Embed Size (px)

Citation preview

Latin America Fertilizer Demand

GPCA

September 2017

Douglas Hoadley

Legal Notice

This presentation is private and confidential. It must not be disclosed in whole or in part, directly or indirectly

or in any other format without the prior written permission of CRU International Limited.

CRU International Limited’s responsibility is solely to its clients and its liability is limited to the amount of the

fees actually paid for professional services.

Although reasonable care and diligence has been used in the preparation of this presentation, we do not

guarantee the accuracy of any data, assumptions, forecasts or other forward-looking statements.

We accept no liability to third parties, howsoever arising.

2

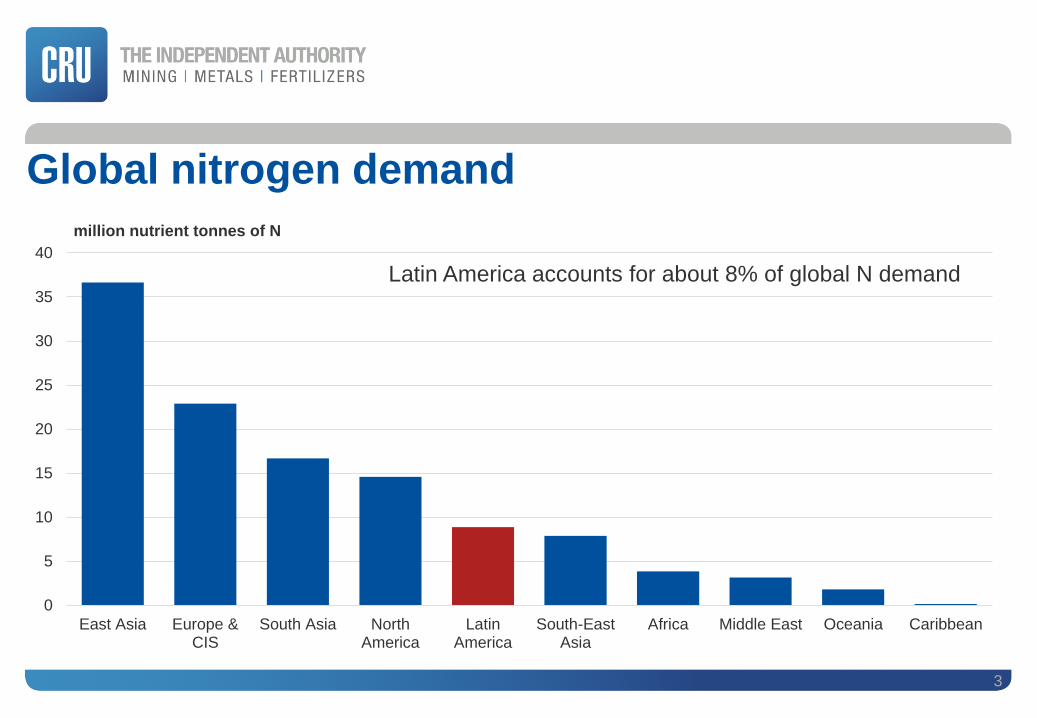

Global nitrogen demand

3

0

5

10

15

20

25

30

35

40

East Asia Europe &CIS

South Asia NorthAmerica

LatinAmerica

South-EastAsia

Africa Middle East Oceania Caribbean

million nutrient tonnes of N

Latin America accounts for about 8% of global N demand

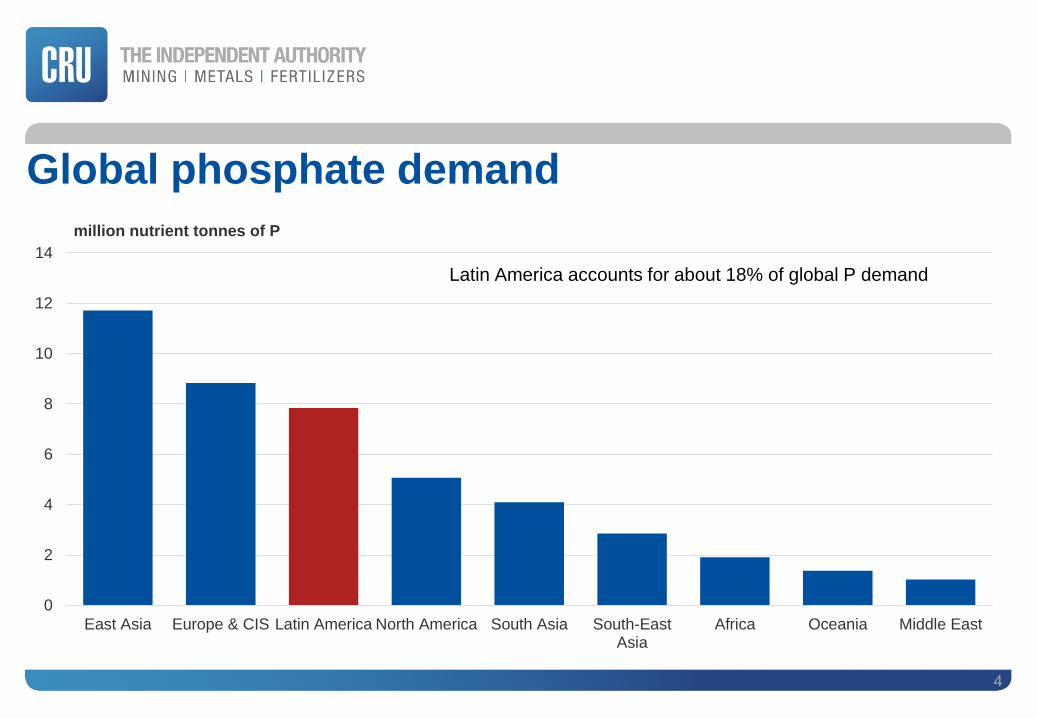

Global phosphate demand

4

0

2

4

6

8

10

12

14

East Asia Europe & CIS Latin America North America South Asia South-EastAsia

Africa Oceania Middle East

million nutrient tonnes of P

Latin America accounts for about 18% of global P demand

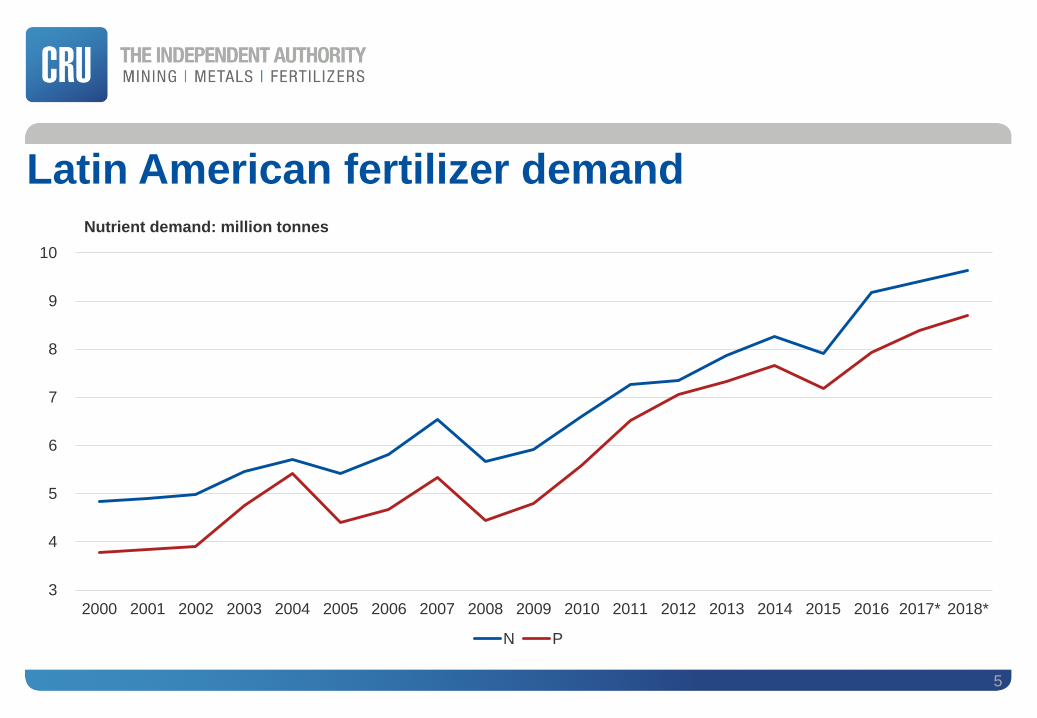

Latin American fertilizer demand

5

3

4

5

6

7

8

9

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018*

Nutrient demand: million tonnes

N P

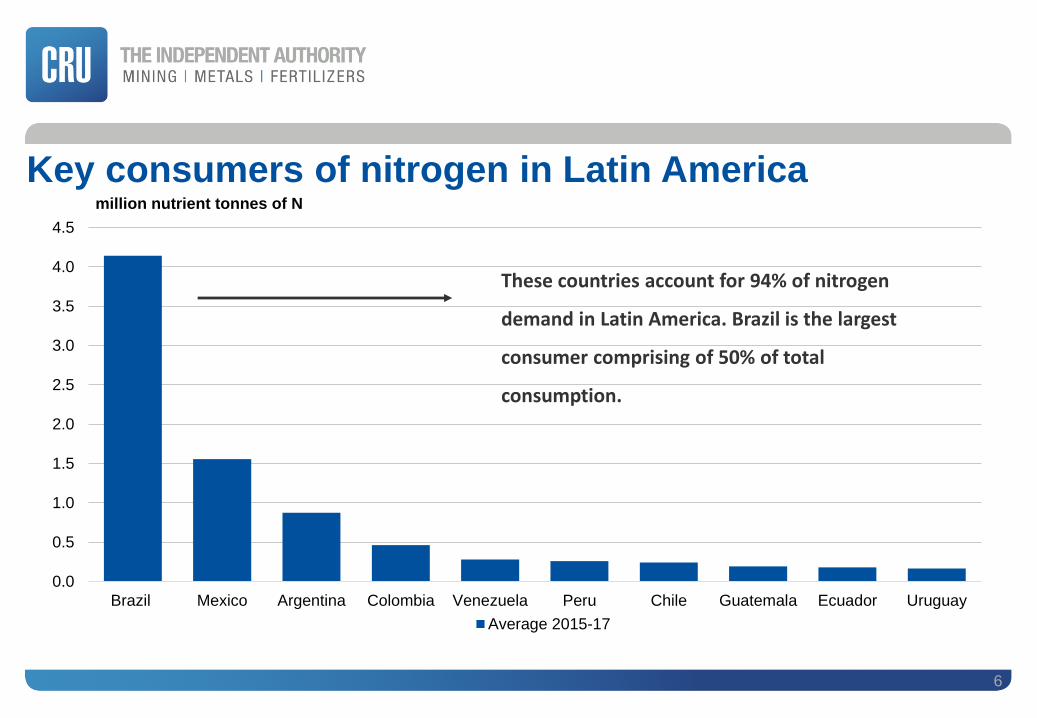

Key consumers of nitrogen in Latin America

6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Brazil Mexico Argentina Colombia Venezuela Peru Chile Guatemala Ecuador Uruguay

million nutrient tonnes of N

Average 2015-17

These countries account for 94% of nitrogen

demand in Latin America. Brazil is the largest

consumer comprising of 50% of total

consumption.

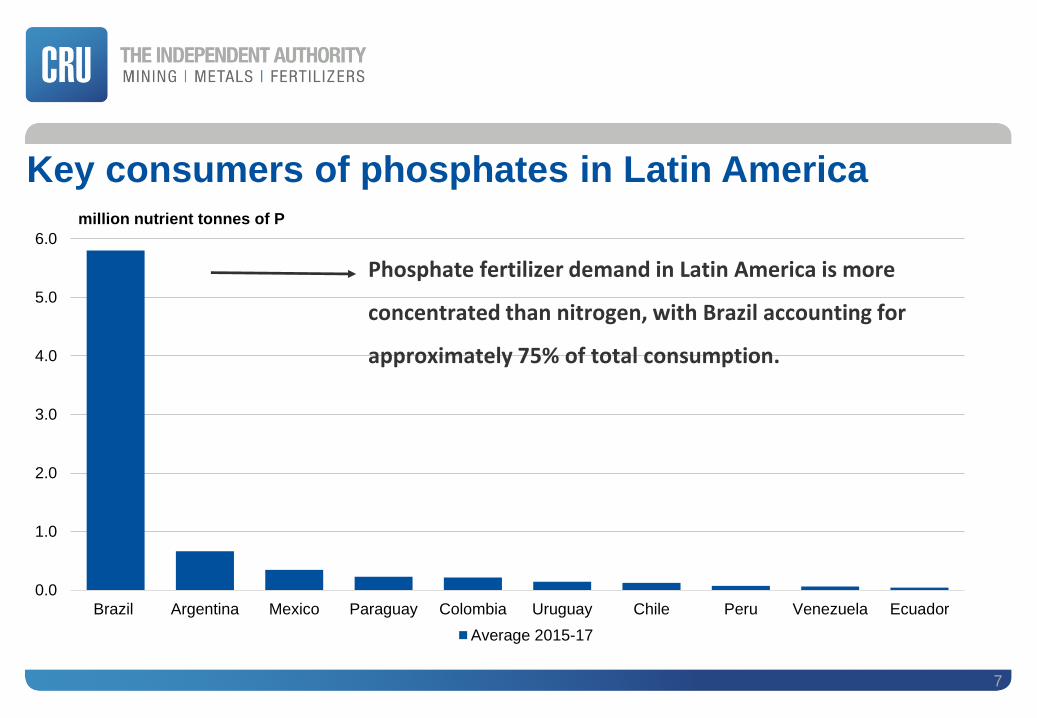

Key consumers of phosphates in Latin America

7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Brazil Argentina Mexico Paraguay Colombia Uruguay Chile Peru Venezuela Ecuador

million nutrient tonnes of P

Average 2015-17

Phosphate fertilizer demand in Latin America is more

concentrated than nitrogen, with Brazil accounting for

approximately 75% of total consumption.

Brazil is an agricultural powerhouse

8

• Availability of arable land, regular rainfall and suitable climatic conditions.

• World’s largest producer of sugar, the second biggest producer of soybeans.

• Total fertilizer demand (N, P and K) has grown at approximately 7.1% per annum between 2008-2017.

• A majority of the expansion has occurred in the Cerrado, a vast tropical savannah region in centre-west Brazil covering states such as Goias, Mato Grosso and Mato Grosso do Sul.

• Crop expansion has been driven by the conversion of pasture lands in the Cerrado from livestock to soybeans and corn.

• Brazilian fertilizer demand is mainly met through imports

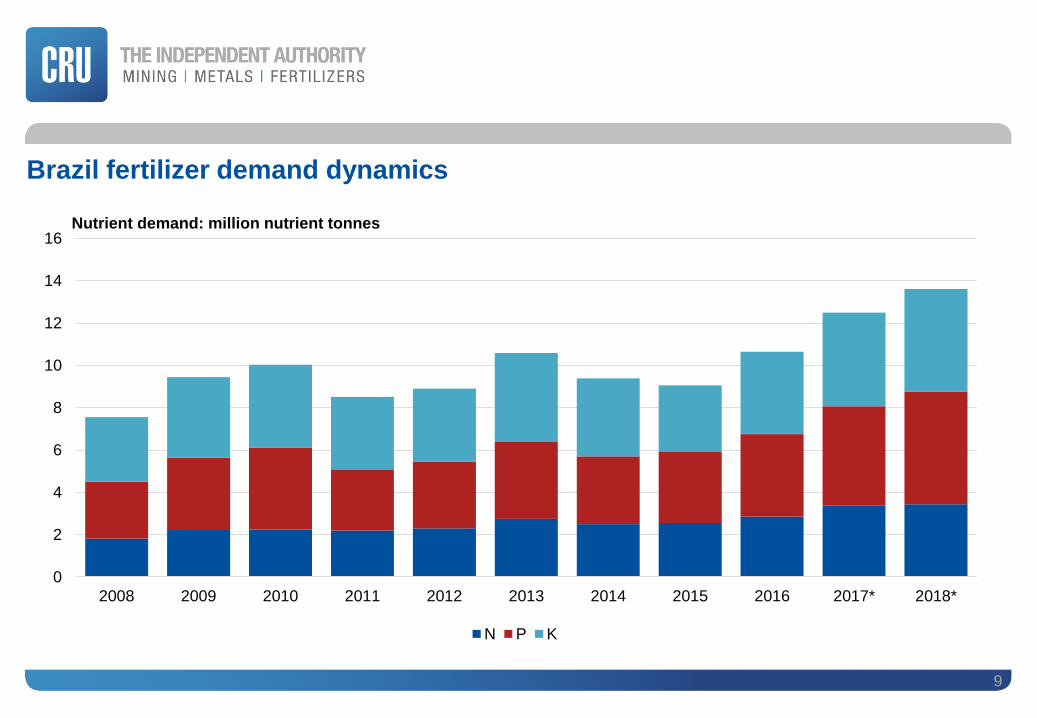

Brazil fertilizer demand dynamics

9

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018*

Nutrient demand: million nutrient tonnes

N P K

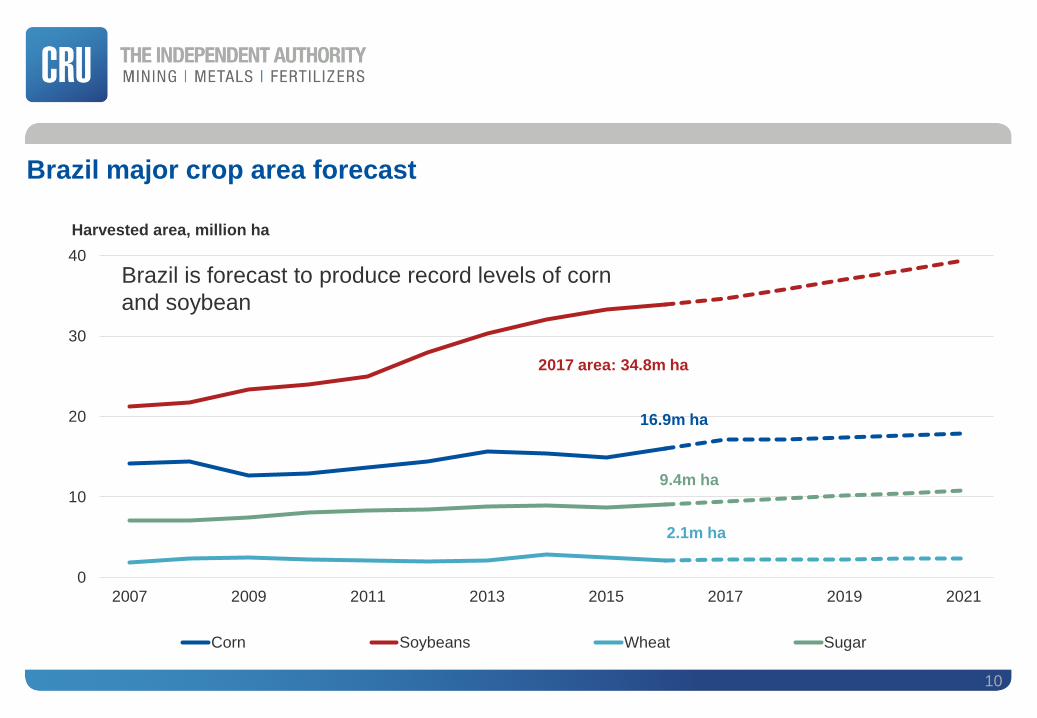

Brazil major crop area forecast

10

0

10

20

30

40

2007 2009 2011 2013 2015 2017 2019 2021

Harvested area, million ha

Corn Soybeans Wheat Sugar

16.9m ha

2017 area: 34.8m ha

2.1m ha

9.4m ha

Brazil is forecast to produce record levels of corn

and soybean

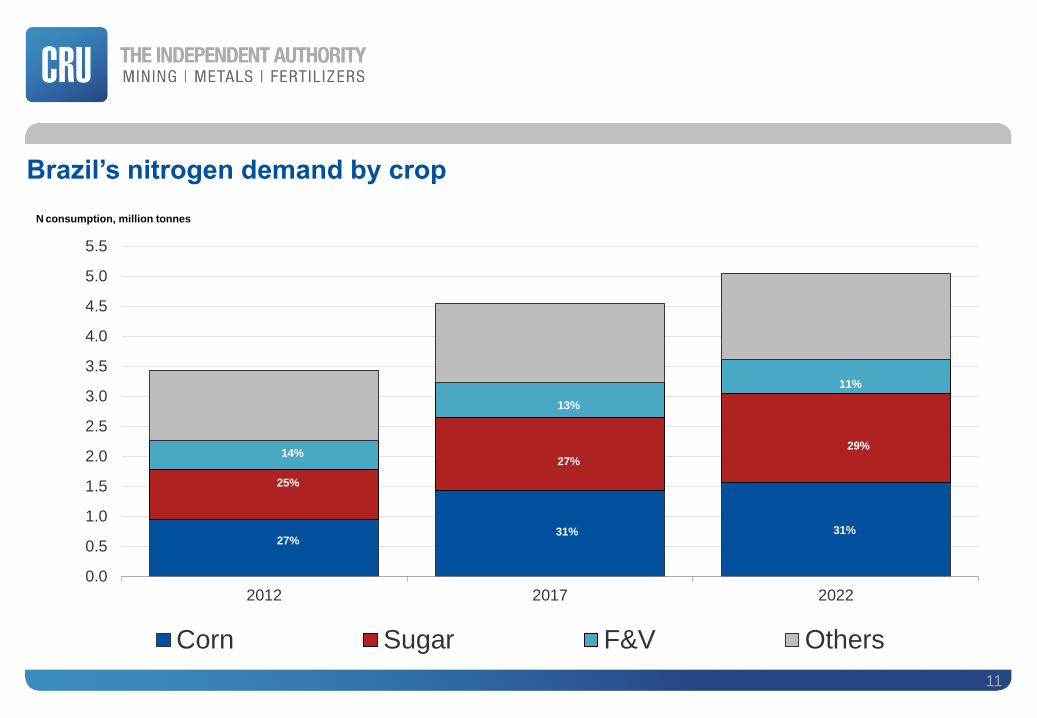

Brazil’s nitrogen demand by crop

11

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2012 2017 2022

Corn Sugar F&V Others

N consumption, million tonnes

27%31% 31%

25%

27%

29%14%

13%

11%

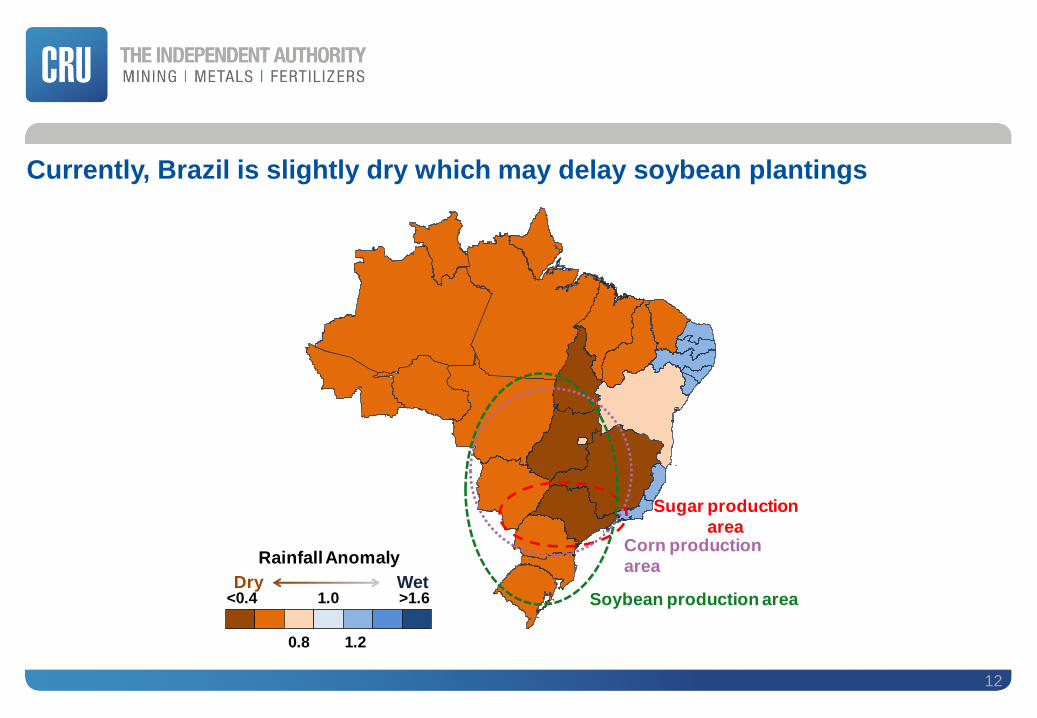

Currently, Brazil is slightly dry which may delay soybean plantings

12

Sugar production

area

Soybean production area

Corn production

area

<0.4 1.0

0.8 1.2

>1.6

Rainfall Anomaly

Dry Wet

Brazil’s Cerrado region is large scale agriculture

13

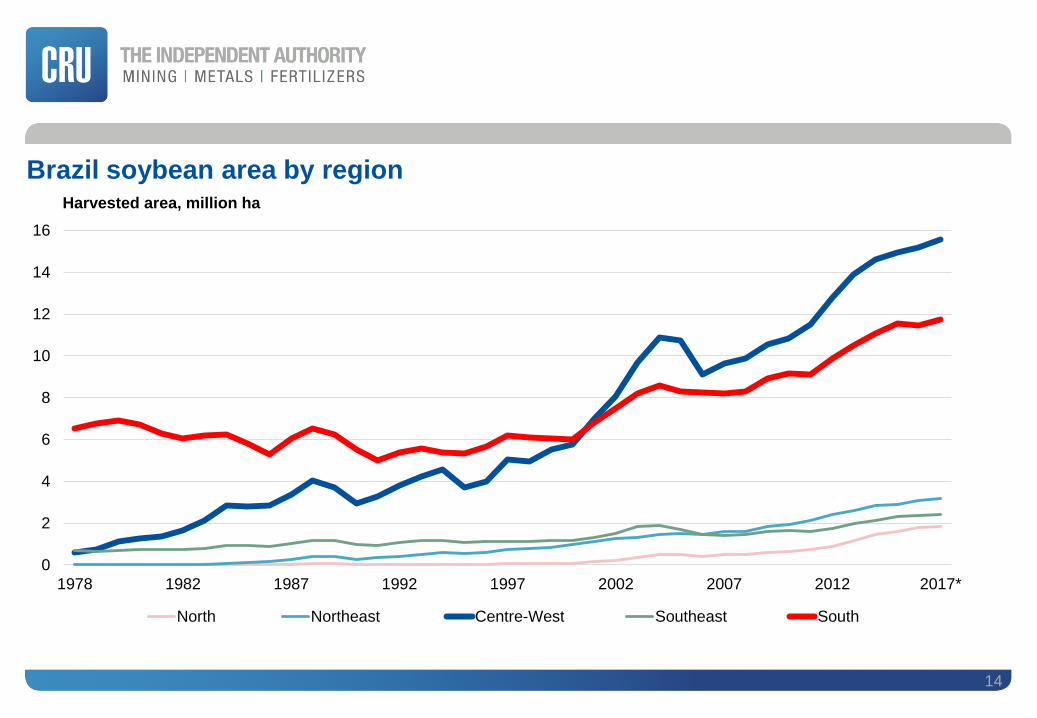

Brazil soybean area by region

14

0

2

4

6

8

10

12

14

16

1978 1982 1987 1992 1997 2002 2007 2012 2017*

Harvested area, million ha

North Northeast Centre-West Southeast South

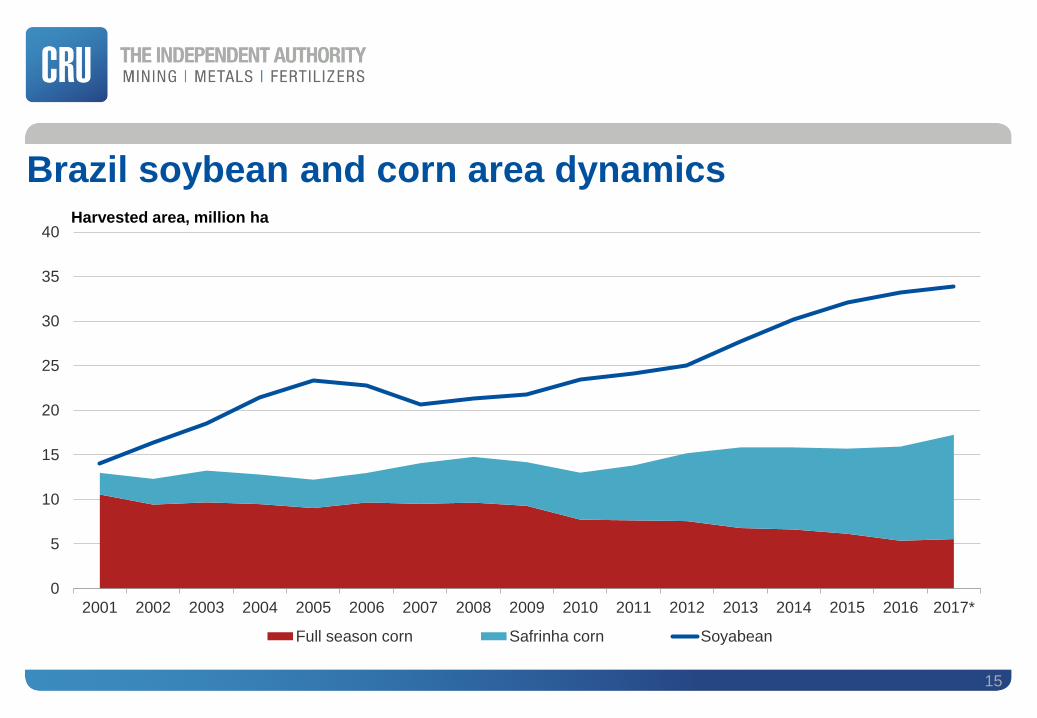

Brazil soybean and corn area dynamics

15

0

5

10

15

20

25

30

35

40

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Full season corn Safrinha corn Soyabean

Harvested area, million ha

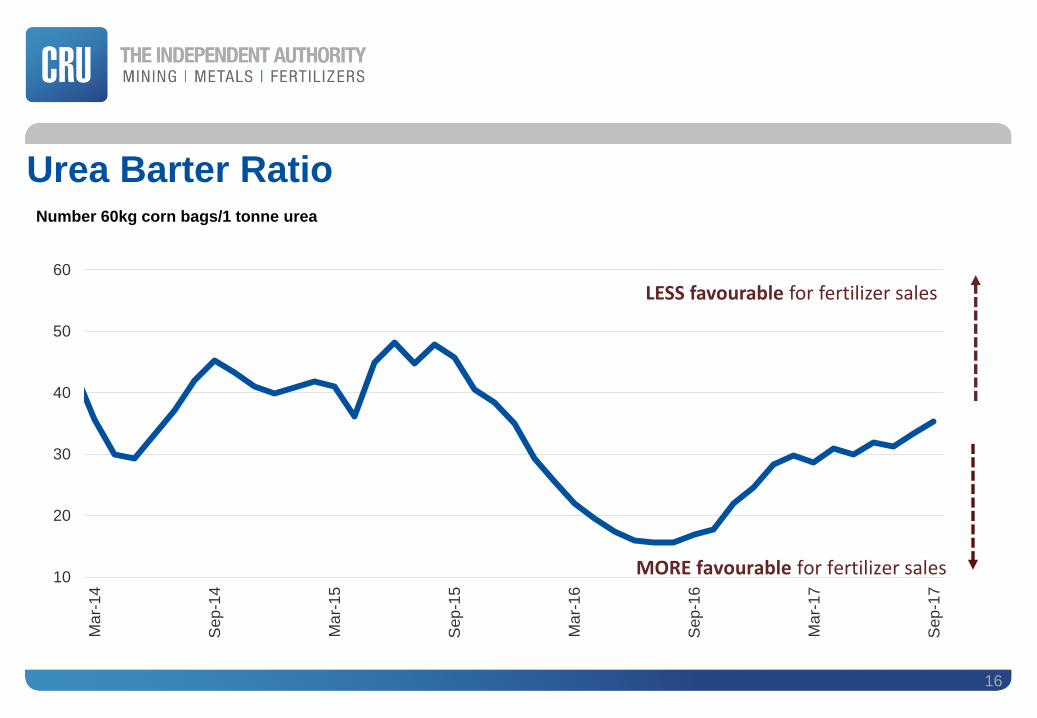

Urea Barter Ratio

16

10

20

30

40

50

60

Ma

r-14

Sep

-14

Ma

r-15

Sep

-15

Ma

r-16

Sep

-16

Ma

r-17

Sep

-17

Number 60kg corn bags/1 tonne urea

LESS favourable for fertilizer sales

MORE favourable for fertilizer sales

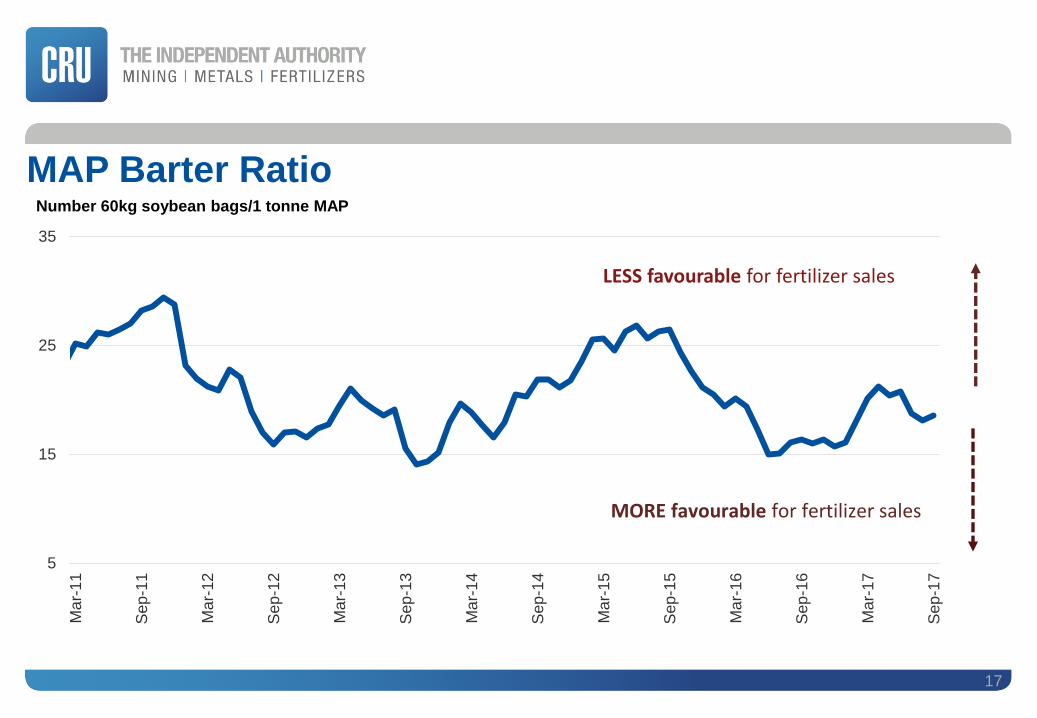

MAP Barter Ratio

17

5

15

25

35

Ma

r-11

Sep

-11

Ma

r-12

Sep

-12

Ma

r-13

Sep

-13

Ma

r-14

Sep

-14

Ma

r-15

Sep

-15

Ma

r-16

Sep

-16

Ma

r-17

Sep

-17

Number 60kg soybean bags/1 tonne MAP

LESS favourable for fertilizer sales

MORE favourable for fertilizer sales

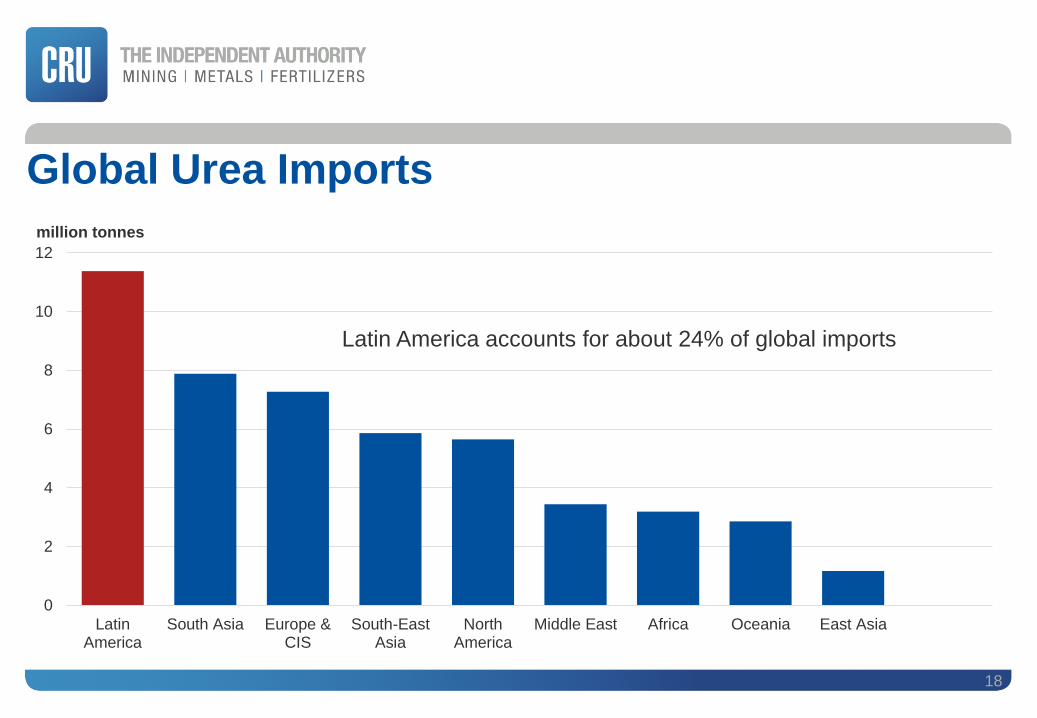

Global Urea Imports

18

0

2

4

6

8

10

12

LatinAmerica

South Asia Europe &CIS

South-EastAsia

NorthAmerica

Middle East Africa Oceania East Asia

million tonnes

Latin America accounts for about 24% of global imports

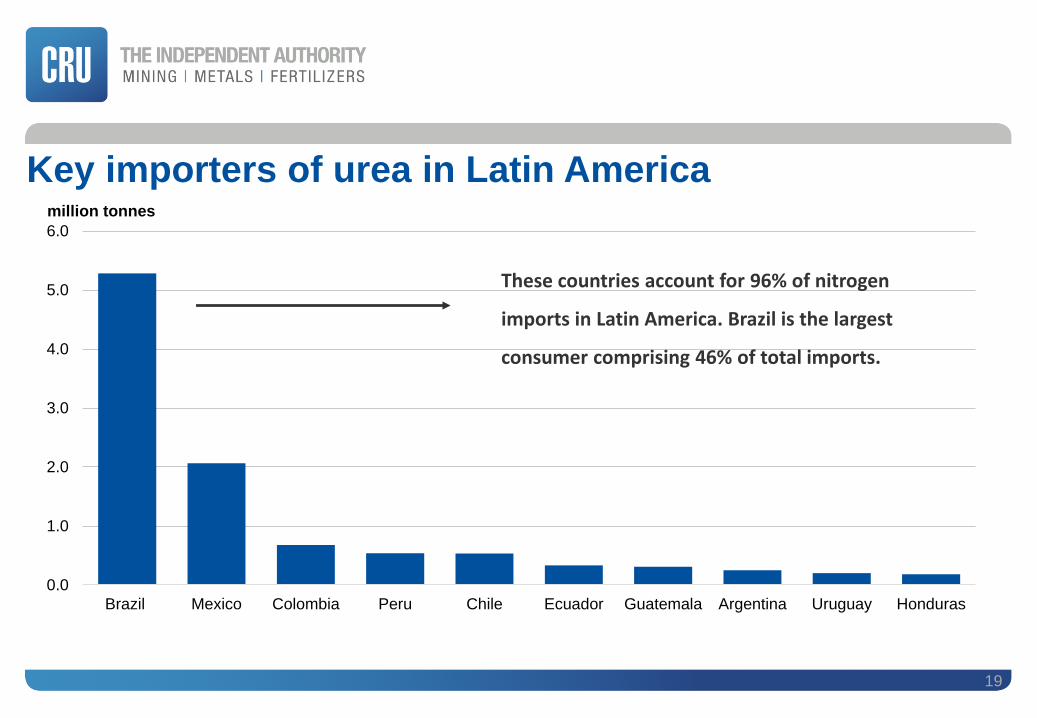

Key importers of urea in Latin America

19

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Brazil Mexico Colombia Peru Chile Ecuador Guatemala Argentina Uruguay Honduras

million tonnes

These countries account for 96% of nitrogen

imports in Latin America. Brazil is the largest

consumer comprising 46% of total imports.

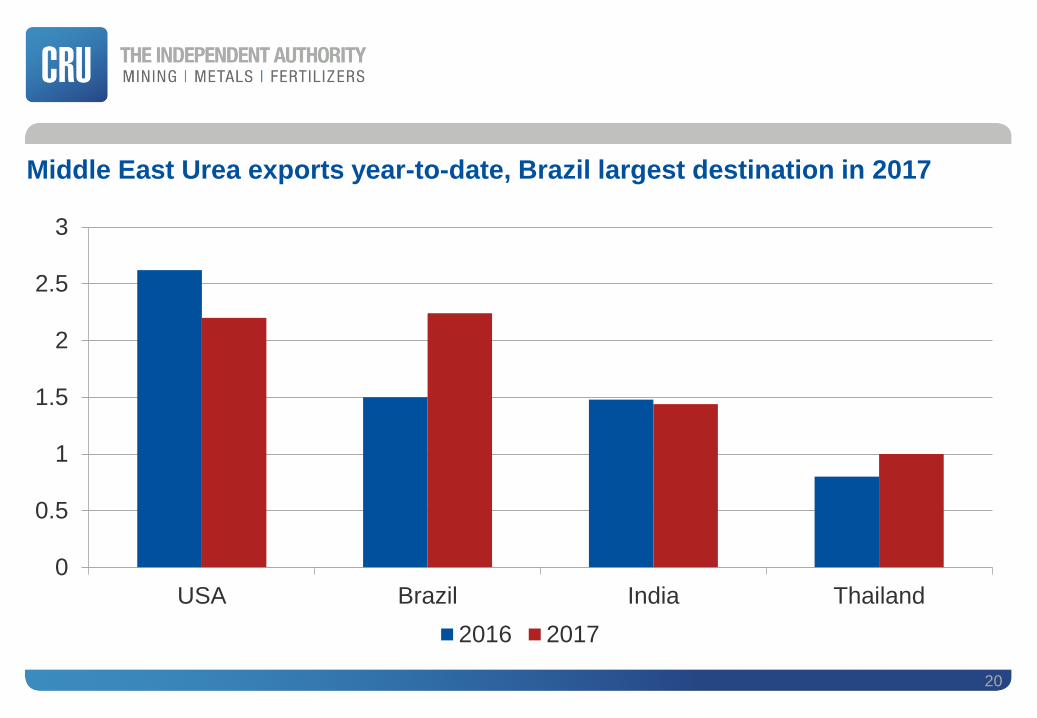

Middle East Urea exports year-to-date, Brazil largest destination in 2017

20

0

0.5

1

1.5

2

2.5

3

USA Brazil India Thailand

2016 2017

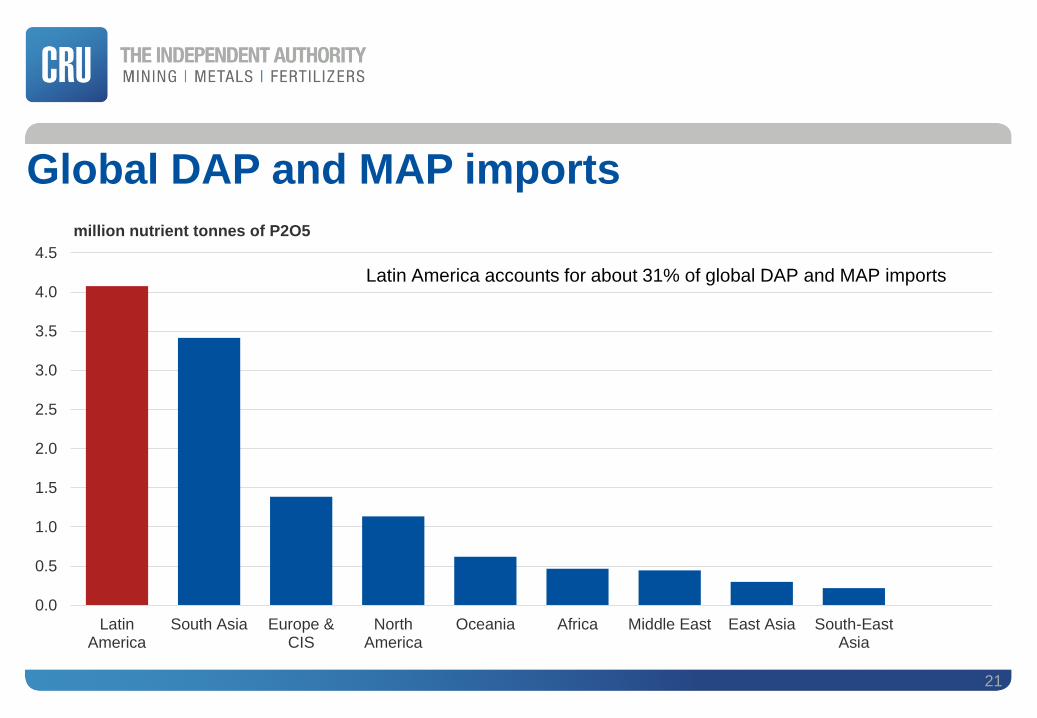

Global DAP and MAP imports

21

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

LatinAmerica

South Asia Europe &CIS

NorthAmerica

Oceania Africa Middle East East Asia South-EastAsia

million nutrient tonnes of P2O5

Latin America accounts for about 31% of global DAP and MAP imports

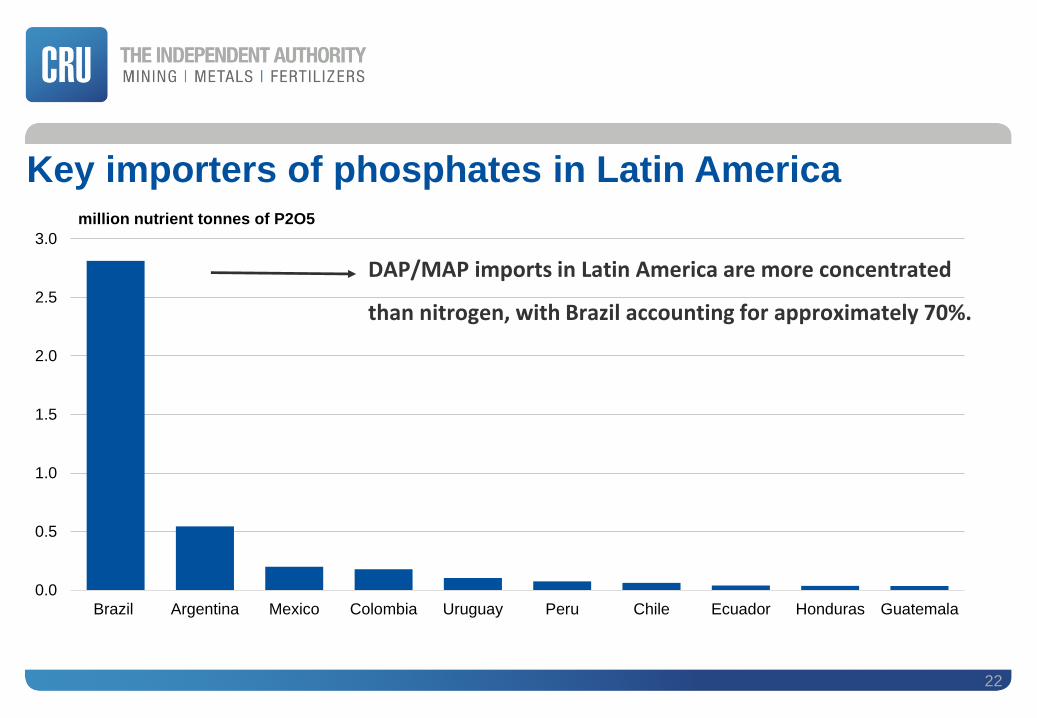

Key importers of phosphates in Latin America

22

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Brazil Argentina Mexico Colombia Uruguay Peru Chile Ecuador Honduras Guatemala

million nutrient tonnes of P2O5

DAP/MAP imports in Latin America are more concentrated

than nitrogen, with Brazil accounting for approximately 70%.

Conclusions

23

•Latin America accounts for 8% of global nitrogen demand and 18% of phosphates demand.

•Brazil, Argentina, Mexico, Colombia are the largest consumers in the region; Brazil alone accounts for 50% of the region’s nitrogen demand and 75% of phosphates.

•Brazil is a large market with high growth rates as soybeans and corn plantings continue to increase.

•Most of this region’s demand is met by imports and Latin America accounts for 24% of global nitrogen imports and 31% of phosphates imports.

•The Middle East has shifted some urea exports from the US to Brazil over the last year.

CRU’s Market Outlook products each provide a medium-term

market analysis service across a range of mining, metals and

fertilizer commodity markets.

Subscribers also have access to:

Market Outlooks

● An executive summary, including key narratives in graphical

form, and scenario analysis as part of the main report

● A comprehensive, downloadable, global demand, supply,

capacity, trade and price data

● Timely CRU Views on the latest market developments

● CRU’s macroeconomic and exchange rate forecasts from

CRU’s own in-house team of economists

● Personal contact with our global team of analysts

24

Thank You!

25

![Genesis Disclosed eBook[1]](https://img.pdfslide.net/doc/110x75/577ce4091a28abf1038d8e66/genesis-disclosed-ebook1.jpg)