Embed Size (px)

Citation preview

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 1/104

1

Introduction to Foreign Trade

Policy

SESSION 1

LEGAL ENVIRONMENT OF BUSINESS

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 2/104

Background

Waves of change:

Condition before 90s

New world economic order

Globalisation, Liberalisation of trade and investment

Development of IT & communication

Rule based multilateral trading systems – Uruguay

round

Reduction in M tariffs & removal of non-tariff barriers

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 3/104

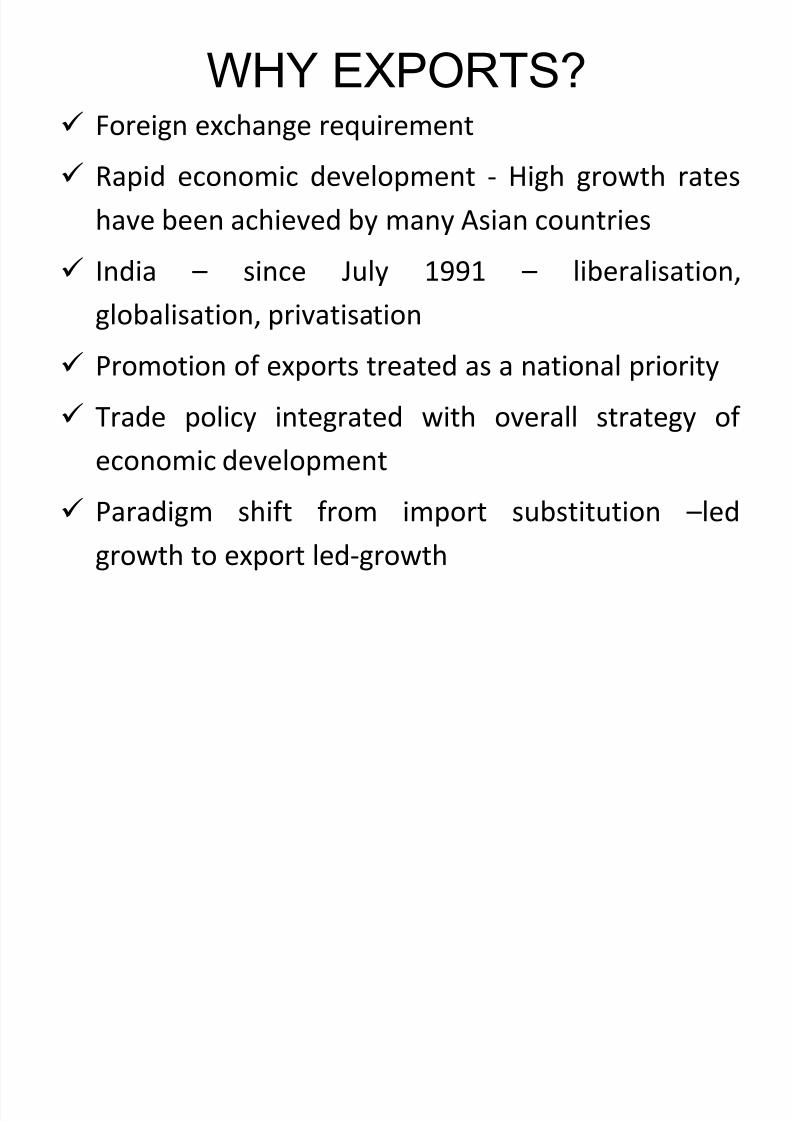

WHY EXPORTS?

Foreign exchange requirement Rapid economic development - High growth rates

have been achieved by many Asian countries

India – since July 1991 – liberalisation,globalisation, privatisation

Promotion of exports treated as a national priority

Trade policy integrated with overall strategy of economic development

Paradigm shift from import substitution –led

growth to export led-growth

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 4/104

How is it different ?

International trading environment (trade

agreements, policies)

Consumer preferences in different markets

Terms & conditions of biz

Communication and negotiations hold the key

Logistics plays important role

Realising payment against the shipment

Claiming incentives/facilities

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 5/104

5

Foreign Trade Policy27thAugust 2009 - 31st March 2014

Government of India

Ministry of Commerce and IndustryDepartment of Commerce

Website: http://dgft.gov.in

FOREIGN TRADE POLICY 2009-14

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 6/104

In India,

the legal framework for regulation of international

trade is mainly provided by the Foreign Trade

(Development And Regulation) Act, 1992 which

replaced the earlier law namely, the Imports &

Exports (Control) Act 1947

6

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 7/104

The Ministry of Commerce, Government of India,

formulates the Foreign Trade Policy (Export –

Import policy), in terms of section 5 of the

Foreign Trade (Development And Regulation)

Act, 1992

7

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 8/104

Foreign Trade (Development And Regulation)

Act, 1992

Export (Quality Control and Inspection) Act, 1963

Customs & Central Excise Duties Drawback Rules,

1995

Foreign Exchange Management Act, 1999

Customs and Central Excise Regulations

In India, Legal Framework for foreign trade is

provided by:

8

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 9/104

Main policy provisions are given in Foreign

Trade Policy : 2009-2014

Covers procedures, agencies & docs required to

take advantage of certain provisions of policy

9

Foreign Trade Policy : 2009-14

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 10/104

Deals with EXIM of merchandise and services

Policy has been described in the following:

Foreign Trade Policy : 2009-14

Handbook of Procedures - Volume I

Handbook of Procedures - Volume II

ITC (HS) Classification of Import-Export Items

Indian Trade Clarification based on Harmonized System of

Coding 10

Foreign Trade Policy : 2009-14

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 11/104

Achievements of FTP 2003-2008

11

2003-04 2008EXPORTS USD 63 bn USD 168 bn

Share of global

merchandise trade

0.83% 1.45%

share of global

commercial services

export

1.4% 2.8%

share in goods andservices trade 0.92% 1.64%

*WTO estimates

14 million jobs were created due to increased exports in

the last 5 years

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 12/104

Short term

to arrest and reverse the declining trend of

exports

to provide additional support to those sectors

which have been hit badly by recession in the

developed world

to achieve 15% annual export growth (US$ 200

bn March 2011)

Objectives of FTP 2009-2014

12

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 13/104

Short term

to achieve an annual growth of 25% upto 2014

to double India’s exports of goods and services

by 2014

long term

to double India’s share in global trade by 2020

Objectives of FTP 2009-2014

13

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 14/104

fiscal incentives

institutional changes

procedural rationalizationenhanced market access across the world

diversification of export markets

Strategy for implementation of FTP

14

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 15/104

Neutralising the incidences of all levies, duties

on inputs used in exports

Duties/levies should not be exported

Avoiding skewed duty structure and ensuring

that India's domestic sectors are not

disadvantaged in FTA/RTA/PTA that India enters

into

15

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 16/104

Identifying and nurturing special focus area for

generating employment in semi-urban and rural

areasFacilitating technological and infrastructural

upgradation of all sectors of Indian Economy,

especially through import of capital goods & equipment

16

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 17/104

Revitalising Board of Trade by redefining its role,giving it due recognition & inducting experts on

FTP

Activating India's embassies as key players for

trade intelligence and enquiry dissemination by

linking commercial wings of the embassies throughan electronic platform

17

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 18/104

under advance authorization scheme, a

minimum of 15% value addition on imported

inputs has been stipulated

diversification of products and markets through

enhancement of incentive rates in particular

product group and market

Additional resources have been made available

under the Market Development Assistance

Scheme and Market Access Initiative Scheme. 18

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 19/104

for market expansion

Comprehensive Economic Partnership Agreement

with South Korea

Trade in Goods Agreement with ASEAN w.e.f. 1.1.10

Mercosur Preferential Trade Agreement

Promotion of Brand India through more than six

‘Made in India’ shows across the world

Technological upgradation : promoting imports of

capital goods under EPCG at 0% duty19

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 20/104

‘Towns of Export Excellence’ and units located

therein have been granted additional focused

support and incentives. high level coordination committee in the

Department of *Commerce facilitates X’s by

creating synergies in the line of credit extended

through EXIM Bank for new & emerging markets

20

Strategy for implementation of FTP

*committee = Ministry of External Affairs + Department of Economic Affairs + EXIM Bank + R.B.I.

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 21/104

zero duty EPCG scheme and incentives for

production and export of ‘green products’

e-trade project : to reduce transaction cost andinstitutional bottlenecks

Additional ports/locations are being EDI

enabled

21

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 22/104

single window mechanism : Inter-Ministerial

Committee has been estd. to resolve trade

related grievances

22

Strategy for implementation of FTP

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 23/104

Schemes to Encourage X

SERVED FROM INDIA SCHEME (SFIS)

FOCUS MARKET SCHEME (FMS)

VISHESH KRISHI AND GRAM UDYOG YOJANA (VKGUY)

FOCUS PRODUCT SCHEME (FPS)

Scheme for Assistance to States for Developing

Export Infrastructure and Allied Activities (ASIDE)

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 24/104

Policy initiative

SPECIAL FOCUS INITIATIVES

Market Diversification

26 new countries have been included within the ambit

of Focus Market Scheme. The incentives provided under Focus Market Scheme

have been increased from 2.5 % to 3 %.

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 25/104

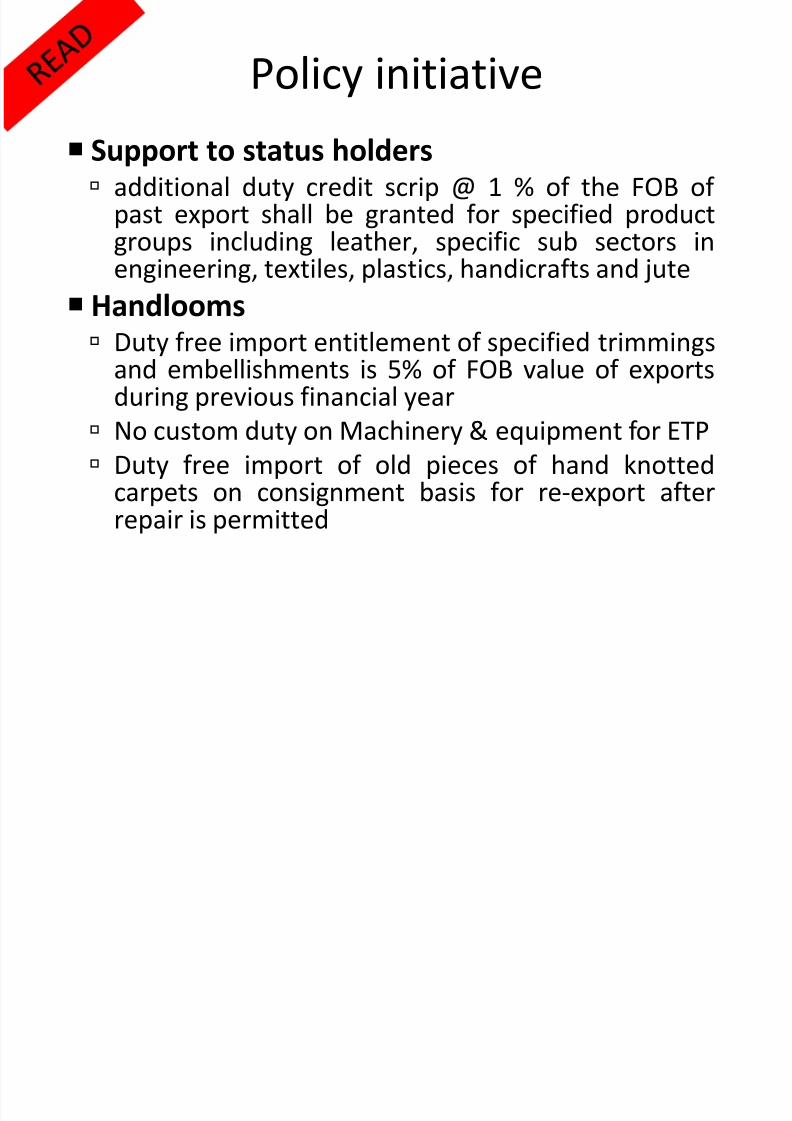

Support to status holders additional duty credit scrip @ 1 % of the FOB of

past export shall be granted for specified productgroups including leather, specific sub sectors in

engineering, textiles, plastics, handicrafts and juteHandlooms Duty free import entitlement of specified trimmings

and embellishments is 5% of FOB value of exportsduring previous financial year

No custom duty on Machinery & equipment for ETP

Duty free import of old pieces of hand knottedcarpets on consignment basis for re-export afterrepair is permitted

Policy initiative

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 26/104

Handicrafts

Duty free import entitlement of tools, trimmings andembellishments is 5 %of FOB value of exports duringprevious financial year.

No custom duty on Machinery and equipment for ETP

All handicraft exports would be treated as special Focus

products and entitled to higher incentives. Leather and Footwear Duty free import entitlement of specified items is 3 % of

FOB value of exports of leather garments during precedingfinancial year.

Re-export of unsuitable imported materials such as rawhides & skins and wet blue leathers is permitted.

Re-export of unsold hides, skins and semi finished leathershall be allowed from Public Bonded warehouse at 0% of the applicable export duty.

Policy initiative

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 27/104

General Provisions Regarding EXIM

Free EXIM unless regulated

Can X gifts of value < Rs. 5L in a licensing year

All X contracts and invoices shall be

denominated either in freely convertible

currency or Indian rupees but X proceeds shall

be realised in freely convertible currency

Units in SEZ shall be exempted from service tax

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 28/104

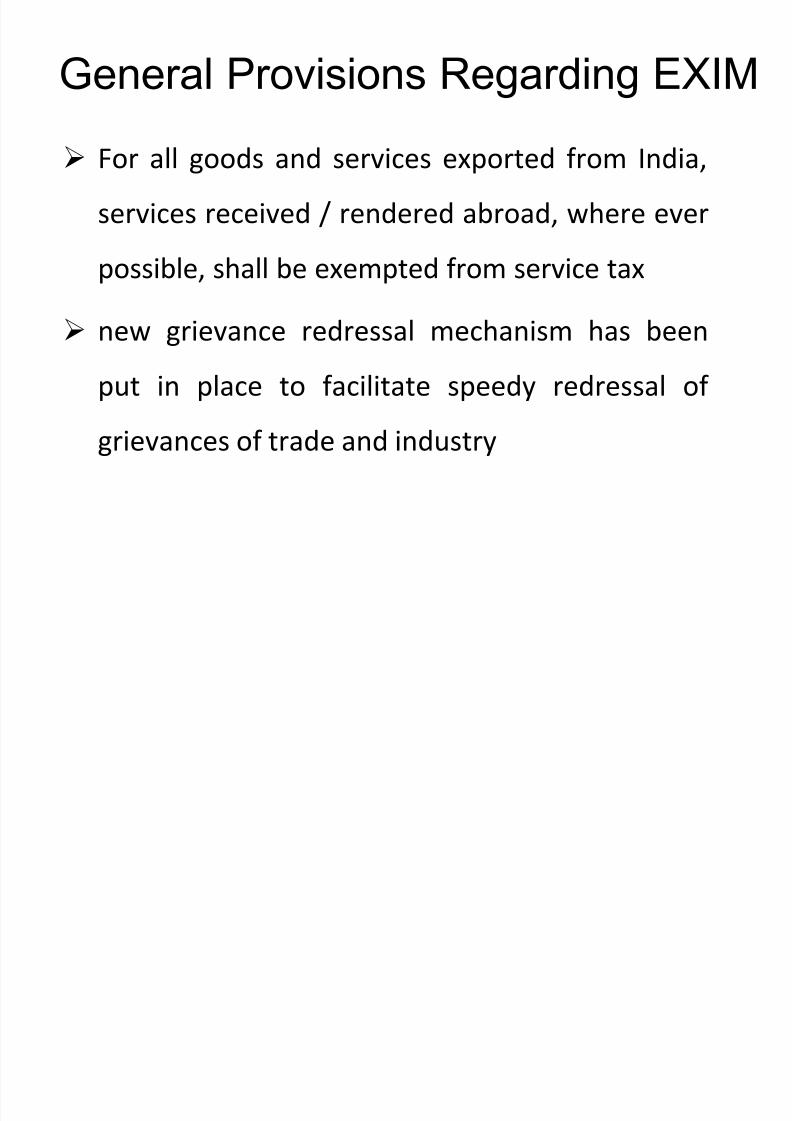

General Provisions Regarding EXIM

For all goods and services exported from India,

services received / rendered abroad, where ever

possible, shall be exempted from service tax

new grievance redressal mechanism has been

put in place to facilitate speedy redressal of

grievances of trade and industry

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 29/104

1. *Stability of Policy

2. Liberalised Exports & Imports

3. Imports of capital goods

4. Export Promotion Capital Goods scheme

5. Duty Exemption/Remission Scheme

6. *Import of Replacement of Goods

7. *Export and Import of Free Trade Samples8. *Replacement of Defective Goods

9. *Export of Goods after Repairs

10. *Export of Imported Goods

Main Provisions : FTP 2004-09

29

Main pro isions FTP 2004 09

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 30/104

2. Liberalised Exports & Imports

Main provisions : FTP 2004-09

Provides for liberalised EXIM

Also provides for Restrictions based on

protection of

a. Public morals

b. Human, Animal or Plant life or health

c. Patents, Trademarks, Copyrights

d. National Treasures (art, history, etc.)

e. Prevention of use of prison labour

f. Conservation of exhaustible natural resources

30

Main provisions FTP 2004 09

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 31/104

2. Liberalised Exports & Imports

Main provisions : FTP 2004-09

EXPORT of various items can be classified into

four categories

A. Prohibited

B. Restricted

C. State Trading Enterprise

D. Free with terms and conditions

31

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 32/104

Can’t be exported!!!

Prohibited

32

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 33/104

Can be exported only against a valid export

licence or subject to such conditions as may be

specified for a particular item in *ITC(HS)

Classification

Export Licence is granted against confirmed

export order only

Restricted

33*Indian Trade Clarification based on Harmonized System of Coding

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 34/104

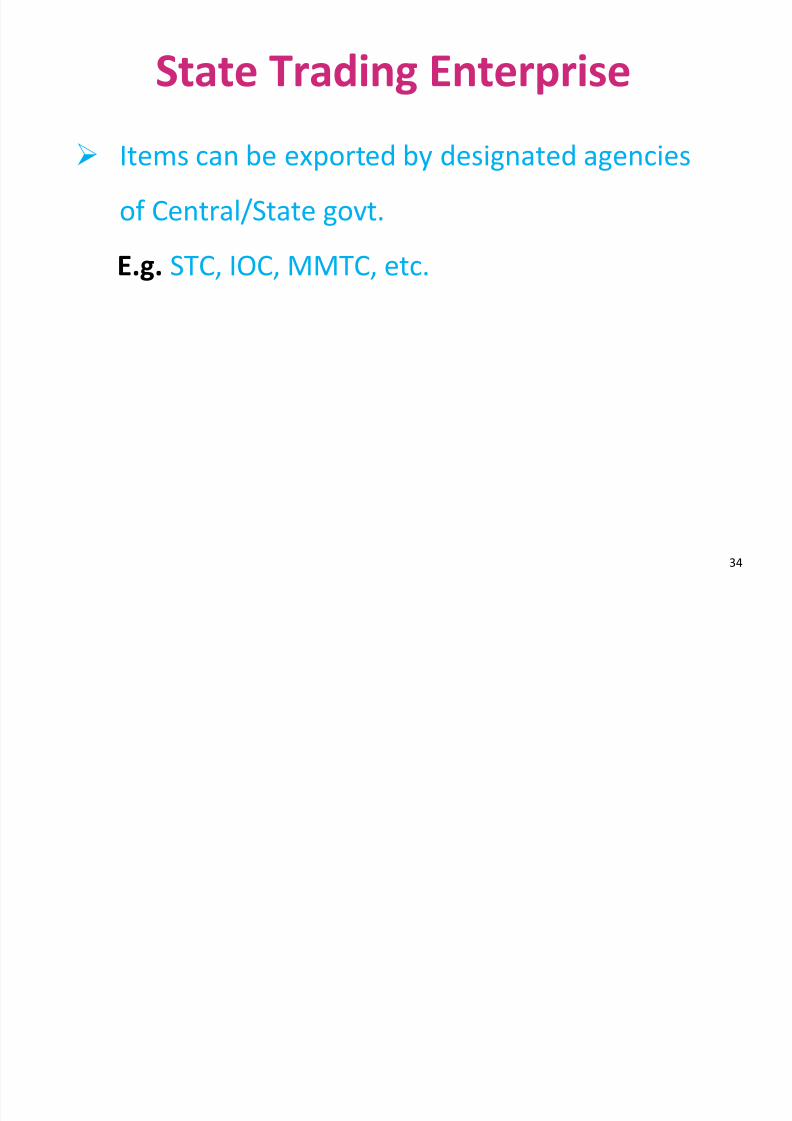

Items can be exported by designated agencies

of Central/State govt.

E.g. STC, IOC, MMTC, etc.

State Trading Enterprise

34

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 35/104

Certain items are free to export

No licence is required.*

*Subject to conditions like

a) Minimum export price

b) Registration with export promotion council

c) Registration of export contracts, etc.

Free with terms & conditions

35

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 36/104

Items which don’t fall in any category can

be exported without any restriction!!!

36

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 37/104

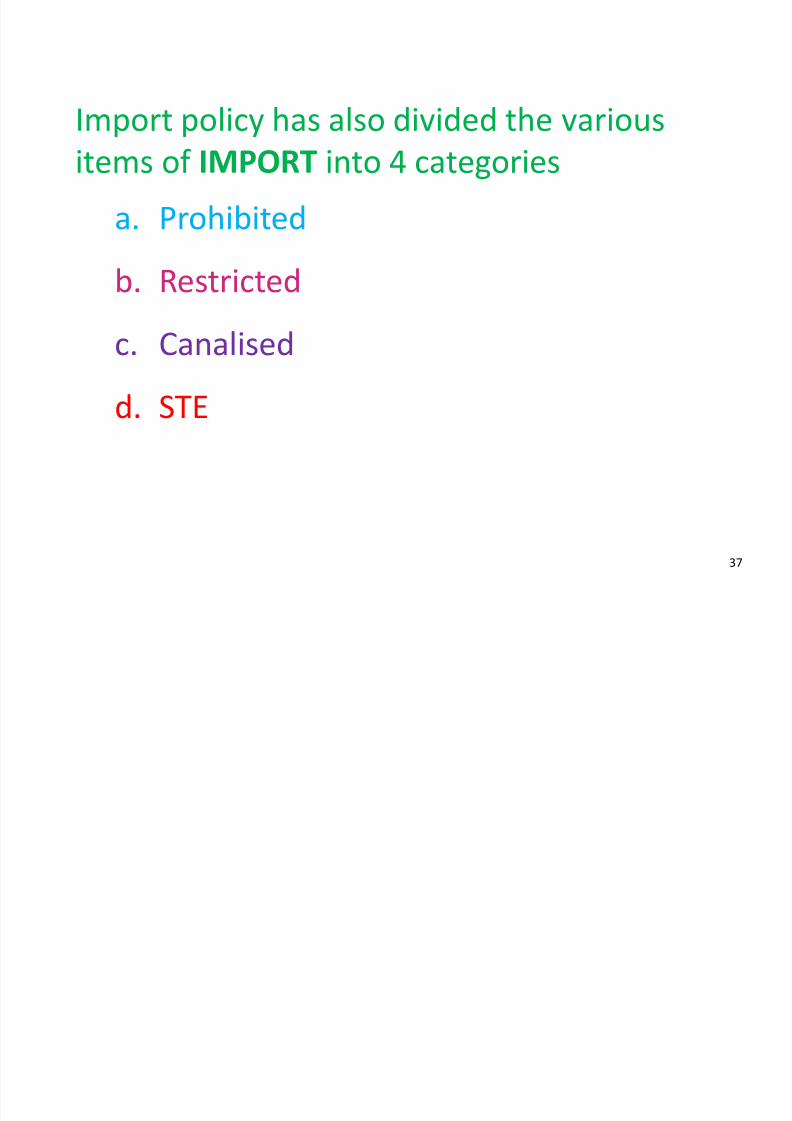

Import policy has also divided the various

items of IMPORT into 4 categories

a. Prohibited

b. Restricted

c. Canalised

d. STE

37

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 38/104

Can’t be imported

BEEF, IVORY, etc.

Prohibited

38

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 39/104

Prohibited items

• All forms of wild life including their parts and products except Peacock Tail

Feathers, including handicrafts made thereof and manufactured articles,and shavings of Shed Antlers of Chital and Sambhar subject to conditions.

• Exotic birds

• wild orchids, as well as plants as specified

• Beef

• Human skeletons

• Tallow, fat and/or oils of any animal origin excluding fish oil• Wood and wood products in the form of logs, timber, stumps, roots, barks,

chips, powder, flakes, dust, pulp and charcoal except sawn timber madeexclusively out of imported teak logs/timber subject to conditions

• Chemicals included in Schedule 1 of the Chemicals Weapons Conventionof the United Nations

• Sandalwood in any form, but excluding fully finished handicrafts made outof sandalwood and machine finished sandalwood products

• Red Sanders wood in any form, whether raw, processed or unprocessed aswell as any product made thereof.

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 40/104

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 41/104

Restricted items

• Cattle, Camel

• Chemical fertilizers

• Dress materials/readymade garments fabrics/textileitems with imprints of excerpts or verses of the HolyQuran

• Hides and skins

• Viscose staple fibre (Regular), excluding high

performance viscose staple fibre• Silk worms, silkworm seeds and silk worm cocoons

• And the list goes on and on …

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 42/104

Items can be imported only through

designated agencies of GOI

Canalised

42

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 43/104

Canalised items

Petroleum products

Mica waste

Mineral ores , concentrates and compounds

Niger seeds

Onions

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 44/104

Import of items is permitted by STE

Solely in accordance with commercial

considerations including PRICE, QUALITY,

AVAILABILITY, MARKETABILITY,

TRANSPORTATION, ETC.

Items – wheat, rice, urea, petrol, diesel, etc.

State Trading Enterprise

44

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 45/104

Exporter is required to obtain exportlicence for each order in case of export of

restricted item

Exporter should take into account the

impact on delivery schedule before

agreeing on delivery dates.

45

Main provisions : FTP 2004-09

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 46/104

3. Imports of capital goods

Main provisions : FTP 2004 09

Today, no licence required, just pay import duty

a firm can import second hand capital goods

w/o any import licence, no age restriction

Minm value of 2nd hand plant & m/c = 25 cr.

46

Main provisions : FTP 2004-09

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 47/104

4. Export Promotion Capital Goods scheme

Main provisions : FTP 2004 09

To enable cost competitiveness, GOI introduced

EPCG scheme

Firms now pay only *5% custom duty Capital goods includes :

a) New as well as second hand capital goods

b) Computer software systems

c) Spares, jigs, dies, fixtures & moulds

d) Components of capital goods

e) Spares of existing plant & machinery

47*subject to fulfillment of export obligation

Main features of EPCG scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 48/104

Following firms can import at 5% duty

1 Manufacturer Exporters, 2 Merchant Exporters

and 3 Service providers

Common service providers in towns of export

excellence, e.g. Tirupur, Panipat, Ludhyana

Retailers having minimum area of 1000 sq.mt.

Project imports notified by the Central Board of

Excise & Customs wherein basic customs duty

on imports is 10% with a CVD of 16%

Main features of EPCG schemeEligibility of import

48

Main features of EPCG scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 49/104

8 times the amount of duty saved on import of

capital goods under this scheme

6 times the amount of duty saved in case of

SSI units provided the landed CIF value of

capital goods < 25 lakhs and after inclusion of

goods should be < SSI limit of investment (1Cr.)

Main features of EPCG schemeAmount of Export Obligation

49

Main features of EPCG scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 50/104

Within 8 years from date of issuance of licence.

Up to 12 years in the following cases:

Amount of duty saved is > 100 crores

EPCG licence holder is a unit under the revival plan of

BIFR (Banking for Industrial and Financial

Restructuring)

Licence holder is in Agri-export zone

Main features of EPCG schemePeriod of Discharge of Export Obligation

50

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 51/104

Main features of EPCG scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 52/104

3. Licence holder shall fulfill export obligation over the

specified period in the following proportions

Main features of EPCG schemeDischarge of Export Obligation

Period of export obligation

(8 years)

Minimum export obligation to

be fulfilled

1 to 6th year 50 %

7th and 8th year 50 %

Period of export obligation

(12 years)1 to 10th year 50 %

11th and 12th year 50 %

Export obligation of a particular block of years may be set off by the excess of

export made in the preceding block of year52

Main features of EPCG scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 53/104

Licence holder may source new capital goods

from domestic leasing company/domestic

manufacturer. No permission of licensing authority is required

under leasing financial arrangement

Licence holder alone shall be responsible for

fulfillment of export obligation

Main features of EPCG schemeLeasing of Capital Goods

53

Main provisions : FTP 2004-09

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 54/104

p

FTP provides for duty exemption/ remission

scheme + EPCG scheme to augment Indian

export

Exporters can import duty free inputs required

for manufacture of products for export

5. Duty Exemption/Duty Remission Scheme

54

Main features of EPCG scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 55/104

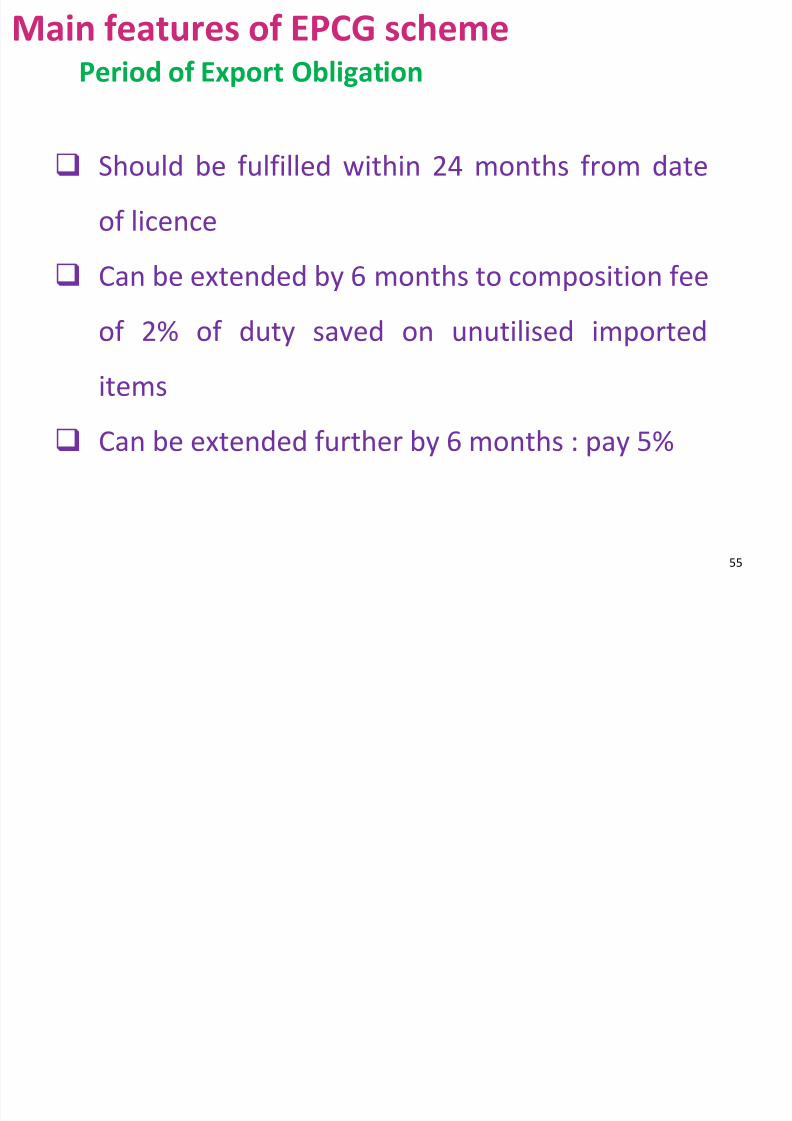

Should be fulfilled within 24 months from date

of licence

Can be extended by 6 months to composition feeof 2% of duty saved on unutilised imported

items

Can be extended further by 6 months : pay 5%

Main features of EPCG schemePeriod of Export Obligation

55

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 56/104

SEZ, EOU, STP & EHTP

Schemes

56

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 57/104

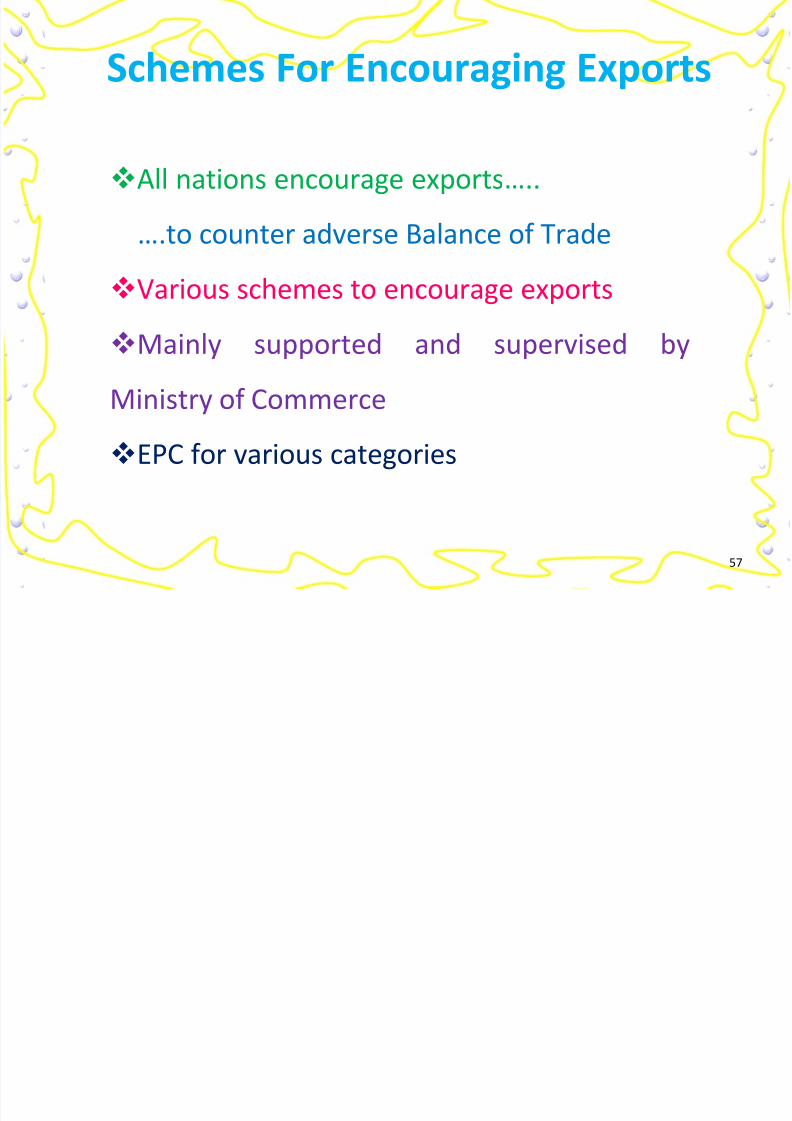

Schemes For Encouraging Exports

All nations encourage exports…..

….to counter adverse Balance of Trade

Various schemes to encourage exports

Mainly supported and supervised by

Ministry of Commerce

EPC for various categories

57

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 58/104

Export Incentives for Manufacturer

Indigenous inputs w/o payment of excise duty

No excise charged on final product

Imported inputs w/o payment of customs duty

No export duty on export of final product

Fast finance at concessional interest rates

Exemption from income tax

Exemption from SALES TAX on final product

(refund of CST paid on inputs in certain cases) 58

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 59/104

WTO STIPULATION

‘No country can give export incentives’

However….goods can be made tax free for export

purposeAll export promotion schemes ensure that inputs

as well as final products are made ‘TAX FREE’

59

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 60/104

Various schemes – to obtain duty free inputs OR

get refund later

1. Some schemes – unit has to be isolated from

domestic production units

E.g. EOU, STP, EHTP and SEZ

60

Input Duty Relief Scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 61/104

2. Other schemes –domestic producers are also

entitled to get inputs/capital goods free of taxes

E.g. a) Advance Licence scheme

b) Duty Entitlement Pass Book scheme (DEPB)

c) Duty Free Replenishment Certificate

scheme (DFRC)d) EPCG scheme (Export Promotion Capital

Goods scheme)61

Input Duty Relief Scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 62/104

e. Rebate of duty on inputs if final product is

exempt from duty

f. Under duty drawback scheme, excise duty paidon inputs is returned as rebate

62

Input Duty Relief Scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 63/104

Highlights of EOU/SEZ scheme

SEZ unit has to be located within the specified

zones developed, 114 operational, another 500

formally approved

EOU unit can be set up at any of over 300 places

all over India

63

Currently there are 114 SEZs (as of October 2010) operating throughout India in the following states[8]: Karnataka - 18; Kerala - 6;

Chandigarh - 1; Gujarat - 8; Haryana - 3; Maharashtra - 14; Rajasthan - 1; Tamil Nadu - 16; Uttar Pradesh - 4; West Bengal - 2: Orissa -

1.

Additionally, more than 500 SEZs are formally approved (as on October 2010) by the Government of India in the following states[9]:

Andhra Pradesh - 109; Chandigarh - 2; Chattisgarh - 2; Dadra and Nagar Haveli - 4; Delhi - 3; Goa - 7; Gujarat - 45; Haryana - 45;

Jharkhand - 1; Karnataka - 56; Kerala - 28; Madhya Pradesh - 14; Maharashtra - 105; Nagaland - 1; Orissa - 11; Pondicherry - 1;

Punjab - 8; Rajasthan - 8; Tamil Nadu - 70; Uttarkhand - 3; Uttar Pradesh - 33; West Bengal - 22.

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 64/104

Similarly, STP/EHTP unit can be situated

within SEZ or at any place where EOU can

be set up

64

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 65/104

No custom duty on import of capital

goods, raw materials, consumables,

packing material, spares etc.

No excise duty on indigenous inputs

*Second hand capital goods can also be imported.

65

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 66/104

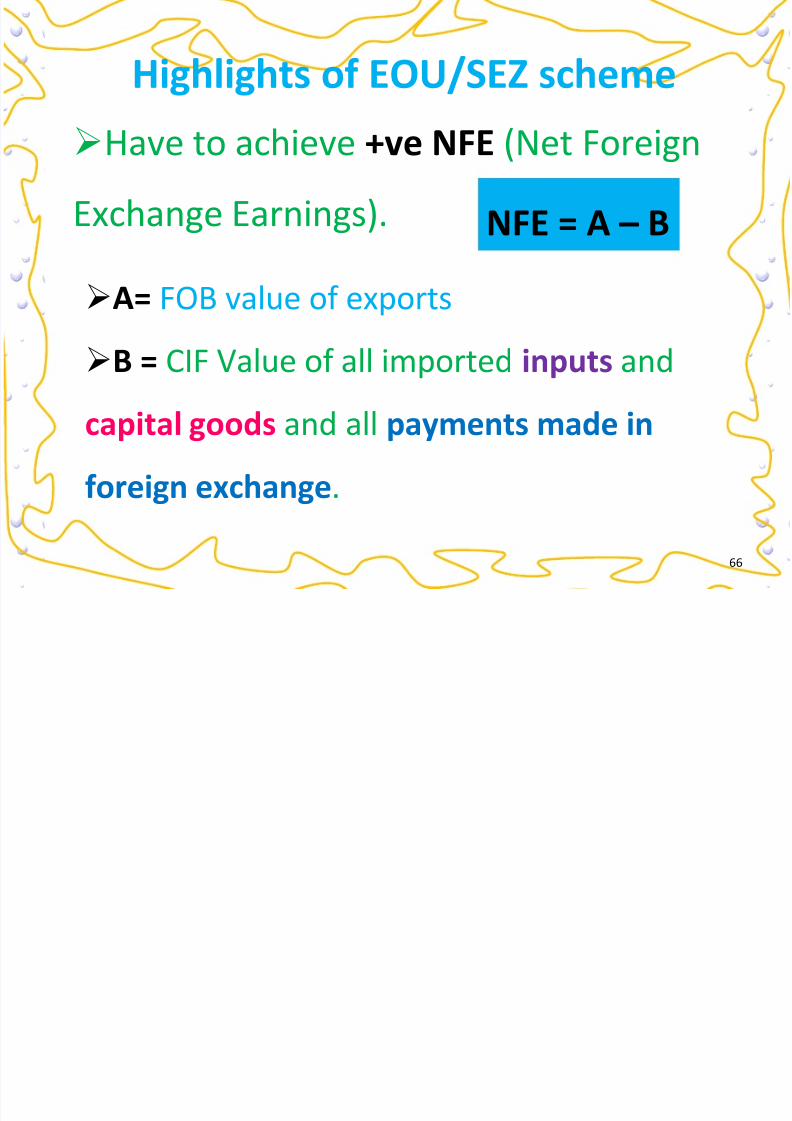

Have to achieve +ve NFE (Net Foreign

Exchange Earnings). NFE = A – B

A= FOB value of exports

B = CIF Value of all imported inputs and

capital goods and all payments made in

foreign exchange.

66

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 67/104

calculated cumulatively for 5 yrs from

commencement of commercial production

All foreign exchange outgo is included*

Requirements of +ve NFE

67

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 68/104

Capital goods

Raw materials

Consumables and spares

Dividend payable in foreign exchange

Royalty to collaborators

Design and know-how fee

Foreign exchange outgo includes…

68

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 69/104

Payment to foreign technicians

Training to Indian technicians abroad

Foreign travelInterest paid on ECB / deferred payment credit

Any other payment in foreign exchange.

69

Foreign exchange outgo includes…

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 70/104

If NFE is not achieved, duty and

interest in proportion to default will

be payable

70

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 71/104

EOUMinimum investment in plant and

machinery and building = Rs 1 crore. This

should be before commencement of

commercial production

SEZ No such limit

71

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 72/104

A bond in prescribed form has to be executed.

EOUB-17

SEZ Form prescribed in SEZ Rules, 2003

*There is NO physical supervision of customs / excise

authorities over production and clearances, BUT

prescribed records are required to be maintained.

72

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 73/104

EOU Fast Track Clearance Scheme (FTCS) for

clearances of imported consignments

SEZ customs clearance for export and import is

obtained within the zone itself

73

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 74/104

Generally, all final production should be exported,

EXCEPT rejects up to prescribed limit.

74

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 75/104

Sale within India should be on payment of excise

duty = normal customs duty (If imported)

Exceptions

In certain cases, excise duty payable

= 50%/30% of normal customs duty applicable if

goods are imported into India

75

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 76/104

SUB-CONTRACTING is allowed subject to

permission on annual basis

JOB WORK for exports is permitted

SAMPLES can be sold / given free within

prescribed limit

UNUTILISED RAW MATERIAL can be disposed of

on payment of applicable duties

76

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 77/104

The unit can EXIT (DE-BOND) with

permission of Development Commissioner,

on payment of applicable duties.

77

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 78/104

EOU Central Sales Tax (CST) paid on

purchases is refundable. Refund is obtained

from Development CommissionerSEZ Supplier DOES NOT have to pay CST

78

Highlights of EOU/SEZ scheme

/

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 79/104

Prescribed %age of foreign exchange

earnings can be retained in *EEFC account in

foreign exchange100% foreign equity is permissible, except

in a few cases*

*EEFC A/C – Exchange Earners Foreign Currency Account

79

Highlights of EOU/SEZ scheme

/

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 80/104

Supplies made to EOU by Indian supplier are

‘deemed exports’ and supplier is entitled to

benefits of ‘deemed export’

Supplies to SEZ are ‘exports’ and all export

benefits are available

80

Highlights of EOU/SEZ scheme

hl h f / h

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 81/104

Restrictions under Companies Act on

*managerial remuneration are not

applicableNo restrictions on External Commercial

Borrowings

*20 lakhs/month

81

Highlights of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 82/104

STP / EHTP UNIT

Concept of STP/EHTP is similar to EOU/SEZ.

Administered by Ministry of Information

Technology.STP/EHTP unit can be set up as an EOU unit

anywhere in India or as a SEZ unit at specified

developed locations in India.

82

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 83/104

A software development firm qualifies as

STP/EHTP unit.

Can import goods on loan from clients forspecific period.

Can export software electronically or through

physical transport.

83

STP / EHTP UNIT

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 84/104

Activities allowed…..

exports of professional services

development of computer software

data entry and conversion

data processing, analysis and control

data management

call centre services.

84

STP / EHTP UNIT

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 85/104

If your major production is towards sale in DTA

(Domestic Tariff Area), schemes like DEPB* or

DFRC* or Advance License are suitable.

Which Scheme to Choose?

* Duty Entitlement Passbook scheme (DEPB)

* Duty Free Replenishment Certificate scheme (DFRC)

85

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 86/104

Schemes like EOU/SEZ are suitable

when the undertaking is predominantly

export oriented

Requirement of imported capital goods

and raw material is high

86

EOU vs SEZ

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 87/104

‘EOU is more flexible than SEZ’

Wide choice of location (EOU unit can be

set up at any place declared as ‘warehousing

station’ under Customs Act) [300 places]

EOU can be set up even within a part of

the factory, thus saving considerable costs.

Even use of common utilities is possible.

EOU vs. SEZ

87

EOU vs SEZ

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 88/104

EOU is more flexible than SEZ

If export orders dry up, conversion of EOU

to DTA unit by exit (de-bonding) is

comparatively very easy.

In case of SEZ, the unit has to be physically

moved out of the zone after exit (de-

bonding).

EOU vs. SEZ

88

EOU vs SEZ

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 89/104

On the other hand

infrastructure available at SEZ unit is much

better than EOU units.

Customs clearance for exports is obtained

within the zone itself, which is convenient.

EOU vs. SEZ

89

Overview of EOU/SEZ scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 90/104

EOU/SEZ schemes are under Ministry of

Commerce

Basic Policy of EOU : Chapter 6 of Export

and Import Policy 2009-2014

Procedural Aspects : Chapter 6 of

Handbook of Procedures Volume I

Overview of EOU/SEZ scheme

90

Overview of EOU/SEZ Scheme

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 91/104

Prescribed Forms : Appendices to the

Handbook of Procedures

EOU units are closely connected with

Customs Law, Excise Law, Income Tax Act and

Foreign Exchange Management Act

Overview of EOU/SEZ Scheme

91

Power

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 92/104

Power generation/distribution can be set

up in EOU/STP unit.

can supply surplus power to another

EOU/STP/EHTP/SEZ unit.

Can supply surplus power to DTA unit on

payment of duty on consumables and raw

materials used for power generation

Power

92

Service Sector

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 93/104

Duty free imports will be permitted ONLY

to units exporting services and NOT to

domestic service providers

Further, NO trading units are permitted

Each EOU must have its website and e-mail

address.

Service Sector

93

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 94/104

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 95/104

PERMISSIBLE CAPITAL GOODS

material handling equipments, captive power

plants, office equipment, tools, prototypes, AC

system, computers, laptops can be brought as'capital goods' IF these are essential in

manufacture of goods

should be located in regd./administrative

office95

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 96/104

ANTI-DUMPING DUTY or SAFEGUARD DUTYNot applicable for imports by EOU or SEZ

units, UNLESS it is specifically made

applicable

96

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 97/104

CT-3 CERTIFICATEThe EOU/EHTP/STP unit can procure

indigenous material w/o payment of excise

duty.

97

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 98/104

EXPORT/IMPORT OF DEFECTIVE

INPUTS/FINAL PRODUCTS

98

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 99/104

RETURN OF REJECTED GOODS TO

INDIGENOUS SUPPLIER

99

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 100/104

INTER UNIT TRANSFER

Inter unit transfers of manufactured goods

and capital goods from one EOU/SEZ unit

to another EOU/SEZ unit w/o payment of

duty is permitted.

100

EOU All d A ti iti

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 101/104

Besides manufacturing,

(a) Import of goods for service activities

(b) Reconditioning, repairs of imported goods and

return to foreign suppliers

(c) Destruction of waste and rejects with

permission of Asstt. Commissioner even outside

the premises

EOU : Allowed Activities

101

EOU – Allowed Activities

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 102/104

SERVICE has also been included as 'export

product' as per EXIM Policy.

EOU Allowed Activities

102

Routine procedures by EOU unit

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 103/104

QUARTERLY AND ANNUAL REPORT

Submit in prescribed form to

Development Commissioner.

Routine procedures by EOU unit

103

7/29/2019 Leb Session 1

http://slidepdf.com/reader/full/leb-session-1 104/104

Maintenance of Separate Accounts

separate accounts and balance sheet of

EOU and Domestic Unit is required to claim

Income tax benefits.

Routine procedures by EOU unit

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxXXXXXXXXXXXXXXXXXXXXXxxxxxxXXXXXXXXXXXXXXXXX