Los Alamos National Laboratory New Employee Benefits Orientation

LANL New Hire Benefits Orientationlanl.gov/.../new-hires/_assets/docs/new-hire-benefits-presentation.pdf · Benefits Orientation. ... 开开开开开开开开尨look this up before

Good morning/afternoon, my name is ____________ . On behalf of the benefit’s department welcome to Los Alamos National Laboratory. At Los Alamos National Laboratory, we are committed to helping you achieve your highest level of well-being. We know how challenging choosing the right benefit plans can be so we are here to help you enroll in the benefit plans that best meet the needs of you and your family. We are located here in the Otowi building on the ground level through the double doors past the badge office. We welcome visitors during our normal business hours of 8am-5pm Monday through Thursday and 8am-4pm on Friday

• LANL cares about your Health and Wellness• We offer competitive and cost effective

benefit plan options• Financial plans and programs for a brighter

tomorrow

Great News!

Presenter

Presentation Notes

LANL cares about the health and wellness of our employees, our benefits package reflects this deep care. Because of the many health incentives and programs that the laboratory provides we have been able to keep our health care costs down. As a result our premiums have had no increase in 3 years and for the last 2 years we have had a “Premium Holiday.”

Agenda

• Benefits Eligibility• Benefit Plan Options• Required Forms • Important Dates and Reminders • Questions

Presenter

Presentation Notes

Today we will be going over the following Agenda. First we will determine your benefits eligibility, review our plan options, discuss the required forms, leave you with some important dates and reminders and answer all your questions along the way.

Eligibility

• Full Time• Part Time

Presenter

Presentation Notes

The Laboratory offers a comprehensive benefits package to our full-time and part-time employees. Part time employment is 50% time or minimum of 20 hours per week for 12-month period.

Eligible Dependents• Legal Spouse

• Marriage certificate or signed federal tax return if filed jointly

• Domestic Partner• Declaration form and 6 months proof of

financial interdependence

• Child • Birth certificate or adoption papers

• Legal Ward• Legal document granting custody

Presenter

Presentation Notes

Page 5 of your handbook lists the eligible dependents and the approved supporting documentation to establish them as a dependent on your insurance. Please review this list. Some examples of people you can cover on your insurance are your legal spouse, your domestic partner and their children, your children, or your legal ward. You can also cover over age disabled children. Children are eligible to remain on your plan until the age of 26. Legal wards are allowed to remain on your plan to age 18. Supporting Documentation establishing the eligibility of your dependents is required to accompany your enrollment form.

New Employee Checklist

31 days to enroll or make changes You can view your benefit elections

through Oracle Worker Self Service once enrolled

Visit with the Benefits staff for more assistance

Page 4 of your New Employee Benefits HandbookYOUR Period of Initial Eligibility (PIE) Ends on ________________

Presenter

Presentation Notes

Move Slide or reword On page 4 of your New Hire Benefits Handbook Full Benefits Checklist – The Benefits Checklist will help keep you on track with your benefit activities over the next few weeks. I WANT EVERYONE TO WRITE IN THEIR PERIOD OF INITIAL ELIGIBILITY DATE. IF YOUR HIRE DATE WAS TODAY YOUR PIE Ends on ________(look this up before your presentation). If today is not your hire date come see us for your PIE end date. The first few items are all related to reviewing the plan materials. The next few items are related to designating your emergency contacts and beneficiaries, accessing your 401(k) account and updating any changes to your personal information. Please review and keep this checklist to make sure you complete all the activities that apply to you.

Medical Benefits

(BCBSNM)

Presenter

Presentation Notes

Now that we’ve gone over some of the forms and information you have available in your packet we would now like to assist you in the decisions involved with selecting your medical plan. Blue Cross Blue Shield of New Mexico is our Medical provider for both medical plan options LANL offers.

Medical Benefits

Medical Plan Options• Preferred Provider Organization

(PPO)• High Deductible Heath Plan

(HDHP)

Presenter

Presentation Notes

Let’s start with your Medical coverage options. We offer two comprehensive medical plan options. We have a Preferred Provider Organization or PPO and a High Deductible Health Plan or HDHP. Both plans offer free preventive care, an in and out of network coverage option and a large nationwide network of Blue Cross Blue Shield providers. We also have some Tax-Advantage accounts available for use with either plan that we will be discussing in a later slide.

• The 24/7 Nurseline can help you figure out if you should call your doctor, go to the ER or treat the problem yourself

• Fitness Program• Pay only $25 a month with no long-term contract for access to

gyms and discounts on wellness services.

Medical Benefits

Presenter

Presentation Notes

24/7 Nurseline (800) 973-6329 Could your child’s fever or sore throat turn into something more serious? Is your 1am asthma attack cause for a trip to the ER? The 24/7 Nurseline can help you figure out if you should call your doctor, go to the ER or treat the problem yourself Fitness Program Pay only $25 a month with no long-term contract Access to discounts on a nationwide network of 40,000 health and well-being providers such as massage therapists, personal trainers, and nutrition counselors. Instant access to a nationwide network of more than 8,00 participating gyms. SANTA FE, AB’S, ANYTIME FITNESS, PLANET FITNESS, ETC. GINO’S GYM IN ESPANOLA AND MANY GYMS IN ALBUQUERQUE.

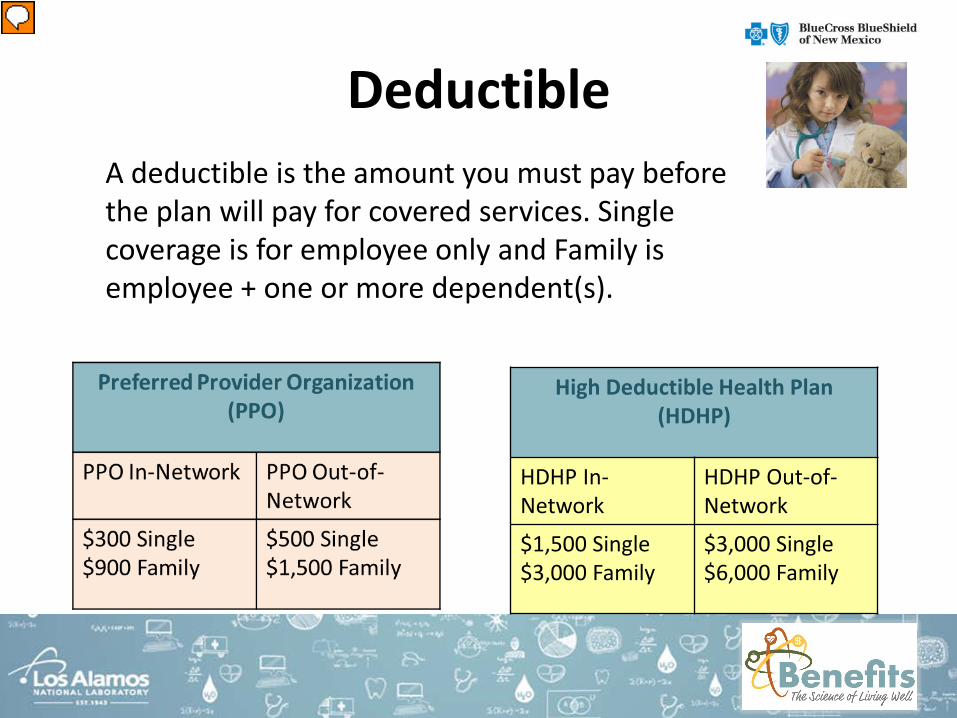

DeductibleA deductible is the amount you must pay before the plan will pay for covered services. Single coverage is for employee only and Family is employee + one or more dependent(s).

High Deductible Health Plan(HDHP)

HDHP In-Network

HDHP Out-of-Network

$1,500 Single$3,000 Family

$3,000 Single$6,000 Family

Presenter

Presentation Notes

Let’s compare how these two plans will work for you. First let’s look at the deductibles. A deductible is the amount you must pay up to before the plan begins to pay for covered services you use. Discuss the PPO Deductibles Now let’s compare that to the High Deductible Health Plan (HDHP Deductibles float in) Discuss HDHP Deductibles The deductibles for the PPO and HDHP work a little different. Let’s discuss. The deductible in the PPO is based on each individual in the plan. For example, a single person has their own in-network deductible of $300. If a family is covered under this plan anywhere from 2 – 10 dependents, each individual has to meet their own deductible, once their $300 is met then their deductible is met for the plan year. There is a $900 cap for the entire family so once that $900 is met, no matter who meets it then the deductible is met for that year. The deductible in the HDHP plan is $1,500 for single coverage and $3,000 for family in-network. There is no individual deductible. The family as a whole must meet the entire deductible for that plan year.

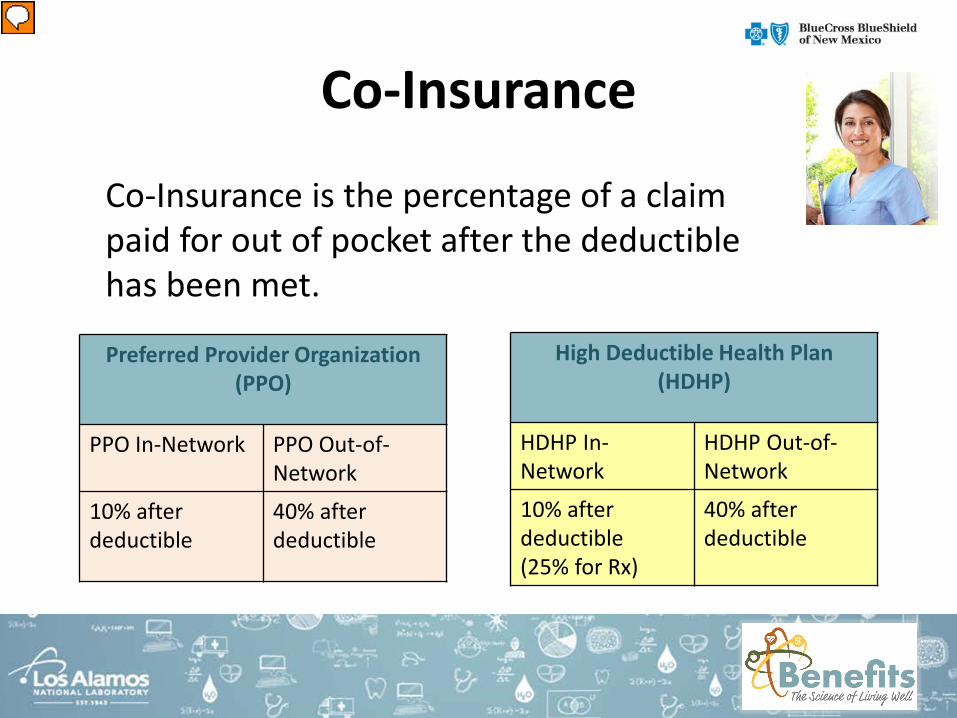

Co-Insurance

Co-Insurance is the percentage of a claim paid for out of pocket after the deductible has been met.

Preferred Provider Organization(PPO)

PPO In-Network PPO Out-of-Network

10% afterdeductible

40% after deductible

High Deductible Health Plan(HDHP)

HDHP In-Network

HDHP Out-of-Network

10% afterdeductible(25% for Rx)

40% after deductible

Presenter

Presentation Notes

So once you’ve met the deductible the Co-Insurance will kick in. What is Co-Insurance? Co-Insurance is the percentage of a claim that you will pay for after the deductible has been met. Let’s look at the PPO first. DISCUSS THE CO-INSURANCE Now let’s compare that to the HDHP DISCUSS THE CO-INSURANCE

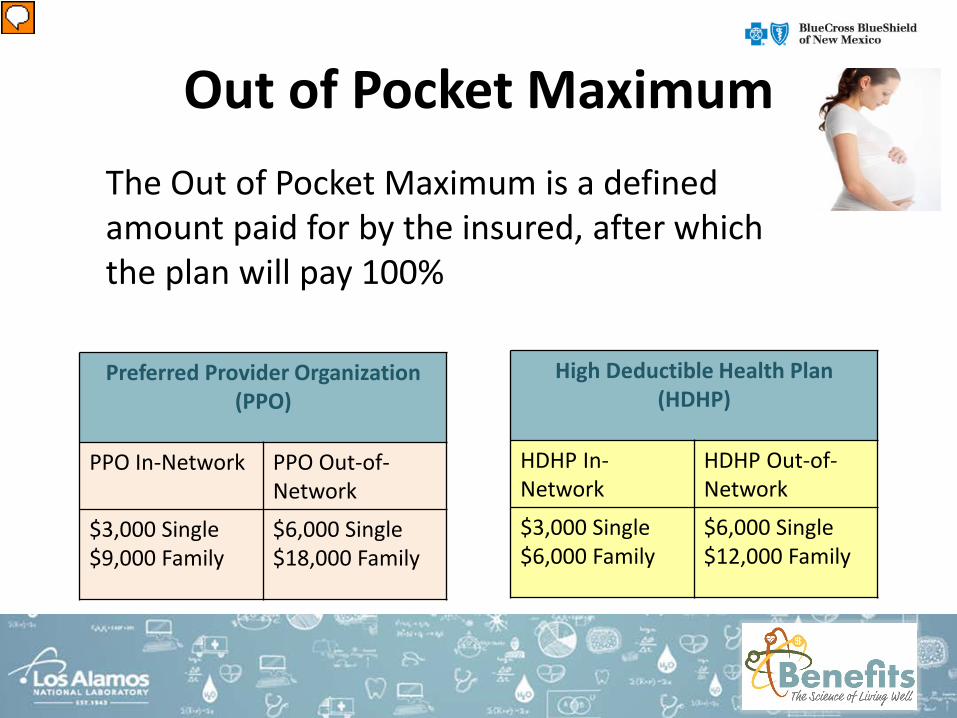

Out of Pocket MaximumThe Out of Pocket Maximum is a defined amount paid for by the insured, after which the plan will pay 100%

Preferred Provider Organization(PPO)

PPO In-Network PPO Out-of-Network

$3,000 Single$9,000 Family

$6,000 Single $18,000 Family

High Deductible Health Plan(HDHP)

HDHP In-Network

HDHP Out-of-Network

$3,000 Single $6,000 Family

$6,000 Single$12,000 Family

Presenter

Presentation Notes

So will the insurance ever cover the claim at 100%? Let’s take a look at what happens when you have a busy year of claims and pay a high amount out of pocket. The plan has a ceiling to protect you if you have a year full of claims. There is a limit to the amount you will pay out of pocket. This is your Out of Pocket Maximum. Once you pay a certain amount out of your own pocket, the limit kicks in and the plan reverts to 100% coverage of allowed services for the rest of the year. The Out of Pocket Maximum is a defined out of pocket amount paid for by the insured after which BCBS will pay 100% Let’s look at the Out of Pocket Max for the PPO DISCUSS Now let’s compare that to the HDHP DISCUSS

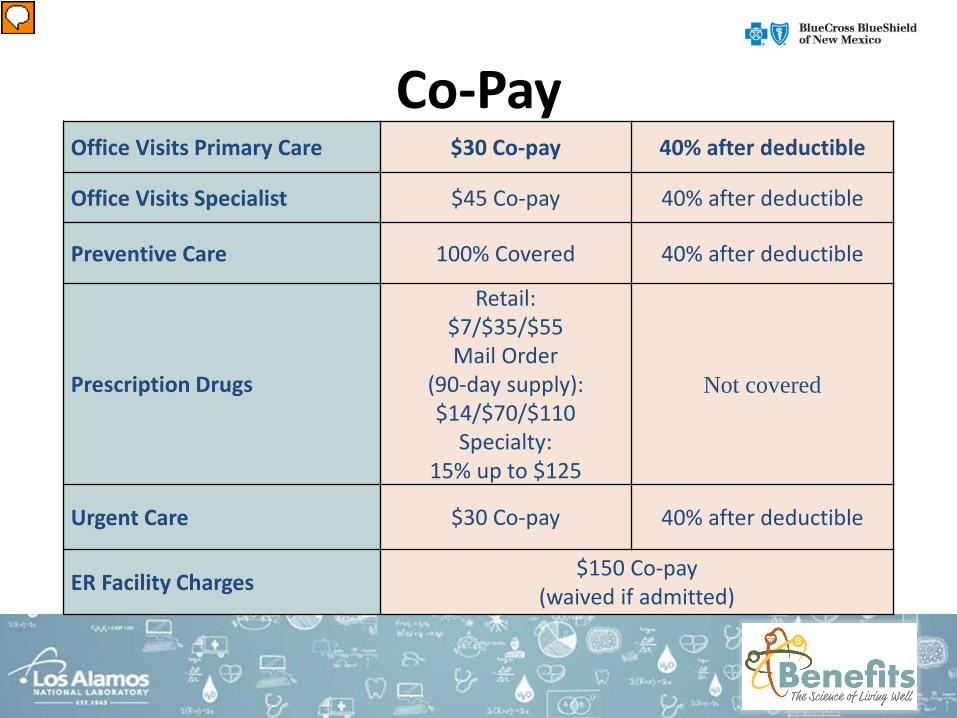

Co-PayThe Co-Pay is a unique feature to the PPO plan. It is a fixed dollar amount paid at the time of service

Office Visits Primary Care $30 Co-pay 40% after deductible

Office Visits Specialist $45 Co-pay 40% after deductible

Preventive Care 100% Covered 40% after deductible

Prescription Drugs

Retail:$7/$35/$55 Mail Order

(90-day supply): $14/$70/$110

Specialty:15% up to $125

Not covered

Urgent Care $30 Co-pay 40% after deductible

ER Facility Charges $150 Co-pay(waived if admitted)

Presenter

Presentation Notes

Now I’d like to discuss a feature that is unique to the PPO plan. Co-pay is a fixed dollar amount paid at the time of service. This is a fixed dollar amount that you would pay for at the time of service for common services that you don’t have to meet the deductible for. PPO only. Here is an excerpt from your packet reviewing the various co-pays on the PPO plan. DISCUSS

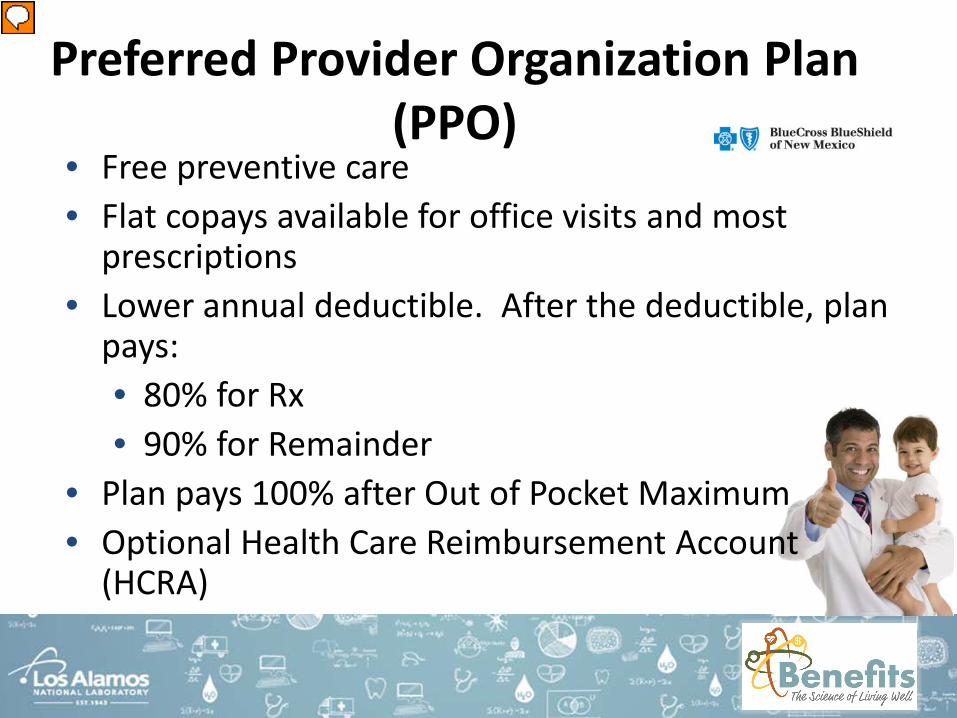

Preferred Provider Organization Plan (PPO)

• Free preventive care• Flat copays available for office visits and most

prescriptions• Lower annual deductible. After the deductible, plan

pays:• 80% for Rx• 90% for Remainder

• Plan pays 100% after Out of Pocket Maximum• Optional Health Care Reimbursement Account

(HCRA)

Presenter

Presentation Notes

These are the key features of the PPO plan. The PPO offers a lower annual deductible and pays at 90% after the deductible has been met. Each individual on the plan has their own deductible of $300 to meet up to a maximum deductible of $900 for a family. This plan is a more traditional plan in which you pay a fixed amount, or copay for office visits and most prescriptions. The deductible does not apply to the co-pay. BCBS offers a discount for your mail order prescriptions if you participate in the PPO. There is also an optional Flexible Spending arrangement called your Health Care Reimbursement Account that you can choose to contribute to.

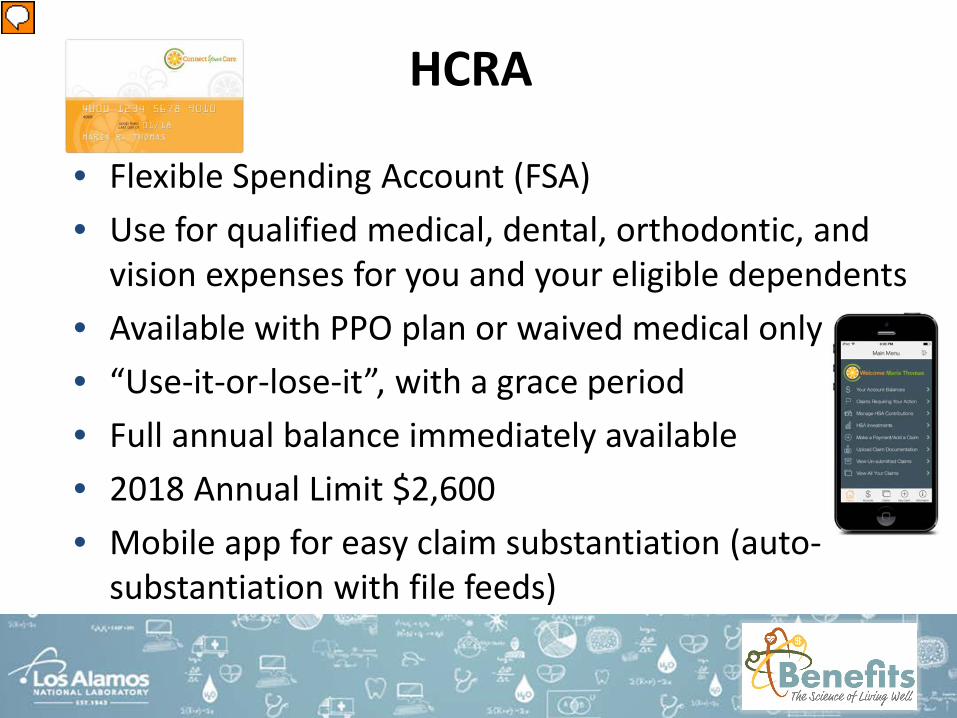

Health Care Reimbursement Account (HCRA)

Presenter

Presentation Notes

So what is a Health Care Reimbursement Account? The HCRA is a Flexible Spending Arrangement, or FSA, administered by ConnectYourCare that will lower your taxable income and allow you to use the funds you set aside for qualified medical, dental, and vision expenses.

• Flexible Spending Account (FSA)• Use for qualified medical, dental, orthodontic, and

vision expenses for you and your eligible dependents• Available with PPO plan or waived medical only• “Use-it-or-lose-it”, with a grace period• Full annual balance immediately available• 2018 Annual Limit $2,600• Mobile app for easy claim substantiation (auto-

substantiation with file feeds)

HCRA

Presenter

Presentation Notes

The Health Care Reimbursement account is available to employees who either waive their medical coverage or participate in the PPO Medical Plan option. This is a use-it or lose-it account. You want to designate an amount that you will be able to use in the calendar year or you will forfeit any left over funds. There is a grace period if you are unable to use all your money up by the end of the calendar year, the plan will allow you to use your funds until March 15th of the following calendar year. The plan offers a user friendly mobile app for easy claim substantiation. And for our Medical Dental and Vision claims we offer an automatic claim substantiation feature, meaning that BCBS, DeltaDental, and VSP will automatically send claims information to ConnectYourCare. So for many of your claims you will not have to do a thing, other than swipe your card. You can use this account for any qualified expenses under medical, dental, and vision. For specific information regarding eligibility and annual contribution limits, please visit the IRS website at www.irs.gov.

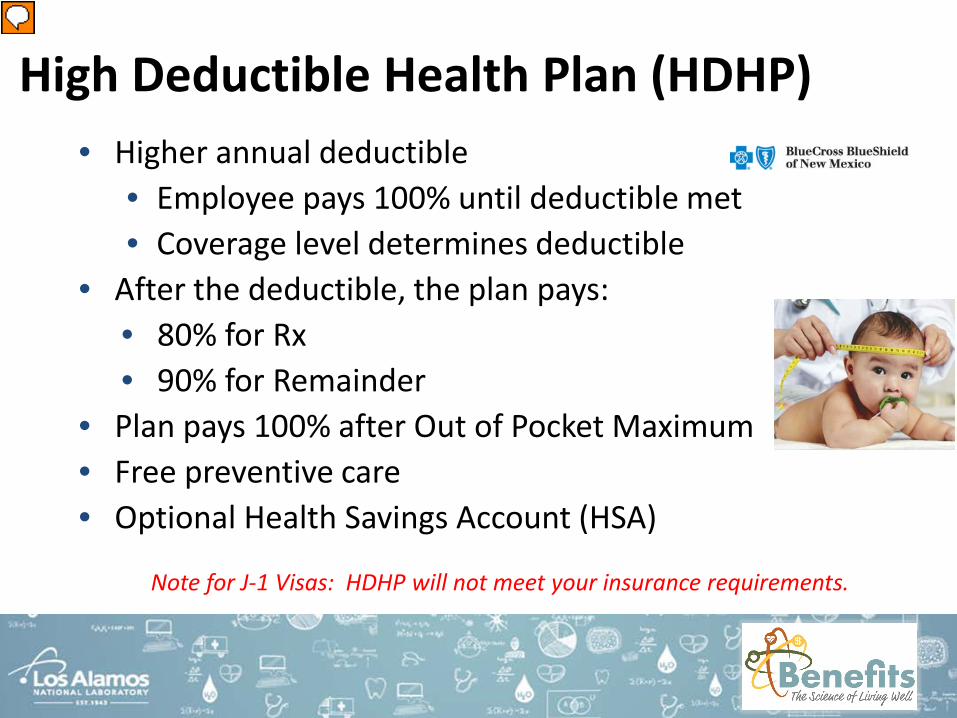

High Deductible Health Plan (HDHP)• Higher annual deductible

• Employee pays 100% until deductible met• Coverage level determines deductible

• After the deductible, the plan pays:• 80% for Rx• 90% for Remainder

• Plan pays 100% after Out of Pocket Maximum• Free preventive care• Optional Health Savings Account (HSA)

Note for J-1 Visas: HDHP will not meet your insurance requirements.

Presenter

Presentation Notes

Next are the key features of the High Deductible Health Plan. This plan offers lower premiums and as the name suggests has a higher deductible. The coverage level will determine the deductible. For example, a single person covering just themselves will have a $1,500 deductible and a family of 1 or more will have a deductible of $3,000 to meet as a family. After the deductible has been met the plan will pay 80% for prescription and 90% for all other services (in network) until the out of pocket max is met, at which point BCBS will pay at 100%. This plan has an optional Health Savings Account (HSA) that you can choose to participate in. Even if you do not contribute any money to this account LANL will make a contribution on your behalf of $250 for single coverage and $500 for family coverage. If you want the HSA contribution from LANL you must choose to enroll on the form and you can elect to contribute $0 per paycheck if you would like.

Heath Savings Account (HSA)

Presenter

Presentation Notes

What is an HSA? Like the HCRA we discussed with the PPO plan the HSA is an account that allows you to set aside pre-tax dollars, lowering your taxable income to use for qualified medical dental and vision expenses not covered by your plan. This account can help you fund yourself to meet your deductible.

HSA• Available only with HDHP• Interest-bearing or invest assets• Balance rolls over, portable• Mobile app available• LANL annual contributions:

• $250(Employee Only) / $500(Employee + 1 or more)• These count towards the annual maximum

• 2018 annual contribution limits:• $3,450 (Employee Only) / $6,900 (Employee + 1 or more)• $1,000 catch up for 55+

• Use for qualified medical, dental and vision expensesNote: Not everyone is eligible with other non-HDHP coverage (Medicare, Tricare, etc.)

Presenter

Presentation Notes

Health savings accounts (HSA)�The HSA is a tax-advantaged, interest-bearing medical savings account available to employees enrolled in the High-Deductible Health Plan (HDHP). This account allows you to pay for eligible medical expenses and rolls over from year to year. Like the HCRA you can use this account to help you pay for qualified medical, dental, and vision expenses not covered by your plans. You do want to make sure you are qualified. If you have other coverage, such as Medicare, Tricare, etc you might not qualify for an HSA. Again, For specific information regarding eligibility and annual contribution limits, please visit the IRS website at www.irs.gov. You must enroll for the HSA, even at $0/pay, in order to get the HDHP incentive or any other contributions from LANL.

Premiums

• Premiums are the amount of money you pay out of your paycheck for the plan option and coverage level you choose.

• Premiums deductions are taken twice a month as payroll deductions.

Presenter

Presentation Notes

What are premiums? Premiums are the amount of money you pay out of your paycheck for the plan option and coverage level you choose. Premium deductions are taken twice a month. Example – August has 3 pay periods, premium deductions will only be taken on the first two pay periods. Your premiums are based on salary bands.

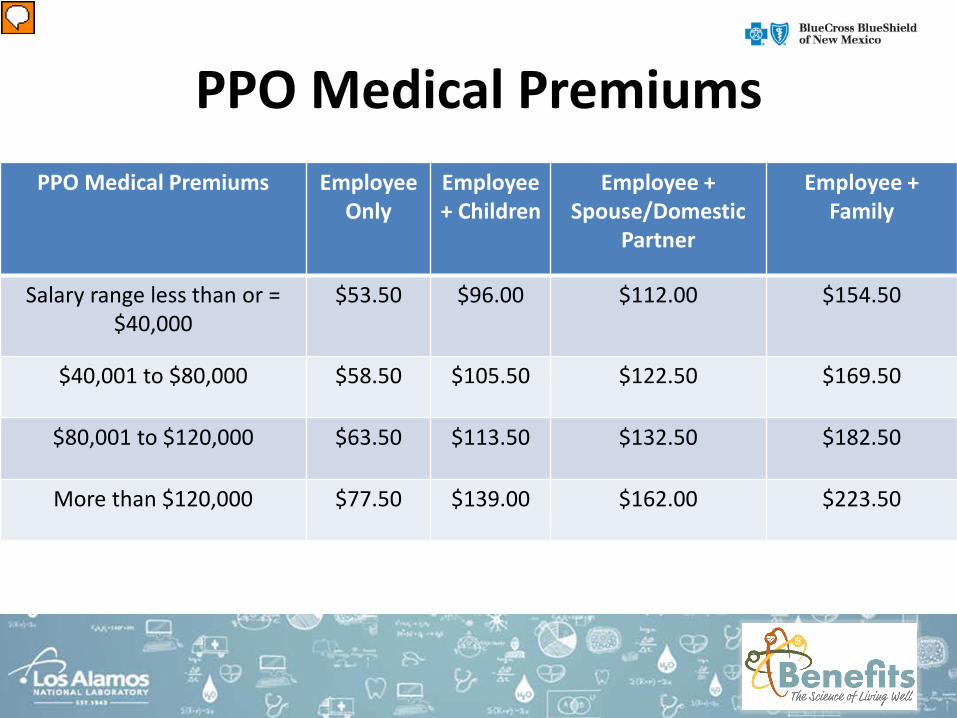

PPO Medical PremiumsPPO Medical Premiums Employee

OnlyEmployee + Children

Employee + Spouse/Domestic

Partner

Employee + Family

Salary range less than or = $40,000

$53.50 $96.00 $112.00 $154.50

$40,001 to $80,000 $58.50 $105.50 $122.50 $169.50

$80,001 to $120,000 $63.50 $113.50 $132.50 $182.50

More than $120,000 $77.50 $139.00 $162.00 $223.50

Presenter

Presentation Notes

For PPO Plan -

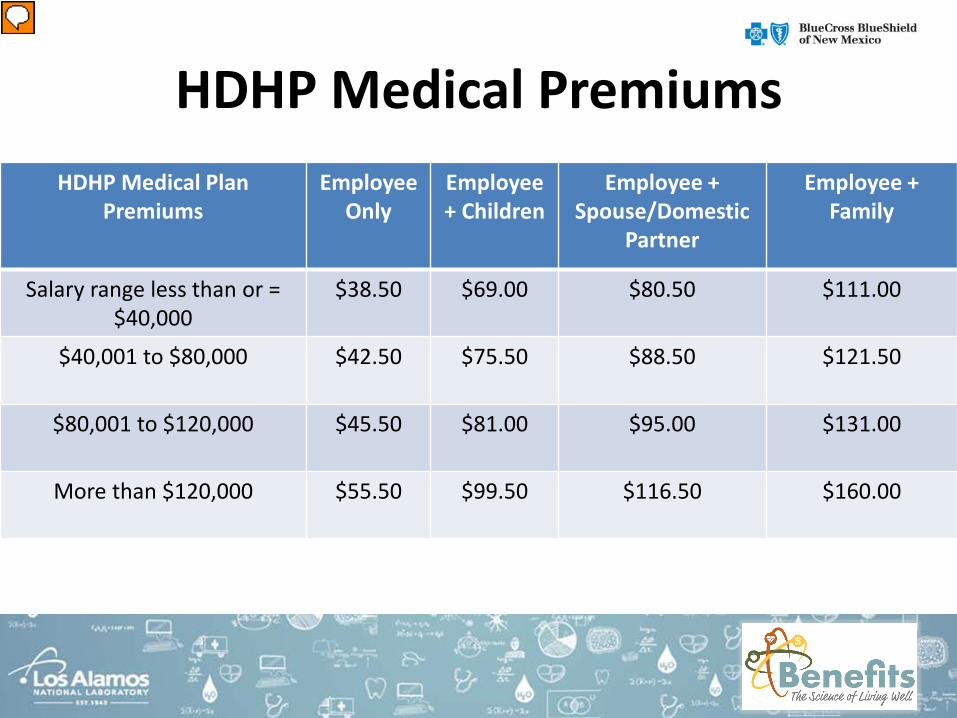

HDHP Medical PremiumsHDHP Medical Plan

PremiumsEmployee

OnlyEmployee + Children

Employee + Spouse/Domestic

Partner

Employee + Family

Salary range less than or = $40,000

$38.50 $69.00 $80.50 $111.00

$40,001 to $80,000 $42.50 $75.50 $88.50 $121.50

$80,001 to $120,000 $45.50 $81.00 $95.00 $131.00

More than $120,000 $55.50 $99.50 $116.50 $160.00

Presenter

Presentation Notes

For HDHP Plan -

Decision Support Tools

ALEX

Premium Calculator

Use these tools to choose the best insurance options for you!

Premium Calculator: From the LANL internal web site, Select Employees > Benefits > Health & Welfare > Medical > Tools

Presenter

Presentation Notes

Meet ALEX, our virtual Benefits Counselor. This system is here to help you navigate the options here at LANS and help you weigh your options. Find ALEX on our Benefits website. The Premium Calculator walks you through the enrollment form and you can complete it online and see your premiums as you make your choices. A great feature of this tool also is that you can see how much your 401k will cost out of your paycheck and get a glimpse into how much money you can get with your LANS 401k matching contribution which my colleague will go over in more detail.

For enrolling in the High Deductible Health Plan, LANS will contribute $250 for single coverage and $500 for family coverage, even if you don’t sign up for the HSA.

Medical True or False Edition

Presenter

Presentation Notes

Now that we’ve gone over all that information I want to make sure I haven’t lost you. Let’s test your brain! For enrolling in the HDHP LANS will contribute $250 for single coverage and $500 for family coverage even if you don’t sing up for the HSA? True or False? Well that’s False. LANS will contribute these amounts into your HSA but you do have to sing up. If you don’t’ want to contribute that’s fine. Indicate that you are selecting this plan and enter a $0 amount for your payroll deductions. This opens an account for you at HSA and LANS will have somewhere to make that deposit. Before we move on are there any questions on our medical plan options?

Dental Plan

Presenter

Presentation Notes

Now that we’ve covered your available medical plan options and the optional Tax advantaged accounts associated with each plan I’d like to take you on a tour of the other coverages LANL provides. Delta Dental of California is our carrier for our Dental plan. These next few slides will discuss the highlights of this plan.

Dental• LANL pays your dental premiums for you and your

eligible dependents• Delta Dental offers:

– Large national network – Low deductibles– Preventive service– Many covered services including orthodontics

Presenter

Presentation Notes

Delta Dental of California offers a large national network with low deductibles, preventive care allowances, and other covered services including orthodontic allowances for children or adults. One of the highlights of this plan is that the Laboratory pays 100% of the premium for you and your eligible dependents! Enrollment is not automatic

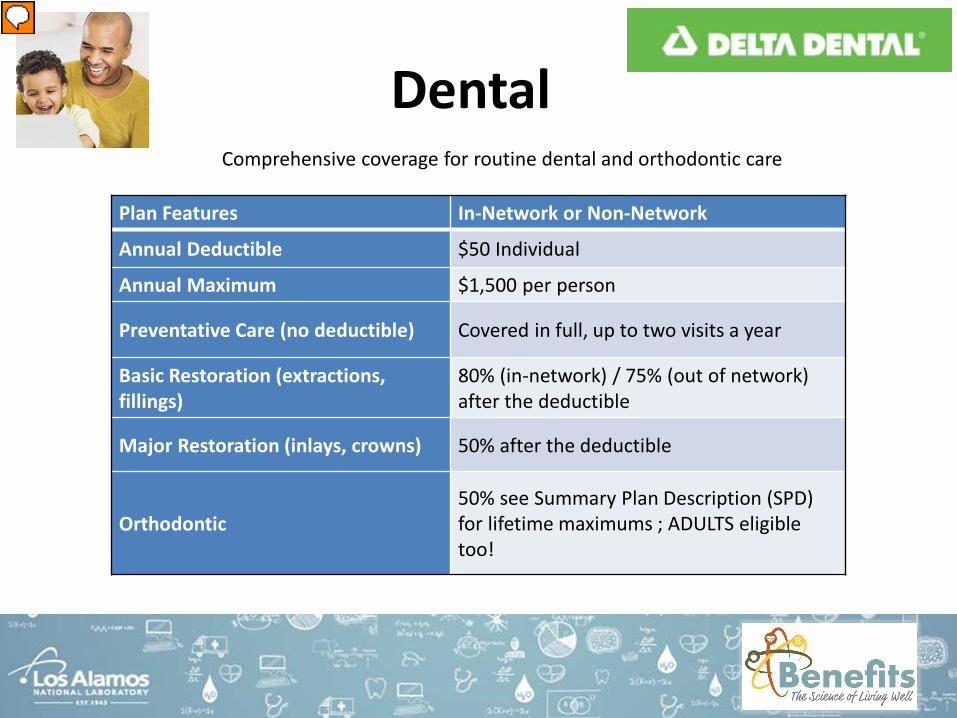

DentalComprehensive coverage for routine dental and orthodontic care

Plan Features In-Network or Non-Network

Annual Deductible $50 Individual

Annual Maximum $1,500 per person

Preventative Care (no deductible) Covered in full, up to two visits a year

Basic Restoration (extractions, fillings)

80% (in-network) / 75% (out of network) after the deductible

Major Restoration (inlays, crowns) 50% after the deductible

Orthodontic50% see Summary Plan Description (SPD)for lifetime maximums ; ADULTS eligibletoo!

Presenter

Presentation Notes

In your handbook you have this chart going over some of the more common covered services under your dental plan. Please note that this is not a comprehensive listing and more information is available on the benefit homepage.

Vision Plan

Presenter

Presentation Notes

Along with Dental LANL also offers Vision insurance. Our Vision carrier is the Vision Service Plan, or VSP. These next few slides will go over the details of this plan.

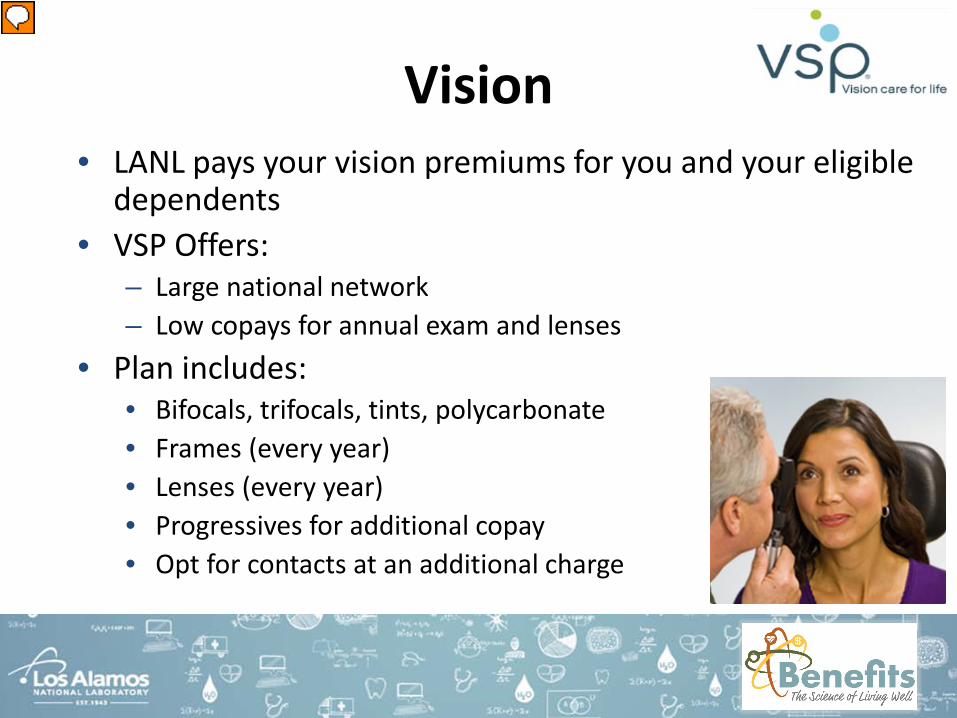

Vision• LANL pays your vision premiums for you and your eligible

dependents• VSP Offers:

– Large national network– Low copays for annual exam and lenses

• Plan includes:• Bifocals, trifocals, tints, polycarbonate• Frames (every year)• Lenses (every year)• Progressives for additional copay• Opt for contacts at an additional charge

Presenter

Presentation Notes

VSP offers a large national network with low copays for annual exams and lenses as well as allowances for other covered options. Enrollment is not automatic Another great part of our vision plan is that like the Dental LANL pays 100% of the premiums for you and your eligible dependents. You just need to sign up for this plan.

VisionComprehensive coverage for exams, contact lenses,

eyeglass lenses and frames

Presenter

Presentation Notes

You have this in your handbook. Again this is not a comprehensive listing of covered services but is a list of some of the more commonly utilized services. If you would like more information please review our website.

LANL pays Dental and Vision Insurance premiums for you and your eligible

dependents

Dental and Vision True or False Edition

Presenter

Presentation Notes

True

Other Flexible Spending Accounts

Presenter

Presentation Notes

We discussed the Health Care Reimbursement Account and how that relates to your medical plan. The lab also offers some other tax advantaged plans through Connect your care that I’d like to highlight. These plans, just like the HCRA, allow you to set aside pre-tax dollars to pay for qualified expenses thus lowering your taxable income.

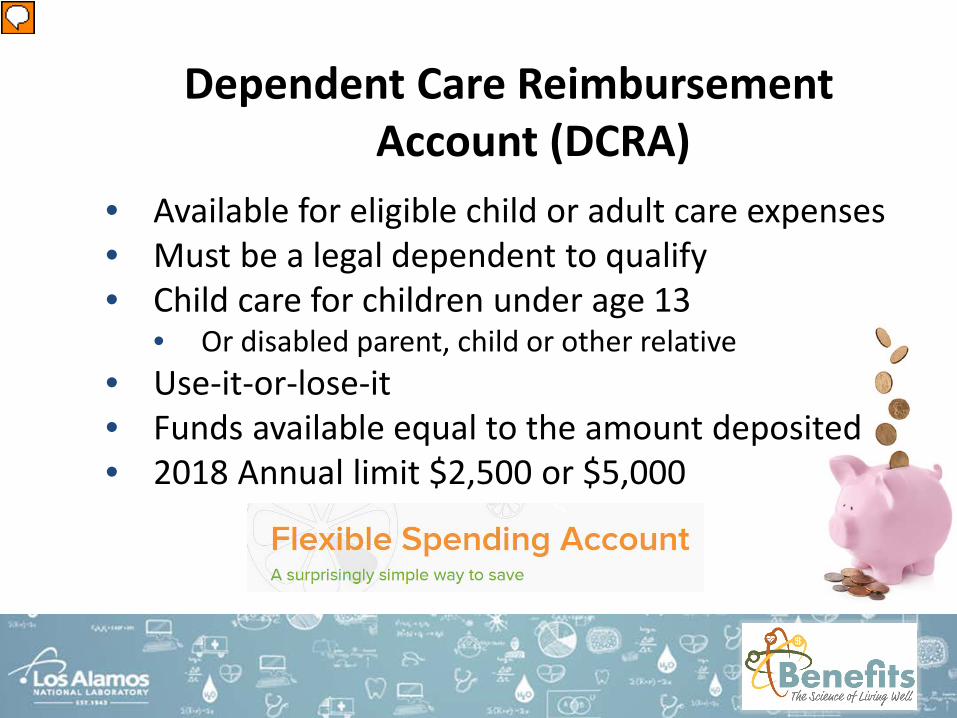

Dependent Care Reimbursement Account (DCRA)

• Available for eligible child or adult care expenses • Must be a legal dependent to qualify• Child care for children under age 13

• Or disabled parent, child or other relative• Use-it-or-lose-it• Funds available equal to the amount deposited• 2018 Annual limit $2,500 or $5,000

Presenter

Presentation Notes

LANL offers the Dependent Care Reimbursement Account (DCRA) to help fund your needs for dependent care. It is use it or lose it so you want to designate an amount you can use within the plan year or you will forfeit those funds. It cannot be used for any overnight care services (summer camp, nursing home). The plan is different from the HCRA in that you pay as you go. You cannot use all the designated funds on day one but only use what is available in the account at the time of the claim.

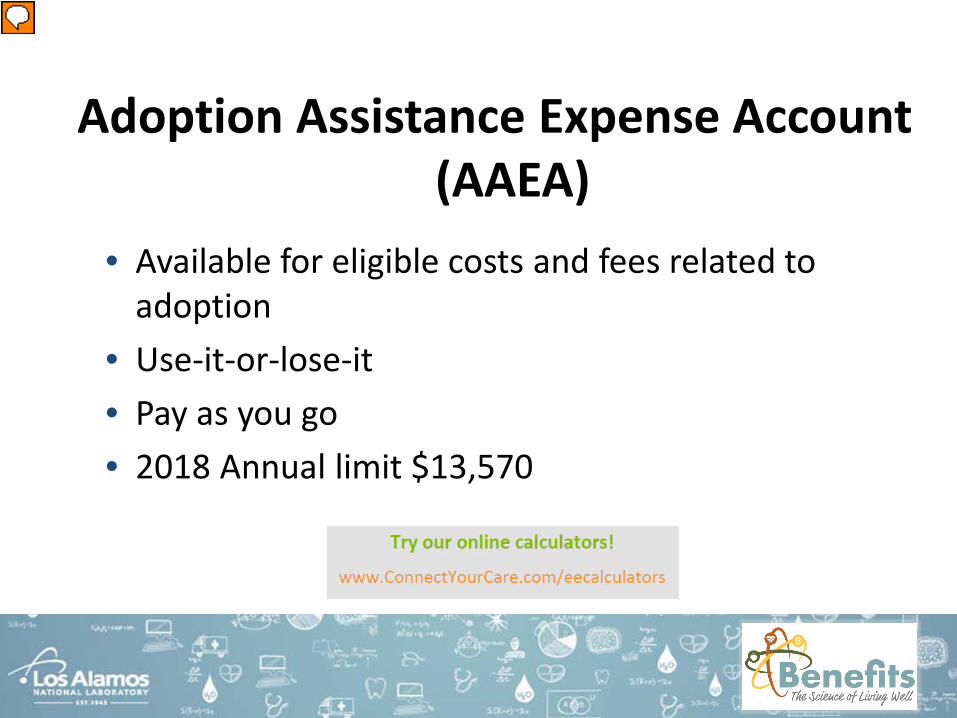

Adoption Assistance Expense Account (AAEA)

• Available for eligible costs and fees related to adoption

• Use-it-or-lose-it• Pay as you go • 2018 Annual limit $13,570

Presenter

Presentation Notes

LANL also offers an account to help you pay for expenses associated with the adoption of a child. Adoption Assistance Expense Account (AAEA)�The Adoption Assistance Expense Account allows you to pay for eligible costs and fees related to adoption. These accounts are governed by the Internal Revenue Service (IRS), so be sure to verify the contribution limits and eligible expenses of the plan before you enroll.

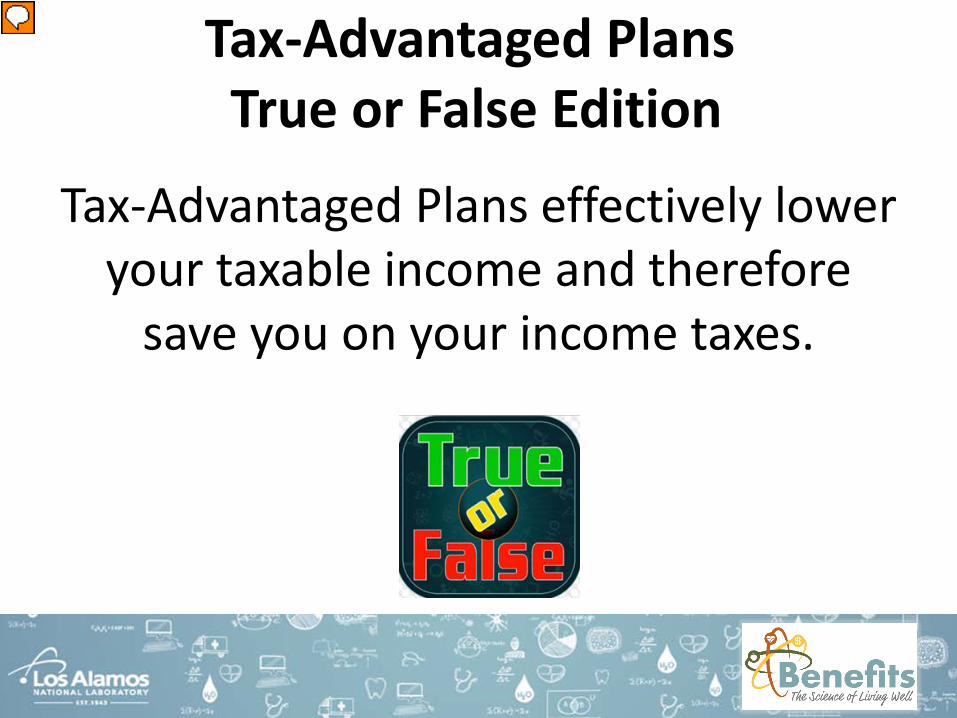

Tax-Advantaged Plans effectively lower your taxable income and therefore

save you on your income taxes.

Tax-Advantaged PlansTrue or False Edition

Presenter

Presentation Notes

True

Legal Plan

Presenter

Presentation Notes

Now that we’ve covered our health and welfare and our tax advantage plans we will be discussing our Peace of mind plans. First up is the available Legal plan provided through ARAG Legal Group.

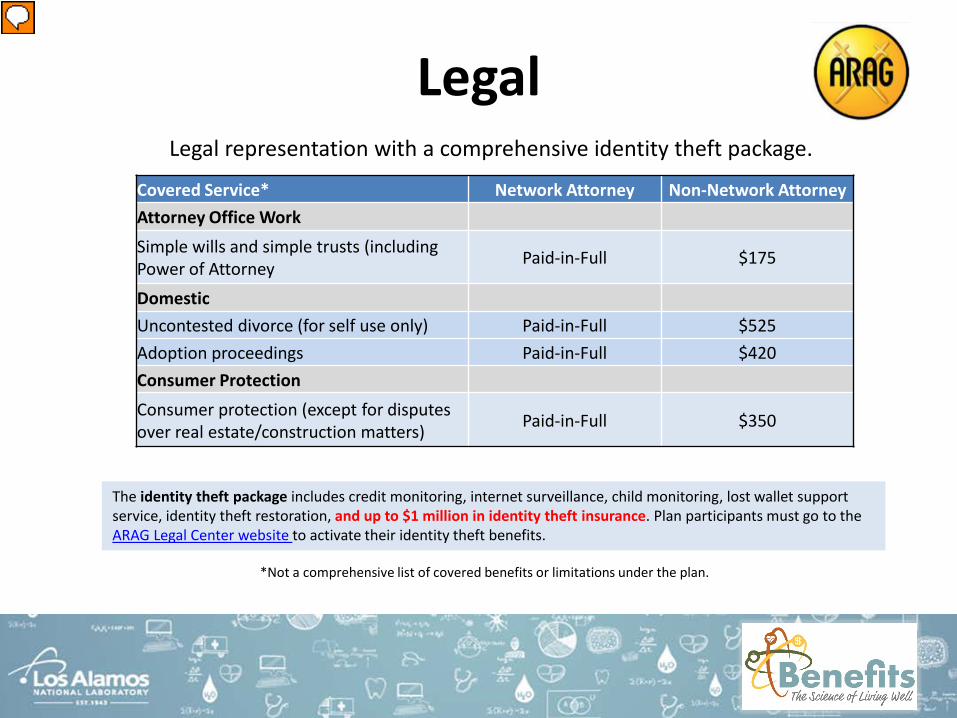

LegalLegal representation with a comprehensive identity theft package.

Covered Service* Network Attorney Non-Network AttorneyAttorney Office WorkSimple wills and simple trusts (including Power of Attorney Paid-in-Full $175

DomesticUncontested divorce (for self use only) Paid-in-Full $525 Adoption proceedings Paid-in-Full $420 Consumer ProtectionConsumer protection (except for disputes over real estate/construction matters) Paid-in-Full $350

*Not a comprehensive list of covered benefits or limitations under the plan.

The identity theft package includes credit monitoring, internet surveillance, child monitoring, lost wallet support service, identity theft restoration, and up to $1 million in identity theft insurance. Plan participants must go to the ARAG Legal Center website to activate their identity theft benefits.

Presenter

Presentation Notes

This plan offers affordable legal representation for a variety of situations. As well as access to their law library and DIY documents. The legal plan also offers a comprehensive identity theft package. This package includes credit monitoring, internet surveillance, child monitoring, lost wallet support service , identity theft restoration and up to $1,000,000 identity theft insurance. If you select ARAG legal and would like the Identity Theft package you just need to sign up through their website at no additional charge.

You are automatically enrolled in the identify theft protection if you sign up

for legal insurance.

Legal True or False Edition

Presenter

Presentation Notes

True- however, if you want to take full advantage of the Identify theft monitoring protection, you will have to log onto the ARAG legal website and register with your information.

Disability Plan Options

Presenter

Presentation Notes

Next we will be discussing the plan options that are here to protect your income in the event of an accident or illness. The lab offers 3 disability plan options. These next slides will discuss these options.

What is disability insurance?

Why do you need it? Pregnancy Surgery Injury Illness

Presenter

Presentation Notes

So what exactly is disability insurance? Take a look at this brief video (hover over the picture)

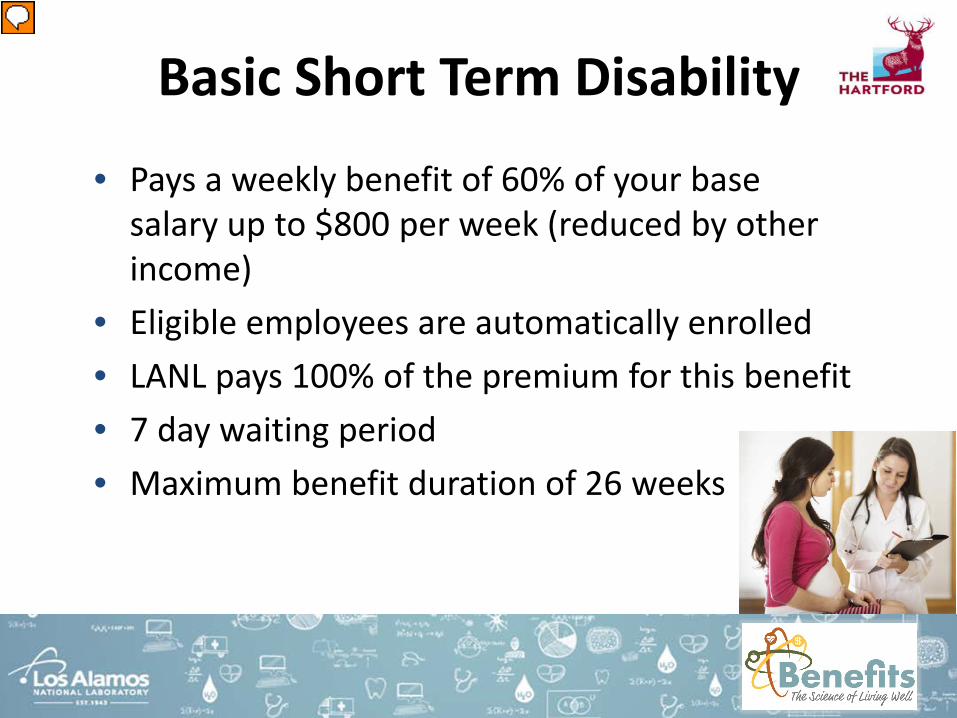

Basic Short Term Disability

• Pays a weekly benefit of 60% of your base salary up to $800 per week (reduced by other income)

• Eligible employees are automatically enrolled• LANL pays 100% of the premium for this benefit• 7 day waiting period• Maximum benefit duration of 26 weeks

Presenter

Presentation Notes

The lab provides a basic Short Term Disability coverage. Eligible employees are automatically enrolled because it is a lab paid short term disability. The weekly benefit is 60% of your base salary up to $800 a week. There is a 7 day waiting period. You will first need to exhaust up to 26 weeks of sick leave before the plan will pay. The maximum duration of short term disability is 26 weeks.

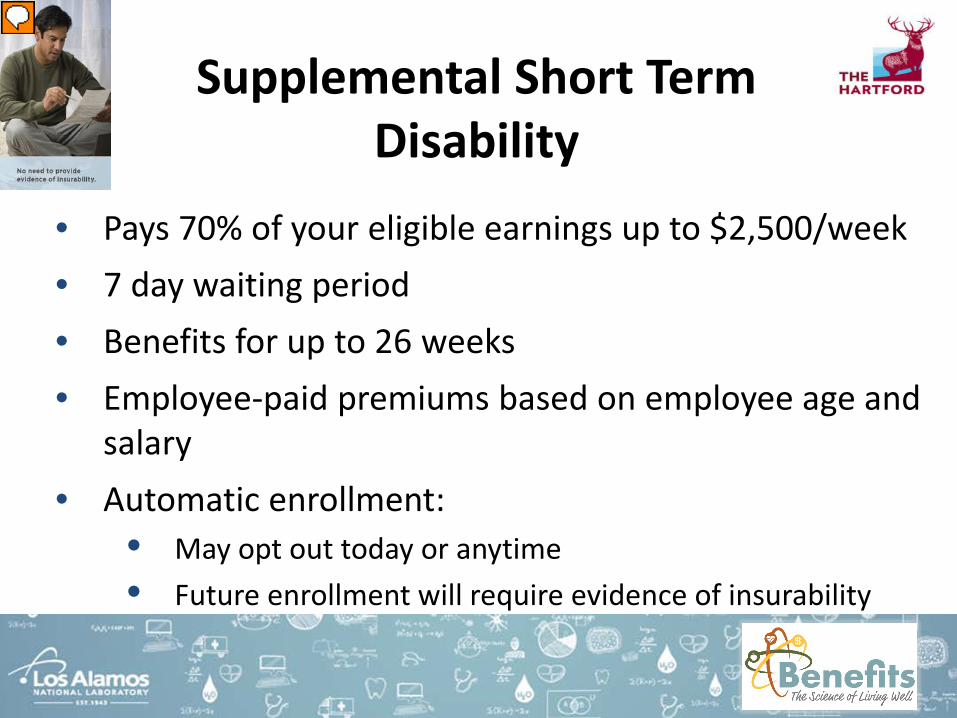

Supplemental Short Term Disability

• Pays 70% of your eligible earnings up to $2,500/week• 7 day waiting period• Benefits for up to 26 weeks • Employee-paid premiums based on employee age and

salary• Automatic enrollment:

• May opt out today or anytime • Future enrollment will require evidence of insurability

Presenter

Presentation Notes

If you wanted a little extra the lab also offers a Supplemental Short Term Disability plan option. This plan will pay 70% of your eligible earnings up to $2,500 a week. Similar in design to the Lab Paid Short Term Disability there is a 7 day waiting period and you will have to exhaust up to 26 weeks of sick leave, if available. The premiums will be based on your age and salary. Page 19 in your handbook. This plan has an automatic enrollment so if you don’t want it you will have to indicate that on your benefits enrollment form. This is your one time opportunity to enroll without having to prove insurability. If you opt out now and want this plan in the future you will have to apply and be approved by Hartford. What happens after 26 weeks?

Long Term Disability

• Pays a weekly benefit of the lesser of:• 50% of your base salary up to $10,000 per month or • 70% of your base salary reduced by other income

• Waiting period of 180 days (26 weeks or 6 months)• Pays up to Social Security normal retirement age • Premiums based on employee age and salary• Automatic enrollment:

• May Opt out today or anytime• Future enrollment will require evidence of insurability

Presenter

Presentation Notes

Dove-tails with the short term benefit. So after the short term plan stops paying at 26 weeks if you still remain disabled you can file for Long term Disability. Long term disability pays a weekly benefit of the lesser of 50% of your base salary up to $10,000 a month or 70% of your base salary reduced by other income (such as social security disability income). This one would begin 180 days after your first date of disability, so it would begin when your short term plan would end. This plan would pay you until your Social Security Normal Retirement Age (mid 60’s, 67, for most). Premiums are based on your age and salary ( refer to page 19 of your handbook) Like the supplemental short term disability this is an automatic enrollment so if you don’t want it you will have to opt out on the form knowing that future enrollment could be denied. This is your one-time opportunity to pick up this coverage without proof of insurability.

Supplemental Disability allows you to take time off to take care of a sick

relative.

Disability True or False Edition

Presenter

Presentation Notes

False- Disability coverage is used to cover your salary if you are unable to work due to you own condition.

Health and Welfare Activity• Guess the Phrase

• Each “row” is a team• Puzzle starts at 25,30, or 40 points• Teams alternate guessing letters, each guess reduces the

puzzle value by 1 point, vowels reduce value by three. Turn passes to next person on next team.

• Solve the puzzle to claim the points for your team• You cannot guess a letter and solve the puzzle on the same

turn.• Three puzzles [on next page]

Presenter

Presentation Notes

We’ve gone over a lot of information today so I think a break is in order. To help you retain the information we’ve gone over we’ve created a Wheel of Fortune game to engage your mind. We will separate into teams. Each team will guess letters, each letter you guess will reduce the puzzle value by one point and vowels will reduce it by 3. To win you must solve the puzzle. You cannot guess a letter and solve a puzzle on the same turn. Let’s start playing! TAKE A BRIEF RESTROOM BREAK AFTER THE GAME IS OVER, APX. 5 MINUTES.

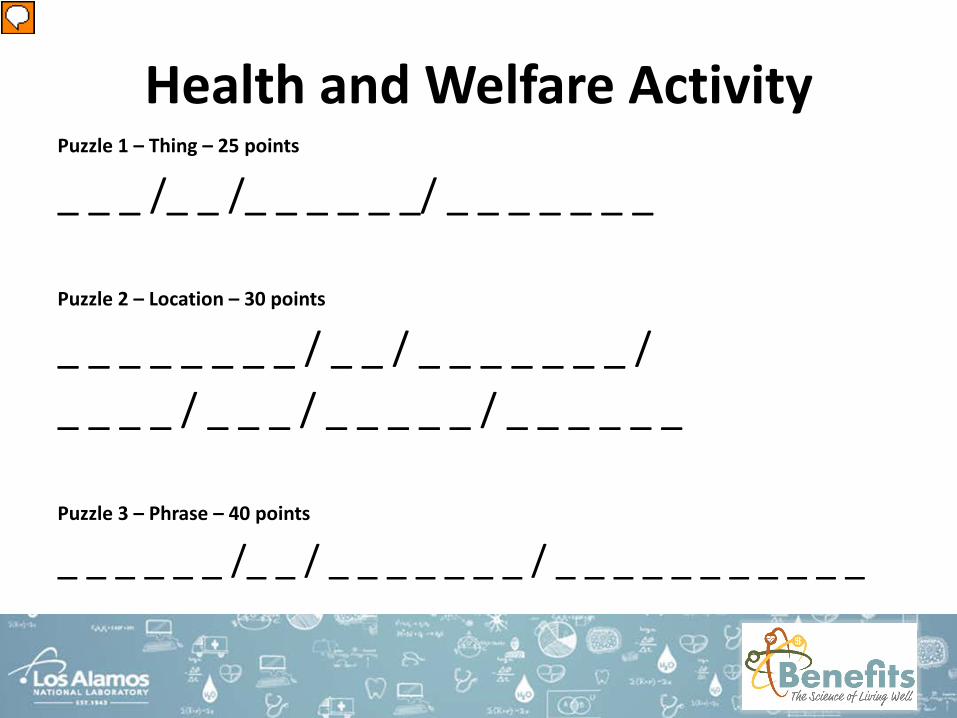

Health and Welfare ActivityPuzzle 1 – Thing – 25 points

Out of Pocket Maximum Benefits is located past the badge office Period of initial eligibility Tie Break: Benefits Start Today

Accidental Death and Dismemberment

(AD&D)

Presenter

Presentation Notes

Another plan option offered by The Hartford is the Accidental Death and Dismemberment insurance or AD&D.

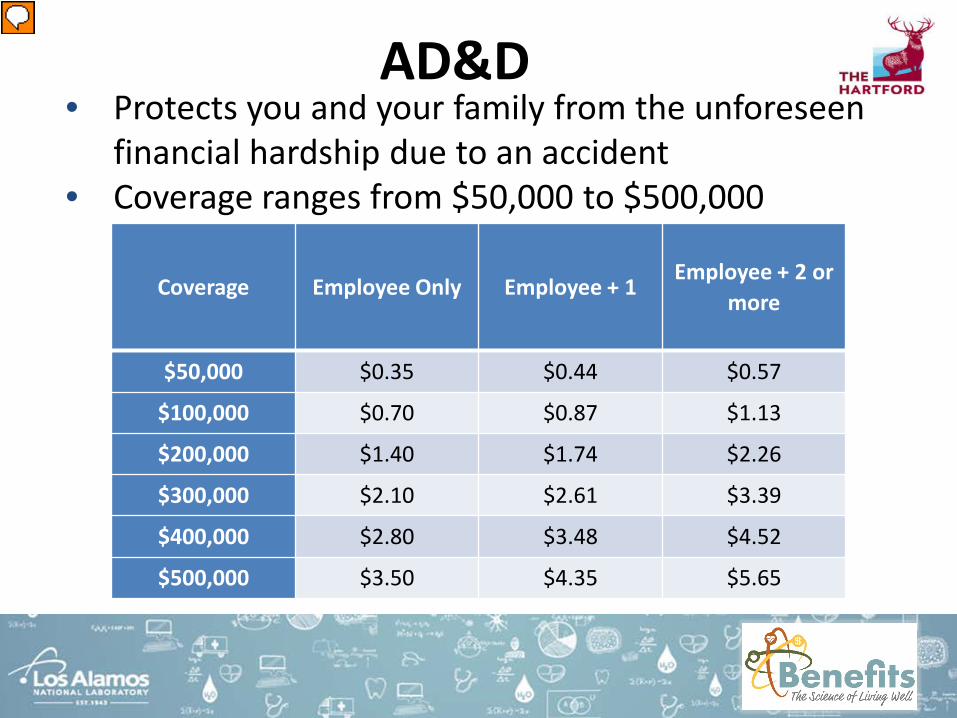

AD&D• Protects you and your family from the unforeseen

financial hardship due to an accident• Coverage ranges from $50,000 to $500,000

Coverage Employee Only Employee + 1Employee + 2 or

more

$50,000 $0.35 $0.44 $0.57

$100,000 $0.70 $0.87 $1.13

$200,000 $1.40 $1.74 $2.26

$300,000 $2.10 $2.61 $3.39

$400,000 $2.80 $3.48 $4.52

$500,000 $3.50 $4.35 $5.65

Presenter

Presentation Notes

AD&D protects you and your family from the unforeseen financial hardship of an accident that causes death, dismemberment, paralysis, and/or loss of sight, speech, or hearing. The AD&D plan is one of the 3 term life options LANL offers. The Lab offers a variety of AD&D coverage levels and options through The Hartford. Coverage levels range from $50,000 to $500,000 and employees can choose to cover eligible dependents. The most expensive option is under $6 for your whole family

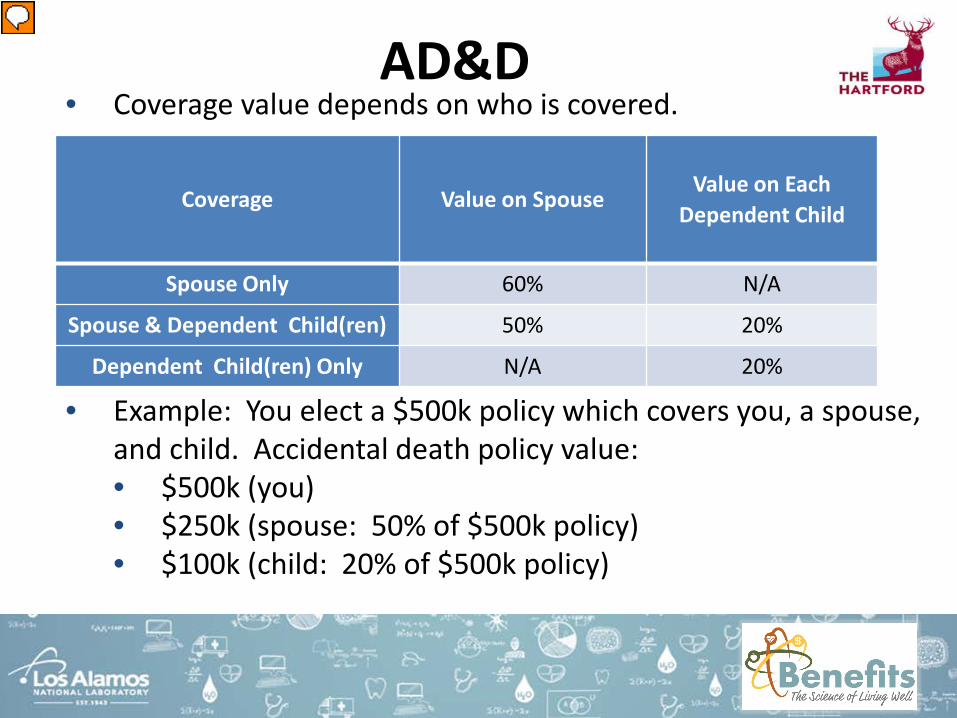

AD&D• Coverage value depends on who is covered.

• Example: You elect a $500k policy which covers you, a spouse, and child. Accidental death policy value:• $500k (you)• $250k (spouse: 50% of $500k policy)• $100k (child: 20% of $500k policy)

Coverage Value on SpouseValue on Each

Dependent Child

Spouse Only 60% N/A

Spouse & Dependent Child(ren) 50% 20%

Dependent Child(ren) Only N/A 20%

Presenter

Presentation Notes

AD&D protects you and your family from the unforeseen financial hardship of an accident that causes death, dismemberment, paralysis, and/or loss of sight, speech, or hearing. The AD&D plan is one of the 3 term life options LANL offers. The Lab offers a variety of AD&D coverage levels and options through The Hartford. Coverage levels range from $50,000 to $500,000 and employees can choose to cover eligible dependents. The most expensive option is under $6 for your whole family

Life Insurance

Presenter

Presentation Notes

Also provided by The Hartford are our Life Insurance plans.

Employee Life Insurance

• Basic Life • 1 times your annual salary, rounded up to next $1,000 (up

to $50,000)• LANL pays 100% of the premium for eligible employees• Automatic enrollment

• Supplemental Life• Options from 1 to 5 times your annual base salary• One time opportunity: guaranteed issue amount (GIA) up

to 3 times your salary• Rates are based on your age and coverage level

Presenter

Presentation Notes

Basic Life�this plan provides life insurance up to 1 time your annual salary with a maximum of $50,000. The premiums for Basic Life insurance are paid by the Lab. Eligible employees are automatically enrolled in this coverage. Supplemental Life�The Supplemental Life plan offers you the flexibility to select the appropriate amount of coverage for you and your family. The cost for this coverage is based on your age and the amount of coverage you select. You can select coverage from 1 time to 5* times your salary. New hires are offered Supplemental Life up to 3 times your annual earnings without evidence of insurability (Statement of Health). If you elect 4 or 5 times, a Personal Health Application form will be sent to you to complete and submit for approval to The Hartford and you will be enrolled in the 3x’s option until you are approved for the higher coverage

Spouse/Domestic Partner Life Insurance

• Employee must enroll in Supplemental Life to enroll spouse/DP

• One time opportunity: GIA at $50,000• Spouse/DP is eligible for up to 50% of employee’s

coverage up to a maximum of $200,000• Rates are based on spouse’s/DP’s age

Example: 3x your salary = $500,00050% = $250,000, but capped at $200,000

Presenter

Presentation Notes

�Dependent Life provides a financial benefit to you in the event you experience the loss of a dependent. You must be enrolled in Supplemental Life to enroll your eligible dependents in Dependent Life. Employees can choose between the basic or expanded coverage level. The cost of this coverage is based on the covered dependents, the plan, and the coverage level you select. Premiums for the Employee Life Insurance options are on page 21 of your handbook.

Child Life

• 2 levels of coverage: $5,000, $10,000• Flat rate, regardless of the number of children covered• Covers dependent child up to age 26

Presenter

Presentation Notes

�Dependent Life provides a financial benefit to you in the event you experience the loss of a dependent. You are the beneficiary of any payout. Premiums for the Employee Life Insurance options are on page 21 of your handbook.

Beneficiaries

• A beneficiary is a person, trust or an estate eligible to receive benefits upon your death.

• Establish these using form 1938• Primary• Contingent

• For all LANL-sponsored insurance policies:• LANL employee life (1x annual pay up to $50k)• Supplemental Employee Life Insurance• AD&D

• Update at any time• Retirement plan beneficiaries are handled by Fidelity Investments

Presenter

Presentation Notes

Submit the form to [email protected] and we will update your beneficiaries for you.

Free Additional Services Provided by The Hartford

• Funeral Planning and Concierge Services by Everest

• Beneficiary Assist® Counseling Services• EstateGuidance® Will Services• Travel Assistance and ID Theft and Protection

Services• Ability Assist® Counseling Services

Presenter

Presentation Notes

In addition to the Disability and Life Insurance options The Hartford also provides these additional services. You must be enrolled in our Long-term Disability plan and have a claim approved by The Hartford to be eligible for Ability Assist.

As a new hire, you can choose to enroll in up to 5X your salary without

evidence of insurability.

Life Insurance True or False Edition

Presenter

Presentation Notes

False – the guaranteed issued is 3x your salary with the option to apply for 4 or 5x.

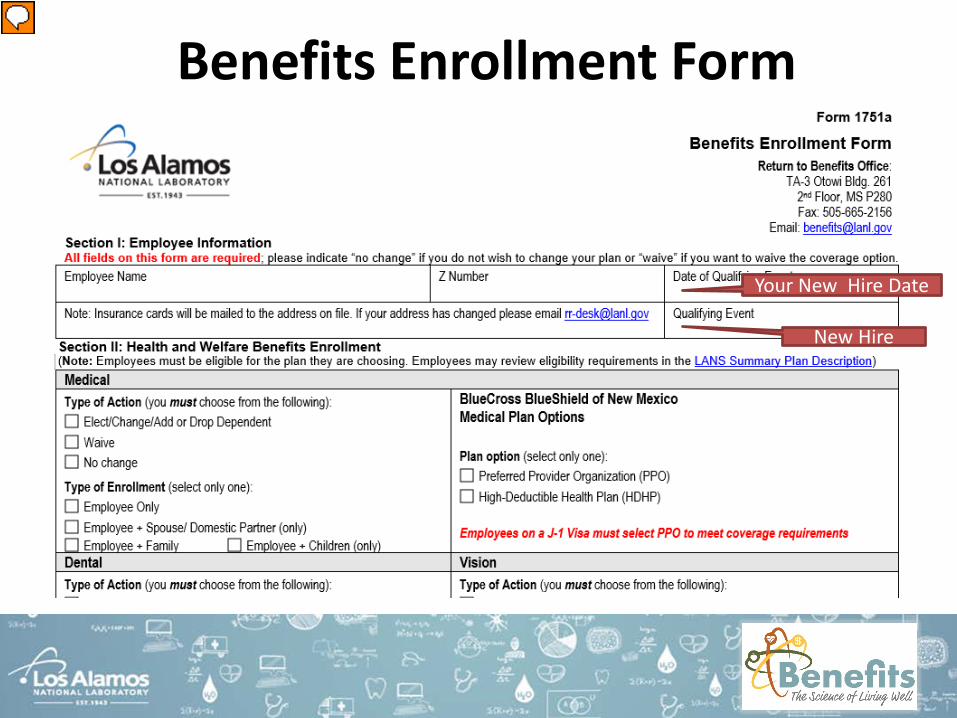

Benefits Enrollment Form

Your New Hire Date

New Hire

Presenter

Presentation Notes

This is an example of the form you all have in your handbook. Please fill this out in order to enroll you and your dependents. Complete all sections telling us: Enrollment or Waiver. Do not use “No Change” as a new hire. Qualifying event is NEW HIRE. Date of qualifying Event is YOUR NEW HIRE DATE.

Wellness

Presenter

Presentation Notes

LANL cares about our Wellness as employees. We have programs throughout the year to engage our employees in their financial, emotional, and physical wellness. We have health fairs, classes, a great wellness facility and many other opportunities to engage in our wellness. How this ties to your benefits is through our Virgin Pulse Wellness program. These following slides will educate you on how your choices in living a healthy lifestyle can add to the richness of your LANL benefits.

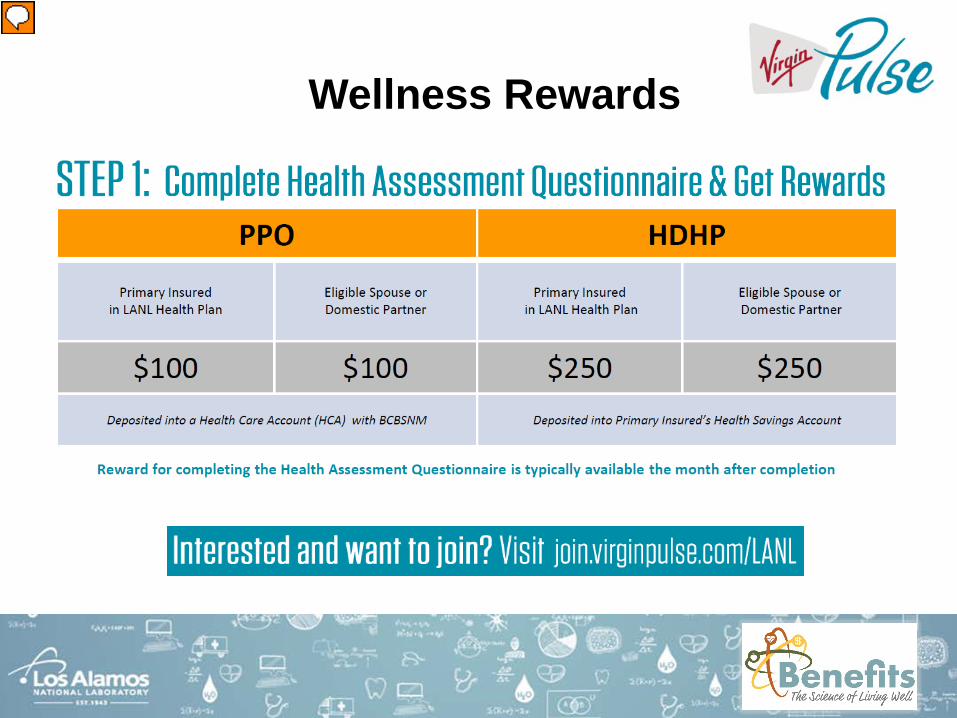

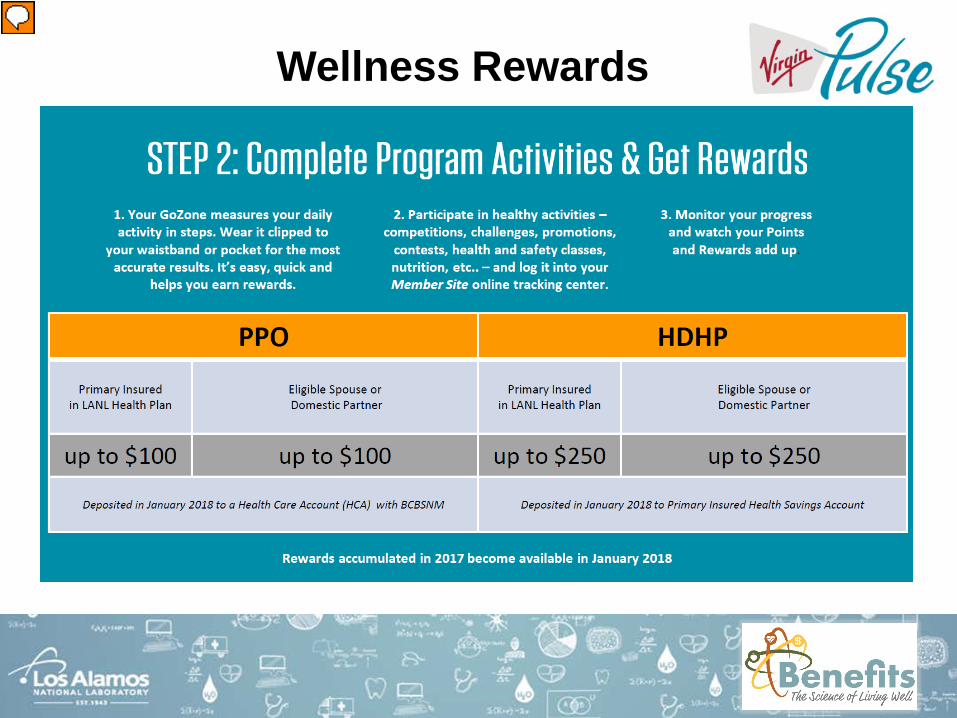

Wellness Rewards

Presenter

Presentation Notes

You should be receiving an email from the wellness program in the coming weeks telling you how to enroll. You should not complete your HAQ until you are enrolled in your medical option. After you enroll in the program you can earn the first incentive by completing the Health Assessment Questionnaire (HAQ). A person will receive $100 or $250 depending on which plan they are signed up for. Eligible ENROLLED spouses or domestic partners can also sign up and earn incentives for completing the Health Assessment Questionnaire. Your spouse or partner cannot participate if they are not enrolled on your medical coverage. HDHP – deposited into the Health Savings Account (HSA); so you must enroll for the HSA to get the contribution (even at $0/pay). PPO – Deposited into the Health Care Account (HCA) managed by BCBSNM

Wellness Rewards

Presenter

Presentation Notes

Participants also earn incentives by participating in health related activities to Earn Health Miles towards incentives. Depending on which health plan a person is signed up under, they can earn up to $100 or $250 for participation in health related activities. All participants are provided with a “GoZone” pedometer to track their steps. Note: Eligible spouses and domestic partners are also eligible to earn incentives for participating in health related activities. Spouse/Domestic partner must be a dependent on the employee’s medical plan to participate.

• Variety of ways to earn points• Make healthy decisions every day!• The more healthy decisions you make, the more you earn.• Attend the monthly “How to Maximize Your Virgin Pulse

Points” seminar, held the last Thursday of each month and earn 250 points!

Wellness Rewards

Presenter

Presentation Notes

Physical Activity Learning with daily cards based on your set interests Challenges Tracking a variety of Healthy Habits Attending informational sessions and other LANL events Tracking your nutrition via MyFitnessPal The Wellness Center will be sending you an e-mail invitation to attend their course “How to Maximize your Virgin Pulse Points”. Earn a 250 point voucher to kick-start your rewards. Tracking your sleep at home (via FitBit) On-site FitBit is only allowed at the Wellness Center

Wellness Rewards

• Where is the money deposited?

Preferred Provider Organization

(PPO)

Health CareAccount - HCA

High Deductible Health Plan

(HDHP)

Health Savings Account – HSA

Presenter

Presentation Notes

Where the money is deposited. BCBS HCA – It is deposited into your BCBS HCA, housed at BCBS and applied to your co-pays and co-insurance before you pay out-of-pocket. HDHP HSA – It is deposited into your HSA account with HSA Bank. Even if you don’t want to make any payroll contributions, you still must open an account with HSA Bank. On enrollment form, indicate I am selecting/choosing an HSA and you can put a $0 for payroll deductions.

Your Spouse/Domestic Partner must be a LANL employee in order to receive the wellness incentives.

Wellness True or False Edition

Presenter

Presentation Notes

False- Your Spouse/Domestic Partner does not have to work at LANL to participate.

Savings and Retirement

Saving For the Future

• Will you be prepared for retirement?

• Let LANL help you start saving today!

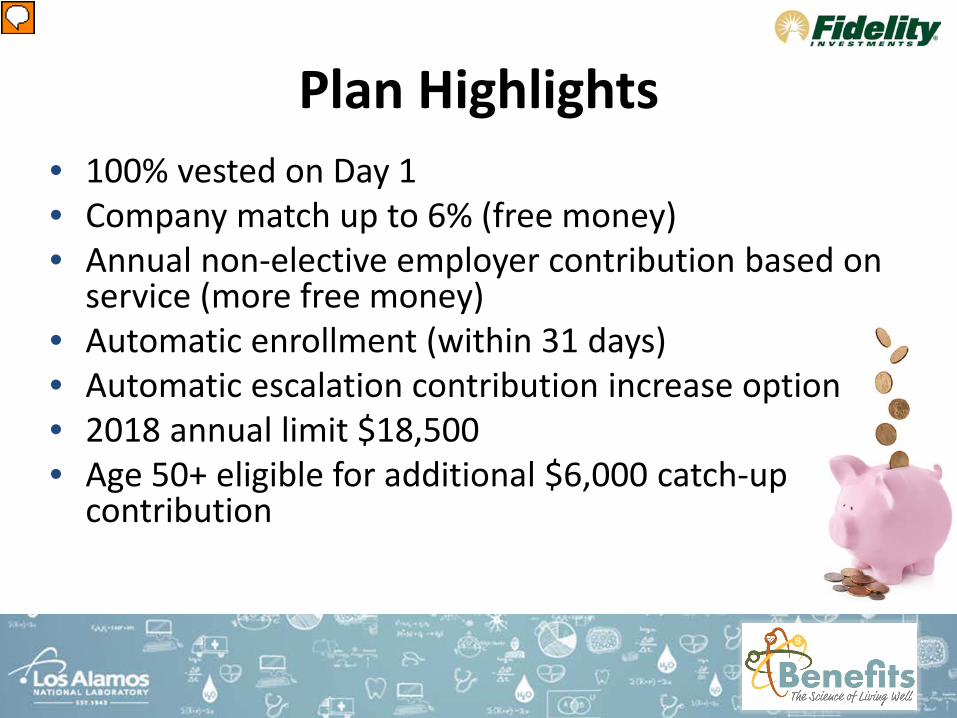

Plan Highlights• 100% vested on Day 1• Company match up to 6% (free money)• Annual non-elective employer contribution based on

service (more free money)• Automatic enrollment (within 31 days)• Automatic escalation contribution increase option • 2018 annual limit $18,500 • Age 50+ eligible for additional $6,000 catch-up

contribution

Presenter

Presentation Notes

LANL is just as invested as you are in saving for your future and has so many vehicles to help you get started. Company Match: We offer a 6% dollar for dollar company match which is free money An annual non-elective employer contribution which is also free money In our retirement plan, you are 100% vested in the 401(k) on day one. Other companies may ask you to be vested in their plan for a certain amount of years. But not us, you are vested 100% today. Administrative Fees: Our 401k plan has extremely low administration fees and get this LANL will pay for both the administrative and recordkeeping fees on your account until balance is greater than $25,000. Because this plan is so great, we don’t want anyone to miss out. We automatically enroll all our new employees in the 6% contribution after 31 days of your new hire. If you would like to get a jump start on saving sooner you can. LANS 401(k) Retirement Plan offers several contribution options to help you save your money like the pre-tax, after-tax, Roth 401(k), and catch-up contribution options. And in addition the plan offers rollover, loan, and different withdraw options

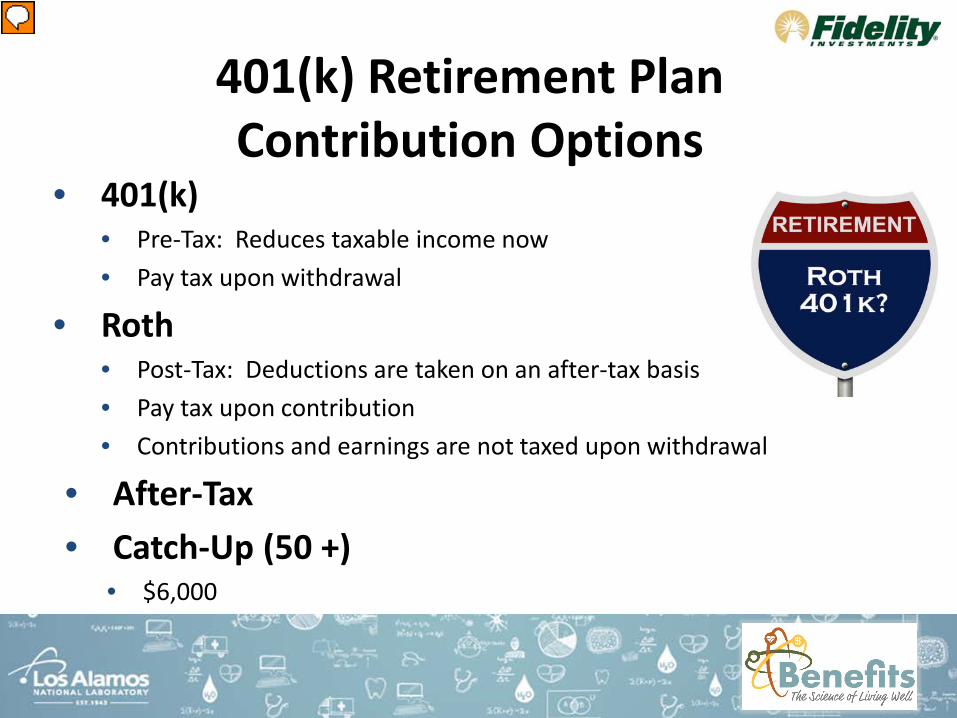

401(k) Retirement Plan Contribution Options

• 401(k)• Pre-Tax: Reduces taxable income now• Pay tax upon withdrawal

• Roth• Post-Tax: Deductions are taken on an after-tax basis • Pay tax upon contribution• Contributions and earnings are not taxed upon withdrawal

• After-Tax • Catch-Up (50 +)

• $6,000

Presenter

Presentation Notes

These are our contribution options: The pre-tax contribution allows you to save and invest a piece of your paycheck before taxes are taken out. (on a pre-tax basis). Taxes are not paid until the employee starts withdrawing the money from their 401(k). Again we have the Company match up to 6% of eligible compensation and the automatic enrollment in 6% after 31 days. Make note that there are IRS limits for the 401(k) plan and for 2018 that is $18,500. LANS also offers a Roth contribution option: The Roth contribution allows you to save and invest a piece of your paycheck after taxes are taken out (On a after-tax basis). Roth can be used in combination with the pre-tax 401(k) and the same IRS limits apply. If the employee meets the annual pre-tax contribution limit for the year they can elect to continue contributions on an after-tax basis. After-tax contributions like the pre-tax contributions are deducted from your salary after applicable taxes are withheld. The catch- up contribution is for individuals who are age 50 or over. At the end of the calendar year can they make an annual catch-up contributions up to $6,000.

Presenter

Presentation Notes

So by now you might be asking yourself, “what does all this mean?” Well here’s a short video that may help you make things more clear. – Show Video embedded on computer/ USB drive.

Years of Completed Service % of Employer Contribution0-9 3.5%

10-19 4.5%20+ 5.5%

Non-Elective Employer Contribution

• Free money (no contributions required)• Based on service and eligible compensation• Paid annually (first quarter of the following year)

Presenter

Presentation Notes

Krista find piggy bank or money icon of some sort Non-elective employer contribution In addition to the of 6% company match, you will also receive an annual non-elective employer contribution. Or as I like to call it…Free Money. You are automatically enrolled in this plan regardless of your contributions to the 401(k) Retirement Plan. LANS will make a "non-elective" employer contribution each plan year for each eligible employee. The amount of the non-elective employer contribution is based on your years of service and your eligible compensation. This money is paid annually and is deposited the quarter after the completed year. - For Example: You will receive 2017 NEC the first quarter of 2018. The non-elective employer contribution for an eligible employee is designed as follows: Demonstrate Chart.

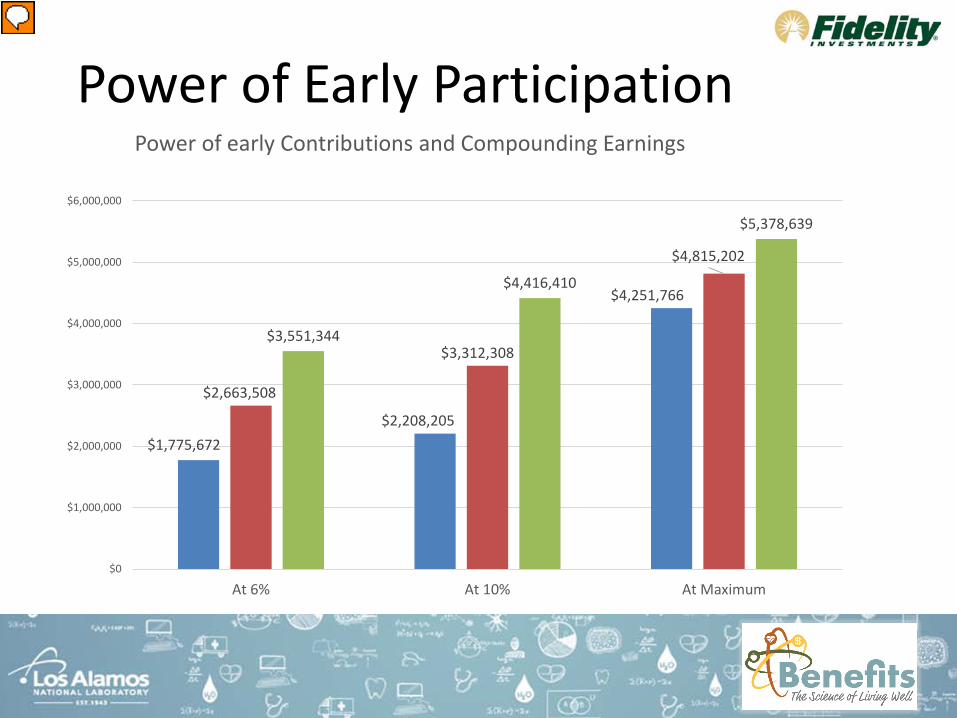

Power of Early Participation

$1,775,672$2,208,205

$4,251,766

$2,663,508

$3,312,308

$4,815,202

$3,551,344

$4,416,410

$5,378,639

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

At 6% At 10% At Maximum

Power of early Contributions and Compounding Earnings

Presenter

Presentation Notes

Assumptions: Start at age 25 ends Age 65 (40 year Career) $50K (Blue), $75k (Orange), or $100k (Grey) annual base salary to start 2% annual raise over career 6% Average growth in Investments over 40 years 6% Employer Match Increasing Non Elective Employer Contribution: (3.5% 0-9 yos, 4.5% 10-19 yos, 5.5% 20 and more yos) Maximum Contribution is $18k per year until age 50 then $24k per year

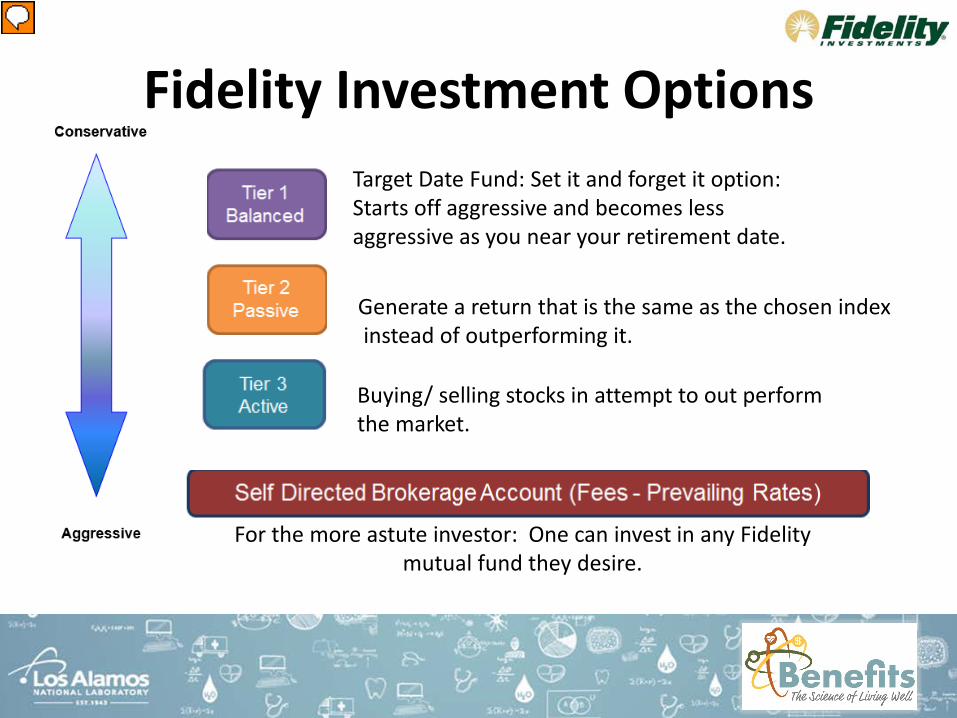

Fidelity Investment OptionsTarget Date Fund: Set it and forget it option: Starts off aggressive and becomes less aggressive as you near your retirement date.

Generate a return that is the same as the chosen indexinstead of outperforming it.

Buying/ selling stocks in attempt to out perform the market.

For the more astute investor: One can invest in any Fidelity mutual fund they desire.

Presenter

Presentation Notes

Here are some investment plan options that Fidelity Investments offers. Tier 1 - Target Date Funds AKA Set it and forget it fund. - This option operates under an asset allocation formula that assumes you will retire in a certain year, and adjusts its asset allocation model as you get closer to that year. So in other words, it starts off aggressive and becomes less aggressive as you near your retirement date Tier 2 – Passive Portfolio Management This option involves the creation of a portfolio allocation that is the same as a specific index. The purpose is to generate a return that is the same as the chosen index instead of outperforming it. Tier 3 – Active Portfolio Management - Allows managers or brokers to buy and sell stocks in an attempt to out preform a specific index. Self Directed Brokerage Account – - An investment option that allows the investor more options outside of the core options that their employer provides. The give more control to the investor. It also carries the most risk. For more information on these plans, call Fidelity Investments

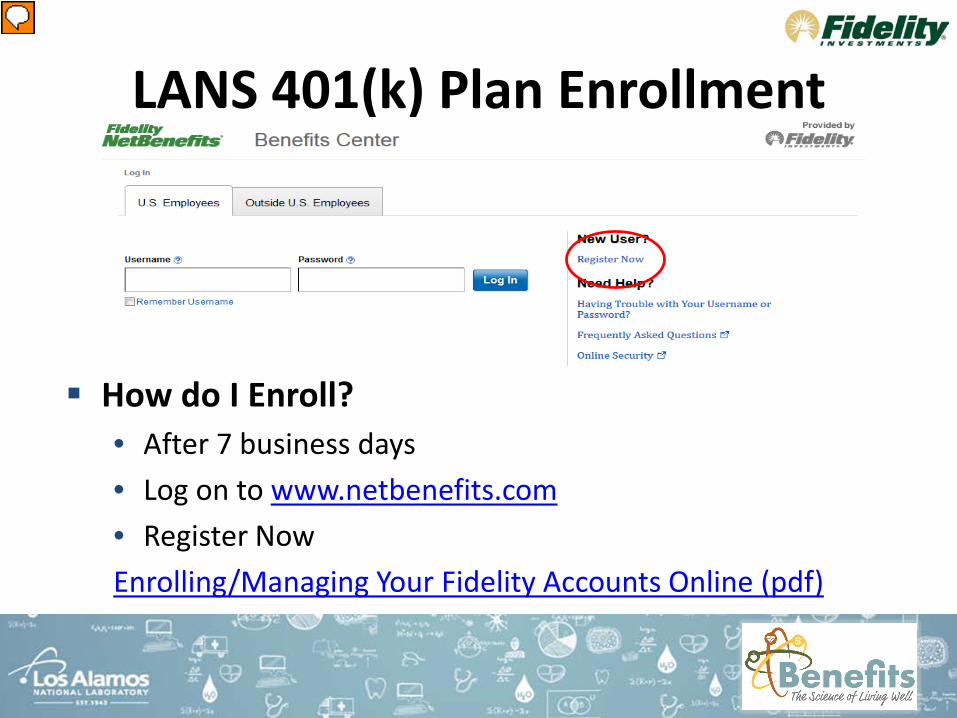

LANS 401(k) Plan Enrollment

How do I Enroll?• After 7 business days• Log on to www.netbenefits.com• Register NowEnrolling/Managing Your Fidelity Accounts Online (pdf)

Presenter

Presentation Notes

Let me show you how to get started by enrolling in your 401(k) fidelity account. After 7 business days, you can log on to www.netbenefits.com and click on register now. Once you are register in your account you can stat choosing your contributions, picking investment options, and watching your money grow.

• Fidelity• Online financial support tools• Financial advice through Fidelity

• Other Resources

Financial Health Assessment Tool

Presenter

Presentation Notes

Here are some other ways to start taking charge of your future now Yearly, LANL offers additional savings and retirement via classes, expos, presentations, vendor talks, These are always a great opportunity for employees to come out and learn more about investing in their futures. For upcoming classes, head to the benefits website and sign up to attend. Fidelity's also offers a slew of information on their website. You can access their financial support tools, calculators, or meet face to face with a representative to discuss your retirement and investment options. Lastly there are many resources out there provided to you to help you make your investment and retirement decisions. A great resource that we often use here is GuideSpark. GuideSpark allows you to gage your financial heath and give suggestions on how to get yourself into a better financial state. There are several on topics they touch on like retirement, savings, budging, debit management and so much more. If you are interested in this site, please go onto our benefits website and create yourself and account.

Savings and Retirement True or False Edition

LANS provides an employer matching contribution up to 6% of your eligible

compensation every payroll.

Presenter

Presentation Notes

True – Yes LANS will match your contributions up to 6% of your eligible compensation. You may choose to make changes to the amounts you contribute throughout the year if you wish by logging on to netbenefits.com. And with that, I will turn it back over to __________ and he/she will conclude the presentation.

Important Dates• Coverages effective on day 1• Period of Initial Eligibility reminder• Payroll deductions are taken twice a

month• Carrier files sent every Thursday morning• Auto enroll in 401(k) 31 days from hire

date• Reminder: 31 days for life event changes• Use the checklist in your handouts

Presenter

Presentation Notes

Your coverage is effective on your date of hire (day 1), as long as you submit your completed enrollment form and supporting documentation within your 31 calendar day enrollment period. Your Period of Initial Enrollment Ends _____________________ Our carrier files are sent every Thursday morning, so enrollment forms received on Thursday or after will wait for the next carrier file. If you need to obtain services before your enrollments have been processed and received by the carrier, you will need to pay out of pocket and file for reimbursement. Explain how many pay periods could be missed if they do not sign up for their 401(k) prior to 31 day auto enrollment.

Legal NoticesContinuation Coverage Rights Under COBRA Notice

Premium Assistance under Medicaid and the CHIP Program

Notice from LANS about Your Prescription Drug Coverage and Medicare

Women’s Health and Cancer Rights Act (WHCRA)

Wellness Reward Alternative Notice

HIPAA Special Enrollment Rights

Health Insurance Marketplace Coverage Options

Presenter

Presentation Notes

These are some required notices we are supposed to give to you. They are on the last pages of your booklet. Please review these at your leisure and sign the Acknowledgement form that you have received the notices.

ID cards• Will receive cards within 3 weeks of completing

enrollment:• Medical • HSA• Flexible Spending Account (HCRA only)

• Legal

• Dental and Vision:• No Cards

Presenter

Presentation Notes

Data files are sent to our carriers every Thursday on a weekly file feed. As long as the benefits department receives your form by Wednesday at noon it will go over on the Thursday file feed. Within 3 weeks of submitting your form you will receive a card for your Medical insurance, your HSA (if you participate), Connect Your Care for your FSA, and a Legal insurance card from ARAG Delta Dental and VSP do not issue cards. When you make an appointment with a provider they will run your information through the system to verify your enrollment in the plans.

• Phone 505-667-1806 • Provider Contact Information

Presenter

Presentation Notes

Please view our website for answers to many of your questions. You can email us at [email protected] or call us at 667-1806. Our hours are Monday through Thursday 8-5 and Fridays we are open until 4pm. This is the end of the benefits presentation. Does anyone have any questions?