Embed Size (px)

Citation preview

FUTURES

LDCs: Futures Reduce Regulatory Risk Lance W. Schneier

With the introduction of the natural gas futures contract in April. for the first time industry participants could engage in risk-management programs designed to protect against gas-price volatility. While the ability to avoid unanticipated price change is certainly desirable for all industry participants, it must be understood that each indus- try segment has its own set of issues that must be considered before such companies actively engage in futures trading. In this column we will address how one segment, local distribution companies, can participate in the futures mar- ket and will discuss certain of the issues that are unique to LDC participation.

LDC Risk Management In today’s competitive gas marketplace, LDCs must

now be concerned aboutprice volatility, i.e., unanticipated price increases or decreases. For example, LDCs are con- cerned about potential price spikes, which increase the acquisition cost of gas and render it less competitive against other sources of natural gas or alternate fuels. Additionally, LDCs must also be concerned about price decreases. LDCs often commit to purchase gas for a future period at a fixed price. If the spot price drops below the fixed price, the LDC’s large customers can tum to the spot market for their supplies, causing the LDC to lose market share. Natural gas futures can protect an LDC against both

price increases and price declines. Classic hedging strate- gies, as discussed in the June futures column of Natural Gas, describe how an LDC can protect its gas-aquisition Costs.

~

Lance W . Schnrier is chairman, pnsklml, and chuf crccutive officr of Access Energy Corporation of Dub% 0 H . S c h n ~ ~ d A c c e s s i n 1982 as Yankee Resources. For sawn yeus prior to h e , he practiced ellcrgy h w .

Price Risk Exposure Risk management .A appropriate for those who have

price risk. If exposure to price change does not affect profitability, risk management is unnecessary.

At one time, LDCs were insulated from price risk. Granted pass-through authority by their state public utility commissions (PUCs), LDCs merely passed on their gas acquisition costs to their customers. Today, that cultural and legal phenomenon no longer strictly applies. Due to competition from other gas suppliers-marketers, produc- ers and maybe even other LDCs-as well as from other fuel sources, e.g.. fuel oil, pass-through pricing is a vestige of the past.

By applying 20-20 hindsight, a regulutor can determine whether an LI)C’s gas acquisition costs wouId have been lower had it engaged in a successful hedging strategy.

Regulators have also redefined and sharply limited LDCs ’ pass-through ability. Prudency standards are designed to determine whether or not an LDC did an acceptable job in gas procurement (read “bought it cheap enough”). In fact, the growth of the spot market is somewhat attributable to such regulatory pressure.

Until a few years ago, the LDC could satisfy its regula- tors by purchasing all of its supplies from its interstate supplier@). There were no alternatives, and there were no standards upon which to measure LDC performance. Once alternative suppliers emerged, the “safe harbor” of relying upon interstate pipeline supplies was no longer safe. LDCs were and are judged on their ability to sort through all supply options and choose the best mix for their customers. If a PUC determines that an LDC should have purchased more gas on the spot market, it can and does disallow the difference between the actual cost experience and the hypothetical prudent purchasing strategy.

Futures As a Measuring Stick With the advent of natural gas futures, regulators have

one additionalmeasuringstick. Byexaminingfuturesprices, a PUC can objectively determine whether an LDC was

19

I

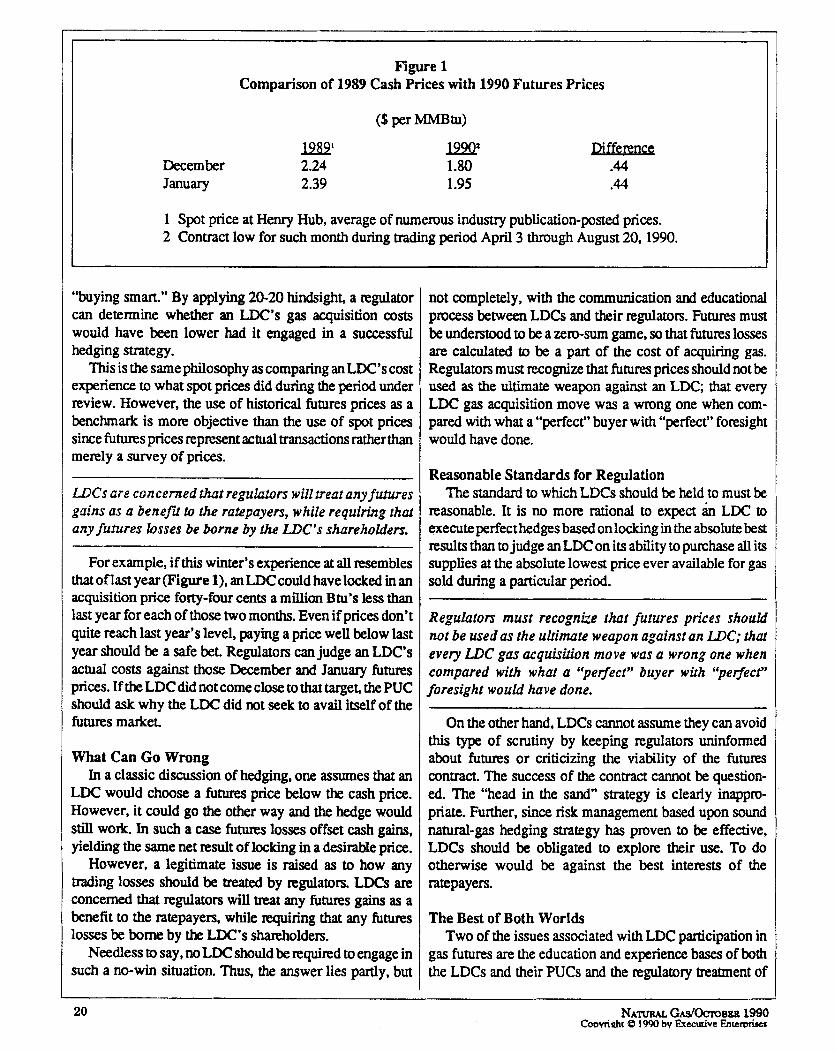

Figure 1 Comparison of 1989 Cash Prices with 1990 Futures Prices

lSs2 December 2.24 January 2.39

m2 1.80 1.95

Difference .44 .44

1 Spot price at Henry Hub, average of numerous industry publication-posted prices. 2 Contract low for such month during trading period April 3 through August 20,1990.

“buying smart.” By applying 20-20 hindsight, a regulator can determine whether an LDC’s gas acquisition costs would have been lower had it engaged in a successful hedging strategy.

This is the same philosophy as comparing an LDC’s cost experience to what spot prices did during the period under review. However, the use of historical futures prices as a benchmark is more objective than the use of spot prices since futures prices represent actual transactions ratherthan merely a survey of prices.

LDCs are concerned t h f reguhtors wifl treat any futures gains as a benefu to the ratepayers, while requiring that any futures losses be borne by fhe LDC’s shareholders.

For example, if this winter’s experience at all resembles that of last year (Figure 1)* an LDC could have locked in an acquisition price forty-four cents a million Btu’s less than last year for each of those two months. Even if prices don’t quite reach last year’s level, paying a price well below last year should be a safe bet. Regulators can judge an LDC’s actual costs against those December and January futures prices. If the LDC did not come close to that target, the PUC should ask why the LDC did not seek to avail itself of the futures market.

What Can Go Wrong In a classic discussion of hedging, one assumes that an

LDC would choose a futures price below the cash price. However, it could go the other way and the hedge would still wok. In such a case futures losses offset cash gains, yielding the Same net result of locking in a desirable price.

However, a legitimate issue is raised as to how any trading losses should be treated by regulators. LDCs are concerned that regulators will mat any futures gains as a benefit to the ratepayers, while requiring that any futum losses be bome by the LDC’s shareholders.

Needless to say, no LDC should be required to engage in such a no-win situation. Thus’ the answer lies partly, but

not completely, with the communication and educational process between LDCs and their regulators. Futures must be understood to be a zero-sum game, so that futures losses are calculated to be a part of the cost of acquiring gas. Regulators must recognize that futures prices should not be used as the ultimate weapon against an LDC; that every LDC gas acquisition move was a wrong one when com- pared with what a “perfect” buyer with “perfect” foresight would have done.

Reasonable Standards for Regulation The standard to which LDCs should be held to must be

reasonable. It is no more rational to expect LDC to execute perfect hedges based on locking in the absolute best results than to judge anLDC on its ability to purchase all its supplies at the absolute lowest price ever available for gas sold during a particular period.

Regulators must recognize that futures prices should not be used as the ulrimote weapon against an LDC; that every LDC gas acquisition move was a wrong one when compared with what a “perfecf” buyer with “petfecf” foresight would have done.

On the other hand, LDCs cannot assume they can avoid this type of scrutiny by keeping regulators uninformed about futures or criticizing the viability of the futures contract. The success of the contract cannot be question- ed. The “head in the sand” strategy is clearly inappro- priate. Further, since risk management based upon sound natural-gas hedging strategy has proven to be effective, LDCs should be obligated to explore their use. To do otherwise would be against the best interests of the ratepayers.

The Best of Both Worlds Two of the issues associated with LDC participation in

gas futures are the education and experience bases of both the LDCs and their PUCs and the regulatory treatment of

20

trading activity. Both these issues can be successfully addressed by utilizing the umcept of passive hedging.

S i p i y put. passive hedging is a strategy that permits LDcs to lock in prices by monitoring futures trading activity but leaves the hedging to the seller of gas. For example, an LDC can contract with a marketer to purchase fixed volumes monthly over the next year. The contract price would be established as the NYMEX price plus an agreed-upon differential. The differential would include mark-up, transportation, and the differential, if any, be- tween the value of gas at the delivery point and the value at Henry Hub.

The NYMEX price would be selected by the LDC at any time during the agreement but before the delivery month ceases trading. Thus, an LDC on any given day could lock in the next month’s price or all twelve months.

Price Risk to the Seller The seller assunes the price risk, i.e., that the gas will be

purchased below the locked-in futures price. Of course, the seller should and could hedge that very risk by buying futures contracts.

The LDC is thus able to lock in future prices, obtain physical delivery of the gas and not engage in active

NA~JRU. G A S / ~ B E R 1990 Gpyrighr 0 1990 by Execurive Enterprises

hedging. By avoiding the latter, there would be no %admg losses” with which to contend.

Conclusion LDCs are understandably wary about utilizing the

gas futures contract, because of a concern a b u t the reg- ulatory treatment of trading losses. However, once PUG fully understand the way hedging works, they will appreciate why such “losses” should be included as appropriate gas acquisition costs. At that point, those LDCs that have not yet embraced futures trading wilI be forced to “get with the program” in much the same way as nxalcitrant LDCs were persuaded to become active in the spot market. In the meantime, futures-based pricing can accomplish most of the same results without attend- ant regulatory issues.

LDCs are understandably wary about utilizing the gas futures conpact, because of a concern about the regula- tory treatmenf of trading losses.

The message is obviou-futures are here to stay and LDCs would be better served to acknowledge the merits of risk management than to debate the inevitable.

21