Embed Size (px)

DESCRIPTION

Lecture 1 1. Introduction

Citation preview

Corporate Finance

1. Introduction

MIF/ME/MIM ● Corporate Finance/Financial Management ● 2015/2016

2

Corporate finance encompasses all of a firm’s decisions that have financial

implications

Aswath Damodaran, Corporate Finance, Theory and Practice (2nd Edition)

What is Corporate Finance?

3

I. The Financial Paradigma of the Firm

II. The Corporation and the Financial System

Summary

4

• The main objective of the corporation

I. The Financial Paradigm of the Firm

Value creation

5

• Value creation

• Can the financial function creat value on its own?

• YES

• Any financing operation allowing for a reduction in the firm´s average cost of

capital will create value on its own;

• However,

• It is also very important that the financial function helps the firm as a whole to

create value, namely by meeting the requirements allowing the firm to implement

all investment projects with a positive NPV.

I. The Financial Paradigm of the Firm

6

• Value creation

• What type of value? How can we measure value?

I. The Financial Paradigm of the Firm

The goal of financial management is to maximize the

value of the owners’ equity

Ross, Westerfield and Jaffe, Corporate Finance (9thEdition)

The objective in conventional corporate financial theory is to maximize the

value of the firm

Aswath Damodaran, Corporate Finance, Theory and Practice (2nd Edition)

Are these objectives compatible? Can the firm adopt more than one objective?

7

• Value creation

• What type of value? How can we measure value?

• Equity Value vs. Enterprise Value vs. Firm Value

• From Accounting/Book Value to Market/Substancial Value to Market Price

• The Liquidation Value

• A company balance sheet can be divided in:

I. The Financial Paradigm of the Firm

Assets ● Fixed assets ● Current assets ● Non-operating assets

Equity

Liabilities ● Debt (Interest

bearing liabilities) ● Current liabilities

(Non-interest bearing liabilities)

8

• Value creation

• What type of value? How can we measure value?

• Balance Sheet of Procter & Gamble (PG) at end of 2014

I. The Financial Paradigm of the Firm

Equity

Current Assets:

Cash and cash equivalents $ 8,558

Available-for-sale investment 2,128

Accounts receivable 6,386

Inventories 6,759

Deferred income tax 1,092

Prepaid expenses 3,845

Assets held for sale 2,849

Total current assets 31,617

Property, plant and equipment, net 22,304

Goodwill 53,704

Intangible assets, net 30,843

Other non-current assets 5,798

Total assets $ 144,266

Shareholders’ equity:

Common stock $ 69,031

Treasury stocks (75,805)

Retained earnings 84,990

Other (8,240)

Total shareholders’ equity $ 69,976

Current liabilities

Accounts payable $ 8,461

Accrued and other liabilities 8,999

Liabilities held for sale 660

Debt due within a year 15,606

Total current liabilities 33,726

Long-term debt 19,811

Deferred income tax 10,218

Other non-current liabilities 10,535

Total l iabil it ies $ 74,290

(million USD)

9

• Value creation

• What type of value? How can we measure value?

• Balance Sheet of Procter & Gamble (PG) at end of 2014 (re-arranged)

I. The Financial Paradigm of the Firm

Equity

Fixed Assets $ 106,851

Property, plant and equipment, net 22,304

Goodwill 53,704

Intangible assets, net 30,843

Currents Assets $ 32,438

Accounts receivable 6,386

Inventories 6,759

Deferred income tax 1,092

Prepaid expenses 3,845

Other non-current assets 5,798

Cash and cash equivalents (?) 8,558

Non-operating assets $ 4,317

Available-for-sale investment 2,128

Assets held for sale, net 2,189

Debt $ 35,417

Debt due within a year 15,606

Long-term debt 19,811

Shareholders’ equity $ 69,976

Common stock 69,031

Treasury stocks (75,805)

Retained earnings 84,990

Other (8,240)

Current liabilities $ 38,213

Accounts payable 8,461

Accrued and other liabilities 8,999

Deferred income tax 10,218

Other (non-current) liabilities 10,535

10

• Value creation

• What type of value? How can we measure value?

• Balance Sheet of Procter & Gamble (PG) at end of 2014 (Book Value)

I. The Financial Paradigm of the Firm

Fixed Assets $106,851

Debt $35,417

Equity $69,976

Working Capital (Current assets less current liabilities)

- $5,775

Investments Financing

Non-Operating Assets $4,317

Enterprise value

Firm value

11

• Value creation

• What type of value? How can we measure value?

• Market/Substancial Value

I. The Financial Paradigm of the Firm

Fixed Assets

Net Debt (Debt less Non-

Operating Assets)

Equity

Working Capital

Investments Financing

1 )1(ii

a

i

r

FCFFEV

1 )1(ii

e

i

r

FCFEEqV

MVNOAr

N

r

CD

n

d

n

ii

d

i

)1()1(1

12

• Value creation

• What type of value? How can we measure value?

• Market Price

• When financial markets are efficient, market price will equal market value;

I. The Financial Paradigm of the Firm

Fixed Assets

Net Debt (Debt less Non-

Operating Assets)

Equity

Working Capital

Investments Financing Nº of shares x

Share Price

(Nº of bonds x Bonds Price) -

MVNOA

E + net D

13

• Value creation

• What type of value? How can we measure value?

• Liquidation Value

• The value which would be obtained if all assets were sold and debt and

all liabilities were paid back;

• Anytime the liquidation value is persistently higher than the financial

value, the company will be worth more “dead” than staying “alive”, for

its shareholders.

I. The Financial Paradigm of the Firm

14

• Value creation

• What type of value should we maximize?

• Take into consideration the actual reality of the activity of the firm

I. The Financial Paradigm of the Firm

Managers

Shareholders

Financial Markets

Society Creditors

Shareholders have little control over managers, who thus might place their own interests above shareholders´ interests.

Managers might manipulate information in order to misinform the markets. Markets can also be wrong.

Because creditors cannot control management, they will be exposed to the risk of wealth expropriation by managers or shareholders.

Firms might jeopardize the interests of society as a whole and those costs might be difficult to allocate to firms (e.g. pollution).

Agency conflicts

15

• Value creation

• What type of value should we maximize?

I. The Financial Paradigm of the Firm

Objective: Maximize Firm Value

(Subject to complying with the ethical values related to the costs that might be imposed on society by meeting this objective)

Reduction or elimination of conflicts between the firm/management and

society.

Objective: Maximize shareholders Wealth

Objective: Maximize Equity Price

If conflicts of interest between shareholders and creditors and other stakeholders are eliminated or at least minimized.

If managers do not attempt to cheat or manipulate the markets and markets are efficient.

16

• Value creation

• What type of value should we maximize?

• Even though the main objective of the firm is to maximize firm value,

value creation may be measured by changes in stock prices, providing

that:

• Managers act in the interest of shareholders and adopt the objective of maximizing

stock prices;

• Creditors are protected against the risk of wealth expropriation by shareholders;

• Managers do not manipulate information and do not succeed in cheating the

markets (efficient markets);

• Management decisions do not impose costs (externalities) on society.

I. The Financial Paradigm of the Firm

Briefly: providing that agency conflicts are minimized.

17

• Value creation

• Advantages of adopting the objective of stock price maximization:

• Stock prices are the best observable figure amongst all other alternative

measures (in the case of listed companies).

• Contrary to net profits or sales, stock prices reflect permanently up-dated

information.

• Stock prices reflect the long-term effects of company decisions.

• Stock prices are the true measure of shareholders wealth.

• They allow for the choice of models to select the best investment projects

for the company and their best financing structure, and facilitate empirical

testing of those models.

I. The Financial Paradigm of the Firm

18

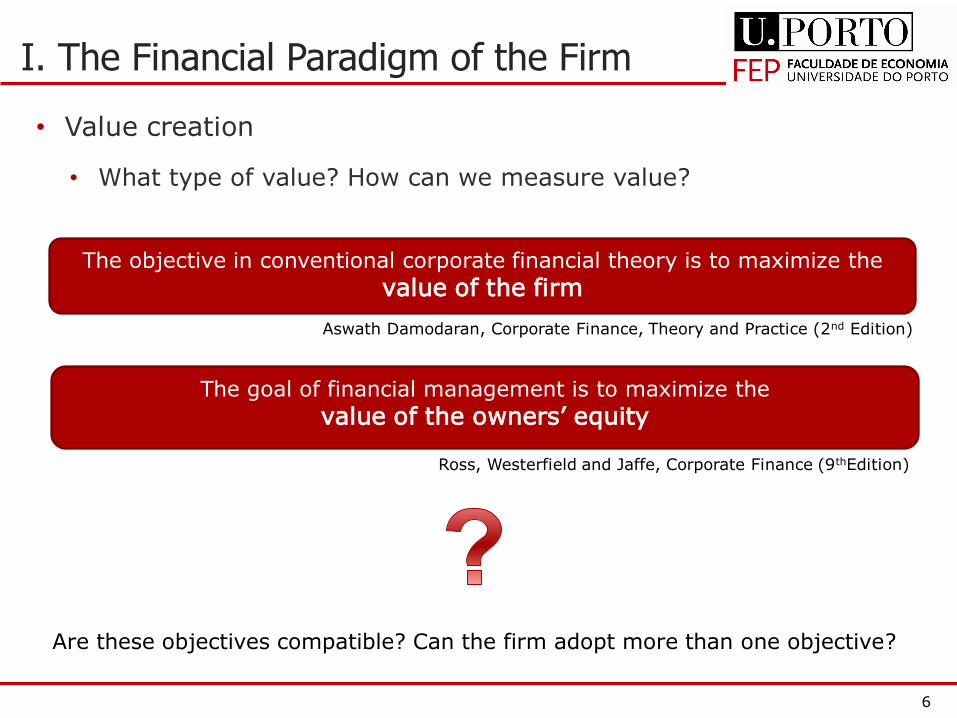

• Value creation

• How?

I. The Financial Paradigm of the Firm

Objective: Maximizing Firm Value

Investment Decisions

Invest in assets offering a return higher than the required rate of return

[hurdle rate].

Financing Decisions

Find the optimal capital mix to finance investments and the nature of debt which better meets the needs of

the corporation.

Dividend Decisions

Return to shareholders any cash exceeding investments

offering a return higher than the expected rate of

return.

The hurdle rate must reflect the investment risk

and the financing mix.

The return on the asset must

take into consideration

the amount and timing of cash-

flows

The optimal mix of equity and

debt maximizes enterprise value

The nature of debt depends

on the characteristics

of the enterprise

assets

How much cash to return will depend on

present and future

investment opportunities

Dividend policy will depend on shareholders preference for cash or stock

dividends.

19

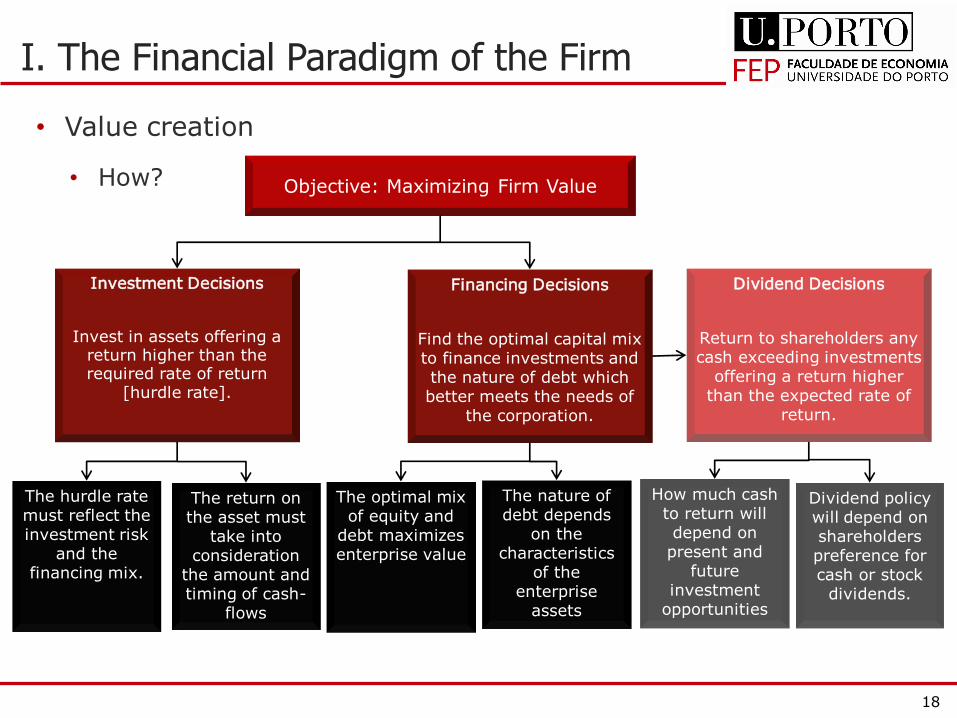

• Value creation

• Questions for which a CFO might have to provide an answer:

• Invest 25 million euros in increasing production capacity or wait for one

year to observe market demand performance?

• Implement or not a strategy of fixing [Risk Management]

• commodity prices;

• export exchange rates;

• interest rate on loans?

• How to finance the aggressive investment plan designed for the next three

years?

• Implement or not a new management incentive scheme, based on

incentives to be decided upon? [Corporate Governance]

I. The Financial Paradigm of the Firm

20

• Value creation

• Questions for which a CFO might have to provide an answer:

• To meet or not the demand of institutional investors for higher dividends?

Choose to offer stock dividends? Choose to offer stock repurchases?

• There is a merger proposal by a big telecom company. What to do? [EACC]

• Is it in the best interest of shareholders?

• What will be the reaction by foreign joint venture partners?

• Should the company remain listed in the stock market?

• Should capital structure be consolidated through an increase in equity?

I. The Financial Paradigm of the Firm

21

I. O Paradigma Financeiro da Empresa

II. The Corporation and The Financial System

Summary

22

II. The Corporation and The Financial System W

orld

The Corporation

Investment

decisions

Financing

decisions

Financial

Markets

Inve

sto

rs

Financial

Intermediaries

Direct financing

Indirect financing

Exchange of capital and financial assets

Exchange of capital

& real assets

Corporate Finance Financial Markets and

Intermediaries

Financial

Assets

23

• A Classification of Financial Markets

Fin

ancia

l M

ark

ets

Money Market

(S-T)

Capital Market

(L-T)

IMM

Commercial Paper [Corporate Debt]

Public Debt (Bills)

Equity

(Stocks)

Hybrid

Debt

(Bonds) [Government & Corporate]

Libor rates (Euribor)

Yields

Yields

Repurchase agreements

(REPO)

Sort-term bank loans

Commercial paper

Treasure bills (T-bills)

Common stocks

Preferred stocks

Convertible bonds

Warrant bonds

Perpetual bonds

Treasury bonds (T-bonds)

Corporate bonds (fixed rate &

float rate), zero-cupon

II. The Corporation and The Financial System

24

• Other important classifications of financial markets

• Primary market vs. Secondary market

• Cash market (spot market) vs. Futures market (derivatives)

• Domestic market vs. Currency market

• Domestic market vs. International market

II. The Corporation and The Financial System

25

Financial Institutions

Credit Institutions

Central

Bank Banks

Other

Intermediaries

Commercial

Banks

Savings

Banks

Investment

Banks

Leasing

Companies

Factoring

Companies

Venture

Capital

Private Equity

Holding

Companies

Dealers

Other Financial

Institutions Auxiliary Institutions

Insurance Companies

Pension Funds

Insurance Brokers

Brokers

Assets Management

Firms

Information Services

• The financial system

II. The Corporation and The Financial System

Mutual

Banks

Mutual Agro

Banks