Embed Size (px)

Citation preview

The Financial ReporterThe Newsletter of the Life Insurance Company Financial Reporting Section

AICPA Releases SOP 05-1Accounting by Insurance Enterprises for Deferred Acquisition Costs inConnection With Modifications or Exchanges of Insurance Contractsby John W. Morris

L I F E I N S U R A N C E C O M PA N Y F I N A N C I A L R E P O R T I N G S E C T I O N“A KNOWLEDGE COMMUNITY FOR THE SOCIETY OF ACTUARIES”

March 2006 Issue No. 64

AICPA Releases SOP 05-1

I n September 2005, the American Institute ofCertified Public Accountants, (AICPA)released the long-awaited Statement of

Position 05-1: Accounting by InsuranceEnterprises for Deferred Acquisition Costs inConnection With Modifications or Exchangesof Insurance Contracts (SOP or SOP 05-1).More than five years in development, the SOPprovides guidance on how insurance companiesshould account for deferred acquisition costs(DAC) relating to insurance and investment con-tracts that have had modifications in productbenefits, features, rights or coverages. The modi-fications can occur in various forms, such as acontract exchange, by amendment, endorsementor rider to an existing contract, or by the electionof a feature or coverage within an existing con-tract. The SOP (and this article) refers to all suchmodifications as “internal replacements,” thusdefining the term more broadly than what theinsurance industry may have referred to in thepast as internal replacements (typically explicitcontract exchange programs).

The primary issue addressed by the SOP is thetreatment of DAC associated with replaced poli-cies. Is the replacement considered to be a termi-nation of the initial contract, which would there-fore result in a reduction in the DAC asset? Or,is the replacement effectively a continuation ofthe original contract and, therefore, is there con-tinued amortization of the DAC asset relating to

the original contract? In addition to the financialreporting impact, the SOP may have an effect onfuture policy designs.

This article provides a review of the require-ments of the SOP, concentrating on the defini-tion of an internal replacement and the criteriafor determining whether such replacements areconsidered substantially changed. It also raisespotential implementation issues, and raises thepossibility that companies will consider modifi-cation to policy designs as a result of issueshighlighted by the SOP. As companies develop,update and execute their in-force managementstrategies, the SOP generates further considera-tions for companies seeking to address prof-itability, customer service and compliance issues

continued on page 3 >>

The Financial Reporter

Published by the Life Insurance CompanyFinancial Reporting Section of the Society of Actuaries

475 N. Martingale Road, Suite 600Schaumburg, Illinois 60173p: 847.706.3549f: 847.706.3599 w: www.soa.org

This newsletter is free to section members. A subscription is $15.00. Current-year issues areavailable from the communications department.Back issues of section newsletters have been placed in the SOA library and on the SOA Website (www.soa.org). Photocopies of back issues may be requested for a nominal fee.

2005-2006 Section LeadershipDarin G. Zimmerman, ChairpersonHenry W. Siegel, Vice-ChairpersonJerry F. Enoch, SecretaryRichard H. Browne, TreasurerErrol Cramer, Board PartnerKerry A. Krantz, Council Member(Web Liaison)Mike Leung, Council MemberRaymond T. Schlude, Council MemberVincent Y.Y. Tsang, Council MemberYiji S. Starr, Council Member

Rick Browne, Newsletter EditorKPMG LLP303 East Wacker Drive • Chicago, IL • 60601p: 312.665.8511f: 312.275.8509e: [email protected]

Jerry Enoch, Associate Editore: [email protected]

Carol Marler, Associate Editore: [email protected]

Keith Terry, Associate Editore: [email protected]

Joe Adduci, DTP Coordinatore: [email protected]: 847.706.3548

Clay Baznik, Publications Directore: [email protected]

Jeremy Webber, Project Support Specialiste: [email protected]

Facts and opinions contained herein are the soleresponsibility of the persons expressing themand shall not be attributed to the Society ofActuaries, its committees, the Life InsuranceCompany Financial Reporting Section or theemployers of the authors. We will promptly correct errors brought to our attention.

Copyright ©2006 Society of Actuaries.All rights reserved.Printed in the United States of America.

March 2006 Issue No. 64

AICPA Releases SOP 05-01A review of the new SOP dealing with DAC on internal replacements. This is one of a series

of articles by the American Academy’s Life Insurance Financial Reporting Committee.

John W. Morris

Chairperson’s Corner: Thoughts from the ChairInaugural comments from the new chairperson of the Financial Reporting Section Council.

Darin G. Zimmerman

Editor’s CornerRick Browne

RBC C3 Phase II: Easier Said Than DoneHow are actuaries coping with the new C3 Phase II requirements? This survey looks at

implementation practices by a number of life companies.

Patricia Matson and Don Wilson

On the Fair Value of Insurance Liabilities: The Continuing DebateContinuing discussion of the issue of how and whether an insurer’s “own credit risk” should

be reflected in the fair value of its insurance liabilities.

Don Solow

The Fair Value of Insurance Liabilities: The Information Set PerspectiveA follow up to December’s article on the “The Fair Value of Insurance Liabilities: the

Regulator’s Option” (Luke Girard).

Mike Davlin

Highlights of the December 2005 NAIC Life and Health Actuarial Task ForceMeeting and Other NAIC TopicsA good summary of LHATF and other life and health related meetings at the NAIC December

Chicago NAIC meeting.

Ted Schlude

8th Bowles Symposium & Second International Longevity Risk and CapitalMarket Solutions SymposiumUpcoming symposium being held on April 24, 2006 at the Sheraton Hotel in Chicago,

Illinois.

What’s Outside

What’s Inside

1

7

9

10

14

17

20

27

28

Financial Reporter | March 20062

associated with customer-driven and company-driven replacements.

Requirements of the SOPOn the surface, internal replacements may notappear to be a difficult subject. It would seem thateveryone knows what internal replacements are, orat least would be able to recognize one when theysaw it. However, developing and applying a defini-tion of an internal replacement that fits all situa-tions is not simple once one gets into the details andvariety of transactions that companies have withtheir policyholders. (For example, is there anaccounting implication of adding a general accountoption to a variable annuity, or of adding a seconddriver on an auto policy?) Since the SOP containsextensive guidance, any reasonable summary of theSOP is sure to omit certain provisions that may beimportant to a company’s specific situation. Asalways, readers (particularly preparers of financialstatements) are strongly encouraged to read theSOP and not to rely on this or other summaries astheir sole source of information.

OverviewThe initial guidance in the SOP covers whether theprovisions of the SOP apply to specific contractexchanges or modifications by:

Ø

Determining whether the internal replacement relates to the election of a benefit or right that was present in the existing contract. If so, deter-mine whether it meets the exclusion criteria in the SOP.

Ø

Determining whether the feature being added is a “nonintegrated contract feature,” as defined in the SOP. If so, the feature is not considered to change the original contract, and is treated in a manner similar to a separately issued contract, thus not impacting the accounting for the original contract.

If the internal replacement does not meet either ofthe exclusions noted above, it is considered an inte-grated contract feature, and must meet all of the sixconditions specified in the SOP to be considered a“substantially unchanged” contract. In general, thatguidance in the SOP is:

Ø

For internal replacements, which result in contracts that are “substantially unchanged,” the replacement contract should be treated as a continuation of the original contract for the purpose of DAC amortization.

Ø

Otherwise, when an internal replacement results in contracts that are “substantially changed,” the original contract should be accounted for as a termination, and the modi-fied contract accounted for as a new issue. In these situations, because the original contract is effectively considered extinguished, the DAC asset relating to the terminated contract can no longer be deferred. New acquisition costs asso-ciated with the replacement contract are to be capitalized and amortized as DAC if they meet the criteria for deferral, and amortization would be based on the characteristics of the replace-ment contract only.

Ø

Accounting for sales inducement assets, unearned revenue liabilities and any additional liabilities (e.g., guaranteed minimum death benefits of variable annuities) associated with the original contract would be accounted for in a similar manner as described above for the DAC asset. That is, if the contracts are substan-tially unchanged, those balances would continue to be recognized as part of the replace-ment contract accounting. If the contract were considered substantially changed, those asset and liability balances would be accounted for as

Financial Reporter | March 2006

>> AICPA Releases SOP 05-1

John Morris, FSA,MAAA, is a member ofthe American Academyof Actuaries’ FinancialReporting Committee,and is a managingdirector for PriceWaterhouseCoopers in Downington, Penn.He may be reached [email protected].

3

continued on page 4 >>

>> AICPA Releases SOP 05-1

part of the extinguishment ofthe replaced contract and theissuance of a new contract.

Although the guidance in theSOP is applicable to life as wellas property & casualty insur-ance companies, life companieswill experience the main impact

of the pronouncement.

Definition of Internal ReplacementAn internal replacement under the SOP could resultfrom one of three main types of modifications to thebenefit features in the contract:1. A contract exchange (legal extinguishment of

one contract and the issuance of a new contract),

2. Amendment or attachment of an endorsement or a rider to an existing contract, or

3. The election of a benefit feature, right or coverage within an existing contract.

The purpose of having such a broad definition of aninternal replacement is to enable application of theguidance in the SOP consistently to similar transac-tions regardless of the form of the transaction. Forexample, the same accounting guidance applies to avariable annuity in the following two situations:a Additional variable account investment options

are added to the contract through a contract amendment, or

b. The contract is replaced with another variable annuity, with the only changes being the addi-tion of additional variable account investment options.

Similarly, the same accounting guidance applieswhen a guaranteed minimum withdrawal benefit(GMWB) is added to a variable annuity in either oftwo situations:a. A GMWB rider is added to a contract

previously issued without such a guarantee, orb. The contract is replaced with a new contract

where the only material change is the addition of the GMWB.

Likewise, there are instances when the election of abenefit feature within an existing contract will resultin a contract modification, for example, when aguarantee feature can voluntarily be elected subse-quent to contract issuance and the fee charged forthis additional benefit is not specified until elected.

Substantially UnchangedPerhaps at the heart of the SOP are the six criteriathat must all be satisfied in order for a contract mod-ification to be considered “substantially unchanged.”While all six are important, the first two criteriainvolving the insured event and investment returnrights are the most critical for the usual contractmodifications currently occurring in the market-place.1. The first criterion requires that there be no

significant change in the kind and degree of insurance risk within the contracts. For example, replacing a mortality contract with a morbidity contract changes the kind of insured event. In addition, although a life insurance contract and a life contingent payout annuity both contain mortality risk, they are clearly different types of mortality risk.

When the kind of risk is determined to be the same, the degree of risk needs to be assessed. That determination will be subjective as there is no specific guidance in the SOP on how to measure “degree of risk.” Re-underwriting all or a portion of the original base contract will generally result in a substantial change to the insurance risk. Companies will need to develop and consistently follow an accounting policy on what constitutes a significant change in the degree of risk.

2. The second criterion requires that there be no change in the nature of the investment return (i.e., the manner is which the policyholder’s investment return rights are determined). The SOP provides examples of various ways that interest may be credited in the policy—either by formula (such as that found in equity indexed products), pass-through of actual performance (such as that typically found in separate account products), or credited at the discretion of the insurance company (the typical general account product design). Changes between these three different types of interest crediting would fail the “substantially unchanged” test and require the original contract to be considered term-inated and the modified contract to be considered a new issue.

One of the most challenging aspects of application islikely to be in the interpretation of what constitutesa change in the degree of mortality risk and in thenature of investment return for modifications relat-ing to complex contracts such as variable contracts

Perhaps at the heart of the SOPare the six criteria that must all besatisfied in order for a contractmodification to be considered“substantially unchanged.”

Financial Reporter | March 20064

with minimum guarantees. For example, variablecontracts with existing mortality guarantees may bemodified to offer enhanced mortality guarantees. Insome cases, the enhancement may be deemed to beso significant as to result in a substantial change,while in other cases, it may not. The addition of asignificant investment floor, such as a GMWB addedto a variable product, is considered to be a significantchange. Interestingly, it is not clear in the SOP if thedeletion of such a floor should also be considered asubstantial change. If the original contract contains aclear right of the policyholder to delete the coverage,this type of transaction could be interpreted as notbeing an internal replacement subject to the guid-ance in the SOP. In analyzing the effect of the SOPon a change in the investment floor, the companywill need to consider the degree of change associatedwith the modification when applying the SOP tothis type of transaction.

The remaining four criteria include provisions thatthe internal replacement not require any additionaldeposit/premium/charge, a reduction in the con-tract holder’s account value, a change in the partic-ipation or dividend features or a change in theamortization method or revenue classification ofthe contract. If any of the criteria are not met, thenthe internal replacement is deemed to be a “sub-stantial change.”

Integrated vs. Non-Integrated BenefitFeaturesThe SOP recognizes that there may be certain riders,benefit features, endorsements or coverages thatfunction as separate contracts from the original con-tract. The underwriting and pricing for a non-inte-grated benefit are typically executed separately fromother components of the contract. An accidentaldeath benefit rider added to a whole life insurancepolicy is an example of a non-integrated benefit. Incontrast, an integrated benefit feature for a long-duration contract, such as a universal life policy, isone in which the benefits provided by the feature canbe determined only in conjunction with the balancesrelated to the base contract. A GMWB is an exampleof an integrated benefit feature.

Under the SOP, the addition of a non-integratedbenefit feature should be accounted for as if the fea-ture is a separate contract, and, therefore, most ofthe other provisions of the SOP are not applicable.In contrast, additions or changes determined to beintegrated features require further analysis to deter-mine whether the addition of the integrated feature

produce a contract that is substantially changed orsubstantially unchanged.

Now if you think this is all getting a little complicat-ed, you are not alone. The Accounting StandardsExecutive Committee of the AICPA thought so aswell. Included as Appendix C of the SOP is an appli-cation flowchart designed to help clarify the compli-cated steps.

Prospective Revision Method for FAS 60ProductsAn interesting provision in the SOP is the require-ment to use a “prospective revision” method forapplying the SOP for FAS 60 products that are sub-stantially unchanged. Under the prospective revisionmethod, DAC balances at the time of the transactionare unchanged, and any changes in the contract arereflected in future amortization only. Interestingly,the SOP states that this method is considered anappropriate application of the FAS 60 guidance onpremium changes for indeterminate premium lifeinsurance and guaranteed renewable health products.Although many have already considered this to bethe appropriate GAAP accounting treatment for pre-mium rate changes under FAS 60, the guidance inthe SOP appears to be the first time this issue hasbeen addressed in authoritative GAAP literature.

Implementation Although the SOP has a required effective date ofJanuary 1, 2007, companies that have not begun toimplement the SOP are probably already behindschedule. The long lead time was set knowing thatthe SOP will be difficult for many companies toimplement.

Financial Reporter | March 2006 5

continued on page 6 >>

The following steps are suggest-ed as an approach to implementthe SOP:1. Prepare an inventory of cur-rent and expected potentialinternal replacement transac-tions (types and volume). 2. Determine whether any of thetransactions meet one of the twoexclusions provided by the SOP

(i.e., either election by the contract holder of a benefit, feature, right or coverage that was within the original contract or qualifies as a non-integrated feature).

3. Determine whether each transaction that does not qualify for exclusion is an internal replace-ment resulting in (a) a substantially unchanged contract or (b) a substantially changed contract.

4. Follow the appropriate SOP accounting for the related deferred acquisition cost asset, sales inducement asset, unearned revenue liability and any additional liability categorized in Step (3) above.

5. Identify when the accounting treatments identi-fied in Step 4 differ from a company’s current accounting policies.

6. Create or modify administrative and accounting information systems as appropriate to capture the required information for implementing the SOP. DAC amortization models will likely need to be modified to properly account for internal replacements under the SOP.

For companies that are part of a large group of affil-iated companies with multiple insurance companylegal entities, the implementation of the SOP maybe particularly challenging for several reasons. First,for a consolidated financial statement presentation,an internal replacement under the SOP could resultfrom the replacement of a policy from one companyby one from a different but affiliated company, caus-ing the need to be able to track such replacementswithin the entire organization. In addition, theaccounting for internal replacements may becomeeven more taxing if stand-alone financial statementsare also necessary for individual companies withinthe entire group.

Longer Term EffectsIt is reasonable to predict that companies will notwant to increase DAC amortization every time afloor is added to a separate account product. It is alsoreasonable to expect that product design profession-als will consider, among other factors, how changesin contract designs effect the results in their GAAP

financial statements, and may choose a design meet-ing other company objectives that lessens the effectsof the SOP. Will, for example, the provisions in theSOP now make it more attractive for companies tofix the price at issue of the original contract of cer-tain elect-able benefits? Will companies find a way todesign product features so that they are consideredto be non-integrated under the SOP? For example,would a GMWB tied to an outside index be asattractive to a company or a policyholder as one tiedto the policyholder’s specific account value? Theseare just a couple of examples of how the SOP mayaffect future policy design.

ConclusionsSOP 05-1 seeks to address current diversity in indus-try practice on accounting for internal replacements,providing authoritative and relatively detailed guid-ance for insurance entities. The required effectivedate of 2007 recognizes the administrative chal-lenges, including likely systems development work,for implementation. In addition, companies are like-ly to want to take proactive steps in managing theirinforce or adjusting their new business product port-folios in advance of implementing the SOP. As aresult, the author strongly encourages companies toquickly begin a process to review in detail the guid-ance of the SOP, establish cross-functional teams toidentify the variety of situations addressed by theSOP, and develop the administrative and financialsystem applications to track and implement theaccounting requirements.

Financial Reporter | March 2006

In addition, companies are likelyto want to take proactive steps in managing their inforce oradjusting their new businessproduct portfolios in advance of implementing the SOP.

>> AICPA Releases SOP 05-1

$

6

T he structure for the inaugural column for thechairperson’s corner is largely determined bytradition: 1) perfunctory remarks; 2) thank the

previous chairperson; 3) laud heaping praise on theother council members; and 4) briefly describe yourvision for the direction of the council in the upcom-ing year. Given that I plan to follow this tradition(mostly), I really have no excuse for being threeweeks late in my submission of this column.Nonetheless, I am. So without further delay, here isthe rest of the column:

Preliminary RemarksWere you aware that “perfunctory” means “doneroutinely with little interest or care?” I’m certainlynot going to deliver these words with “little interestor care” and so my first official act as chairperson willbe to rename the opening section of the inauguralcolumn. I find it ironic that my first act in followingtradition is to change things. I imagine all of the sec-tions’ chairpersons are pondering this curiosity.

The nature of life is one large balancing act. The actof leading any institution requires one to find theright balance of things to leave alone and things tochange. My survey of the section’s current situationshows that things are humming along prettysmoothly. This is my way of saying, “Don’t expectdramatic changes.” I anticipate that we will continuethe section’s mission of delivering a host of educa-tional opportunities and funding research. The itemsI will try to change are described more fully in thelast section.

Thank the Previous ChairpersonSpeaking of “humming along smoothly,” our sec-tion owes a debt of gratitude to Tom Nace. Heremy remarks are the opposite of perfunctory. Therewere a number of changes at the SOA during 2005.The SOA implemented a number of initiatives con-tained in the SOA Strategic Plan, aimed at improv-ing SOA membership value, knowledge manage-ment, the marketplace relevance of actuaries andadvancing external recognition of our professionalcommunity. These are all worthwhile goals to besure, but success requires a lot of additional efforton the part of the section councils’ chairpersons totransform these goals into concrete actions aimed atachieving the goals. I think Tom did an admirablejob of taking these intangible concepts and

transforming them into initiatives with form andsubstance.

And if those challenges weren’t difficult enough forTom, 2005 also saw the retirement of LoisChinnock. Lois had been a fixture at the SOA for anumber of years, and she had handled all of theadministrative details for our section. To say thatLois was incredibly good at her job is an understate-ment of monumental proportions. The next timeyou run into a former chairperson of our section(like Mark Freidman, John Bevacqua, Tom Herget,or Shirley Shao) simply mention Lois’s name. Nomatter how many nice things I say about her, youwill still be surprised by the testimonials these peoplewill offer on Lois’s behalf.

Laud Heaping Praise on Our Council MembersI am fully aware that my remarks can at times seemflippant. They are not intended to be. Furthermore,it would be a travesty if my remarks here werebelieved to contain even a hint of insincerity. Perhapsit’s the time of year (today is December 23), but Ifind myself reflecting on the subtle distinctionbetween being lucky and being blessed. Both wordsare synonymous with the condition of good fortune;however, I believe the latter is the reason I will get toserve with the following people:

• Henry Siegel is the council’s vice chair. He is diligent, dependable and experienced, and has been extremely helpful.

Financial Reporter | March 2006

Thoughts from the Chairby Darin G. Zimmerman

Chairperson’s Corner

continued on page 8 >>

Darin G. Zimmerman,FSA, MAAA, is managing actuary withAEGON USA, Inc. inCedar Rapids, Iowa. He may be reached [email protected].

7

Financial Reporter | March 2006

• Kerry Krantz is our commu-nications and publications coordinator. He has worked tirelessly to develop and expand our Web site.

• Rick Browne is treasurerand newsletter editor. Rick is

incredibly understanding when I miss my deadlines. He is also very creative in awarding the FROSTIES and FRUMPIES.

• Yiji Star is our membership coordinator.• Mike Leung is our continuing education

coordinator and is in charge of coordinating the SOA Spring Meeting program.

• Jerry Enoch is our secretary and research team coordinator. He is also the past newsletter editor.

• Ted Schlude is our basic education team coordinator.

• Vincent Tsang is our marketplace relevance team coordinator

I also need to mention Mike Bell, a staff actuary atthe SOA; Jeremy Webber, who is our project supportspecialist; and Errol Cramer, who is our Board ofGovernors partner. There is no question that theSOA is committed to providing our council with theresources it needs to succeed.

Vision for the FutureAs I pondered what to write in this inaugural column,I found myself often thinking of the phrase, “Thevision thing.” As you may recall, the current president’sfather was mercilessly (and appropriately) mocked forcasually dismissing the most important component ofleadership as, “The vision thing.” I’ve always associat-ed this comment with the mental picture of Dogbertdismissively waving his paw and grunting, “Bah!”

Currently my vision includes the following objec-tives:• Continue and improve on the development and

delivery of basic educational opportunities:o SOA Spring Meeting Programo SOA Annual Meeting Programo Seminars (GAAP, Principles-based

reserving, etc.)o Webcasts (IAS, Fair Value Measurement, etc.)

• Continue and improve the section’s quarterly newsletter by ensuring that it contains informative, interesting and timely articles

• Identify and implement initiatives aimed at achieving the objectives laid out in the SOA’s Strategic Plan

• Educate actuaries as to the differences between the AAA and the SOA

• Work with the AAA to help promote the actuarial profession

• Develop a policy of surplus management for the section.

And finally, identify and recruit a slate of talentedand enthusiastic candidates for next year’s sectionelections.

I think this vision is ambitious without being over-ly ambitious (that is, just the right balance.) And Icould really use your help. Please send me yourthoughts and ideas throughout the year in order tohelp me with the objectives outlined here. If youhave research ideas, or ideas for newsletter articles,or if you can think of a topic that would make areally excellent webcast, please send an e-mail to [email protected].

>> Chairperson’s Corner

There is no question that theSOA is committed to providingour council with the resources itneeds to succeed.

$

8

Financial Reporter | March 2006

Greetingsby Rick Browne

T he Financial Reporter has featured severalarticles in the past year on the fair value ofliabilities, with good discussion of the “own

credit risk” question: if and how the credit risk ofan insurer should be reflected in determining thefair value of its insurance liabilities. The December2004 issue contained Don Solow’s article “On theFair Value of Insurance Liabilities.” Then inSeptember 2005 we carried Luke Girard’s piece,“On the Fair Value of Insurance Liabilities—TheOther Viewpoint,” and in December 2005 anoth-er article by Luke which introduced the concept ofthe regulator’s option in “On the Fair Value ofInsurance Liabilities: The Regulator’s Option.”

In this issue we follow up with two more articles onthis topic. The first is a rebuttal by Don Solow toLuke Girard’s September article. The second is a dif-ferent, but complementary, perspective on Luke’sregulator’s option article written by Mike Davlin. Ihope our readers will find this ongoing and livelydiscussion to be informative and interesting.

The March issue also includes an article by JohnMorris on SOP 05-01, which addresses GAAPaccounting for DAC on internal replacements. Thisis one in a series of articles for The Financial Reporterprepared by the American Academy’s Life InsuranceFinancial Reporting Committee (LIFRC). This SOPis effective next year (2007).

As a complement to last issue’s article by Tim Ruarkon some of the practical considerations involved inimplementing the C3 Phase 2 requirements, we havein this issue the results of a Deloitte survey on C3Phase 2 practices reported by Patricia Matson andDon Wilson.

Finally, Ted Schlude has provided us with his reporton the December 2005 meeting of the NAIC Lifeand Health Actuarial Task Force. Thanks to Ted foranother excellent update.

– Rick

Editor’s Corner

$

Reserve your copy of U.S. GAAP for Life InsurersMake room on your bookshelf for the second edition of U.S. GAAP for Life Insurers. After over a year of work, the new edition is available. The authors have teamed up to provide text in these new and emerging areas:

Sales inducements, persistency bonuses, other SOP 03-1 issues, FAS133 interpretations including B36, treatments for GMDB, GMAB, GMIB, and GMWB, no-lapse guarantees, EIA valuation, shock lapse examples, totally new purchaseGAAP addressing FAS141 and FAS142, VA DAC practices, more foreign product examples, reinsurance accounting,fair value perspectives and GAAP balance sheet and income statement examples.

These are covered in 200 new pages and 100 new spreadsheet examples.

The cost of the new book is $115. If you need the old as well as the new, it’s $150 for both.

For ordering information, please visit http://books.soa.org/GAAPII.

The Section Council thanks authors Frank Buck, Mark Freedman, Tom Kochis, Dan Kunesh, Mike McLaughlin, Ed Robbins, Dave Rogers, Eric Schuering, Brad Smith, editor Tom Herget and overseer Shirley Shao for this fine effort.

9

Financial Reporter | March 2006

RBC C3 Phase II: Easier Said Than Doneby Patricia Matson and Don Wilson

M ost life insurance companies have faced thechallenge of implementing the recentlyadopted Life Risk-Based Capital Phase II

Instructions, which include new requirements forvariable annuity contracts. Adopted by the NAIC onOctober 14, 2005, the new requirements are effec-tive for year-end 2005 and require a stochastic mod-eling approach (subject to a minimum “standard sce-nario” requirement) for determining the C3 compo-nent of risk-based capital for variable annuities. Theapproach is complicated, involving multiple stepsand certain choices. A background summary of theapproach is shown in the shaded box.

In December 2005, when companies were in themidst of implementing the new regulations, DeloitteConsulting LLP performed an industry surveyregarding the application of the new rules. Theresults of that survey were shared with the partici-pants and are outlined in this article.

BackgroundThe new requirements involve determination ofa “Total Asset Requirement,” or TAR, as thegreater of (1) the results of a stochastic projec-tion and (2) the results of applying the “StandardScenario.” The C3 market risk component ofRBC is the excess of the TAR over reportedstatutory reserves (with a floor of 0), aftersmoothing and transitional rules and a possibletax adjustment.

The stochastic projection is performed using “realworld,” as opposed to risk neutral, assumptions forgenerating the economic scenarios. A minimum of1,000 scenarios are required, and the scenario gener-ator used must meet specific calibration points spec-ified by the American Academy of Actuaries’ report.Assumptions are to be based on “prudent best esti-mates.” Limits on reinsurance ceded (such as caps onrecoveries and/or floors on premiums) must be rec-ognized. While some companies are using a seriatimapproach to modeling, compression of policy datainto representative model cells is allowed to mini-mize run time.

Each stochastic scenario’s result is the lowest year-endpresent value of future projected surplus (for thebusiness in aggregate). The total asset requirementequals the negative of the mean of the results for the10 percent “worst” scenarios (conditional tail expec-tation 90, or CTE 90).

In modeling the underlying assets, any existing hedg-ing assets must be included. In addition, if the com-pany has a “clearly defined hedging strategy,” creditfor the hedge strategy can be taken in the projec-tions. Companies may use an integrated economicmodel to assess both interest rate and market (equi-ty) risk, but there are also several “shortcut”approaches suggested for modeling interest rate risk,in the event that an integrated stochastic approach isnot feasible.

The standard scenario involves a deterministic modelwith specific assumption requirements as specified inthe RBC Instructions. These assumption require-ments include specified:• Separate account returns, which involve an

initial shock drop in account values and a modest return thereafter

• Portions of contractual charges• Lapse and benefit election assumptions that are

dependent on the “in-the-moneyness” of the underlying contracts

• Mortality rates

The standard scenario results must be calculated foreach policy.

Don P. Wilson, FIA, is asenior manager andconsulting actuary withDeloitte Consulting, LLPin Hartford, Conn. Hemay be reached at [email protected].

Patricia E. Matson,FSA, MAAA, is a seniormanager and consultingactuary with DeloitteConsulting, LLP inHartford, Conn. Shemay be reached [email protected].

10

Financial Reporter | March 2006

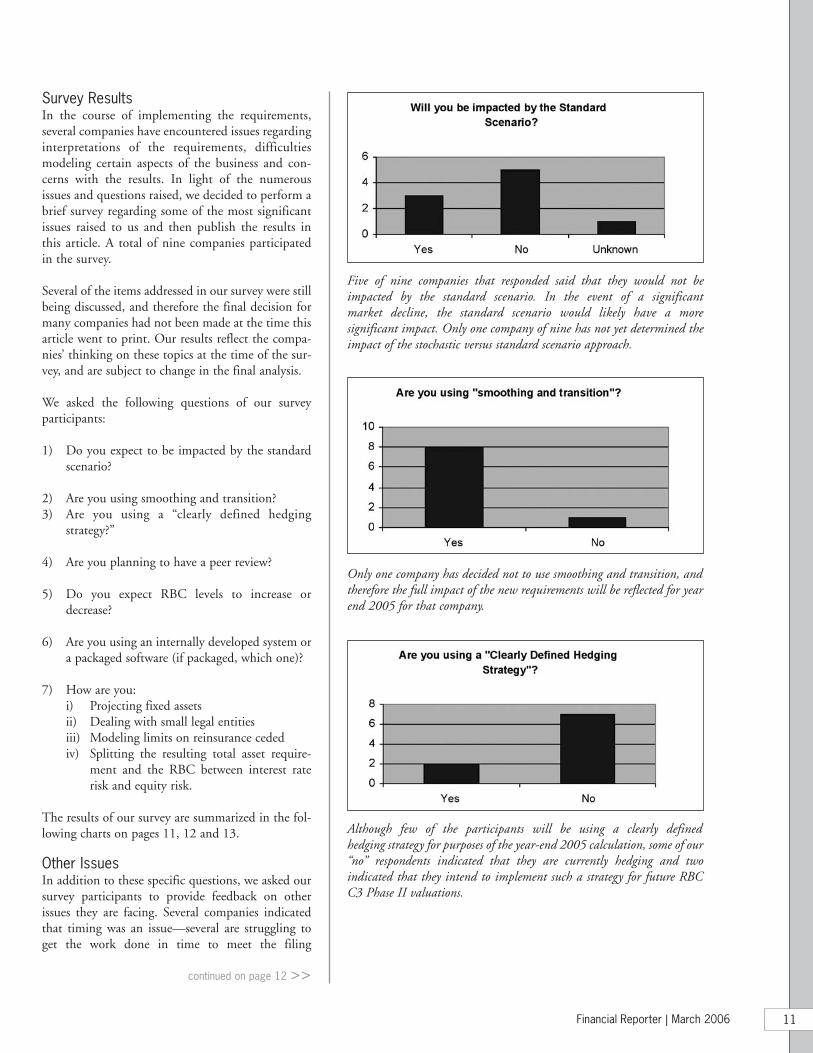

Survey ResultsIn the course of implementing the requirements,several companies have encountered issues regardinginterpretations of the requirements, difficultiesmodeling certain aspects of the business and con-cerns with the results. In light of the numerousissues and questions raised, we decided to perform abrief survey regarding some of the most significantissues raised to us and then publish the results inthis article. A total of nine companies participatedin the survey.

Several of the items addressed in our survey were stillbeing discussed, and therefore the final decision formany companies had not been made at the time thisarticle went to print. Our results reflect the compa-nies’ thinking on these topics at the time of the sur-vey, and are subject to change in the final analysis.

We asked the following questions of our survey participants:

1) Do you expect to be impacted by the standard scenario?

2) Are you using smoothing and transition?3) Are you using a “clearly defined hedging

strategy?”

4) Are you planning to have a peer review?

5) Do you expect RBC levels to increase or decrease?

6) Are you using an internally developed system or a packaged software (if packaged, which one)?

7) How are you:i) Projecting fixed assets ii) Dealing with small legal entitiesiii) Modeling limits on reinsurance ceded iv) Splitting the resulting total asset require-

ment and the RBC between interest rate risk and equity risk.

The results of our survey are summarized in the fol-lowing charts on pages 11, 12 and 13.

Other IssuesIn addition to these specific questions, we asked oursurvey participants to provide feedback on otherissues they are facing. Several companies indicatedthat timing was an issue—several are struggling toget the work done in time to meet the filing

11

continued on page 12 >>

Five of nine companies that responded said that they would not beimpacted by the standard scenario. In the event of a significant market decline, the standard scenario would likely have a more significant impact. Only one company of nine has not yet determined theimpact of the stochastic versus standard scenario approach.

Although few of the participants will be using a clearly defined hedging strategy for purposes of the year-end 2005 calculation, some of our“no” respondents indicated that they are currently hedging and two indicated that they intend to implement such a strategy for future RBCC3 Phase II valuations.

Only one company has decided not to use smoothing and transition, andtherefore the full impact of the new requirements will be reflected for yearend 2005 for that company.

Financial Reporter | March 2006

requirements for 2005. The following additionalissues were also mentioned:

• Interpretation of the AAA report: There are several areas in which the AAA report is am-biguous, and there are some apparent inconsis-tencies between the AAA report and the RBC instructions. This may lead to inconsistent results from company to company, and may require some follow-up clarification to reach resolution.

• Incomplete programming of the standard scenario in packaged software: Due to the relatively late adoption of requirements, software vendors have struggled to completely define and test the necessary coding in their packages systems.

• How results should be adjusted for taxes.• How best to organize results for reporting:

Meaningful to management and provide the appropriate detail for regulators.

• How rating agencies will interpret results: In light of the complexity, a significant amount of communication with the rating agency commu-nity will be required, particularly if results look different from most of the industry.

• Model run time: This was an issue for several companies, some of whom indicated that an overnight run was required.

• The impact on results of performing a “model point,” rather than seriatim, valuation: Some companies expressed concern that a model point approach would understate results, while others found little difference running seriatim versus model point models. This appears to indicate that careful determination of grouping rules is critical.

• Meeting the criteria for a clearly defined hedg-ing strategy:” As per our discussion there, a couple of companies with a hedging program had not incorporated it into their model for year-end 2005.

• Developing appropriate future revenue sharing assumptions after existing contracts expire: Since the requirement for assumptions is “prudent best estimate,” it may not be appropri-ate to assume current levels of revenue sharing will continue in the future.

As evidenced by our survey, there are several areasof uncertainty and some wide variations in practicecurrently. Most of the responses we received wereidentified as “current state” and subject to changeas models are finalized. It will be interesting to see

>> RBC C3 Phase II: Easier Said Than Done

As suggested by the AAA Report, five of the companies in our survey willbe having a peer review for year-end 2005. In all but one instance, thepeer review will be internal. Of those companies that do not plan to havea peer review at year-end 2005, all but one indicated that they will likely have one performed in the future.

As indicated by our survey, there is wide variation in systems used to perform the calculation, and several companies are using more than onesystem. In addition, we are aware of some companies that are having a parallel run performed in an alternate system as a mechanism totest their results.

Most respondents indicated that their results were tentative at the time ofour survey; however, the majority indicated that RBC levels were likely todecrease as a result of RBC C3 Phase II. Both companies that indicatedRBC would increase were also impacted by the standard scenario.

12

how practice evolves, and how results are impactedas companies continue to refine their approach.

We plan a further, wider survey once results havebeen filed, to help companies move forward towardsDecember 2006, when it is likely that the VACARVM reserving requirements will also be inplace. If you would like to participate in this survey,please contact the authors.

Financial Reporter | March 2006 13

Only one company in our survey has the capability todirectly project assets backing fixed accounts in theirRBC model. Most companies are assuming a specifiedearned rate (typically based on Treasury yields) plussome spread. Two companies are projecting their assetsin a separate model and using the result to determine aweighted average yieldtaking into account current fixedassets and future investments, and then inputting thatresult into their liability model.

Most companies had not yet finalized their methodology for modeling lim-its on reinsurance ceded at the time of our survey. Due to the complexi-ties of such limits for many treaties, adequately reflecting this in the mod-els can be difficult. For the most part, those surveyed did not believe thiswould materially impact their overall results.

Most of the companies we surveyed will continue to use either the factor-based approach or the RBC C3 Phase I approach to calculate theinterest rate component of RBC (one company indicated they would useone of these two methods, and therefore is counted twice in the chartabove), and three companies had not yet decided on a methodology. Onlytwo companies indicated that they would directly model interest rate riskby using an integrated stochastic interest rate generator in the C3 Phase IImodel.

The majority of companies we surveyed are directly modeling RBC C3Phase II for all legal entities. One company is using the alternativemethodology for a small subsidiary.

$

Financial Reporter | March 2006

T he September 2005 issue of The FinancialReporter contained an article by Luke Girardentitled “On the Fair Value of Insurance

Liabilities: The Other Viewpoint.” Mr. Girard’s arti-cle was written in response to my article in theDecember 2004 issue.

Mr. Girard appears to agree with my argument that apolicyholder, in purchasing a policy or contract froman insurance corporation, writes a credit put to theowner of the corporation. Where we appear to dis-agree is on the question of which balance sheet thisput belongs on: the corporation’s or the owner’s.According to Mr. Girard, “The put arises because ofthe limited liability of the corporation, thus the com-pany owns the put written by the policyholder. Andbecause the company owns it, it inures to the benefitof the owner of the company. The owner’s only inter-est is in the equity of the company and limited liabil-ity means the value of that equity cannot be negative.”

I believe Mr. Girard’s statements are incorrect. First,a corporation does not have limited liability: itsowners do. I quote from investorwords.com, whichdefines a corporation as “The most common form ofbusiness organization... This form of business ischaracterized by the limited liability of its owners...”.In the same vein, the legal Web site www.nolo.com,in its definition of corporation, states: “One advan-tage of incorporating is that a corporation’s owners(shareholders) are legally shielded from personal lia-bility for the corporation’s liabilities...”.

Second, limited liability does not mean that share-holders’ equity cannot be negative. Shareholders’equity is just another name for net assets or networth, and is simply the arithmetical result of sub-tracting total liabilities from total assets. Consider acorporation, which has cash of $100 and an accountpayable, immediately due, of $110. Clearly, theamount of net assets of the corporation, or its share-holders’ equity, is negative. Limited liability meansthat the owner or shareholder of a corporation can-not lose more than the amount invested. It does notmean that corporate liabilities cannot exceed corpo-rate assets.

Mr. Girard takes the position that the credit putbelongs on the corporation’s balance sheet as a com-ponent of shareholders’ equity. In order for this to betrue, the credit put must be shown to be an asset ofthe corporation. I believe it can be demonstratedthat the credit put is not an asset of the corporation.

An asset is an economic resource. It is property.Characteristics of the owner of any property include(1) the right to sell, transfer or otherwise assign theproperty to another party and (2) the ability to enjoya benefit from an increase in value of the property,and to suffer harm from a decrease in value. We canconsider the credit put in light of these characteris-tics. The owner of the credit put can transfer (or evenrelinquish) the credit put by, for example, writing aguaranty of the corporation’s liabilities for the benefitof creditors, issuing a net worth maintenance agree-ment, or co-signing a stand-by letter of credit. Inaddition, creditors will place higher value on theseguaranties as the corporation’s credit quality decreas-es. This means the market price for such a guaranteewill go up as credit quality goes down. However, thisis just another way of saying that the value of theowner’s credit put goes up as credit quality goesdown. We see, then, that the characteristics of thecredit put are such that only the owner of the corpo-ration has the right to transfer the put, and only theowner of the corporation realizes increasing value ofthe put from a decrease in credit quality. Conversely,the corporation itself has no right to transfer the put.It cannot force the owners to guarantee the corpora-tion’s debts or otherwise to accept additional liability.It cannot force the owners to relinquish their rights to

On the Fair Value of Insurance Liabilities:The Continuing Debateby Don Solow

14

limited liability. The corporation, in fact, enjoys noneof the benefits of the put. Therefore, the put cannotproperly be viewed as property of the corporation,but only as property of the shareholders. This meansthe put is not an asset of the corporation and, by def-inition, cannot be a component of its net worth.

Reasoning from basic economic principles, we canuse the arguments presented here to conclude thatthe credit put is owned by the shareholders of aninsurer and is not part of the insurer’s own accounts.We can reach, I believe, the same conclusion by rea-soning from the practical basics of financial state-ments. Specifically, the goal of a financial statementis to produce useful information for users of thefinancial statement. The users are interested in mak-ing certain economic decisions about the enterprise,which may include investing in the enterprise, re-appointing (or replacing) its management and so on.

Let us consider, in this light, two identical insurancecompanies, termed Company A and Company B,both rated AAA currently. Suppose both companieshave agreed by contract to make a payment to a pol-icyholder of $1,000 in five years’ time. Let us assumethe five-year AAA spot rate is 5 percent. If we acceptMr. Girard’s arguments, each company should valueits liability at $1,000 x (1.05)^(-5), or approximate-ly $784.

Let us further assume, immediately following theissuance of this contract, that Company B hires theThree Stooges as its management. (Please do notwrite to me saying the Three Stooges are already man-aging your company). Anticipating future problems,the market reacts by adding three percentage pointsto Company B’s credit spread.

If we accept the idea that liabilities of Company Bshould be valued using Company B’s current creditspread, the new liability value becomes $1,000 x(1.08)^(-5), or $681. Since the assets of the compa-ny have remained unchanged, the effect of hiring theStooges is to increase reported net worth by $103.On the other hand, Company A’s net worth remainsthe same.

A user of financial statements could reach a numberof conclusions: (1) Company B is worth more thanCompany A, even though both companies havemade the same contractual promise, (2) the Stoogesare excellent managers, having increased the networth of the company very quickly, (3) Company Bis a better investment opportunity and (4) CompanyB has more surplus to absorb deviations. I believe theabsurdity of all these conclusions suggests that

Company B’s financial statements are not useful tousers of the statements, whether those users arecurrent shareholders, potential investors, lenders,rating agencies or regulators. The financial state-ments could cause the user to make poor econom-ic decisions.

By reasoning, then, either from economic principlesor from the practical purpose of financial statements,I believe that it is incorrect to assert that the creditput is part of shareholders’ equity.

I would like to turn to some other comments madeby Mr. Girard in his article. First, Mr. Girard statesthat the use of a risk-free discount rate is inconsistentwith past practice. This is true. My December 2004article did not deal with the merit (or lack thereof )of deviating from past practices, so I will not addressthe point here, other than to indicate that, by defini-tion, any change in accounting method is a deviationfrom past practice.

Second, Mr. Girard expresses concern that discount-ing at the risk-free rate “... could lead to life insurersreporting losses when writing profitable new busi-ness.” My article addressed only the valuation of lia-bilities, but the following observations can be made.Suppose a company issues a contract with a $10profit load, which is priced under the assumptionthat the insurer will earn a rate of 6 percent. Supposethe risk-free rate is 5 percent, and suppose furtherthe contract requires a payment of $1,000 in fiveyears’ time. The insurer collects $10 plus $1,000 x(1.06)^(-5), or $757, and establishes a liability of$1,000 x (1.05)^(-5) = $784. It would appear, uponissue, that the insurer has suffered a loss of $784 -$757, or $27.

Financial Reporter | March 2006 15

continued on page 16 >>

Financial Reporter | March 2006

Presumably the 6-percent rate isthe rate expected to be earnedon some sort of risky security.Let us assume the risk is adefault risk. The actual rate ofreturn on the security can onlybe known as time passes. Thatis, we do not know uponissuance of the contract if therisky security will default (and

hence yield less than 6 percent) or not default (andhence yield 6 percent).

From an economic perspective, the issuer has suf-fered a loss at issue. This can be demonstrated bycomparing the amount received for the policy to theeconomic cost of issuing the contract. The econom-ic cost of the contract is the cost of completelydefeasing the liability. This defeasement can beaccomplished in two ways, either by selling the riskysecurity and buying a risk-free security that preciselymatches the liability, or by retaining the risky securi-ty and buying credit protection in the market. Underthe first option, the insurer sells the risky security for$747 and buys risk-free instruments for $784, suf-fering a loss of $37 less the load of $10, or $27. Inthe second case, the cost of the credit protection is$37 (the present value of the credit spread), so theloss is again $27 after considering the $10 load.

In summary, I would like to commend Mr. Girardfor adding his thoughts to the ongoing debate.Nevertheless, I remain convinced that the IASB’s useof issuer credit spreads in valuing liabilities is botheconomically incorrect and produces less usefulfinancial statements.

>> Fair Value of Insurance Liabilities: The Continuing Debate

I remained convinced that theIASB’s use of issuer creditspreads in valuing liabilities isboth economically incorrect andproduces less-useful financialstatements.

$

Donald D. Solow, FSA,MAAA, is a director withBNP Paribas in NewYork. He may bereached at [email protected].

16

I n his most recent in a series of insightful articleson the fair valuation of insurance liabilities(December 2005 The Financial Reporter), Luke

Girard identified and introduced the very real con-cept of the regulator’s call option, and ably discussedhow its recognition by insurance accounting systemscan better align stakeholders’ interests and incen-tives. In so arguing, I believe Luke is right on themoney. As often happens when ideas are in the air, Irecently arrived at the very same destination as Lukebut from an entirely different starting point: the newC3 Phase II capital regulations for variable annu-ities. I believe our two perspectives are complemen-tary, and together might identify common groundbetween insurers and regulators where future discus-sions on fair valuation can less contentiously beadvanced. In this short note, I hope to describe myown path to Luke’s discovery, reformulate the issuefrom the currently fashionable perspective of creditrisk theory, and then briefly suggest how that refor-mulation might allow future debate to centeraround technical rather than ideological issues.

While a constructive criticism of the new C3P2regulation is far outside the scope of this note, Ithink it is fair to observe that, beyond the expenseof compliance, its implications for financial man-agement are not obvious. In order to get my ownmind around the essence of C3P2, I tried to iden-tify what sort of financial instrument the new reg-ulation most resembled, and then consideredwhether or not it made economic sense for anannuity writer to initiate hedging activities in reac-tion to its having to issue this instrument. Thereremains no element of surprise in my revealing myown conclusions. From the perspective of manage-ment, C3P2 represents a barrier call option with azero strike price. In respect to a company thatwrites only variable annuities, it gives regulators aknock-in call option for control of the insurer, or atleast raises the call boundary of the existing regula-tory option Luke described in his article. If andwhen the C3P2 framework is extended to otherproduct lines, they will jointly determine a new

dynamic boundary on the regulator’s call on corpo-rate control for all types of insurers.

As Luke correctly noted, the regulator’s option hasreal economic value that reduces the economic valueof the firm to all stakeholders with claims junior tothose of policyholders—most obviously, stockhold-ers, but bondholders as well. That insight enables usto see that, even if C3P2 granted no liability creditsfor clearly defined hedging strategies, stockholdersand bondholders now have an increased interest inseeing that the insurer’s management reduces thevalue of the regulator option. This can be effectedeither through the liability side, by reducing guaran-tees or increasing fees, or on the asset side, throughan investment strategy that includes capital markethedges and conventional indemnity reinsurance. Inthe presence of C3P2, hedging creates its ownreward by partially reversing the newly increasedeconomic value of the regulator’s call option.

From the perspective of policyholders, C3P2 andother minimum asset requirements create a protec-tive covenant that is missing from the capital instru-ments they have purchased from the insurer. Othermore informed and better bargaining purchasers ofcapital instruments routinely insist such covenantsbe placed in their bond debentures. As do other

The Fair Valuation of Insurance Liabilities:The Information Set Perspectiveby Mike Davlin

Financial Reporter | March 2006 17

continued on page 18 >>

Financial Reporter | March 2006

debt covenants, statutory capi-tal standards attempt to mini-mize agency costs by definingan intervention boundary, apoint at which claimants canstep in to protect their inter-ests. I note in passing that anydebt issued by an insurancecompany likely creates an

unrecognized intervention barrier in addition tothat of the regulator’s option. Even the moststaunch proponent of unfettered insurance mar-kets—arguably, the present writer—can admit toboth the presence of agency hazards and, while hemight be inclined to quibble about its form andlevel, to some form of protective covenant for poli-cyholders being both unobjectionable and neces-sary. In the absence of such a covenant, the eco-nomic value of an insurer’s promises to its policy-holders is reduced by possible future states of theworld wherein the insurer’s total assets are exhaust-ed. Management’s tenure lasts until bankruptcy, astopping point before which all claims can be metin full, and after which no claim can be met. In thepresence of a protective covenant, such as C3P2,management’s tenure lasts until default, an earlierstopping point before which all claims can be metin full, and after which all claims can be only bepartially met, but in a way that more equitably allo-cates a smaller and earlier shortfall to a larger groupof claimants.

Whether the stopping time for management’s con-trol is defined by actual bankruptcy or by formula-rized default, it can be modeled in a manner similarto the stochastic analysis required by C3P2. Theexcess of the fair value of policyholder claims in thepresence of a regulator defined default barrier overthe corresponding fair value under a bankruptcy bar-rier is exactly the fair value of the regulator’s option;the fair value transferred to policyholders from otherlower priority stakeholders. By incorporating bank-ruptcy and default scenarios, cash flows can be dis-counted at the risk-free rate, side stepping the nettle-some question of the appropriate transformation ofown credit risk into higher than risk-free discountrates for valuing promised benefits in a different typeof model. In this approach, the shortfalls from bank-ruptcy and default are directly simulated, enablingthe calculation of probability term structures for

hitting each barrier. This sort of modeling isextremely detailed, and both consumes and producesan immense amount of information not normallyvisible to outside observers, such as rating agencies,regulators, and participants in capital markets.

The academic literature on credit risk reflects anongoing debate over the relative superiority of twotypes of models: structural models and reduced formmodels. Structural models, which were first intro-duced by Merton, Black, and Scholes, appraisedefault risk by simulating a firm’s total assets and lia-bilities. Reduced form models, introduced by Jarrowand Turnbull, attempt to directly model default timeas a stochastic process calibrated to publicly availableinformation on the firm, or similar firms. In a 2004working paper, Jarrow and Protter discussed thisdebate over the relative merits of these two models.They made the cogent observation that neithermodel form is uniformly superior; whether one orthe other is to be preferred in a given situationdepends entirely on the information available to themodeler. Jarrow and Turnbull dub their analysis theinformation set perspective. As the modeler’s informa-tion set approaches that of a firm’s manager (or actu-ary!), a structural model is most appropriate. As theinformation set is reduced to that typically availableto rating agencies and regulators, only reduced formmodels remain feasible. For the discussion at hand,the model I described would obviously be a structur-al model with high information requirements. Themodel Luke attributed to rating agencies would be areduced form model, although these agencies haverecently expressed interest in utilizing an insurer’sinternal structural models in their analyses. The cur-rent statutory framework has attributes of both; amyriad of contract details, invisible to the outsideworld, are reflected in simplified models whoseparameters are calibrated to industry, rather thanentity-specific, experience.

The information set perspective recasts a problemLuke discussed—an insurer attempting to boost itsequity in response to a rating downgrade—in asomewhat different light. When a rating agencydowngrades an insurer based upon a reduced formmodel and information set, the affected insurer hastwo options. It can adjust its internal structuralmodel so it is judged to comport with the new rating—an act tantamount to an embarrassing

>> The Fair Valuation of Insurance Liabilities: The Information Set Perspective

The academic literature on credit risk reflects an ongoingdebate over the relative superiority of two types of models: Structural models...andReduced Form Models ...

18

admission that a rating agency with its reduced infor-mation set somehow arrived at a better appraisal ofthe company’s prospects than did its own manage-ment in full possession of an enormous information-al advantage—or construct a logical defense of itsinternal model as it stands. Luke’s concern was witha company electing the first option. From the infor-mation set perspective, insurance company manage-ment should be maintaining as realistic and relevanta structural model as possible, given the informationat hand. It is important to note that, in a structuralmodel such as I described, the term structures ofbankruptcy and default probabilities are calculatedoutputs, not assumed inputs. The same holds true fortheir re-expression as higher yield rates that could beused for discounting promised benefits rather thanbenefits paid in a different structural model. Theonly legitimate way for management to bring theirbankruptcy and default based structural model insynch with the rating agency’s reduced form modelwould be to adjust its assumptions for asset and lia-bility behavior in a manner that increases the result-ant probabilities of bankruptcy and default. Doing sodoes increase the discount rates, which would, insome other model that does not allow for bankrupt-cy or default, equate promised benefits to the fairvalue of policyholder liabilities. But at the same timeit would decrease equity in its internal structuralmodel. This is exactly how it should be; such games-manship as Luke described would be both transpar-ent and subject to deserved ridicule. Credible compa-nies could not jump back and forth between reducedform and structural models as their outcomes suitedthem. I conclude that, under a thoroughly fair valu-ation system such as I described, the most likely out-come of an unexpected rating downgrade would be avigorous defense by management of its internalstructural model; a dialog that would eventually pro-duce a consensus view.

And what of the common ground I promised? Itseems to me that everyone should be able to agreethat the raison d’être of insurance regulators, ratingagencies, FASB and the IASB, is to protect contrac-tual stakeholders; that unlike other stakeholders,policyholders currently lack protective covenants intheir contracts; that when viewed as dynamicallyredefining the boundary of the regulator’s option,C3P2 style minimum asset determinations can be avery efficient and effective way of creating just such

a covenant; that such boundaries increase incentivesto engage in hedging activities; that such boundariesencapsulate superior information sets and conse-quently obviate the need to continue to spend valu-able resources maintaining an informationally infe-rior, quasi-reduced form, statutory valuation model;that standards of absolute realism in a model shouldbe replaced by an evaluation of a model’s realism rel-ative to alternative models and consistently appliedto all models, including the current framework; thatmodels and their associated assumptions should bejudged on the degree to which they advance theinterests of all stakeholders. I believe such a techni-cal discussion would garner far more support forimproved C3P2 style protective covenants, sturdilyundergirded by increasingly detailed structural fairvaluation models.

Financial Reporter | March 2006 19

$

Michael F. Davlin, ASA,is a consulting actuaryin Haymarket, Va. Hemay be reached at [email protected].

Financial Reporter | March 2006

I attended the NAIC Winter Meeting heldDecember 1-5, 2005, in Chicago, including meet-ings of the Life and Health Actuarial Task Force

(LHATF) and selected meetings of the NAIC.Summarized here are the activities, which took placeat these meetings.

LIfe and Health Actuarial Task ForceThe LHATF met on Thursday and Friday and dis-cussed the following topics.

1. C-3 Phase II – Update (AG VACARVM): Theagenda for this meeting was to first receive theAcademy’s comments related to AG VACARVM aswell as its response to certain New York commentletters, review the most recent New York proposaland then receive comments from the ACLI includ-ing a new proposal for a simplified version of thestandard scenario.

a) Academy Comment Letter: This letter respondsto certain comments/proposals contained in twoNew York comment letters dated August 19 andSeptember 22, 2005. The discussion focused onitems impacting 1) the CTE Amount and 2) thestandard scenario.

Comments on Proposal that Impact CTE: Followingare several of the Academy’s comments.

1) CTE 80 vs. CTE 65: New York proposedCTE 80 rather than CTE 65 to offset someof the aggressiveness it sees in the actuarialassumptions. The Academy pointed out thatCTE 65 for reserves had already been decid-ed by LHATF in prior meetings and also thatCTE 80, which is a pretax calculation couldresult in no capital requirement because CTE80 (pre-tax) would be greater than CTE 90(after-tax) in many situations.

2) VAGLBs vs. Non-VAGLBs: The Academyargued that the New York proposal to sepa-rate VAGLBs from non-VAGLBs is inconsis-tent with general risk management aggrega-tion principles by not allowing offsetsbetween different types of benefits.

3) Revenue Sharing: New York wants a state-ment in AG VACARVM that recognition ofrevenue sharing should only be allowed ifthat revenue is contractually guaranteed tothe insurer and its successor. The Academyfeels that the language in AG VACARVM isalready clear.

4) Credibility: New York would like to haveprescribed assumptions where there is noexperience or credibility. The Academy feelsthat the concept of Prudent Best Estimate(PBE) already addresses this issue and thatfocus of work prospectively should be onresearch, literature and studies used to sup-port assumptions where experience is lacking,and highlighting generally accepted practicerather than on prescriptive methodology andassumptions.

Standard Scenario Comments: The Academycomments with respect to the StandardScenario continue to be the same from thestandpoint that there are many different runsrequired, which tend to defeat the purpose ofthe C-3 Phase II modeling process by divert-ing the valuation actuary’s attention from

Highlights of the December 2005 NAICLife and Health Actuarial Task ForceMeeting and Other NAIC Topicsby Ted Schlude

20

evaluating risks in the contracts using a prin-ciples-based approach, to performingmechanical exercises specified by the actuari-al guideline. The Academy would prefer asimplified process for the standard scenario,serving as a benchmark for regulators’ use inreviewing the reasonableness of reserves setusing the principles-based approach. TheAcademy asked that the concept of limitedaggregation be pursued and pointed out thatbecause of the lack of aggregation in the stan-dard scenario, reserves could be greater thanthe capital requirement.

b) New York Proposal: New York next reviewed its most recent modifications submitted in a November 10, 2005 e-mail. Modifications included, among other things:

– Language was added indicating that reserves should “substantially cover the tails.”

– Prudent Best Estimate was strengthened to include a margin above best estimate when full credible data is used.

– Policyholder Behavior: When credible data is available currently but credible experi-ence is not available in later years, a five-year grade from the assumption based on credible data to the worst optimal policy-holder behavior would be required.

The Academy commented that it has not yetreviewed the modifications contained in themost recent New York proposal, but felt thatassuming 100 percent adverse policyholderbehavior was not reasonable.

c) ACLI Presentation: LHATF heard a presentationfrom John Bruins of the ACLI related to AGVACARVM. The ACLI recommended adop-tion of the April 29, 2005 AG VACARVMexposure draft with changes as recommended inthe AAA August 10, 2005 document. TheACLI is 1) opposed to extending from CTE 65to CTE 80 as New York has proposed, 2) doesnot support New York’s recommendation toseparate VAGLBs from other guarantees andtherefore not allowing hedging of differentproduct benefits and 3) is opposed to use of thestandard scenario as a floor and recommended asimplified alternative to the standard scenario ina separate proposal.

The ACLI also recommendedthat AG 39 not be extendedto January 1, 2008, becausethere is no release mechanismin the accumulation ofcharges methodology and noprovision in the reserve torecognize hedging of risks.Their feeling is that focusshould be on moving forwardto get a reasonable version ofAG VACARVM in place by December 31,2006, which could be adjusted as necessarygoing forward.

LHATF exposed for comment the April 29,2005 AG VACARVM, supplemented asdescribed in the AAA August 10, 2005, docu-ment along with the ACLI standard scenariorecommendation. The ACLI will begin to draftlanguage for AG VACARVM with respect to itssimplified standard scenario recommendationfor LHATF to consider.

2. Interim Proposals Relative to New ValuationStandards from ACLI: The ACLI sponsored a proj-ect aimed at alleviating reserve levels for life insur-ance on an interim basis prior to formal adoption ofa principles-based approach to reserves. The interimproposal introduces preferred mortality rates bysplitting the 2001 CSO Table into preferred andresidual standard mortality, introduces the use oflapse rates in the calculation of reserves for UL poli-cies with secondary guarantees, and allows non-pre-mium-paying UL contracts with secondary guaran-tees to use a surrender charge as an offset to the addi-tional reserve calculation. The ACLI proposalincluded a cover letter outlining the proposal, areport from Tillinghast on a Preferred Version of2001 CSO Mortality Table, a draft model regulationimplementing such a Preferred Table and a revisionto AG 38 to allow use of lapse rates subject to certainconstraints for UL policies with secondary guaran-tees. The proposal splits the 2001 CSO Table intothree non-smoker and two smoker tables. For exam-ple, the 2001 NS VBT was split into super-preferred(SP-NS), preferred (P-NS) and residual standard(RS-NS) classes.

Michael Taht, who was closely involved in develop-ing the 2001 CSO Table, provided a presentationrelated to the 2001 CSO Preferred Tables.Regulators also discussed a letter from New Yorkobjecting to various aspects of the ACLI proposal.

The ACLI sponsored a projectaimed at alleviating reserve levelsfor life insurance on an interimbasis prior to formal adoption of aprinciple-based approach toreserves.

Financial Reporter | March 2006 21

continued on page 22 >>

It was noted that mortality haslittle impact on reserves for ULproducts with secondary guar-antees so as a result, the propos-al includes two other elements:1) introduction of lapse rates of2 percent (in years 1-5) and 1percent thereafter subject to cer-tain limitations and 2) a surren-der charge offset to the addi-tional reserve for non-premium

paying UL policies with secondary guarantees.

The ACLI asked that the Tillinghast report, themodel regulation for preferred table use and the revi-sions to AG 38 be exposed for comment at thismeeting to facilitate ongoing discussions related tothe proposal. A separate independent legal review ofthe consistency of these changes with existingStandard Valuation laws is underway, as well.

Regulators felt uncomfortable exposing the docu-ments given they had little time to review them,rather a February conference call will consider thesedocuments in more detail and possibly expose themat that time.

3. Joint SOA-AAA Project Interim Table forPreferred and Standard Mortality: Next, LHATFreceived an update from the SOA, MIB and AAA ondevelopment of preferred tables by the SOA. It wasnoted that this project is not linked to the ACLI pro-posal discussed above, however, it is similar in naturein terms of its goal. The goal of this project is to havea preferred valuation table or factors for use with the2001 CSO Table by April 15, 2007. Various teamshave been formed including a data validation team,an underwriting criteria team, an experience analysisteam, a valuation basic team, an implementationteam and a valuation table team. The goal is to havean experience table by September 30, 2006, a valua-tion table by December 31, 2006 and a regulatorydocument by some time in 2007.

4. Report of Academy SVL II Work Group:Donna Claire gave a presentation related to theAcademy’s Risk Management and FinancialSoundness Committee (also known as the SVL2Steering Committee), its structure, as well as thesubcommittees reporting to it (Capital Adequacy,Experience, Life Valuation and its work groups suchas the Life Reserve Work Group, Variable AnnuityWork Group and Annuity Reserve Work Group).

Focus will be on a principles-based approach asdefined by the Academy, which captures all materialrisks, benefits and guarantees including the tail risks,as well as the revenue to fund the risks. Theapproach would also use risk analysis, stochasticmodels where appropriate, permit recognition ofcompany experience subject to credibility and rele-vance constraints and provide for an appropriatelevel of conservatism through prudent best-estimateassumptions.

Further work will be done in all areas including peerreview, format standards for reviewers and regula-tors, standard definitions of terms, use of judgmentand the system of governance.

The ACLI noted that it has formed a committee oflawyers and actuaries to begin to put a new valuationlaw together for consideration by LHATF in March2006.

Finally, New York made a motion, which was adopt-ed, to continue pursing its proposed valuation lawchanges via a small subgroup of LHATF members.The ACLI indicated that there were still significantindustry concerns with the New York document.

5. Life Reserve Work Group (formerly ULWG):LHATF heard two presentations from the Academyrelated to the Life Reserve Work Group (LRWG).The first presentation by David Neve outlined anAcademy proposal for a principles-based valuationstandard for Life Products, which had been submit-ted to LHATF previously.

The Academy requested that LHATF expose thisdocument, which includes:

a) A draft model regulation, which outlinesbasic principles

b) AG PBR, which defines prudent best esti-mate valuation assumptions

c) AG DIS,which provides a documentationand disclosure framework

d) AG MAR, which deals with margins to bereflected in assumptions

The above proposal assumes that the StandardValuation Law has been changed to a principles-based approach and that an acceptable governanceprocess is in place.

Focus will be on a principles-based approach as defined bythe Academy, which captures allmaterial risks, benefits and guarantees including the tailrisks, as well as the revenue tofund the risks.

Financial Reporter | March 2006

>> Highlights of the December 2005 NAIC Life and Health Actuarial Task Force Meeting and Other NAIC Topics

22

Additional changes to the proposal include:

a) Scope is expanded to all life products.

b) The mortality assumption would define anNAIC approved valuation table that bestmaps to the actuary’s prudent best estimateassumption.

c) A company’s own interest rate generatorcould be used if calibration standards were met.

d) Aggregation of policies would be allowed,but limited by a deterministic reserve.

e) A methodology for earned and discount rateswould be defined.

f ) Deterministic reserve approach is permittedprovided it is demonstrated by the actuary to besufficient.

g) Non-guaranteed elements would change toreflect changing conditions under different sce-narios in the models.

h) Documentation and disclosure requirementsare expanded in AG DIS.

i) Other areas being considered include: sepa-rate account revenue sharing, stochastic reserveallocation to individual policies, quantificationof the aggregate margin resulting from allassumptions (including disclosure) and model-ing of hedges.

The goal of the Academy is to have a form for adop-tion by LHATF by December 2006 and to roll thenew methodology out on a state-by-state basis in 2007.LHATF exposed the Academy proposal for comment.