Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Lender Recovery in Bankruptcy: Pre-Petition

Default Interest, Pre-Payment Penalties,

Late Fees, OID, Attorney Fees Maximizing Recovery of Secured Lender's Remedies in the Loan Documentation

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JUNE 17, 2015

Presenting a live 90-minute webinar with interactive Q&A

Michael J. Riela, Shareholder, Vedder Price, New York

Dustin P. Smith, Esq., Hughes Hubbard & Reed, New York

Kevin Walsh, Member, Mintz Levin Cohn Ferris Glovsky and Popeo, Boston

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-328-9525 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about CLE credit processing call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Mintz Levin. Not your standard practice.

Secured Creditor Recoveries

Make-Whole Provisions in Bankruptcy

By: Kevin J. Walsh, Esq.

5

What is a Make-Whole Provision?

Make-Whole provision requires payment of a premium for a

borrower to voluntarily repay debt prior to its stated maturity.

Designed to compensate lender for the loss of future return in

the event of early repayment of the loan.

Typically calculated to compensate for loss of interest they would

have received had the loan not been repaid early.

Typically consists of a formula to estimate the amount of lost

interest.

Make-Wholes are generally enforceable outside of

bankruptcy.

6

Make-Wholes differ from No-Calls.

No-Call restricts a borrower from refinancing the debt before

maturity or for a stated period of time.

Make-Whole payments typically are not applicable during a No-

Call period.

Some loan documents provide for both types of provisions.

o Prohibit prepayment for a certain period.

o Permit prepayment thereafter subject to the prepayment premium.

No-Calls are generally enforceable outside of bankruptcy.

No-Calls are usually not enforceable in bankruptcy.

May be a claim for damages for breach in bankruptcy.

What is a Make-Whole Provision? (cont.)

7

How Do Make-Wholes work?

Make-Wholes allow a borrower to repay a loan before maturity

in order to take advantage of declining interest rates.

Make-Wholes provide yield protection for lenders whose loans

are paid prior to maturity in a declining rate market to

compensate lender for the loss of investment return.

Make-Wholes are a modification to the “perfect tender in

time” rule found in many jurisdictions that prohibits a borrower

from repaying a loan before the stated maturity.

8

Make-Wholes in bond documents are typically expressed as a

formula based on the NPV of the remaining amount that would

be due under the agreement discounted against an index

(e.g., Treasuries) plus a premium basis point amount.

The formula is designed to approximate actual damages to the

lender for the loss of future yield.

Make-Wholes in loan agreements are typically expressed as a

fixed percentage fee that may decline over time.

Generally unrelated to actual damages incurred by the lender.

How Do Make-Wholes work? (cont.)

9

Enforceability of Make-Wholes in Bankruptcy

Most courts analyze the enforceability of Make-Whole

provisions under a two-step approach:

Is the Make-Whole provision enforceable under applicable state

law?

If yes, must the claim be disallowed under the Bankruptcy Code?

Analysis begins with the language of the loan documents.

Does the loan agreement/indenture include clear and

unambiguous language requiring payment of the prepayment

premium on default and acceleration?

10

Was the provision triggered prepetition?

Does the provision require payment of the premium upon the

acceleration of the debt due to the bankruptcy filing?

Typical provisions do not specifically require payment of a

premium upon default and automatic acceleration as occurs

upon a bankruptcy filing. This act moves the maturity date to the

bankruptcy petition date and courts generally regard payment at

or after that time as a repayment after maturity rather than

prepayment before maturity.

Enforceability of Make-Wholes in Bankruptcy (cont.)

11

Does the document permit the lender to decelerate

accelerated debt?

Automatic stay likely applies to prevent postpetition deceleration.

Is the premium due on default and acceleration?

Is the premium due on automatic acceleration?

Does the contractual language specifically exclude the

payment of the premium upon bankruptcy acceleration?

Is the debt deemed matured on acceleration such that any

subsequent payment will not be a prepayment?

Enforceability of Make-Wholes in Bankruptcy (cont.)

12

Is the premium liquidated damages or a penalty?

Premium will be considered an unenforceable penalty unless (i)

actual damages represented by the premium are difficult to

calculate, and (ii) the premium amount is not plainly

disproportionate to the possible loss.

Most court find that Make-Wholes are liquidated damages rather

than penalties.

Enforceability of Make-Wholes in Bankruptcy (cont.)

13

Is the Make-Whole premium unmatured interest that is

disallowed under section 502(b)(2) of the bankruptcy code?

Majority view is that the premium is not unmatured interest, but

rather charges that fully matured on the petition date.

Is the Make-Whole premium allowable postpetition interest

under section 506(b) of the bankruptcy code?

Was the Make-Whole triggered postpetition?

Is the lender oversecured and entitled to such interest?

Any issue with the reasonableness of the premium?

o Likely allowed if premium is not a penalty under state law.

Enforceability of Make-Wholes in Bankruptcy (cont.)

14

Is the debtor solvent?

If yes, enforceability of Make-Wholes generally dependent solely

with reference to state law.

If no, the bankruptcy issues above will be analyzed.

Enforceability of Make-Wholes in Bankruptcy (cont.)

15

Tips for enforceable Make-Wholes

Use clear and unambiguous language to specify when

borrowers are responsible for paying make-whole premiums.

Provide that the premium is due upon default and acceleration,

including acceleration upon the filing of bankruptcy.

Provide that premium is due on prepayment even if during a no-

call period.

Try to approximate actual damages to the lender when

formulating the amount of the make-whole premium.

16

State in the document that the premium is liquidated damages

and not unmatured interest or a prepayment penalty.

State in the document that the premium is a reasonable

approximation of damages for prepayment, which damages

are difficult to calculate at the time of the transaction.

Include the premium as part of the debt (i.e., the principal

amount) owed that is subject to any security interest and lien in

favor of the lender.

Tips for enforceable Make-Wholes (cont.)

17

Include the premium as part of any damages owed by

borrower on account of any breach of the Make-Whole

provision.

Ensure that the remedies provisions are cumulative to the

extent permitted by law.

Tips for enforceable Make-Wholes (cont.)

19

In re Calpine Corp. (Calpine I)

365 B.R. 392 (Bankr. S.D.N.Y. 2007)

Solvent debtor; lenders oversecured.

Proposed DIP loan would save debtors approximately $92

million a year in interest after prepetition loan was refinanced.

Debt refinanced prior to expiration of no-call.

Court held that no-calls are unenforceable in bankruptcy.

Indentures did not require make-whole premium during no-call

period.

20

Indentures provided default and automatic acceleration upon

bankruptcy – debt matured at that point so any subsequent

payment was after maturity and not a prepayment.

Indentures did not provide for liquidated damages for

payment during no-call period – therefore no claim under

506(b).

Court did award expectation damages for breach of the

Indentures in the amount equal to the respective prepayment

premiums, but as unsecured claims.

In re Calpine Corp. (Calpine I)

365 B.R. 392 (Bankr. S.D.N.Y. 2007) (cont.)

21

In re Calpine Corp. (Calpine II)

2010 U.S. Dist. LEXIS 96792 (S.D.N.Y.)

No liability for breach of provisions that are rendered

unenforceable under bankruptcy law.

Lenders could have had premiums during the no-call period if

the Indentures had required them.

Damages equal to the full amount of interest due over the life

of the loans but not yet due as of the petition date is

unmatured interest that is disallowed under section 502(b)(2) of

the bankruptcy code.

22

Lenders, even though oversecured, did not have a claim

under section 506(b) of the bankruptcy code.

Lenders have no allowed claim under section 502, which is a

threshold issue for allowance of a claim under section 506.

The Indentures provide for interest payments over the life of the

loans, they do not provide for a “charge” equal to the lost interest

payments in the context of a bankruptcy filing.

In re Calpine Corp. (Calpine II)

2010 U.S. Dist. LEXIS 96792 (S.D.N.Y.) (cont.)

23

In re Solutia Inc.

379 B.R. 473 (Bankr. S.D.N.Y. 2007)

Insolvent debtor; lenders were oversecured.

“Premium” sought was approximately $60 million.

Indentures provided for default and automatic acceleration

upon bankruptcy.

Indentures did not permit deceleration unless acceleration was

by notice as opposed to automatic. In any event, the court

held that any attempt to decelerate would violate the

automatic stay.

24

Court found that acceleration moves the maturity date from

the original date to the acceleration date. The acceleration

date become the new maturity date. Accordingly, any

payment after acceleration is a repayment and not a

prepayment.

By agreeing to automatic acceleration without providing for a

premium upon such occurrence, lenders agreed to give up

the future stream of payments in favor of the immediate right

to collect the entire debt.

In re Solutia Inc.

379 B.R. 473 (Bankr. S.D.N.Y. 2007) (cont.)

25

In re Chemtura Corp.

439 B.R. 561 (S.D.N.Y. 2010)

Analysis occurred in consideration of whether a proposed

settlement satisfied the “range of reasonableness” standard.

Settlement on Make-Whole and No-Call was $50 million (42% of

contractual amount) and $20 million (39% of contractual

amount), respectively.

Court noted that the Indentures did not specifically provide for

payment of a premium upon bankruptcy default and

automatic acceleration.

26

Indentures defined “Maturity” “Maturity Date” and “Stated

Maturity” and provided for premium payment if paid before

the “Maturity Date”. Automatic acceleration only affected

Maturity and not Maturity Date.

Discussed likelihood of disallowing make-whole and no-call

amounts as unmatured interest if dealing with an insolvent

debtor.

In re Chemtura Corp.

439 B.R. 561 (S.D.N.Y. 2010) (cont.)

27

Acceleration of the debt, and therefore the maturity,

precluded a subsequent voluntary prepayment. Any payment

would be a repayment.

Court would not permit lenders to decelerate the debt as

violative of the automatic stay.

Court concluded that entitlement to make-whole payments is

a matter of contract, not policy.

Court disagreed that debtors' election under section1110

decelerated the debt.

In re Chemtura Corp.

439 B.R. 561 (S.D.N.Y. 2010) (cont.)

28

In re Premier Entertainment Biloxi LLC

445 B.R. 582 (Bankr. S.D. Miss. 2010)

Solvent debtor; lenders were oversecured.

Automatic acceleration upon bankruptcy moved the maturity

date to the petition date.

Indenture does not expressly grant right to a premium after

acceleration or during the no-call period.

Allowed damages for breach of no-call because debtor was

solvent.

Indenture provided that '[a]ll remedies are cumulative to the extent

permitted by law," allowing for common law breach award.

29

In re Trico Marine Services

450 B.R. 474 (Bankr. D. Del. 2011)

Lenders were unsecured, but had a secured guaranty from

MARAD that was secured by property of the debtor.

Make-Whole provision would be approximately $500,000.

Premium is neither principal nor interest, therefore not within

scope of guaranty.

Court found Make-Whole to be liquidated damages; rejected

unmatured interest argument.

30

In re South Side House

2012 U.S. Dist. LEXIS 10824

Court agreed with precedent that prepayment premiums will

not be enforced after default and acceleration unless either

the borrower intentionally evaded the premium or clear

contract language requires it.

Here, agreements required premium only when borrower

tendered payment before maturity, but did not require

premium only after default and acceleration.

31

In re LaGuardia Assocs., L.P.

2012 Bankr. LEXIS 5612 (Bankr. E.D. Pa.)

Premium sought in the amount of $15 million.

Parties agreed that the maturity date was accelerated.

Note provided "Upon such acceleration, payment of such

accelerated amount shall constitute a prepayment of the

[note] and any prepayment fee provided for in the Note shall

then be immediately due and payable."

Based upon this language, the court disallowed the premium

because only upon payment is the note prepaid and only then is

the premium due and payable.

32

In re School Specialty, Inc.

2013 Bankr. LEXIS 1897

Make-Whole triggered prepetition after default that led to

forbearance and acknowledgement of premium.

Committee objected that premium was "grossly

disproportionate" to the lender's anticipated damages making

the premium a penalty.

Based on expert testimony, court found (i) premium was

calculated to approximate the bargained for yield, and (ii) the

premium was the result of arms-length negotiations between

sophisticated parties.

33

In re AMR Corp., 485 B.R. 279 (Bankr. S.D.N.Y. 2013), aff’d. 730

F.3d 33 (2d Cir. 2013)

Debtors sought to refinance their prepetition financing through

a DIP loan that would save debtors in excess of $200 million.

Indentures specifically excluded payment of “Make-Whole

Amount” upon the occurrence and continuance of a default

caused by a bankruptcy filing.

Court disagreed with lenders that a post bankruptcy

refinancing was a voluntary prepayment of the debt by the

debtors.

34

In re MPM Silicones, LLC

2014 Bankr. LEXIS 3926 (Bankr. S.D.N.Y. 2014)

Lenders were oversecured and seeking a premium of

approximately $200 million.

Citing previously discussed cases, the court noted:

"Indeed, in each of the reported cases that quote language that

would be explicit enough to overcome the waiver of the make-

whole upon acceleration under New York law, more was required

than is contained in the relevant sections of the indentures and

notes . . . either an explicit recognition that the make-whole

would be payable notwithstanding the acceleration of the loan

or . . . a provision that requires the borrower to pay a make-whole

whenever debt is repaid prior to its original maturity."

35

Court rejected the argument that the lender was entitled to

damages for a breach of its right to rescind acceleration under

the Indenture.

Section 506(b) of the bankruptcy code permits oversecured

creditors claims for “reasonable fees, costs, or charges” that are

“provided for under the agreement . . .”

No such provisions existed in Indenture.

Affirmed 2015 U.S. Dist. LEXIS 66420.

In re MPM Silicones, LLC

2014 Bankr. LEXIS 3926 (Bankr. S.D.N.Y. 2014) (cont.)

36

In re Energy Future Holdings Corp.

527 B.R. 178 (Bankr. D. Del. 2015)

Seeking premium in excess of $430 million.

Court concluded that the plain language in Indenture did not

provide for a Make-Whole upon a bankruptcy acceleration.

The automatic acceleration provision did not refer explicitly to the

payment of an “Applicable Premium,” nor did it incorporate the

Optional Redemption Clause of the Indenture that was the only

provision in the Indenture that referred to the "Applicable

Premium.”

37

Court compared language at bar to language in Calpine,

Premier, Momentive and Solutia.

Thus, under New York law, absent explicit language entitling

lender to a premium acceleration, the premium is not owed.

Court would not imply a no-call provision and found therefore

no breach of any such provision.

Court found no breach of the "perfect tender" rule because

the automatic acceleration clause directly modified the rule

and permitted the debtors to repay the matured debt anytime

thereafter.

In re Energy Future Holdings Corp.

527 B.R. 178 (Bankr. D. Del. 2015) (cont.)

What is Default Interest?

• Higher rate of interest that applies when a default or event of default occurs under the agreement.

• Designed to be a form of liquidated damages, to compensate the lender for:

– The additional risks relating to the borrower, and

– The costs and inconvenience of monitoring untimely payments.

• Generally enforceable under state law, unless it is a penalty.

39

How Are Pre-Petition Default Interest Claims Generally Treated in Bankruptcy?

• Claims for pre-petition default interest are governed by Section 502 of the Bankruptcy Code. Most courts agree that Section 506(b) does not govern.

• Most courts allow claims for pre-petition default interest, so long as it is provided for in the agreement and is not prohibited under applicable non-bankruptcy law.

• A few courts have refused to allow claims for pre-petition default interest, if application of the default rate would be “inequitable.”

40

In re 785 Partners LLC

• In re 785 Partners LLC, 470 B.R. 126 (Bankr. S.D.N.Y. 2012). – Court assumed that the creditor’s claim was oversecured,

and debtor was solvent. Creditor sought allowance of pre-petition default interest and late payment fees.

– Approximately $8 million of pre-petition default interest was due.

– Late payment fee was 5% of the amount of any overdue payments. Almost $4 million of late fees were due as of the petition date.

– Loan documents were governed by NY law.

41

In re 785 Partners LLC (Cont.)

• Pre-petition interest is generally allowable to the extent, and at the rate, permitted under applicable non-bankruptcy law.

• Agreements to pay interest at a higher rate in the event of default typically is not an unenforceable penalty. Rather, it is a bargained-for risk allocation.

• Even when the default rate strikes the judge as high, the court should not re-write the bargain based on its own notions of fairness and equity, absent persuasive evidence of overreaching.

42

In re 785 Partners LLC (Cont.)

• The court found no basis to disturb the parties’ bargain relating to pre-petition default interest.

– The debtor and the lenders were sophisticated parties and were represented by counsel.

– There was no evidence of overreaching by the lenders.

– The court noted that the non-default rate under the loan documents might have been higher, had the parties not negotiated a default rate.

– The price that the new lenders paid to acquire the loans was irrelevant.

43

In re 400 Walnut Assocs., L.P.

• In re 400 Walnut Assocs., L.P., 473 B.R. 603 (E.D. Pa. 2012).

– Default interest rate was 16%, compared to the non-default rate of 5%.

– Debtor objected to claim for pre-petition default interest.

– Loan documents were governed by PA law.

– Citing cases relating to Section 506(b), the Bankruptcy Court disallowed the creditor’s claim for pre-petition default interest on equitable grounds. In re 400 Walnut Assocs., L.P., 461 B.R. 308 (Bankr. E.D. Pa. 2011).

44

In re 400 Walnut Assocs., L.P. (Cont.)

• The District Court reversed the Bankruptcy Court’s holding with respect to pre-petition default interest.

– The District Court held that an equitable analysis should not be used to decide whether to allow pre-petition default interest.

– Rather, the allowability of pre-petition default interest is governed by the loan documents and applicable state law.

– Equitable/reasonableness analysis applies to claims for post-petition interest under Section 506(b) of the Bankruptcy Code. Majority view is that Section 506(b) does not apply to claims for pre-petition interest.

45

In re Sultan Realty, LLC

• In re Sultan Realty, LLC, No. 12-10119, 2012 WL 6681845 (Bankr. S.D.N.Y. 2012).

– Default interest rate was 24%, compared to the non-default rate of 6.125%. Over $100,000 of pre-petition default interest had accrued. Debtor was solvent.

– Debtor’s Chapter 11 plan provided for the allowed amount of the creditor’s claim to be paid in full and in cash, and stated that the claim was unimpaired.

– Debtor argued that the creditor was not entitled to pre-petition default interest, and argued that its confirmed Chapter 11 plan cured any defaults in any event.

46

In re Sultan Realty, LLC (Cont.)

• The court refused to apply equitable considerations to the creditor’s claim for pre-petition default interest.

– Citing 785 Partners, the court held that agreements to pay pre-petition default interest are governed by state law.

– Courts cannot re-write the parties’ bargain based on its own notions of fairness and equity.

47

In re Sultan Realty, LLC (Cont.)

• Did the debtor’s Chapter 11 plan (which treated the creditor’s claim as unimpaired) cure the defaults under Section 1124(2) of the Bankruptcy Code?

• Some courts have held that a plan that meets the definition for non-impairment nullifies the effects of a default (including the right to default interest). – In re Southeast Co., 868 F.2d 335 (9th Cir. 1989).

– In re Entz-White Lumber & Supply, Inc., 850 F.2d 1338 (9th Cir. 1988).

– In re Johnson, 184 B.R. 570 (Bankr. D. Minn. 1995).

– In re Forest Hills Assocs., 40 B.R. 410 (Bankr. S.D.N.Y. 1984).

48

In re Sultan Realty, LLC (Cont.)

• Other courts had concluded that Section 1124(2) merely nullifies the acceleration of the debt, and does not affect a creditor’s right to default interest. • In re 139-141 Owners Corp., 313 B.R. 364 (S.D.N.Y. 2004).

• In re K&J Props. Inc., 338 B.R. 450 (Bankr. D. Colo. 2005).

• In re Frank’s Nursery & Crafts, Inc., No. 04-15826, 2006 WL 2385418 (Bankr. S.D.N.Y. 2006).

• The bankruptcy court in Sultan held that Section 1124(2) of the Bankruptcy Code did not affect the creditor’s right to default interest, under the facts of that case.

49

In re Parker

• In re Parker, No. 12-03128, 2014 WL 6545025 (Bankr. E.D.N.C. 2014).

– Creditor extended two secured loans to the debtors, each bearing a default interest rate of 25% (the non-default rate was 15%). Creditor’s claim was oversecured.

– The creditor did not disburse all of the loan proceeds to the debtors. Instead, it held back a substantial amount to cover various perceived risks.

– The debtors challenged the creditor’s claim for pre-petition default interest, arguing that it was an unenforceable penalty.

50

In re Parker (Cont.)

• The court disallowed the creditor’s claim for pre-petition default interest in its entirety, because it found the imposition of the default rate to be inequitable.

• The court examined the following factors: – Whether the creditor faced a significant risk that the debt

would not be repaid.

– Whether the non-default rate is the prevailing market rate.

– Whether the difference between the default rate and the non-default rate is reasonable.

– Whether the default rate is a penalty.

51

In re Deep River Warehouse, Inc.

• In re Deep River Warehouse, Inc., No. 04-52749, 2005 WL 1513123 (Bankr. M.D.N.C. 2005).

– Default interest rate under the loan documents was 3% higher than the non-default rate. Approximately $115,000 of pre-petition default interest had accrued.

52

In re Deep River Warehouse, Inc. (Cont.)

• The court stated that the question of whether pre-petition interest will be allowed at the default rate is determined on a case-by-case basis and is fact-specific.

• The court allowed the creditor’s claim for pre-petition default interest, after considering:

– The size of the loan; the nature of the collateral; the proportion of the default rate to the non-default rate; the commercial nature of the loan; and the sophistication of the parties.

53

In re Shree Mahalaxmi, Inc.

• In re Shree Mahalaxmi, Inc., 505 B.R. 794 (Bankr. W.D. Tex. 2014). – Ten years before filing its bankruptcy petition, the debtor

defaulted under the loan documents by permitting the lender’s collateral to be encumbered by junior liens.

– The trustee for the holders of the debt discovered the breach post-petition, and later asserted a pre-petition default interest claim for approximately $400,000.

– The debtor objected to the pre-petition default interest claim, on the grounds that default interest was not owing under the terms of the loan documents (governed by TX law).

54

In re Shree Mahalaxmi, Inc. (Cont.)

• The court held that, even though an Event of Default had occurred, the trustee was not entitled to pre-petition default interest because the loan documents required it to exercise its option to accelerate the debt before default interest could be imposed.

• The trustee did not effectively exercise its option to accelerate the debt before the petition date.

– To exercise the option under TX law, the trustee had to provide a notice of intent to accelerate the debt, and a notice of acceleration. The Trustee did not do that.

55

Other Cases Regarding the Possible Need to Take Action to Accelerate

• In re Crystal Properties, Ltd., 268 F.3d 743 (9th Cir. 2001) (lender could not collect default interest because it failed to take affirmative action to accelerate the debt).

• In re Payless Cashways, Inc., 287 B.R. 482 (Bankr. W.D. Mo. 2002) (same).

• In re South Side House, LLC, 451 B.R. 248 (Bankr. E.D.N.Y. 2011) (default charge was fully enforceable from date of default, without the need to provide notice to the debtor).

56

Treatment of Late Fees in Bankruptcy

57

What Are Late Fees?

• Additional fees that become due if any payment under the agreement is late.

– The agreement will state the circumstances under which a late fee will become due, as well as how the late fee is calculated.

• Principal purpose of late fees is to cover the creditor’s administrative and other costs relating to the handling of delinquent payments.

– Late fees and default interest serve many of same purposes.

58

How Are Late Fee Claims Generally Treated in Bankruptcy?

• There must be an underlying enforceable right to late fees under applicable non-bankruptcy law.

• Section 502 of the Bankruptcy Code governs claims for pre-petition late fees.

• Under Section 506(b) of the Bankruptcy Code, oversecured creditors are entitled to “reasonable fees, costs, or charges provided for under the agreement or State statute under which such claim arose.”

59

How Are Late Fee Claims Generally Treated in Bankruptcy? (Cont.)

• Several courts have disallowed claims for late fees where no late payments were actually made (and, therefore, the creditor incurred no expenses in handling delinquent payments).

– In re 785 Partners LLC, 470 B.R. 126 (Bankr. S.D.N.Y. 2012) (the creditor’s rights under the pre-petition loan documents were extinguished under the Chapter 11 plan, and replaced by a completely new note and mortgage).

– In re Woodmere Investors Ltd. P’ship, 178 B.R. 346 (Bankr. S.D.N.Y. 1995).

60

How Are Late Fee Claims Generally Treated in Bankruptcy? (Cont.)

• Oversecured creditors are generally entitled to either default interest or late fees, but not both.

• The reason is that default interest and late fees are largely designed to compensate the creditor for the same injury, so awarding both would amount to double recovery. – In re 785 Partners LLC, 470 B.R. 126 (Bankr. S.D.N.Y. 2012).

– In re Cliftondale Oaks, LLC, 357 B.R. 883 (Bankr. N.D. Ga. 2006).

– In re 1095 Commonwealth Ave. Corp., 204 B.R. 284 (Bankr. D. Mass. 1997).

61

Covered Today

• “Original Issue Discount”(OID)

– What is OID?

– How does OID intersect with the Bankruptcy Code?

– Can creditors claim for OID?

• Post-petition Attorney’s Fees

– Pre-petition Agreements

– Pre-petition Judgments

63

What is Original Issue Discount and how does it impact the Bankruptcy Code?

• A form of interest created by certain debt instruments.

• OID is the difference between a debt instrument’s issue price and its redemption price.

• For example: The issue price of BOND A is $7,000. The redemption price is $10,000. The OID generated by BOND A is $3,000.

• OID is a form of interest under the Tax Code. Section 502(b)(2) of the Bankruptcy Code prohibits any claim for “unmatured interest,” but does not define the term.

64

Can a creditor assert a claim including OID?

• Yes – depending on the type of OID involved.

• Three types of OID

– Actual OID : generated by a debt instrument

– Face Value OID: generated by a face value debt exchange

– Fair Market Value OID : generated by a fair market value debt exchange.

65

Actual OID

• Actual OID is the original issue discount on the initial debt instrument.

• The legislative history of the Bankruptcy Code and case law hold that Actual OID is unmatured interest and disallowable.

– The Senate and House Reports - S.Rep. No. 989, 9th Cong., 2d Sess. 62; H.R.Rep. No. 595, 95th Cong., 2d Sess. 352.

– In re Public Serv. Co., 114 B.R. 800, 803 (Bankr. D. N.H. 1990)

– In re Chateaugay Corp., 961 F.2d at 380 (2d Circ.)

– Matter of Pengo Industries, Inc., 962 F.2d 543, 546 (5th Cir. 1992)

66

Debt-For-Debt Exchanges

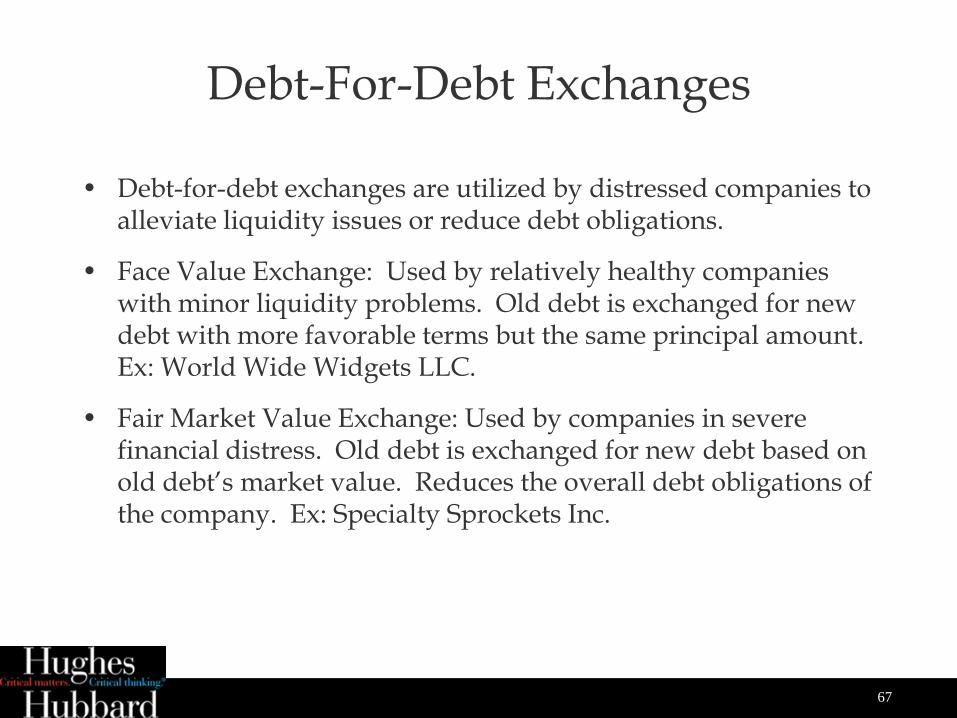

• Debt-for-debt exchanges are utilized by distressed companies to alleviate liquidity issues or reduce debt obligations.

• Face Value Exchange: Used by relatively healthy companies with minor liquidity problems. Old debt is exchanged for new debt with more favorable terms but the same principal amount. Ex: World Wide Widgets LLC.

• Fair Market Value Exchange: Used by companies in severe financial distress. Old debt is exchanged for new debt based on old debt’s market value. Reduces the overall debt obligations of the company. Ex: Specialty Sprockets Inc.

67

Are Face Value and Fair Market OID “Unmatured Interest?”

• No. Both Face Value and Fair Market OID are both allowable bankruptcy claims.

68

Face Value OID

• Face Value OID can serve as an allowable claim, though that result was at first in doubt.

• In re Chateaugay, 109 B.R. 51 (Brank. S.D.N.Y. 1990) - Bankruptcy Court found that the face value exchange of debt-for-debt created new OID. Because OID was by definition “unmatured interest” the bankruptcy could found the OID on the New Notes issued after LTV’s face value exchange was disallowable.

69

Face Value OID

• In re Chateaugay Corp., 961 F.2d 378, 380 (2d Cir. 1992): The Second Circuit reversed in part, finding that actual OID is disallowed, but allowing the interest created by the face value exchange. The Second Circuit found that a face value exchange of debt obligations in a consensual workout does not, for the purposes of section 502(b)(2), generate new OID.

• The Second Circuit’s decision rested largely on the fact that a face value exchange leaves the liability of the original debt unchanged.

• Texas Commerce Bank, N.A. v. Licht (In re Pengo Indus., Inc.), 962 F.2d 543 (5th Cir. 1992): The Fifth Circuit held that a Face Value exchange did not create new OID or unmatured interest.

70

Fair Market Value OID

• Even though the fair market value exchange of the Sprocket Bonds reduced the company’s overall debt obligations, Specialty Sprockets cannot recover and declares bankruptcy. Do the holders of the New Sprocket Bonds have an allowable claim for the OID created by the exchange? Yes.

• In re Residential Capital, LLC, 501 B.R. 549 (Bankr. S.D.N.Y. 2013): Rescap engaged in a fair market value exchange with Junior Note Holders. The Bankruptcy Court determined that there was no reason to treat Fair Market exchanges differently than Face Value exchanges and focused mainly on the fact that both types of debt-for-debt exchanges create an opportunity for distressed entities to restructure without entering bankruptcy.

71

The Takeaway

• Fair market and Face Value OID are not disallowable as “unmatured

interest” under section 502(b)(2).

• The decisions in Chateaugay, Pengo, and ResCap likely encourages

debt holders to engage in exchanges.

• Non-exchanging debt holders face the reality that Actual OID on the

initial debt instrument is not allowable.

• Exchanging parties, however, can rest assured that the full value of the

debt, including unamortized OID is potentially an allowable claim.

72

Attorney’s Fees

• Generally, attorney’s fees are not allowed in bankruptcy. See In re FINOVA Grp., 304 B.R. 630, 638 (D. Del. 2004).

• But Courts have allowed claims for post-bankruptcy legal fees, as long as those fees arise out of pre-petition agreements and judgments.

73

Pre-petition Agreements

• Travelers Casualty & Surety Co. of America v. Pacific Gas & Electric, 549 U.S. 443 (2007): the Supreme Court held that the Bankruptcy Code does not eliminate contractual obligation to cover attorney’s fees because the Bankruptcy Code provides that contractual fees are allowable claims unless when the Bankruptcy Code specifically prohibits them.

• In Ogle v. Fid. & Deposit Co., 586 F.3d 143 (2d Cir. 2009) – The Second Circuit held that attorney’s fees were not bared by section 502(b) or 506(b), and were allowable as long as underlying agreement was valid as a matter of state substantive law.

74

The Takeaway

• Parties can protect their right to seek a claim for attorney’s fees by making sure their underlying contracts and agreements specifically provide the right to seek those fees.

• A valid underlying contract, with a valid, clearly drafted provision regarding fees, can serve as the basis of a post-bankruptcy claim for attorney’s fees.

75

Pre-petition Judgments

• In In re Rubin Family Irrevocable Stock Trust, 516 B.R. 221 (Bankr. EDNY 2014) –The Eastern District of New York held that post-petition attorney’s fees and costs were allowable in a chapter 11 case where the right to such fees and costs arose from an enforceable and final prepetition judgment against the debtor.

• More specifically, the court held that valid prepetition judgments are entitled to res judicata effect in the bankruptcy court, but are not entitled to secured status because they are not based on a contract or statute.

• Parties likely cannot and indeed don’t need to do much to protect their rights in this regard.

76