Embed Size (px)

Citation preview

Leading Tax Advice in Cyprus... and across the World

Investments in and out of the Czech Republic

Avoidance of double taxationPrague, 17th June 2010

• Cross border transactions & Double Taxation

• Cyprus and the favourable DTT concluded with the Czech Republic

• Investing in & out of the

Czech Republic via Cyprus

AgendaLeading Tax Advice in Cyprus... and across the World www.eurofast.eu

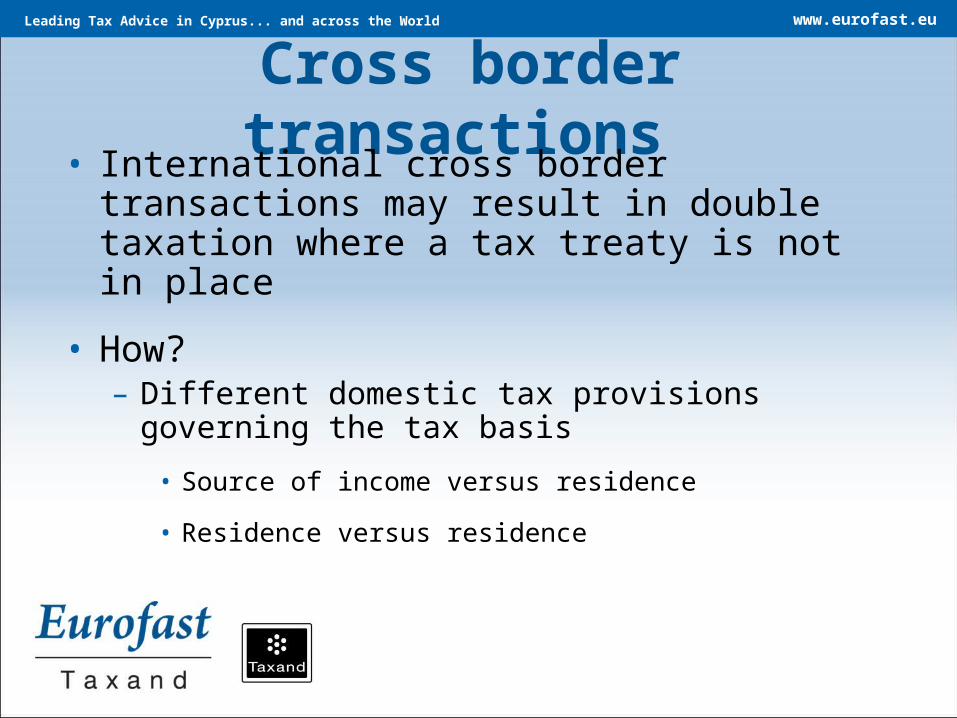

Cross border transactions • International cross border transactions may

result in double taxation where a tax treaty is not in place

• How? – Different domestic tax provisions governing the tax

basis

• Source of income versus residence

• Residence versus residence

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Double TaxationCross border transactions – cross border trouble?

Country ACountry B

Country A residentIncome from business

deriving from Country B

Tax claims on Source of IncomeTax claims on Residency

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Double Tax Treaties • Prevention of double taxation

• More favourable tax provisions; withholding taxes are in most cases reduced and/or eliminated

• Enable the free flow of investments

• Provide for the principles in sharing tax revenue between the countries involved

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Why Cyprus?• Favorable Tax Regime

• Extensive network of Double Tax Treaties concluded– Treaties with key-destinations including the

Czech Republic

• Offers tremendous possibilities for tax planning

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

New Double Tax Treaty:Czech Republic - Cyprus

• Signed on 28 April 2009;

• Replaces the existing treaty between Cyprus and the former Czechoslovakia effective since 1980;

• In force since 1 January 2010

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Withholding taxes: dividends, interest, royalties

• Maximum withholding tax rates under the new Protocol are:

– 0-5% on dividends; • eliminated where a direct holding of at least 10% in the capital of the

subsidiary for an uninterrupted period of 1 year can be established

– No withholding tax at source on interest; taxable only at the level of the recipient;

– 10% on royalties.

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Capital Gains on Investments in Real Estate Companies

• Capital gains:– Gains from the sale of shares or other rights and interests in a

company, a partnership or a trust deriving more than 50% of their value from immovable property situated in the other contracting state may be taxed where the immovable property is situated;

• Income from immovable property– Taxed in the country the immovable property is situated in

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Foreign Investments in the Czech Republic via Cyprus

• Investing in the Czech Republic via Cyprus:

– Withholding taxes capped under the Tax treaty as follows:• 0 – 5% WHT at source on dividends;

• No WHT at source;

• 10% WHT at source on royalties

– Capital Gains• Generally taxed at the level of the

alienator

• Express limitations apply affecting real estate companies– Double layer of Cyprus Companies

may be suggested» Application of the favorable

domestic legislation of Cyprus as opposed to the provisions of the double tax treaty between Czech Republic and Cyprus on capital gains.

Fig. 1

Cyprus Holding CoCyprus Holding Co

Cyprus Subsidiary CoCyprus Subsidiary Co

Czech CoCzech Co

Dividends/Interest/Royalties

Dividends/Interest/Royalties

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Overview of Cypriot Tax Implications• Cyprus Companies

Corporate Income Tax 10%Gains from the sale of securities – exemptIncoming dividends – exemptInterest not in the ordinary course of business –

exempt

Capital Gains Tax 20%Only triggered by the direct or indirect sale of

immovable property situated in Cyprus

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

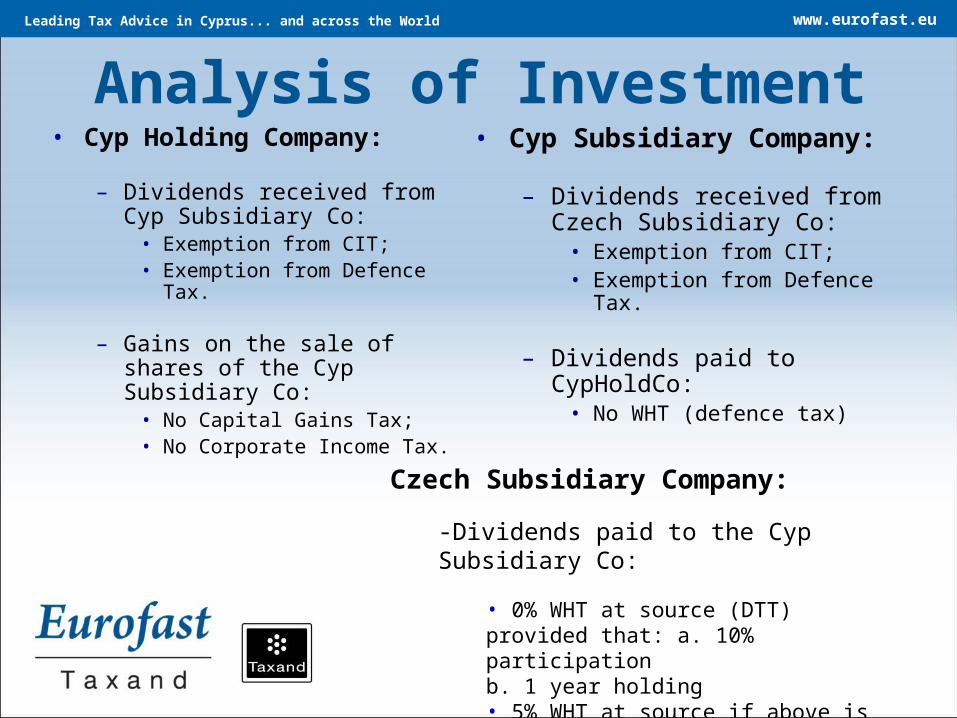

Analysis of Investment• Cyp Holding Company:

– Dividends received from Cyp Subsidiary Co:

• Exemption from CIT;• Exemption from Defence Tax.

– Gains on the sale of shares of the Cyp Subsidiary Co:

• No Capital Gains Tax;• No Corporate Income Tax.

• Cyp Subsidiary Company:

– Dividends received from Czech Subsidiary Co:

• Exemption from CIT;• Exemption from Defence Tax.

– Dividends paid to CypHoldCo:• No WHT (defence tax)

Czech Subsidiary Company:

-Dividends paid to the Cyp Subsidiary Co:

• 0% WHT at source (DTT) provided that: a. 10% participationb. 1 year holding• 5% WHT at source if above is not met

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Exit structure: benefits of using Cyprus• Direct disposal of CZ Co would

trigger a tax obligation in the Czech Republic

– Capital gains tax provision under the treaty

• Double layer of Cyp Companies

Cyprus HoldCo disposes its participation in the Cyprus SubsCo

Cyprus will have sole right to tax gains deriving therefrom

No tax in Cyprus No Capital gains payable on gains

from disposal of any property located outside Cyprus;

Gains on the sale of securities are exempt from Corporate Income Tax.

Fig. 2

Dividends

Dividends

Cyprus Holding CoCyprus Holding Co

Cyprus Subsidiary CoCyprus Subsidiary Co

Czech CoCzech Co

Capital gains

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Investing out of the Czech Republic: in real estateFig. 3 Czech Co / individualCzech Co / individual

Cyprus Holding CoCyprus Holding Co

RussiaUkraineRussiaUkraine BalkansBalkans Latin AmericaLatin America Central Eastern

EuropeCentral Eastern

EuropeChinaIndia

ChinaIndia

No/low WHT onDividends/interest/

royalties

Cyprus:•10% CIT•Dividends:

•No CIT•Generally exempt from SCDF

•No participation requirements• No holding requirements

•Extensive tax treaty network•No tax on sale of securities

100%No WHT on

Dividends/interest/Royalties (rights exercised

outside Cyprus)

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Analysis of Investment• Cyprus is an EU Member State hence eligible to qualify

for the tax exemption on incoming dividends• Favourable regime for structuring investments

– Used as a holding company for investments in RE Companies• Dividends received from RE Cos

– Low/no WHT at source– Generally no tax in Cyprus

• Capital gains from the disposal of participation in RE Cos– No tax in Cyprus (Assumption: no Cypriot RE)– Favourable tax treaty provisions generally eliminate any right to tax at

the source state

• Dividend payments to CZ Co– No WHT in Cyprus as per the domestic law provisions (irrespective of

treaty provisions)

Leading Tax Advice in Cyprus... and across the World www.eurofast.eu

Thank you!

Leading Tax Advice in Cyprus... and across the World