Embed Size (px)

Citation preview

Law & Business

Editorial Board: Fred C. de Hosson, General Editor, Baker & McKenzie, Amsterdam Otmar Thömmes, Deloitte & Touche Tohmatsu, München Dr. Philip Baker OBE, QC, Barrister, Grays Inn Tax Chambers, Senior Visiting Fellow, Institute of Advanced Legal Studies, London University Prof. Dr. Ana Paula Dourado, University of Lisbon, PortugalProf. Dr. Pasquale Pistone, WU Vienna University of Economics and Business and University of Salerno

Editorial address: Fred C. de HossonClaude Debussylaan 541082 MD AmsterdamThe NetherlandsTel. (int.) +31 20 551 7555Fax. (int.) +31 20 551 7121Email: [email protected]

Book reviews: Pasquale Pistone via G. Melisurgo 1580133 Naples Italy Email: [email protected]

Published by: Kluwer Law InternationalPO Box 3162400 AH Alphen aan den RijnThe NetherlandsWebsite: www.kluwerlaw.com

Sold and distributed in North, Central and South America by: Aspen Publishers, Inc. 7201 McKinney Circle Frederick, MD 21704 United States of America Email: [email protected]

Only for IntertaxSold and distributed in Germany, Austria and Switzerland by:Wolters Kluwer Deutschland GmbHPO Box 235256513 NeuwiedGermanyTel: (int.) +49 2631 8010

Sold and distributed in Belgium and Luxembourg by:Établissement Émile BruylantRue de la Régence 67Brussels 1000BelgiumTel: (int.) + 32 2512 9845

Sold and distributed in all other countries by:Turpin Distribution Services Ltd.Stratton Business ParkPegasus Drive, BiggleswadeBedfordshire SG18 8TQUnited KingdomEmail: [email protected]

Intertax is published in 12 monthly issues

Print subscription prices 2011: EUR 973/USD 1298/GBP 715 (12 issues, incl. binder)Online subscription prices 2011: EUR 901/USD 1201/GBP 662 (covers two concurrent users)

Intertax is indexed/abstracted in IBZ-CD-ROM; IBZ-Online

For electronic and print prices, or prices for single issues, please contact our sales department for further information. Telephone: (int.) +31 (0)70 308 1562Email: [email protected]

For advertising rates contact:Marketing DepartmentKluwer Law InternationalPO Box 316 2400 AH Alphen aan den RijnThe NetherlandsTel: (int.) + 31 172 641548

Printed on acid-free paper.

ISSN: 0165-2826© 2011 Kluwer law International BV, The Netherlands

All rights reserved. No part of this journal may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without written permission from the publisher,

fiiceps deilppus lairetam yna fo noitpecxe eht htiw cally for the purpose of being entered and executed on a computer system, for exclusive use by the purchaser of the work.

Permission to use this content must be obtained from the copyright owner. Please apply to: Permissions Department, Wolters Kluwer Legal, 76 Ninth Avenue, 7th Floor, New York, NY 11011-5201, USA. Email: [email protected].

Printed and Bound by CPI Group (UK) Ltd, Croydon, CRO 4YY.

Articles can be submitted for peer review. In this procedure, articles are evaluated on their academic merit by two (anony-mous) highly esteemed tax law experts from the academic world. Only articles of outstanding academic quality will be published in the peer-reviewed section.

Contributing Editors:

EC Otmar Thömmes, Susan LyonsBelgium Dirk Deschrijver, Prof. André J.J. SpruytFrance Pierre-Yves BourtouraultGermany Manfred Günkel, Prof. Dr. Otto Jacobs, Mr. Michael WichmanHong Kong Michael A. OlesnickyHungary Mr. Daniel DeákIndia Gagan K. KwatraIreland Mary WalshItaly Dr. Guglielmo Maisto, Dr. Siegfried MayrJapan Mr. Daisuke Kotegawa, Prof. Hiroshi Kaneko, Masatami OtsukaNetherlands Prof. Sijbren Cnossen, Prof. Kees van RaadPortugal Prof. Gloria Teixeira, Prof. José Luis Saldanha SanchesSpain Juan José Bayona de Perogordo, Maria Teresa Soler RochSweden Maria HillingSwitzerland Daniël Lüthi, Dr. Robert DanonUK Malcolm GammieUSA Prof. William B. Barker

Charity CrossingBorders The FundamentalFreedoms’ In�uenceon Charity and DonorTaxation in Europeby Sabine Heidenbauer

HOW TO ORDER:Online: www.kluwerlaw.com

Or contact our Sales Departments at:For Europe and rest of the world: [email protected]

For USA and Latin America: [email protected] Canadian customers: [email protected]

For Asia and Australia: [email protected]

www.kluwerlaw.com 7.9.11

Throughout the European Union, national income tax systems support charitable activities by way ofpreferential treatment. However, a number of Member States operate relief regimes which appear to triggerthe question of compatibility with Union law with respect to the fundamental freedoms. In this �rst study toexamine charity and donor taxation regimes across a wide range of Member States, the author focuses oncompatibility with EU non-discrimination law. She examines twenty national regimes, both comparatively andfrom the perspective of overarching EU law.

The countries covered are Austria, Belgium, Bulgaria, Cyprus, Estonia, Finland, Germany, Hungary, Ireland, Italy,Latvia, Lithuania, Malta, The Netherlands, Poland, Portugal, Slovakia, Spain, Sweden, and the United Kingdom.

Even in a fully harmonized scheme of charity and donor taxation, the Member States must observe primaryUnion law and grant non-discriminatory treatment where a fact pattern falls within the ambit of thefundamental freedoms. In the course of de�ning this framework, the study addresses such issues as thefollowing:

• types of relief schemes maintained for charities and donors; • administrative requirements; • international aspects (both inbound and outbound); • privileged donations and capital gains treatment of in-kind donations; • eligible donees; • whether and to what extent charitable entities and donors can actually rely on the fundamental

freedoms; • speci�c applicability of each of the relevant fundamental freedoms; • the issue of comparability; • justi�cations for restrictive measures in Member State practice; and • the issue of proportionality.

September 2011, 312 pp., hardboundISBN: 9789041138132Price: EUR 130.00 / USD 176.00 / GBP 104.00 © 2011 Kluwer Law International

Peer-Reviewed Article526 Dividend Withholding Tax Planning Techniques: Part 2

Paulus Merks

Articles534 Pioneering Decision of the Constitutional Court of Hungary to Invoke

the Protection of Human Dignity in Tax MattersDaniel Deák

543 Tax Avoidance and Non-proportional DemergersFilippo Alessandro Cimino

547 New Tax Rules on Cross-Border Mergers and Demergers in Norway and TheirCompatibility with the EEA AgreementAnna B. Scapa Passalacqua

557 Non-exhausted Losses and the Merger Directive: What It Fails to SayJeanette Calleja Borg

564 Applicability of Double Taxation Avoidance Agreements to FiscallyTransparent Entities: An Indian PerspectiveAnish Agarwal & Tarumoy Chaudhuri

570 Legal Valuation in Chinese VAT and Business TaxXiaoqiangYang

Volume 39 November 2011 11

CONTENTS

Dividend Withholding Tax PlanningTechniques: Part 2

Paulus Merks*

Although there is a confounding variety of cross-border dividend withholding tax planning techniques available to the modern corporate taxpayer,this study has sought to identify, analyse and categorize these techniques in abstracto and, unless stated otherwise, without linking these techniquesto particular countries.

Whereas Part 1 of this two-part study focused on the so-called formal dividend withholding tax planning techniques, the underlying Part 2identifies, analyses and categorizes the so-called substantive dividend withholding tax planning techniques. In addition, this Part 2 provides aframework whereby the various dividend withholding tax planning techniques can be categorized in a consistent and universal manner.

1. INTRODUCTION

Part 1 of this two-part study discusses formal dividendwithholding tax planning techniques, defined astechniques that retain the substance of the activityhowever insert steps or transactions for the purpose ofreducing the amount of dividend withholding tax due. Aswas discussed and analysed in Part 1, formal dividendwithholding tax planning techniques typically includenothing more than one or more paper transactions. Theunderlying Part 2 discusses, analyses, and categorizessubstantive dividend withholding tax planning techniques.Different from formal tax planning techniques,substantive tax planning techniques do alter the pattern ofthe economic activity.1 For example, if the dividendwithholding tax rate is effectively high in a certainjurisdiction, a company may either leave that jurisdictionin response to the high tax rate and move its operations toan effectively low dividend withholding tax jurisdiction(e.g., Cyprus, Ireland, Malta, the United Kingdom) or,alternatively, it may not start operations in the highdividend tax jurisdiction in the first place.

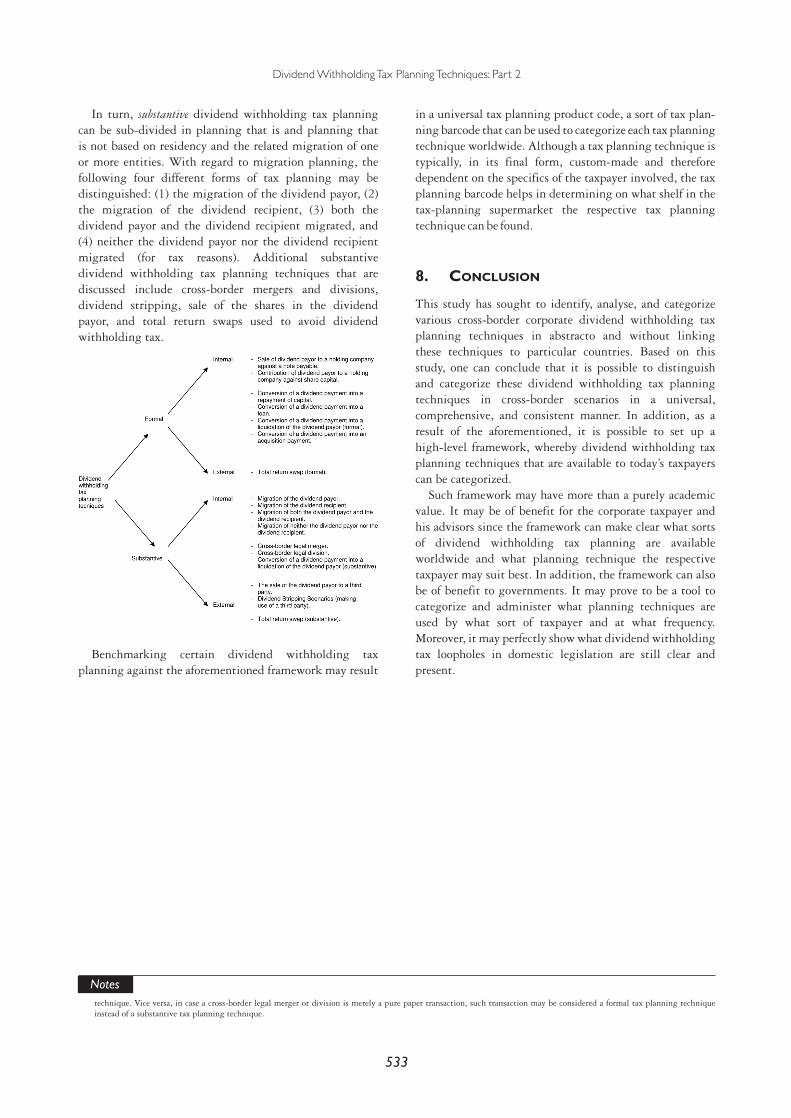

In this regard, substantive dividend withholding taxplanning will be sub-divided in planning that is and is notbased on residency and the related migration of one ormore entities. With regard to migration planning, thefollowing four different forms of tax planning will be

discussed: (1) the migration of the dividend payor, (2) themigration of the dividend recipient, (3) both the dividendpayor and the dividend recipient migrated, and (4) neitherthe dividend payor nor the dividend recipient migrated (fortax reasons).2 Additional substantive dividend withholdingtax planning techniques (that are not based on residency)that are discussed include cross-border mergers and divi-sions, dividend stripping, the sale of the shares in thedividend payor, and total return swaps used to avoiddividend withholding tax.3 In addition, Part 2 provides aframework whereby various dividend withholding taxplanning techniques, both formal and substantive, maybe categorized in a consistent and universal manner.

2. MIGRATION PLANNING

The categorization of substantive dividend withholdingtax planning techniques makes clear that substantivedividend withholding tax planning may often entail themigration of one or more companies.4 For this reason, it isrelevant to discuss in more detail the concepts anddefinition of corporate residency for tax purposes.Typically corporate residency is based on the concepts of‘the place of effective management’, which is used incontinental Europe and as a ‘tiebreaker’ in theOrganization for Economic Cooperation and Development

Notes* Partner, DLA Piper, New York/Amsterdam.1 See Dirk A. Albregtse, Fiscaal-economische aspecten van internationale belastingvermijding (Deventer: Kluwer, 1983).2 In the same line, for corporate income tax purposes, see Paulus Merks, ‘Categorizing Corporate Cross-Border Tax Planning Techniques’, Tax Notes International 10 (October

2006): 195–11.3 See the recent US IRS ‘Industry Directive on Total Return Swaps (“TRSs”) Used to Avoid Dividend Withholding Tax’, No. LMSB-4-1209-044, 14 Jan. 2010.4 See, for example, the Dutch dividend withholding tax planning cases Hoge Raad, 11 Oct. 2000, BNB 2001/121, and the final decision in this case, Hoge Raad, 16 Apr. 2004,

BNB 2004/295. See O.C.R. Marres & P.J. Wattel, Dividendbelasting (FED Fiscale Studieserie, no. 26) (Deventer: Kluwer 2006), paras 3.5.2 and 3.5.3, 192 et seq.

PEER-REVIEWED ARTICLE

526INTERTAX,Volume 39, Issue 11© 2011 Kluwer Law International BV,The Netherlands

(OECD) Model Tax Convention 2010 and ‘the place ofcentral management and control’, which is used incommon law countries (including Australia, Canada,Ireland, and the UK).5

The OECD Model Tax Convention 2010 contains someguidance as to the meaning of ‘place of effectivemanagement’. Article 4, paragraph 3, of the OECD ModelTax Convention 2010 states that a non-individual that isresident of both contracting states ‘shall be deemed to be aresident only of the contracting state in which its place ofeffective management is situated’. The meaning of theterm ‘place of effective management’ is not defined inArticle 4 of the OECD Model Tax Convention 2010.However, paragraph 24 in the Commentary to Article 4,which was included in the 2000 Update to the Model,offers some guidance on the meaning of this term:

The place of effective management is the place wherekey management and commercial decisions that arenecessary for the conduct of the enterprise’s business arein substance made. The place of effective managementwill ordinarily be where the most senior person or group ofpersons (for example a board of directors) makes its deci-sions, the place where the actions to be taken by theenterprise as a whole are determined; however, no defini-tive rule can be given and all relevant facts andcircumstances must be examined to determine the placeof effective management. An enterprise may have morethan one place of management, but it can have only oneplace of effective management at any one time.

Finding out the content of the term ‘place of effectivemanagement’ is a question of law even though it should bebased on an analysis of all the relevant facts. A definitionwould be helpful in this regard; the term ‘place of effectivemanagement’ is not defined in any of the articles of the2010 OECD Model Tax Convention nor is any furtherguidance given on its meaning. In the absence of anyspecific definition of ‘place of effective management’,many commentators have been influenced by conceptsused in domestic tax law residence rules, such as ‘centralmanagement and control’ and ‘place of management’,6

when considering the meaning of the term ‘place ofeffective management’.7

While the expression ‘central management and control’is often used in common law jurisdictions, the expressionis typically not defined by those countries. However, thereare a number of court cases that provide guidance on howthe place of central management and control should bedetermined.8 These decisions state that while determininga place of central management and control is a question offact, it ordinarily coincides with the place where thedirectors of the company exercise their power andauthority, which will typically be where they meet.9

As can be seen from the definitions and examples above,there are many similarities between the concepts of ‘placeof effective management’ and place of ‘centralmanagement and control’. Both notions rely on separatingthe place of administrative or day-to-day managementfrom the place of key decision making, usually by theboard of directors, to determine where a company isresident.10 Furthermore, both ideas are based on questionsof fact, and similar issues such as place of incorporation,place of residence of directors, and place where businessoperations are conducted are considered in both cases. Forsimplicity’s sake, the scenarios discussed below are basedon the ‘place of effective management’ concept only.

2.1. Migration of the Dividend Payor

A dividend payor resident in a country that leviesdividend withholding tax may be tempted to avoid beingsubject to this tax in its source country by moving itsresidence abroad altogether, for example, winding up of allattachment to the territory of a certain tax jurisdiction.11

Obviously, such shift of residence will be typicallyinitiated by the shareholder(s) of the dividend payer sinceit is the shareholder that is liable to the dividendwithholding tax. As most jurisdictions do not levy an‘exit’ dividend withholding tax at the moment of acorporation migrating from the original country of source,this planning may prove to be tax efficient from ataxpayer’s perspective.12

Notes5 See Klaus Vogel, ‘Double Taxation Conventions: A Commentary to the OECD-, UN- and US Model Conventions for the Avoidance of Double Taxation of Income and Capital

with Particular Reference to German Treaty Practice’, 144 et seq.6 See Klaus Vogel, Double Taxation Conventions, 3rd edn (The Hague: Kluwer Law International, 1997), 262.7 See also ‘The Impact of the Communications Revolution on the Application of “Place of Effective Management” as a Tie Breaker Rule’, a discussions paper from the OECD

technical advisory group on monitoring the application of existing treaty norms for the taxation of business profits, OECD, February 2001.8 See, for example, for Canada, Birmount Holdings Ltd v. R [1978] CTC 358; Tara Exploration & Development Co Ltd v. MNR [1970] CTC 557; and Capitol Life Insurance Co v. R

[1984] CTC 141 cases.9 A leading case establishing this is the UK case De Beers Consolidated Mines Ltd. v. Howe (Surveyor of Taxes), House of Lords, 30 Jul. 1906, AC 455. In this case, a company

registered in South Africa had its head office and its activities in South Africa. In addition, it held all its general meetings of shareholders in South Africa. Its directors heldmeetings both in South Africa and the United Kingdom, but the directors’ meetings held in the United Kingdom were found to be those where real control of the companywas exercised. Accordingly, the company was found to be UK resident.

10 See Guglielmo Maisto (ed.), ‘Residence of Companies under Tax Treaties and EC Law’, IBFD, EC and International Tax Law Series, vol. 5, 2009.11 See the OECD Report, ‘International Tax Avoidance and Evasion, Four related studies’ (Paris, 1987), 24.12 For example, in the Netherlands, the Under-Minister of Finance has repeatedly expressed that he considers the introduction of such an exit charge for dividend withholding

tax purposes not desirable and that he does not intend to propose legislation to that effect. Therefore, it can be considered a deliberate choice of the legislature not to subject a

Dividend WithholdingTax PlanningTechniques: Part 2

527

For example, if the effective management of a company(company A) is moved from the Netherlands to a countrywith which the Netherlands has in effect a tax treatymodelled after the OECD Model Treaty 2010 for purposesof application of the tax treaty, company A will cease to bea resident of the Netherlands and be deemed to be aresident of the other contracting state. If company Asubsequently distributes a dividend that is not paid to aresident of the Netherlands, Article 21 assigns the right totax the dividend solely to the other contracting state.13

Consequently, the levy of Dutch dividend withholding taxis prevented.14 Moreover, if the country to which thecompany relocates does not levy a dividend withholdingtax, possibly all dividend withholding tax with regard tofuture dividends is avoided.

In this respect, a Dutch Supreme Court case of the early1990s (BNB 1992/379)15 is illustrative. The SupremeCourt held that no Dutch dividend withholding tax wasdue on a dividend distribution by a company incorporatedunder Dutch law but resident in Ireland to its USshareholder. In that case, the dividend was derived entirelyout of profits accrued in Ireland. Possibly, Dutch Revenuecould argue that the Supreme Court’s decision would nothold for company A’s case, for example, because companyA’s earnings accrued while company A was a Dutchresident. The Supreme Court case seems to indicate that itis irrelevant whether or not the dividend was paid out ofprofits accrued while company A was a Dutch resident.

Although most countries do not have an exit tax ondividends, the migration of an entity may have corporateincome tax implications since most countries do have anexit tax for corporate income tax purposes. In this regard, theEuropean Commission has recently requested Belgium,Denmark, and the Netherlands to change tax rules thatimpose an immediate exit tax when companies transfer theirseat or assets to another Member State.16,17 The EuropeanCommission considers these provisions to be incompatiblewith the freedom of establishment provided for in Article49 of the Treaty on the Functioning of the European Unionand has decided to take the cases to the ECJ.18,19

2.2. Migration of the Dividend Recipient

Similar to the tax planning mentioned under section 2.1,also the taxpayer that receives dividend income andtherefore may be liable to dividend withholding tax maybe tempted to avoid being subject to this tax in its homecountry by moving its residence abroad altogether. Forexample, the effective management of a parent company(company P) is moved to a country with which the sourcecountry has in effect a tax treaty that prevents thewithholding tax on intercompany dividend payments(e.g., under Article 10, paragraph 2 or paragraph 3 of thetax treaty).20 Consequently, company P will be deemed tobe a resident of the other contracting state. If Psubsequently receives a dividend payment, Article 10assigns the right to tax the dividend solely to the countryof residence of P. Consequently, the levy of dividendwithholding tax by the source country is prevented. Alsoin this scenario, possibly all dividend withholding taxwith regard to future dividends is avoided.

Another example is the scenario whereby the parentcompany receives a loan from a group company resident inthe parents’ company (original) jurisdiction. When thisparent company is subsequently moved to the sourcecountry, the loan will become a cross-border loan. Therepayment of a loan is typically tax free. In summary, thedifferent tax treatments between a dividend payment anda loan repayment may form an incentive for a taxpayer to(step 1) increase debt financing, (step 2) migrate thedividend recipient to the source country, and (step 3) repaythe loan.

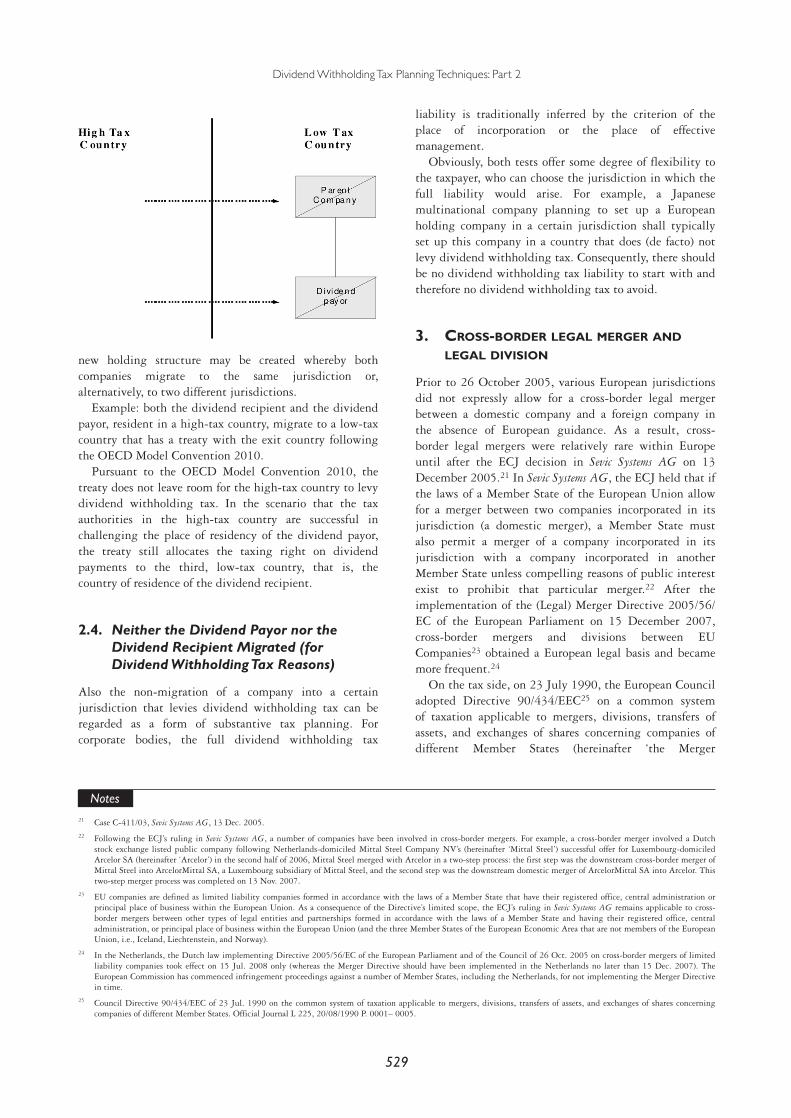

2.3. Migration of Both the Dividend Payorand the Dividend Recipient

A combination of the tax planning mentioned under Aand B is the scenario whereby both the dividend payor andthe foreign dividend recipient migrated for dividendwithholding tax reasons. As a consequence, a complete

NotesDutch company’s profits reserves to dividend taxation upon emigration to another country. See White Paper on a balanced treatment of international tax issues of 16 Jul.1993, No. 93/120, and the Parliamentary discussions involving the new 2001 Income Tax Act. Invoeringswet Wet inkomstenbelasting 2001, 26 728, nota naar aanleiding van hetnader verslag, Artikelgewijze toelichting, Art. VI.

13 Ibid., Stef van Weeghel, The Improper Use of Tax Treaties (Deventer/Boston: Kluwer, 1998), 139.14 Ibid., E.C.C.M. Kemmeren, ‘De Hoge Raad heeft de dividendbelasting afgeschaft’, Weekblad fiscaal recht (1995): 355. Of a different opinion is Brandsma, who feels that a

Dutch abuse-of-law provision may apply in case the transfer of a cash box entity has no real purpose(s) except tax purpose(s). R.P.C.W. M. Brandsma, ‘Thuisbankieren enkasgeld-vennootschappen’, Weekblad fiscaal recht (1991): 1566.

15 See Hoge Raad, 2 Sep. 1992, BNB 1992/379.16 The incriminated provisions are the following: in Belgium, Arts 208, 209, and 210, para. 1, point 4 of the Income tax code (CIR92); in Denmark, s. 7A of the Danish

Corporate Tax Act; and in the Netherlands, Arts 3.60 and 3.61 of the Income tax law 2001 and Art. 15c and 15d of the Corporate tax law 1969.17 The European Commission’s case reference numbers are 2008/4250 (BE), 2008/2157 (DK) and 2008/2207 (NL), IP 10/299, Brussels, 18 Mar. 2010.18 A similar case against Sweden has been closed, since Sweden had complied with the Commission’s request. See IP/08/1362, Brussels, 18 Sep. 2008.19 IP/10/1565, Brussels, 24 Nov. 2010. The Commission had already referred Spain and Portugal to the Court of Justice for similar exit tax rules. See IP/09/1460, Brussels, 8

Oct. 2009. In the same line, the European Commission has formally requested Ireland to amend provisions that impose an exit tax on companies when they cease to be taxresidents in Ireland. See IP/11/78, Brussels, 27 Jan. 2011.

20 Examples include the Netherlands’ treaties concluded with Albania, Armenia, Belarus, Denmark, Egypt, Iceland, Ireland, Jordan, Kazakhstan, Macedonia, Malaysia, Norway,Singapore, South Africa, Sweden, Switzerland, the United States, and Venezuela.

Intertax

528

new holding structure may be created whereby bothcompanies migrate to the same jurisdiction or,alternatively, to two different jurisdictions.

Example: both the dividend recipient and the dividendpayor, resident in a high-tax country, migrate to a low-taxcountry that has a treaty with the exit country followingthe OECD Model Convention 2010.

Pursuant to the OECD Model Convention 2010, thetreaty does not leave room for the high-tax country to levydividend withholding tax. In the scenario that the taxauthorities in the high-tax country are successful inchallenging the place of residency of the dividend payor,the treaty still allocates the taxing right on dividendpayments to the third, low-tax country, that is, thecountry of residence of the dividend recipient.

2.4. Neither the Dividend Payor nor theDividend Recipient Migrated (forDividend WithholdingTax Reasons)

Also the non-migration of a company into a certainjurisdiction that levies dividend withholding tax can beregarded as a form of substantive tax planning. Forcorporate bodies, the full dividend withholding tax

liability is traditionally inferred by the criterion of theplace of incorporation or the place of effectivemanagement.

Obviously, both tests offer some degree of flexibility tothe taxpayer, who can choose the jurisdiction in which thefull liability would arise. For example, a Japanesemultinational company planning to set up a Europeanholding company in a certain jurisdiction shall typicallyset up this company in a country that does (de facto) notlevy dividend withholding tax. Consequently, there shouldbe no dividend withholding tax liability to start with andtherefore no dividend withholding tax to avoid.

3. CROSS-BORDER LEGAL MERGER AND

LEGAL DIVISION

Prior to 26 October 2005, various European jurisdictionsdid not expressly allow for a cross-border legal mergerbetween a domestic company and a foreign company inthe absence of European guidance. As a result, cross-border legal mergers were relatively rare within Europeuntil after the ECJ decision in Sevic Systems AG on 13December 2005.21 In Sevic Systems AG, the ECJ held that ifthe laws of a Member State of the European Union allowfor a merger between two companies incorporated in itsjurisdiction (a domestic merger), a Member State mustalso permit a merger of a company incorporated in itsjurisdiction with a company incorporated in anotherMember State unless compelling reasons of public interestexist to prohibit that particular merger.22 After theimplementation of the (Legal) Merger Directive 2005/56/EC of the European Parliament on 15 December 2007,cross-border mergers and divisions between EUCompanies23 obtained a European legal basis and becamemore frequent.24

On the tax side, on 23 July 1990, the European Counciladopted Directive 90/434/EEC25 on a common systemof taxation applicable to mergers, divisions, transfers ofassets, and exchanges of shares concerning companies ofdifferent Member States (hereinafter ‘the Merger

Notes21 Case C-411/03, Sevic Systems AG, 13 Dec. 2005.22 Following the ECJ’s ruling in Sevic Systems AG, a number of companies have been involved in cross-border mergers. For example, a cross-border merger involved a Dutch

stock exchange listed public company following Netherlands-domiciled Mittal Steel Company NV’s (hereinafter ‘Mittal Steel’) successful offer for Luxembourg-domiciledArcelor SA (hereinafter ‘Arcelor’) in the second half of 2006, Mittal Steel merged with Arcelor in a two-step process: the first step was the downstream cross-border merger ofMittal Steel into ArcelorMittal SA, a Luxembourg subsidiary of Mittal Steel, and the second step was the downstream domestic merger of ArcelorMittal SA into Arcelor. Thistwo-step merger process was completed on 13 Nov. 2007.

23 EU companies are defined as limited liability companies formed in accordance with the laws of a Member State that have their registered office, central administration orprincipal place of business within the European Union. As a consequence of the Directive’s limited scope, the ECJ’s ruling in Sevic Systems AG remains applicable to cross-border mergers between other types of legal entities and partnerships formed in accordance with the laws of a Member State and having their registered office, centraladministration, or principal place of business within the European Union (and the three Member States of the European Economic Area that are not members of the EuropeanUnion, i.e., Iceland, Liechtenstein, and Norway).

24 In the Netherlands, the Dutch law implementing Directive 2005/56/EC of the European Parliament and of the Council of 26 Oct. 2005 on cross-border mergers of limitedliability companies took effect on 15 Jul. 2008 only (whereas the Merger Directive should have been implemented in the Netherlands no later than 15 Dec. 2007). TheEuropean Commission has commenced infringement proceedings against a number of Member States, including the Netherlands, for not implementing the Merger Directivein time.

25 Council Directive 90/434/EEC of 23 Jul. 1990 on the common system of taxation applicable to mergers, divisions, transfers of assets, and exchanges of shares concerningcompanies of different Member States. Official Journal L 225, 20/08/1990 P. 0001– 0005.

Dividend WithholdingTax PlanningTechniques: Part 2

529

Directive’).26 The objective of the Merger Directive is toremove fiscal obstacles to cross-border reorganizationsinvolving companies situated in two or more MemberStates.27 The Merger Directive provides for deferral of thecorporate income tax that could be charged on thedifference between the real value of such assets andliabilities and their value for tax purposes. The deferral isgranted provided the receiving company continues withits tax values and effectively connects them to its ownpermanent establishment in the Member State of thetransferring company.

Pursuant to the implementation of the MergerDirective, both legal mergers and share-for-share mergersmay take place tax free. Under a legal merger, it may bepossible for a company to be dissolved without going intoliquidation and to transfer all its assets and liabilities toanother existing company. The company will legally‘disappear’, whereby the receiving company is the legalsuccessor of the disappearing company.28 The MergerDirective provides for tax deferral of the corporate incometax and at the level of personal income taxes that could becharged on the income or capital gains derived by theshareholders of the dissolving company; in addition, itprovides for a deferral of the corporate income tax at thelevel of the dissolving entity.

Moreover, in case the dissolving company has profitreserves that would typically result in a dividendwithholding tax claim in the original source state, thisclaim may end in case the receiving company, the legalsuccessor of the disappearing company, is resident of aEuropean jurisdiction that does not – de jure or de facto –levy dividend withholding tax.29

There are three subtypes of this dividend withholdingtax planning:

– an existing company that is resident of a jurisdictionthat levies dividend withholding tax merges intoanother existing company that is resident of ajurisdiction that levies (de facto or de jure) no dividendwithholding tax;

– two or more existing companies that are resident ofjurisdictions that levy dividend withholding tax mergeinto a newly formed company in a jurisdiction that

levies (de facto or de jure) no dividend withholding tax;and

– a wholly owned subsidiary, resident of a jurisdictionthat levies dividend withholding tax, collapses into itsparent company (quasi-liquidation) that is resident ofjurisdiction that levies (de facto or de jure) no dividendwithholding tax.

In the same line, a legal division takes place when anexisting company transfers all of its assets and liabilities totwo or more newly incorporated or existing companies,which become its legal successors. The transferringcompany thereupon ceases to exist and is dissolvedwithout going into liquidation. Also in these transactions,the Merger Directive provides for tax deferral of the taxesthat could be charged on the income or capital gainsderived by the shareholders of the transferring or theacquired company from the exchange of such shares forshares in the receiving or the acquiring company.

In the scenario whereby the dissolving company has adividend withholding tax claim, this claim may end in thecase whereby its legal successors are resident companies injurisdictions that do not levy dividend withholding tax. Inall these transactions, the Merger Directive provides forplanning opportunities with regard to dividendwithholding tax. Although the aforementioned techniquesrelate in particular to cross-border EU scenarios, the sameplanning techniques may exist between entities in non-EUjurisdictions that allow for cross-border legal mergers ordivisions.30

4. THE SALE OF THE DIVIDEND PAYOR TO A

THIRD PARTY

The tax consequences of the sale of shares are generallydifferent from those of the receipt of dividends, both in apurely domestic context and in an international level.31 Adividend is generally taxable as ordinary income, subjectto intra-group exemptions and – in countries where one oranother form of imputation of tax paid by the payorcompany exists – available tax credits.32 A capital gainrealized in respect of the sale of shares is, in manycountries, either exempt from tax or subject to a lower rate

Notes26 On 17 Oct. 2003, the Commission adopted a proposal (COM(2003) 613) amending Council Directive 90/434/EEC on a common system of taxation applicable to mergers,

divisions, transfer of assets, and exchanges of shares concerning companies of different Member States, which was subsequently adopted after negotiations by Council on 17Feb. 2005, as Directive 2005/19/EC.

27 The Merger Directive includes a list of the legal forms to which it applies. The companies must be subject to corporate tax, without being exempted, and resident for taxpurposes in a Member State.

28 See B.J.M. Terra & P.J. Wattel, European Tax Law (Deventer: Kluwer, 2008), 542.29 To the extent the hidden reserve is attached to an asset at a permanent establishment left in the source country, tax on this asset may still occur on realization or exit.30 See, for example, the recent ruling of the Indian Authority for Advance Rulings in the case of an Indian capital gain tax-free amalgamation of Star Television Entertainment

Ltd., an Indian company, with other group entities and shareholders incorporated under the laws of the British Virgin Islands and the United Arab Emirates. 2010-TIOL-01-ARA-IT.

31 See van Weeghel, 141.32 See also Freek Snel, ‘Van Moeders en Dochters – Systemen ter voorkoming van cumulatie van vennootschapstax in deelnemingssituaties’, Sdu 2005.

Intertax

530

than ordinary income. In addition, the tax treatment mayalso be dependent on whether the shares are owned in thecourse of a trade or business.33

Under tax treaties that follow the OECD ModelConvention 2010, a capital gain can, pursuant to Article13, paragraph 4, be taxed only in the country of residenceof the shareholder. Dividends, however, pursuant toArticle 10, paragraphs 1 and 2 of the OECD ModelConvention 2010, can be taxed both in the source stateand in the state of residence of the shareholder. Whateverthe reason for the difference between the taxation ofcapital gains and dividends and the assignment of theright to tax them, taxpayers are using these differences totheir advantage.34

Consequently, another form of substantive dividendwithholding tax planning is the planning whereby theshares in the dividend payor are sold, either within thecorporate group or to a third party.35 As a result, adividend – typically free of dividend withholding tax –may be paid to the acquirer of the shares. In a case, theselling shareholder may be able to avoid dividendwithholding tax altogether simply because the sellingshareholder is not the recipient of a dividend. Whether ornot the sale of the shares will result in the completeavoidance of tax on the dividends depends, inter alia, onthe circumstances relevant to the other party of thetransaction: the acquirer of the shares in the dividendpayor.

5. DIVIDEND STRIPPING

Dividend stripping entails a variety of techniques aimed atreducing or eliminating the burden of dividendwithholding tax. In a dividend stripping scenario, theshareholder may transfer both his economic and legalinterest in the shares and will therefore not benefit onfuture dividends or growth. However, this transfer istypically for a short period of time only, and theshareholder generally buys back his original shares.

In its simplest form, dividend stripping can bedescribed in the following three steps:

(1) the sale of the shares in a company with undistributedprofits;

(2) the dividend distribution to the recent acquirer, and

(3) the re-sale of the shares to the original shareholder.

Different from the dividend withholding tax planningscenarios earlier discussed and essential to dividendstripping is the fact that the shares are ultimately soldback to the original shareholder.36,37

A specific dividend stripping technique is securitieslending. Securities lending is the temporary transfer ofsecurities on a collateralized basis from one party (thelender) to another (the borrower) for a fee.38 In thisscenario, the borrower can typically receive dividends onthe shares borrowed against a lower rate than the originallender. Or, alternatively, by borrowing additional shares,the borrower obtains a lower dividend withholding taxrate on the shares it already owns.39 Typically, theborrower must return the securities to the lender after anagreed period of time or on demand.

Most securities lending is collateralized using othersecurities, cash, or a letter of credit. When a security isloaned, the ownership title transfers from the lender to theborrower. This transfer gives the borrower theshareholder’s rights, such as voting rights and rights todividends or interest payments. However, these coupon ordividend payments are normally transferred back to thelender through equivalent payments. The borrower is alsoable to loan or sell the securities.40

6. INTERNAL AND EXTERNAL DIVIDEND

WITHHOLDING TAX PLANNING

Another distinction that one can make in dividendwithholding tax planning techniques is the distinctionbetween tax planning between associated entities (‘internaltax planning’) and tax planning involving a third party

Notes33 See the Commentary on Art. 13 of the OECD Model Convention (2010).34 It can be agreed with Van Weeghel that it would not be illogical to give the source state a limited right to tax capital gains where it has a limited right to tax the dividends.

See van Weeghel.35 The third party acquirer is typically a so-called trust company or a banking institution.36 Or, alternatively, the original shareholder buys back similar shares from another third party.37 Since the shares are ultimately sold back to the original shareholder, this planning technique may be considered more aggressive than other techniques whereby shares are not

sold back. For this reason, specific anti-dividend stripping rules have been implemented in various jurisdictions to counter this specific dividend withholding tax planningtechnique.

38 Third-party security lenders are primarily asset managers, custodian banks, or other third-party lenders. Examples of substantial US-based securities lenders include Bank ofNew York, Charles Schwab Corporation, Citibank, and JP Morgan Chase.

39 For example, because the borrower now obtains a certain percentage that results in a better tax treaty threshold.40 As explained, one of the reasons for transferring ownership by securities lending is tax arbitrage. Other reasons include ways to (1) cover a short position, (2) finance – when

the lender receives cash in exchange for lending the securities; and (3) increase the voting power in a corporation.

Dividend WithholdingTax PlanningTechniques: Part 2

531

(‘external tax planning’).41 An example of an internaldividend withholding tax planning technique may includean intra-group transfer of the dividend payor or,alternatively, the migration of the dividend payor to adividend withholding tax-free jurisdiction.

In turn, external dividend withholding tax planningtechniques include the techniques whereby the underlyingshares in the dividend payor are transferred to a thirdparty. This technique can be divided into planningwhereby the underlying shares or dividend coupon rightswill be transferred to a third party indefinitely andplanning whereby the underlying shares or dividendcoupon rights will be transferred for a certain period oftime and eventually transferred back to the originalshareholder, typically after the distribution of one or moredividend payments.

The US Internal Revenue Service (IRS) discusses varioussorts of dividend withholding tax planning techniques –whereby the underlying shares are transferred for a certainperiod of time only – in its industry directive on totalreturn swaps used to avoid US dividend withholdingtax.42 Illustrative is the so-called cross-in/cross-outscenario whereby a foreign person owns equity securities(hereinafter ‘shares’) issued by a publicly traded UScorporation that pays regular or extraordinary dividendswith respect to these shares.43

In this scenario, the foreign person sells its US shares toa US financial institution. Simultaneously, the foreignperson enters into a total return swap with the same USfinancial institution as the swap counterparty. The totalreturn swap references the same shares sold to the USfinancial institution by the foreign person, and thenotional amount of the total return swap equals the fairmarket value of the US shares sold to the financialinstitution.44

The simultaneous sale of US shares and acquisition of anequity equivalent position pursuant to a total return swapis referred to as a ‘cross-in’. The foreign person holds the

equity equivalent position in the swap over the record dateor dates.45 After the record date or dates, the foreignperson terminates the swap and, at the same time,repurchases the US shares from the US financialinstitution (also referred to as a ‘cross-out’).46 Althoughthis technique is specifically outlined in a US context,similar techniques can be found in various otherjurisdictions that levy dividend withholding tax.

7. THE DIVIDEND WITHHOLDING TAX

PLANNING FRAMEWORK

Based on the dividend withholding tax planningtechniques discussed and analysed in both Part 1 and Part2 of this study, it is possible to set up a basiccomprehensive framework categorizing the variousdividend withholding tax planning techniques that areavailable to taxpayers worldwide.

The foundation of this framework may consist of thedistinction between substantive and formal dividendwithholding tax planning. Formal dividend withholdingtax planning can in turn be sub-divided in two mainforms of dividend withholding tax planning, bothentailing the use of a holding company: (1) the sale of thedividend payor to a holding company against a notepayable and (2) the contribution of the dividend payor to aholding company against share capital.

The second mentioned form of formal dividend with-holding tax planning techniques whereby no special hold-ing company is used can in turn be sub-divided in thefollowing four subgroups: (1) the conversion of the dividendpayment in a repayment of capital to the parent company,(2) the conversion of the dividend payment into a loan tothe parent company, (3) the conversion of the dividendpayment into an acquisition price, and (4) the conversion ofthe dividend payment into a liquidation of the companythat would otherwise pay out the dividend.47

Notes41 A similar distinction can be made for corporate income tax planning purposes. For example, the distinction between a tax-efficient sale and lease back transaction within a

corporate group and a tax-efficient sale and lease back transaction with a third-party bank.42 See ‘Industry Directive on Total Return Swaps (“TRSs”) Used to Avoid Dividend Withholding Tax’, No. LMSB- 4-1209-044, 14 Jan. 2010.43 In this regard, the industry directive states that in the event that the field examines a transaction in which the share is an equity interest in a publicly traded partnership as

defined in s. 7704(c) of the Internal Revenue Code, the field should seek the assistance of counsel.44 Pursuant to the terms of the total return swap, the foreign person is required to make payments to the US financial institution based on an interest component (e.g., a

LIBOR-based payment) and any depreciation with respect to the notional investment in the US shares. The US financial institution is required to make payments to theforeign person in an amount equal to any appreciation with respect to the notional investment in the US shares and any dividend paid with respect to the US shares (a so-called synthetic issuer position). Payment obligations with respect to the equity equivalent and synthetic issuer positions may be netted against each other.

45 The industry directive states in this regard that the record date is the ‘date on which a firm’s books are closed during the process of identifying the owners of a certain class ofsecurities for purposes of transmitting dividends’. The directive continues: ‘For example, only the common stockholders who are listed on the record date will receive thedividends that are to be mailed on the payment date’ and makes reference to David L. Scott, Wall Street Words, 3rd edn (2003).

46 The fair market value of the US shares on the cross-in and the repurchase price on the cross-out are likely to be determined in such a manner that ensures the foreign personhas no pricing risk on the cross-in and the cross-out but retains the overall ownership risk in the US shares. To determine the notional principal amount of the total returnswap and the appreciation or depreciation with respect to the US shares referenced by the total return swaps, the documents may reference the same pricing mechanism (e.g.,market on close) or may require the use of a single interdealer broker or the circumstances may show that the parties are likely to be in the market together upon a cross,particularly where the volume is typically low and the number of market participants is limited based upon a pattern of dealing or other relevant facts. See the recent US IRS‘Industry Directive on Total Return Swaps (“TRSs”) Used to Avoid Dividend Withholding Tax’.

47 In case a liquidation of the company for dividend withholding tax planning purposes is more than a pure paper transaction, for example, because the liquidated entity ownsdifferent sorts of assets (other than cash or a note receivable), this planning technique may be considered a substantive tax planning technique instead of a formal tax planning

Intertax

532

In turn, substantive dividend withholding tax planningcan be sub-divided in planning that is and planning thatis not based on residency and the related migration of oneor more entities. With regard to migration planning, thefollowing four different forms of tax planning may bedistinguished: (1) the migration of the dividend payor, (2)the migration of the dividend recipient, (3) both thedividend payor and the dividend recipient migrated, and(4) neither the dividend payor nor the dividend recipientmigrated (for tax reasons). Additional substantivedividend withholding tax planning techniques that arediscussed include cross-border mergers and divisions,dividend stripping, sale of the shares in the dividendpayor, and total return swaps used to avoid dividendwithholding tax.

Benchmarking certain dividend withholding taxplanning against the aforementioned framework may result

in a universal tax planning product code, a sort of tax plan-ning barcode that can be used to categorize each tax planningtechnique worldwide. Although a tax planning technique istypically, in its final form, custom-made and thereforedependent on the specifics of the taxpayer involved, the taxplanning barcode helps in determining on what shelf in thetax-planning supermarket the respective tax planningtechnique can be found.

8. CONCLUSION

This study has sought to identify, analyse, and categorizevarious cross-border corporate dividend withholding taxplanning techniques in abstracto and without linkingthese techniques to particular countries. Based on thisstudy, one can conclude that it is possible to distinguishand categorize these dividend withholding tax planningtechniques in cross-border scenarios in a universal,comprehensive, and consistent manner. In addition, as aresult of the aforementioned, it is possible to set up ahigh-level framework, whereby dividend withholding taxplanning techniques that are available to today’s taxpayerscan be categorized.

Such framework may have more than a purely academicvalue. It may be of benefit for the corporate taxpayer andhis advisors since the framework can make clear what sortsof dividend withholding tax planning are availableworldwide and what planning technique the respectivetaxpayer may suit best. In addition, the framework can alsobe of benefit to governments. It may prove to be a tool tocategorize and administer what planning techniques areused by what sort of taxpayer and at what frequency.Moreover, it may perfectly show what dividend withholdingtax loopholes in domestic legislation are still clear andpresent.

Notestechnique. Vice versa, in case a cross-border legal merger or division is merely a pure paper transaction, such transaction may be considered a formal tax planning techniqueinstead of a substantive tax planning technique.

Dividend WithholdingTax PlanningTechniques: Part 2

533