Embed Size (px)

Citation preview

WHITE PAPER

KYC Sparks an Automation Revolution:

New Tools to Keep Your Processes Compliant and Your Customers Content

KYC Sparks an Automation Revolution: New Tools to Keep Your Processes Compliant and Your Customers Content

Know Your Customer (KYC)—More Than Just a Compliance Headache

The goal of any financial institution is to attract and retain clients, reduce the costs of doing business, and

drive growth and profitability. In an era of transformation and digitization, key industry drivers include

delivering a rich, omnichannel experience to your increasingly savvy customers, modernizing your

infrastructure to keep costs in check and finding better ways to keep up with a seemingly endless list of rules

and regulations.

One of the most critical among this list is the requirement to determine the trustworthiness and the true

intent of a potential customer or company who engages with you. Know Your Customer (KYC) is the process

of a business verifying the identity of its clients by using reliable, independent source documents, data or

information. The term is also used to refer to the bank regulation that governs these activities. KYC policies

and practices are becoming much more important globally to prevent identity theft, financial fraud, money

laundering and terrorist financing.

KYC and the associated Anti-Money Laundering (AML) requirements first come into play when an individual or

company desires to enter a business relationship with you, such as when opening a new account or securing

approval for a loan. The KYC/AML compliance requirements include checking a potential customer’s identity

information against numerous external watch lists and public record databases, as well as collecting and

integrating the necessary external data with internal systems. Customer Due Diligence (CDD) is also critical,

comprising regular checks and ongoing monitoring of the information gathered.

And although KYC requirements are stringent and create many challenges for a

financial institution, the consequences of non-compliance are significant. KYC

is not merely a compliance headache that can result in heavy fines. The way in

which KYC is implemented and managed within an organization can also have

far-reaching consequences that impact client retention, labor costs and,

ultimately, revenue and profit margins for the long term.

The client experience is key. Customer frustration (and the resultant risk of abandonment during the

onboarding process) has invariably increased as banks struggle with KYC compliance. For example, when KYC

processes rely on manual input of information between systems, customers are often asked to provide the

same information repeatedly. In one study, banks contacted their clients an average of four times during the

onboarding process (often different personnel from different departments), and corporate clients reported an

average of eight contacts across a higher number of different bank departments.1 This suggests that an

uncoordinated and inefficient process is likely leading financial institutions to unwittingly duplicate KYC

requests; this can damage the customer’s confidence in the financial institution’s ability to balance protecting

the accuracy and security of their information with a customer-friendly experience.

Client onboarding, customer screening and ongoing reviews account for close to 40% of banks’ KYC/AML spending.Artificial Intelligence in KYC-AML, Celent

1

1 Thompson Reuters, 2016 Know Your Customer Survey

KYC Sparks an Automation Revolution: New Tools to Keep Your Processes Compliant and Your Customers Content

The KYC Status Quo—Mired in Manual Processes

Financial institutions are beginning to realize that the status quo is not a viable go-forward strategy if they are

to have a realistic expectation of addressing their compliance challenges. First of all, KYC is costly. The

average financial firm spends $60 million per year on KYC and CDD and $58 million per year on client

onboarding. Some firms spend more than $500 million annually on these activities.2 But although the costs

of compliance are high, the costs of non-compliance are even greater. Since 2010, banks have paid more than

$300B in fines for non-compliance.3

The status quo also commonly includes the hiring of additional staff to

process the avalanche of manual tasks required to ensure that information

submitted by every new potential customer is complete and accurate. In fact,

50% of financial institutions have added employees to keep up with KYC

compliance over the past year, and an average of 68 employees work on KYC

adherence and processing within a financial institution.4

However, adding more humans to the equation invariably increases the

likelihood of errors (not to mention labor costs and the difficulty in finding

qualified compliance workers), and a snowball effect pattern begins to

emerge. These manual inaccuracies lead to risk of non-compliance, which can

lead to hefty fines and delays in the onboarding process. Delays can alienate customers, damage a firm’s

reputation and result in slowed revenue realization or even loss of business. Today’s customer demands a fast

frictionless engagement with you, and it is this initial information-intensive first interaction that can make or

break the relationship, whether you are onboarding a retail client, a wealth management client, institutional

client or corporate client.

And this snowball effect shows no signs of slowing. Consider that in 2015, it took financial institutions 24

days to onboard a new client—22% higher than it took in 2014—and onboarding times are expected to have

increased by another 18% in 2016.5

Lost sales

64% Rate of banks that report lost deals and revenue

due to problems in their current onboarding

Lost revenue

$400 Negative impact of an attritioned customer

Lost customers

25-40%

First year rate of attrition among top

100 institutions

Compliance

$B Billions in fines to banks

in recent years

“Banks’ approach to KYC-AML traditionally has been reactive rather than proactive, always looking to address imminent issues, which has resulted in short-term fixes like adopting multiple systems and hiring more resources.”Artificial Intelligence in KYC-AML, Celent

2,4,5 Thompson Reuters, 2016 Know Your Customer Survey

3 Insights: Another Fine Mess, Capco

2

KYC Sparks an Automation Revolution: New Tools to Keep Your Processes Compliant and Your Customers Content

And it’s not only the customers who are dissatisfied. Increasing numbers of

employees are mired in tedious work that inhibits their job satisfaction and

distracts the organization from focusing its personnel on more strategic,

revenue-related activities. Furthermore, senior management is diverted from

focusing on growth initiatives to spending time on non-cash generating KYC

processes. In one study, a significant 70% of C-level respondents reported that

they had dedicated more time and attention to KYC and client due diligence

changes over the past 12 months, while 19% described their involvement as

“significantly more.”9

Complicating the situation further is the fact that KYC regulations are always evolving, becoming increasingly

stringent and comprehensive, yet no consistent standard exists. Financial institutions must interpret KYC and

AML regulations and develop their own process for compliance. Embracing a dynamic, flexible response model is

critical for firms—a “set and forget” mentality will invariably fail and make the bank vulnerable, particularly to

increasingly sophisticated and dedicated criminal enterprises.

It’s important to note that although the first client interactions during the onboarding process can be the most

critical and set the trajectory of the firm/client relationship, KYC is an ongoing process. Financial organizations

must ensure client information is maintained, and remains current and valid; therefore, they must revisit KYC

documentation on a regular basis and conduct due diligence.

KYC Automation Best Practices—Taking the Complexity out of Compliance

KYC is complicated enough—your automation solution shouldn’t add to the complexity. Financial institutions

are best-served by leveraging smart, agile technology for acquiring, approving and onboarding new customers

and ensuring the processes are in place to ensure compliance—from the first critical customer touchpoints

and throughout the business relationship. Of course, the goal of any business that wants to be competitive is

to reduce process complexity wherever possible, while ensuring their organization is nimble enough to swiftly

respond to market fluctuations, and in the case of KYC, regulatory changes.

70% of financial institutions are worried about the consequences of non-compliance, which can include restrictions on business, financial penalties, brand damage/reputational risk and loss of customer and investor confidence.Thompson Reuters, 2016 Know Your Customer Survey

6 Forrester Consulting

7,8 Digital Banking Report

9 Thompson Reuters, 2016 Know Your Customer Survey

3

Failure to address onboarding problems can have serious ramifications. For example:

� 64% of banks have lost deals and revenue due to problems with their onboarding.6

� The top 100 institutions have a 25%-40% rate of attrition.7

� Each lost customer equals $400 in lost revenue.8

Taking Automation to the Next Level

A Valuable Tool in Your Compliance Toolbox – Software “Robots”

When it comes to addressing KYC, you know that manual processes are not a long-term solution. Yet not all

automation solutions will get you where you need to be in terms of compliance, customer satisfaction and

profitability. Newer cost-effective technology can help your firm vastly improve its compliance efforts to meet

KYC requirements—while reducing your labor costs, and streamlining your customers’ experience when

engaging with your business.

One revolutionary tool you can employ to help lessen your KYC compliance

burden and streamline your processes is robotic process automation (RPA). In

its simplest definition, RPA is software that transforms your manual tasks to

automated ones. RPA makes use of software “robots” that mimic the specific

actions a person would take while performing tasks in various applications.

Automation will touch more than 230 million knowledge workers, 9% of the global workforce by 2025.Disruptive Technologies, McKinsey & Company

RPA can reduce costs by 70% by replacing manual approaches with electronic identity verification.Kofax Advisor Blog

4

Consider the 6 Es of a smart, automated KYC/AML/CDD compliance workflow:

� Enhanced customer engagement via shortened processing time during onboarding (including swift

identity verification), along with ongoing monitoring and communications for due diligence

� Elimination of manual errors that lead to compliance risk, costly fines and delays, and increase

customer defection rates

� Efficiency built in to the process that cuts unnecessary manual tasks, saving time and reducing costs,

and freeing knowledge workers for value-add work

� Easy-to-use software that is simple and user-intuitive—and does not require coding

� End-to-end tools for design development and real-time testing and debugging

� Expandable architectures that easily scale and adapt to fast-changing regulations, external threats or

internal processes

KYC Sparks an Automation Revolution: New Tools to Keep Your Processes Compliant and Your Customers Content

When tackling KYC compliance, for example, these robots eliminate manual regulatory data collection and

monitoring. The robots interface directly with disparate internal systems and external websites or databases

and automatically select all of the information needed to authenticate an individual’s identity. The robot will

automatically check the individual’s supplied information against any number of data sources such as

sanctions lists from the U.S. Treasury and Immigration and Customs Enforcement, data from regulatory

agencies (such as SEC) and law enforcement agencies (FBI, Interpol), credit bureaus, telephone companies,

post offices, DMV, etc. And, importantly, multiple data sources can be queried simultaneously.

During those information-intensive first interactions with a new potential

customer—the opening of an account or application for a loan—RPA

streamlines the KYC compliance process and can consistently deliver a 100%

accuracy rate; this will help you meet your customers’ expectations for a

hassle-free experience and reduce your risk of non-compliance.

These robots are easily built through a one-time setup process and can be deployed in weeks, not months.

The robot “learns” how to extract the necessary identity verification data from third-party sources and then

pass the customer information to populate the account application or loan approval document, for example.

(Typically, your employee would have to manually key in all of this information and then manually validate each

and every time. With RPA, the robots handle this time-consuming and error-prone process.) Once the

information has been extracted and verified against the necessary sources, the results are then submitted to

your employee for review. If no discrepancies between the customer information supplied and third-party

sources are noted, the application can be routed for STP (straight-through processing) without further action

by the employee. If discrepancies are noted, the employee will receive notification of the discrepancies and

can take further action.

And because KYC is not a one-time process, RPA is designed to help you respond faster to regulatory

updates by automatically monitoring and extracting external data from regulatory sites, as well as performing

due diligence checks on your customers’ information on a periodic basis to ensure their data is maintained,

current and valid. The KYC workflow can be executed on a fixed schedule or on-demand; if a material change

from a customer is submitted, the KYC process can also be triggered. The software provides you with detailed

audit trails, so your compliance and risk management teams don’t have to worry about reputational damage

and costly fines due to non-compliance.

RPA slashes processing times by up to 90% (30%-50% reduction for an average process).Benefits of Robotic Process Automation, Virttia

5

KYC Sparks an Automation Revolution: New Tools to Keep Your Processes Compliant and Your Customers Content

Building a Smarter Solution Through a Platform Approach

It’s clear that RPA can remove a tremendous manual task burden on your employees, reducing costs, errors

and timelines, and thereby increasing customer satisfaction. However, the ideal automation solution can and

should deliver even greater value. It’s helpful to think of RPA as a hyper-efficient tool that does the tedious

and time-consuming work of gathering clean, accurate data.

But what do you do with that data once you receive it? This is where a platform approach (as depicted in the

graphic below) can yield wide-ranging benefits.

Half of North American and European organizations stated that automation will significantly improve their processes over the next 3-5 years.

The Robot and I: How New Digital Technologies Are Making Smart People and Businesses Smarter by Automating Rote Work, Cognizant

Ease Burden on Customer

Material Changes

360° Customer View

Automated Monitoring

External Internet Sources

External Identity

Data Sources

Internal Media Sources and Publications

Analytics and Insight Into Every Step

of the Process

Audit TrailsBusiness Process

& Rule Based Automation

Scheduled CDD Checks

Automated Risk Assessment

Scoring

Any Input Device or Channel

Internal Identity Data Sources

Potentially Valid Event

CAPTURE PRO

CES

S MANAGE

D

ELIV

ER

6

Ideally, RPA should comprise one of many building blocks in a flexible automation platform that will deliver

comprehensive, long-term value for your business—a business that is people-intensive and subject to

frequent change. Agility is key. An out-of-the box, one-size-fits-all system cannot give you the flexibility to tailor

the solution as your business grows, and the needs and demands of your customer base inevitably evolve.

Think about your current onboarding process. Do you rely heavily on manual efforts? Are you automated in

some areas, but not others? Could you do more to engage your customers—not only during the first critical

interactions, but throughout the business relationship—and differentiate your services from the competition?

Are you taking too many risks when it comes to compliance because you feel overwhelmed?

A modular software framework can help you address many of these challenges by allowing you to quickly

respond to change—whether that’s changing market conditions or regulations, or customer expectations. By

deploying a solution framework that empowers you to build your own unique workflow via reusable,

customizable software components, you can deploy a smart solution that will:

7

� Offer new customers the ability to scan their ID with a mobile device to jumpstart the account opening

process and speed approval.

� Continue to engage customers through regular communication across multiple channels (online,

mobile, print) using intelligent templates.

� Help your staff ensure approval criteria are applied consistently using rules-based workflows that can

be easily modified.

� Enable your managers to identify process bottlenecks and make insightful comparisons to historical

performance through built-in analytics dashboards.

� And, of course, empower your risk management personnel through RPA to quickly and accurately

authenticate identity data, eliminate errors, create an audit trail and strengthen regulatory compliance.

KYC Sparks an Automation Revolution: New Tools to Keep Your Processes Compliant and Your Customers Content

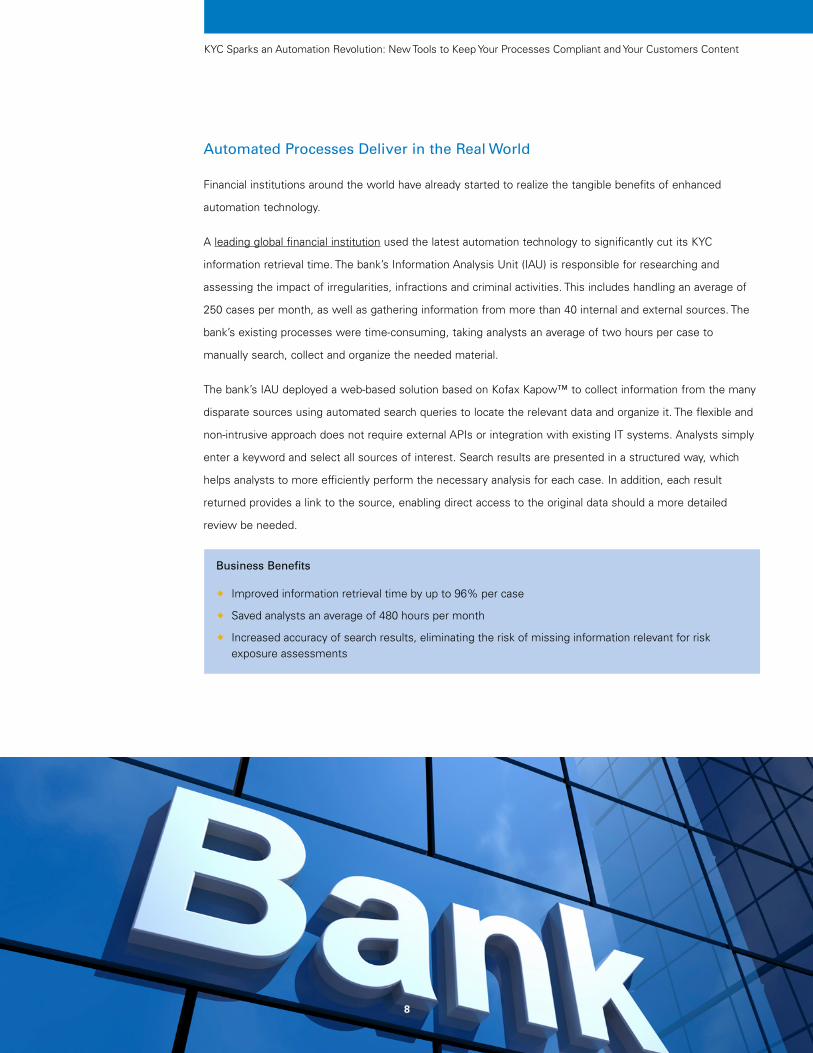

Automated Processes Deliver in the Real World

Financial institutions around the world have already started to realize the tangible benefits of enhanced

automation technology.

A leading global financial institution used the latest automation technology to significantly cut its KYC

information retrieval time. The bank’s Information Analysis Unit (IAU) is responsible for researching and

assessing the impact of irregularities, infractions and criminal activities. This includes handling an average of

250 cases per month, as well as gathering information from more than 40 internal and external sources. The

bank’s existing processes were time-consuming, taking analysts an average of two hours per case to

manually search, collect and organize the needed material.

The bank’s IAU deployed a web-based solution based on Kofax Kapow™ to collect information from the many

disparate sources using automated search queries to locate the relevant data and organize it. The flexible and

non-intrusive approach does not require external APIs or integration with existing IT systems. Analysts simply

enter a keyword and select all sources of interest. Search results are presented in a structured way, which

helps analysts to more efficiently perform the necessary analysis for each case. In addition, each result

returned provides a link to the source, enabling direct access to the original data should a more detailed

review be needed.

8

Business Benefits

� Improved information retrieval time by up to 96% per case

� Saved analysts an average of 480 hours per month

� Increased accuracy of search results, eliminating the risk of missing information relevant for risk exposure assessments

kofax.com© 2017 Kofax. Kofax and the Kofax logo are trademarks of Kofax, registered in the United States and/or other countries. All other trademarks are the property of their respective owners.

One of the largest banks in the Netherlands also embraced enhanced automation processes and realized

newfound efficiency and accuracy on CDD and KYC checks with robotic process automation.

The bank carries out extensive KYC/CDD checks to prevent identity theft and financial crimes, performing

upwards of 3,000 investigations every week. Previously, the bank relied on manual methods to complete

these investigations, and analysts spent hours every day on tedious, time-consuming data-gathering work.

With regulations growing increasingly complex, the bank found that the cost and effort of ensuring

compliance was fast becoming unsustainable.

Kofax Kapow was deployed to automate data-gathering processes linked to CDD and KYC investigations.

When the bank needs to perform a check on a new customer, Kapow software robots will search the group’s

internal systems and databases, as well as external sources, to verify the customer’s identity and confirm that

they are not linked to any illicit activity. With Kapow, the bank was able to significantly cut costs and reduced

their risk of regulatory non-compliance through fast, accurate customer checks. They also freed up highly

skilled analysts for more strategic work, boosting satisfaction and retention.

Business Benefits

� Reduced the time it takes to complete data-gathering work from 25 minutes to 2 minutes

� Easily scaled up to 24x7 service

� Increased data accuracy by 40%

� Implemented in only 5 months

� Saved 1000s of person-hours of work every week on KYC checks

Next Steps

Ready to learn more about how you can streamline your automation workflows, enhance KYC/AML

compliance and deliver a superior customer onboarding experience? We invite you to watch the KYC

Automation with RPA demo. You can also read about other successful RPA deployments at kofax.com.