Embed Size (px)

Citation preview

Salary – Sec 15,16,17

Lecture 7

What is salary?

• Salaries mean and include remuneration in any form due for personal service as per the contract of employment or service.

• Essential Element for Taxability of Income as Salaries is Employer Employee Relationship

• Salary, in simple words, means remuneration of a person, which he has received from his employer for rendering services to him. But receipts for all kinds of services rendered cannot be taxed as salary.

• The remuneration received by professionals like doctors, architects, lawyers etc. cannot be covered under salary since it is not received from their employers but from their clients. So, it is taxed under business or profession head.

Characteristic of Salary

1. The relationship of payer and payee must be of employer and employee for an income to be categorized as salary income. For example: Salary income of a Member of Parliament cannot be specified as salary, since it is received from Government of India which is not his employer.

2. The Act makes no distinction between salary and wages, though generally salary is paid for non-manual work and wages are paid for manual work.

3. Salary received from employer, whether one or more than one is included in this head.

4. Salary is taxable either on due basis or receipt basis which ever matures earlier:

i) Due basis – when it is earned even if it is not received in the previous year.

ii) Receipt basis – when it is received even if it is not earned in the previous year.

iii) Arrears of salary- which were not due and received earlier are taxable when due or received, which ever is earlier.

5. Compulsory deduction from salary such as employees’ contribution to provident fund, deduction on account of medical scheme or staff welfare scheme etc. are examples of instances of application of income. In these cases, for computing total income, these deductions have to be added back.

Components of Salary1. Salaries, wages and advance against salary / wages2. Annuity / pension3. Gratuity4. Fees/ commission5. Perquisites6. Profits in lieu of / in addition to salaries/ wages7. Incentive/ bonus8. Contribution made by Central Government or any other employer in the

account of the employee under new pension scheme effective 1.4.049. Leave encashment10. Allowances11. Annual accretion in RPF to the extent taxable12. Transferred balance to a RPF to the extent taxable

To sum up, it is the gross salary that will be taxed and not the net received by the employee

Allowances• Allowances not charged to tax are Allowance to Government Employees outside India : is

exempt u/s 10 (7)

Allowance to High Court or Supreme Court Judges u/s is also exempt

Allowance paid by United Nations Organization-Exempt by virtue of Section 2 of United Nations (Privileges and Immunities) Act, 1974

Compensatory allowance under Article 222(e) of the Constitution of India received by a Judge- Exempt from tax.

• Transfer Allowance granted to meet the cost of travel on tour or on transfer including any sum paid for transfer, packing and transportation of personal effects on such transfer

• Tour/ Travelling Allowance whether granted on tour of for the period of journey to meet the ordinary daily charges incurred by an employee on account of absence from his normal place of duty;

• Conveyance Allowance granted to meet the expenditure incurred on conveyance in performance of duties of an office or employment of profit,

• Helper Allowance granted to meet the expenditure incurred on a helper where such helper is engaged for performance of the duties of an office or employment of profit

• Research Allowance granted for encouraging the academic, research and training pursuits in educational and research institutions;

• Uniform Allowance granted to meet the expenditure on the

purchase or maintenance of uniform for wear during the performance of duties of an office or employment of profit

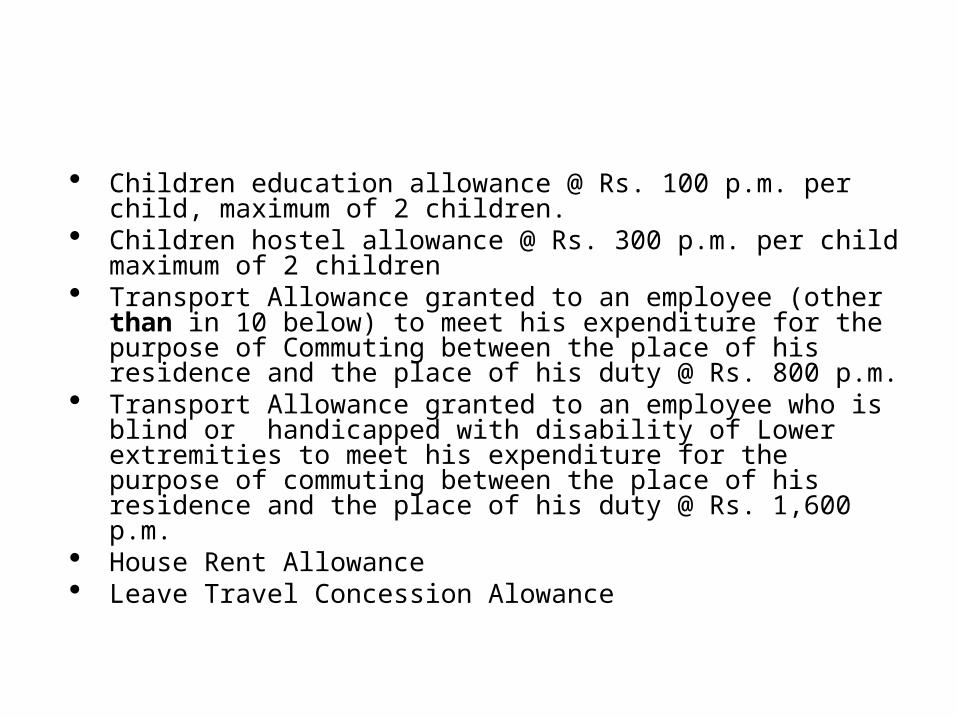

Children education allowance @ Rs. 100 p.m. per child, maximum of 2 children.

Children hostel allowance @ Rs. 300 p.m. per child maximum of 2 children

Transport Allowance granted to an employee (other than in 10 below) to meet his expenditure for the purpose of Commuting between the place of his residence and the place of his duty @ Rs. 800 p.m.

Transport Allowance granted to an employee who is blind or handicapped with disability of Lower extremities to meet his expenditure for the purpose of commuting between the place of his residence and the place of his duty @ Rs. 1,600 p.m.

House Rent Allowance Leave Travel Concession Alowance

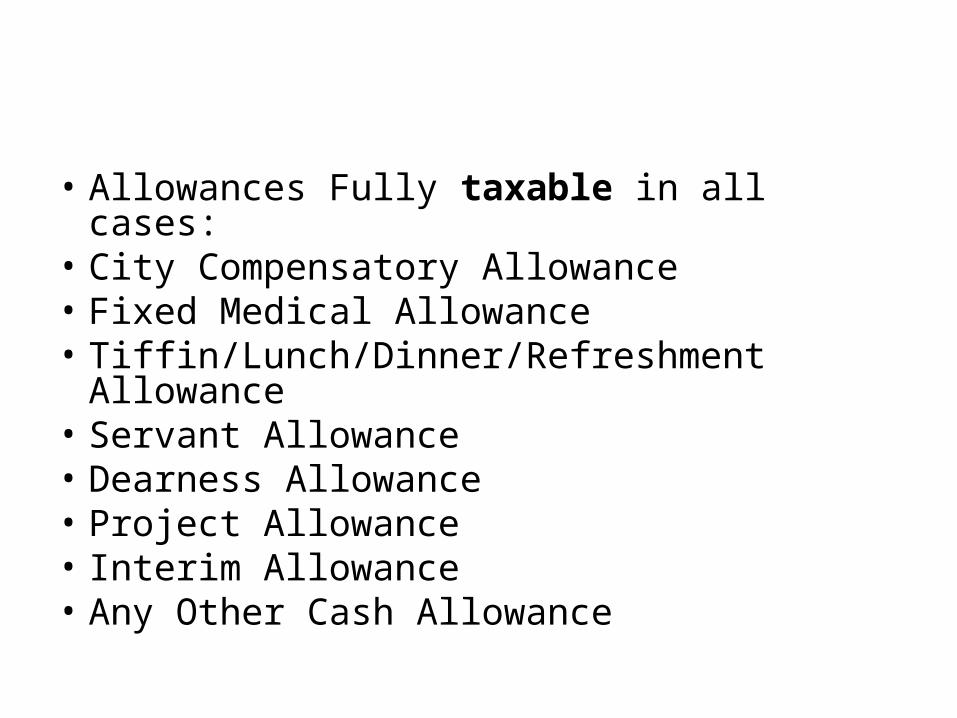

• Allowances Fully taxable in all cases: • City Compensatory Allowance • Fixed Medical Allowance • Tiffin/Lunch/Dinner/Refreshment Allowance • Servant Allowance • Dearness Allowance • Project Allowance • Interim Allowance • Any Other Cash Allowance

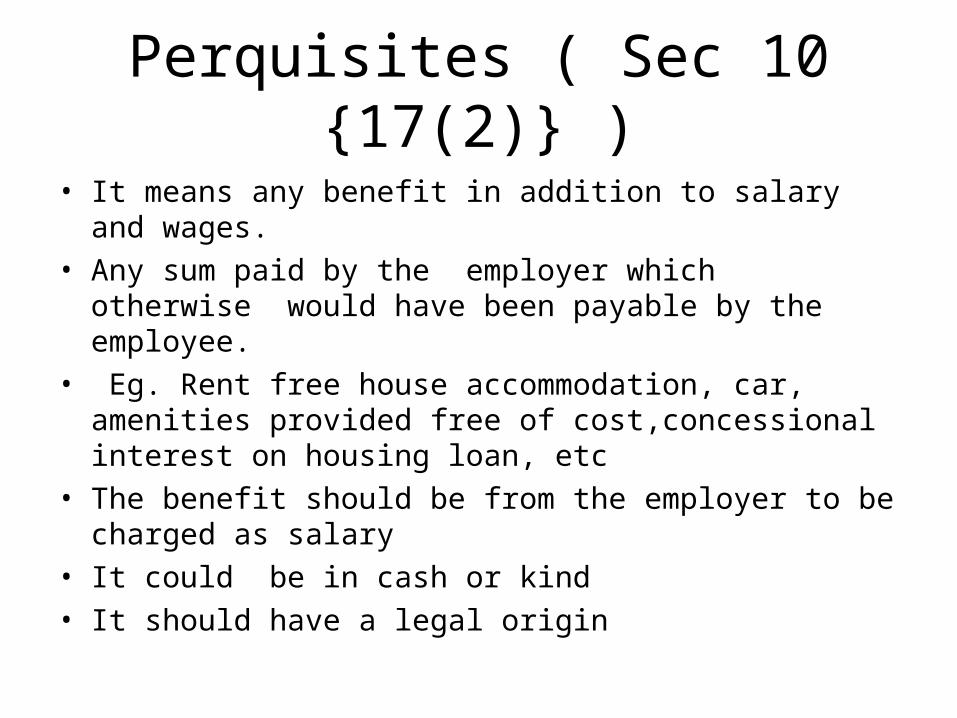

Perquisites ( Sec 10 {17(2)} )

• It means any benefit in addition to salary and wages. • Any sum paid by the employer which otherwise would have

been payable by the employee.• Eg. Rent free house accommodation, car, amenities provided

free of cost,concessional interest on housing loan, etc• The benefit should be from the employer to be charged as

salary• It could be in cash or kind• It should have a legal origin

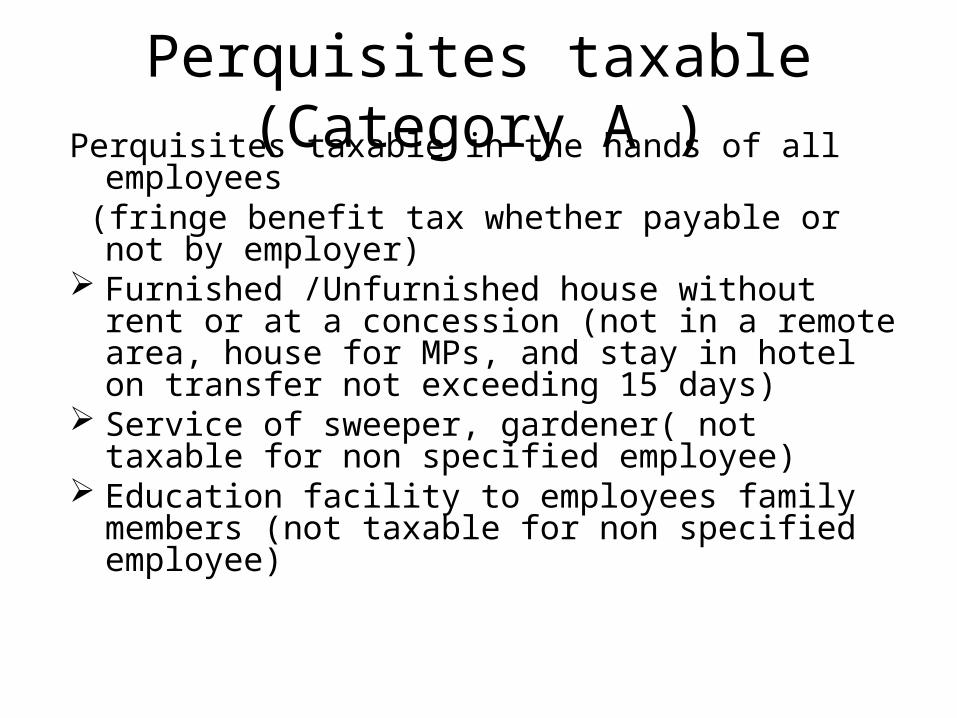

Perquisites taxable (Category A )Perquisites taxable in the hands of all employees (fringe benefit tax whether payable or not by

employer) Furnished /Unfurnished house without rent or

at a concession (not in a remote area, house for MPs, and stay in hotel on transfer not exceeding 15 days)

Service of sweeper, gardener( not taxable for non specified employee)

Education facility to employees family members (not taxable for non specified employee)

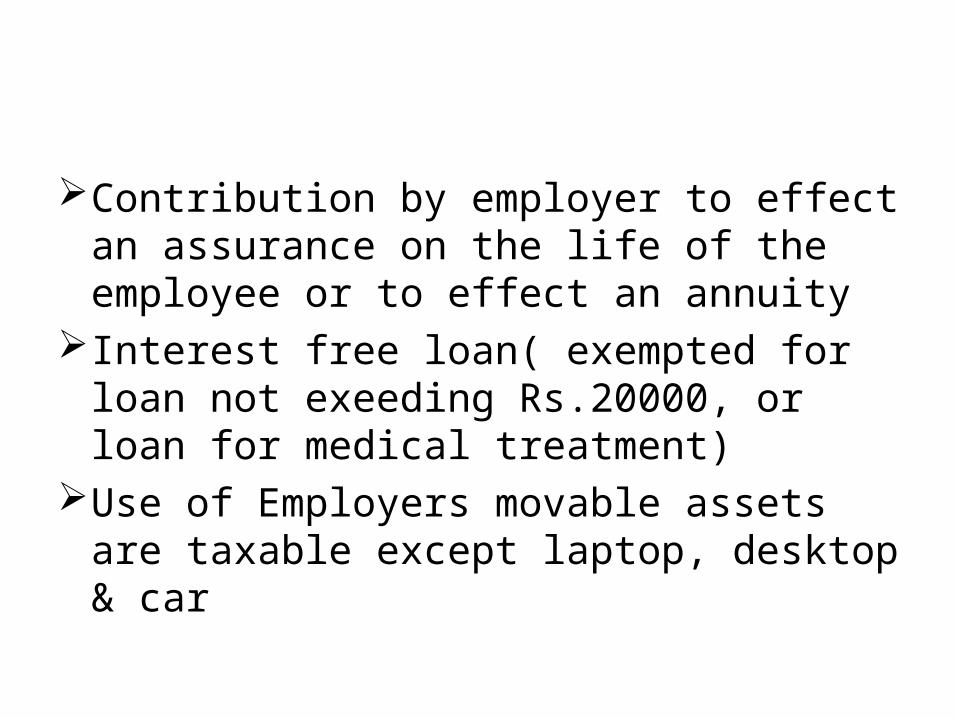

Contribution by employer to effect an assurance on the life of the employee or to effect an annuity

Interest free loan( exempted for loan not exeeding Rs.20000, or loan for medical treatment)

Use of Employers movable assets are taxable except laptop, desktop & car

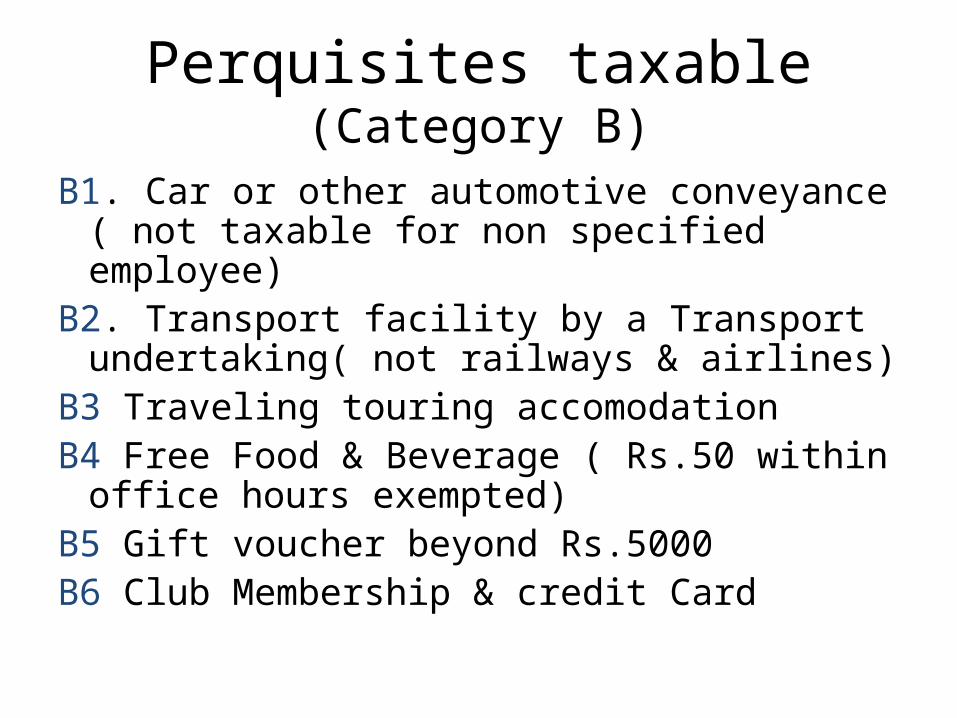

Perquisites taxable (Category B)

B1. Car or other automotive conveyance ( not taxable for non specified employee)

B2. Transport facility by a Transport undertaking( not railways & airlines)

B3 Traveling touring accomodationB4 Free Food & Beverage ( Rs.50 within office

hours exempted)B5 Gift voucher beyond Rs.5000B6 Club Membership & credit Card

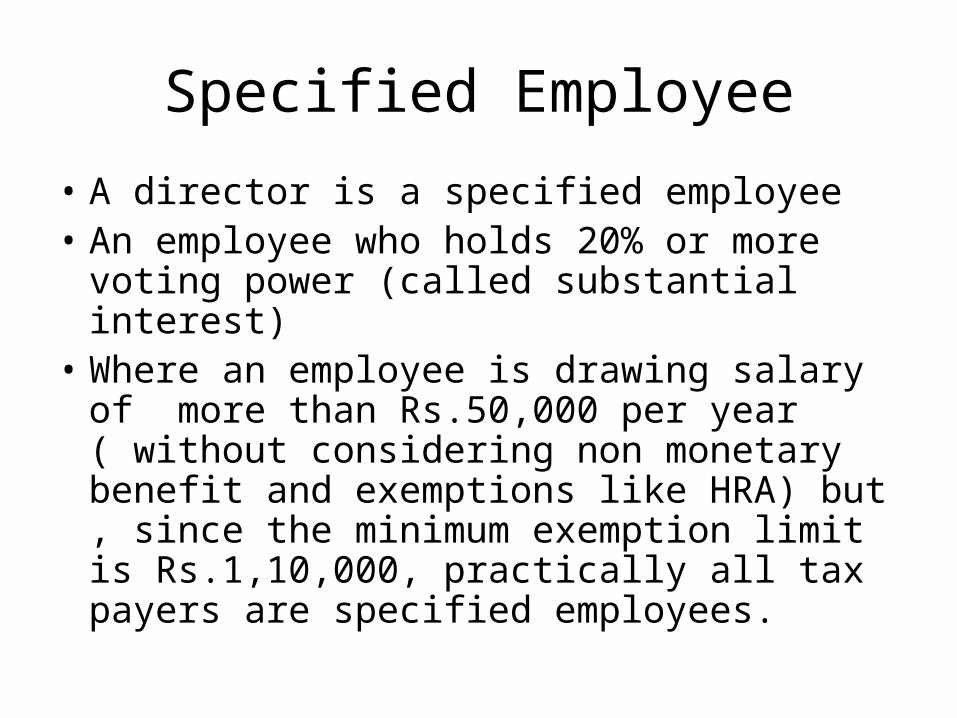

Specified Employee

• A director is a specified employee• An employee who holds 20% or more voting

power (called substantial interest)• Where an employee is drawing salary of more

than Rs.50,000 per year ( without considering non monetary benefit and exemptions like HRA) but , since the minimum exemption limit is Rs.1,10,000, practically all tax payers are specified employees.

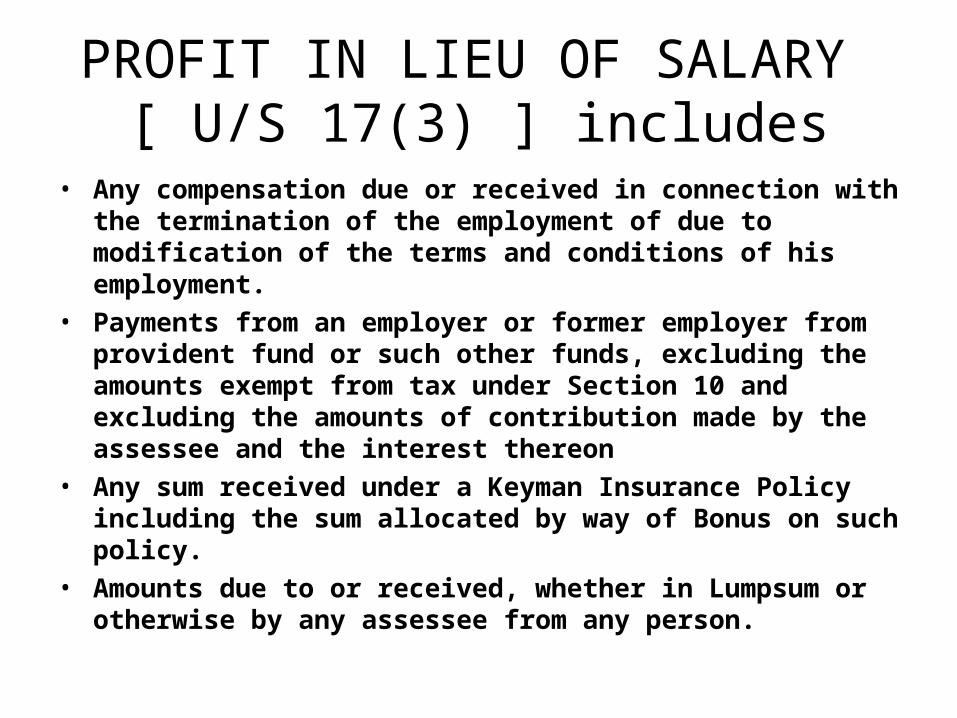

PROFIT IN LIEU OF SALARY [ U/S 17(3) ] includes

• Any compensation due or received in connection with the termination of the employment of due to modification of the terms and conditions of his employment.

• Payments from an employer or former employer from provident fund or such other funds, excluding the amounts exempt from tax under Section 10 and excluding the amounts of contribution made by the assessee and the interest thereon

• Any sum received under a Keyman Insurance Policy including the sum allocated by way of Bonus on such policy.

• Amounts due to or received, whether in Lumpsum or otherwise by any assessee from any person.

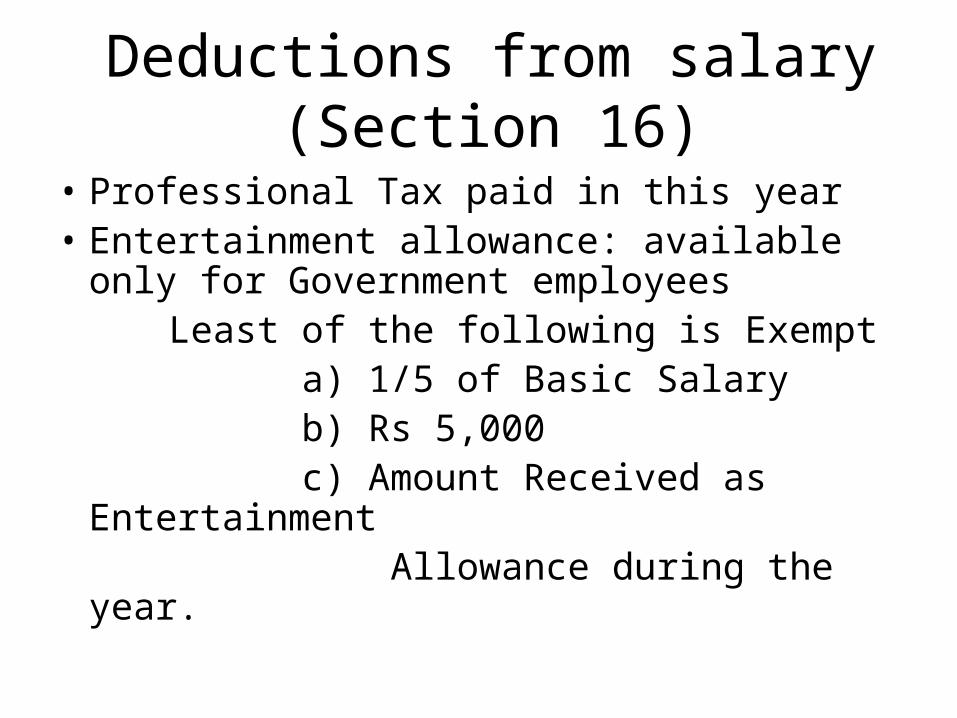

Deductions from salary (Section 16)

• Professional Tax paid in this year• Entertainment allowance: available only for

Government employees Least of the following is Exempt a) 1/5 of Basic Salary b) Rs 5,000 c) Amount Received as Entertainment Allowance during the year.

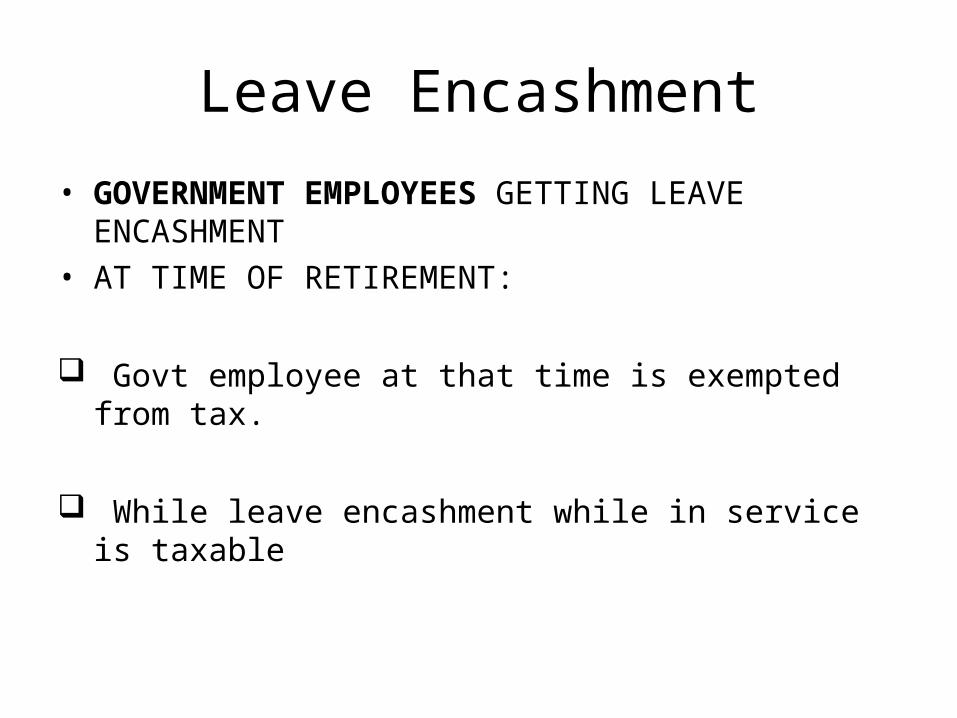

Leave Encashment

• GOVERNMENT EMPLOYEES GETTING LEAVE ENCASHMENT • AT TIME OF RETIREMENT:

Govt employee at that time is exempted from tax.

While leave encashment while in service is taxable

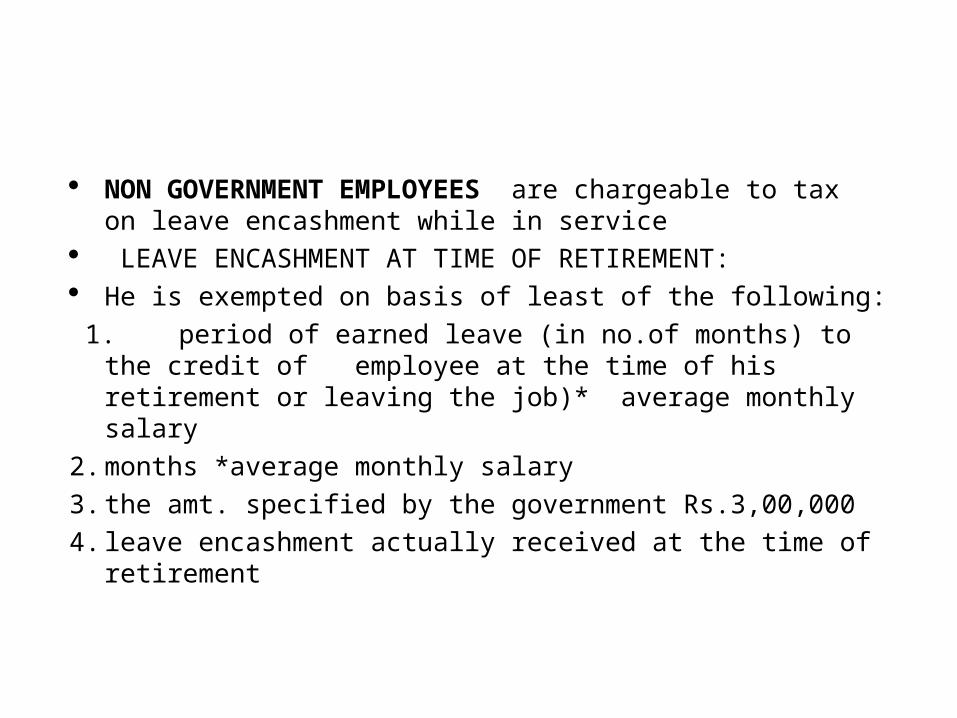

NON GOVERNMENT EMPLOYEES are chargeable to tax on leave encashment while in service

LEAVE ENCASHMENT AT TIME OF RETIREMENT: He is exempted on basis of least of the following: 1. period of earned leave (in no.of months) to the credit of

employee at the time of his retirement or leaving the job)* average monthly salary

2. months *average monthly salary3. the amt. specified by the government Rs.3,00,000 4. leave encashment actually received at the time of

retirement

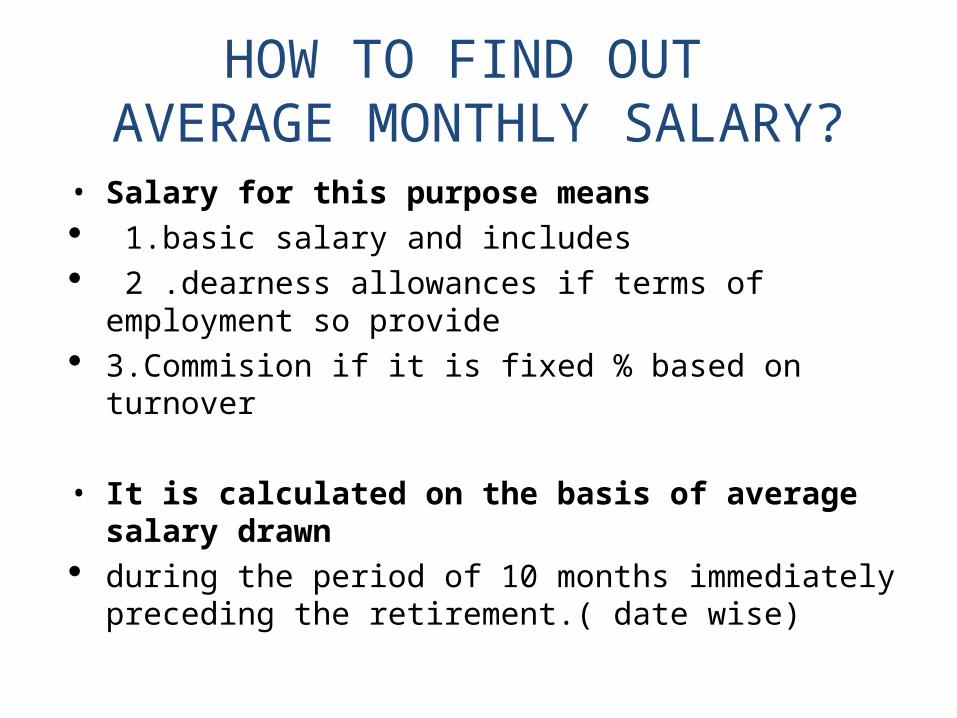

HOW TO FIND OUT AVERAGE MONTHLY SALARY?

• Salary for this purpose means 1.basic salary and includes 2 .dearness allowances if terms of employment so

provide 3.Commision if it is fixed % based on turnover

• It is calculated on the basis of average salary drawn during the period of 10 months immediately

preceding the retirement.( date wise)

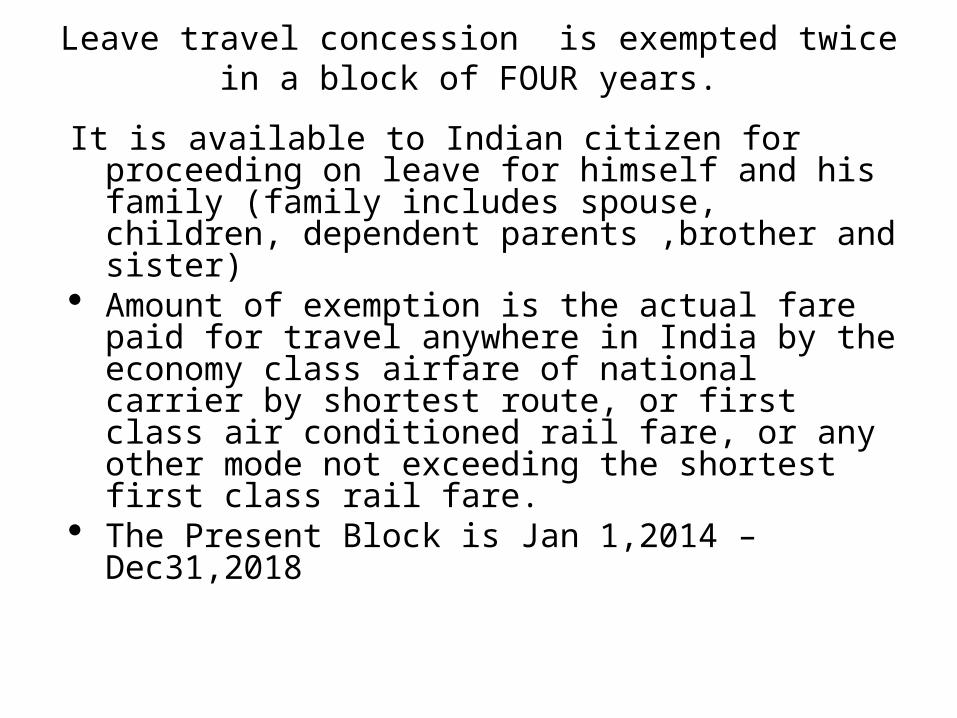

Leave travel concession is exempted twice in a block of FOUR years.

It is available to Indian citizen for proceeding on leave for himself and his family (family includes spouse, children, dependent parents ,brother and sister)

Amount of exemption is the actual fare paid for travel anywhere in India by the economy class airfare of national carrier by shortest route, or first class air conditioned rail fare, or any other mode not exceeding the shortest first class rail fare.

The Present Block is Jan 1,2014 – Dec31,2018

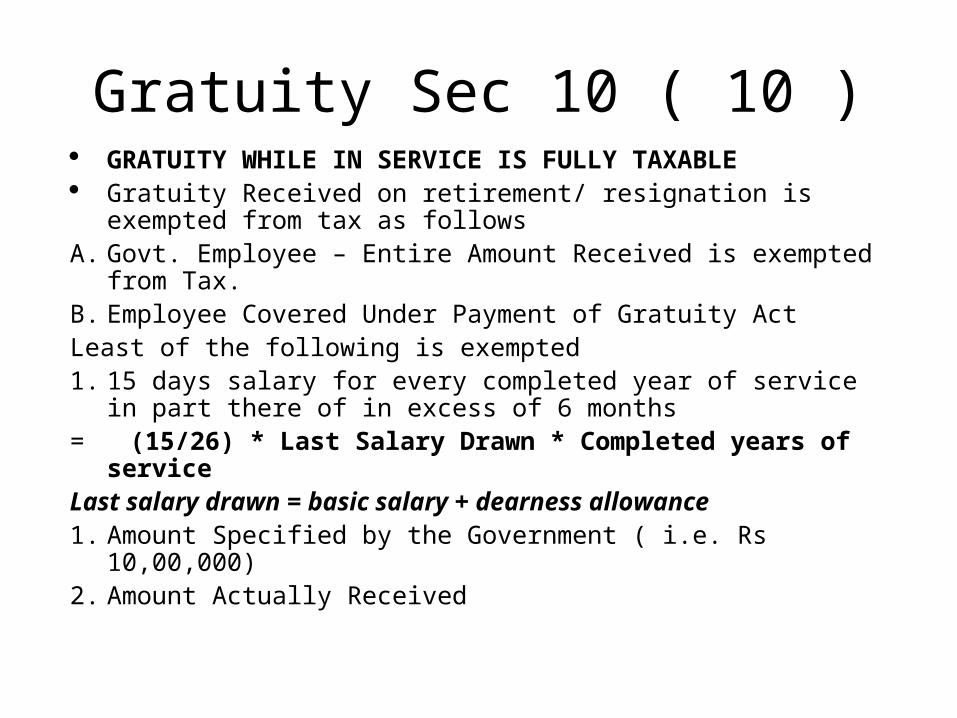

Gratuity Sec 10 ( 10 ) GRATUITY WHILE IN SERVICE IS FULLY TAXABLE Gratuity Received on retirement/ resignation is exempted from

tax as followsA. Govt. Employee – Entire Amount Received is exempted from Tax.B. Employee Covered Under Payment of Gratuity ActLeast of the following is exempted1. 15 days salary for every completed year of service in part there of

in excess of 6 months= (15/26) * Last Salary Drawn * Completed years of serviceLast salary drawn = basic salary + dearness allowance1. Amount Specified by the Government ( i.e. Rs 10,00,000)2. Amount Actually Received

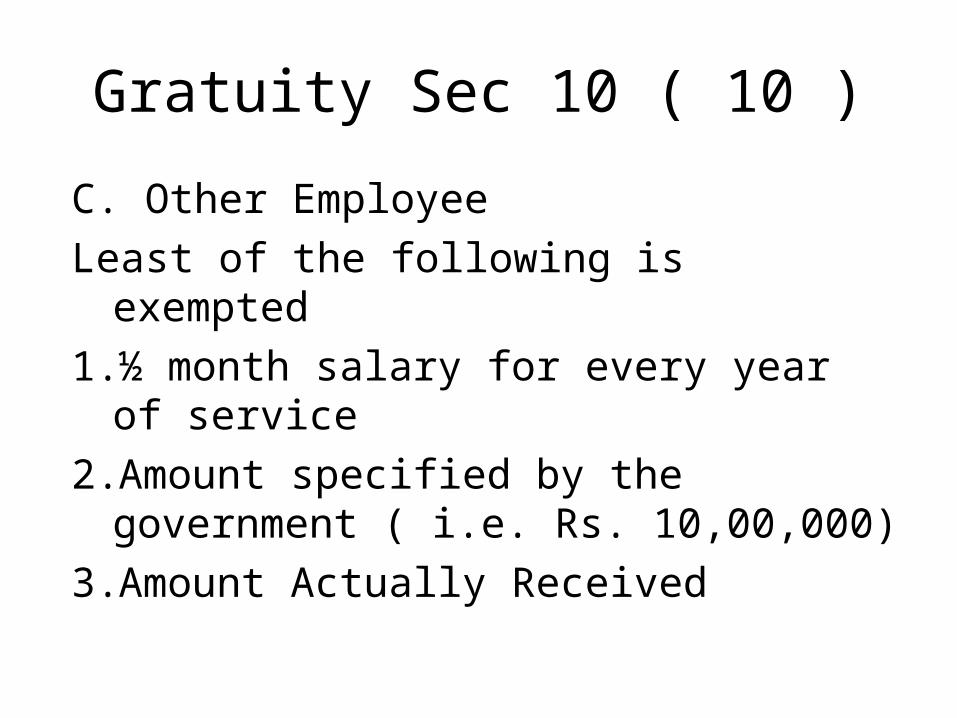

Gratuity Sec 10 ( 10 )

C. Other EmployeeLeast of the following is exempted1. ½ month salary for every year of service2. Amount specified by the government ( i.e.

Rs. 10,00,000)3. Amount Actually Received

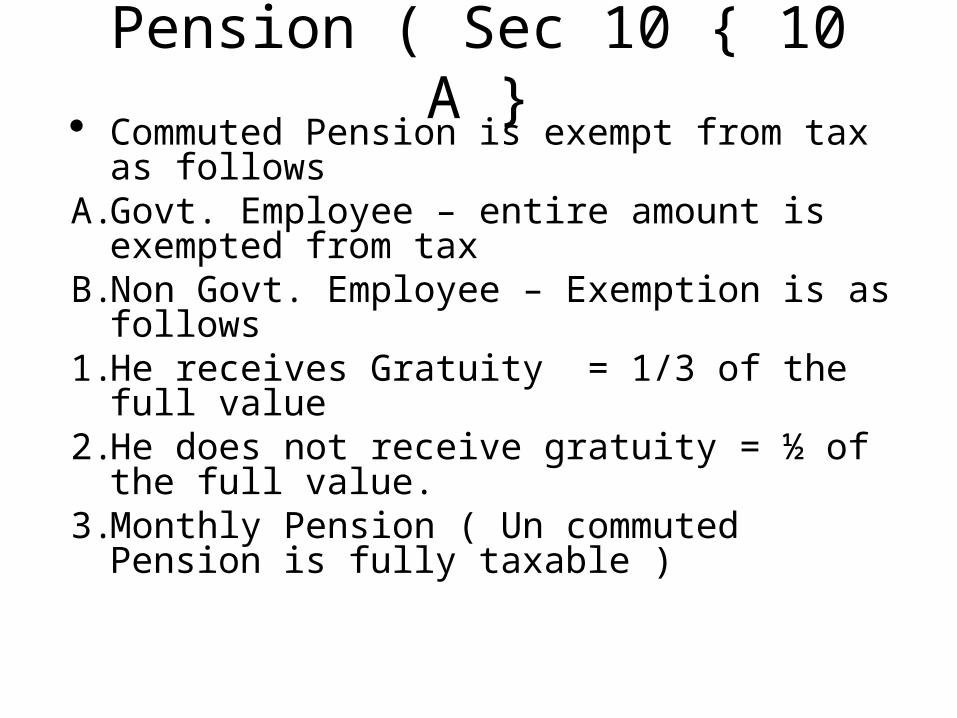

Pension ( Sec 10 { 10 A } Commuted Pension is exempt from tax as

followsA. Govt. Employee – entire amount is exempted

from taxB. Non Govt. Employee – Exemption is as follows1. He receives Gratuity = 1/3 of the full value2. He does not receive gratuity = ½ of the full

value.3. Monthly Pension ( Un commuted Pension is

fully taxable )

THANK YOU