Embed Size (px)

Citation preview

LAW BUSINESS17e

for

John D. Ashcroft, J.D.Distinguished Professor of Law and Government

Regent University Member of the Missouri and District of Columbia Bar

Janet E. Ashcroft, J.D.Member of the Missouri and District of Columbia Bar

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

© 2011, 2008 South-Western, Cengage Learning

ALL RIGHTS RESERVED. No part of this work covered by the copyright herein may be reproduced, transmitted, stored, or used in any form or by any means graphic, electronic, or mechanical, including but not limited to photocopying, recording, scanning, digitizing, taping, web distribution, information networks, or information storage and retrieval systems, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without the prior written permission of the publisher.

For product information and technology assistance, contact us atCengage Learning Customer & Sales Support, 1-800-354-9706

For permission to use material from this text or product,submit all requests online at www.cengage.com/permissions

Further permissions questions can be emailed [email protected]

ExamView® is a registered trademark of eInstruction Corp. Windows is a registered trademark of the Microsoft Corporation used herein under license. Macintosh and Power Macintosh are registered trademarks of Apple Computer, Inc. used herein under license.© 2008 Cengage Learning. All Rights Reserved.

Library of Congress Control Number: 2009939663

ISBN-13: 978-0-324-78653-8

ISBN-10: 0-324-78653-0

South-Western Cengage Learning5191 Natorp BoulevardMason, OH 45040USA

Cengage Learning products are represented in Canada by Nelson Education, Ltd.

For your course and learning solutions, visit www.cengage.com Purchase any of our products at your local college store or at ourpreferred online store www.ichapters.com

Law for Business, Seventeenth EditionJohn D. Ashcroft and Janet E. Ashcroft

Vice President of Editorial, Business: Jack W. Calhoun

Publisher: Rob Dewey

Acquisitions Editor: Vicky True

Developmental Editor: Daniel Noguera

Marketing Manager: Jenny Garamy

Marketing Coordinator: Heather McAuliff e

Content Project Manager: Darrell E. Frye

Media Editor: Kristin Meere

Frontlist Buyer, Manufacturing: Kevin Kluck

Production Service: Integra

Sr. Art Director: Michelle Kunkler

Cover and Internal Designer: Beckmeyer Design

Cover Image: © Todd Davidson/Stock Illustration Source/Getty Images, Inc.

Printed in the United States of America1 2 3 4 5 6 7 13 12 11 10 09

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

232 Part 5 Negotiable Instruments

CHAPTER

Nature of Negotiable InstrumentsL E A R N I N G O B J E C T I V E S

1 Discuss how negotiable instruments are transferred.

2 Differentiate between bearer paper and order paper.

3 Describe an electronic fund transfer.

egotiable instruments or commercial paper are writings drawn in a special form that can be transferred from person to person as a substitute for money or as an instrument of credit. Such an instrument must meet

certain definite requirements in regard to its form and the manner in which it is transferred. Two types of negotiable instruments include checks and notes. Since a negotiable instrument is not money, the law does not require a person to accept one in payment of a debt.

egotiable instrspecial form thafor money or as

certain definite requiremtransferred. Two types o

N

P R E V I E W C A S E

To purchase real property, Albert Austin executed a thirty-year promissory note for $65,913 payable to Harbor Financial Mortgage Corp. The note was reassigned several times, the last time to Countrywide Homes Loans. After two years, Austin stopped making the monthly payments and a lawsuit ensued. Austin alleged Countrywide was not a valid

assignee of the note and thus it was unlawful for it to try to collect it. Kimberly Dawson, vice president of Countrywide, testified that the original note payable to Harbor was indorsed to Countrywide, which had possession of it and had not in any way transferred or pledged it or any interest in it. How may a note be transferred? What is the significance of an indorsement?

20

Commercial Paper or Negotiable InstrumentWriting drawn in special form that can be transferred as substitute for money or as instrument of credit

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

Chapter 20 Nature of Negotiable Instruments 233

History and DevelopmentThe need for instruments of credit that would permit the settlement of claims between distant cities without the transfer of money has existed as long as trade has existed. Negotiable instruments were developed to meet that need. References to bills of exchange or instruments of credit appeared as early as 50 b.c. Their widespread usage, however, began about a.d. 1200 as international trade began to flourish in the wake of the Crusades. At first, these credit instruments were used only in international trade, but they gradually became common in domestic trade.

In England, before about a.d. 1400, special courts set up on the spot by the merchants settled all disputes between merchants. The rules applied by these courts became known as the law merchant. Later, the common-law courts took over the adjudication of all disputes, including those between merchants. However, these courts retained most of the customs developed by the merchants and incorporated the law merchant into the common law. Most, but by no means all, of the law merchant dealt with bills of exchange or credit instruments.

In the United States, each state modified the common law dealing with credit instruments so that eventually the various states had different laws regard-ing them. The American Bar Association and the American Banks Association appointed a commission to draw up a Uniform Negotiable Instruments Law. In 1896, the commission proposed a uniform act. This act was adopted in all the states, but Article 3 of the Uniform Commercial Code (UCC) then displaced it.

In 1990, a commission that writes uniform laws issued a revised Article 3. This text explains the law according to the changes made by the revision. The revision uses the term negotiable instruments, whereas the original Article 3 uses the term commercial paper. Although states adopt uniform laws, it is important to note that the states do not necessarily adopt the uniform laws exactly as writ-ten. Frequently they make minor changes that do not significantly affect the impact of the law. We say that a state has adopted a uniform law when it has adopted the law with but minor changes.

NegotiationNegotiation is the act of transferring ownership of a negotiable instrument to another party. The owner may negotiate a negotiable instrument owned by and payable to such owner. The owner negotiates it by signing the back of it and delivering it to another party. The signature of the owner made on the back of a negotiable instrument before delivery is called an indorsement.1

When a negotiable instrument is transferred by negotiation to one or more parties, these parties may acquire rights superior to those of the original owner. Parties who acquire rights superior to those of the original owner are known as holders in due course. It is mainly this feature of the transfer of superior rights that gives negotiable instruments a special classification all their own.

Order Paper and Bearer PaperIf commercial paper is made payable to the order of a named person, it is called order paper. If commercial paper is made payable to whoever has possession of it, the bearer, it is called bearer paper. Bearer paper may be made payable to

Law MerchantRules applied by courts set up by merchants in early England

1 Indorsement is the spelling used in the UCC, although endorsement is commonly used in business.

LO 2Bearer paper versus order paper

Order PaperCommercial paper payable to order

LO 1Transfer of negotiable instruments

NegotiationAct of transferring ownership of negotiable instrument

Holder in Due CoursePerson who acquires rights superior to original owner

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

234 Part 5 Negotiable Instruments

bearer, cash, or any other indication that does not purport to designate a specific person. Order paper must use the word order, as in the phrase, “pay to the order of John Doe,” or some other word to indicate it may be paid to a transferee. Order paper is negotiated only by indorsement of the person to whom it is then payable and by delivery of the paper to another person. In the case of bearer paper, merely handing the paper to another person may make the transfer.

Payment is made on a different basis with order paper than with bearer paper. Order paper may be paid only to the person to whom it is made payable on its face or the person to whom it has been properly indorsed. However, bearer paper may be paid to any person in possession of the paper.

Bearer PaperCommercial paper payable to bearer

Facts: Doseung Chung purchased a voucher for use in SAMS machines at Belmont Park Racetrack. The SAMS allow a bettor to enter a bet by inserting money, vouchers, or credit cards, and selecting the number or combination desired. The SAMS issue betting tickets and, when a voucher is used, a new voucher showing the balance left. Chung left the SAMS, taking his betting tickets but not the new voucher that showed he had thousands of dol-lars in value left. Chung noticed his mistake with-in minutes, but the new voucher was gone. The track issued a stop order on it, but it had already

been cashed out. Each voucher was marked “Cash Voucher” and “Bet Against the Value or Exchange for Cash.” Chung sued the racetrack.

Outcome: The terms of the vouchers indicated they were bearer paper. As such, a fi nder could negotiate them by transfer of possession even if it was involuntary.

—Chung v. New York Racing Assn.,714 N.Y.S.2d 429 (N.Y. Dist. Ct.)

C O U R T C A S E

Classification of Commercial PaperThe basic negotiable instruments are:

1. Drafts

2. Promissory notes

DraftsA draft is also called a bill of exchange. It is a written order signed by one person requiring the person to whom it is addressed to pay on demand or at a particular time a fixed amount of money to order or to bearer. Checks and trade acceptances are special types of drafts. When you make out a check on your bank account, you are actually writing out a type of draft. (See Chapter 22.)

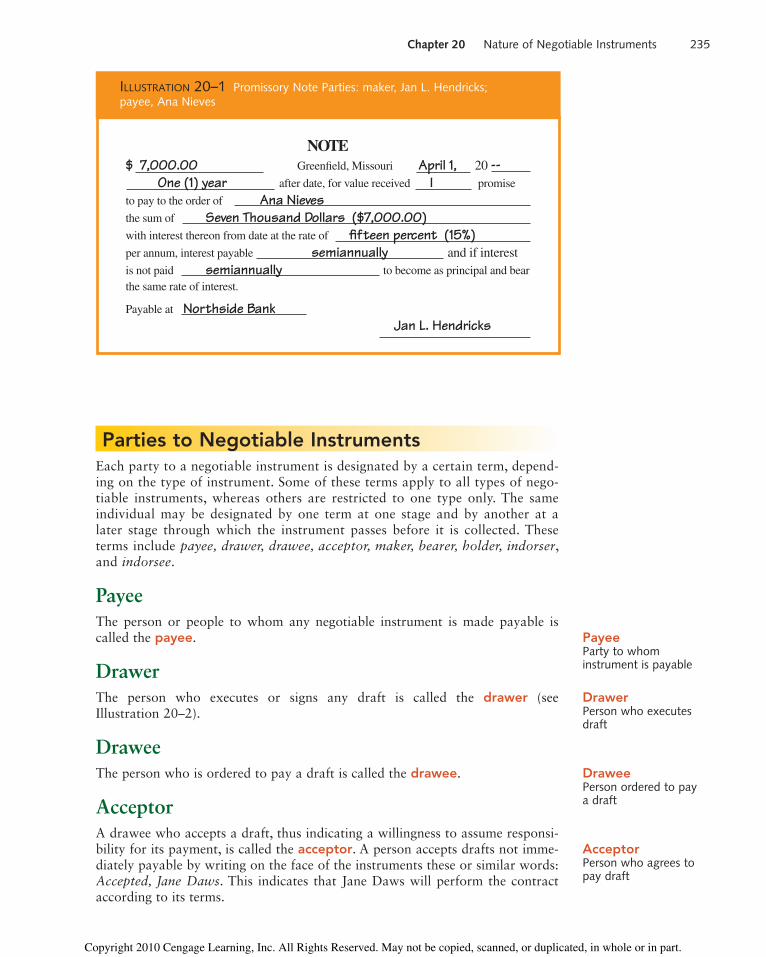

Promissory NotesA promissory note is an unconditional promise in writing made by one person to another, signed by the promisor, engaging to pay on demand of the holder, or, at a definite time, a fixed amount of money to order or to bearer (see Illustration 20–1). If the note is a demand instrument, the holder may demand payment or sue for payment at any time and for any reason.

Draft or Bill of ExchangeWritten order by one person directing another to pay sum of money to third person

Promissory NoteUnconditional written promise to pay sum of money to another

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

Chapter 20 Nature of Negotiable Instruments 235

Parties to Negotiable InstrumentsEach party to a negotiable instrument is designated by a certain term, depend-ing on the type of instrument. Some of these terms apply to all types of nego-tiable instruments, whereas others are restricted to one type only. The same individual may be designated by one term at one stage and by another at a later stage through which the instrument passes before it is collected. These terms include payee, drawer, drawee, acceptor, maker, bearer, holder, indorser, and indorsee.

PayeeThe person or people to whom any negotiable instrument is made payable is called the payee.

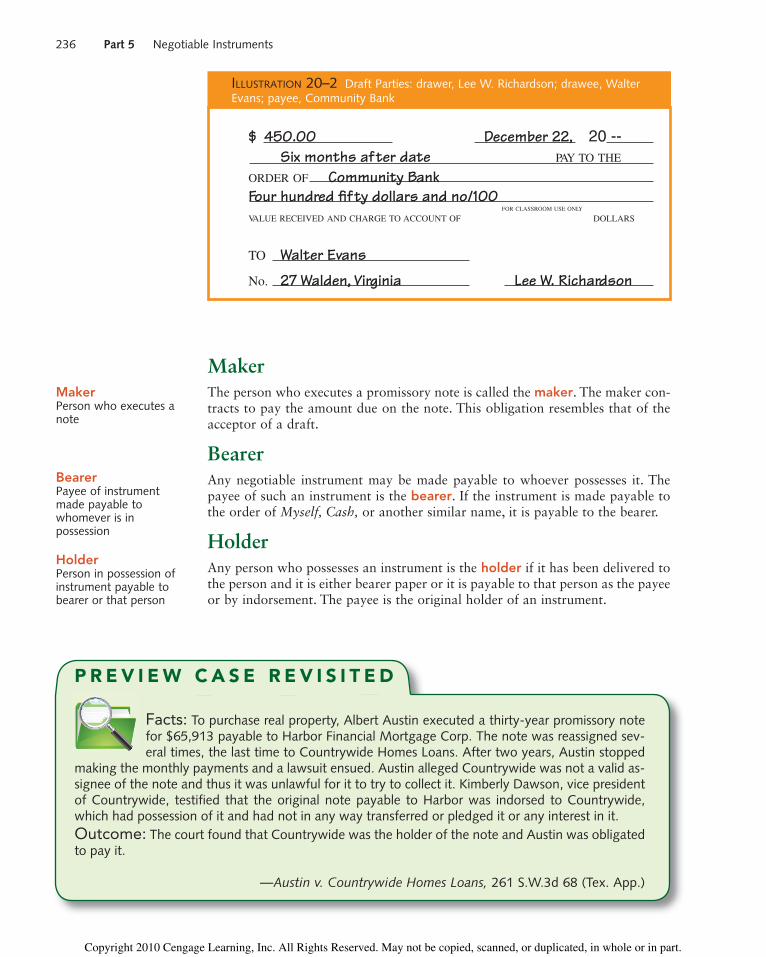

DrawerThe person who executes or signs any draft is called the drawer (see Illustration 20–2).

DraweeThe person who is ordered to pay a draft is called the drawee.

AcceptorA drawee who accepts a draft, thus indicating a willingness to assume responsi-bility for its payment, is called the acceptor. A person accepts drafts not imme-diately payable by writing on the face of the instruments these or similar words: Accepted, Jane Daws. This indicates that Jane Daws will perform the contract according to its terms.

PayeeParty to whom instrument is payable

DrawerPerson who executes draft

DraweePerson ordered to pay a draft

AcceptorPerson who agrees to pay draft

NOTE$ 7,000.00 Greenfield, Missouri April 1, 20 --

One (1) year after date, for value received I promise

to pay to the order of Ana Nievesthe sum of Seven Thousand Dollars ($7,000.00)with interest thereon from date at the rate of fifteen percent (15%)per annum, interest payable semiannually

Jan L. Hendricks

and if interestis not paid semiannually to become as principal and bearthe same rate of interest.

Payable at Northside Bank

ILLUSTRATION 20–1 Promissory Note Parties: maker, Jan L. Hendricks; payee, Ana Nieves

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

236 Part 5 Negotiable Instruments

MakerThe person who executes a promissory note is called the maker. The maker con-tracts to pay the amount due on the note. This obligation resembles that of the acceptor of a draft.

BearerAny negotiable instrument may be made payable to whoever possesses it. The payee of such an instrument is the bearer. If the instrument is made payable to the order of Myself, Cash, or another similar name, it is payable to the bearer.

HolderAny person who possesses an instrument is the holder if it has been delivered to the person and it is either bearer paper or it is payable to that person as the payee or by indorsement. The payee is the original holder of an instrument.

MakerPerson who executes a note

ILLUSTRATION 20–2 Draft Parties: drawer, Lee W. Richardson; drawee, Walter Evans; payee, Community Bank

,22 rebmeceD00.054 $ 20 -- Six months after date PAY TO THE

ORDER OF Community BankFour hundred fifty dollars and no/100VALUE RECEIVED AND CHARGE TO ACCOUNT OF

FOR CLASSROOM USE ONLY

DOLLARS

TO Walter Evans

No. 27 Walden, Virginia Lee W. Richardson

P R E V I E W C A S E R E V I S I T E D

Facts: To purchase real property, Albert Austin executed a thirty-year promissory note for $65,913 payable to Harbor Financial Mortgage Corp. The note was reassigned sev-eral times, the last time to Countrywide Homes Loans. After two years, Austin stopped

making the monthly payments and a lawsuit ensued. Austin alleged Countrywide was not a valid as-signee of the note and thus it was unlawful for it to try to collect it. Kimberly Dawson, vice president of Countrywide, testified that the original note payable to Harbor was indorsed to Countrywide, which had possession of it and had not in any way transferred or pledged it or any interest in it.Outcome: The court found that Countrywide was the holder of the note and Austin was obligated to pay it.

—Austin v. Countrywide Homes Loans, 261 S.W.3d 68 (Tex. App.)

BearerPayee of instrument made payable to whomever is in possession

HolderPerson in possession of instrument payable to bearer or that person

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

Chapter 20 Nature of Negotiable Instruments 237

Holder in Due CourseA holder who takes a negotiable instrument in good faith and for value is a holder in due course.

IndorserWhen the payee of a draft or a note wishes to transfer the instrument to another party, it must be indorsed. The payee is then called the indorser. The payee makes the indorsement by signing on the back of the instrument.

IndorseeA person who becomes the holder of a negotiable instrument by an indorsement that names him or her as the person to whom the instrument is negotiated is called the indorsee.

Negotiation and AssignmentThe right to receive payment of instruments may be transferred by either nego-tiation or assignment. Nonnegotiable paper cannot be transferred by negotia-tion. The rights to it are transferred by assignment. Negotiable instruments may be transferred by negotiation or assignment. The rights given the original parties are alike in the cases of negotiation and assignment. In the case of a promissory note, for example, the original parties are the maker (the one who promises to pay) and the payee (the one to whom the money is to be paid). Between the original parties, both a nonnegotiable and a negotiable instrument are equally enforceable. Also, the same defenses against fulfilling the terms of the instru-ment may be set up. For example, if one party to the instrument is a minor, the incapacity to contract may be set up as a defense against carrying out the agreement.

IndorserPayee or holder who signs back of instrument

IndorseeNamed holder of indorsed negotiable instrument

Facts: Brian and Penny Grieme bought a house fi nanced by a loan from the North Dakota Housing Finance Agency (NDHFA). The home was insured by Center Mutual Insurance Co. Sometime later, the house was damaged by hail. Center issued a check for the damage payable jointly to Brian and NDHFA and mailed it to Brian. He presented the check for payment at a bank. The check bore Brian’s indorse-ment signature and below in hand-printed block letters the words “ND Housing Finance.” The check was paid to Brian. Center refused to pay NDHFA. The Griemes had defaulted on the mortgage and fi led for bankruptcy. NDHFA sued Center.

Outcome: Because the check was order paper, the indorsement of NDHFA was necessary to ne-gotiate it. The unauthorized writing of “ND Hous-ing Finance” did not negotiate the check. NDHFA recovered the amount of the check.

—State ex rel. North Dakota Housing Finance Agency v. Center Mut. Ins. Co.,720

N.W.2d 425 (N.D.)

C O U R T C A S E

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

238 Part 5 Negotiable Instruments

However, the rights given to subsequent parties differ depending on whether an instrument is transferred by negotiation or assignment. When an instrument is transferred by assignment, the assignee receives only the rights of the assignor and no more. (See Chapter 12.) If one of the original parties to the instrument has a defense that is valid against the assignor, it is also valid against the assignee.

When an instrument is transferred by negotiation, however, the party who receives the instrument in good faith and for value may obtain rights that are superior to the rights of the original holder. Defenses that may be valid against the original holder may not be valid against a holder who has received an instru-ment by negotiation.

Credit and CollectionNegotiable instruments are called instruments of credit and instruments of col-lection. If A sells B merchandise on sixty days’ credit, the buyer may at the time of the sale execute a negotiable note or draft due in sixty days in payment of the merchandise. This note or draft then is an instrument of credit.

If the seller in the previous transaction will not extend the original credit to sixty days, a draft may be drawn on the buyer, who would be the drawee. In this case, the drawer may make a bank the payee, the bank being a mere agent of the drawer. Or one of the seller’s creditors may be made the payee so that an account receivable will be collected and an account payable will be paid all in one transac-tion. When the account receivable comes due, the buyer will mail a check to the seller. In this example, the draft is an instrument of collection.

Electronic Fund TransfersMore and more transfers of funds occur today in which a paper instrument is not actually transferred and the parties do not have face-to-face, personal contact. An electronic fund transfer (EFT) is any transfer of funds initiated by means of an electronic terminal, telephonic instrument, or computer or magnetic tape that instructs or authorizes a financial institution to debit or credit an account. An EFT does not include a transfer of funds begun by a check, draft, or similar paper instrument.

EFTs are popular because they are faster and less expensive than the transfer of paper instruments. EFTs can reduce the risk of problems resulting from lost instru-ments. If a check, for example, does not have to make the entire trip from the payee to the drawee bank to the drawer customer, costs and delays can be reduced.

A federal law, the Electronic Fund Transfer Act (EFTA), regulates EFTs and defines them as carried out primarily by electronic means. A transfer initiated by a telephone call between a bank employee and a customer is not an EFT unless it is in accordance with a prearranged plan.

The EFTA requires disclosure of the terms and conditions of the EFTs involv-ing a customer’s account at the time the customer contracts for an EFT service. This notification must include:

1. What liability could be imposed for unauthorized EFTs

2. The type of EFTs the customer may make

3. The charges for EFTs

Under the EFTA, a customer’s liability for an unauthorized EFT can be limited to $50; however, the customer must give the bank very prompt notice of

LO 3Electronic fund transfers

Electronic Fund TransferFund transfer initiated electronically, telephonically, or by computer

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

Chapter 20 Nature of Negotiable Instruments 239

circumstances that lead to the belief that an unauthorized EFT has been or may be made. Also, a bank does not need to reimburse a customer who fails to notify a bank of an unauthorized EFT within sixty days of receiving a bank statement on which the unauthorized EFT appears. Some states also have laws applying to EFTs that may give customers greater protection than the federal law.

Several widely used types of EFTs include check truncation, preauthorized debits and credits, automated teller machines, and point-of-sale systems.

Check TruncationA system of shortening the trip a check makes from the payee to the drawee bank and then to the drawer is called check truncation. It used to be that all banks returned cancelled checks to customers with their monthly bank state-ment. However, most banks no longer return the actual cancelled checks to their customers with the monthly statements. Instead, the statements to customers list the check numbers. The dollar amounts on the checks are shown, and the transactions are printed in numerical order. The customer can easily reconcile the account without having the cancelled checks. However, banks must be able to supply legible copies of the checks at the customers’ request for seven years. This is a type of check truncation.

Preauthorized Debits and CreditsChecking account customers may authorize that recurring bills, such as home mortgage payments, insurance premiums, or utility bills, be automatically deducted from their checking accounts each month. This is called a preautho-rized debit. It allows a person to avoid the inconvenience and cost of writing out and mailing checks for these bills.

A preauthorized credit allows the amount of regular payments to be auto-matically deposited in the payee’s account. This type of EFT is frequently used for depositing salaries and government benefits, such as Social Security payments. It benefits the payor, who does not have to issue and mail the checks. The payee does not have to bother depositing a check and normally has access to the funds sooner.

Automated Teller MachinesAn automated teller machine (ATM) is an EFT terminal capable of performing routine banking services. Many thousands of such machines exist at locations designed to be accessible to customers. The capabilities of the machines vary; however, some ATMs do such things as dispense cash and account information and allow customers to make deposits, transfer funds between accounts, and pay bills. ATMs are conveniently found at many locations, even in foreign countries, and are open when banks are not.

Point-of-Sale SystemsElectronic fund transfers that begin at retailers when consumers want to pay for goods or services with debit cards are called point-of-sale systems (POS). These transactions occur when the person operating the POS terminal enters information regarding the payment into a computer system. The entry debits the consumer’s bank account and credits the retailer’s account by the amount of the transaction.

Check TruncationShortening a check’s trip from payee to drawer

Preauthorized DebitAutomatic deduction of bill payment from checking account

Preauthorized CreditAutomatic deposit of funds to an account

Automated Teller MachineEFT terminal that performs routine banking services

Point-of-Sale SystemEFTs begun at retailers when customers pay for goods or services

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

240 Part 5 Negotiable Instruments

Q U E S T I O N S

1. Does the law require a person to accept a negotiable instrument in payment of a debt?

2. What need did the development of negotiable instruments meet?

3. Is the law exactly the same in all states that have adopted Article 3 of the UCC? Explain.

4. How does the owner negotiate a negotiable instrument?

5. To whom may order paper and bearer paper be paid?

6. What does it mean for a promissory note to be a demand instrument?

7. Who is a holder?

8. Are the rights given to parties subsequent to the original payee the same whether the instrument is transferred by assignment or negotiation? Explain.

9. What is the limit of a customer’s liability for an unauthorized EFT, and what is the customer’s responsibility in order to so limit the liability?

10. What are the benefits of a preauthorized credit to both the payor and payee?

C A S E P R O B L E M S

1. Key Bank National Association operated ATMs that permitted bank customers and noncustomers to conduct transactions. Key Bank customers could use the ATMs without fees, but the bank assessed fees on most noncustomers. Noncustomers who were not charged fees included members of the military, customers of affiliat-ed banks, and users of the Key Bank Cleveland Clinic ATM. When a noncustomer put a card in a Key Bank ATM and entered a personal identification number, the following message appeared on the screen:

“This terminal may charge a fee of $2.00 for a cash withdrawal. This charge is in addition to any fees that may be assessed by your financial institution. Do you wish to continue this transaction?

If yes press to accept fee If no press to decline fee”

Once a noncustomer accepted the fee, the bank would determine whether a fee would be charged. Michael Clemmer, not a Key Bank customer, made a with-drawal at a Key Bank ATM. When the screen had asked whether he accepted the fee, he had selected “yes” and Key Bank had charged him $2. Clemmer sued the bank, alleging he did not receive adequate on-screen notice that he would be charged a fee. Had he received notice of the charge for using the ATM?

2. When Mark Shannahan refinanced his home, First Equity conducted the settle-ment and issued checks to pay off the refinanced mortgage and a second lien. It gave Shannahan a check for $87,764, payable to him, which was his “cash out” from the refinance, as well as a check payable to Farmers Bank in the amount of $40,760 drawn on First Equity’s account at Allfirst. The check payable to Farmers was to pay off Shannahan’s line of credit secured by a lien on the home. Shannahan went to Farmers and deposited the $87,464 check in his personal account there. He indorsed the $40,760 check with his signature and attempted to deposit it in his account. The teller took the check to the bank manager, who saw the check was payable to Farmers and called Shannahan into his office.

LO 3

LO 1

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

Chapter 20 Nature of Negotiable Instruments 241

The manager allowed Shannahan to deposit the Farmers check in his account. Later, Farmers tried to foreclose on Shannahan’s home because the $40,760 line of credit balance was delinquent. First Equity then found out Farmers had not applied the $40,760 check against the unpaid note. First Equity notified Allfirst and asked it to recredit its account. Allfirst refused. In addition to Shannahan’s indorsement, two stamped indorsements of Farmers Bank were on the back of the check. First Equity sued Farmers Bank and Allfirst. Who had negotiated the $40,760 check?

3. Cathy and Ray Vigneri authorized Nationwide Credit, Inc., a debt collector, to withdraw $100 per month from their checking account to pay a debt to American Express. For four months, Nationwide initiated $100 debits on the Vigneris’ account at U.S. Bank National Association. Nationwide initiated the transfers by depositing a paper draft at its bank. The drafts contained the bank’s routing num-ber, the bank’s stamp, and other coding and symbols indicating they had been processed through the Federal Reserve. In August, Nationwide told the Vigneris that American Express wanted the debt paid off and without the Vigneris’ consent withdrew $1,075. As it had done previously, this withdrawal was done by means of a paper draft. The Vigneris sued U.S. Bank, alleging it had violated the EFTA by making an unauthorized withdrawal from their account. Had U.S. Bank violated the EFTA?

4. Gary and Clara Delffs signed a note to Joe Waldron that read, “_____ after date _____ promise to pay to the order of.” After the word “of” was a long blank line on which was handwritten, “one hundred and fifty-three thousand and four hundred and forty dollars.” Following this was printed, “Dollars.” The parties agreed the document was not order paper. A lawsuit ensued, and the court had to decide whether the note was bearer paper. Decide the case.

5. Charles Risner owned Metro Electric & Maintenance, Inc., and Computer Power and Technology, Inc., which both had checking accounts with Bank One Corp. Metro had customers and frequent deposits, but Computer was dormant. Risner’s daughter Janece was the office manager and bookkeeper for both corporations. She deposited checks payable to Metro into Computer’s account. The checks had no indorsement. Janece would then write checks to herself from Computer’s account. When Charles discovered the embezzlement, he sued Bank One and Janece. Were the funds validly negotiated to Computer?

6. While the head of a department at the Charlotte Observer, Oren Johnson sub-mitted phony invoices from Graphic Image, Inc. (GII). Knight Publishing Co., the owner of the Observer, would issue checks in payment payable to GII. Johnson and others used this scheme to steal from the newspaper. They had the checks indorsed by Graphic Color Prep, a business they owned, and deposited in its account. About fifty-five checks were deposited this way for a total of $1.5 mil-lion. When Knight found out, it sued its bank for paying the checks on allegedly improper indorsements. May Knight recover?

7. Miller Furs, Inc., executed a note that stated it “promised to pay, on demand” to the Shawmut Bank an amount not more than $1 million. The note also specified that upon the occurrence of certain events, the bank could decide that the note “shall become and be due and payable forthwith without demand, notice of non-payment, presentment . . . .” Two years later, Shawmut demanded payment of the note. In the lawsuit that followed, Miller argued that the note was not a demand note due and payable when issued, and the bank could only demand payment in good faith. Was the note a demand note?

LO 2

LO 3

LO 1

LO 2

LO 3

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.

![[Business Law] Business Ethics](https://img.pdfslide.net/doc/110x75/5879657c1a28ab1e388b709b/business-law-business-ethics.jpg)