Embed Size (px)

Citation preview

Latam Tigers Fund October 2014

Roadshow Presentation

2

EuroAmerica Investments

• Introduction

• The Opportunity

• Case Studies

• Fund Details

• Annex

3

EuroAmerica Investments

• Introduction

• The Opportunity

• Case Studies

• Fund Details

• Annex

4

Introduction

Source: EuroAmerica.

President Bachelet Chile

President Santos Colombia

President Peña Nieto Mexico

President Humala Peru

President Rouseff Brazil

President Maduro Venezuela

President Kirchner Argentina

5

Introduction: Investment Rationale

Source: EuroAmerica.

• Invest in listed Equity of fast growing & increasingly politically stable Economies. Best of Latam: As of today – Colombia, Peru & Chile (Andeans) and Mexico.

• Capture Growth of rising Consumer base: Focus on growing local demand.

• Benefit from favorable institutional and economic developments: Pacific Alliance.

• Common Stock Exchange (MILA) improves liquidity for larger markets.

• Strong domestic consumption growth due to an increase in real wages, demographics and improvements in income distribution.

• Solid Infrastructure pipeline on the horizon.

• Modern and growing Pension Funds environment.

• Political reforms underway as a result of growing world market interconnection.

• Strong IPO Pipeline in place (offering entrepreneurs a better way of growing their businesses).

• Strengthening Corporate Governance as a result of PFs acting as corrective shareholders.

• Offer True Alternative to Brazil and/or second Building Block to cover the whole Latam Region.

• Bottom-up Investment Style requires Local Fund Managers.

6

30,3%

21,7%8,3%

7,9%

6,7%

5,8%

4,4%

9,2%

5,7%Financial

Consumer & Retail

Logistics

Transportation

Food & Beverage

Cement

Construction

Others

Cash

34,3%

20,6%

20,4%

16,5%

2,4%5,7%

Mexico

Chile

Peru

Colombia

Argentina

Cash

Introduction: Latam Tigers Portfolio as of September 22nd, 2014

Source: EuroAmerica.

Breakdown by Country Breakdown by Sector

7

00

50

100

150

200

250

300

jun

-09

en

e-1

0

ago

-10

mar

-11

oct

-11

may

-12

dic

-12

jul-

13

feb

-14

sep

-14

Model Portfolio Base 100

Latam Tigers Portfolio Serie I (USD)

Latam Tigers I Series Statistics (USD)

Accumulated Return 146,7%

Annualized Return 18,8%

Max Monthly Return 20,5%

Min Monthly Return -17,6%

Monthly Volatility 6,1%

Annual Volatility 21,0%

P/E 15,7x

EPS Growth 14,7%

Expected Return (USD) 10-15% p.a. Over 10Y

Introduction: Model Portfolio

Source: Bloomberg and EuroAmerica.

Model Portfolio + Latam Tigers Historic Returns (USD)

Average Market Cap

Market Cap Fund Positions (%)

<1.0bn 8,4%

1.0bn<2.5bn 24,1%

2.5bn<5.0bn 13,9%

5.0bn<10bn 26,6%

>10bn 27,5%

Total holdings 34

8

Introduction: Performance as of September 22nd, 2014

Source: Bloomberg and EuroAmerica.

Latam Tigers Series I (USD)

75

80

85

90

95

100

105ab

r-1

3

may

-13

jun

-13

jul-

13

ago

-13

sep

-13

oct

-13

no

v-1

3

dic

-13

ene

-14

feb

-14

mar

-14

abr-

14

may

-14

jun

-14

jul-

14

ago

-14

sep

-14

Latam Tiger Serie I USD

Jun

2013 N/A N/A N/A N/A -5,4% -6,1% -2,8% -3,9% 6,6% 2,7% -3,7% 2,9%

2014 -7,8% -1,6% 5,7% 2,7% 4,0% 1,4% -0,3% 0,2% N/A N/A N/A N/A

Inception

3,7%0,2% 1,3% 14,3% 12,6%I (USD)

Cumulative

MayJan Feb Mar AprMonthly

1M 3M 6M

Dic

-7,1%

Year

-10,4%

Jul Ago Sep Oct Nov

3,7%

1Y YTD

9

Introduction: Currencies

Source: EIU Big Mac Index, and EuroAmerica.

• Independent Central Banks.

• FX Reserves at High Levels.

• Solid Fiscal Position.

• Additional FX Depreciation Risk is Limited.

12

34

56

78

910

1112

1314

1516

1718

1920

2122

2324

2526

2728

2930

3132

INR

ZA

R

MY

R

HK

D

IDR

RU

B

TW

D

CN

Y

PLN

TH

B

MX

N

CZK

PE

N

JPY

PH

P

CLP

HU

F

SG

D

KR

W

TR

Y

CO

P

US

D

AU

D

GB

P

NZD

EU

R

ILS

CA

D

BR

L

SE

K

CH

F

NO

K

Undervalued

Neutral

Overvalued

Currency Valuation Ranking

Equity FX

Chile -1,5% -5,6%

Mexico 5,1% -2,4%

Peru -1,1% -1,7%

Colombia 3,0% -1,1%

Argentina 0,3% 0,0%

Fund performance - ITD

10

EuroAmerica Investments

• Introduction

• The Opportunity

• Case Studies

• Fund Details

• Annex

11

0

0,5

1

1,5

2

2,5

3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mexico China

The Opportunity: Mexico

Source: JPM, World Bank, ILO, and EuroAmerica.

• Largest Market in Latam after Brazil: In the 2010 population census Mexico had around 112.3mn people -the 11th-largest population in the world. Close to 48% of the population is under 25 years old. Yet to become new entrants to the Labor force and new consumers. Exposure through: Banorte, Bachoco and Walmex.

• Market Size /U.S. Proximity: Potential mobilization of industrial and manufacturing processes from the U.S. to Mexico due to lower labor costs. Additionally, remittances are the second-largest source of FX after exports, close to 90% of the remittances end up in consumption. Exposure through: Sanborns, Walmex & Liverpool.

Population Pyramid Labor Costs Comparison

USD

/ho

ur

- 2,0 4,0 6,0

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90+

Male

- 2,0 4,0 6,0

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90+

Female

Population (in millions)

12

Bank Credit to Private Sector (% GDP)

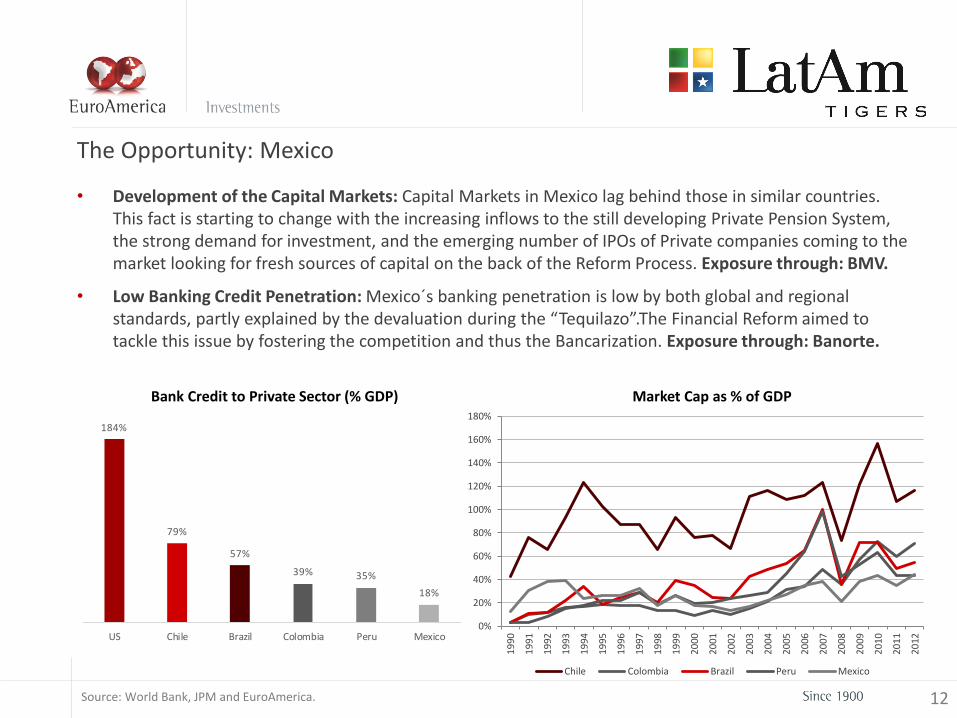

The Opportunity: Mexico

Source: World Bank, JPM and EuroAmerica.

• Development of the Capital Markets: Capital Markets in Mexico lag behind those in similar countries. This fact is starting to change with the increasing inflows to the still developing Private Pension System, the strong demand for investment, and the emerging number of IPOs of Private companies coming to the market looking for fresh sources of capital on the back of the Reform Process. Exposure through: BMV.

• Low Banking Credit Penetration: Mexico´s banking penetration is low by both global and regional standards, partly explained by the devaluation during the “Tequilazo”.The Financial Reform aimed to tackle this issue by fostering the competition and thus the Bancarization. Exposure through: Banorte.

Market Cap as % of GDP

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Chile Colombia Brazil Peru Mexico

184%

79%

57%

39% 35%

18%

US Chile Brazil Colombia Peru Mexico

13

The Opportunity: Mexico

Source: Pemex.

• Mexican Reforms: During the past year Mexico overcame a mostly expected Reform Process, tackling 7 major issues for the country - Education, Financial, Telecom, Fiscal, Political, Labor, and the most relevant one, the Energy Reform: Mexico will increase its potential GDP by over 1% in the medium term with the Energy Reform. Even though there are no directs plays to tackle this sector yet, we expect they will arrive to the Capital markets in the next couple of years. Exposure through: ASUR, and Cementos Moctezuma.

New Framework for the Energy Sector in Mexico

14

The Opportunity: Colombia

Source: JPM, World Bank and EuroAmerica.

• Emerging Middle Class: Close to 2mn households have joined the ranks of the country´s middle class over the past decade, doubling its size, and it is expected to double again in the next ten years. Consequently, the country has experienced strong growth in private consumption, which now accounts for close to 61% of GDP. Exposure through: Exito and Bancolombia.

• Informality: Colombia’s labor informality is estimated at 58% and its unemployment rate is one of highest in the region. We would expect penetration to increase gradually over time, not only as the level of formality increases but also as new reforms (payroll taxes) and job creation initiatives are implemented. Exposure through: Bancolombia, Grupo Sura and Exito.

Supermarkets Penetration Latam Population by Socio-Economic Level

Argentina

Chile Mexico

Brazil

Colombia

Peru

0

20

40

60

80

100

120

140

4.000 6.000 8.000 10.000 12.000 14.000 16.000

Are

a M

2 p

er

1,0

00

po

ps

GDP per capita (US$)

Formal 48%

Informal 52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

BR CL CO MX PE

Poor Vulnerable Middle Class Upper Class

15

The Opportunity: Colombia

Source: DANE, Exito and EuroAmerica.

• Peace Process & Infrastructure: Due to historical reasons, a complex geography and 50 years of FARC´s war on infrastructure, Colombia lacks of adequate infrastructure. The Government has a US$55bn infrastructure Agenda that tackles this major issue for the Country. An improvement in this sense would not only imply an increased competitiveness for Colombia but better connectivity and access to untapped markets. Exposure through: El Condor and Cementos Argos.

• Access to Central America: Colombia serves as entrance to High Growth Non-Traditional Markets in Central America. In recent years Colombian companies have looked to Central America as the natural expansion. Exposure through: AviancaTaca, Bancolombia, Cementos Argos.

4G Concessions Program

Existing concessions

New concessions

Central America´s Potential

3,9%

6,8%

4,0% 4,1%3,5% 3,1%

1,7%

Central AmericaPanama Nicaragua Costa Rica Guatemala Honduras El Salvador

4.469

10.838 10.433

3.875 3.513 2.323 1.840

Central AmericaPanama Nicaragua Costa Rica Guatemala Honduras El Salvador

Real GDP CAGR 13-16E

GDP / Capita (US$)

Real GDP

CAGR 11-134,4% 9,4% 4,7% 4,3% 3,2% 3,2% 1,8%

Population

(Mn)44,5 3,7 4,8 6,3 15,5 8,1 6,1

16

The Opportunity: Peru

Source: ProInversión, EuroAmerica.

• Accelerated Growth Rhythm: Peru’s economy continues to be a leader in high growth and low inflation in the region, which has been achieved through a prudent macroeconomic policy implementation, and a far-reaching structural reform agenda. Exposure through: InRetail, IFS and Credicorp.

• Infrastructure Deficit: According to the National Infrastructure Association, Peru has an estimated infrastructure deficit of US$88bn, being 90% of the deficit in transportation and energy. The government recently announced an ambitious plan for 2014-18. Exposure through: Pacasmayo and Graña y Montero.

Projects in the Transportation Sector (US$bn) GDP Growth (Base= 100)

11,5

0,8

7,6

0,5

Total road andhighways

Total Airports Total Railways (inc.Subway)

Total Ports

90

110

130

150

170

190

210

230

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Chile Colombia Brazil Peru Mexico

17

0

100

200

300

400

500

600

700

0 5.000 10.000 15.000

52% 2% 6%

3%

46%

32%

19%

1st Quartile

2nd Quartile

3rd Quartile

4th Quartile

• Highly Competitive in Metals & Mining: Peru is one of the world´s biggest producers of base and precious metals. Currently its is the third largest producer of copper and zinc in the world. Additionally, it is also a major producer of gold, and silver among other minerals. The success of Peru’s mining sector stems not only from an abundance of rich natural resources, but also from an attractive legal and tax regime designed to support the industry.

• Peru´s Mining investment pipeline considers close to US$55bn of investment in projects and mining related infrastructures focused on three minerals: Copper, Gold and Iron. Exposure through: Ferreyros, and Graña y Montero.

The Opportunity: Peru

Source: Mckinsey&Co, Wood Mackenzie and EuroAmerica.

% of Peruvian Production on the Copper Cash Cost Curve

40%

% of Peruvian Production per Quartile for Each Mineral

51%

9%

31%

9%

1st Quartile

2nd Quartile

3rd Quartile

4th Quartile

35%

13%

47%

5%

1st Quartile

2nd Quartile

3rd Quartile

4th Quartile

Gold Zinc Lead

Kt

c/lb

1st Quartile 2st Quartile 3rd Quartile 4th Quartile

18

The Opportunity: Chile

Source: Bloomberg, IDC, EuroAmerica.

• Regional Platform: Chilean companies have become major investors in the sectors they lead within the Region, transforming themselves into Pan-Latam Players in underpenetrated industries. Exposure through: Falabella, and Cencosud.

• Access to sectors not present in the Region: Through investing in Chilean Companies, one can invest in sectors not present in the rest of the Region such as healthcare, IT or homebuilders. Exposure through: Sonda, Banmedica and Socovesa.

IT Spending as a Percentage of GDP Percentage of Sales Outside of Chile Excluding Exports

As of June’14 Chile Rest of Latam Rest of the World

CFR 19,4% 76,2% 4,4%

Andina 28,2% 71,8%

Cencosud 35,3% 64,7%

Sonda 37,0% 63,0%

LATAM Airlines 12,3% 58,0% 29,7%

Falabella 62,5% 37,5%

Embonor 63,4% 36,6%

Parauco 65,7% 34,3%

Ripley 66,0% 34,0%

Banmedica 75,2% 24,8%

CCU 81,1% 18,9%

Forus 82,6% 17,4%

SK 66,1% 12,0% 21,9%

GD

P/C

apit

a (U

SD0

00

)

IT Spending / GDP (%)

19

The Opportunity: Argentina

Source: EuroAmerica, Financial Times.

• We believe Argentina is on the verge of a turn around and we should see some opportunities ahead.

20

The Opportunity: Argentina

Source: EuroAmerica, Company Data.

• Political Change

• Macro stabilization

• Assets converted to real prices

• Investment expansion on the Oil sector

• As a first approach to the Argentinean equity market, we decided to build a position on Grupo Galicia, one of the leading private financial groups in the country, with local funding, high income from fees and a strong position in the Credit Card business.

0%

4%

8%

12%

Galicia Cons. Santander Macro BBVA HSBC

Grupo Galicia – Business Structure Market Share – Loans to Private Sector

21

The Opportunity

Source: Bloomberg and EuroAmerica.

• The Portfolio is trading at 18,2 times last 12 months earnings.

Portfolio Trailing LTM P/E Evolution

10,0x

11,0x

12,0x

13,0x

14,0x

15,0x

16,0x

17,0x

18,0x

19,0x

20,0x

Dec

-10

Feb

-11

Ap

r-11

Jun

-11

Au

g-11

Oct

-11

Dec

-11

Feb

-12

Ap

r-12

Jun

-12

Au

g-12

Oct

-12

Dec

-12

Feb

-13

Ap

r-13

Jun

-13

Au

g-13

Oct

-13

Dec

-13

Feb

-14

Ap

r-14

Jun

-14

Au

g-14

22

EuroAmerica Investments

• Introduction

• The Opportunity

• Case Studies

• Fund Details

• Annex

23

Case-Studies: How to Find Value in Latam and How to Avoid Accidents

Source: EuroAmerica.

Intense bottom-up Research led by 5 Senior and 3 Junior Analysts. The former 5 being constantly on the road to visit companies.

• Low Coverage for Certain Stocks.

• Block Trades.

• IPO´s.

• Management Assessment: Understand Their Incentives.

• Corporate Governance.

• Anticipate Capital Increases.

24

Investment Process – Case-Study: Credicorp

Source: Company Data, EuroAmerica.

The team was familiar with the name as part of the sector coverage in the region – when selecting names to take advantage of the low banking penetration in the region and strong expected growth in Peru in the years ahead, Credicorp came as a strong alternative given its high ROE levels, high capitalization ratios and potential for additional profitability from efficiency gains.

Idea Generation

As part of our investment process we had met several times with Credicorp’s management, both in Chile and in Peru, to discuss the business outlook. We also conducted several meetings with other industry players to gather greater visibility on industry dynamics.

Corporate Analysis

We created our forecast model, stressed the valuation as per key drivers as loan growth, NIM, NPLs and efficiency levels. A price range and valuation was set based on a dividend discount and residual income models.

Valuation & Sensibilization

140 160 180 200 220 240

NIM (+/- 50bps)

NPLs (+/- 50bps)

Loan growth (+/- 50%)

Efficiency Ratio (+/-200bps) Perpetuity growth rate

Co

st o

f Eq

uit

y

3,0% 4,0% 5,0%

8,4% 222 273 355

8,9% 199 241 304

9,4% 180 214 264

9,9% 163 192 232

10,4% 149 173 206

10,9% 136 157 185

11,4% 125 143 167

Valuation Sensitivity Analysis

25

Investment Process – Case-Study: Credicorp

Source: Company Data, EuroAmerica.

The investment case was discussed in the Committee, where it was decided to include the name on the model portfolio of the fund. Main reasons behind the decision were an estimated upside of 32% at the time, strong and stable ROE levels in a market with significant room for growth and the scarcity value of the name being the most liquid vehicle for cyclical exposure to Peru.

Investment Committee

The PM built a position on the name since the inception of the fund though its ADR. There was a sharp correction on the stock price after new cost growth guidance and results were hit by translation losses, opening a new buy opportunity for the name. After building our position, Credicorp decided to switch is reporting currency to Soles (from USD, previously) reducing bottom line volatility, delivered efficiency improvements on cost control initiatives and expanded its participation to microlending by acquiring MiBanco earlier this year.

Implementing & Monitoring

-1,0%

-0,5%

0,0%

0,5%

1,0%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Acc Contribution

Price performance and % of portfolio Contribution to portfolio’s performance

100

110

120

130

140

150

160

170

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Shar

e p

rice

(% o

f To

tal H

old

ings

)

Weight on PF Stock Price (Values)

26

Investment Process – Case-Study: PINFRA

Source: Company Data, EuroAmerica.

Having the infrastructure deficit as a as a key driver for the region, PINFRA came as an attractive alternative to tackle the opportunity in Mexico. The company’s existing portfolio of concessions, stable cash flow generation and high profitability vs. peers translates into a strong balance sheet to pursue new opportunities arising from the deficit and the government’s National Infrastructure program.

Idea Generation

As part of our investment process, we met several times with PINFRA’s management, visited key assets in our trips to Mexico and also met with other players from the infrastructure industry to gain better visibility on the opportunity.

Corporate Analysis

Ecatepec – Peñon Toll Road

Ecatepec – Piramides Toll Road

New Airport Project

Peñon – Texcoco Toll Road

New airport project and Pinfra assets

Region 3 5 assets 117kms 34 years

Altamira Port

Region 1 4 assets 112kms 34 years

Region 1 4 assets 288 kms 25 years

Pinfra assets

27

Investment Process – Case-Study: PINFRA

Source: Company Data, EuroAmerica.

We built our forecasting model around key metrics for both the company and the industry, such as traffic and tariff growth and margin per assets. A price range was set based on a DCF analysis and the sensibilization. In addition, we believe the company’s upside could increase significantly from the extension of existing contracts, the awarding of new concession contracts and the impact from the new Mexico City Airport, which could boost traffic for PINFRA’s assets that surround it.

Valuation & Sensibilization

140 160 180 200 220 240 260

Traffic (+/-10%)

Tariffs (+/-20%)

Margins (+/-10%)

Capex (+/-50%) WACC Other businesses

WA

CC

Co

nce

ssio

ns

10,0% 11,0% 12,0%

7,1% 250 247 245

7,6% 233 231 229

8,1% 218 216 214

8,6% 205 202 200

9,1% 192 190 188

9,6% 181 178 176

10,1% 171 168 166

Valuation Sensitivity Analysis

The analyst presented the investment case to the Committee where it was determined that given the potential upside of 30% at the time of the initial analysis, the solid track record of the company, the room for additional upside from new projects/extensions and the impact from the airport, the fund would build a position on the name.

Investment Committee

28

Investment Process – Case-Study: PINFRA

Source: Company Data, EuroAmerica.

The PM built a position and reached an exposure of 2.5% of the portfolio. Afterwards, PINFRA continued to deliver strong results, won a 14kms extension on one concession and was awarded a new concession. During 2Q14, the company announced a capital increase to further strengthen its balance sheet for inorganic growth and ended up raising P$7.4bn in a follow-on offer at P$172/share through non-voting (L-series) shares. We met with the company after the deal was announced, updated our valuation models and given strong demand on the name, we decided to participate and increase our exposure to the name. Proceeds were used by the company to restructure its Mexico-Toluca highway debt , reducing financial costs by 44,1% (cost of debt of 6,02%). Lastly, the company recently announced it entered into a JV with OHL Mexico to construct and operate a 13,3km 30-year concession roadway.

Implementing & Monitoring

-0,2%

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Acc Contribution

Price performance and % of portfolio Contribution to portfolio’s performance

100

120

140

160

180

200

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Shar

e p

rice

(% o

f To

tal H

old

ings

)

Weight on PF Stock Price (Values)

29

Investment Process – Case-Study: Bachoco

Source: Company Data, EuroAmerica.

Idea Generation

Corporate Analysis

Bachoco is the leader in the poultry industry in Mexico and the second largest player in the egg industry. Last year, the company’s controlling family decided to sell a 9.5% stake in Bachoco to avoid new ruling regarding capital gain taxes effective Jan’14, while keeping the company’s control. This transaction would also boost share liquidity and represented an entry opportunity for investors so we decided to evaluate the transaction.

As part of our investment process, we met several times with Bachoco’s management during our trips to Mexico. The company leads the chicken market both in market share and production capacity and also has the widest cold distribution within the country. Additionally, Bachoco entered the US market through the acquisition of OK Foods in 2011 and currently represents 2% of total US poultry market.

60 65 70 75 80 85 90 95

MX Chicken Vol (+/-10%)

US Chicken Vol (+/-10%)

MX Chicken Price (+/-15%)

US Chicken Price (+/-15%)

EBITDA Mg (+/-100bps)

Perpetuity growth rate

Co

st o

f Eq

uit

y

2,5% 3,5% 4,5%

8,5% 84,0 96,9 116,3

9,0% 78,4 89,1 104,6

9,5% 73,6 82,6 95,3

10,0% 69,5 77,2 87,7

10,5% 65,9 72,5 81,3

11,0% 62,7 68,4 76,0

11,5% 59,8 64,9 71,4

Valuation Sensitivity Analysis

30

Investment Process – Case-Study: Bachoco

Source: Company Data, EuroAmerica.

Investment Committee

Implementing & Monitoring

-0,5%

0,0%

0,5%

1,0%

1,5%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Acc. Contribution

The investment case was presented to the committee where it was highlighted the company’s solid business model based on its leading market position, vertical integration and its well-developed distribution network across Mexico. Additionally, it was determined that the company presents additional opportunities coming from inorganic growth given its solid balance sheet (net cash equivalent to ~20% of its market share) and potential efficiency gains if Mexico poultry imports are allowed into the US.

The PM built a position on the name at the time of the 9.5% stake sale. Since then, the share liquidity has significantly increased and Bachoco is now included in the MSCI Latam Index. Share performance has been strong, reaching over 50% upside since the initial position was built. However, trading multiples show significant room for the stock to continue its upward trend and we believe there should be further potential coming from accretive acquisitions as Bachoco’s multiples expand.

Price performance and % of portfolio Contribution to portfolio’s performance

20

30

40

50

60

70

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Shar

e P

rice

(% o

f To

tal H

old

ings

)

Weight on PF Stock Price (Values)

31

Investment Process – Case-Study: Grupo Lala

Source: Company Data, EuroAmerica.

Idea Generation

Corporate Analysis

Grupo Lala entered our investment universe at the time of its IPO announcement on Sept’13. The company is a leading player in the dairy industry in Mexico and the team was familiar with its leading brands: LALA and Nutrileche. Given the ample appetite for food & beverage names in Mexico, we decided to evaluate the deal.

Prior to the listing and as part of their roadshow, we met with the company’s management during their visit in Santiago. We also discussed the case with several analysts covering the food & beverage sector across the region and closely monitored the appetite for the name on the days prior to the listing.

Investment Committee

The investment case was discussed at the committee where it was decided that the offer’s price range was attractive given the company’s solid business model and room for organic growth on products diversification and increasing penetration of value-added products. Additionally, it was determined that there was additional potential from M&A activity given the company’s solid balance sheet.

-0,4%

-0,2%

0,0%

0,2%

0,4%

0,6%

0,8%

Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14

Acc Contribution

Price performance and % of portfolio Contribution to portfolio’s performance

24

26

28

30

32

34

36

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14

Shar

e p

rice

(% o

f To

tal H

old

ings

)

Weight on PF Stock Price (Values)

32

Investment Process – Case-Study: Grupo Lala

Source: Company Data, EuroAmerica.

Implementing & Monitoring

The PM built a position on the name at the time of its IPO. The company posted strong share performance and in less than a year was included in the IPC and the MSCI Latam Stock Indexes, further boosting its share price. Given strong performance on the name, we did not see significant upside left. Additionally, the company’s guidance regarding acquisition targets has not be consistent throughout the year. Based on the above, we decided to step out of the name and collect gains from share performance (+22%) while we continue to monitor the company’s performance and strategy on the M&A front.

Valuation & Sensibilization

Being the only public name in the dairy industry in Mexico, we built valuation multiples based on the offer’s price range (P$23.5 – P$27.5/share) and compared them to international peers in the dairy industry and regional players in the food & beverage sector. After strong rally of the name and based on valuation multiples, Lala appeared above industry average with no concrete catalysts going forward.

As of Aug’14 P/E EV/EBITDA P/S

2014 2015 2014 2015 2014 2015

Mexico food & beverages 23,2x 20,4x 11,3x 10,2x 1,5x 1,5x

Rest of Latam food & beverages 21,9x 18,6x 12,4x 11,2x 1,7x 1,5x

Latam food & beverages 22,3x 19,1x 12,1x 10,9x 1,6x 1,5x

World Dairy 21,9x 19,6x 13,7x 12,5x 1,8x 1,7x

Lala 25,2x 22,0x 13,2x 11,6x 1,8x 1,7x

Premium/Discount over peers 13% 13% 7% 4% 9% 10%

Grupo Lala vs. Peers

33

EuroAmerica Investments

• Introduction

• The Opportunity

• Case Studies

• Fund Details

• Annex

34

Fund Details

• Public UCITS Fund (FCP) domiciled in Luxemburg.

• Tax transparency & registration in Switzerland, Germany & Austria.

• ManCo. & Custodian Bank: Sal Oppenheim (Lux) & DB Group.

• Fund Currencies: USD. Additionally CHF & EUR share classes.

• FX Hedging: No hedging of local currencies. USD risk for CHF & EUR classes will be hedged.

• Share Classes:

• Performance Fee: 10% with HWM & hurdle rate of 5% p.a.

• Fund Launch Date: April 21st 2013.

• AUM: Strategy capacity 250 Mn USD / Actual AUM: 36 Mn USD.

• Advisory Board.

Liquidity Share Class Mgt Fee Min. Redemption Fee

Weekly I-Class 1,10% 250k -

Weekly HN-Class 1,10% 50k -

Daily P-Class 1,10% 0,50%

Daily R-Class 1,75% 0,50%

35

EuroAmerica Investments

• Introduction

• The Opportunity

• Case Studies

• Fund Details

• Annex

36

Annex I – Investment Process: Approach

• Style:

• Looking for Value & Growth at reasonable prices within Companies with best practices and top management.

• Active, Bottom-up & Research driven.

• Spreadsheets with detailed analysis for all Companies in the Investment Universe.

• Frequent visits & meetings: Know the management/understand ownership & corporate governance.

• Position size & liquidity constantly monitored.

• Permanent Risk Control: Returns are associated with risks.

• Concentrating Portfolio.

Investment Universe (ex Brasil)

172 Companies

Excl. Materials, Energy Utilities & Telecom

110 Companies

Latam Tigers Fund 25-30 Companies

37

Annex I – Investment Process: Euroamerica´s Team

Simón Rosinsky Portfolio Manager

Experience: 12 Years

Andrés Murúa Equity Chile

Experience: 6 Years

Borja Claro

Head of Equity Research

Experience: 10 Years

Giovanna Musa

Senior Analyst

Experience: 7 Years

Jorge Rivera

Equity Chile

Experience: 8 Years

Denise Jacard

Junior Analyst

Experience: 1 Years

Pablo Vicuña

Junior Analyst

Experience: 1 Years

Ariel Schonberger

Junior Analyst

Experience: 1 Year

38

Annex I – Investment Process

•Screening

•Conferences and meetings

•Relevant news and events

Idea Generation

•Industry and perspectives analysis

•Strategy and track record

•Management

•Operating risks and characteristics

•Financials

•Ownership and Corporate governance

Corporate Analysis

•DCF, NAV and SoP

•Multiples (Absolut, Relative and Industry)

•Key Factors Sensibilization

•Downside Risk

Valuation and Sensibilization

•Analyst presentation

•Team discussion

•PM point of view

•Decision

Investment committee

•Position size

•Liquidity

•Risk measures and portfolio impact

•Timing

•Price follow-up

Implementation and Monitoring

PO

RTFO

LIO

Macroeconomic

Follow-up

Analysis and

Risk Control

• Over 300 Company Meetings in the last 12 months.

39

Annex II – Latam Tigers Portfolio Top 15 Positions

Source: EuroAmerica.

Company Weight Country Sector

Pinfra 5,18% Mexico Logistics

Avianca Taca 5,10% Colombia Transportation

Credicorp 5,09% Peru Financial

Walmart Mex 4,85% Mexico Consumer & Retail

Banorte 4,09% Mexico Financial

Bachoco 4,04% Mexico Food & Beverage

Grupo Sura 3,82% Colombia Financial

Asur 3,47% Mexico Logistics

BCI 3,33% Chile Financial

Liverpool 3,11% Mexico Consumer & Retail

Banmedica 3,05% Chile Healthcare

Sport 3,04% Mexico Consumer & Retail

Cementos Argos Comun 2,99% Colombia Cement

Coca Cola Femsa 2,97% Mexico Food & Beverage

Graña y Montero 2,94% Peru Construction

40

Annex II – Performance Attribution ITD

Source: Bloomberg and EuroAmerica.

Total Contribution

Country Contribution Sector Contribution

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Price Contribution FX

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Pe

ru

Ch

ile

Co

lom

bia

Mex

ico

Arg

enti

na

Price Contribution FX

-4%

-2%

0%

2%

4%

6%

8%

Fin

anci

al

Hea

lth

care

Logi

stic

s

Med

ia

Co

mm

erci

alP

rop

erti

es

Tech

no

logy

Tran

spo

rtat

ion

Cem

ent

Foo

d &

Bev

erag

e

Mac

hin

ery

Co

nst

ruct

ion

FX Price Contribution

41

Disclaimer

Vertreter und Zahlstelle in der Schweiz Vertreter und Zahlstelle in der Schweiz ist BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zürich, Schweiz. Bezugsort der massgeblichen Dokumente Der Verkaufsprospekt, die wesentlichen Anlegerinformationen, die Satzung sowie die Jahres- und Halbjahresberichte sind kostenlos beim Vertreter in der Schweiz erhältlich. Representative and Paying Agent in Switzerland The representative and paying agent in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Switzerland. Place where the relevant documents may be obtained The prospectus, the key investor information documents (KIIDs), the articles of incorporation as well as the annual and semiannual reports may be obtained free of charge from the representative in Switzerland. Le Représentant et Service de Paiements du Fonds en Suisse BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich, Suisse, a été désigné Représentant et Service de Paiements du Fonds en Suisse. Lieu de distribution des documents déterminants Le règlement, le prospectus, les documents d’informations clés pour l’Investisseur, les rapports annuel et semestriel du Fonds pour la Suisse peuvent être obtenus gratuitement auprès du Représentant en Suisse.

Latam Tigers Fund October 2014

Roadshow Presentation