Embed Size (px)

Citation preview

l3^o

THIRTY-SIXTH JUDICIAL DISTRICT ATTORNEY PARISH OF BEAUREGARD

STATE OF LOUISIANA

ANNUAL FINANCIAL STATEMENTS WITH AUDITOR'S REPORT

DECEMBER 31, 2008

^'nder provisions of state law, this report is a pubiic document. Acopy ofthe report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office ofthe Legislative Auditor and, where appropriate, at the office of the parish clerk of court.

Release Date

Table of Contents

INDEPENDENT AUDITOR'S REPORT

BASIC FINANCIAL STATEMENTS: Statement of Net Assets Statement of Activities Balance Sheet - Govemmental Funds Reconciliation ofthe Govemmental Funds Balance Sheet to Statement of Net Assets

Statement of Revenues, Expenditures and Changes in Fund Balances - Govemmental Funds

Reconciliation ofthe Statement of Revenues, Expenditures and Changes In Fund Balance of Govemmental Funds to the Statement of Activities

Statement of Fiduciary Net Assets - Agency Funds

Statement

-

A B C

Page(s)

1-2

4 5 6

9 10

Notes to the Financial Statements

Required Supplemental Information General Fund - Schedule of Revenues, Expenditures

and Changes in Fund Balances - Budget and Actual Special Revenue Fund - Title IV-D Fund -Schedule of Revenues, Expenditures and Changes in Fund Balances - Budget and Actual

Special Revenue Fund - Worthless Check Fund -Schedule of Revenues, Expenditures and Changes in Fund Balances - Budget and Actual

Truancy Assessment Fund - Schedule of Revenues, Expenditures and Changes in Fund Balances ~ Budget and Actual

Schedule 12-20

Page(s)

22

23

24

25

Other Supplemental Schedules Schedule of Fiduciary Net Assets - Agency Funds 27

Other Reports Schedule of Prior Year Audit Findings 29

Report on Intemal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Governmenl Auditing Standards 30-31

John A. Windham, CPA A Professional Corporation

1620 North Pine Street John A. Windham, CPA DeRidder, LA 70634 Tel: (337) 462-3211 Fax: (337) 462-0640

INDEPENDENT AUDITOR'S REPORT

The Honorable David Burton Thirty-Sixth Judicial District Attomey Parish of Beauregard State of Louisiana

I have audited the accompanying financial statements ofthe govemmental activities, each major fund, and the aggregate remaining fund information ofthe Thirty-Sixth Judicial District Attomey, as of and for the year ended December 31,2008, which collectively comprise the District Attomey's basic financial statements as listed in the table of contents. These financial statements are the responsibility ofthe Thirty-Sixth Judicial District Attomey's management. My responsibility is to express opinions on these financial statements based on my audit.

1 conducted my audit in accordance with auditing standards generally accepted in the United States of America, and the standards applicable to financial audits contained in Govemment Auditing Standards, issued by the Comptroller General of the United States. Those standards require that I plan and perform the audit to obtain reasonable assurance about whether the financial statements are fi-ee of material misstatement An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. I believe that my audit provides a reasonable basis for my opinions.

In my opinion, the financial statements referred lo above present fairly, in all material respects, the respective financial position ofthe governmental activities, each major fund and the aggregate remaining ftind information ofthe Thirty-Sixth Judicial District Attorney, as of December 31,2008, and the respective changes in financial position, thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, I have also issued my report dated June 22, 2009 on my consideration of the Thirty-Sixth Judicial District Attomey's internal control over financial reporting and my tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is to describe the scope of my testing of intemal control over financial reporting and compliance and the results of that testing and not to provide an opinion on the intemal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of my audit.

The Thirty-Sixth Judicial District Attomey. has not presented management's discussion and analysis that accounting principles generally accepted in the United States has determined is necessary to supplement, although not required to be part of, the basic financial statements.

The budgetary comparison information on pages 22 through 25, is not a required part ofthe basic financial statements but is supplementary information required by accounting principles generally accepted in the United States of America. ! have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation ofthe required supplementary information. However, I did not audit the information and express no opinion on it.

The Honorable David Burton Thirty-Sixth Judicial District Attomey Parish of Beauregard State of Louisiana Page 2

My audit was conducted for the purpose of forming opinions on the fmancial statements that collectively comprise the Thirty-Sixth Judicial District Attomey's basic financial statements. The schedule of fiduciary net assets and prior year audit findings is presented for purposes of additional analysis and is not a required part ofthe basic financial statements. The schedule of fiduciary net assets and schedule of prior year audit findings have not been subjected to the auditing procedures applied in the audit ofthe basic financial statements and, accordingly I express no opinion on the schedules.

Mitt- Ul<*^, cffi DeRidder, Louisiana June 22, 2009

BASIC FINANCIAL STATEMENTS

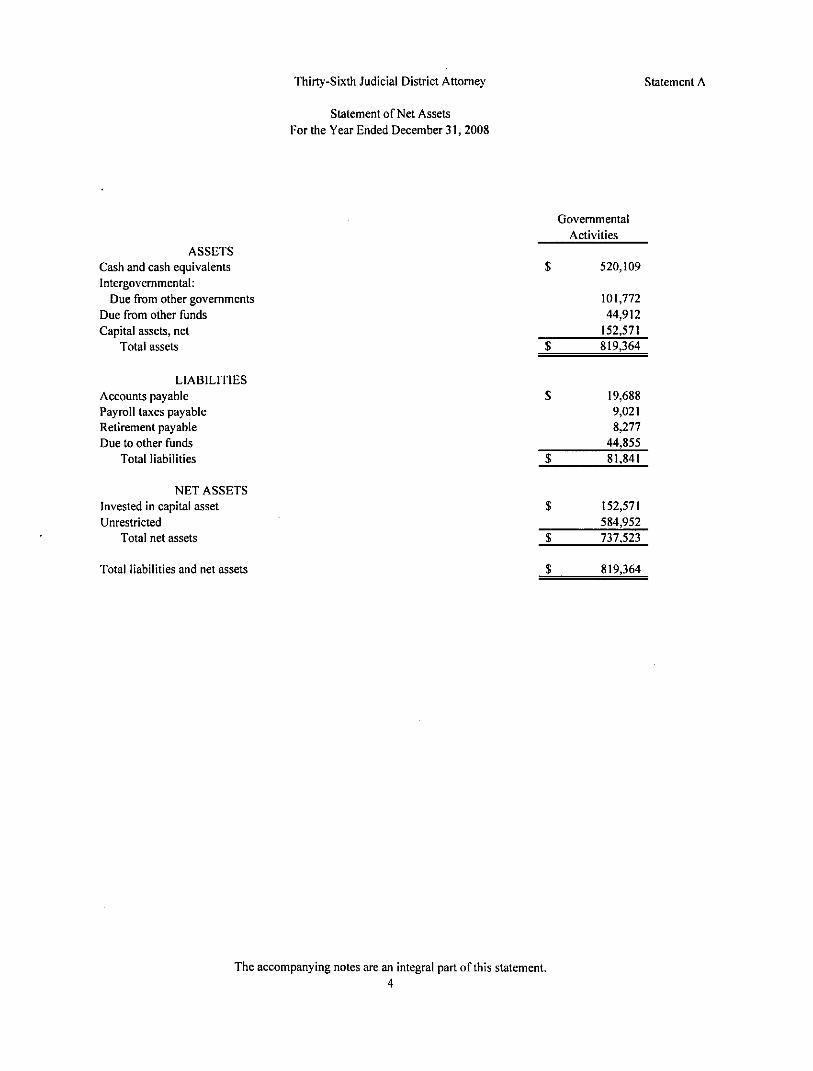

Thirty-Sixth Judicial District Attomey Statement A

Statement of Net Assets For the Year Ended December 31, 2008

Govemmental Activities

ASSETS Cash and cash equivalents $ 520,109 Intergovemmental:

Due from other govemments 101,772 Due from other funds 44,912 Capital assets, net 152,571

Total assets $ 819,364

LIABILITIES Accounts payable $ 19,688 Payroll taxes payable 9,021 Retirement payable 8,277 Due to other funds 44,855

Total liabilities $ 81,841

NET ASSETS Invested in capital asset $ 152,571 Unrestricted 584,952

Total net assets $ 737,523

Total liabilities and net assets $ 819,364

The accompanying notes are an integral part of this statement. 4

Thirty-Sixth Judical District Attomey

Statement of Activities For the Year Ended December 31, 2008

Statement B

Program Revenues

Program activities General govemment

Judiciary

Expenses

774,938

Fees, Fines and Charges for

Services

$ 407,082

Operating Grants and

Contributions

J 316,041

General revenues: Investment eamings Rental Miscellaneous

Total general revenues and transfers Change in net assets

Net assets at beginning of year Net assets at end of year

Net (Expenses) Revenues and Changes in Net Assets Governmental Activities

_$ (51.815)

12,411 4,500

772 17,683

(34,132) 771,655 737,523

The accompanying notes are an integral part ofthe statement. 5

£ > O

o S t2

iri —

r~-r -— o

1 ^

Tf

r*l

r-\r>

b<)

oo — r-- u-i 00 <N r- u-i ^0 CS (N 00 oC oT 00 T '

r^ 00 (N fO O U l

M

O o <l

— 00

*N t r t Ov T T 00 l o

f A

f n 0^ r -

>« VC ^O

M

.2

11 « ,= S .5 — u

5 S I i Is C c

ra g w

>•

•s

o

o O o o

f A

fM SO

( A

ON

(

s©

699

^

SO so Tf

1*1 o l l-l r-j •V

(*) V i r j M-

b<»

<N r -^ M

r -• *

V )

o SO '

o

V i

OS

(S OS Os'

b ^

O r-rn

V i

ro SO

ro r r (N

r-r-<N • ^

ro

Vi

o> 00 r- o —• — r- oo O^ <N (N -^^ •o m ' 00 fN

r o 00 <N r o

U-.

6 ^

t -

»N

fO >o

f A

Cfl

E -tZl

<

m ra

B < a.

.O TD a c ra '—

i s « 3 a: Q

1 2 t2

i/i

8 g

-w

u<

_c

T3

- 3 •a «

s o O

. 2 U'

| 1 > S

"3 s

C/5

« . c T3

c«

in u

I D .2

3 H

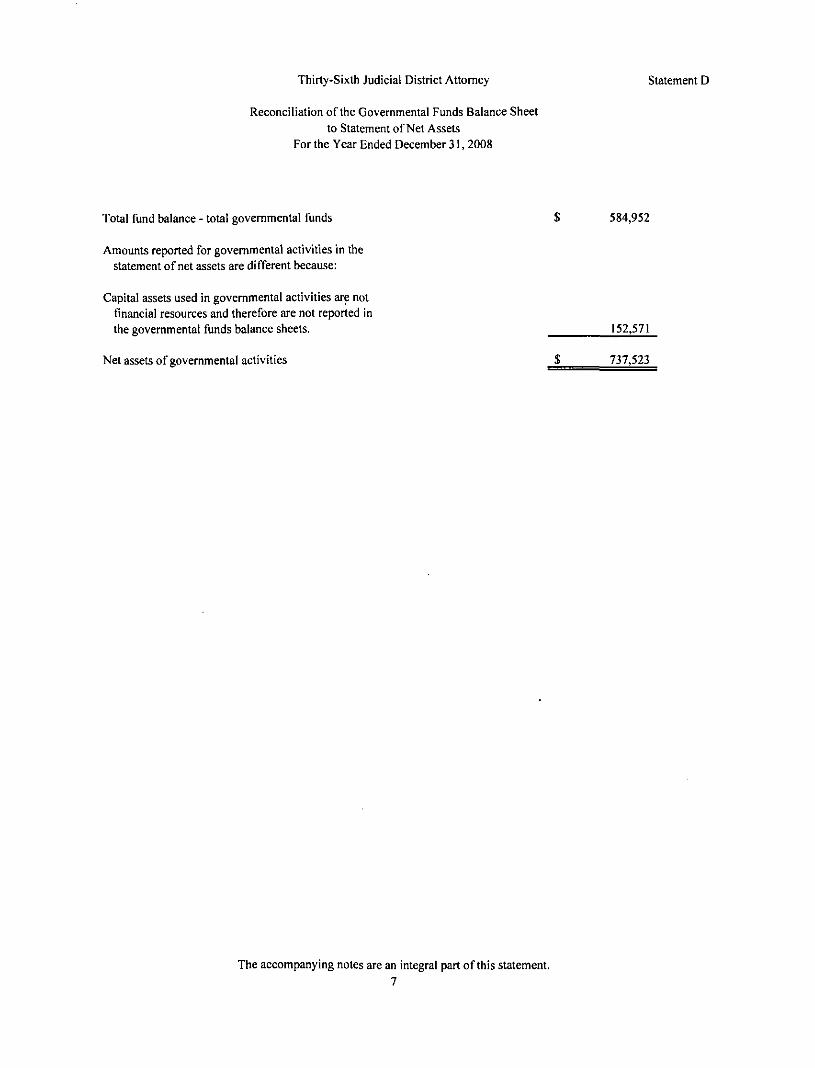

Thirty-Sixth Judicial District Attomey Statement D

Reconciliation ofthe Govemmental Funds Balance Sheet to Statement of Net Assets

For the Year Ended December 31, 2008

Total fund balance - total govemmental funds $ 584,952

Amounts reported for govemmental activities in the statement of net assets are different because:

Capital assets used in govemmental activities are not financial resources and therefore are not reported in the govemmental funds balance sheets. 152,571

Net assets of govemmental activities _$ 737,523

The accompanying notes are an integral part of this statement. 7

c u

B

B

B c u B E > O O

>n r~ Os (N r * r o — C> O l 0 0 fO t o "O — r o

I N 0 0

c-> r^ C5 • *

1

. — 1

•<t

<N

^

<N l~-<N

WI

< 1 (T) 0 0

O • ^

(>4

• * — OO • * Tj-0 0 ( N o o ( N r o 00 O ON oo_ r-; Tj-'- s o s o " f o ' o o ( N r ^ V I ^ ON

W

• ^

so OS

^^

r^ Os l O

• ^

ON

m

( N

"n OS

• *

OO

>n

a CQ • O c 3

r o

— u 2

M OJ 00

c

c .c

" — o

3 S -o 1 F -^

C L > w-i >< o !a w a s

> •

•s o

u c > ft;

c

I 55

c

b tn C S "I 3

H in

o

Os "n ly-i r o 00 ON oo r o TT fN (N fO —' — t - '

fO

( N

i n oo ^ r o •* o

00 — »o 1> m IT) ON OS r-^ —„ f^„ —, fo" s o W^ so' ^ <N fN

o ( N

0 0

OS o • * so^ • *

at

c

i n !>• (N r-— 0^ 00 m

—

r * f O s n T t V I r o

O

o I N

.—, ^ 1

( N r-~ ( N m

v ~

I N r o no VN

i A

00

w>

O • * CN Os fN — t - • * Os O t v r~ Os <N r-J t~-' o * 0 SO liO r o —' (N — m r o —

00 rs

ro rM !Ts

o so

fO

o VN

CN

^

Vi

" r , r -s n r -r*!

CN OS

OS r o

&<»

Os Os ON

> / i f^

f O 0 0 ( N

O VN

( A

o

a. "rt i -0 0

o c 00 .H '?. a. E

00

a. o o

c «-5^ C

^ § £ i2 ^ .D

- 1 . 1 & - ^ i i s ^ £i 1 1 1 £ 3 « 4> O £ c t- S

Vi H Vi c c y ^ ^

fti

I g 3 ^ S 23 I B I

c:

I B CL

> ^ -a

y - =

W

ra c g

(4* U

11

2 o, §• H O 00

Vi u

S 2 o ^

o

.£1

-o s

3 on

u J Z

u * - l

^

s V

>". tfc-O 0 0

c c: PO

^ ^ H S

• ra

X i •T3

c 3 U .

V

( M

o T i

ra u

s ra X I

• o

3 U .

Thirty-Sixth Judicial District Attomey Statement F

Reconciliation ofthe Statement of Revenues, Expenditures and Changes in Fund Balance ofGovemmental Funds to the

Statement of Activities For the Year Ended December 31,2008

Net change in fund balances - total govemmental funds $ (9,645)

Amounts reported for govemmental activities in the statement of activities are different because:

Depreciation expense on capital assets is reported in the govemment-wide statement of activities and changes in net assets, but they do not require the use of current financial resources. Therefore, depreciation expense is not reported as an expenditure in governmental funds. (24,487)

Change in net assets of govemmental activities _$ (34,132)

The accompanying notes are an integral part of this statement. 9

Thirty-Sixth Judicial District Attomey Statement G

Statement of Fiduciary Net Assets Agency Funds

For the Year Ended December 31, 2008

Agency Funds Assets

Cash and cash equivalents $ 251 Due from others 6

Total assets $ 257

Liabilities Due to other funds $ 57 Due to others 200

Total liabilities $ . 257

The accompanying notes are an integral part of this statement. 10

NOTES TO THE FINANCIAL STATEMENTS

II

Thirty-Sixth Judicial District Attomey

Notes to the Financial Statements As of and for the Year Ended December 31, 2008

INTRODUCTION

As provided by Article V, Section 26 ofthe Louisiana Constitution of 1974, the District Attomey has charge of every criminal prosecution by the state in his district, is the representative ofthe state before the grand jury in his district, and is the legal advisor to the grand jury. He performs other duties as provided by law. The district attomey is elected by the qualified electors of the judicial district for a term of six years. His office is staffed by four assistant district attomeys, an investigator and six secretarial/clerical employees. The Thirty-Sixth Judicial District comprises all ofthe Parish of Beauregard, State of Louisiana, and is located in the southwestem region ofthe state.

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. BASIS OF PRESENTATION

The accompanying basic financial statements ofthe Thirty-Sixth Judicial District Attomey have been prepared in conformity with govemmental accounting principles generally accepted in the United States of America. The Govemmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing govemmental accounting and financial reporting principles. The accompanying basic financial statements have been prepared in conformity with GASB 34, Basic Financial Statements for State and Local Governments, issued in June 1999.

B. REPORTING ENTITV

Section 2100 ofthe GASB Codification ofGovemmental Accounting and Financial Reporting Standards (GASB Codification) established criteria for determining the governmental reporting enfity and component units that should be included within the reporting entity. For financial reporting purposes, in conformance with GASB Codification Section 2100, the district attomey includes all fiinds, account groups and activities that are controlled by the district attomey as an independently elected parish official. As an independently elected parish official, the district attomey is solely responsible for the retention of employees, authority over budgefing, the responsibility for deficits, and the receipt and disbursement of ftinds. Other than certain operating expenditures ofthe district attorney's office that are paid by the parish police jury as required by Louisiana law, the district attomey's office is financially independent. Accordingly, the district attomey is a separate govemmental reporting entity. Certain units of local govemment over which the district attomey exercises no oversight responsibility, such as the parish police jury, parish school board, other independently elected parish officials, and municipalities within the parish, are excluded from the accompanying financial statements. These units of govemment are considered separate reporting entities and issue financial statements separate fi-om those ofthe parish district attomey.

C. FUND ACCOUNTING

The district attomey uses funds to maintain its financial records during the year. Fund accounfing is designed to demonstrate legal compliance and to aid management by segregating transactions relating to certain district attomey fiinctions and activities. A ftind is defined as a separate fiscal accounting entity with a self-balancing set of accounts.

Govemmental Funds

Governmental ftinds account for all or most ofthe district attomey's general activities. These funds focus on the sources, uses, and balances of current financial resources. Expendable assets are assigned to the various govemmental ftinds according to the purposes for which they may be used. Current liabilities are assigned to the ftind from which they will be paid. The difference between a govemmental ftind's assets and liabilities is reported as ftind balance. In general, ftind balance represents the accumulated expendable resources, which may be used to finance ftiture period programs or operations ofthe district attomey. The following are the district attomey's govemmental ftinds:

12

Thirty-Sixth Judicial District Attomey

Notes to the Financial Statements (Continued)

General Fund - the primary operafing fund ofthe district attomey and it accounts for all financial resources, except those required to be accounted for in other funds. The General Fund is available for any purpose provided it is expended or transferred in accordance with state and federal laws and according to the district attomey's policy.

Special Revenue Funds

Title IV-D Fund - The Title IV-D Fund consists of reimbursement grants from the Louisiana Department of Social Services, authorized by Act 117 of 1975, to establish family and child support programs compatible with TiUe IV-D ofthe social security act. The purpose ofthe ftind is to enforce the support obligafion owed by absent parents to their families and children, to locate absent parents, to establish patemity, and to obtain family and child support.

Worthless Check Fund - The Worthless Check Collection Fee Fund consists of fees collected in accordance with Louisiana Revised Statute 16:15, which provides for a specific fee whenever the district attomey's office collects and processes a worthless check. Expenditures from this ftind are at the sole discretion ofthe district attomey and may be used to defray the salaries and the expenses ofthe office ofthe district attomey, but may not be used to supplement the salary ofthe district attorney.

Tmancy Assessment Fund - The Truancy Assessment and Service Center Project will prevent and reduce the incidence of out-of-wedlock births by identifying children at risk of school failure due to excessive and unexcused absences and providing services to these children and their families. Tmancy has been identified as a risk factor that contributes to the incidence of out-of-wedlock births. The purpose ofthe tmancy assessment assessment centers is to provide for the early identification and assessment of tmants and the prompt delivery of coordinated interventions to prevent continued unauthorized school absences.

Fiduciary Funds - Fiduciary fund reporting focuses on net assets and change in net assets. The only funds accounted for in this category by the district attomey are agency funds. The agency fiands account for assets held by the district attomey as an agent for various taxing bodies (tax collections) and for deposits held pending court action. These funds are custodial in nature (assets equal liabilifies) and do not involve measurement of results of operafions. Consequently, the agency funds have no measurement focus, but use the modified accmal basis of accounting. The following are the district attomey's fiduciary fiinds.

Agency Funds

Asset Forfeiture Tmst Fund - The Asset Forfeiture Tmst Fund was established under the provisions of LSA-R.S. 40:2616(8) which requires that all monies collected fi'om the sale of seized or forfeited assets be deposited into the fiind. The district attomey administers the distribution of monies to the appropriate local, state or federal law enforcement agency that participated in the activity that led to the seizure or forfeiture of the property or deposit of monies under and subject to LSA-R.S. 40:2616 (B).

Bail Bond Collection Tmst Fund - The Bail Bond Collection Trust Fund was established in compliance with revised statute 15:571.n. The District Attomey collects on a judgment of bond forfeiture and distributes the proceeds according to this stattite. Thirty percent of all funds collected shall be disbursed to the district attomey's general fund, twenty-five percent of all funds collected shall be disbursed to the parish's criminal court fund, twenty-five percent shall be disbursed to the sheriffs general fund and the remaining twenty percent shall be disbursed to the Indigent Defender Program. All funds shall be disbursed to the parish where the bonds were posted.

D. MEASUREMENT FOCUS/BASIS OF ACCOUNTING

Fund Financial Statements (FFS)

The amounts reflected in the General Fund and Other Funds, of Statements C and E, are accounted for using a current financial resources measurement focus. With this measurement focus, only current assets and current liabilities are generally included on the balance sheet. The statement of revenues, expenditures, and changes in fund balances reports on the sources (i.e., revenues and other financing sources) and uses (i.e., expenditures and other financing uses) of current financial resources. This approach is then reconciled, through adjustment, to a govemment-wide view of district attomey operations.

13

Thirty-Sixth Judicial District Attomey

Notes to the Financial Statements (Confinued)

The amounts reflected in the General Fund and Other Funds, of Statements C and E, use the modified accmal basis of accounting. Under the modified accmal basis of accounting, revenues are recognized when susceptible to accmal (i.e., when they become both measurable and available). Measurable means that amount ofthe transaction can be determined and available means collecfible within the current period or soon enough thereafter to pay liabilities of the current period. The district attomey considers all revenues available if they are collected within 60 days after the fiscal year end. Expenditures are recorded when the related fund liability is incurred, except for interest and principal payments on general long-term debt which is recognized when due and certain compensated absences and claims and judgments which are recognized when the obligafions are expected to be liquidated with expendable available financial resources. The govemmental funds use the following practices in recording revenues and expenditures;

Revenues Commissions on fines and bond forfeitures are recorded in the year in which they are collected by the parish tax collector.

Reimbursements are recorded when the district attomey is entitled to the funds.

Interest income on investments is recorded when the investments have matured and the income is available.

Substantially all other revenues are recorded when received.

Expenditures Expenditures are generally recognized under the modified accmal basis of accounting when the related fund liability is incurred.

Other Financing Sources fUses) Transfers between funds that are not expected to be repaid (and any other financing source/use) are accounted for as other financing sources (uses). These sources (uses) are recorded when the expenditure is incurred.

Government-Wide Financial Statements (GWFS)

The column labeled Statement of Net Assets (Statement A) and the column labeled Statement of Activities (Statement B) display informafion about the district attomey as a whole. These statements include all the financial activifies ofthe district attomey. Information contained in these columns reflect the economic resources measurement focus and the accrual basis of accounting. Revenues, expenses, gains, losses, assets and liabilities resuhing from exchange or exchange-like transactions are recognized when the exchange occurs (regardless of when cash is received or disbursed). Revenues, expenses, gains, losses, assets and liabilities resulting from nonexchange transactions are recognized in accordance with the requirements of GASB Statement No. 33, Accounting and Financial Reporting for Nonexchange Transactions.

Program Revenues - Program revenues included in the column labeled Statement of Activities (Statement B) are derived directly from disttict attorney users as a fee for services; program revenues reduce the cost ofthe function to be financed from the disttict attomey's general fund.

E. BUDGET

The district attomey uses the following budget pracfices:

The budgets ofthe District Attomey ofthe Thirty-Sixth Judicial Disttict, are adopted in accordance with Louisiana Revised Statutes 39:1301-1314. Annually the district attomey adopts a budget for the General and Special Revenue Funds. The budgetary pracfices include public notice ofthe proposed budget, public inspection ofthe proposed budget, and public hearings on the budget. Formal budgetary integration is employed as a management control device during the year. Budgeted amounts included in the accompanying financial statements include original adopted budget amounts and all subsequent amendments. The budget for the General and Special Revenue Funds is adopted on a basis consistent with generally accepted accounting principles (GAAP).

14

Thirty-Sixth Judicial Disttict Attomey

Notes to the Financial Statements (Continued)

F. CASH AND CASH EQUIVALENTS

Cash includes amounts in demand deposits, interest bearing demand deposits, money market accounts and time deposits. Cash equivalents include amounts in time deposits and those other investments with original maturities of 90 days or less. Under state law, the district attomey may deposit ftinds in demand deposits, interest bearing demand deposits, money market accounts, or fime deposits with state banks organized under Louisiana law or any other state ofthe United States, or under the laws ofthe United States.

Under state law, the district attomey may invest in United States bonds, tteasury notes, or certificates. These are classified as investments, if their original maturities are 90 days or less, they are classified as cash equivalents. Investments are stated at cost. At December 31,2008 the district attomey had no investments.

G. SHORT-TERM INTERFUND RECEIVABLES/PAYABLES

During the course of operafions, numerous ttansacfions occur between individual funds for goods provided or services rendered. These receivables and payables are classified as due from other funds or due to other funds on

• the balance sheet. Short-term interfund loans are classified as interfiind receivables/payables.

H. CAPITAL ASSETS

Capital assets are capitalized at historical cost or estimated cost if historical cost is not available. Donated assets are recorded as capital assets at their estimated fair market value at the date of donafion. The district attomey maintains a threshold level of $5,000 or more for capitalizing capital assets.

Capital assets are recorded in the Statement of Net Assets and Statement of Activities. Since surplus assets are sold for an immaterial amount when declared as no longer needed for public purposes, no salvage value is taken into consideration for depreciation purposes. All capital assets, other than land, are depreciated using the straight-line method over the following usefiil lives:

Description Estimated Lives Improvements 20 years

Fumiture and equipment 5-15 years

I. COMPENSATED ABSENCES

The district attomey has the following policy relating to vacation and sick leave: Employees ofthe disttict attomey eam vacation leave at varying rates, depending on length of service, which does not accumulate. Upon resignation, unused vacation leave is paid to the employee at his current rate of pay.

Employees eam sick leave at the rate of one day a month, effective immediately upon employment. Ten days a year, not to exceed 30 days, may be accumulated. Unused sick leave lapses upon termination of employment.

At December 31, 2008 the disttict attomey had no accumulated and vested leave benefits required to be reported in accordance with NCGA Statement 4 and Statement of Financial Accounting Standard (SFAS) 43.

J. FUND EQUITY

In the fund financial statements, govemmental fiinds report reservafions of fiind balance for amounts that are not available for appropriation or are legally restricted by outside parties for use for a specific purpose. Any designations of fiind balance represent tentative management plans that are subject to change.

K. EXTRAORDINARY AND SPECIAL ITEMS

Extraordinary items are ttansactions or events that are both unusual in nature and infrequent in occurrence. Special items are ttansacfions or events within the control ofthe disttict attomey, which are either unusual in nature or infrequent in occurrence. The district attomey had no exttaordinary or special items as of December 31,2008.

15

Thirty-Sixth Judicial Disttict Attomey

Notes to the Financial Statements (Confinued)

L. INTERFUND TRANSACTIONS

Transacfions that constitute reimbursements to a fund for expenditures initially made from it that are properly applicable to another fund are recorded as expenditures in the reimbursing fund and as reducfions of expenditures in the fund that is reimbursed. Nonrecurring or non-roufine permanent ttansfers of equity are reported as residual equity transfers. All other interfund transactions are reported as transfers.

M. ESTIMATES

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America require management to make esfimates and assumptions that affect the reported amounts of assets and liabilifies and disclosure of contingent assets and liabiiities at the date ofthe financial statements and the reported amounts of revenues, expenditures, and expenses during the reporting period. Actual results could differ from these estimates.

CASH AND CASH EQUIVALENTS

At December 31, 2008, the disttict attomey has cash and cash equivalents (book balances) totaling $520,109 as follows:

Interest bearing demand deposits Demand deposits Time deposits

Total

67,008 302

452,799 $ 520,109

These deposits are stated at cost, which approximates market. Under state law, these deposits (or the resulfing bank balances) must be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent bank. The market value ofthe pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent. These securities are held in the name ofthe pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties.

At December 31,2008, the disttict attomey has $537,592 in deposits (collected bank balances). These deposits are secured from risk by $537,592 of federal deposit insurance.

DEFICIT FUND EQUITY

The following individual fiind had a deficit in it's unreserved fiind balance (net assets) at December 31,2008.

Fund Tmancy Assessment Fund

1 Deficit Amount | 1 $ 26 1

The Tmancy Assessment Fund began September 1, 2008. As of December 31, 2008 the district attomey's office had not been reimbursed by the state for the fiind expenditures. The Disttict Attomey believes that when the reimbursements are received they will be suf^cient to cover the cost ofthe program.

EXCESS OF EXPENDITURES OVER APPROPRIATIONS

The following individual funds had actual expenditures over budgeted appropriations for the year ended December 31,2008:

Fund Worthless Check Fund Tmancy Assessment Fund

Original Budget

$ 55,100 41,200

_

Final Budget

$ 71,200 40,333

™ Actual

$ 71,903 40,402

~

Unfavorable Variance

$ 703 69

16

Thirty-Sixth Judicial District Attomey

Notes to the Financial Statements (Confinued)

RECEIVABLES

The receivables of $101,772 at December 31, 2008, are as follows:

Special Revenue Funds

Class of receivable Intergovemmental

General Fund Title IV-D Fund

Truancy Assessment

Fund Total 46,730 $ 14,690 $ 40,352 $ 101,772

INTERFUND RECEIVABLES/PAYABLES

The following due to/from balances exist due to payments made out of one fiind that relate to the other fiind. The balance in each respective due to/from account is expected to be paid within the current year.

Due from Due lo General fund Title IV-D ftind Worthless check fund Truancy assessment fund Agency funds

Total

$

$

42,432 -

2,480 --

44,912

$

$

2,480 375 -

42,000 57

44,912

CAPITAL ASSETS

Capital assets and depreciation activity as of and for the year ended December 31, 2008, for the district attomey is as follows:

Govemmental activities: Capital assets being depreciated

Improvements Equipment and furniture

Total capital assets being depreciated

Less accumulated depreciation for: Improvements Equipment and furniture

Total accumulated depreciation

Total capital assets being depreciated, net

Beginning Balance

$ 90,943 272,035 362,978

56,839 129,081 185,920

$ 177,058

$

$

Increase

-

-

4,547 19,940 24,487

(24,487)

$

$

Decrease

-

-

-

-

.

S

$

Ending Balance

90,943 272,035 362,978

61,386 149,021 210,407

152,571

Depreciation expense of $24,487 for the year ended December 31,2008, was charged to the following govemmental fiincttons:

Judicial 24,487

17

Thirty-Sixth Judicial District Attomey

Notes to the Financial Statements (Continued)

7. ACCOUNTS, AND OTHER PAYABLES

The payables of $36,986 at December 31,2008, are as follows:

8.

Accounts Retirement Payroll taxes

Total

PENSION PLAN

General Fund $ 15,019

8,277 5,218

$ 28,514

TiUe IV-D Fund $

3,803 S 3,803

Worthless Check Fund

$ 4,669

$ 4,669

$

$

Total 19,688 8,277 9,021

36,986

The disttict attomey and assistant district attorneys are members ofthe Louisiana District Attomeys Retirement System (System), a cost sharing multiple-employer defined benefit pension plan administered by a separate board of tmstees.

Assistant disttict attorneys who eam, as a minimum, the amounts paid by the state for assistant district attomeys and are under the age of 60 at the fime of original employment and all district attomeys are required to participate in the System. For members who joined the System before July 1, 1990, and who elected not to be covered by the new provisions, the following applies: Any member with 23 or more years of creditable service regardless of age may retire with a 3 percent benefit reduction for each year below age 55, provided that no reduction is applied if the member has 30 or more years of service. Any member with at least 18 years of service may retire at age 55 with a 3 percent benefit reducfion for each year below age 60. In addifion, any member with at least 10 years of service may rettre at age 60 with a 3 percent benefit reduction for each year refiring below the age of 62. The retirement benefit is equal to 3 percent ofthe member's average final compensation multiplied by the number of years of his membership service, not to exceed 100 percent of his average final compensation.

For members who joined the System after July 1,1990, or who elected to be covered by the new provisions, the following applies; Members are eligible to receive normal retirement benefits if they are age 60 and have 10 years of service credit, are age 55 and have 24 years of service credit, or have 30 years of service credit regardless of age. The normal retirement benefit is equal to 3.5 percent ofthe member's final-average compensation muhiplied by years of membership service. A member is eligible for early retirement if he is age 55 and has 18 years of service credit. The early retirement benefit is equal to the normal retirement benefit reduced 3 percent for each year the member retires in advance of normal retirement age. Benefits may not exceed 100 percent of average final compensafion. The System also provides death and disability benefits. Benefits are established by state statute.

The System issues an annual publicly available financial report that includes financial statements and required supplementary information for the System. That report may be obtained by wrifing to the Louisiana District Attomeys Retirement System, 2109 Decattir Street, New Orleans. Louisiana 70116-2091. or by calling (504) 947-5551.

FUNDING POLICY Plan members are required by state statute to contribute 7.0 percent of their annual covered salary. As of June 30, 2007 the district attorney is no longer required to contribute to the plan. Contributions to the System also include .2 percent ofthe ad valorem taxes collected throughout the state and revenue sharing fiinds as appropriated by the legislature. The contribution requirements of plan members and the district attomey are established and may be amended by state statute. As provided by Louisiana Revised Statute 11:103, the employer contributions are determined by actuarial valuation and are subject to change each year based on the results ofthe valuafion for the prior fiscal year. The district attomey's contt-ibutions to the System for the years ending December 31,2008,2007, and 2006 were $0, $2,997, and $6,962, respecfively equal to the required contributions for each year.

Substanfially alt other employees ofthe District Attomey ofthe Thirty-Sixth Judicial District, Parish of Beauregard, State of Louisiana are members ofthe Parochial Employees' Retirement System of Louisiana (System), a cost sharing, multiple-employer defined benefit pension plan administered by a separate board of tmstees. The System is composed of two distinct plans. Plan A and Plan B, with separate assets and benefit provisions. All employees of the district are members of Plan A.

18

Thirty-Sixth Judicial District Attomey

Notes to the Financial Statements (Confinued)

All permanent employees working at least 28 hours per week who are paid wholly or in part from parish fiinds and all elected parish officials are eligible to participate in the System. Under Plan A. employees who retire at or after age 60 with at least 10 years of creditable service, at or after age 55 with at least 25 years of creditable service, or at any age with at least 30 years of creditable service are entitled to a refirement benefit, payable monthly for life, equal to 3% of their final-average salary for each year of creditable service. However, for those employees who were members ofthe supplemental plan only before January 1, 1980, the benefit is equal to 1% of final average salary plus $24 for each year of supplemental-plan-only service eamed before January 1, 1980. Final-average salary is the employee's average salary over the 36 consecuttve or joined months that produce the highest average. Employees who terminate with at least the amount of creditable service stated above and do not withdraw their employee confributions may retire at the ages specified above and receive the benefit accmed to their date of termination. The System also provides death and disability benefits. Benefits are established or amended by state statute.

The System issues an annual publicly available financial report that includes financial statements and required supplementary information for the System. That report may be obtained by wrifing to the Parochial Employees' Refirement System, PO Box 14619, Baton Rouge, Louisiana 70898-4619, or by calling (225) 928-1361.

FUNDING POLICY Under Plan A, members are required by state statute to contt-ibute 9.5% of their annual covered salary and the district attomey is required to contribute at an actuarially determined rate. The current rate is 12.75% of annual covered payroll. Contributions to the System also include one-fourth of 1% (except Orleans and East Baton Rouge Parishes) ofthe taxes shown to be collectible by the tax rolls of each parish. These tax dollars are divided between Plan A and Plan B based proportionately on the salaries ofthe active members of each plan. The contribution requirements of plan members and the disttict attorney are established and may be amended by state statute. As provided by R.S. i 1:103, the employer contributions are determined by actuarial valuation and are subject to change each year based on the results ofthe valuation for the prior fiscal year. The disttict attomey's confributions to the System under Plan A for ttie years ending December 31, 2008, 2007. and 2006, were $22,323, $16,297,and $14,586, respectively, equal to the required contributions for each year.

9. DEFERRED COMPENSATION PLAN

The district attomey offers membership in the State of Louisiana, Public Employees Deferred Compensation Plan, a qualified retirement plan under section 457 ofthe Intemal Revenue Code administered by Great West Life and Annuity Insurance Company.

The Louisiana Deferred Compensation Plan provides state, parish and municipal employees with the opportunity to invest money on a before-tax basis, using payroll deduction. Participants defer federal and state income tax on their contributions. In addifion, interest or earnings on the account accumulates tax-deferred. Participants may join the plan with as little as $10 per pay period, or $20 per month, and contribute up to a maximum of 25% of taxable compensation, not to exceed $ 15,500 per calendar year for those participants under age 50, for participants age 50 and older the limit is 20,500.

A special "catch-up" provision may be used to invest up to $31,000 per year for the three years prior to retirement. Any amount excluded from gross income through salary reduction under a 403(b) annuity, a 401(k) profit-sharing plan or a Simplified Employee Pension (SEP) is to be treated as amounts deferred under this deferred compensafion plan. Participants joining the Plan may choose the amount to contt-ibute and the investment option (s). They may revise their choice at any time, transfer monies to other available investment opfions and may increase, decrease or stop deferrals at any fime. The Plan offers both a guaranteed option and variable investment options, from which participants may select a fiind or combination of fiinds to satisfy their personal investment objectives. Each ofthe fiinds has independent investment objectives and utilizes different investtnent sttategies. Witti die exception ofthe Great-West Guaranteed Fund, the remaining investments options are variable in nature. Values ofthe variable options are not guaranteed as to a fixed dollar amount and may increase or decrease according to the investment

19

Thirty-Sixtti Judicial Disttict Attomey

Notes to the Financial Statements (Concluded)

experience ofthe underlying portfolio. The expense to administer the Plan is bome by all participants. The administrafive fee is .85% and is assessed on each ofthe options selected. The variable options also have investment management fees that vary based upon the options chosen. Both the administrative and investment management fees are calculated and deducted daily on a pro-rata basis. There are no annual conttact charges or transaction charges. At retirement, 100% ofthe account value will be applied to any ofthe following settlement options chosen. These options include among others:

• Periodic payment • Payments over your lifetime • Payments for a specific time or amount • Joint and survivor benefits • Lump-sum payment • Any combination ofthe above option

The Plan is administered by Great-West Life and Annuity Insurance Company; 2237 South Acadian Thmway, Suite 702; Baton Rouge, LA 70808; (800) 937-7604 or (225) 926-8086.

10. EXPENDITURES OF THE DISTRICT ATTORNEY NOT INCLUDED IN THE ACCOMPANYING FINANCIAL STATEMENTS

The accompanying financial statements do not include certain expenditures ofthe district attomey paid out ofthe criminal court fiind, the parish police jury or directly by the state. A portion ofthe salaries ofthe district attomey and assistant disttict attomeys are paid directly by the state. The parish police jury pays certain salaries and employer contributions of secretarial personnel.

20

REQUIRED SUPPLEMENTAL INFORMATION

21

3 -O «J

•B

3?

<

-a 1:3 •—>

CQ T3 C 3

^ 00 c o — o 13 <^ ea „ '

U

C C 3 ra

— JJ 2 ^

a §_ X

W

o

" 3

U

x:

_ « ^ u < T3

g . ^ j

V 0 0

T3 3

4J X £ 4J 0

Q - 0 u T3 c UJ

u >" u 3

o

Cl.

^ 0 0

*-* 4J BO

T3 3

ffi

S Vi 3 .—

s ^ E (0 < a.

1^ ^ ^

u.

> 0 f i " i T U OJ 0 - 0 c c K 3

^ . ^ Vi

§ 1 0 CQ

I Am

ta

ry '.

ra V 3 00 0 " a

<£g

i2 c 3 o

B < T3 U 01

3 CQ

VI (N

00 NO

t^ r -Os ro

r~ rO s£>. Tf VN rO

0 0 (N

»" ""

(N t--rN \n

r~ r O SC^ • * "

^^ 0 0 00

, „ , 0 0 r 4 t N

NO 00 VN

VN

V i

VN r -( N r -^ ^ t^V 00 ' r o -O —

r~ ro sC>_

t t VN rO

0 0 ( N

^ ->

( N r-( N

V I

, pp«>

CN f O V I VN

VN O ( N O — O 00 ' CN SO —

0 0 OS 0 " V I r O

0 0 0 CN • > •

0 0 VN V>

V l CN SO

r-" VN

o o o o

v f 00 ' VN O

0 0 0 0 " T t f O

0 0 0 CN 1 — 1

0 0 V l • ^

0 0 VN ON f — I

V )

O " ^ CN O N ( N — 1^ r r ON o r-; r-^ os^ ( N CN r ^ o ' V N ' s o VN r o - - CN — VN f O ^ -

O ^ fs l ON 0 0 ON CN ^ ON O s r - i M ON CN r -

CN

OS Os ON

VN ON • *

ro 00 CN

r o 0 VN

f A

00 '

o ^ r - i ON CN — r - ^ Os o r - r-^ ON^ CN CN P- ' o ^ vC so VN r o — (N ^ VN r o —

0 0 CN

OS ON

°V VN Os • *

ro 00 (N ro 0 VN

(.

0 0 0 0

ro

0 0

(N

0

0 ,

CN CN

0 0 0 ,

V N '

0 0 0

0 ' O

0 0 0

ON

V N

OS Os ON VN ON • ^

<* tN SO • *

ON f

M

0 0 0 0 0 0 0 0 0 0 o^ o o o_, o o ' ' T CN —" VN • * — t o — ro —

O O

0 0 0 ^ 0 ' OS • *

0 0 VN

K 0 VN

V i

c:

« .2 00 Vi

Vi aj 3 c

a:

Vi OJ u .

3 C

u a X u

1 ^ 3

c u X i

T 3 3 ra il

T3

n

£

"ra c 0 Vi

ft.

g 0 . _o "w > : ! "ra c .2 '55

s D .

> ra h-

in OJ y

E 00

.s 1 a. 0

Vi _aj

"H. D . 3

V5

CA U u £ OJ

• a

0

2

0

U

v\

k. 3

c a. X U

"ra 0

u 0

^ ra

3

u 0 0

U

S 2

^ u > I M 0 00 c

' c c

'ob J (3

0 c ra

"ra .£3 •T3 c 3 U.

k^

ra

0 T J C OJ

•3

u

"ra • 0 c 3 u.

fN

< ft, "ra <t a <

r-0 0 VN

fO ON

V i

ON • *

so fO t ^ ro OS

V i

• t

r-r-0 0

o o so

"*'

V I

5 Os ^ H

tN tN ON

V i

B Q

Vi

5 ra

' o ••5 3 — > sz x

I? <U 3 3 U.

g Q

ra "3 •g •&= a .

Cfl

c/1

§ "ra ffl •a c 3 IX C Vi u 00

ra

-a 3 s <

^ "S — -*-* - n d j

a 3 >< CD

PJ

u 3 C U

> u

o 4J

3 • o

-6 (/)

00

o o CN _^ t o

X t

E u

T J

t 3 C

LL)

^ OJ

> •

OJ

^ I . .

o u.

cu < J3 ^ o o * OJ 0 0

3

m

h > o BN " C

?i -s c: c ii 3 ta ^

*o En r 1 ^ ra u 3 0£

" 3

< ffl

i2 c 3 o < T J U

3

m

"ra U^

"ra c ]5j *c O

_, t o ON — Tj-• *

V i

^ . • ^

so t o

V i

1> Os 00 • * V | —

f O ON

i A

O O O O o^ — "* ON

V i

so r o r- ro OS

( A

O O

"* ON

V i

o o o o o^ — r o OS

V i

o o

f o ' OS

V i

, , so O CN O 00 —

•—

V i

•* o t-- o — so_ r-" TT oo

V i

o o o o 'R. "0. ON" T t ' oo

t A

o o o o O ^ v j ^

so" r f 00

V i

VN VN

^m 00 r-•—

( A

V I r f • *

C> ^P V^

Os

CN f N OS

CA

O o o^ • *

ON

V i

o

^ ( N

o o VN ( N Os

(•'

r^ 1 - ^

• ^

—

fe^

r-1 — 1

VN

^

V i

• o o ""

i A

o o 'Cl

V i

1

VN r-o r-' ro

VN t - ' so r- ro

o o o^ o ' r r

t - ' V k l

• ^

—

V i

t N Os l - M

ON r o

V i

VN t - . P-^

r - ' r o

( A

o O so o ' TT

V i

a c

Vi V 3 C

u > OJ oi

o 0 0

.3 u a. o

o c

s OJ Vi b-3

£ *S ft;

u £ 8

c

1 OJ > c

V I 4J 3 C

> Si

3 o H

3

'•B u Q . X UJ

^ 3

1 T3

Vi U

o £ CJ VI

"ra c 0

a.

(J

E OJ in 00

.£ 1 O

:3 ( / I

I -3

C 4J Cl . X

2 o

X) T3 C

3 .£ u 00

u 4J

12

t—

o 0 0

c 3 c '5b OJ S i

ra Vi o u

"ra -u c 3 u.

>s

o T3 C

o

13

• a n 3 u.

3

2 ^ < ft, ra < 3 <

VN

4 t N VN

V i

00 CO

o ^

ro oo

ro VN

V i

00 ^ - VN ON VN VN Os ON r-_ — , t~V " , r o ' s o ' V N ' \ D — t N t N

^^ o CN • V

oo' ^ - 1

V i

r o CN Os^

o" O

ro O VN t N T T

V i

ft.

E o

< t j

'B Vi

5 , .—I

ra ' 5

3

.a _x

#

• o c 3 u. u 3 C u > a: "ra 'a a

-o c 3 U.

u

. s

to VI u

•g O

u o § ra ffl

T3 C 3

U .

.£ <u 0 0

U T3

y j U

3 •5 c a X

UJ i n

3 C

> u a:

' u o 3 W

o

"ra 3 < T J

U OO

T3 3

ffl

0 0

o o CN

^ ro

X )

£ y

D •o o

T J C

UJ

u >-y

3 o u.

^ O 2 0 0

3

ffl

> o M

u c: ii

^

c 3 O E < ra 3 t j

<

u u

T J C 3

V I

1 ffl

1 U DO

-a 3 ffl

c 3 o £ < TJ

u a> 01

TJ 3 ffl

VN 00 VN r o VN

OO ON VN Os VI •* ON ON P-^ 00 t ^ Os — r o " " ^ —'

VN • *

" ^ CN V I

V i

00 ro O

^

r o oo • *

r o VN

V i

O

o o -a-VN

V i

o o o 1 - ^

o o o VN VN

( A

o o o^ VN SO

i A

o o o^ w—

o o o_ so so

Vi

o t N t N

OO — VN Os VN V I Os O N P-^ — r ^ —^ r o so v f so ' — CN CN

,^ o t N • * _

oo' ^ 4

V i

ro ( N

°V o ' SO

ro O VN CN

•

V i

o o o o o o o o 0_^ O ^ O ^ t N CN O VN^ T f ^ r o CN

,_ o o CN

so'

V i

ro CN Os^

o " so

ro CN r^ TT • t r

V i

CN

o o o o o o ' " r . R . R . V ' r o ' oo '

CN CN

o o ON

o

Vi

o o o^ ^ - 1

so

o o Os

^ r-

V i

1 'S

S o DO ' ^

(U CJ 3

& -

U [O

£ S

M l -. u

C K Q U OJ Si 3 >

u £ a. _o "u > u

T3

"ra c ^o ' v i Vi Vi i i 3 .2 S £ = K C 00

3 5" .•=: "1 > h " • -5

"H :3 2 1 - ^ § G T) f - O WD U "^ .5 X "^

bJ

W l

u ^ s

1 y

a. X V

3 o

"ra X i

C

3 .£ u 00

X u

.-. u 2

u > s

I —

o DO

c '£ c ' ^ X)

ra i n u u § "rt X T J C 3

U .

o • o

c OJ ra V I 4J O

5 ra

T3 C 3

U .

3

C 3 O

E < •a 3

CN ^ VN I N

O

Os VN r o V N 00 ON r o 00 •^^ t N r o CN

r o

so tN

SO CN

E o

< t j

'B V i

D

ra '•B 3

•—i

•s _x

t '3

-o c 3 U . i i 3 C

> fti "ra

D .

T J C 3

U .

C V £ in in i i Vi Vi

<

5 H

u y

§ ra ffl

• a

c 3

u. .£ cn UJ OO

^ X

CJ T J C ra in i i

c, 3 "5 c

X

W in" 4) 3 C 4J >

"ra 3

o < B ra aj

3 ffl

00 o o CN

^ ro

^ 1 U

Q TJ 9J

T J C

<u >-•S

a: o

j U 3

•T3 U

O

O Vi y 4 j y -o

ffl ^

ra aS 3 00

0 0 ^

SO O s SO

ro Os so

VN ro (T)

V i

T t I N

sj-l r-ro O • ^

V J

Os VN f O V ) 00 Os r o OO ' T t N ro^ CN — ' p-.' - « '

r o

CN s o CN

O O

o

O O ro O O O ro O VN ro ro_ (N — p-.' —*•

ro

•O so

so SO

O O

O O o o O o o o so ro O ro — ' OO ^

O O

O O

E a. o

3 <U X

0 0 .E •(0 t-i i a. o

( ^ y cn O g ^

1.1 I

¥ 1> r-£ oi 3 fti

> u .T3

"n c o

e y . .

I T3 C u Q . X

UJ

.2 >

1 ^

Vi Vi Si y y

| E u y y cn '^ TJ 00 y

.£ o

1 §

as o u

IO

T ) C y C L

2

T> S

o 0 0

3 _c 'ob y

y 2

c 3

l l .

y >-.

C t -O -o c y

5 S "s rt X TJ C 3

a.

OTHER SUPPLEMENTAL SCHEDULES

26

Assets Cash and cash equivalents Due from others

Total assets

Liabilities Due to other funds Due o others

Total liabilities

Thirty-Sixth Judicial District Attomey Schedule 5

Schedule of Fiduciary Net Assets Agency Funds

For the Year Ended December 31,2008

Bail Bond Collection Trust Asset Forfeiture Total

Fund Trust Fund Agency Funds

$

$

$

$

242 -242

42 200 242

$

$

$

S

9 6 15

15 -15

$

$

$

$

251 6

257

57 200 257

27

OTHER REPORTS

28

Thirty-Sixth Judicial District Attomey Schedule 6

Schedule of Prior Year Audit Findings Year Ended December 31, 2008

Finding - Financial Statement Audit

Audit Finding 2007-1

Late Submission of Audit Report

Finding - By state statute the audit report was due in the Louisiana Legislative Auditor's Office no later than June 30,2008. The audit was scheduled to began June 16,2008 which would have given sufficient time to complete the audit and submit it to the Legislative Auditor's Office no later than the June 30,2008 deadline. On June 13,2008 the district attomey's finance director had to leave for an emergency surgery on an immediate family member and was unable to return for the audit until June 24,2008. This did not leave enough time to complete the audit and submit it by the statutory deadline. Even though an extension was granted the district attomey's audit report was submitted to the Legislative Auditor after the statutory deadline of June 30, 2008.

Date of initial occurrence - December 31, 2007

Corrective action taken - Yes

29

John A. Windham, CPA A Professional Corporation

1620 North Pine Street John A. Windham, CPA DeRidder, LA 70634 Tel: (337) 462-3211 Fax:(337)462-0640

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS

BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

The Honorable David Burton Thirty-Sixth Judicial District Attomey Parish of Beauregard State of Louisiana

I have audited the accompanying financial statements ofthe govemmental activities, each major fiind and aggregate remaining fund information ofthe Thirty-Sixth Judicial District Attomey, as of and for the year ended December 31,2008, which collectively comprise the Thirty-Sixth Judicial District Attomey's basic financial statements and have issued my report thereon dated June 22,2009. I conducted my audit in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General ofthe United States.

Intemal Control Over Financial Reporting

In planning and performing my audit, I considered the Thirty-Sixth Judicial District Attomey's intemal control over financial reporting as a basis for designing my auditing procedures for the purpose of expressing my opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness ofthe Thirty-Sixth Judicial District Attomey's intemal control over financial reporting. Accordingly, I do not express an opinion on the effectiveness ofthe Thirty-Sixth Judicial District Attomey's intemal contt-ol over financial reporting.

A control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the Thirty-Sixth Judicial District Attomey's ability to initiate, authorize, record, process, or report financial data reliably in accordance with generally accepted accounting principles such that there is more than a remote likelihood that a misstatement ofthe Thirty-Sixth Judicial District Attomey's financial statements that is more than inconsequential will not be prevented or detected by the Thirty-Sixth Judicial District Attomey's intemal control.

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement ofthe financial statements will not be prevented or detected by the Thirty-Sixth Judicial District Attomey's internal control.

My consideration of intemal control over financial reporting was for the limited purpose described in the first paragraph of this section and would not necessarily identify all deficiencies in intemal contt-ol that might be significant deficiencies or material weaknesses. I did not identify any deficiencies in intemal control over financial reporting that I consider to be material weaknesses, as defined above.

30

The Honorable David Burton Thirty-Sixth Judicial District Attomey Parish of Beauregard State of Louisiana Page 2

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Thirty-Sixth Judicial District Attomey's financial statements are free of material misstatement, I performed tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of my audit and, accordingly, I do not express such an opinion. The results ofmy tests disclosed no instance of noncompliance or other matters that is required to be reported under Government Auditing Standard. '

This report is intended solely for the information and use of management, others within the organization, and the Legislative Auditor and is not intended to be and should not be used by anyone other than these specified parties, although under Louisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document.

DeRidder, Louisiana June 22, 2009

31