Embed Size (px)

Citation preview

Lease Accounting: Lease Accounting: --Residual Value ReviewResidual Value Review

--End Of LeaseEnd Of LeaseMr. Scott LeedsMr. Scott Leeds Mr. James S. Mr. James S. BrzoskaBrzoska, CPA, CPASr. Financial Research AnalystSr. Financial Research Analyst Chief Accountant WWChief Accountant WWPHILIP MORRIS CAPITAL CORP.PHILIP MORRIS CAPITAL CORP. IBM GLOBAL FINANCINGIBM GLOBAL FINANCING225 High Ridge Road225 High Ridge Road North Castle DriveNorth Castle DriveSuite 300Suite 300 Armonk, NY 10504Armonk, NY 10504--17851785Stamford CT 06905Stamford CT 06905

Part 1Part 1Residual Value ReviewResidual Value Review

GAAP Requirements for Impairment Reviewunder SFAS 13 and SFAS 144

Testing for Impairment

Writedown Methodology

SummaryDisclaimer: The information contained in this document represents the accounting viewpoints of the presenting ELA members. The information and examples contained herein do not necessarily reflect the policies or practices of IBM or any of its affiliates.

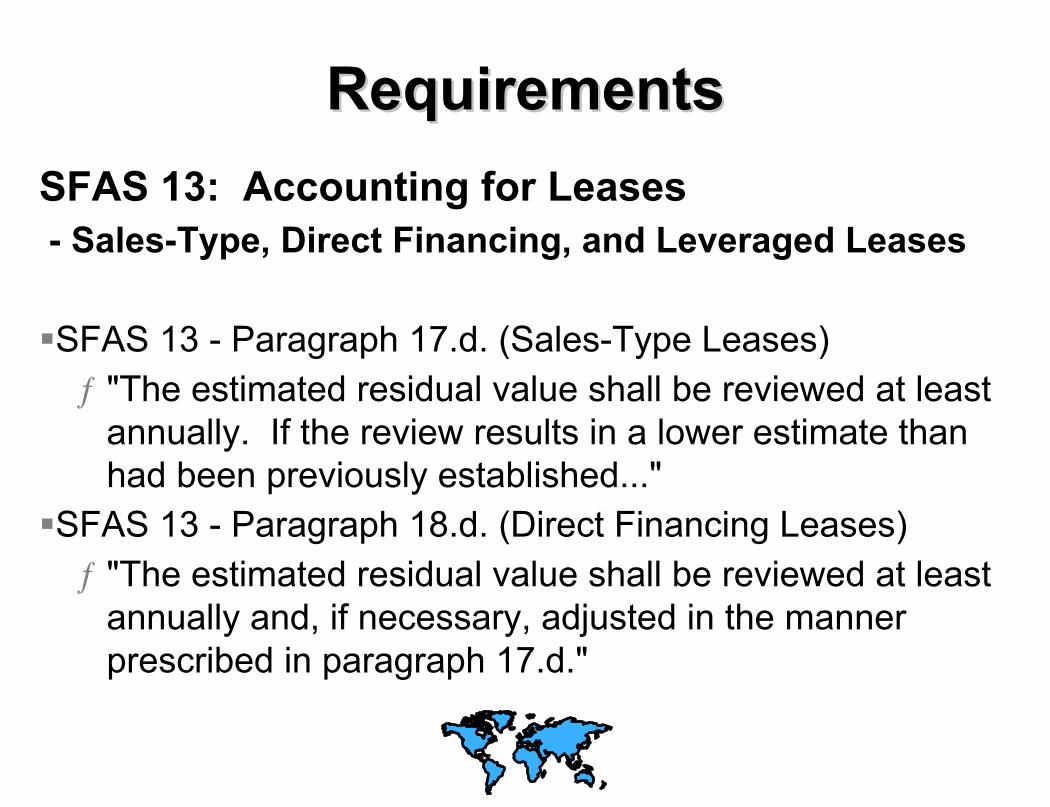

RequirementsRequirementsSFAS 13: Accounting for Leases- Sales-Type, Direct Financing, and Leveraged Leases

SFAS 13 - Paragraph 17.d. (Sales-Type Leases)ƒ "The estimated residual value shall be reviewed at least

annually. If the review results in a lower estimate than had been previously established..."

SFAS 13 - Paragraph 18.d. (Direct Financing Leases)ƒ "The estimated residual value shall be reviewed at least

annually and, if necessary, adjusted in the manner prescribed in paragraph 17.d."

Requirements Requirements (continued)(continued)

SFAS 13 - Paragraph 46 (Leveraged Leases)ƒ "Any estimated residual value and all other important

assumptions affecting estimated total net income from the lease shall be reviewed at least annually. If during the lease term the estimate of the residual value is determined to be excessive..."

RequirementsRequirements (continued)(continued)SFAS 144: Accounting For the Impairment or Disposal of Long-Lived Assets- Operating Lease Assets

SFAS 144 - Supersedes SFAS 121ƒ "....this statement (SFAS 144) retains the fundamental provisions of Statement 121

for (a) recognition and measurement of the impairment of long-lived assets..."SFAS 144 Paragraph 3 - Scopeƒ "...this Statement applies to recognized long-lived assets of an

entity...including...long-lived assets of lessors subject to operating leases,...."

Long-lived Assets should be reviewed for recoverability whenever events or changes in circumstances indicate that their carrying amount may not be recoverable

SFAS 144 "retains the requirement of SFA 121 to recognize an impairment loss only if the carrying amount of a long-lived asset (asset group) is not recoverable from its undiscounted cash flows and exceeds its fair value."

Capital leases of lessees are covered under SFAS 144

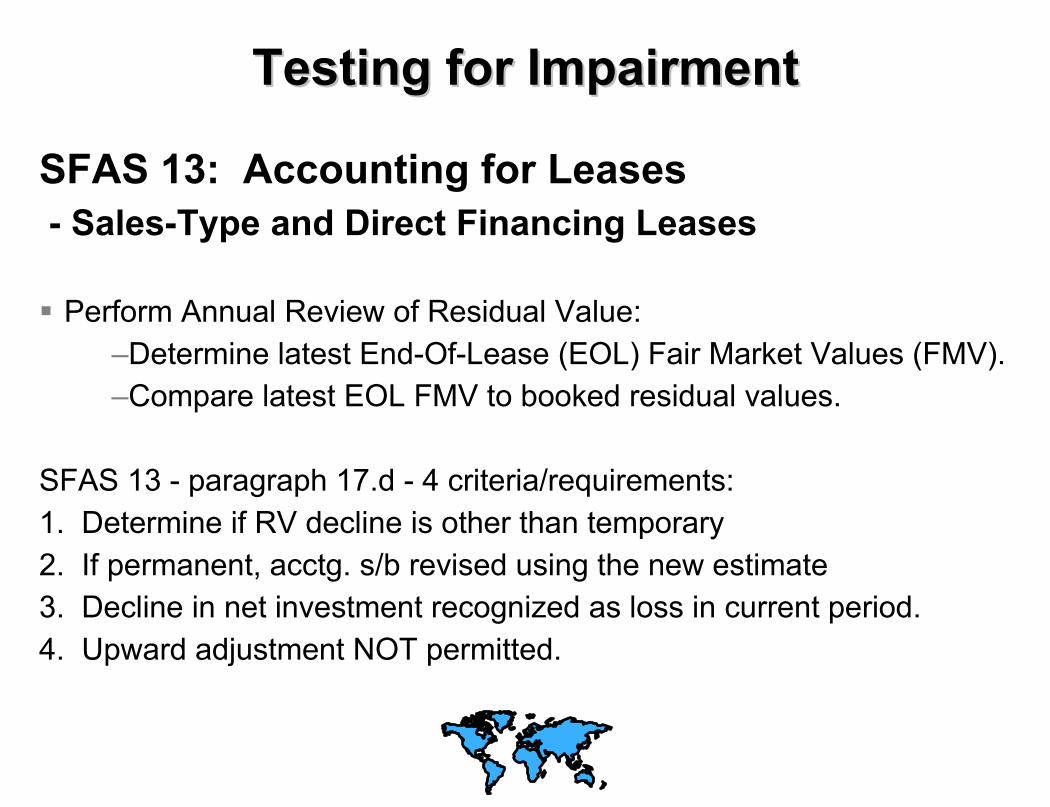

Testing for Impairment Testing for Impairment

SFAS 13: Accounting for Leases- Sales-Type and Direct Financing Leases

Perform Annual Review of Residual Value:–Determine latest End-Of-Lease (EOL) Fair Market Values (FMV).–Compare latest EOL FMV to booked residual values.

SFAS 13 - paragraph 17.d - 4 criteria/requirements:1. Determine if RV decline is other than temporary2. If permanent, acctg. s/b revised using the new estimate3. Decline in net investment recognized as loss in current period.4. Upward adjustment NOT permitted.

SFAS 144: Accounting For the Impairment or Disposal of Long-Lived Assets- Impairment is the condition that exists when the carrying amount of a long-lived asset exceeds its fair value, which can be based upon:

Future Cash Flows Test for Recoverability: Long-Lived Assets to be held and usedƒ Estimate the future cash flow (undiscounted and without interest charges)

expected from the use of the asset.ƒ Assets grouped at the lowest level for identifiable cash flow.ƒ Impairment recognized if future cash flow is less than carrying amount of

the asset.

Comparison to FMV: Fair market value is the amount an asset can be bought or sold for in a current transaction between willing parties. Assess salvage value of entire asset.

Testing for Impairment (continued)Testing for Impairment (continued)

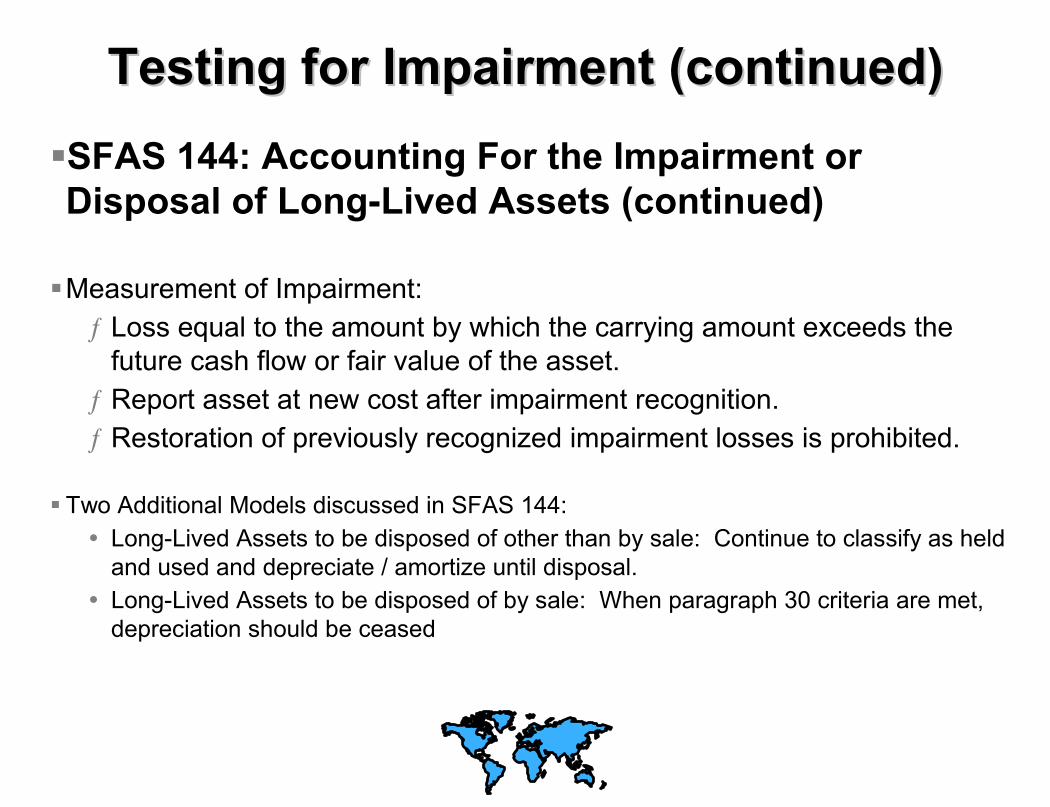

Testing for Impairment (continued)Testing for Impairment (continued)SFAS 144: Accounting For the Impairment or Disposal of Long-Lived Assets (continued)

Measurement of Impairment:ƒ Loss equal to the amount by which the carrying amount exceeds the

future cash flow or fair value of the asset.ƒ Report asset at new cost after impairment recognition.ƒ Restoration of previously recognized impairment losses is prohibited.

Two Additional Models discussed in SFAS 144:Long-Lived Assets to be disposed of other than by sale: Continue to classify as held and used and depreciate / amortize until disposal.Long-Lived Assets to be disposed of by sale: When paragraph 30 criteria are met, depreciation should be ceased

Assumptions:Asset Carrying Value 5,000,000Original Monthly Lease Payment 80,000Residual Value 600,000Lease Term 60 MonthsDiscount Rate 8%

Asset Impairment Test ExampleAsset Impairment Test ExampleOperating Lease Asset, under SFAS 144Operating Lease Asset, under SFAS 144

AFTER YEAR 1Impairment Test - Cash Flows:Cash Inflow: Assume restructured / Revised payment Amount =

$60,000Future Rental Payments (60,000 X 48 Months) 2,880,000Residual Value 600,000Total Cash Inflow 3,480,000

Carrying Value 4,160,000Impairment Writedown Required (680,000)

Writedown MethodsWritedown MethodsSales-type Lease, Direct Financing Lease, and Leveraged Lease Accounting implementation methods

ƒ Sales-type and Direct Financing Leases (para 17d, 18d)–Calculate PV of initial and new residual value

DR: P&L for the delta of the PV's of the initial vs. new RV's.DR: Unearned Income for the delta b/w EOL RV decrease and the PV delta

CR: Gross Investment in lease for the reduction in EOL RV

ƒ Leveraged Leases (para 46)–Recalculate total net income and IIR from inception of lease using the revised RV assumption

–Adjust net investment accounts to conform to the recalculated balances

–Recognize the change in net investment as a gain or loss in current year P&L

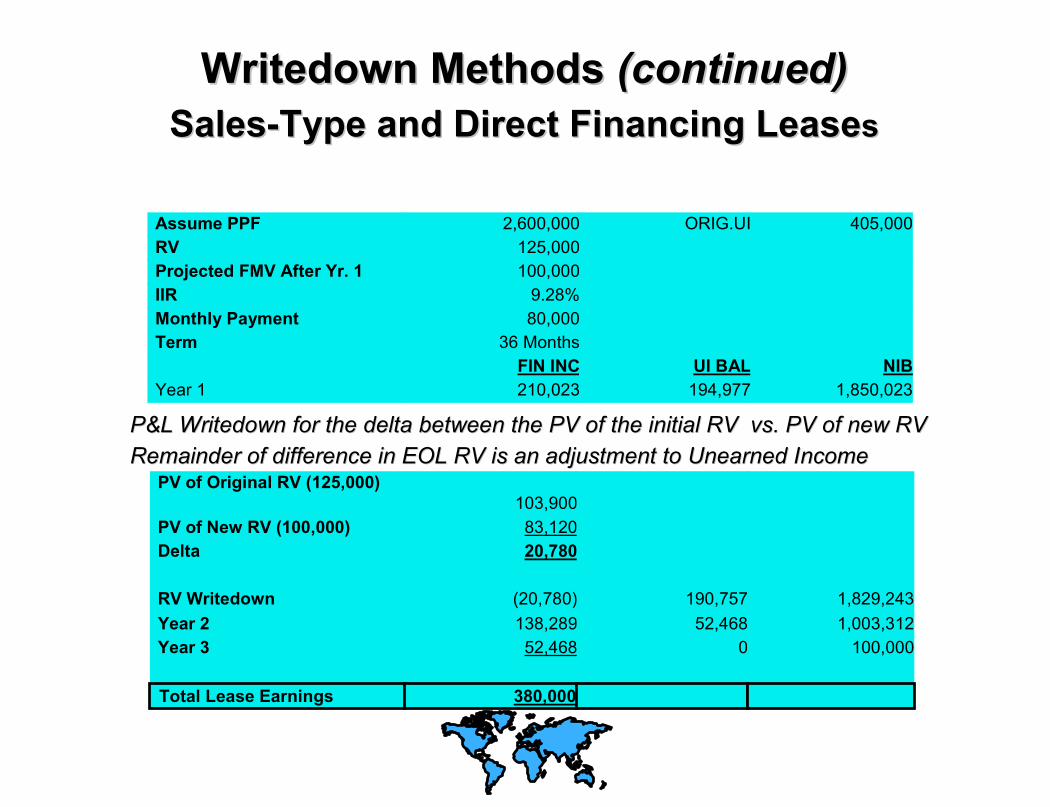

Writedown MethodsWritedown Methods (continued)(continued)SalesSales--Type and Direct Financing LeaseType and Direct Financing Leasess

Assume PPF 2,600,000 ORIG.UI 405,000RV 125,000Projected FMV After Yr. 1 100,000IIR 9.28%Monthly Payment 80,000Term 36 Months

FIN INC UI BAL NIBYear 1 210,023 194,977 1,850,023

PV of Original RV (125,000)103,900

PV of New RV (100,000) 83,120Delta 20,780

RV Writedown (20,780) 190,757 1,829,243Year 2 138,289 52,468 1,003,312Year 3 52,468 0 100,000

Total Lease Earnings 380,000

P&L Writedown for the delta between the PV of the initial RV vsP&L Writedown for the delta between the PV of the initial RV vs. PV of new RV. PV of new RVRemainder of difference in EOL RV is an adjustment to Unearned IRemainder of difference in EOL RV is an adjustment to Unearned Income ncome

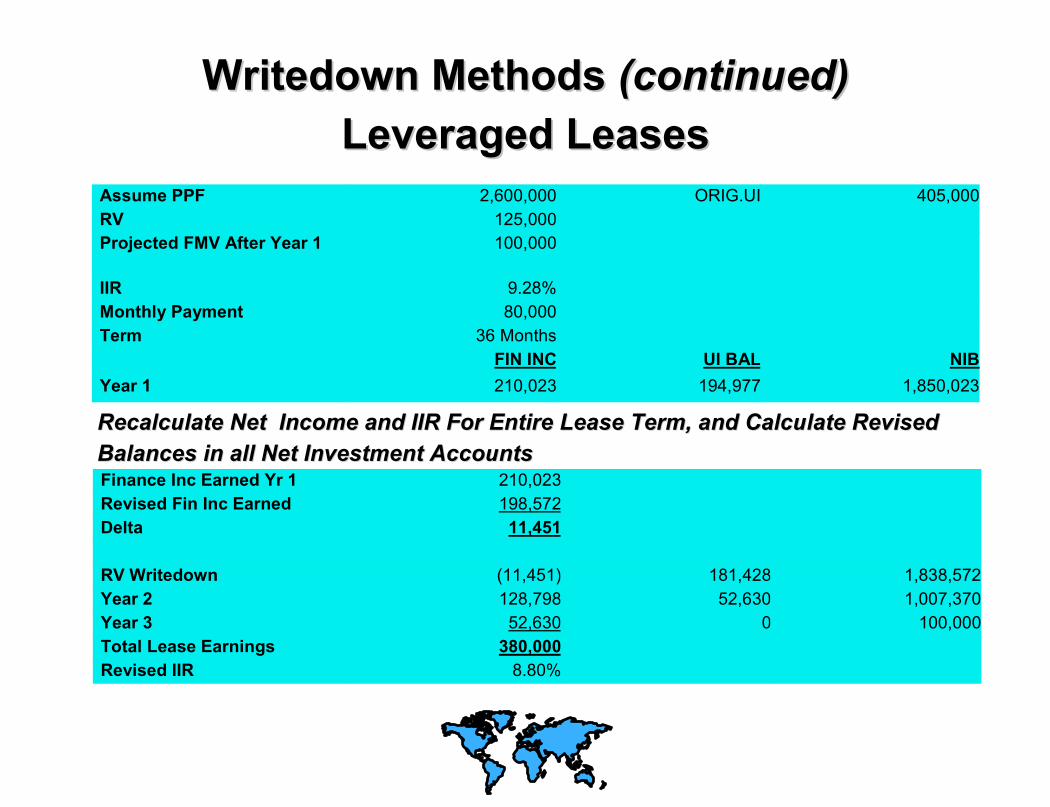

Writedown MethodsWritedown Methods (continued)(continued)Leveraged LeasesLeveraged Leases

Assume PPF 2,600,000 ORIG.UI 405,000RV 125,000Projected FMV After Year 1 100,000

IIR 9.28%Monthly Payment 80,000Term 36 Months

FIN INC UI BAL NIBYear 1 210,023 194,977 1,850,023

Finance Inc Earned Yr 1 210,023Revised Fin Inc Earned 198,572Delta 11,451

RV Writedown (11,451) 181,428 1,838,572Year 2 128,798 52,630 1,007,370Year 3 52,630 0 100,000Total Lease Earnings 380,000Revised IIR 8.80%

Recalculate Net Income and IIR For Entire Lease Term, and CalcuRecalculate Net Income and IIR For Entire Lease Term, and Calculate Revised late Revised Balances in all Net Investment AccountsBalances in all Net Investment Accounts

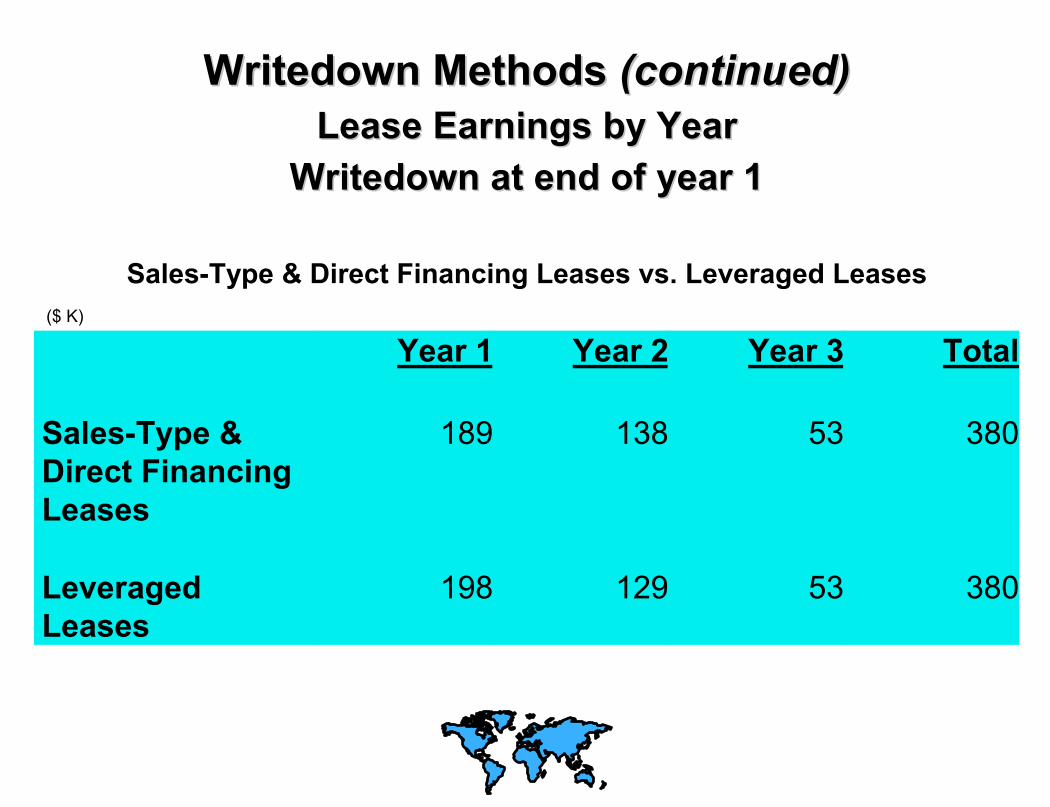

Writedown MethodsWritedown Methods (continued)(continued)Lease Earnings by YearLease Earnings by Year

Writedown at end of year 1Writedown at end of year 1

Sales-Type & Direct Financing Leases vs. Leveraged Leases

Year 1 Year 2 Year 3 Total

Sales-Type & Direct Financing Leases

189 138 53 380

Leveraged Leases

198 129 53 380

($ K)

Writedown MethodsWritedown Methods (continued)(continued)

Operating Lease Assets - Residual ValueAccounting implementation methodƒ Create a revised depreciation schedule based upon the new

estimate of EOL residual value / salvage value.–Calculate the incremental increase in depreciation-to-date for the asset

–Charge the incremental amount to P&L, current period depreciation expense.

–Prospective depreciation based upon the revised schedule

SummarySummary

Mechanics should be customized to fit your portfolio and resources.ƒ High vs. Low Volume Portfolioƒ Automated vs. Manual Approach

Trade-Offsƒ Efficiency vs. Precision

SummarySummary (continued)(continued)

Benefits Derived From Reviewƒ Utilize results to aid in the pricing of new transactionsƒ Methods for reducing exposure may be identified

–Entice customers to enhance asset/extend lease–Enhance/ Develop Marketing Channels–Identify assets to sell

ƒ Gain Marketing's Support to Execute Ideas–Improved bottom line will bring support

With proper planning and execution, review can be a powerful management tool.

Part 2Part 2End of Lease TransactionsEnd of Lease Transactions

Lessee Returns the Equipmentƒ Reconditioning Costsƒ Inventory Valuationƒ Disposition of Inventory

Lessee Purchases the Equipment

Lessee Renews Lease for Specified Term

Lessee Continues Monthly Payment (Continuation)

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"

Guidance - SFAS #13, Paragraph 17 F):ƒ A termination of the lease shall be accounted for by removing the net investment from the

accounts, recording the leased asset a the lower of its' original cost, present fair value, or present carrying amount, and the net adjustment will be charged to income of the period.

Capital OperatingDebit Credit Debit Credit

Min Lease Pmts 0 Equip. 500

UI 0 Acc. Depr. 400

RV 100

Inventory 90 Inventory 90

Fin Income 10 Depr. Exp. 10

Assumptions: RV=100 FMV=90

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"(continued)(continued)Other possible charges for the net adjustment:ƒ Cost of Good Soldƒ Other (ex. Allowance for Doubtful Account or NIB)

Segregate from other sources of inventoryƒ Propensity of Lessee Return vs. Purchaseƒ RV Accuracyƒ Future Profitability

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"(continued)(continued)

Reconditioning CostsReconditioning CostsSmall dollars but very controllableLow value parts & laborƒ Expense or Capitalize?ƒ Minimum Refurbishment vs. Value Add?ƒ Standard Cost or Actual Cost?ƒ Deciding Factors

–Materiality–Inventory Systems Capabilities–Cost Recovery / Profitability

High Value Partsƒ Capitalize Costƒ If not purchased, cost may be assigned

–Relative FMV–List Price

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"(continued)(continued)

Inventory ValuationInventory ValuationDeclines in FMV while in Inventory:ƒ Should be recorded to cost of salesƒ Frequencyƒ Level of Precisionƒ Inventory Valuation vs. RV Reviews

–Parts or Whole Units–Better Availability of FMV Data

FMV Listing is a useful tool for other areas:ƒ Comparison to Reconditioning Costsƒ Collateral Position of Lease Portfolioƒ Profit Potential of Current Inventoryƒ Planning & Pricing Use

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"(continued)(continued)

Debit CreditA/R 110

Sales Revenue 110

COGS 90

Inventory 90

Disposition of Inventory Disposition of Inventory -- SaleSaleAssumptions: Retail FMV=110

Sales are the only "Final" transaction, best time to check:ƒ Accuracy of RV Assumptionsƒ Profitability of Certain Offerings/Products

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"(continued)(continued)

Disposition of Inventory Disposition of Inventory -- LeaseLeaseCapital Lease from inventory are treated as sales typeƒ Paragraph 6 B) of SFAS #13 defines sales type leases as "leases that

give rise to manufacturer's or dealer's profit (or loss) to the lessor (i.e. the fair value of the leased property at the inception of the lease is greater than its cost or carrying amount, if different) and that they meet one or more of the criteria in paragraph 7 and both criteria in paragraph 8."

End of Lease Transactions:End of Lease Transactions:"Returned Equipment""Returned Equipment"(continued)(continued)

Sales Type OperatingDebit Credit Debit Credit

FMV- Rev from STL 110 Equip 90Min Lse Pmts 200 Acc Depr 0UI 100RV 10PV of RV-Rev 5PV of RV-Cost 5

Cost of STL 90Inventory 90 Inventory 90

Important to measure profitability of leasesƒ Lease vs. Saleƒ Inventory Turn vs. Profitabilityƒ Data Integrityƒ Program of New Leases

Assumptions: Retail FMV=110

End of Lease Transactions:End of Lease Transactions:"Equipment Purchased at EOL""Equipment Purchased at EOL"

Assumptions: RV=100, Retail FMV=110

Segregation from other channels of sales is desirableƒ Another measure of RV Accuracyƒ Strategic for "Inventory Avoidance

Capital OperatingDebit Credit Debit Credit

A/R 110 A/R 110

Sales Rev 110 Sales Rev 110

Min Lse Pmts 0

UI 0 Equip 500

RV 100 Acc Depr 400

COGS 100 COGS 100

End of Lease Transactions:End of Lease Transactions:"Lease Renewed at EOL""Lease Renewed at EOL"

Sales Type OperatingDebit Credit Debit Credit

FMV-Rev from STL 110 Equip(Old Lease) 500Min Lse Pmts 200 Acc Depr(Old Lease) 400UI 100 Equip(New Lease) 100

RV(New Lease) 10 Acc Depr(New Lease) 0PV of RV-Rev 5PV of RV-Cost 5

Cost of STL 100RV(Old Lease) 100

Similar entry & analysis as leased from inventory

Capital Lease renewals upon EOL are treated as Sales Typeƒ Paragraph 9) of SFAS #13 “…any action that extends the lease beyond the expiration of the existing lease term, such as the exercise of a lease renewal option other than those already included in the lease term, shall be considered as a new agreement, which shall be classified according to the provisions of paragraphs 6-8."

Assumptions: RV =100, Retail FMV=110

End of Lease Transactions:End of Lease Transactions:Existing Lease Payments are Cont.Existing Lease Payments are Cont.Expected term of this continuation is not always givenMateriality of these payments varies greatlyDue to month-to-month nature of commitment, continuations should be classified as operating leasesBillings can be booked as:ƒ Rental Incomeƒ Credit to Residual Value

Depreciation can be calculated using:ƒ End of Month estimated Residual Valueƒ Straight line over a standard renewal (or other) periodƒ Forced depreciation algorithm

End of Lease Transactions:End of Lease Transactions:SummarySummary

No one right way to handle these transactions

Great demand for data

Can be used as a tool

Accounting "Ownership" of results eliminates data disputes

![WELCOME [] · 2019-06-20 · General Partner 1% Investment Fund Tax Credits Depreciation Deductions Cash Flow ... residual buyout Lease Agreement Sales Proceeds Sale of SEFs and Lease](https://img.pdfslide.net/doc/110x75/5f86f92e5bcb522fed1d932f/welcome-2019-06-20-general-partner-1-investment-fund-tax-credits-depreciation.jpg)