Embed Size (px)

DESCRIPTION

banking news

Citation preview

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 1/70

Disclosures in the Balance Sheet

With a view to bring out more transparency in the balance sheets of thebanks, Reserve Bank of India has decided to introduce more disclosures in

the banks annual reports. As a result, banks now disclose in their balancesheets, (a percentage of shareholding of the !overnment of India innationali"ed banks. (b percentage of net non#performing assets to netadvances (c the amount of provision made towards $%As (d towardsdepreciation in the value of investments and (e provision made towardsincome ta&, (f amount of sub#ordinated debt raised as 'ier II apital, (ginterest income as percentage to working funds (h non#interest income aspercentage to working funds (i operating profit as percentage to workingfunds () return on assets (k business per employee (l net profit per employee etc.

FLEXIBLE BANK FINANCE

*ince the Bank +inance is to bridge the gap between urrent Assets andurrent iabilities, this method is based fundamentally on the -%B+ formula.'he assessment procedure in our Bank is for assessing the Working apitalfinance of Rs. .// crore and above other than those class of accounts wheredifferent methods have been prescribed.

0nder the system, +und Based Working apital re1uirement will be assessedas the difference between Working apital !ap and %ro)ected $et Workingapital. 'hough the benchmark for urrent Ratio will continue to be .223,

we may accept some deviation in the same provided the urrent Ratio is notless than .43. In ases where the urrent Ratio has deteriorated onaccount of diversions taking place because of short term funds flow to +i&ed Assets, we may correct the position by giving a 'erm oan to be repaid within5 to 26 months provided the 7ebt *ervice overage Ratio, 7ebt 81uity and*ecurity coverage are at acceptable levels.

0nder this method, the assessment though akin to -%B+ will be morefle&ible. A more liberal approach would also be adopted in working out urrent Assets by including cash margin deposits for etters of redit and !uaranteesand treating +i&ed 7eposits with Banks and temporary investments like

-oney -arket -utual +unds, ommercial %aper, ertificate of 7eposit etc. asurrent Assets. 'he collection of data, analysis of financial statements etc.will be generally as per the -%B+ formula but the classification of currentassets and current liabilities will be more customer friendly.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 2/70

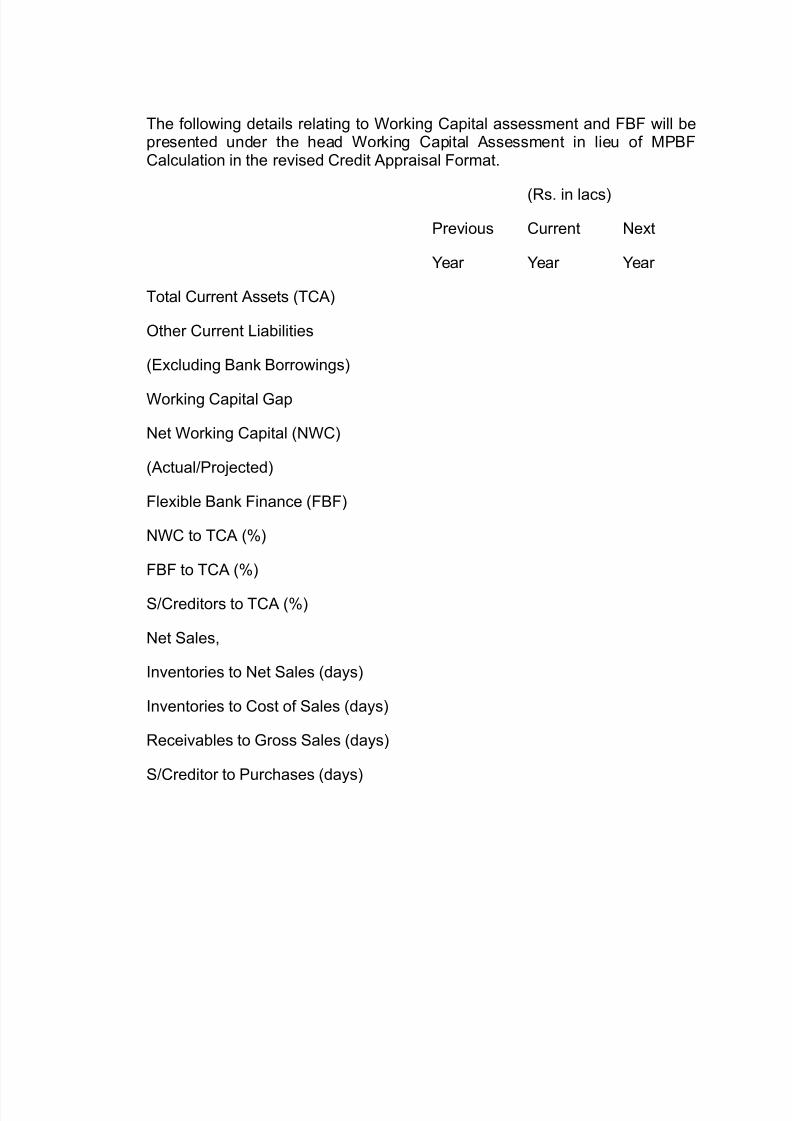

'he following details relating to Working apital assessment and +B+ will bepresented under the head Working apital Assessment in lieu of -%B+alculation in the revised redit Appraisal +ormat.

(Rs. in lacs

%revious urrent $e&t

9ear 9ear 9ear

'otal urrent Assets ('A

:ther urrent iabilities

(8&cluding Bank Borrowings

Working apital !ap

$et Working apital ($W

(Actual;%ro)ected

+le&ible Bank +inance (+B+

$W to 'A (<

+B+ to 'A (<

*;reditors to 'A (<

$et *ales,

Inventories to $et *ales (days

Inventories to ost of *ales (days

Receivables to !ross *ales (days

*;reditor to %urchases (days

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 3/70

CASH MANAGEMENT SERVICE CMS!

"R#D$CT C#NCE"T%

-* is fee based Banking product to orporates as also other organistionshaving re1uirement to collect che1ues and instruments from several centresand collate funds at a single business point. It can also be e&tended as apayment service for orporates through which their payments to upcountrylocations can be serviced efficiently through the system."R#D$CT ATTRIB$TES ollection of che1ues ; instruments from specified centres and remittance

to the main account of the orporate. 7ay : (transaction date collections at any centre to be credited on 7ay

(ne&t working day to 7ay /.ADVANTAGES T# CLIENTS

8nables management of their receivables and payments efficiently. 8nsures efficient cash flows by accelerating collections.

8liminates idle floats and lowers the net cost of funds.

Aids in building predictability of cash inflows ; outflows resulting in superior

cash flow ; treasury management.&H' CMS( -* is a product in heavy demand for clients with several collection

points. 8ssential for Bank to have the product to retain e&isting orporate clients

and also e&pand the client base.

-* opens up a new avenue to generate fee based income. -* also opens up cross#selling opportunities.

KE' FACT#RS F#R S$CCESS 7edicated marketing effort.

A competitive pricing strategy.

8fficient I' systems.

8fficient courier service.

A consistent and focussed approach across the Bank for maintaining

operational efficiency. Wide coverage to leverage e&isting branch network.

Bank=s ability to gear up to the new process capture additional informationand process it centrally.

ADVANTAGES T# THE BANK 'he product will ensure retention of the orporate clientele in our fold and

thereafter e&pansion of our orporate lient base. :ur large network will facilitate wider coverage which will result in larger

volumes. :ver a period of time, the fee based income of the Bank will be boosted by

this product.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 4/70

CA"ITAL ADE)$AC' N#RMS

Meanin* o+ Ca,ital A-e.uac/%

apital Ade1uacy means# a bank must maintain a minimum level of capitalwhich is e1ual to >< of the 'otal Risk Weighted Assets of the Bank by 2 st

march ?6, ?< by 2st -arch 5///. It is likely to be enhanced to /< soon.

Ca,ital Fun-

It may consist of 'ier I @ 'ier II capital.

Tier I ca,ital Core Ca,ital!

It consists of paid up apital and +ree Reserves and *urplus.

Tier II ca,ital Su,,le0entar/ Ca,ital!

It may consist of, undisclosed reserves, revolution reserves, sub#ordinateddebts and cumulative perpetual preferential shares. It is also prescribed bythe RBI that

• 'ier II capital will be limited to ma&imum //< of 'ire I capital.

• *ub#ordianted debts should be limited to /< of 'ier I apital

• Revaluation reserves should be considered at discount < for including

in 'ier II capital.

A! Ris1 &ei*ht +or on the Balance sheet Assets%2ero Ris1 &ei*ht# ash @ RBI Balance, *R Assets, RecapitalisationBonds, Advances to staff, advances against BankCs 'erm 7eposits I%olicy. $* etc and Advances guaranteed by the !overnment of India and*tate !overnment.

3456 Ris1 7ei*hte- % All investments in securities for market risk inaddition to the risk weights assigned towards credit risk.

386 Ris1 &ei*ht9 Bank balance @ due from other banks and Advancesguaranteed by other banks.

586 Ris1 &ei*ht# 8!;7I!;!'*I guaranteed advances.

:886 Ris1 &ei*ht# Investment in other *ecurities, Investment in 81uities,+oreign Investment, all other oans and Advances, +i&ed Assets and other Assets. In addition to //< risk weight 5.< additional risk weight for allcategories of investments in securities including !ovt. *ecurities.

B! Ris1 &ei*ht +or o+ the Balance Sheet Ite0s%

+or such assets (ike @ !, we notionally convert them to fund basedfacility by multiplying them with Credit conversion factorC. 'hen the

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 5/70

resultant product is multiplied by the risk weight assigned to relevantcounter party in the balance sheet to find out the Risk Ad)usted value.

Cre-it con;ersion Factor%

5/< for documentary credit .

/< for all guarantees other than financial and Bid Bond and,

//< for financial !uarantees, Acceptance, 8ndorsements,0nderwriting @ *tandby ommitments, undrawn committed redit linesand liability on account of partly paid shares.

Ris1 &ei*ht

Dero when the govt. is obligant, 5/< when other banks are obligant and

//< for all others.Contracts an- Deri;ati;es Fore< contract=currenc/ o,tions =Currenc/Futures =Crosses Currenc/ #,tion!

• Dero for +ore& contracts with original maturity period of E days.

• 5< for +ore& ontracts;:ption;+utures for original maturity less than

year.

• < for those for period of one year and above but less than 5 years.

• >< for 5 years and less than 2 years and,

• >< F 2< per each additional year for contracts of 2 years and above.

Ris1 &ei*ht

Dero when the !ovt is obligant, 5/< when the bank is obligant and //< for others.

Nettin*

• Incase of advances backed by deposits;cash margin the net amount to be

taken into account.

• Where provision for B77 is already made, the net, amount to be

considered.• In case of off the balance sheet items, the cash;deposit margin should be

deducted before applying credit conversion factor.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 6/70

ASSET9LIABILIT' MANAGEMENT

Asset#iability -anagement is a recent phenomenon in India. 'heimplications of deregulation on the balance sheets of banks are multifacet.

+or e&le, in ??> G ?? , the average cost of deposits of 0nion Bank of India was >.4<, which came down marginally to >.//< in ???#5///.'herefore, the fall in average cost of deposits was /.4<. 7uring the sameperiod, the yield on advances declined from 5.4E< to 5.5<, a fall of /.65<. Both the above phenomena were generally due to general fall ininterest rates in the economy. However, this also gives an insight that in afalling interest rate scenario, fall in yield on advances could be steeper thanfall in costs of deposits. Why is it so 'he reasons can be traced tomismatches in the maturity and re#pricing profile of deposits and advances.While deposits of the bank would generally re#priced over a period of time, theadvances would get re#priced fre1uently as most of the advances are floatingin nature, anchored to the %R of the bank. 'herefore, greater volatility ininterest rates poses challenges to a bank to manage its spread G $et InterestIncome or $et Interest -argin and preserve its economic value, which can beaddressed only through a robust Assets G iability -anagement *ystem.

Asset iability -anagement involves planning, directing and controlling theflow, mi&, cost and yield of the consolidated funds of banks. Alternatively, A-is defined as the process of strategic positioning of balance sheet whichinvolves ensuring the linkages between asset side with liability side andenhancing the linkages through off#balance sheet activities. 'he goals of

A- can be articulated as follows 3

• Accurate determination of market risk.

• 8nhancement of long#term profitability for a given 1uantity of risk.

• Appropriate structuring of hedging positions.

• Raising total return.

• 8nhancing the -arket Jalue of 81uity (-J8.

Total Ris1 Mana*e0ent A,,roach

'he two ma)or risks in the balance sheet of a financial institution are G marketand credit risks. 'hese risks are currently managed and mitigated under aparallel two G track approach. In leading institutions, there are two separatecommittees to address the issues of credit and market risks. While the creditrisk is managed by redit Risk ommittee, Asset G iability ommittee(A: addresses the market risk. 'he credit risk triggered by market risk isalso managed by A:. 'he recent events of market risk G triggered creditrisk calls for effective steps towards integration of both the ommittees.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 7/70

A: is one of the key components of A- system in a bank, A: isconstituted by the Board of 7irectors and it is in overall command of the A-system in a bank. A: is also responsible for various functions like pricing of assets and liabilities, funding, optimal deployment of resources, capital

planning , etc. 7ue to comple&ities of its tasks, A: is constituted bydrawing e&pertise from various business lines, like 'reasury, %lanning, redit,8conomic Research, etc. Head of information technology is an invitee to thecommittee to supplement the efforts of the A: to generate credible and1uality -I*.

'he ma)or ob)ective of A- in any institution is to manage and mitigate thefollowing types of market risk 3

a. i1uidity risk

b. Interest rate risk

c. +oreign e&change rate risk

d. 81uity price risk

a4 Li.ui-it/ ris1

'here are two approaches for measuring li1uidity risk namely stockapproach and flow approach. *tock approach is used for measuring li1uidityon the basis of certain ratios like loans to assets, loans to core deposits,

purchased funds to li1uid assets, large liabilities minus temporary investmentsto earning assets minus temporary investments, etc. However, these ratios donot reflect true li1uidity of institution in as much as some of the assets may notbe having ade1uate li1uidity and securitisation has )ust made a beginning inthe Indian market. 'herefore, the alternative approach i.e. the flow approachis an effective tool in such a situation. 0nder this approach, various items of assets and liabilities and off G balance sheet items are placed under variousmaturity bands like #E days, #5> days, etc. A bank can fi& prudential capson mismatches under each time band based on the maturity profile and mi& of its assets and liabilities. i1uidity can also be measured and managed byassessing it on a dynamic basis. 'his re1uires pro)ecting cash flows based on

behaviour of e&isting assets and liabilities as well as factoring the impact of e&ternal factors like volatility in stock;money market conditions, macro#economic factors, etc on the behaviour of future cash flows. 'he cash flowsarising out of off#balance sheet items are also factored in the dynamic li1uiditypro)ection.

Interest rate ris1

Interest rate risk has arisen in Indian market mainly due to de#regulation of interest rates. Abolition of administered interest rates has given opportunity toIndian banks to price their assets and liabilities in the most competitive

manner. At the same time, it has e&posed them to various types of interestrate risks like basis, yield curve, embedded option, price risks, etc. +or

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 8/70

e&le, a bank financing a / year bond through 2 months deposit may facethe following risks 3

. Re#investment risk arising at the time of reinvestment of coupons from the

bond.

5. Interest rate risk, as the bank has to fund the investment by raisingdeposits at the end of every three months. In case of rising interest ratescenario, the funding cost will increase, affecting the margin adversely.

*imilarly, when a bank funds floating rate assets like %R linked cash creditand demand loans through fi&ed rate liabilities like 2 yearsC deposits, it isagain e&posed to interest rate risk. 'he margins are e&pected to decline in afalling interest rate scenario.

'he other risk faced by a bank in volatile interest rate scenarios is embeddedoption risk. 8mbedded options are typically in built in both deposits andadvances. In a rising interest rate scenario, a customer can e&ercise, withoutmany penalties, the option of pre#mature withdrawal of his deposits. *imilarly,in a falling interest rate scenario pre#payment can take place in advanceaccounts that are contracted on fi&ed rate basis. 'he options e&ercised bycustomers#depositors and borrowers pose significant challenges to a bank inmanaging its li1uidity profile and $et Interest margin.

'he other variants of interest rate risks are 3

• !ap or mismatch risk G risk arising due to holding of assets andliabilities of varying maturities.

• Basis risk G risks that the interest rate of different assets, liabilities and

off#balance sheet items may change in different magnitude.

• 9ield curves risk G risks arising due to non#parallel movements in yield

curves.

• %rice risk G risk arising due to distress sale of assets and distress

pricing of liabilities.

• Reinvestment risk G uncertainty with regard to interest rate of which

future cash flows could be re#invested is known as reinvestment risk.

Mana*in* Interest rate ris1

Interest rate risk should be managed by segmenting the balance sheet into'rading Book and Banking Book. Assets in 'rading book are held primarily for generating profit on short#term movements in price;yield. Banking bookcomprises assets and liabilities G customer deposits, loans and advances,*R investments, $on#*R investments, etc which are contracted basically

for maintaining relationship or for steady income and statutory obligations.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 9/70

!enerally assets and liabilities in the Banking Book are held till maturity. 'heprice risk is the primary concern for a bank in its 'rading Book. 'he likelychanges in $et Interest Income ($II or changes in the market value of e1uityare the primary focus for Banking Book.

'he following methodologies are adopted by a bank for managing interest raterisk 3

• -arking to market on a daily basis and holding period clearly defined.

• %rice risk is measured by adopting internally developed Jalue at Risk

model or BasleCs ommittee on Banking *upervisionCs standardi"edapproach is followed.

• 'he cut#loss limits and duration and composition of the portfolio

stipulated Banking Book.

• In the short#term the earnings impact is 1uantified by !ap Analysis.

• In the long#term, the market values of assets and liabilities and off balance sheet positions are estimated with the help of 7uration !apanalysis.

• *imulation analysis is performed to accommodate the dynamic

behaviour of balance sheet.

It is a general understanding in the banks that crystalli"ation of credit risk i.e.generation of $on %erforming Assets is only the factor that is affecting theprofitability in view of provisioning implications. But, the mismatched assetsand liabilities, in a volatile interest rate scenario, could also trigger losses andthe severity of which could be far deeper than the effects of $%As. 'o

conclude, the potential for profitability or losses due to mismatches issignificant. 'hus, the magnitude of market risk should be clearly understood,identified, measured, monitored and managed.

C#R"#RATE G#VERNANCE

+or long, the orporate *ector in India has been dominated by certainfamilies who cannot hold together after the demise of the heads of thefamilies. 'he investors in the e1uity capital of such companies tend to losebecause they are not running on professional basis. onse1uently, orporate!overnance is now being insisted so that the change at the top does notaffect the working of an enterprise.'oday, global concerns are e&pressed towards increasing long#termshareholdersC value. *ince the shareholders are residual claimants, in a well#performing capital;financial markets, what ma&imises shareholdersC valuemust necessarily ma&imise corporate value and best satisfy suppliers,creditors, customers and public#all stakeholders, governance practices.orporate !overnance includes well#defined systems @ processes to protectshareholdersC interest. In short, orporate !overnance refers to the )ointresponsibility imposed on the Board of 7irectors and management to protectthe rights ; interest of shareholders @ inhance shareholdersC value.

!ood orporate !overnance has the potential to shape the economy and thecapital market of a country. 8mpirical studies corroborate the fact that markets

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 10/70

react positively to well#managed companies, *o with the adoption of goodgovernance practices, companies can take appropriate decisions for thebenefits of owners as well as shareholders @ other stakeholders.'he increasing number of scams taking place in Indian orporate *ector and

being e&posed to internal @ e&ternal competition due to economicliberalisation have left no choice but to go for improving orporate!overnance practices.&hat is Cor,orate Go;ernance A credible and professionally managed8fficient Business *ystem.The nee- +or Cor,orate Go;ernance% When we globalise, need to followglobal standards (post liberalisation.+7I in *econdary market.adbury committee came up in 0K for orporate !overnance."recursor >e+ore i0,le0entation in In-ia4II Ape& body ommittee whether industry can evolve voluntary code of

conduct.*8BI appointed Kumaramanagalam Birla ommittee what is happeninginternationally and how we can adopt. 'hese recommendations were studiedand *8BI introduced clause E? in listing agreement.&hat is clause ?@(-odification in isting, 'ransparency, -ore disclosures, egal framework, code of conduct."ur,oseode of Best %ractices(redibility, 'ransparency, 8fficiency, Responsibility and Accountability of -anagement to Board, Board to *hareholders.The in*re-ients %Board of 7irectors, Audit ommittee , Remuneration of 7irector, Boardprocedures, -anagement, *hareholders, Report of orporate !overnance,ompliance. Di0ensions o+ Cor,orate Go;ernanceLuality of performance, 81uity 3'ransparency, *ocial Responsibility 3 Accountability, Luality of %erformance, -anagement, Appointee of *hareholders, to take care of shareholders interest, -ake shareholdershappy.,*hareholdersC delight (Happiness 'hrough ustomersC delight(Happiness'hrough 8mployee delight.

Hence, -anagement#A $oble %rofession spreads happiness.• *hareholder delight G shareholder Jalue.

• *hareholder Jalue G -arket apitalisation.

Hence -anagement Responsibility 8nhance -arket apitalisation.&hat is Mar1et Ca,italisation(

• -arket apitalisation depends on R:8 (Return on 81uity.

• !rowth G business#8arnings.

• Industry profile G !rowth prospects %erpetuality.

• Luality of -anagement G ompetency, 'ransparency, 8thics.

• Intangible Assets G Brand 81uity others.

• -anagement G a multi#dimensional task, challenging task.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 11/70

Role o+ Mana*e0ent

• Board of 7irectors obviously must ensure -anagement, which can

perform. %erform well when market is good. %erform well when market isbad. %erform when the market is good or bad.

Rele;ant ,ro;isions o+ clause ?@Board of 7irectors.Board procedures.-anagement.&hat is E.uit/(

• 81uity transparency G ob)ective. $o privileged investor. $o privileged

shareholders. Accurate G transparent information. *ingle large holder cancall the shots .Widely dispersed shareholders G -anagement can call theshots. $eed is to protect small shareholdersC interest.. Independent non8&ecutive 7irector. Audit ommittee. ompensation. urbs on insidetrading. 'imely, accurate and sufficient price sensitivity information. Accounting *tandards. *mall shareholder 7irector. ritical factor#trulyindependent 7irectors.

Social res,onsi>ilit/ o>ecti;es

• !ood orporate citi"ens G compliance of various laws. Interest of

secondary shareholders G depositors creditors, etc. How independent areIndependent 7irectors G appointment procedure. Role of Institutional7irectors. +irewall between +und -anagers and $ominee 7irectors.

Ho7 -o 7e -i++erentiate >et7een accounta>ilit/ o+ non9e<ecuti;e an-e<ecuti;e -irector (- Ade1uate compensation of non#e&ecutive director.

B/ K 4K4 Nohria CMD Cro0,ton Grea;es Lt-4!

C#R"#RATE G#VERNANCE IN"$BLIC SECT#R BANKS

'he !overnment ownership of a bank has a potential to alter the strategiesand ob)ectives of the bank as well as the internal structure of the governance.onse1uently, the general principle of sound corporate governance is alsobeneficial to !overnment owned banks.

'o enhance corporate governance, it is of importance that banks are able toarticulate their corporate values, code of conduct and standards of appropriate behaviour. 'he issues that emerge in promoting corporategovernance in the Indian banking system will include role and composition of the Board, disclosure re1uirements, integrity of the accounting practices andthe control systems.

I will e&amine areas for ma)or initiatives under two categories G one relating tosome basic issues to be addressed for promoting corporate governance inpublic sector banks and the other on resetting of the Board of 7irectors.

'he Basic issues are 3

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 12/70

• +irstly, it is a pre#re1uisite to have strategic ob)ectives, if sound

corporate governance practices are to be promoted in an organisation. Arising from this, it is imperative that the !overnment as owners of thepublic sector banks, which dominate the Indian Banking *ystem, spell#

out strategic ob)ectives while continuing !overnment ownership.

• At the stage of nationalisation, the ob)ective of promoting social

banking was well set out and has resulted in the success achievedover the past three decades. Having achieved, a stable framework andinfrastructure for supporting social ob)ective, it is perhaps, time to re#look at the working arrangement. A fresh working arrangement needsto be put in place to clearly demarcate the social and commercial roleof the banking, as the two will have to work on different reward andrecognition system in view of varying nature of risk and responsibility.While, banks may continue to e&tend network support, lending to socialbanking areas can be increasingly channelled through institutions likeKJI, 7istrict Industries entre as well as through $!:s. !overnmentsponsored schemes can be increasingly channelled through suchinstitutional mechanism, with bank funding the same through bonds.

• *econdly, the e&tended ownership of banks arising from public

shareholding on dilution of !overnmentCs stake will need a frameworkfor constitution and functions of the Board. 'his will have to be built intothe scheme of dilution. It has to provide for ade1uate representation onthe Board and through A!-, an effective say in the areas concerning

the shareholders interest. 'his has to precede further public issues of %*Bs so as to find acceptance in the market and a better pricing too.

'hat said, I would now look into the issue of corporate governance throughrestructuring the Board of 7irectors. 'he crucial issues in this area will be 3

• 'o ensure that optimal strength of the Board of 7irectors are available

at all times, through a process of retirement on rotation basis. ongspells of truncated board, followed by over stretched tenure of fullBoards is not conducive for adopting best practices.

•

'o create a database of professional directors at national level for appointments to the banks board.

• 'o redraw the composition of functional and non#e&ecutive directors on

the board. 'his will include delinking the role of hairman of the boardand the 8: of the bank. Additional positions at the board level mayinclude functional heads of credit, treasury and technology areas.

• 'o recast the committee of directors, to address more focused issues

on critical areas including 3

- Articulating corporate strategies.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 13/70

- redit risk management practices.

- Remuneration and recognition system.

-Internal control and audit systems.

- Approving documented policies and procedures on Asset andiability -anagement, redit Risk -anagement, 'echnology and:perational Risk -anagement.

• At the functional level, the board will oversee the discharge of

management responsibilities and delegated powers throughappropriate reporting mechanism and practices and procedures, whichare duly approved by the Board.

• redit decisions will be controlled more through reporting on creditconcentrations and adherence to e&posure norms, in place of delegated powers for credit sanctions.

CA"ITAL ACC#$NT C#NVERTIBILIT'

'he 'arapore committee on capital account convertibility has recommended athree#year timeframe for full convertibility by ???#5///. 'he five#member panel headed by former RBI 7eputy !overnor, *. *. 'arapore, presented itsreport to RBI !overnor in Mune ?4. Highlighting the preconditions for achieving a full float of the rupee, the committee called for3 (I A reduction of

the gross fiscal deficit to 2. per cent by ???#5///, (II An average mandatedinflation rate of 2# per cent, (III total deregulation of interest rates by the endof this fiscal itself, (IJ a reduction in the cash reserve ratio (RR of banks tothree per cent and (J reduction of $%A to < by the year 5///.

If these signposts are not sighted along the way both the timetable and scopeof capital convertibility would have to be alerted.

'he committee has recommended the phased liberalisation of capital inflowsand outflows.

'he panel has recommended that in 5///, a stock taking of the progress onthe preconditions as well as the impact of the measures outlined in the reportshould be undertaken. 'he timing and se1uencing of convertibility measureswould be facilitated by the proposed changes in the legislative frame workgoverning foreign e&change transactions as envisaged in the +oreign8&change -anagement Act (+8-A.

'he most important precondition for convertibility, according to the committee,is a stable macro#economy including sustainable fiscal deficit. It hasrecommended a reduction in the centers= gross fiscal deficit to !7% ratio froma budgeted E. per cent in ??4#?> to E per cent in ??>#?? and further to 2.per cent in ???#5/// accompanied by a reduction in the states deficit as well

as a reduction in the 1uasi#fiscal deficit. Any slackening in the pace of fiscal

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 14/70

ad)ustment would render the task of opening up the capital account difficultwith accompanying dangers of slippages, rollbacks and reversals of capitalflows.

'he ommittee has warned that the practice of financing the amoritisation of !overnment borrowings out of fresh borrowings is unsustainable and stronglyendorsed the 'enth +inance ommission recommendations for the institutionof a consolidated sinking fund for the public debt.

RISK INV#LVED IN BANKING B$SINESS

Banking is primarily a business of accepting and managing risk. BankCs mainrole is intermediation between those having resources and those re1uiringresources, investors do not want to accept the risk of default on the parts of users. 'herefore, Banks came into the scene and assured prompt repayment

of funds and accepted the risk of default. As a compensation, they earninterest margin between what they pay to the investors and what they chargefrom the borrowers.

I0,ortant Ris1s%

Cre-it Ris1

'he risk of erosion of value due to simple default or non# payment by theborrower.

Strate*ic Business Ris1

'his is the risk that entire lines of business may succumb to competition or

obsolescence. e.g. .%. is a CsubstituteC product for large corporate loans. 'hisrisk also occurs when a bank is not ready or able to compete in a newlydeveloping line of business. ate entry makes sometimes, difficult to achievecompetitive advantages.

Re*ulator/ Ris1

Banks are licensed to do business. 'his license may be revoked, whichrenders significant capital investment worthless, e.g. apital Ade1uacyRe1uirement.

#,eratin* Ris1

When the systems simply do not function properly resulting in losses of funds.In ??/s several investment banks lost significant sums due to trading errors,which could not be detected i.e. system malfunction.

Co00o-it/ Ris1

'he value of stocks and bonds of various companies are sub)ect to this risk.

Hu0an Resource Ris1

8N# 7eparture of an employee with specialised knowledge can bring certainsystem to halt due to lack of proper incentive.

Le*al Ris1

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 15/70

'he risks are difficult to be anticipated as they may be unrelated to prior events.

"ro-uct Ris1

When a financial services product may become obsolete or uncompetablee.g. A'-s developed by banks and improved version brought out later bymanufacturers.

Interest Rate Ris1

It can create a li1uidity crisis.

Li.ui-it/ Ris1

Inability to pay desired withdrawals due to asset liability mismatch.

Currenc/ Ris1s

It is the risk of e&change rate volatility .Settle0ent Ris1

It is a particular form of default risk which involves bankCs competitors.

Mana*e0ent o+ Ris1

• Intelligent lending decisions

• 7iversification

• 'hird %arty !uarantee

• 7erivative market through the use of swaps and forward contracts

STRATEGIES F#R S$RVIVAL

• %ublic *ector Banks should be given greater autonomy with respect to

recruitment and promotion of personnel and in determining organisationalstructure.

• 'o adopt more general approach for Asset iability -anagement3

In respect of rate, yield, volume and maturity.

• oncentration on management of credit risk.

• While high level of $%A has come down volume still remains large.

• Better management needed to e1uip @ operate in deregulated

environment.

• 8&pertise needed for developing necessary treasury management while

managing investment portfolio.

#THER IM"#RTANT AREAS

• ustomer *ervice.

• Housekeeping through upgradation of technology for increasing

productivity.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 16/70

• 7iversification of Business.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 17/70

$NIVERSAL BANKING

!lobalisation, liberalisation and deregulation of financial markets in manydeveloped and developing countries have resulted in increased

disintermediation and has made commercial banks vulnerable to interest raterisk. Rela&ing e&change controls, adopting uniform accounting practices inregard to income recognition, asset classification and provisioning norms andprescribing capital ade1uacy norms has further aggravated the position. $owthe developments in information technology and telecommunications areallowing international pooling of financial resources thereby spreading the riskacross more than one market. As a result, there is severe strain on interestspread and bottom line of banks.

Amidst all the above said development banks in the developed countriesstarted emphasising on new sources for non#interest income to arrest thepressure on their bottom lines. 'he efforts of many foreign banks have yieldedgood results as their income from non#fund based business to total incomehas increased manifold. However, this process has led to diversification intheir e&isting activities. In many developed countries, besides traditionalactivities like accepting deposits and making advances, the banks are nowundertaking the following activities G

• +inancing fi&ed investments in industrial pro)ects by way of making

loans and advances on a longer term

• *ecuritising debt

• 'rading in financial instruments, foreign e&change and its derivatives

• reating;financing venture capital funds

• 0nderwriting new debt and e1uity issues

• %roviding corporate advisory services including advice on mergers and

ac1uisitions

• -aking investment management and providing depository services

• *elling insurance products

• Holding e1uity of non#financial firms.

0ndertakings so many activities by commercial banks in various countries haschanged the face of banking from O:mni#present banking facilitiesO to O:mni#potent bankingO having multifarious functions and selling;marketing their newproducts and many modern banking services. 'his development has broughtto the fore the concept of 0$IJ8R*A BA$KI$!.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 18/70

0niversal banking means providing diverse kind of banking services by banks.0nder universal banking, world#over, commercial banking and investmentbanking activities with both e1uity ad debt are integrated and these servicesare provided by the same institution under one roof.

Bene+its o+ $ni;ersal Ban1in* S/ste0

. 8nables a bank to diversify its risk profile and also its income streams.

5. :ffers national competitive advantage at the systemic level by reducingcapital cost.

2. 'he risk of bankCs failure and therefore the cost thereof is reasonablyhedged when a bank is performing diversified activities.

E. Bank has the benefit of economies of scale and scope.

. 'he customer is also benefited as he gets one stop banking facilities.

De0erits o+ $ni;ersal Ban1in* S/ste0

i. 0nder the universal banking system various financial services includinginvestment#banking facilities are provided under one roof. It is,therefore, feared that the universal banking may pose the risk of conflict of interest and may not provide sufficient protection to investorsbecause the bank has inside information on the industry;unit andobviously it would like to protect its own interest.

ii. *ometimes riding the enthusiasm the bank may start a new activity for which e&pertise is not available with it. 'his may even result in failure of the bank.

iii. 0niversal banking results in greater economic efficiency in the form of lower cost higher output and better product mi& on the other side if oneuniversal bank collapses, it leads to a systemic financial risk.

iv. 'he system of providing all services under one roof may prevent theuniversal banks from developing the highly specialised e&pertise

needed to compete in todayCs financial markets.

v. 0nder the universal Banking system, the organisational structures arebig and become overly bureaucratic, which may create problems inattracting top 1uality employees.

$ni;ersal Ban1in* In In-ia

Banks in India are already practicing universal banking by providing a wholerange of financial services. Banks in India are resorting to O+inancialonglomeratesO route. -any public sector banks have set up subsidiaries for

providing various financial services.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 19/70

'he following financial services are already being offered by the commercialbanks through adopting the O+inancial onglomerateO route in India.

i. 'he ommercial banks are active in providing pro)ect finance,

wholesale credit, retail credit, housing finance and mortgage credit.redit derivative products such as factoring, leasing and hire purchaseand number of non#fund based products like guarantees and letters of credit are also being provided.

ii. A good number of commercial banks have set up mutual funds throughtheir subsidiaries.

iii. redit card business is the recent innovation in the Indian commercialbanking.

iv. !old banking is another new product recently launched by a fewcommercial banks.

v. -ost of the commercial banks are actively participating in the moneyand capital markets.

vi. ommercial banks are also providing advisory services through their merchant#banking arm.

#FFSH#RE BANKING

• It refers to international banking business involving non#resident foreign

currency dominated assets and liabilities.

• It refers to banking operations that cover only non#residents and do not

mi& with domestic banking.

• 'his banking is carried out in about 5/ centres throughout the world

which offers following benefits 3

•

8&emption from minimum reserve re1uirement.• +reedom from control on interest rates.

• ow or non#e&istence of 'a& @ evies.

• 8ntry for large international banks is relatively easy.

• icense fees are generally low.

• lose pro&imity to important loan outlet and deposit sources.

8& 3 Bahrain is in offshore base for petro#dollars

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 20/70

MERCHANT BANKING

-erchant Bankers are financial intermediaries. 'hey act as intermediaries inthe process of transfer of capital from those who own it to those who use it.

-erchant Banking is an agency, retained by a company to advise and assistin capital structuring;restructuring and its mobilisation within the prescribed,regulatory framework. 'hus, the merchant bankerCs role can be institutionalloan syndications, institutional placements, advisory services, includingmergers;.ac1uisitions;alliance and primary markets.

In primary markets a merchant banker is one of the many important agenciesretained by the company to assist it in mobilisation of funds. However, there isa critical difference that a merchant banker helps, selects and co#ordinatesthe work of other agencies. In the process the merchant banker has to

shoulder the high responsibility of an elder brother and be indirectlyresponsible for the acts of other agencies.

In Indian conditions, -erchant Banking is understood ordinarily as relatedmainly to issue house activities. Issue house activities include counselling,corporate clients who are in need of capital, capital structure, form of capital tobe raised, terms and conditions, under#writing, timing and preparation of prospectus, publicity for grooming the issue etc.

It includes following range of services 3

• %ro)ect counselling and appraisal.

• ounselling on capital restructuring.• oans syndication.

• %ublic issue management.

• 0nderwriting of shares and debentures.

• Acting as Banker to the issue.

• Acting as Banker for the Refund orders;collection of call money.

• Handling of interest and dividend warrants.

• ounselling for $RIs.

• %ortfolio -anagement etc.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 21/70

TREAS$R' MANAGEMENT

'he domestic treasury management have three main ob)ectives3

a. 'o maintain *tatutory Ratios, namely RR and *R as stipulated by theRBI from time to time.b. 'o ma&imi"e yield on the funds deployed.c. 'o manage the funds in such a way that the short term liabilities are

matched with the corresponding assets without any strain on the fundsmanagement. .

'he prime ob)ective is to ensure that the Bank at all times adheres to thestatutory obligations of the entral Bank stipulated and modified from time totime. Any default, apart from attracting severe penalties would also attach astigma of non#compliance of *tatutory obligations and hence the 'reasury7epartment has to constantly vigilant on this front.

*ince the yield earned on deployment of funds for complying with statutoryobligations would necessarily be low, it is for 'reasury 7epartment to look for other better and remunerative avenues for deployment of residual funds. Inthis respect, the non#*R investments such as investment in e1uity shares of corporates, debentures, bonds of public sector, units of 0'I, commercialpapers and floating interest rate bonds etc. assumes lot of importance.

'he liability management has assumed importance these days which aspectwas not given due importance earlier. 'he liability management includesmatching of liabilities with assets of corresponding maturities, rate of returnand investment risk. 'he constant comparison of these three aspects is amust if any treasury department is to make most of the opportunities whiche&ists in the treasury operations.

'he *R component of any bank consists of mainly the following 3

a. entral !ovt. oans.b. 'reasury Bills GE;?;>5 and 26E days.c. *tate 7evelopment oans.d. 'he bonds floated by *tate sponsored bodies such as *tate 7evelopment

orp, *tate 8lectricity Board etc, as also securities floated by -unicipalcorporations and other developmental agencies repayment of which and

payment of interest on which is guaranteed by *tate !ovts ;entral govt.e. Bonds issued by All India financial Institutions which are specifically floatedas approved securities for the purpose of *R.

f. ash on hand, Balance with other Banks and the portion of RR which isin e&cess of he statutory re1uirement. RR comprises of the balances of the branches of the Bank maintained with the Reserve Bank of India atvarious centres put together.In todayCs conte&t the emphasis has shifted from mere -aintenance of RR and *RC to -anagement of R and *R. 8ffective managementof the treasury has an important role to play in the profit management of the Bank.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 22/70

INTEGRATED TREAS$R'

Forei*n E<chan*e an- Mone/ Mar1et #,erations

As the names indicate +oreign#8&change -arket (+N#-K' operationsinvolve conversion of one currency into another, whereas -oney -arket (-#-K' operations involve only transacting in any particular currency.

In a free and competitive market place, the forces of arbitrage opportunismensure that 3. A currency with higher rate of interest is at discount for forward delivery5. A currency with lower rate of interest is at discount for forward delivery2. 7iscount;%remium (forward e&change differential is e1ual to net

accessible interest rate differential between the two currencies involved.0nder perfect market conditions, e1uilibrium will be attained only and if

forward e&change differentials between currencies are e1ual to their interestrate differentials. +orward e&change differentials are commonly referred to as+N#*WA% differences or *WA% points.In as much as Indian foreign e&change markets as yet are not fully free nor completely competitive, forward e&change differentials of various foreigncurrencies against Indian Rupee are not necessarily e1ual to interest ratedifference between the relative currency and Indian Rupee. As a result of gradual liberalisation of Indian markets since ??2, some co#relationshipbetween +& forward differentials (*WA% points and relative interest atdifferential has since come to play, albeit, occasionally and in a very limitedsegment.

onse1uently, Indian +N and 7omestic -oney -arkets are still not free fromarbitrage. 'here are occasions when interest rate differentials and forwardswap difference are not e1ual and such imperfect market conditions offer scope for arbitrageurs to e&ploit the situation by *wapping foreign currencyinto Indian Rupees or vice versa. 'he regulators, with a view to movingtowards perfect market conditions, have been gradually permitting marketparticipants(Authorised 7ealers to freely borrow;invest foreign currencies;inoverseas centres. However, presently as the e&tent of this freedom is limited(< of unimparied tier G a capital of A7*, market is yet not arbitrage free. Authorised 7ealers, having simultaneous access to both +ore& and -oney-arkets can 1uickly sei"e arbitrage opportunities by their *WI+' and co#

ordinated actions. As such it is of paramount importance that both fore& and-#-K' activities are undertaken in an integrated manner preferably under single roof and under command of same authority.:ur Bank, by establishing 'reasury Branch, has put in place, re1uiredsystems under which various market opportunities, including those arising onaccount of imperfect co#relationship between +N#-K' and -#-K' can befully e&ploited for augmenting BankCs profits. However, while undertakingthese activities, it has to be ensured that RBI guidelines in this regard arestrictly adhered to. +urthermore Risk -anagement parameters of the Bankare to be meticulously followed.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 23/70

BRIDGE L#ANS

Banks are permitted to sanction Bridge oans to the companies for a period

not e&ceeding one year against e&pected e1uity flows;issues. *uch loansshould be accommodated within the ceiling of < of incremental deposits of the previous year prescribed for the bankCs investments in ordinaryshares;convertible debentures of corporates including %*0 shares, loans tocorporates for meeting promoters contribution and units of mutual fundschemes, the corpus of which is not e&clusively invested in corporate debtinstruments. RBI has also advised banks to formulate their own internalguidelines with the approval of their Board of 7irectors for grant of such loansand to e&ercise ade1uate caution and attention to security for such loans.

'hese loans are normally tied up with the underwriting commitments by other

Banks;+inancial Institutions and thus considered secured and self li1uidating,though no tangible security is available to the bank, the control mechanismadopted in his regard interalia includes the following aspects 3

. %ublic issue should have the approval of relevant authorities including*8BI.

5. 'he e&tent of Bridge oan is related to the specified percentage of theamount actually called up each time.

2. 'he period of Bridge oan is related to the time taken for completion of

various formalities related to public issue.

E. *uch Bridge oans are normally considered in AAA;AA rated accountswith the Bank preferably where the lending Bank is Banker to the issue.8&ceptions to this rule can be made only in the case possessing highmerits. In case of consortium accounts, $: from the leader to beobtained.

. +or ensuring proper end use of the Bridge oan, the disbursements aremade through a special account so that the funds do not get mi&ed up.

6. 'he utilisation of Bridge oan is allowed for the purpose for which thepublic issue has been floated. 'his is ensured by obtaining writtenstatement from the company as to how the amount of Bridge oan is goingto be spent. *upporting documentary evidence is obtained wherever considered necessary. Additionally, the ompany may be asked to submita certificate from a reputed hartered Accountant about the end use of funds.

Bri-*e Loans to Go;ern0ent

Banks should not e&tend bridge loans;interim finance for activities, which arere1uired to be legitimately met out of !overnment resources;budgetaryallocations.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 24/70

Bri-*e loans a*ainst recei;a>les +ro0 Go;ern0ent

Banks should not e&tend bridge loans against amount receivable fromentral;*tate !overnments, by way of subsidies, refunds, reimbursements,

capital contributions, etc., sub)ect to the following e&ceptions 3

a. Banks can contribute to finance subsidy receivable under the normalretention %rice *cheme, for periods upto 6/ days, in the case of fertiliser industry.

b. Banks can continue to grant finance to e&porters against receivables from!overnment such as 7uty 7rawback and I%R*, as per the e&istingguidelines.

Banks may consider sanction of bridge loan;interim finance against

commitment made by a financial institutions and;or another bank only incases, where the lending institutions faces temporary li1uidity constraint, andsub)ect to compliance with the following conditions

a. 'he bank e&tending bridge loan;interim finance must obtain prior approvalof the other bank and;or financial institution, which has sanctioned theterm loan

b. 'he sanctioning bank must also obtain a commitment from the other bankand;or financial institution that the latter would directly remit the amount of term loan to it at the time of disbursement

c. %eriod of such bridge loan;interim finance should not e&ceed four months.0nder no circumstances, should banks allow e&tension of time for repayment of bridge loan;interim finance,

d. Banks should ensure that bridge loan;interim finance sanctioned anddisbursed is utilised strictly for the purpose for which the term loan hasbeen sanctioned by the other bank and;or financial institution.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 25/70

HEDGE F$NDS

&hat are he-*e +un-s(

Hedge funds can be defined as eclectic investment pools organised as privatepartnerships for wealthy individuals and institutions, and very often, for offshore residents, primarily for ta& and regulatory purposes whose managersare paid on a fee#for#performance basis. Appro&imately, #5 per cent of post#ta& profit accrues to the hedge fund manager apart from themanagement fee of per cent of the assets, annually. Hedge fund managersas partners, have their own capital invested in the funds they manage. 'his isin sharp contrast to the mutual fund industry, where managers typically do nothave their own fund, invested. 'his has important implications for hedge fundmanagers, as they tend to be oriented towards achieving the highest absolutereturn without taking e&cessive risk.

T/,es o+ he-*e +un-s%

Hedge funds can be classified into following broad categories3

• Macro +un-s G 'hese take a view on the macro#economic policies of

select countries and attempt to profit from perceived discrepancies inthem.

• Glo>al +un-s G 'hese invest in emerging markets. 'hose dedicated to

specific regions in the world, invest in these regions, too. While they takepositions on directional moves in particular markets as the macro fundsdo, they tend to be more bottom#up oriented in that they pick stocks in

individual markets they favour.• Lon* onl/ +un-s G 'hese are traditional e1uity funds that use leverage

and charge incentive fees.

• Mar1et9neutral +un-s G 'hese funds attempt to reduce market risk by

taking offsetting long and short positions and invest in a wide variety of instruments, including those that arbitrage stock and inde& futures, or those that take positions on yield curves in bond markets.

• Sector +un-s G 'hese have an industry focus that includes a wide set of

industries 3 health care, financial services, technology etc.

• Short sale +un-s G *hort sale funds borrow securities they )udge to be

CovervaluedC from brokers and sell them in the market, hoping to buy themback at a lower price when repaying the broker. 'hese funds attractinvestors wishing to hedge long#only portfolios, or those wishing to take aposition that the market is likely to decline.

• E;ent9-ri;en +un-s G 'heir investment theme is to capitalise on events

that are seen as special situations. 'hey encompass distressed securitiesfunds that focus on securities of companies in reorganisation or bankruptcy, and risk arbitrage funds that take a position on the likelihoodof an announced merger or ac1uisition going through by simultaneouslybuying stocks in a company being ac1uired and selling stocks in theac1uiring company.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 26/70

• Fun-s o+ +un-s G 'hese are hedge funds that allocate their portfolio of

investments, sometimes with leverage, among a number of Hedge +unds.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 27/70

LETTERS #F CREDIT

LETTERS #F CREDIT also called 7ocumentary credits are generally usedfor facilitating international trade. However, its use for the domestic (localtrade is also not unknown.

*imply put, etter of redit is an instrument for settling trade payments. It isan arrangement for making payment against documents. 'o elaborate, ; isan undertaking by a bank on behalf of its customer to pay the value of goodsor services to its supplier against submission of specified documents;meetingterms and conditions set out in the ;.

"ARTIES T# A LETTER #F CREDIT

#"ENER is the one at whose re1uest ; is issued by a bank. :pener of ;

is importer or buyer of goods;services.

ISS$ING BANK is the Bank which issues ;.

BENEFICIAR' is the one in whose favour ; is established. Beneficiary of the ; is the e&porter;seller.

ADVISING BANK is the bank which advises the issuance of ; to thebeneficiary. Advising bank verifies the authenticity of the ; before advisingthe beneficiary.

NEG#TIATING BANK is the bank which negotiates documents stipulated inthe ; and is authorised to pay the value (if terms;conditions and documents

as set out in the ; are complied with to the beneficiary.

In addition to above, some times C#NFIRMING BANK is also found in thechain of ; transactions. onfirming Bank is the one which adds its ownconfirmation to pay the value. onfirming bank comes into the picture whenbeneficiary is not comfortable with the opening bank , its creditworthiness or country risk. In such cases, opening bank will arrange to get the ;confirmed through an acceptable bank to the beneficiary.

When opening bank is not maintaining an account with negotiating bank, ithas to reimburse the payment made by the negotiating bank, In such cases,opening bank authorises the negotiating bank to claim the amount of

reimbursement from the bank with which opening bank maintains an account.*uch a bank (where an account is maintained by the opening bank is calledREIMB$RSING BANK4

T'"ES #F L=C%

Re;oca>le L=C is a credit which can be amended or cancelled by the ;issuing bank without notice to the beneficiary.

Irre;oca>le L=C is a credit which cannot be amended or cancelled without theconsent of the parties to ;. In terms of Article 6 of 0%7 //, all ;s areirrevocable unless specifically mentioned as revocable.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 28/70

"a/0ent cre-it is a sight credit, and on presentation of documents specifiedin the ;, value will be paid. In such credits, no bill of e&change or usance billis drawn.

De+erre- ,a/0ent cre-it is a credit under which designated bank makespayments on due dates determined as per terms of ;. *uch ; specifiesthe maturity at which payment has to be made and how such maturity isdetermined. $o drafts;bills of e&changes are drawn under this ;.

Acce,tance cre-it is similar in nature to the deferred payment credit e&ceptthat under this credit, usance bills of e&change are drawn on specified bank or drawee for a specific tenor. 7esignated bank will accept drafts and honour thesame on maturity.

Trans+era>le L=C is a credit that can be transferred at the re1uest of thebeneficiary to another beneficiary in whole or part. However, second

beneficiary cannot transfer it to 2

rd

beneficiary. *uch credit must mention thatit is transferable.

Bac1 to >ac1 L=C is an ; which is issued on the strength of another ;.'his credit helps beneficiary to obtain another ; favouring his supplier. 'his; is like transferable ; e&cept that in case of transferable ;, original ;is transferred to another beneficiary, in case of back#to#back ;, a new ;is issued favouring second beneficiaries.

Re- clause L=C which makes available finance at pre#shipment stageenabling the beneficiary to procure and process goods. *uchpayment;finance at pre#shipment stage is authorised by the opening bank.

*ince clause to this effect is printed in red ink in the ;, it is called Redlause ;.

Green Clause L=C is a ; which contains a clause providing finance for warehousing;storing of goods at the risk of the opening bank till the goodscovered under the credit is put on board.

Re;ol;in* cre-it is a credit under which value and validity of the ; areautomatically reinstated on receiving advice from the issuing bank thatprevious documents have been retired and paid for. *uch credits maintainma&imum drawings under ;.

Stan-9>/ L=C is not strictly ;, It is a substitution of letter of guarantee and

covers only financial commitment. %ayment obligation arises only upon failureof performance. *tand#by credit originated in 0*A and is now widely used inmany countries. 0se of stand by credit in India is increasing in the light of growing liberalisation;globalisation. *ince obligation for payment arises out of non#performance under stand#by credit, opening such credit re1uires e&traprecaution.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 29/70

EX"#RT FINANCE

E<,ort +inance can >e >roa-l/ classi+ie- in 3 cate*ories %

%re#shipment finance, and

5 %ost#shipment finance.

"re9Shi,0ent Finance can >e +urther -i;i-e- into

%acking credit in rupees.

5 %acking credit in foreign currency (%+,

2 Advances against incentives receivable from govt.

E Advances against duty draw#back.

"ost9Shi,0ent Finance can >e in the +or0 o+

%urchase of discount of e&port documents under confirmed orders.

5 $egotiation;payment;acceptance of documents under ;,

2 Advance against e&port bills sent on collection,

E Advance against receivables from !ovt.

8&port bills rediscounted in foreign currency, We will discuss only a few of the above facilities3

"RE9SHI"MENT FINANCE

%acking redit in Rupees is a loan;advance or credit facility granted to ane&porter for procuring and processing raw materials, etc. 'his also includesfinance for transportation, warehousing and shipping. *uch facility can be

granted to an e&porter who has a confirmed e&port order or irrevocable ; inhis name. 8&porter en)oying PAAC;PAAAC rating can be granted OR0$$I$! A:0$'O facility. Where ORunning AccountO facility has been grantedC,re1uirement of prior lodgement of ; is not insisted upon. However, ; firmorders should be produced in reasonable time, ORunning AccountO facility isthe one where that first debit is repaid by the first credit irrespective of the factthat such credit may not pertain to the debit being set#off against.

%acking redit should be repaid from the proceeds of the e&ports. In case it isrepaid from local resources, rate of interest, as applicable to domestic credit(commercial rate, should be charged.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 30/70

%acking credit being in the nature of working capital finance is for short periodonly. 'hese advances are granted for period not e&ceeding >/ days atconcessional rate. 'his period can be e&tended by another ?/ days (total 54/days without reference to RBIQ for where delay is beyond the control of the

e&porter. However, higher rate of interest will be charged for such e&tendedperiod.

+urther, concession in rate of interests is available only if the e&port takesplace within reasonable time from availing of finance. *uch period should note&ceed 26/ days and in case it e&ceeds 26/ days, banks should chargecommercial rate of interest from the date of granting finance. In case noe&port takes place, banks are entitled to charge interest 5< abovecommercial rate.

%+ is packing credit denominated in foreign currency. 'his is done with a

view to avail of low rate of interest prevailing abroad which adds to thecompetitiveness of an e&porter, %+ funds can be used for import of rawmaterial and processing and then ree&porting or for usage in domesticpurposes. %+ is li1uidated by submitting e&port bills for collection or negotiation.

"#ST9SHI"MENT FINANCE

Forei*n Bills ,urchase- or -iscounte- % Increasingly, 1uite a lot of international trade is taking place without the mechanism of ;. Wheredocuments are tendered for purchase or discounting (not accompanied by

;, bank must ensure that the customer is of undoubted worth. *tatusreports, both, on the e&porter as well as the importers should be called for andkept on record. Bank should also verify the kind of goods being e&ported whilepurchasing;discounting the bills. If the goods are of special nature;made#to#order type, it becomes difficult to dispose of such goods in case the buyer fails to pay for it.

Ne*otiation o+ Forei*n Bills un-er L=C % is the most secured form of postshipment finance. Bank negotiates bills complying with terms and conditionsof the ;. Where it does so in pursuance of the mandate given by the issuingbank, negotiating bank is assured of receiving reimbursement from issuing

bank. Bills should be realised within period, failing which it will attractcommercial rate of interest.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 31/70

ECGC SERVICES

As e&ports involve cross border movement of goods and services, theattendant risks are several. 'o mitigate these risks and to encourage bankers

to finance e&port trade on liberal terms, !overnment of India set up 8&portRisk Insurance orporation in Muly ?. It was renamed as 8&port redit @!uarantee orporation of India td. (8! in ?>2.

8! provides %olicies to e&porters and !uarantees to banks coveringvarious risks involved.

&hole Turno;er "ac1in* Cre-it Guarantee &T"CCG!

W'%! is a contract between 8! and Bank, whereby the orporationguarantees protection to Bank against losses sustained in the process of granting pre#shipment finance to e&porters.

'he banks which undertake to obtain cover for packing credit advancesgranted to its customers in all branches, 8! issues Whole 'urnover %acking redit !uarantee W'%!.

Almost all the banks in India have taken the guarantee since then.

Salient +eatures o+ &T"CRis1s co;ere-

• Insolvency of the e&porter.

• %rotracted default of the e&porter.

Guarantee co;era*e+ollowing is the e&tent of coverage 3

• $ormal goods # 4<• Ha"ardous goods # 66.66<

• **8;**I # ?/<

S0all Scale In-ustries 3 Anticipated Annual 8&port 'urnover not e&ceedingRs.5 lacs, irrespective of amount of local sales.

S0all Scale E<,orters 3 Anticipated Annual 'urnover not e&ceeding Rs. E/lacs w;w 8&port 'urnover not to e&ceed Rs. 5 lacs.

Re,ortin* o+ Li0its

Whenever new limits are sanctioned or e&isting limits enhanced, reduced or

cancelled, they should be reported to the orporation immediately but in anycase within 2/ days.

Discretionar/ Li0it

8very !uarantee mentions a limit (in terms of Rupees upto which the bankcan allow packing credit advances to any of its e&porter client without 8!Csapproval. 'his limit is called 7iscretionary imit (7. 4

Monthl/ Declaration an- ,a/0ent o+ ,re0iu0

All branches which have granted % have to submit a monthly declaration to8! along with the amount of premium payable on such declarations. 'he

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 32/70

amount of premium should be calculated at the rate of 4 paise per Rs. // per month on the total average daily products.

%remium is recovered from the e&porters immediately from 7; Account.

Filin* o+ clai0'he Bank should file a claim in respect of an advance within si& months fromthe date of Report of 7efault.

Rene7al o+ Guarantee

'he W'%! issued to the bank e&pires on 2/ th Mune every year and renewalsare made for a period of 5 months i.e. st Muly to 2/th Mune. IB7 takes care of the renewal.

&H#LET$RN#VER "#ST SHI"MENT EX"#RT CREDIT G$ARANTEE&T"SG!

W'%*! was introduced in our Bank w.e.f. .E.??4. It covers post#shipmentfinance granted to e&porters by Banks in the form of purchase, discount andnegotiation of e&port bills. It also covers advance basis and covers entirepost#shipment advance granted by the Bank. In the case of our Bank,W'%*! covers only purchase;discount of e&port bills and advance againste&port bills sent on collection both drawn under contracts.'he salient features of the W'%*! are as under 3Ris1 co;ere-%- Insolvency of the e&porter.- %rotracted default by the e&porter to pay post shipment advance due to

the Bank.- Buyers failure to pay;retire bill will not give rise to claim, unless our

e&porter has failed to ad)ust the advance"ercenta*e o+ co;er%

8&porter who is a Holder of *td. %olicy 8&porter who is not a Holder of *td.%olicy

**8;**I ?/< **8;**I 6<

:thers >< :thers 6/<

"re0iu0

%remium is payable on average amount outstanding calculated on a daily

product basis at the rate of 6 paise for Rs. // per month. %remium is to beborne by the Bank. %resently, we are covering only $on#; e&porttransactions under W'%*!.Re,ort o+ De+ault

In respect of post#shipment advances, non li1uidation of advances will be dueto non#payment by overseas buyer or due to problems in the importingcountries. However, the R:7 has to be filed only if, in the opinion of the bank,the post#shipment advances cannot be recovered from the e&porter in normalcourse. R:7 has to be filed within E months from due date or e&tended duedate or one month from date of recall, whichever is earlier.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 33/70

Clai0slaims should be filed by the branch within 6 months from the date of filing of R:7 with the nearest office of the 8! which services the branch.

N#N RESIDENT DE"#SIT ACC#$NTS

$on#Resident deposit accounts are governed by regulations contained in the+8-A. An e&tract of relevant schemes;guidelines are as under 3Non9resi-ent #r-inar/ Ru,ee NR#! Account% can be opened by anyperson resident outside India. 'hese accounts can be opened in the form of savings, current, recurring or fi&ed deposits. %roceeds of inward remittancesor permitted currency tendered by the account holder during his visit to Indiaor transfers from rupee accounts of non#resident banks are permitted modes

of credits into $R: account. ocal payments, including payments for investments are allowed from $R: accounts. Remittance of current incomenet of applicable ta&es is allowed.oans to account holders can be granted in rupees for personalpurposes;carrying on business sub)ect to norms as applicable to residentaccounts. *uch loans can be granted to third parties also.$R: accounts can be held )ointly with residents.Non9Resi-ent Non9Re,atria>le! Ru,ee De,osit accounts% can be openedby any person resident outside India. 'hese accounts are opened in the formof term deposits only for periods ranging from 6 months to 26 months. Banksare free to determine rates of interest on deposits under this *cheme and onadvances against funds held in such deposits. Interest accrued on $R$Rdeposits is repatriable. However, if the interest is reinvested, amount of interest so reinvested will not be eligible for repatriation.$R$R deposits can be opened in )oint names with the resident.oans; overdrafts can be granted to the account holders and third parties for personal purposes;carrying on business against the security of $R$Rdeposits.Non9Resi-ent S,ecial! Ru,ee Accounts% can be opened by $RI whovoluntarily undertake not to seek remittance of funds held in these accountsas also income earned thereon. 'hese accounts carry the same facilities and

restrictions as applicable to domestic accounts of residents regardingrepatriation of funds and income thereon. 'hese accounts can be held in theform of savings, current, recurring or fi&ed deposit. *uch accounts can be held )ointly with residents. :perations in the account are allowed freely as in caseof domestic accounts. A special application#cum#undertaking form has been devised by ReserveBank of India for opening these accounts.Non9Resi-ent E<ternal! Ru,ee Accounts% can be opened by $RIs and:Bs. *uch accounts can be in the form of savings, current, recurring or fi&eddeposit. Balances held in the account can be repatriated outside India. Andtherefore, credits in the account are regulated as to the source. %roceeds of

inward remittances, che1ues drawn on foreign bank;branches, travellersche1ues or foreign currency notes or transfer from other $R8;+$R accounts

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 34/70

is permitted to be credited into $R8 account. :n the other hand, debits for local disbursements are allowed. Wherever regulations permit, debits areallowed for investment in shares;securities of an Indian company or for purchase of immovable property in India.

oans against the security of the funds held in the $R8 account can begranted to the account holder for personal purposes or for carrying onbusiness activity. Repayment of such loans will be made by means of either appropriating the deposit or fresh inward remittance or out of the local rupeeresources in the $R: account of the borrower. oans can also be granted for direct investment on non#repatriation basis or for the purpose of ac1uisition of flat;house for own residential use.Banks can grant fund#based;non#fund based facility to residentindividuals;firms;companies against the collateral of +7 held in $R8 account.however, for such loans, there should be no direct;indirect foreign e&changeconsideration for the non#resident depositor agreeing to pledge his deposit.

Income from interest is e&empt from Income 'a&. Balances held in the $R8accounts are e&empt from Wealth 'a&.Forei*n Currenc/ Non9Resi-entB! Accounts% can be opened by all $RIsand :Bs in currencies G 0* 7ollar, %ound *terling and euro. 'heseaccounts can be opened only as term deposit for maturities ranging from 5months and up to 26 months. All debits and credits permitted in the $R8accounts are permitted in +$R (B accounts also.*ince the deposit and interest thereon is denominated in foreign currencyonly, the depositor is not e&posed to e&change rate risk. However, ReserveBank of India does not provide e&change rate guarantee;cover to the banks.Banks can lend resources mobilised under these accounts without anyinterest rate stipulations made by Reserve Bank of India. 'hat is to say, bankscan determine rates of interest on loans made out of +$R (B funds.Resi-ent Forei*n Currenc/ Accounts RFC! can be opened by a personresident in India out of foreign e&change received as pension;any other superannuation benefits from his employer outside India or received asgift;inheritance or ac1uired when he was resident outside India.'hese accounts are maintained in foreign currencies only. 'hese accounts arefree from all restrictions regarding utilisation or foreign currency balancesincluding restriction on investment in any form outside India.E<chan*e Earners Forei*n Currenc/ Accounts Sche0e EEFC!% was

introduced in ??5 to enable e&porters and other e&change earners to retain aportion of their receipts in foreign e&change with an authorised dealer in India.//< 8&port#:riented 0nits or a unit in (a 8&port %rocessing Done or (b*oftware 'echnology %ark or (c 8lectronic Hardware 'echnology %ark mayretain 4/< and any other person resident in India may retain /< of theeligible inward remittances.88+ accounts can be held in the form of non interest bearing currentaccounts only. $o credit facility (funded or non#funded can be made availableagainst the 88+ balances. 88+ funds can be used for payments outsideIndia in the nature of current account.$NFIXED DE"#SIT SCHEME #F #$R BANK F#R NRIs

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 35/70

• Withdrawal in multiples of units of Rs.///;# alongwith interest without loss

of interest on continuing units.

• 0nit withdrawal will be treated as prematurely withdrawn.

• 7eposit together with interest is fully repatriable.

• It is treated as $R8 deposits.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 36/70

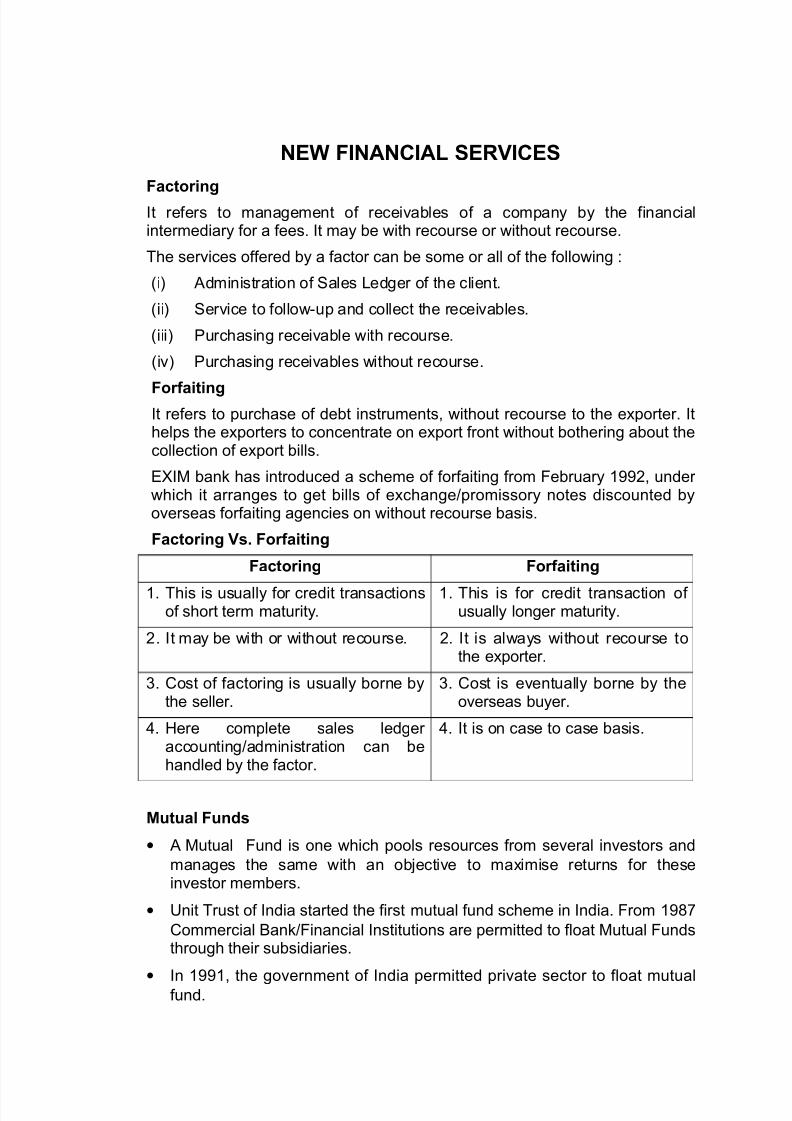

NE& FINANCIAL SERVICES

Factorin*

It refers to management of receivables of a company by the financialintermediary for a fees. It may be with recourse or without recourse.

'he services offered by a factor can be some or all of the following 3

(i Administration of *ales edger of the client.

(ii *ervice to follow#up and collect the receivables.

(iii %urchasing receivable with recourse.

(iv %urchasing receivables without recourse.

For+aitin*It refers to purchase of debt instruments, without recourse to the e&porter. Ithelps the e&porters to concentrate on e&port front without bothering about thecollection of e&port bills.

8NI- bank has introduced a scheme of forfaiting from +ebruary ??5, under which it arranges to get bills of e&change;promissory notes discounted byoverseas forfaiting agencies on without recourse basis.

Factorin* Vs4 For+aitin*

Factorin* For+aitin*

. 'his is usually for credit transactionsof short term maturity.

. 'his is for credit transaction of usually longer maturity.

5. It may be with or without recourse. 5. It is always without recourse tothe e&porter.

2. ost of factoring is usually borne bythe seller.

2. ost is eventually borne by theoverseas buyer.

E. Here complete sales ledger accounting;administration can behandled by the factor.

E. It is on case to case basis.

Mutual Fun-s

• A -utual +und is one which pools resources from several investors and

manages the same with an ob)ective to ma&imise returns for theseinvestor members.

• 0nit 'rust of India started the first mutual fund scheme in India. +rom ?>4

ommercial Bank;+inancial Institutions are permitted to float -utual +undsthrough their subsidiaries.

•

In ??, the government of India permitted private sector to float mutualfund.

7/17/2019 Latest Banking Dev

http://slidepdf.com/reader/full/latest-banking-dev 37/70

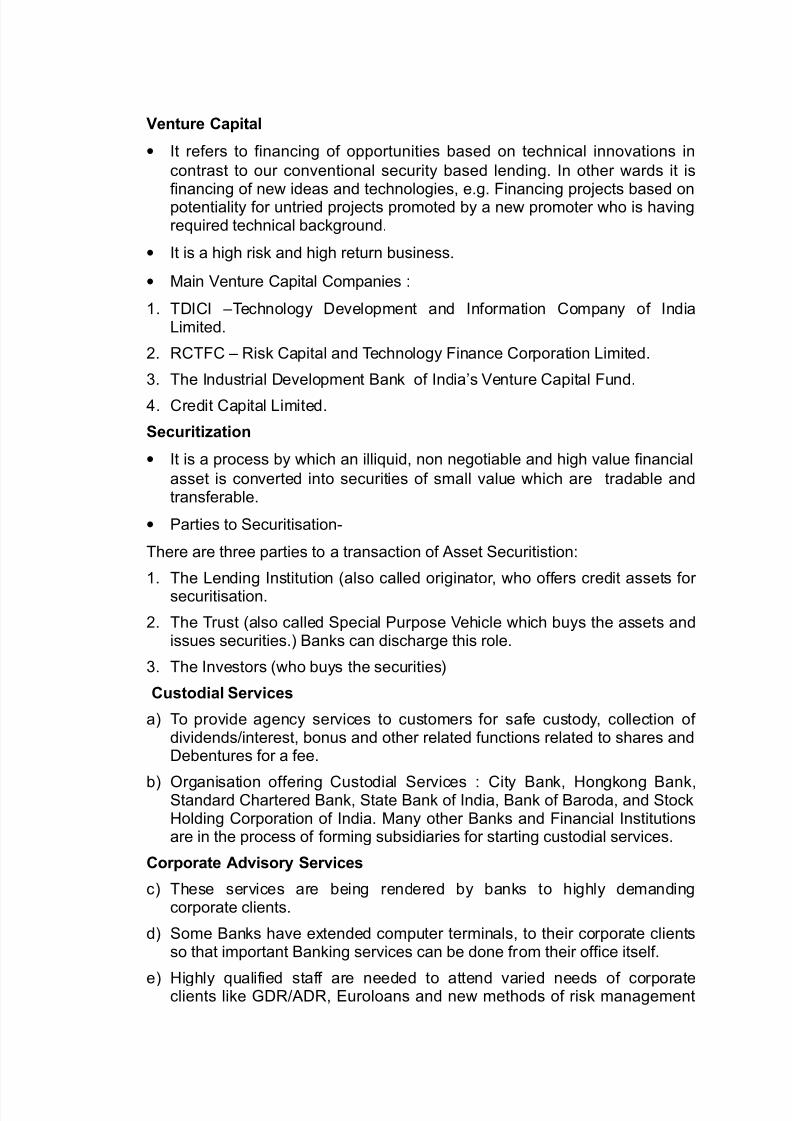

Venture Ca,ital

• It refers to financing of opportunities based on technical innovations in

contrast to our conventional security based lending. In other wards it is

financing of new ideas and technologies, e.g. +inancing pro)ects based onpotentiality for untried pro)ects promoted by a new promoter who is havingre1uired technical background.

• It is a high risk and high return business.

• -ain Jenture apital ompanies 3

. '7II G'echnology 7evelopment and Information ompany of Indiaimited.

5. R'+ G Risk apital and 'echnology +inance orporation imited.

2. 'he Industrial 7evelopment Bank of India=s Jenture apital +und.

E. redit apital imited.

Securitiation

• It is a process by which an illi1uid, non negotiable and high value financial

asset is converted into securities of small value which are tradable andtransferable.

• %arties to *ecuritisation#

'here are three parties to a transaction of Asset *ecuritistion3

. 'he ending Institution (also called originator, who offers credit assets for securitisation.

5. 'he 'rust (also called *pecial %urpose Jehicle which buys the assets andissues securities. Banks can discharge this role.