara Tower, 6th FloorKhaled Ben Al-Waleed Street, Sharq, Kuwait

Tel +965 2426 999Fax +965 2401 666

KUWAIT ENERGY COMPANY K.S.C (CLOSED) AND SUBSIDIARIES36

Opinion

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, thefinancial position of the Group as at 31 December 2009, and of its financial performance and its cash flows forthe year then ended in accordance with International Financial Reporting Standards.

Report on Other Legal and Regulatory Requirements

Furthermore, in our opinion proper books of account have been kept by the Parent Company and the consolidated financial statements, together with the contents of the report of the board of directors relating to these consolidatedfinancial statements, are in accordance therewith. We further report that we obtained all the information andexplanations that we required for the purpose of our audit and that the consolidated financial statementsincorporate all information that is required by the Commercial Companies Law of 1960, as amended, and by the Parent Company’s articles of association, that an inventory was duly carried out and that, to the best of our knowledge and belief, no violations of the Commercial Companies Law of 1960, as amended, nor of the articles of association have occurred during the year ended 31 December 2009 that might have had a material effect on the business of the Group or on its financial position.

Jassim Ahmad Al-Fahad Licence No. 53-A Al-Fahad & Co. Deloitte & Touche

Qais M. Al-Nisf License No. 38-A Moore Stephens Al Nisf & Partners Member of Moore Stephens International

23 March 2010

2009 2008

Notes USD 000’s USD 000’s

Revenue 5 88,312 90,796

Cost of sales 7 (70,761) (71,015)

Gross profit 17,551 19,781

Exploration expenditure written off 13 (4,602) -

Net impairment losses 14 (1,084) (10,634)

Impairment loss on non-current asset held for sale - (4,709)

General and administrative expenses 8 (20,226) (11,983)

Operating loss (8,361) (7,545)

Negative goodwill on acquisition of subsidiaries - 33,535

Other income 9 10,801 8,439

Foreign exchange loss (485) (1,597)

Finance costs 10 (691) (2,352)

Profit before tax, provisions for contribution to Kuwait Foundation for the Advancement of Sciences (“KFAS”), Zakat and Directors’ fees

1,264

30,480

Taxation relating to subsidiaries 16 4,425 -

Provision for contribution to KFAS (51) (274)

Provision for Zakat (58) (305)

Directors’ fees (27) (18)

Profit for the year 11 5,553 29,883

Earnings per share

- Basic (cents) 12 0.54 4.02

- Diluted (cents) 12 0.52 4.02

The accompanying notes set out on pages 43 to 74 form an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENT OF INCOMEFor the year ended 31 December 2009

KUWAIT ENERGY COMPANY K.S.C (CLOSED) AND SUBSIDIARIES38

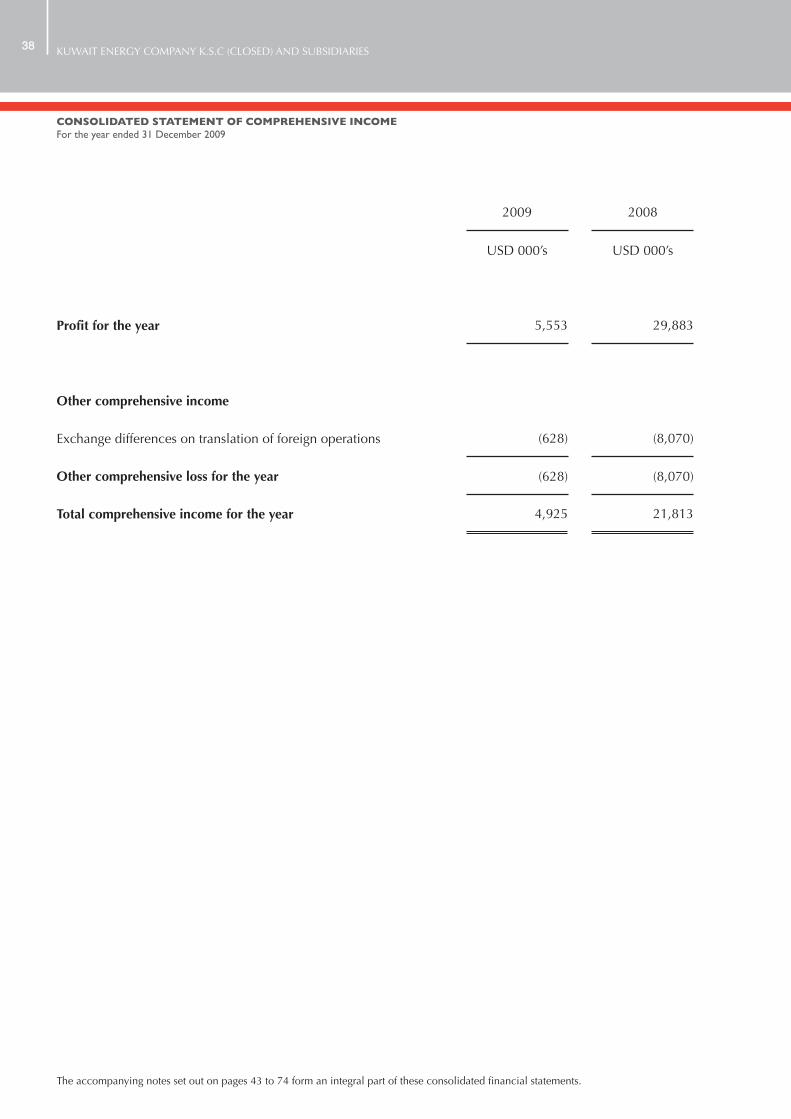

2009 2008

USD 000’s USD 000’s

Profit for the year 5,553 29,883

Other comprehensive income

Exchange differences on translation of foreign operations (628) (8,070)

Other comprehensive loss for the year (628) (8,070)

Total comprehensive income for the year 4,925 21,813

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEFor the year ended 31 December 2009

The accompanying notes set out on pages 43 to 74 form an integral part of these consolidated financial statements.

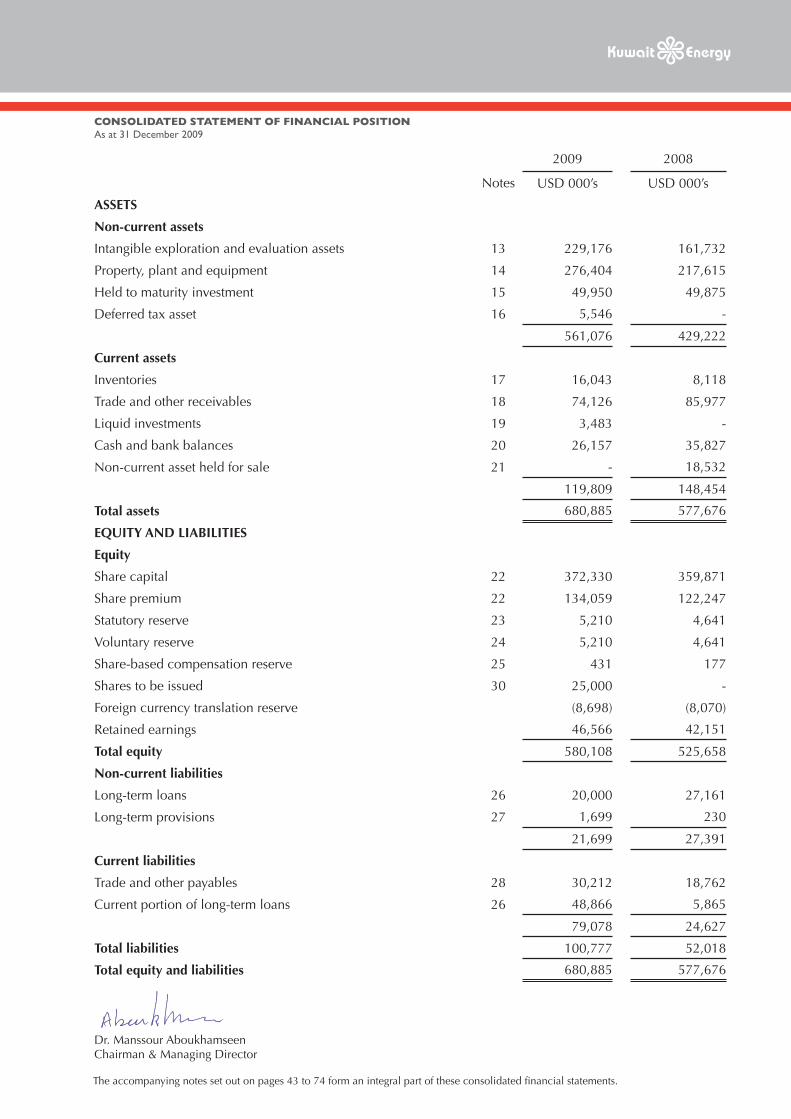

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONAs at 31 December 2009

2009 2008

Notes USD 000’s USD 000’s

ASSETS

Non-current assets

Intangible exploration and evaluation assets 13 229,176 161,732

Property, plant and equipment 14 276,404 217,615

Held to maturity investment 15 49,950 49,875

Deferred tax asset 16 5,546 -

561,076 429,222

Current assets

Inventories 17 16,043 8,118

Trade and other receivables 18 74,126 85,977

Liquid investments 19 3,483 -

Cash and bank balances 20 26,157 35,827

Non-current asset held for sale 21 - 18,532

119,809 148,454

Total assets 680,885 577,676

EQUITY AND LIABILITIES

Equity

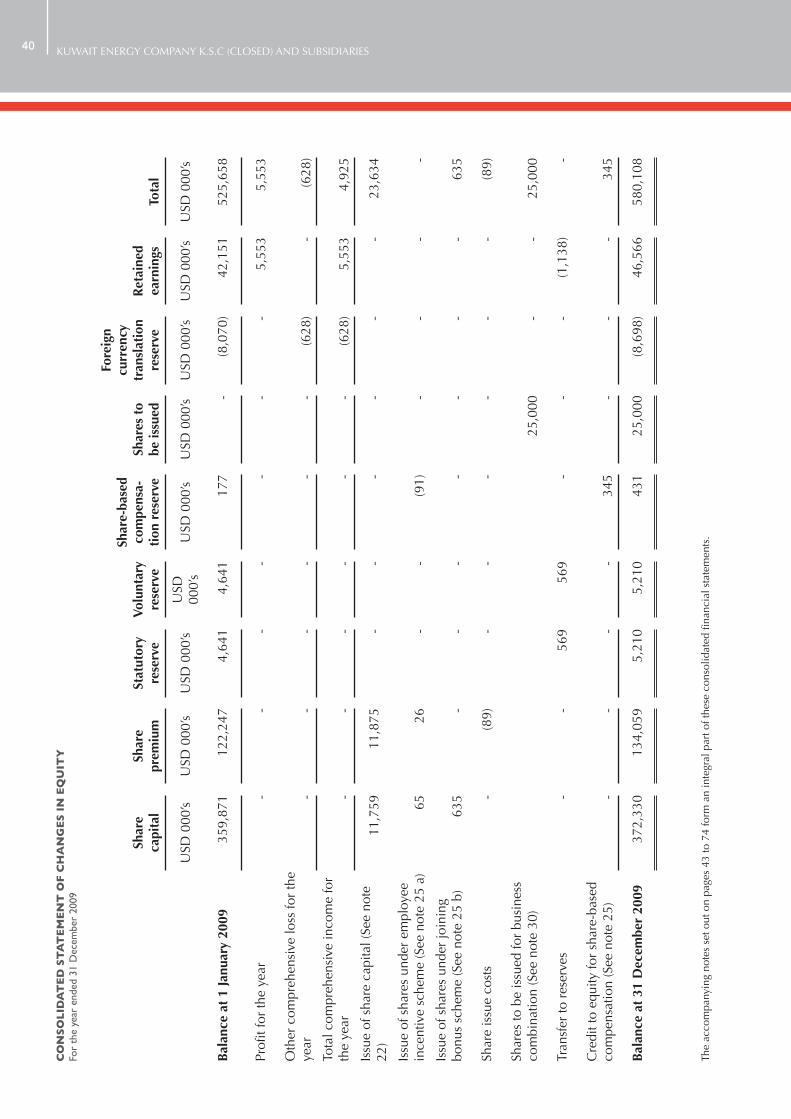

Share capital 22 372,330 359,871

Share premium 22 134,059 122,247

Statutory reserve 23 5,210 4,641

Voluntary reserve 24 5,210 4,641

Share-based compensation reserve 25 431 177

Shares to be issued 30 25,000 -

Foreign currency translation reserve (8,698) (8,070)

Retained earnings 46,566 42,151

Total equity 580,108 525,658

Non-current liabilities

Long-term loans 26 20,000 27,161

Long-term provisions 27 1,699 230

21,699 27,391

Current liabilities

Trade and other payables 28 30,212 18,762

Current portion of long-term loans 26 48,866 5,865

79,078 24,627

Total liabilities 100,777 52,018

Total equity and liabilities 680,885 577,676

The accompanying notes set out on pages 43 to 74 form an integral part of these consolidated financial statements.

Dr. Manssour AboukhamseenChairman & Managing Director

KUWAIT ENERGY COMPANY K.S.C (CLOSED) AND SUBSIDIARIES40

Sh

are

capi

tal

Sh

are

prem

ium

St

atut

ory

rese

rve

Vo

lunt

ary

rese

rve

Sh

are-

base

d co

mpe

nsa-

tion

res

erve

Sh

ares

to

be is

sued

Fore

ign

curr

ency

tr

ansl

atio

n re

serv

e

R

etai

ned

earn

ings

To

tal

USD

000

’sU

SD 0

00’s

USD

000

’sU

SD

000’

sU

SD 0

00’s

USD

000

’sU

SD 0

00’s

USD

000

’sU

SD 0

00’s

Bal

ance

at

1 Ja

nuar

y 20

0935

9,87

112

2,24

74,

641

4,64

117

7-

(8,0

70)

42,1

5152

5,65

8

Prof

it fo

r th

e ye

ar-

--

--

--

5,55

35,

553

Oth

er c

ompr

ehen

sive

loss

for

the

year

- -

- -

- -

(6

28)

-

(628

)

Tota

l com

preh

ensi

ve in

com

e fo

r th

e ye

ar -

- -

- -

-

(628

)

5,55

3

4,92

5

Issu

e of

sha

re c

apita

l (Se

e no

te

22)

11,7

5911

,875

--

--

--

23,6

34

Issu

e of

sha

res

unde

r em

ploy

ee

ince

ntiv

e sc

hem

e (S

ee n

ote

25 a

)

65

26 -

-

(91)

- -

- -

Issu

e of

sha

res

unde

r jo

inin

g

bonu

s sc

hem

e (S

ee n

ote

25 b

)

635

- -

- -

- -

-

635

Shar

e is

sue

cost

s-

(89)

--

--

--

(89)

Shar

es to

be

issu

ed fo

r bu

sine

ss

com

bina

tion

(See

not

e 30

)

25

,000

- -

25

,000

Tran

sfer

to r

eser

ves

--

569

569

--

-(1

,138

)-

Cre

dit t

o eq

uity

for

shar

e-ba

sed

com

pens

atio

n (S

ee n

ote

25)

- -

- -

34

5 -

- -

34

5

Bal

ance

at

31 D

ecem

ber

2009

37

2,33

013

4,05

95,

210

5,21

043

125

,000

(8,6

98)

46,5

6658

0,10

8

The

acco

mpa

nyin

g no

tes

set o

ut o

n pa

ges

43 to

74

form

an

inte

gral

par

t of t

hese

con

solid

ated

fina

ncia

lsta

tem

ents

.

CO

NS

OL

IDA

TE

D S

TA

TE

ME

NT

OF

CH

AN

GE

S I

N E

QU

ITY

For

the

year

end

ed 3

1 D

ecem

ber

2009

Sh

are

capi

tal

Sh

are

prem

ium

St

atut

ory

rese

rve

Vo

lunt

ary

rese

rve

Sh

are-

base

d co

mpe

nsat

ion

rese

rve

Fore

ign

curr

ency

tr

ansl

atio

n re

serv

e

R

etai

ned

earn

ings

To

tal

USD

000

’sU

SD 0

00’s

USD

000

’sU

SD 0

00’s

USD

000

’sU

SD 0

00’s

USD

000

’sU

SD 0

00’s

Bal

ance

at

1 Ja

nuar

y 20

0817

2,13

9-

1,59

31,

593

--

18,3

6419

3,68

9

Prof

it fo

r th

e ye

ar-

--

--

-29

,883

29,8

83

Oth

er c

ompr

ehen

sive

lo

ss fo

r th

e ye

ar -

- -

- -

(8

,070

) -

(8

,070

)

Tota

l com

preh

ensi

ve in

com

e fo

r th

e ye

ar -

- -

- -

(8

,070

)

29,8

83

21,8

13

Issu

e of

sha

re c

apita

l18

7,73

212

3,17

4-

--

--

310,

906

Shar

e is

sue

cost

s-

(927

)-

--

--

(927

)

Tran

sfer

to r

eser

ves

--

3,04

83,

048

-(6

,096

)-

Cre

dit t

o eq

uity

for

shar

e-ba

sed

com

pens

atio

n (S

ee n

ote

25)

- -

- -

17

7 -

-

177

Bal

ance

at

31 D

ecem

ber

2008

35

9,87

112

2,24

74,

641

4,64

117

7(8

,070

)42

,151

525,

658

CO

NS

OL

IDA

TE

D S

TA

TE

ME

NT

OF

CH

AN

GE

S I

N E

QU

ITY

For

the

year

end

ed 3

1 D

ecem

ber

2009

The

acco

mpa

nyin

g no

tes

set o

ut o

n pa

ges

43 to

74

form

an

inte

gral

par

t of t

hese

con

solid

ated

fina

ncia

lsta

tem

ents

.

KUWAIT ENERGY COMPANY K.S.C (CLOSED) AND SUBSIDIARIES42

2009 2008

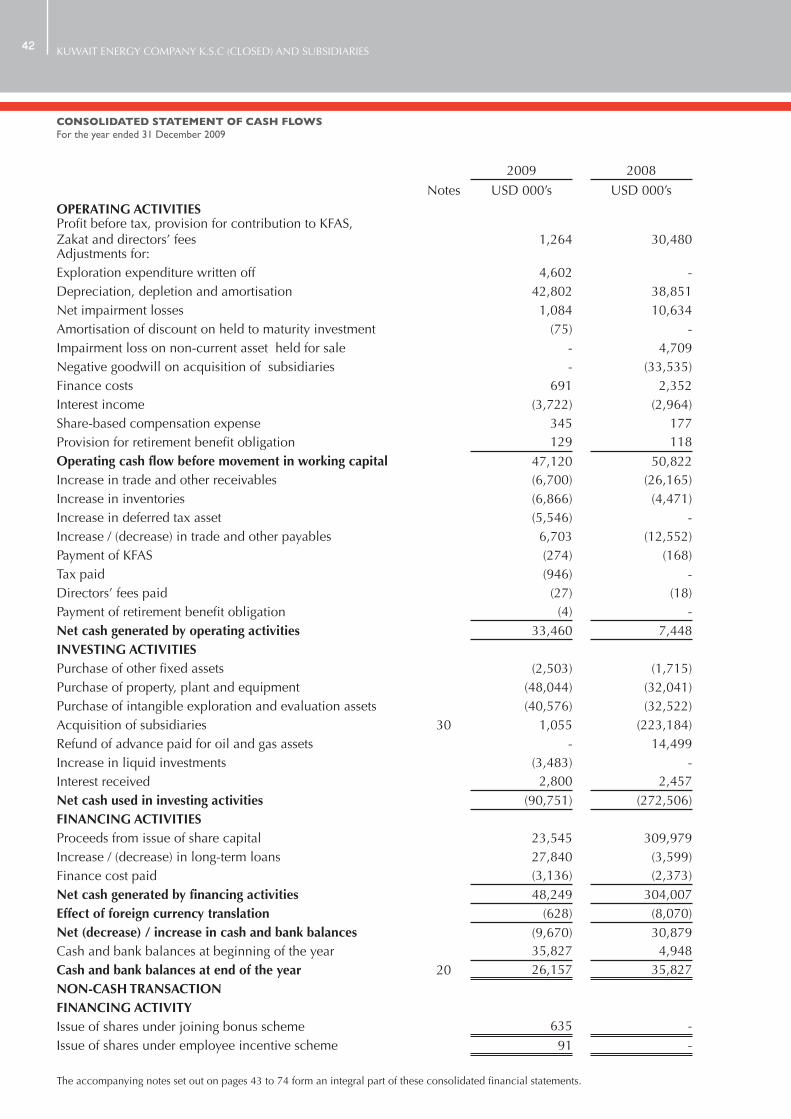

Notes USD 000’s USD 000’sOPERATING ACTIVITIESProfit before tax, provision for contribution to KFAS, Zakat and directors’ fees

1,264

30,480

Adjustments for:Exploration expenditure written off 4,602 -Depreciation, depletion and amortisation 42,802 38,851Net impairment losses 1,084 10,634Amortisation of discount on held to maturity investment (75) -Impairment loss on non-current asset held for sale - 4,709Negative goodwill on acquisition of subsidiaries - (33,535)Finance costs 691 2,352Interest income (3,722) (2,964)Share-based compensation expense 345 177Provision for retirement benefit obligation 129 118Operating cash flow before movement in working capital 47,120 50,822Increase in trade and other receivables (6,700) (26,165)Increase in inventories (6,866) (4,471)Increase in deferred tax asset (5,546) -Increase / (decrease) in trade and other payables 6,703 (12,552)Payment of KFAS (274) (168)Tax paid (946) -Directors’ fees paid (27) (18)Payment of retirement benefit obligation (4) -Net cash generated by operating activities 33,460 7,448INVESTING ACTIVITIESPurchase of other fixed assets (2,503) (1,715)Purchase of property, plant and equipment (48,044) (32,041)Purchase of intangible exploration and evaluation assets (40,576) (32,522)Acquisition of subsidiaries 30 1,055 (223,184)Refund of advance paid for oil and gas assets - 14,499Increase in liquid investments (3,483) -Interest received 2,800 2,457Net cash used in investing activities (90,751) (272,506)FINANCING ACTIVITIESProceeds from issue of share capital 23,545 309,979Increase / (decrease) in long-term loans 27,840 (3,599)Finance cost paid (3,136) (2,373)Net cash generated by financing activities 48,249 304,007Effect of foreign currency translation (628) (8,070)Net (decrease) / increase in cash and bank balances (9,670) 30,879Cash and bank balances at beginning of the year 35,827 4,948Cash and bank balances at end of the year 20 26,157 35,827NON-CASH TRANSACTIONFINANCING ACTIVITYIssue of shares under joining bonus scheme 635 -Issue of shares under employee incentive scheme 91 -

CONSOLIDATED STATEMENT OF CASH FLOWSFor the year ended 31 December 2009

The accompanying notes set out on pages 43 to 74 form an integral part of these consolidated financial statements.

1. INCORPORATION AND ACTIVITIES

Kuwait Energy Company K.S.C. (Closed) (“the Parent Company”) is a Closed Kuwaiti Shareholding Company incorporated on 1 August 2005 in accordance with the Commercial Companies Law in the State of Kuwait.The Parent Company and its subsidiaries (together referred to as “the Group”) have been established with the following objectives: • Conduct feasibility studies of oil and natural gas industries.• Exploration of crude oil and natural gas outside Kuwait after obtaining necessary licences from the Ministry of Energy.• Trade in petroleum and its derivatives through importing and exporting oil and its derivatives to and from Kuwait under the consent of Ministry of Energy and Kuwait Petroleum Corporation. The Group does not currently trade in petroleum or its derivatives.• Participate in the incorporation and ownership of companies involved in the oil and gas industry.• Sell and purchase shares in companies of similar objectives.• Utilize the financial surpluses of the Group by investing them in portfolios by specialised companies and entities.• Own movables and real estate required to conduct its operations within the limits permitted by law.The Parent Company’s address is Salem Al Mubarak Street, Layla Tower, Block 49, Building No. 35, 10th Floor, P.O. Box 5614, Salmiya-22067, Salmiya, Kuwait.

These consolidated financial statements were approved for issue by the Board of Directors of the Parent Company on 23 March 2010 and are subject to the approval of the Annual General Assembly of the shareholders.

2. ADOPTION OF NEW AND REVISED STANDARDS

In the current year, the Group has adopted the following Standards, Interpretations, revisions and amendments to IFRS issued by International Accounting Standards Board which are relevant to and effective for the Group’s consolidated financial statements beginning on or after 1 January 2009.

Standards affecting presentation and disclosureIAS 1 (revised 2007) Presentation of Financial StatementsThe revised Standard has introduced a number of terminology changes (including revised titles for the consolidated financial statements) and has resulted in a number of changes in presentation and disclosure. The revised standard requires all non-owner changes in equity (i.e. comprehensive income) to be presented separately in the consolidated statement of comprehensive income. However, the revised Standard has had no impact on the reported results or financial position of the Group.

IFRS 8 Operating Segments IFRS 8 is a disclosure Standard that has resulted in a redesignation of the Group’s reportable segments (See note 6), but has had no impact on the reported results or financial position of the Group. This new standard which replaced IAS 14 “Segment reporting” requires a management approach for segment reporting under which segment information is presented on the same basis as that used for internal reporting purposes. Reported segment results are now based on internal management reporting information that is regularly reviewed by the chief operating decision maker.

Improving Disclosures about Financial Instruments (Amendments to IFRS 7 Financial Instruments: Disclosures)The amendments to IFRS 7 expand the disclosures required in respect of fair value measurements and liquidity risk. These additional disclosures are disclosed in note 34.

Standards affecting the reported results and financial positionIAS 23 (Revised 2007) Borrowing costs The revised Standard has eliminated the previously available option to expense all borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset when incurred. Instead the Group will now have to capitalise borrowing costs incurred on qualifying assets. The impact of the adoption of the revised Standard, which has been applied on a prospective basis, has been to capitalise USD 2,489 thousand of borrowing costs on qualifying assets.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2009

KUWAIT ENERGY COMPANY K.S.C (CLOSED) AND SUBSIDIARIES44

Standards and Interpretations in issue not yet effectiveAt the date of authorisation of these consolidated financial statements, the following Standards and Interpretations were in issue but not yet effective:

• IAS 1(Revised) Presentation of Financial Statements

Effective for annual periods beginning on or after 1 January 2010

• IAS 7(Revised) Statement of Cash Flows Effective for annual periods beginning on or after 1 January 2010

• IAS 17 (Revised) Leases Effective for annual periods beginning on or after 1 January 2010

• IAS 24 (Revised) Related Party Disclosures Effective for annual periods beginning on or after 1 January 2011

• IAS 27 (Revised) Consolidated and Separate Financial Statements

Effective for annual periods beginning on or after 1 July 2009

• IAS 28 (Revised) Investment in Associates Effective for annual periods beginning on or after 1 July 2009

• IAS 31 (Revised) Interests in Joint Ventures Effective for annual periods beginning on or after 1 July 2009

• IAS 32 (Revised) Financial Instruments Presentation

Effective for annual periods beginning on or after 1 February 2010

• IAS 36 (Revised) Impairment of Assets Effective for annual periods beginning on or after 1 January 2010

• IAS 38 (Revised) Intangible Assets Effective for annual periods beginning on or after 1 July 2009

• IAS 39 (Revised) Financial Instruments: Recognition and Measurement

Effective for annual periods beginning on or after 1 July 2009

• IFRS 1 (Revised) First-time Adoption of International Financial Reporting Standards

Effective for annual periods beginning on or after 1 January 2010

• IFRS 2 (Revised) Share-based Payments Effective for annual periods beginning on or after 1 January 2010

• IFRS 3 (Revised) Business Combinations Effective for annual periods beginning on or after 1 July 2009

• IFRS 5 (Revised) Non-current Assets Held for Sale and Discontinued Operations

Effective for annual periods beginning on or after 1 July 2009

• IFRS 8 Operating Segments Effective for annual periods beginning on or after 1 January 2010

• IFRS 9 Financial Instrument: Classification and Measurement

Effective for annual periods beginning on or after 1 January 2013

• IFRIC 17 Distribution of non cash assets to owners Effective for annual periods beginning on or after 1 July 2009

• IFRIC 18 Transfers of Assets from Customers Effective for annual periods beginning on or after 1 July 2009

• IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments

Effective for annual periods beginning on or after 1 July 2010

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2009

Management anticipate that the adoption of these Standards and Interpretations where applicable and once become effective in future periods will not have a material financial impact on the consolidated financial statements of the Group in the period of initial application, except for treatment of acquisition of subsidiaries and associates when IFRS 3 (revised 2008), IAS 27 (revised 2008) and IAS 28 (revised 2008) come into effect for business combinations for which the acquisition date is on or after the beginning of the first annual period beginning on or after 1 July 2009.

3. SIGNIFICANT ACCOUNTING POLICIES

Statement of complianceThese consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”).

Basis of preparationThese consolidated financial statements have been prepared on the historical cost basis except for the measurement at fair value of share-based payments and certain financial instruments. The accounting policies have been applied consistently by the Group and are consistent with these used in the previous year except for the adoption of new and revised Standards (See note 2) and the adoption of IAS 19 “Employee benefits”. The impact of adoption of IAS 19 on the previous year was not material and no prior year adjustment was made.

These consolidated financial statements are presented in US Dollars (“USD”), which is the Parent Company’s functional and presentation currency, rounded off to the nearest thousand. The principal accounting policies are stated below.

Basis of consolidationThese consolidated financial statements incorporate the financial statements of the Parent Company and entities controlled by the Parent Company (its subsidiaries) as detailed in note 32. Control is achieved where the Parent Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

The results of subsidiaries acquired or disposed of during the year are included in the consolidated statement of income from the effective date of acquisition or up to the effective date of disposal, as appropriate.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with those used by other members of the Group.All intra-group transactions, balances, income and expenses are eliminated in full on consolidation.

Going concernThe directors have, at the time of approving these consolidated financial statements, a reasonable expectation that the Parent Company and the Group have adequate resources to continue in operational existence for the foreseeable future. Thus they continue to adopt the going concern basis of accounting in preparing these consolidated financial statements.

Business combinationsThe acquisition of subsidiaries and businesses is accounted for using the purchase method. The cost of the business combination is measured as the aggregate of the fair values (at the date of exchange) of assets given, liabilities incurred or assumed, and equity instruments issued by the Group in exchange for control of the acquiree, plus any costs directly attributable to the business combination. The acquiree’s identifiable assets, liabilities and contingent liabilities that meet the conditions for recognition under IFRS 3 Business Combinations are recognised at their fair values at the acquisition date, except for non-current assets (or disposal groups) that are classified as held for sale in accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, which are recognised and measured at fair value less costs to sell.

In accordance with normal oil exploration and production industry practice, identifiable assets and liabilities are ascribed fair values, and the balance of the fair value of the consideration given being allocated as the fair value attributable to the oil and gas properties and related hydrocarbon reserves and therefore, goodwill does not normally arise on acquisitions.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2009

KUWAIT ENERGY COMPANY K.S.C (CLOSED) AND SUBSIDIARIES46

Interests in joint venturesA joint venture is a contractual arrangement whereby the Group and other parties undertake an economic activity that is subject to joint control that is when the strategic financial and operating policy decisions relating to the activities of the joint venture require the unanimous consent of the parties sharing control.