Embed Size (px)

Citation preview

Launch & Space Liability Insurance Overview

Presentation to COMSTACWashington, DCOctober 30, 2008

Raymond F. Duffy Jr.Senior Vice PresidentWillis [email protected]

Page 2

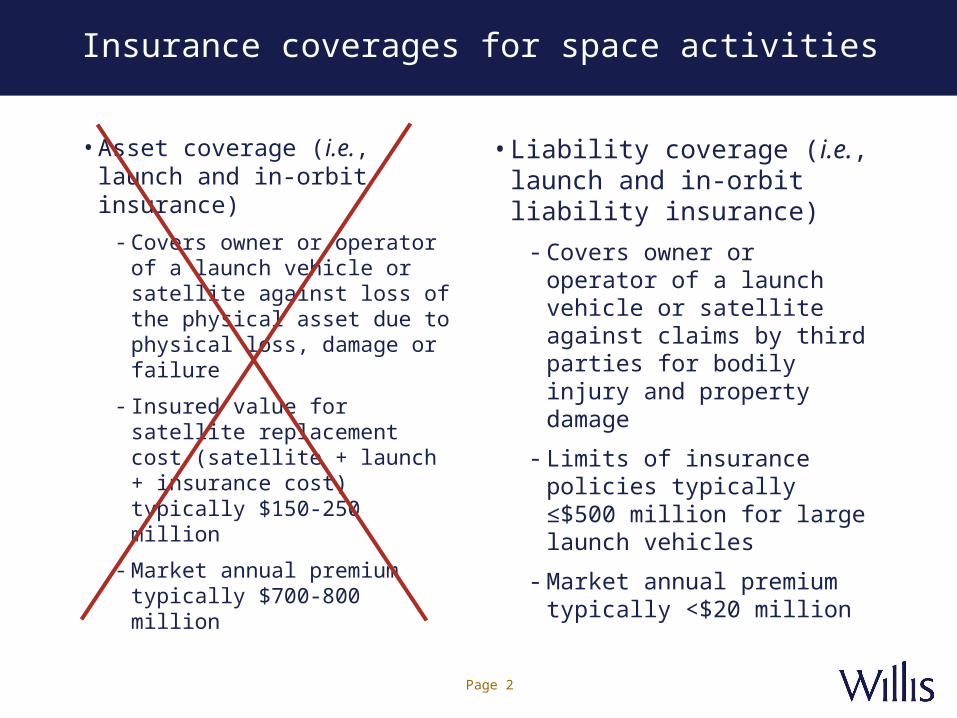

Insurance coverages for space activities

• Asset coverage (i.e., launch and in-orbit insurance)

- Covers owner or operator of a launch vehicle or satellite against loss of the physical asset due to physical loss, damage or failure

- Insured value for satellite replacement cost (satellite + launch + insurance cost) typically $150-250 million

- Market annual premium typically $700-800 million

• Liability coverage (i.e., launch and in-orbit liability insurance)

- Covers owner or operator of a launch vehicle or satellite against claims by third parties for bodily injury and property damage

- Limits of insurance policies typically ≤$500 million for large launch vehicles

- Market annual premium typically <$20 million

Page 3

Space liability - historical developments

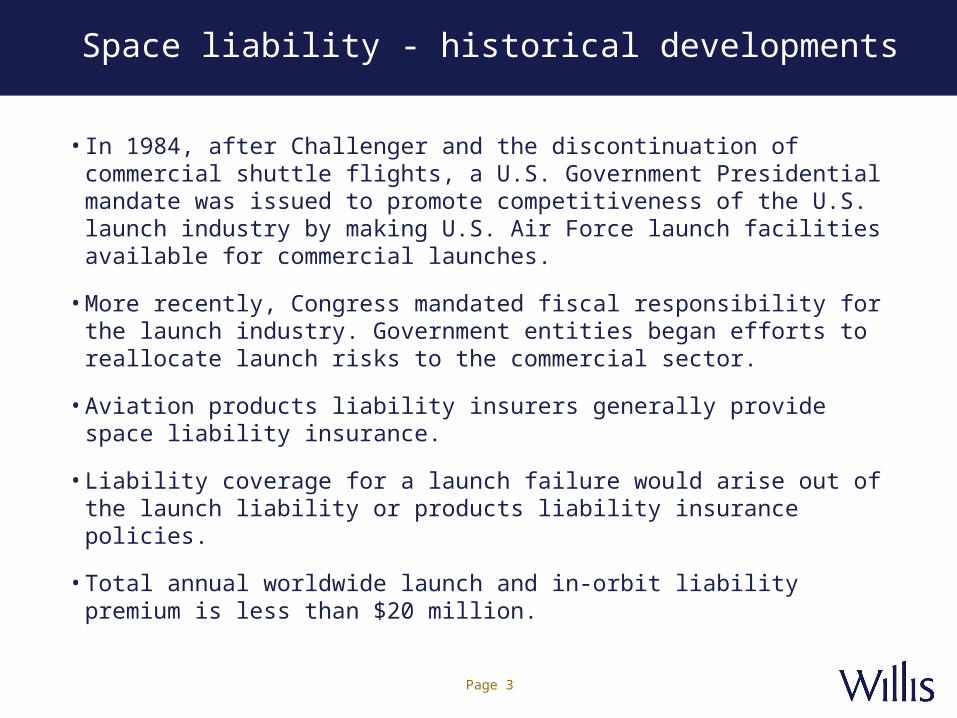

• In 1984, after Challenger and the discontinuation of commercial shuttle flights, a U.S. Government Presidential mandate was issued to promote competitiveness of the U.S. launch industry by making U.S. Air Force launch facilities available for commercial launches.

• More recently, Congress mandated fiscal responsibility for the launch industry. Government entities began efforts to reallocate launch risks to the commercial sector.

• Aviation products liability insurers generally provide space liability insurance.

• Liability coverage for a launch failure would arise out of the launch liability or products liability insurance policies.

• Total annual worldwide launch and in-orbit liability premium is less than $20 million.

Page 4

U.S. Government Launches

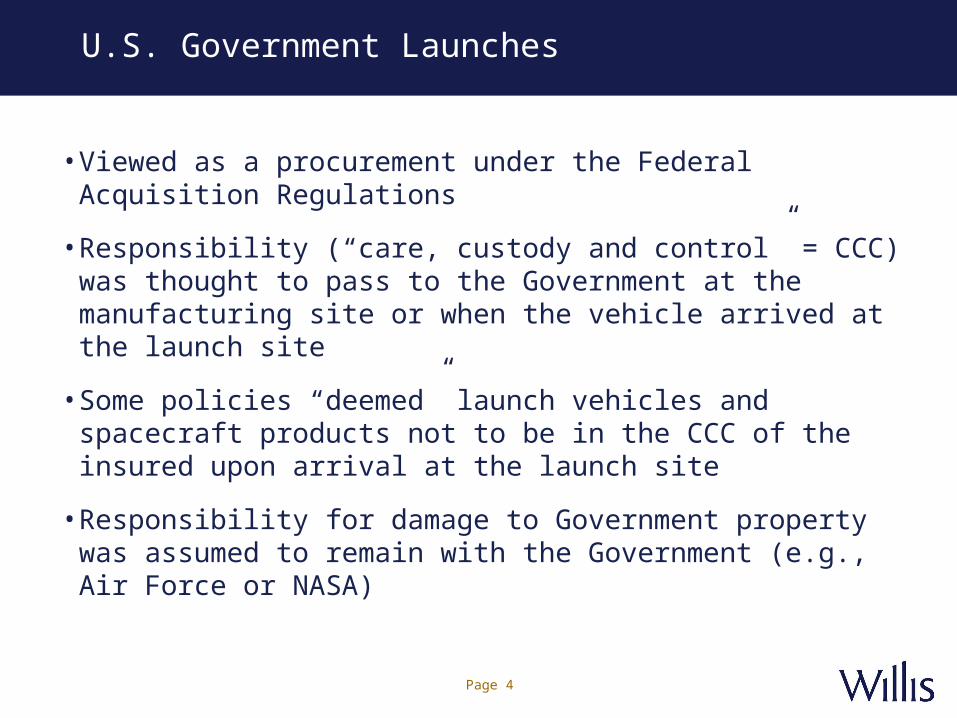

• Viewed as a procurement under the Federal Acquisition Regulations

• Responsibility (“care, custody and control” = CCC) was thought to pass to the Government at the manufacturing site or when the vehicle arrived at the launch site

• Some policies “deemed” launch vehicles and spacecraft products not to be in the CCC of the insured upon arrival at the launch site

• Responsibility for damage to Government property was assumed to remain with the Government (e.g., Air Force or NASA)

Page 5

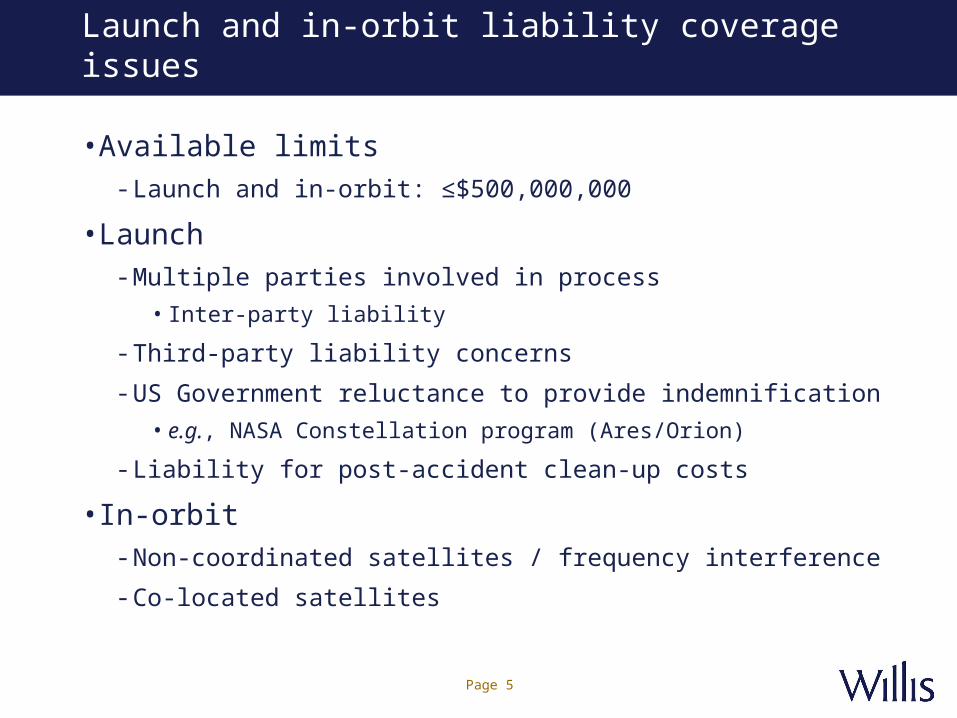

Launch and in-orbit liability coverage issues

• Available limits- Launch and in-orbit: ≤$500,000,000

• Launch- Multiple parties involved in process

• Inter-party liability

- Third-party liability concerns

- US Government reluctance to provide indemnification

• e.g., NASA Constellation program (Ares/Orion)

- Liability for post-accident clean-up costs

• In-orbit- Non-coordinated satellites / frequency interference

- Co-located satellites

Page 6

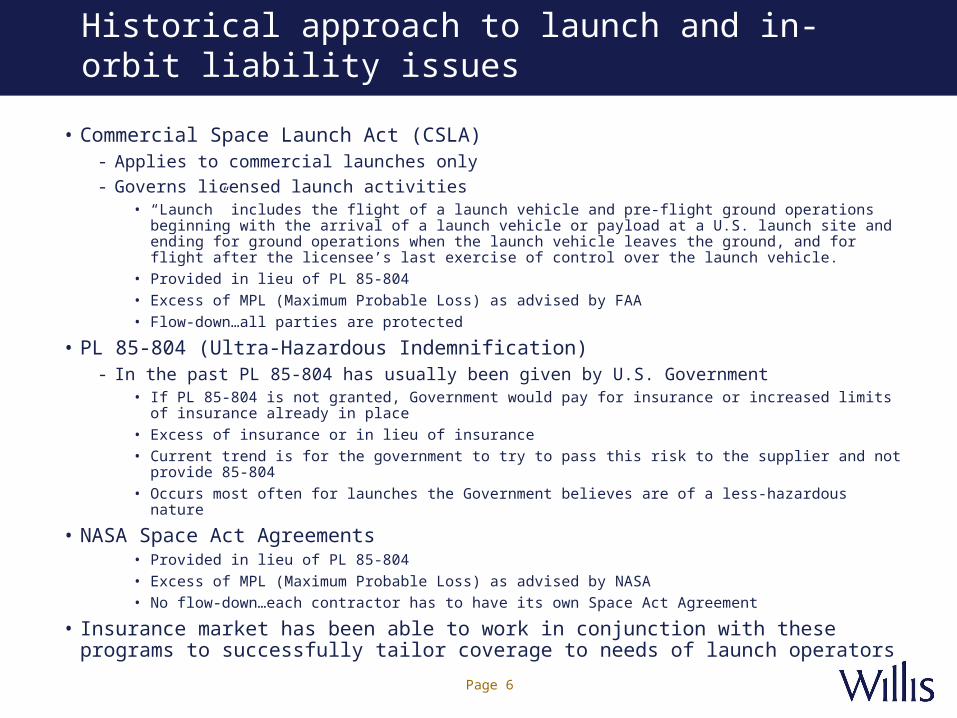

• Commercial Space Launch Act (CSLA)- Applies to commercial launches only

- Governs licensed launch activities• “Launch” includes the flight of a launch vehicle and pre-flight ground operations beginning with the arrival

of a launch vehicle or payload at a U.S. launch site and ending for ground operations when the launch vehicle leaves the ground, and for flight after the licensee’s last exercise of control over the launch vehicle.

• Provided in lieu of PL 85-804

• Excess of MPL (Maximum Probable Loss) as advised by FAA

• Flow-down…all parties are protected

• PL 85-804 (Ultra-Hazardous Indemnification) - In the past PL 85-804 has usually been given by U.S. Government

• If PL 85-804 is not granted, Government would pay for insurance or increased limits of insurance already in place

• Excess of insurance or in lieu of insurance

• Current trend is for the government to try to pass this risk to the supplier and not provide 85-804

• Occurs most often for launches the Government believes are of a less-hazardous nature

• NASA Space Act Agreements• Provided in lieu of PL 85-804

• Excess of MPL (Maximum Probable Loss) as advised by NASA

• No flow-down…each contractor has to have its own Space Act Agreement

• Insurance market has been able to work in conjunction with these programs to successfully tailor coverage to needs of launch operators

Historical approach to launch and in-orbit liability issues

Page 7

Manufacturers in-orbit liability coverage issues

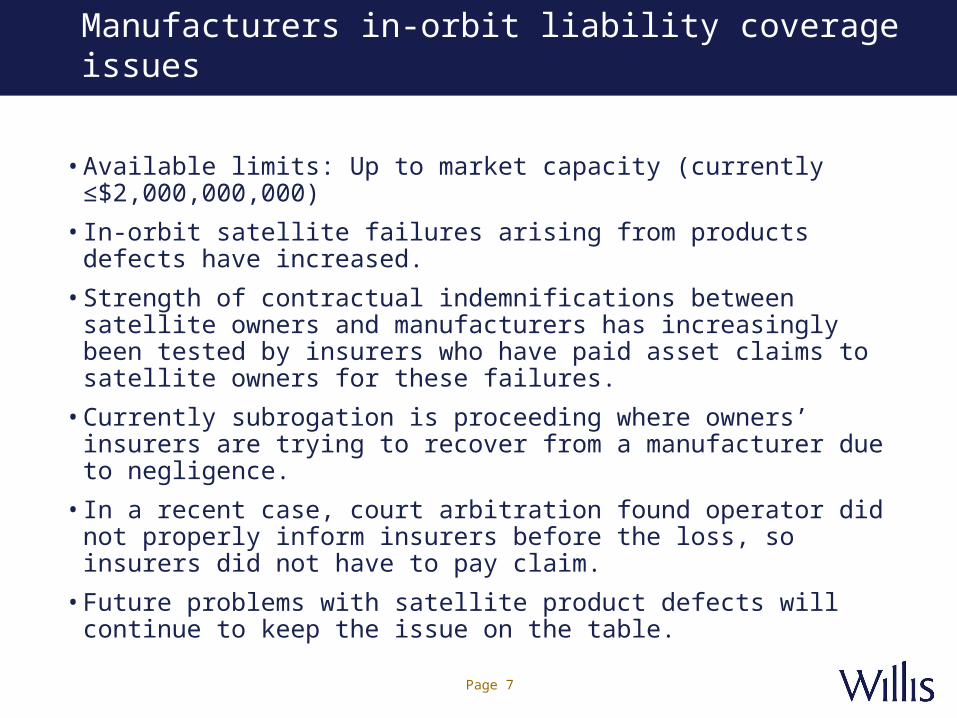

• Available limits: Up to market capacity (currently ≤$2,000,000,000)

• In-orbit satellite failures arising from products defects have increased.

• Strength of contractual indemnifications between satellite owners and manufacturers has increasingly been tested by insurers who have paid asset claims to satellite owners for these failures.

• Currently subrogation is proceeding where owners’ insurers are trying to recover from a manufacturer due to negligence.

• In a recent case, court arbitration found operator did not properly inform insurers before the loss, so insurers did not have to pay claim.

• Future problems with satellite product defects will continue to keep the issue on the table.

Page 8

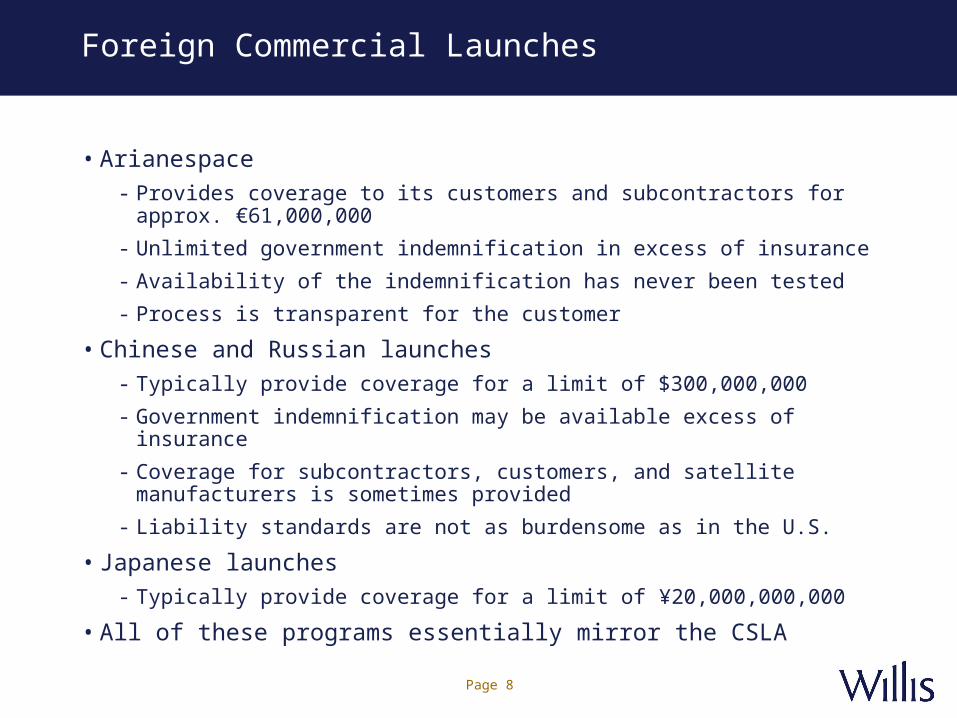

Foreign Commercial Launches

• Arianespace- Provides coverage to its customers and subcontractors for approx.

€61,000,000

- Unlimited government indemnification in excess of insurance

- Availability of the indemnification has never been tested

- Process is transparent for the customer

• Chinese and Russian launches- Typically provide coverage for a limit of $300,000,000

- Government indemnification may be available excess of insurance

- Coverage for subcontractors, customers, and satellite manufacturers is sometimes provided

- Liability standards are not as burdensome as in the U.S.

• Japanese launches- Typically provide coverage for a limit of ¥20,000,000,000

• All of these programs essentially mirror the CSLA

Page 9

Conclusion

• Sufficient aerospace liability insurance capacity exists today to provide coverage for government and commercial launches.

• Insurers will also be able to provide launch liability coverage for new emerging launch vehicles and space operations.

• Insurers look for CSLA indemnification, PL 85-804 designation, NASA Space Act protection, and other limitation of liability clauses.

• Due to the low annual market premium for space liability, a significant insured loss will be subsidized by premium from other lines of insurance business

• As a result of a loss, the market would likely experience:

- Significantly increased pricing

- Potential withdrawal of indemnification and other limitation of liability extensions from the Government.

- Reduction or withdrawal of coverage by insurers