Embed Size (px)

Citation preview

Lecture ?:Lecture ?:MonopolyMonopoly

EEP 1EEP 1

Peter Berck’s ClassPeter Berck’s Class

Who is this guy who Who is this guy who thinks he’s funny?thinks he’s funny?

Maximilian AuffhammerMaximilian Auffhammer

Assistant Professor IAS/AREAssistant Professor IAS/ARE

[email protected]@berkeley.edu

Let’s Deviate From Perfect Let’s Deviate From Perfect CompetitionCompetition

– No Market Power– Perfect Information– No Externalities– No Public Goods

– Look at Market Power first.

MonopolyMonopoly

• Monopolist: Only supplier of a good with no close substitute.

– Firm output = Market output– Firm faces market demand curve, not a

horizontal residual demand• Does not lose all sales if price increases• Faces downward sloping demand

MonopolyMonopoly

• Firm can “set price” within some reasonable range and will still sell goods

• Monopolist is a regular profit maximizing firm:

– MR(Q) = MC(Q)

What is Marginal RevenueWhat is Marginal Revenue

• For a perfectly competitive firm:– Marginal Revenue = Average Revenue =

Price

• For the monopolist: Price is no longer exogenous. Price depends on Q, which is the monopolists output choice

• Average Revenue = (P(Q)xQ)/Q = P(Q)

Average Revenue is not equal to Average Revenue is not equal to Marginal Revenue for the Marginal Revenue for the

Monopolist!!!!Monopolist!!!!

Convenient FactConvenient Fact

• If inverse Demand is linear: – P(Q) = a – bQ– MR(Q) = a – 2bQ

• Same intercept as inverse demand• Twice the slope of the inverse demand• MR hits Q axis “half way”

• Can we show this? Yes!!!!

• If MR = p, demand is perfectly elastic

Where does the monopolist Where does the monopolist produce?produce?

The Monopoly DecisionThe Monopoly Decision

Market PowerMarket Power

• Market Power is the ability of a firm to charge a price above marginal cost profitably.

• Degree of market power depends on elasticity of demand curve at the profit maximizing quantity.

Measure of Market Power: The Measure of Market Power: The Lerner IndexLerner Index

• MR(Q*) = MC(Q*)• Lerner Index: (p- MC)/p• If firm is profit maximizing:

– (p-MC)/p = -1/d

– Ranges from 0 to 1– If p=MC Lerner Index = 0 Perfect Competition

• The more elastic the demand curve, the smaller the markup a monopolist is able to charge.

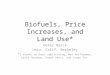

0

5

10

15

20

25

30

35

40

45

0 10 20 30 40 50 60

Output (Q)

$

MC

Qm

The thick solid line is the more inelastic demand curve.The dashed solid line is the corresponding Marginal Revenue Curve

The thin solid line is the more elastic demand curve,The thin dashed line is the corresponding Marginal Revenue Curve.

For both demadn curves the monopolists profit maximizing output is whereMR = MC, which is 10 units and MC at this point is 20 $.

The monopolist would charge 30 $ if the market demand is less elastic at any given quantity. He would charge $30 to the more inelastic demand, yet onlyroughly $23 to the more elastic demand.

Note: For both demand curves the monopolist produces in the elastic section of the demand curve!!!

P(Q)1

MR(Q)1

P(Q)2MR(Q)2

~23

Demand Elasticity and Monopolist's Markup

Sources of Market PowerSources of Market Power

• Demand is inelastic if:– Consumers are willing to pay virtually

anything for a good– No close substitutes– No entry– Similar firms are far away– Other firms products are very different.