Embed Size (px)

Citation preview

The Online Consumer

Antoon Van der Steichel – Research Manager Ipsos

9 October 2013

2

IPSOS

3

1

4

84 COUNTRIES

>15 000 EMPLOYEES

€ 1.7 BN (2012)

Ipsos key Milestones

© 2013 Ipsos. Corporate Presentation 5

First acquisitions outside France : Ipsos becomes a European company.

Didier Truchot founds Ipsos in Paris.

Jean-Marc Lech joins Ipsos.

First acquisitions outside Europe : Ipsos builds its worldwide network.

Ipsos acquires Synovate making it No. 3 in Research worldwide.

Ipsos lists its shares on the stock market (today’s Eurolist of Euronext).

1975 1982 1990 1997 1999 2011

Ipsos: an innovation company

22 M € turnover

120 FTE’S

Projects in 2012

500 >

>

Ipsos in Belgium

6

Over 120 FTE consisting of…

7

Qualitative research

0

Support

0

Operations

Quantitative research

Community research

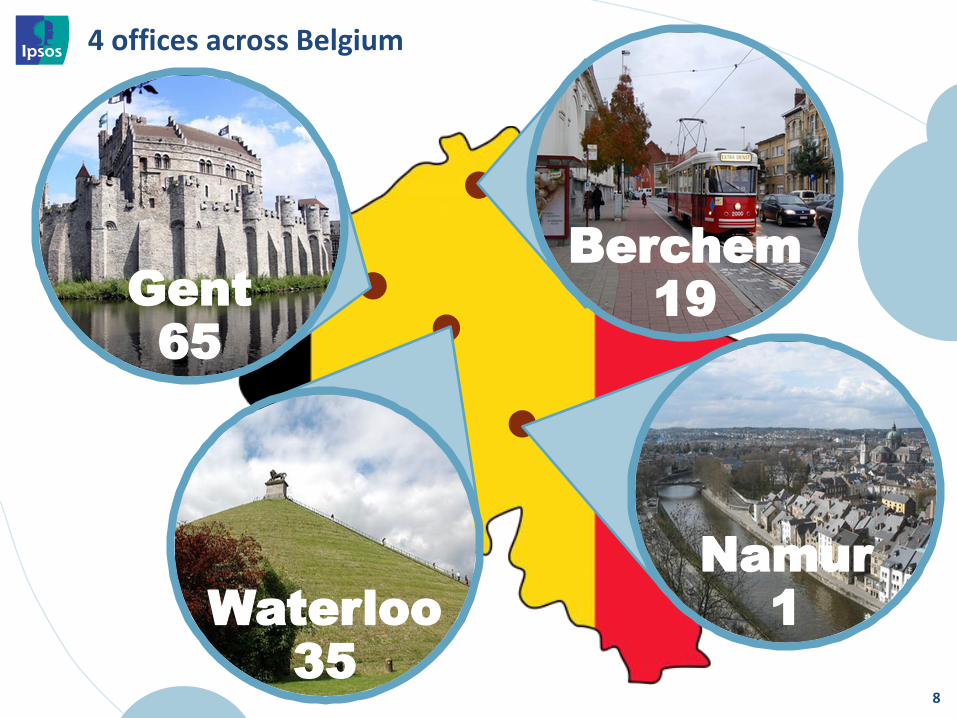

4 offices across Belgium

8

Gent

65

Berchem

19

Namur

1 Waterloo

35

Technical capabilities

9

200 laptops for CAPI

> 100 units for CATI

Test facilities in Antwerp &

Namur

Access Panel >100 K (BE) Eye tracking Mobile

Handhelds Social spaces Biometrics

Passive

10

And many more

Ipsos Belgium : our references

The online Consumer

12

2

WELCOME TO THE

NEW NORMAL

Where consumers are constantly

connected – and “always on” is their

default setting

WELCOME TO THE NEW NORMAL

Where we are accelerating towards the

new singularity – a tipping point where the

storing of a consumer’s life information will

be in a single portable digital device

WELCOME TO THE NEW NORMAL

Where we will need to learn to cope with

“super abundance” – tools, choices, apps will

move to “one touch” actions combined with the

visualization of information

WELCOME TO THE NEW NORMAL

Where we are moving towards a culture

where information about most things

becomes freely available

WELCOME TO THE NEW NORMAL

And where personalization via devices and

applications will continue to quickly grow

BRAND

IMAGE

TV, Press,

Poster, DM

etc…

Sponsorship

Planned PR

Website

PLANNED

COMMS

Share of

Voice

Strategy

Communication COMPETITOR

ACTIVITY

Word of

Mouth

Unplanned

PR Blogs

and

Forums

INCIDENTAL

Product

Experience

Occasion /

Users

POS

experience

USE /

EXPERIENCE

WHY IS ONLINE IMPORTANT TO YOUR BRAND?

18

LOOKING BACK 7 YEARS AGO

Your brand on top of almost all communication

BUT NOW, BRANDS ARE NO LONGER IN CONTROL

They can only observe how consumers create an online image, based on their experiences…

35% of the online consumers claim they have ever “talked” about a brand online, and this will only increase over time

SOURCE OPPA BRAND BUZZ SURVEY

IMPLICATIONS FOR MARKET RESEARCH

23 23

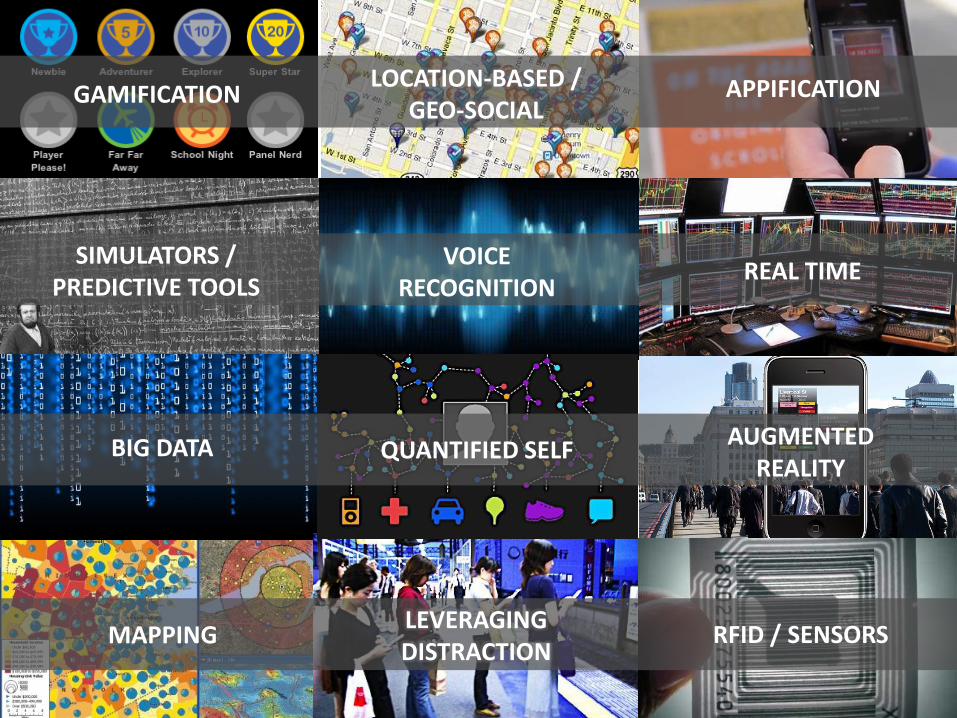

GAMIFICATION

SIMULATORS / PREDICTIVE TOOLS

VOICE RECOGNITION

REAL TIME

QUANTIFIED SELF AUGMENTED

REALITY BIG DATA

MAPPING RFID / SENSORS LEVERAGING DISTRACTION

LOCATION-BASED / GEO-SOCIAL

APPIFICATION

We need to evolve our tools

TECHNOLOGY

WILL BE THE BIG ENABLER

OF THE MARKET RESEARCH

OF THE FUTURE

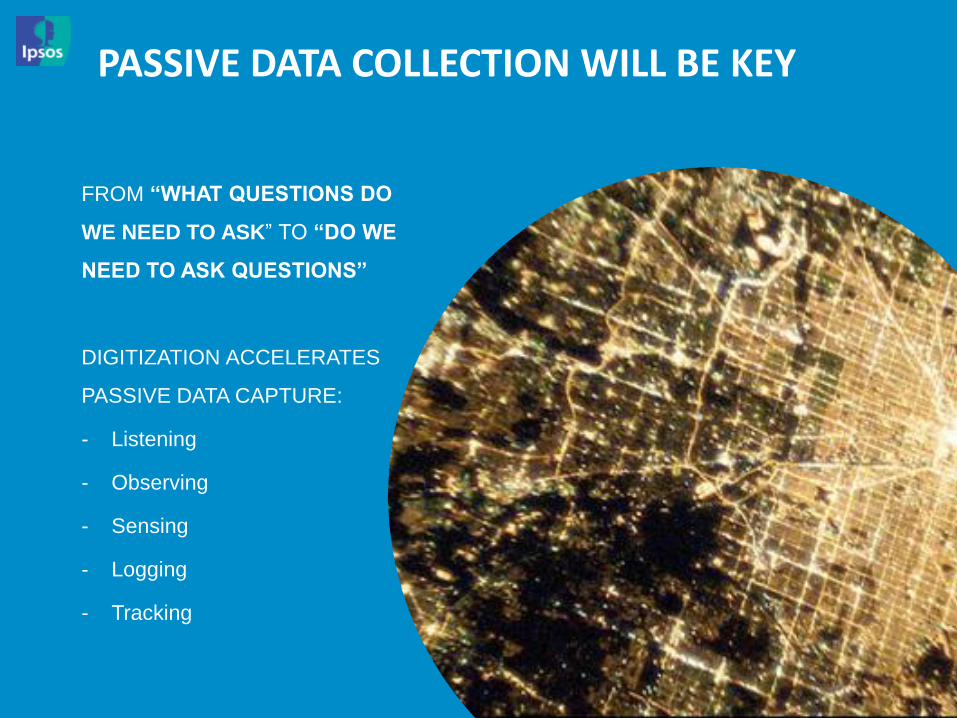

PASSIVE DATA COLLECTION WILL BE KEY

FROM “WHAT QUESTIONS DO

WE NEED TO ASK” TO “DO WE

NEED TO ASK QUESTIONS”

DIGITIZATION ACCELERATES

PASSIVE DATA CAPTURE:

- Listening

- Observing

- Sensing

- Logging

- Tracking

26

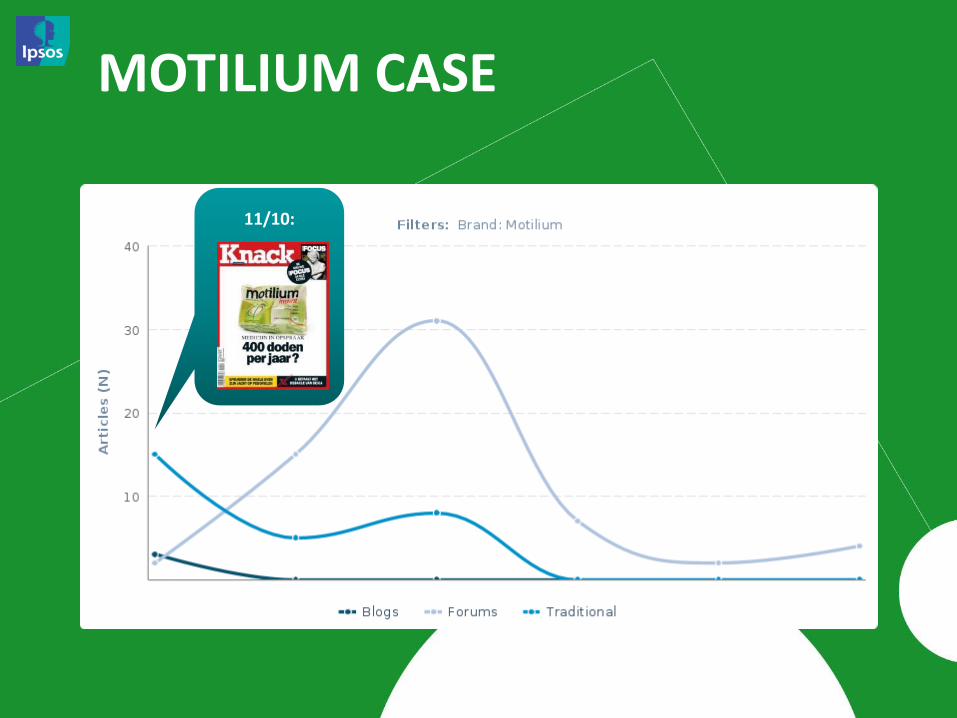

SOCIAL LISTENING OFFERS AN

UNFILTERED VIEW INTO HOW

PEOPLE TALK ABOUT, SHARE,

AND PROMOTE YOUR BRAND

ONLINE

MOTILIUM CASE

27

28

11/10:

MOTILIUM CASE

29

PASSIVE MEASUREMENT

= REAL TIME

OBSERVATION OF

BEHAVIOUR

30

IPSOS PROUDLY PRESENTS

IPSOS DIGITAL VIEW

1. Technology 2. Test panel set-up 3. Key learnings internet usage 4. Research solutions 5. Case studies

IPSOS DIGITAL VIEW

The technology

31

Ipsos Digital View

32

33

EVERYTHING

Ipsos Digital View

34

http:// http://

http:// http://

http:// http://

http:// http://

http:// http://

http://

Ipsos Digital View

35

0 0 0 1 9

Ipsos Digital View

36

Ipsos Digital View

37

xx

Ipsos Digital View

IPSOS DIGITAL VIEW

Test panel set-up

38

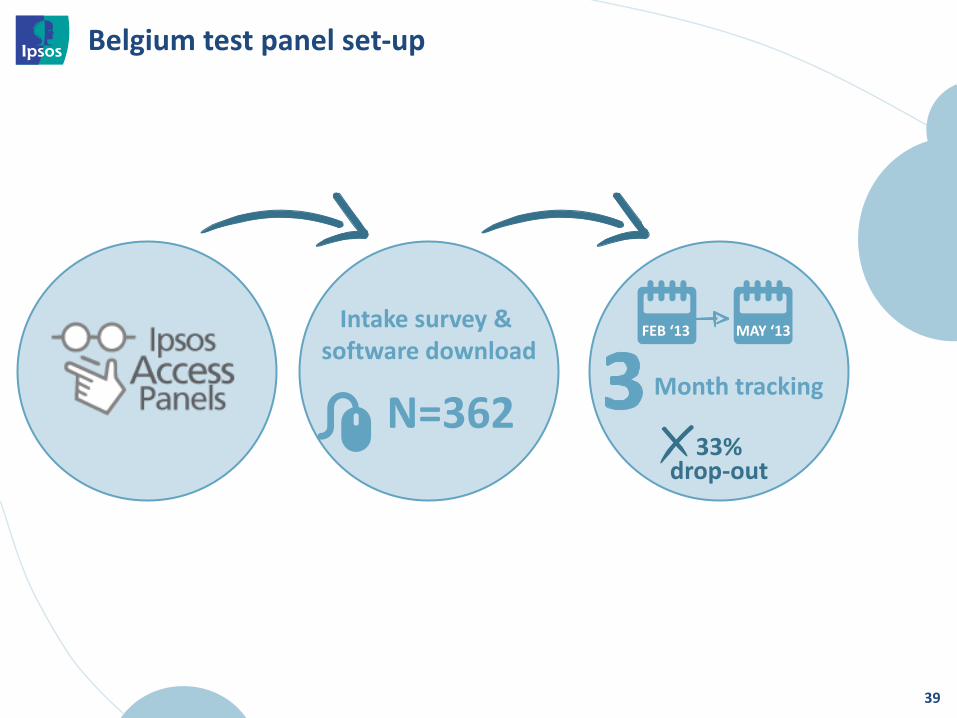

Intake survey & software download

N=362

33% drop-out

Belgium test panel set-up

Month tracking

FEB ‘13 MAY ‘13

39

40

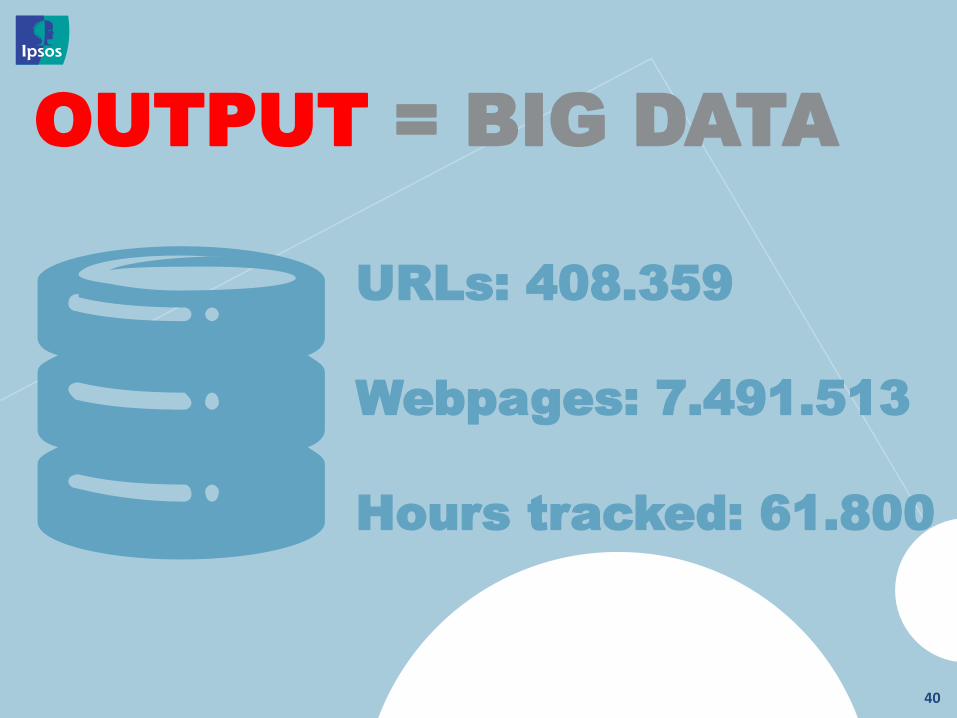

OUTPUT = BIG DATA

URLs: 408.359

Webpages: 7.491.513

Hours tracked: 61.800

IPSOS DIGITAL VIEW

General learning's on internet usage by Belgian consumers

41

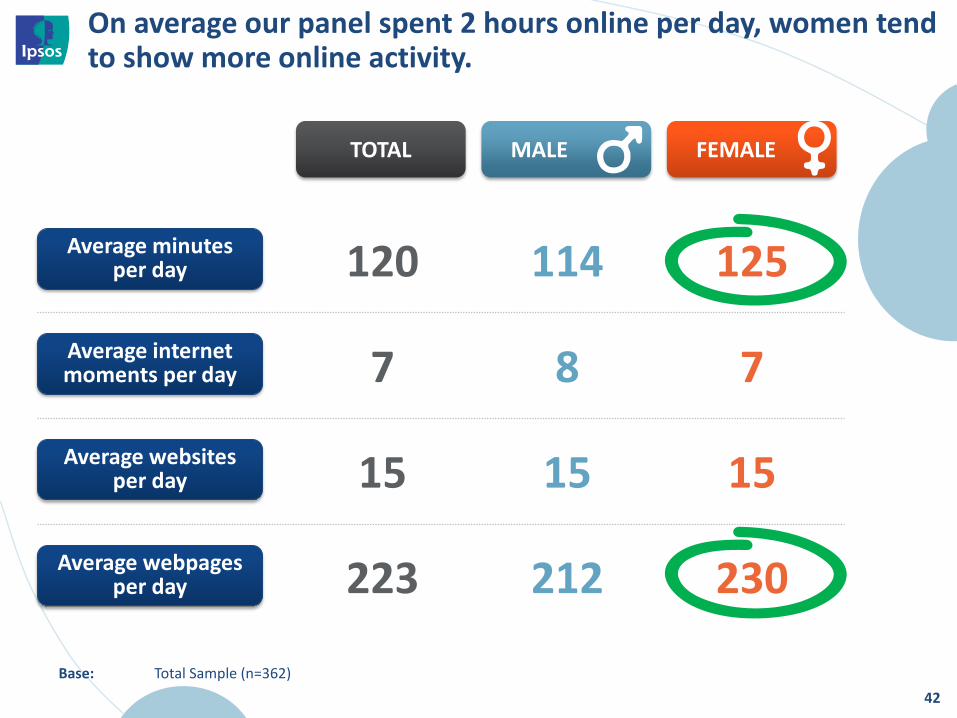

TOTAL MALE FEMALE

On average our panel spent 2 hours online per day, women tend to show more online activity.

42

120 114 125

7 8 7

15 15 15

223 212 230

Average minutes per day

Average internet moments per day

Average websites per day

Average webpages per day

Base: Total Sample (n=362)

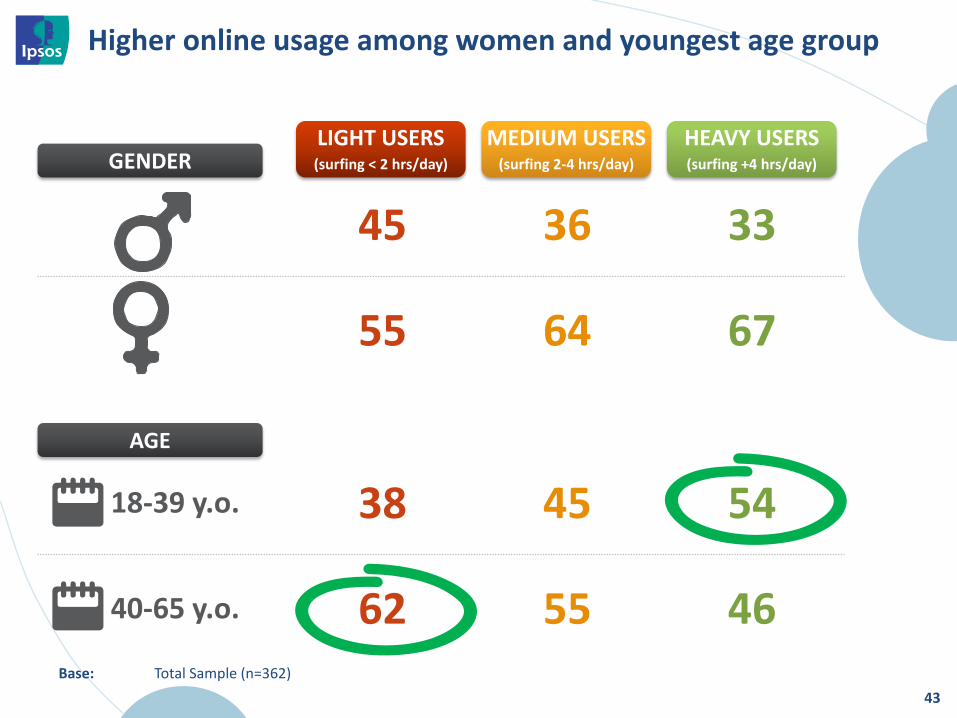

Higher online usage among women and youngest age group

43

45 36 33

55 64 67

38 45 54

62 55 46

GENDER

AGE

18-39 y.o.

40-65 y.o.

Base: Total Sample (n=362)

LIGHT USERS (surfing < 2 hrs/day)

MEDIUM USERS (surfing 2-4 hrs/day)

HEAVY USERS (surfing +4 hrs/day)

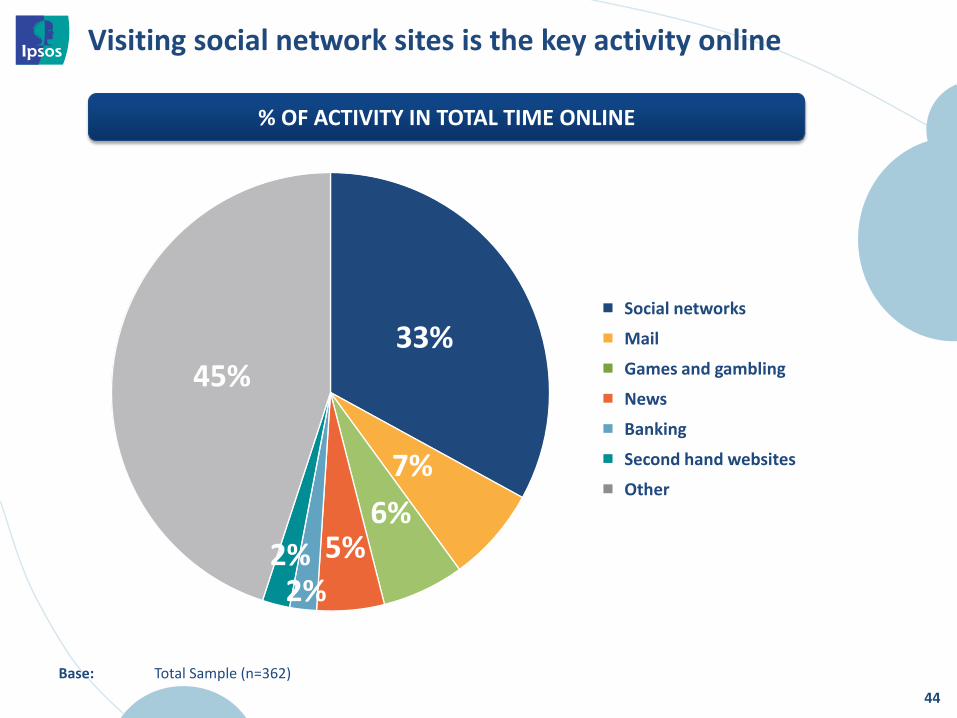

Visiting social network sites is the key activity online

44

33%

7%

6% 5%

2% 2%

45%

Social networks

Games and gambling

News

Banking

Second hand websites

Other

Base: Total Sample (n=362)

% OF ACTIVITY IN TOTAL TIME ONLINE

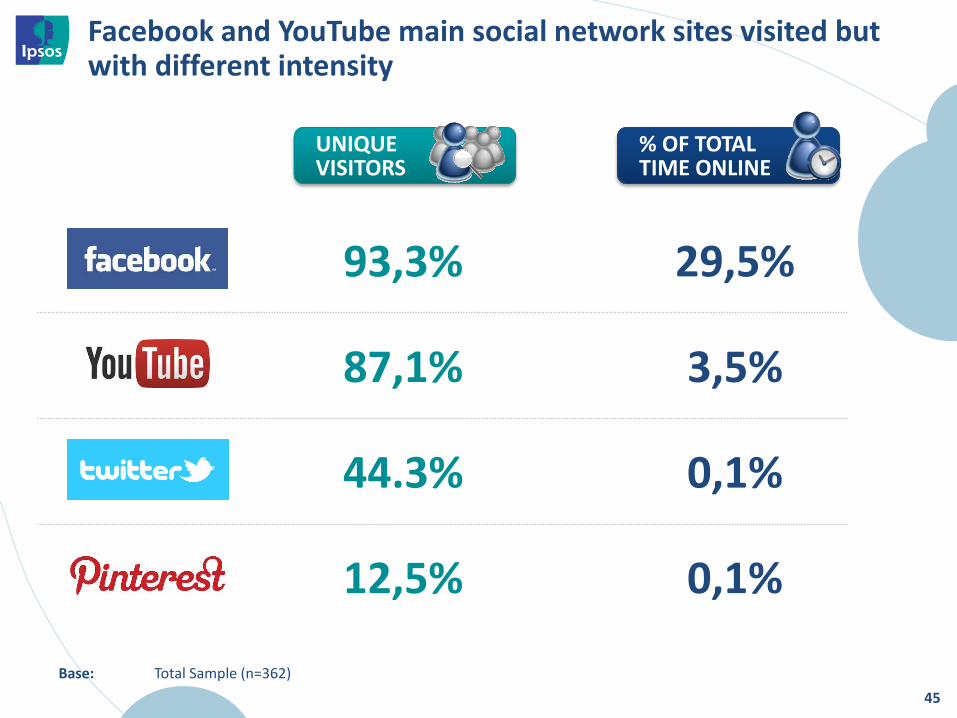

Facebook and YouTube main social network sites visited but with different intensity

45

93,3% 29,5%

87,1% 3,5%

44.3% 0,1%

12,5% 0,1%

UNIQUE VISITORS

% OF TOTAL TIME ONLINE

Base: Total Sample (n=362)

AVG VISITS/ VISITOR

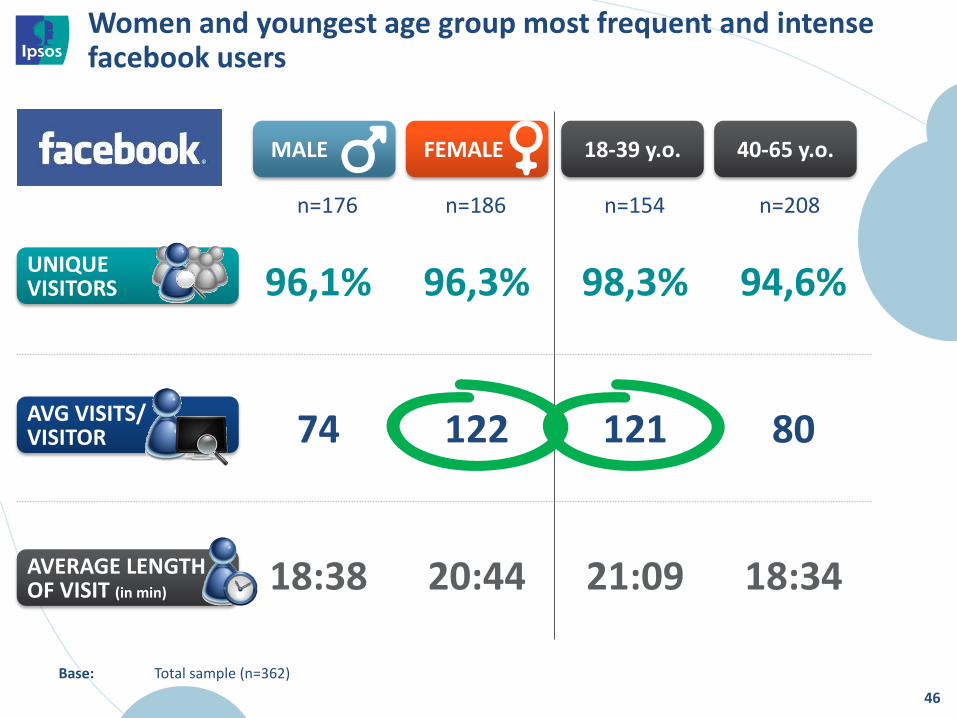

Women and youngest age group most frequent and intense facebook users

46

96,1% 96,3% 98,3% 94,6%

74 122 121 80

18:38 20:44 21:09 18:34

UNIQUE VISITORS

AVERAGE LENGTH OF VISIT (in min)

MALE FEMALE 18-39 y.o. 40-65 y.o.

Base: Total sample (n=362)

n=176 n=186 n=154 n=208

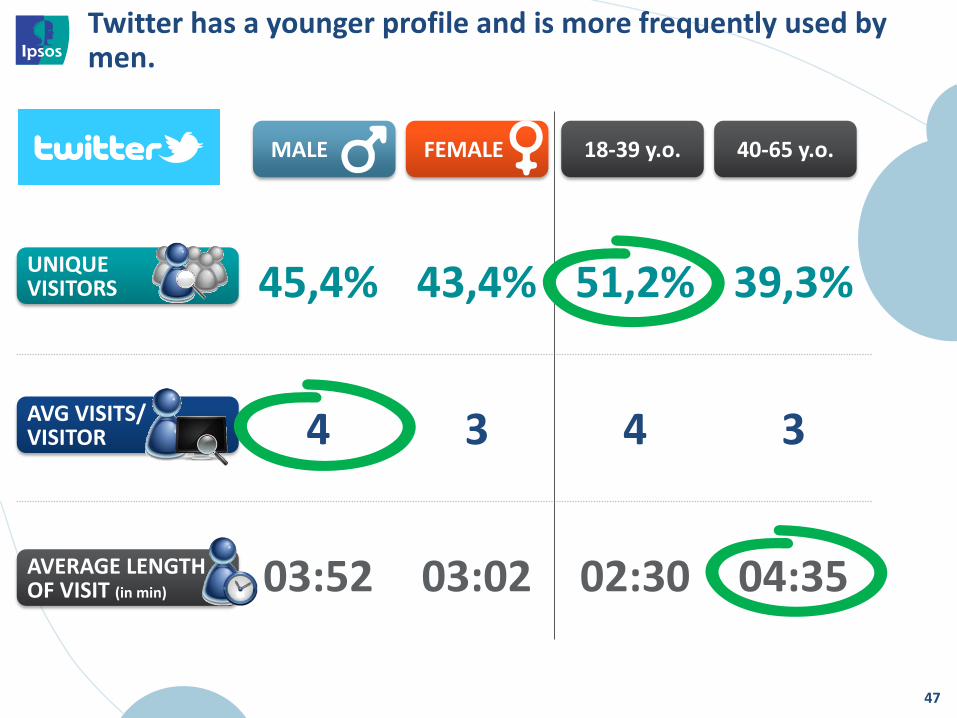

Twitter has a younger profile and is more frequently used by men.

47

45,4% 43,4% 51,2% 39,3%

4 3 4 3

03:52 03:02 02:30 04:35

UNIQUE VISITORS

AVERAGE LENGTH OF VISIT (in min)

AVG VISITS/ VISITOR

MALE FEMALE 18-39 y.o. 40-65 y.o.

AVG VISITS/ VISITOR

Pinterest is clearly a young women’s site although men appear to find their way to the site as well...

48

10,8% 11,9% 17,4% 7,1%

4 14 14 1

05:04 04:04 04:22 02:01

UNIQUE VISITORS

AVERAGE LENGTH OF VISIT (in min)

MALE FEMALE 18-39 y.o. 40-65 y.o.

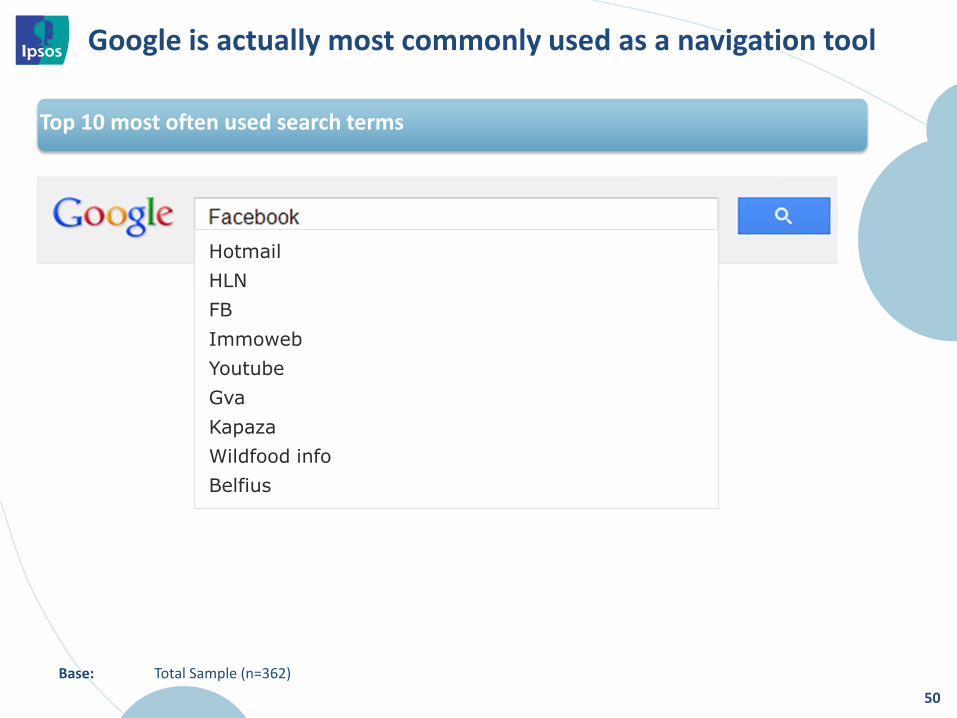

There is almost only 1 search engine used

49

94% of all registered searches are executed by Google

Base: Total Sample (n=362)

Google is actually most commonly used as a navigation tool

50

Hotmail

HLN

FB

Immoweb

Youtube

Gva

Kapaza

Wildfood info

Belfius

Base: Total Sample (n=362)

Top 10 most often used search terms

IPSOS DIGITAL VIEW

Research solutions & cases

51

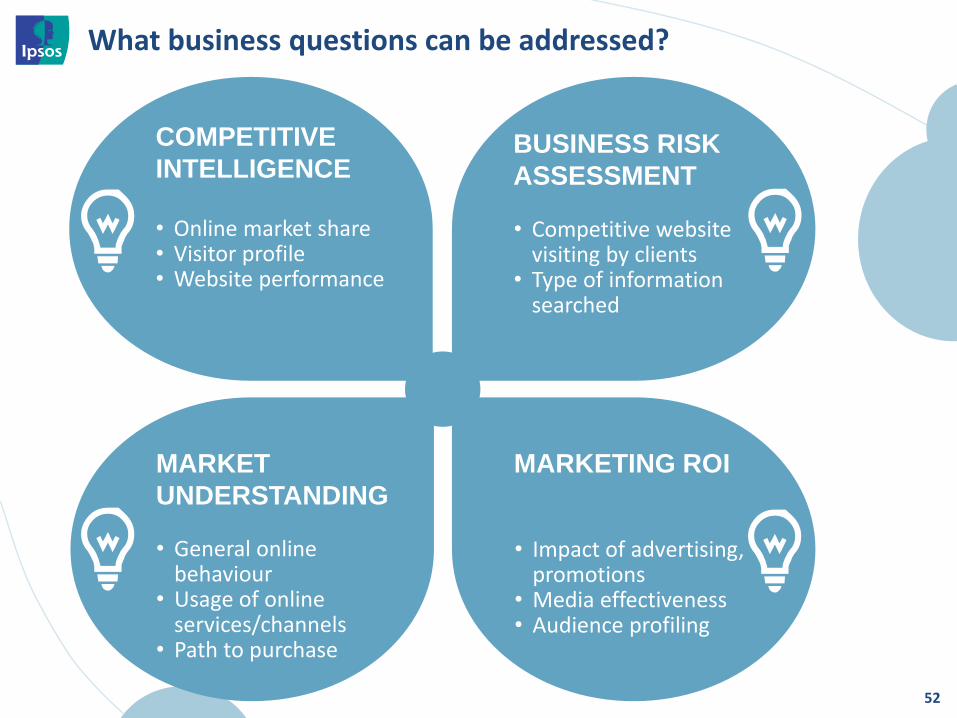

What business questions can be addressed?

52

COMPETITIVE

INTELLIGENCE

BUSINESS RISK

ASSESSMENT

MARKET

UNDERSTANDING

MARKETING ROI

• Online market share • Visitor profile • Website performance

• Competitive website visiting by clients

• Type of information searched

• General online behaviour

• Usage of online services/channels

• Path to purchase

• Impact of advertising, promotions

• Media effectiveness • Audience profiling

SOLUTION 1: COMPETITIVE INTELLIGENCE

53

CASE STUDY 1

54

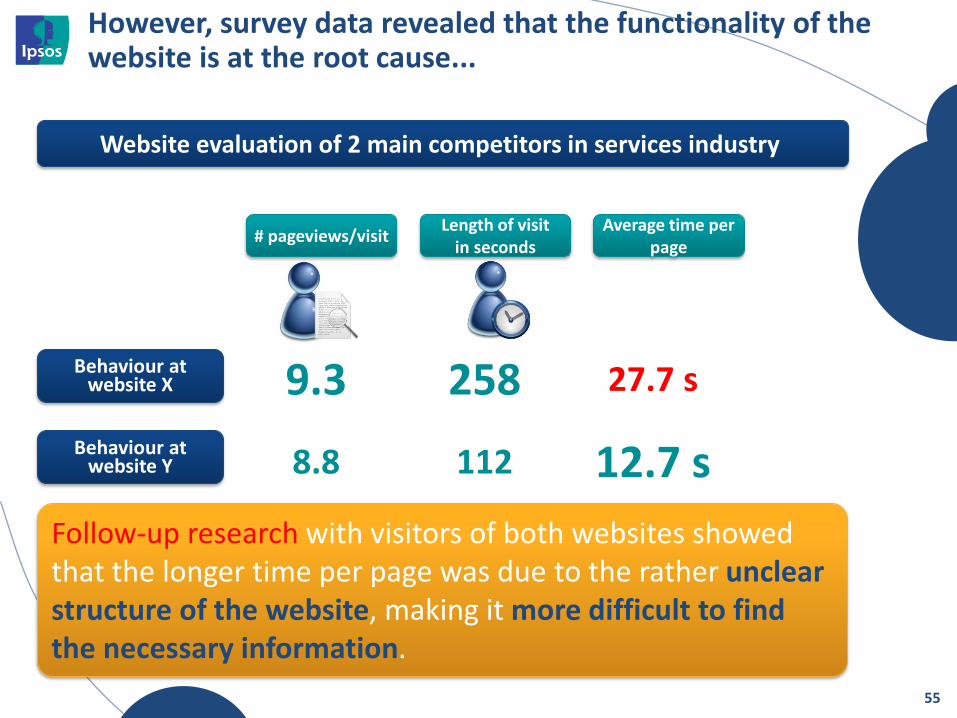

However, survey data revealed that the functionality of the website is at the root cause...

55

Website evaluation of 2 main competitors in services industry

9.3 258 27.7 s

8.8 112 12.7 s

Length of visit in seconds

Behaviour at website X

Behaviour at website Y

# pageviews/visit Average time per

page

Follow-up research with visitors of both websites showed that the longer time per page was due to the rather unclear structure of the website, making it more difficult to find the necessary information.

CASE STUDY 2

56

10%

Looking for news is also a popular activity online

57

97% http://........

News sites visited

10min.

1,8 different websites visited the same day

visits 3 or more different news sites a day

http://

http://

http://

visited at least 1 newssite average time spend browsing for news

Base: Total Sample (n=362)

18-26% also visit De Standaard Online

40-50%

Multiple online newsbrand users primarily loyal within a specific journalistic style

58

also visit HLN.be

visitors

Other news sites visited on the same day

Base: P12Weeks visitors of Het Nieuwsblad (n=102))

Specific events impacting online news consumption in different ways

59

127

Most consumers surfing to at least 1 news site

04/02 compared to an average day

Most consumers visiting 3 different newssites on one day

Most time spent on newssites

an index of

140 12/03 compared to an average day

an index of

139 28/01 compared to an average day

an index of

Base: Total Sample (n=362)

CASE STUDY 3

60

19 February 19 March

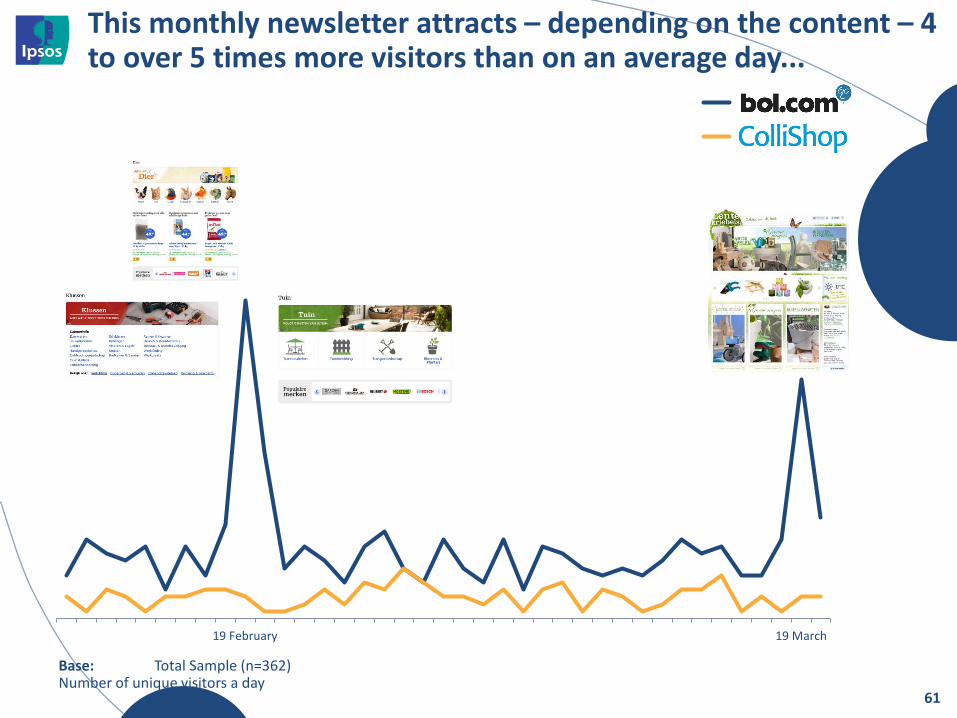

This monthly newsletter attracts – depending on the content – 4 to over 5 times more visitors than on an average day...

61

Base: Total Sample (n=362) Number of unique visitors a day

19 February 19 March

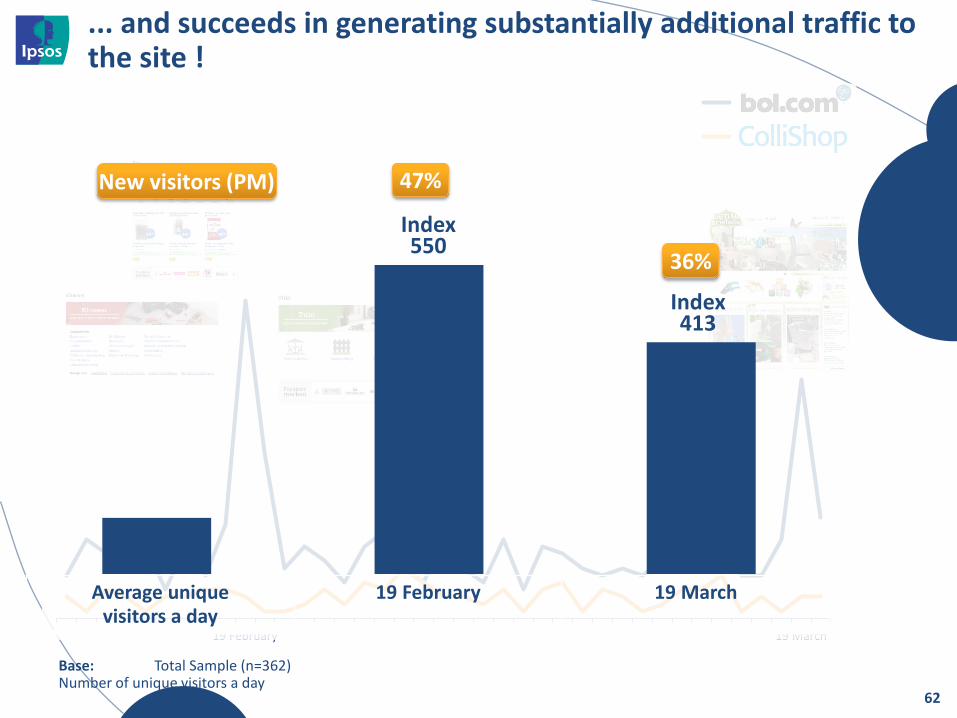

... and succeeds in generating substantially additional traffic to the site !

62

Index 550

Index 413

Average unique visitors a day

19 February 19 March

47%

36%

Base: Total Sample (n=362) Number of unique visitors a day

New visitors (PM)

SOLUTION 2: BUSINESS RISK ASSESSMENT

63

CASE STUDY 1

64

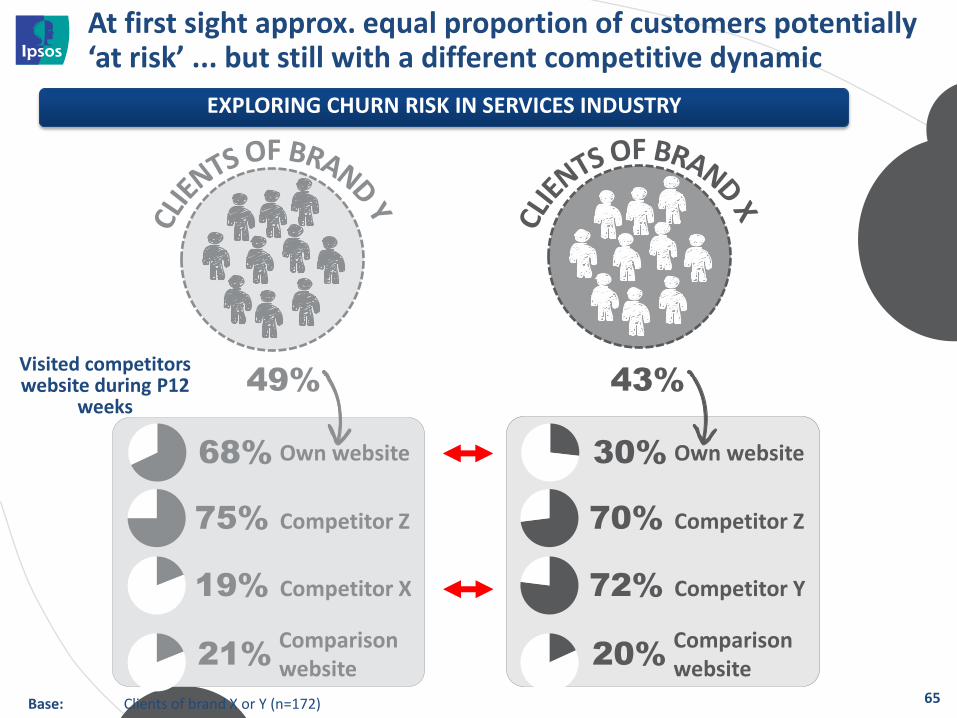

Visited competitors website during P12

weeks

At first sight approx. equal proportion of customers potentially ‘at risk’ ... but still with a different competitive dynamic

72% Competitor Y

70% Competitor Z

20% Comparison website

30% Own website

19% Competitor X

75% Competitor Z

21% Comparison website

68% Own website

43% 49%

EXPLORING CHURN RISK IN SERVICES INDUSTRY

65 Base: Clients of brand X or Y (n=172)

SOLUTION 3: MARKET

UNDERSTANDING

66

E-COMMERCE IN BELGIË

67

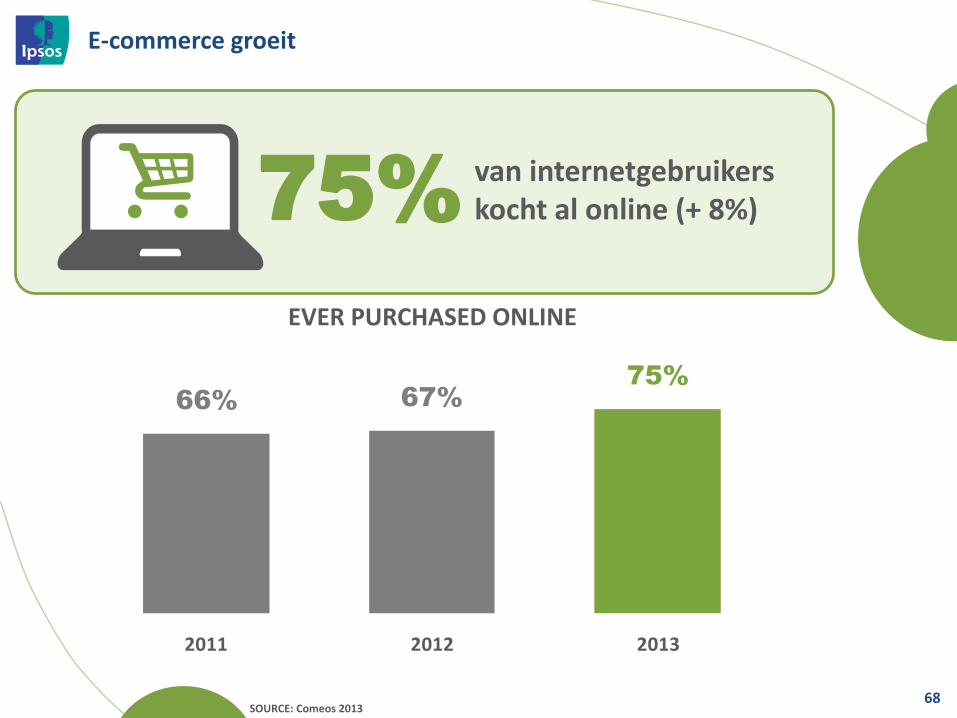

E-commerce groeit

68 SOURCE: Comeos 2013

66% 67%

75%

2011 2012 2013

van internetgebruikers kocht al online (+ 8%) 75%

EVER PURCHASED ONLINE

E-commerce groeit

69 SOURCE: Comeos 2013

van de Belgen deed dat in de voorbije 12 maanden 57%

58% 59%

70%

2011 2012 2013

PURCHASED ONLINE LAST YEAR

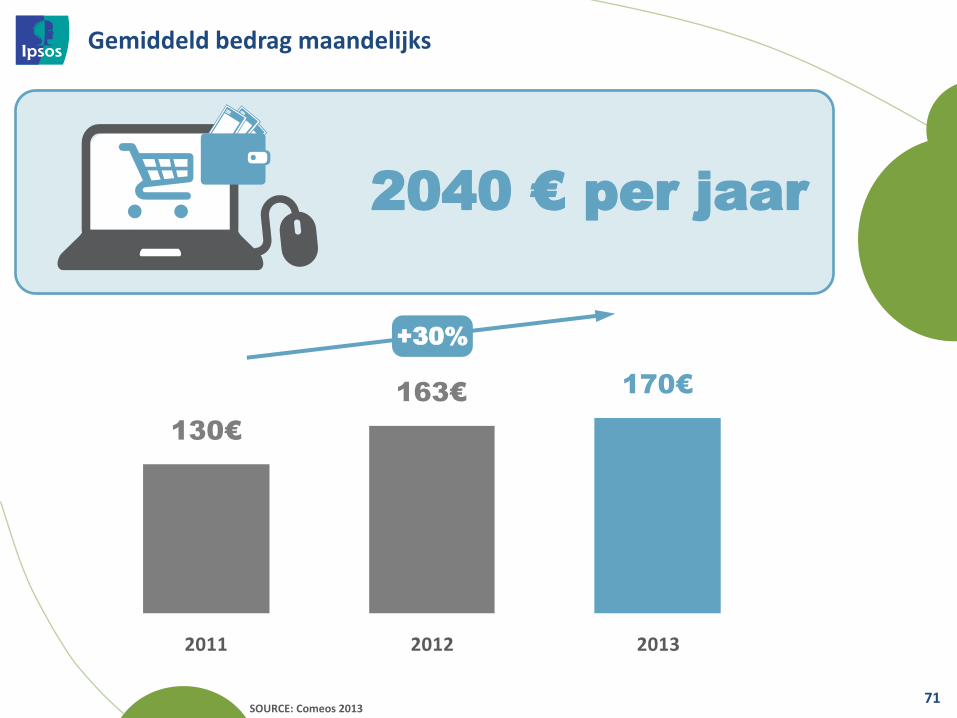

Maandelijkse aankopen

70 SOURCE: Comeos 2013

Aantal mensen dat maandelijks online koopt stijgt met

8%

17% 16%

24%

2011 2012 2013

+8%

Gemiddeld bedrag maandelijks

71 SOURCE: Comeos 2013

2040 € per jaar

130€

163€170€

2011 2012 2013

+30%

38%

31%

30%

23%

20%

14%

12%

10%

9%

9%

8%

8%

6%

5%

4%

3%

12%

21%

31%

40%

15%

16%

18%

Hotel / overnight stay

Event tickets

Boat, plane or train tickets

Books

Computer, hardware and software

Personal care products

Electronic appliances

CD / DVD / Blu-ray / games

Telecom

Household appliances

Toys

Fun fair tickets

Pharmaceutical products

Digital music

Furniture and home decoration

DIY and garden products

Sports products

Food

Films or TV series in digital format

Prepared food

Cars, motorbikes, bicycles

Other

WAT kopen klanten online?

72

Q: Which new products or services did you buy via the Internet (for personal purposes) in the past 12 months? N = 1062 / F = None

SOURCE: Comeos 2013

Kleren en schoenen voor het eerst op 1

Clothing / shoes

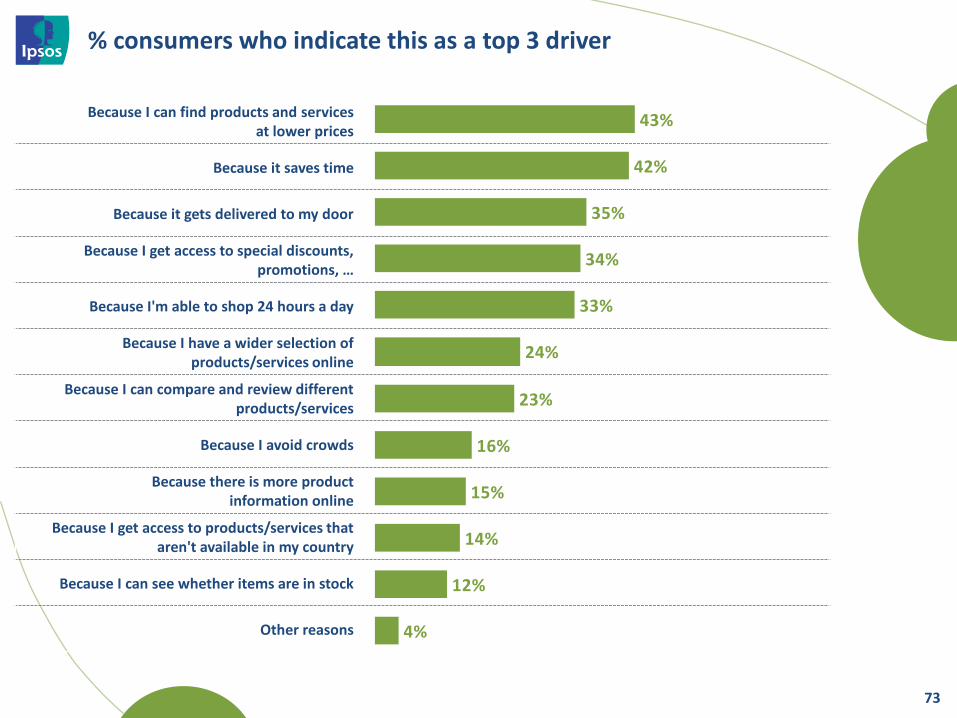

% consumers who indicate this as a top 3 driver

73

Because I can find products and services at lower prices

Because it saves time

Because it gets delivered to my door

Because I get access to special discounts, promotions, …

Because I'm able to shop 24 hours a day

Because I have a wider selection of products/services online

Because I can compare and review different products/services

Because I avoid crowds

Because there is more product information online

Because I get access to products/services that aren't available in my country

Because I can see whether items are in stock

Other reasons

42%

35%

33%

24%

16%

4%

23%

34%

43%

12%

14%

15%

CASE STUDY 1

74

40%

38%

30%

27%

25%

17%

15%

31% No visit of e-shop

High traffic to foreign e-commerce sites

75

Base: Total Sample (n=362) % unique visitors P12weeks

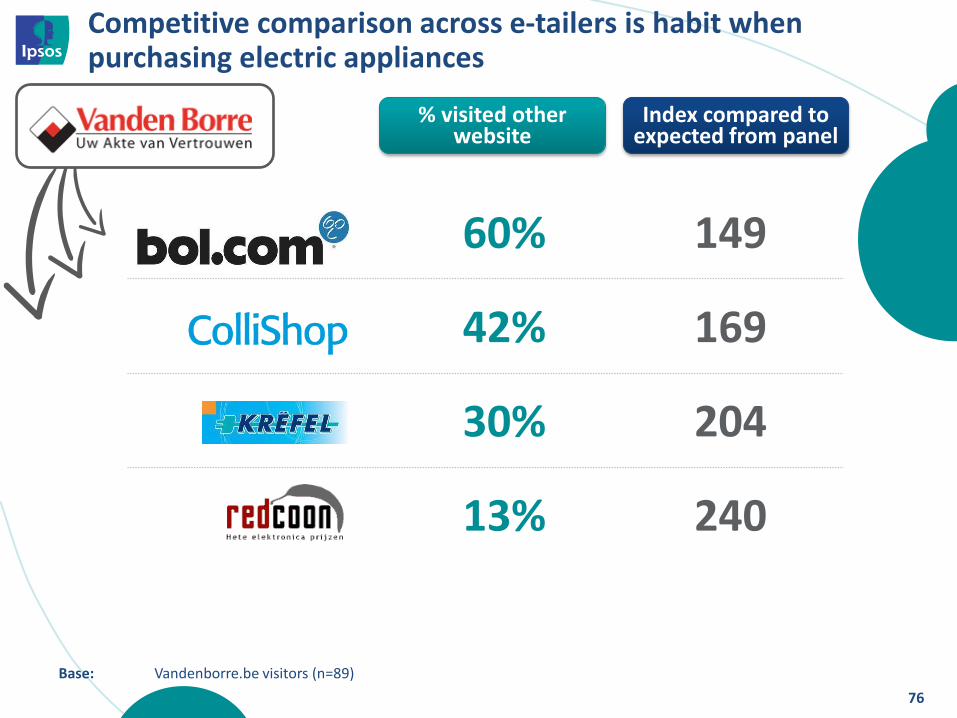

60% 149

42% 169

30% 204

13% 240

Competitive comparison across e-tailers is habit when purchasing electric appliances

76

% visited other website

Index compared to expected from panel

Base: Vandenborre.be visitors (n=89)

CASE STUDY 2

77

78

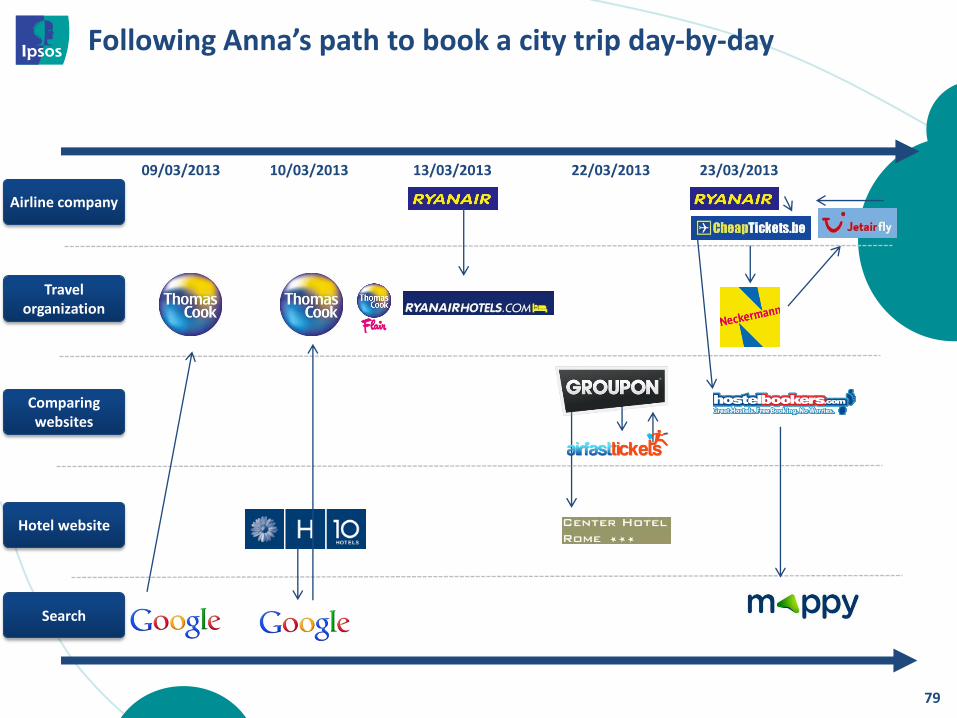

Booking a city trip starting from an offline source…

Following Anna’s path to book a city trip day-by-day

79

Airline company

Travel organization

Comparing websites

Hotel website

Search

09/03/2013 10/03/2013 13/03/2013 22/03/2013 23/03/2013

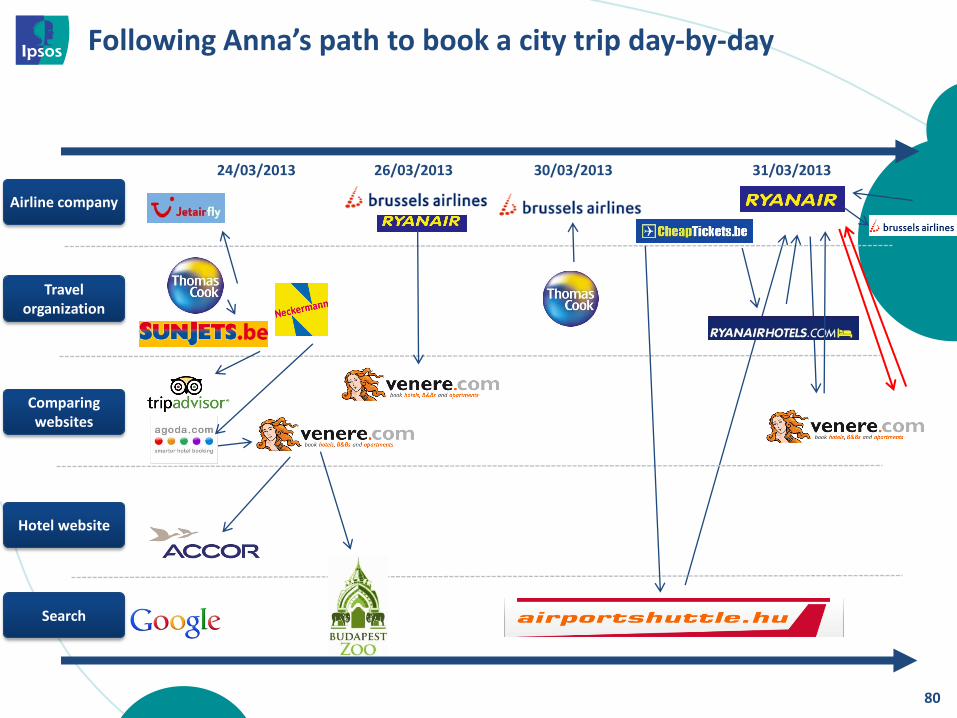

Following Anna’s path to book a city trip day-by-day

80

Airline company

Travel organization

Comparing websites

Hotel website

Search

24/03/2013 26/03/2013 30/03/2013 31/03/2013

The complex path to purchase for a city trip, covering over 3 hours online

81

Airline company

Travel organization

Comparing websites

Hotel website

Search

21 Domains

Main time spending in choosing the flight

82

4 Travel

organization

6 Comparing websites

3 Hotel website

4 Search

4 Airline

company

7’ 86’ 63’ 43’ 12’ Duration:

3.5 hrs

SOLUTION 4: MARKETING

ROI

83

CASE STUDY 1

84

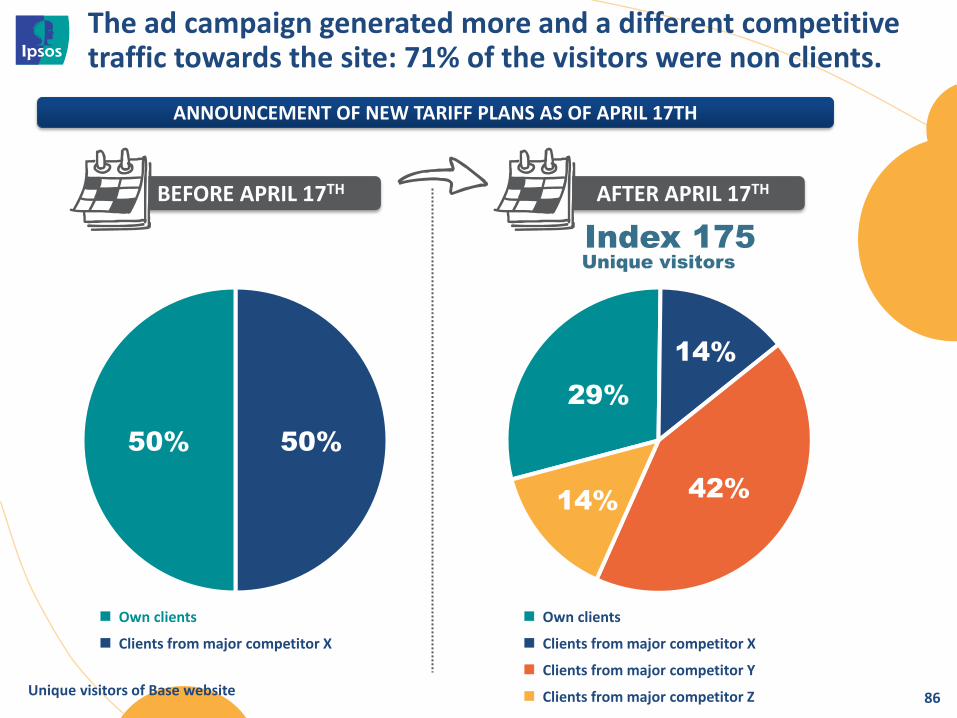

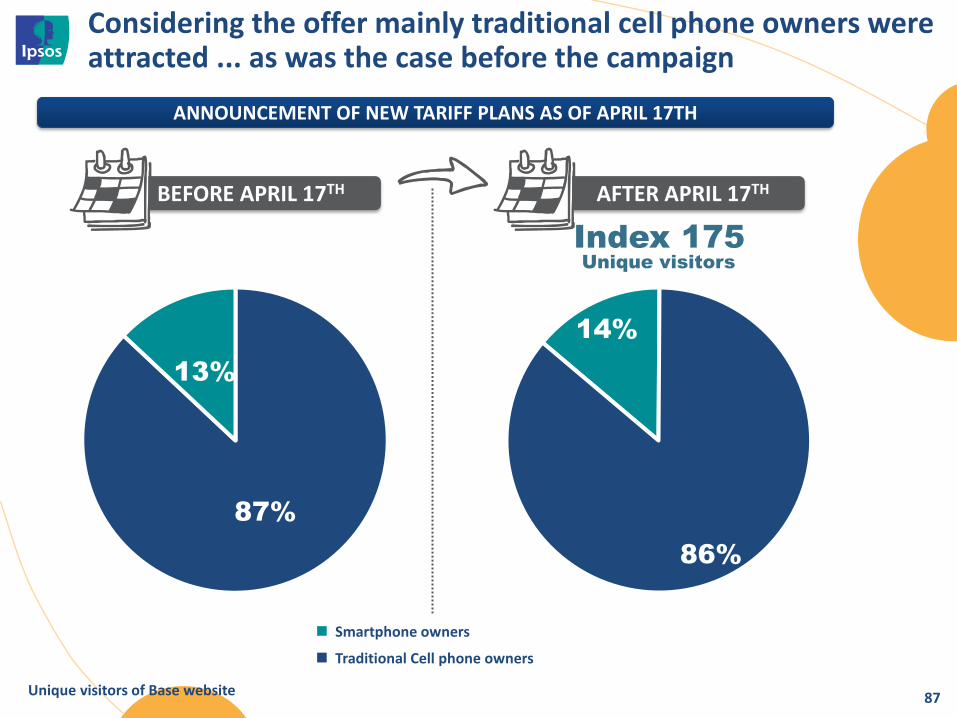

In April BASE announced it would turn the mobile telephone market upside down...

85

BUT WHO DID THEY ACTUALLY ATTRACT TO THEIR SITE?

The ad campaign generated more and a different competitive traffic towards the site: 71% of the visitors were non clients.

86

50% 50%

29%

14%

42% 14%

BEFORE APRIL 17TH AFTER APRIL 17TH

ANNOUNCEMENT OF NEW TARIFF PLANS AS OF APRIL 17TH

Own clients

Clients from major competitor X

Own clients

Clients from major competitor X

Clients from major competitor Y

Clients from major competitor Z

Index 175

Unique visitors

Unique visitors of Base website

Considering the offer mainly traditional cell phone owners were attracted ... as was the case before the campaign

87

87%

13%

14%

86%

BEFORE APRIL 17TH AFTER APRIL 17TH

ANNOUNCEMENT OF NEW TARIFF PLANS AS OF APRIL 17TH

Smartphone owners

Traditional Cell phone owners

Index 175

Unique visitors

Unique visitors of Base website

88

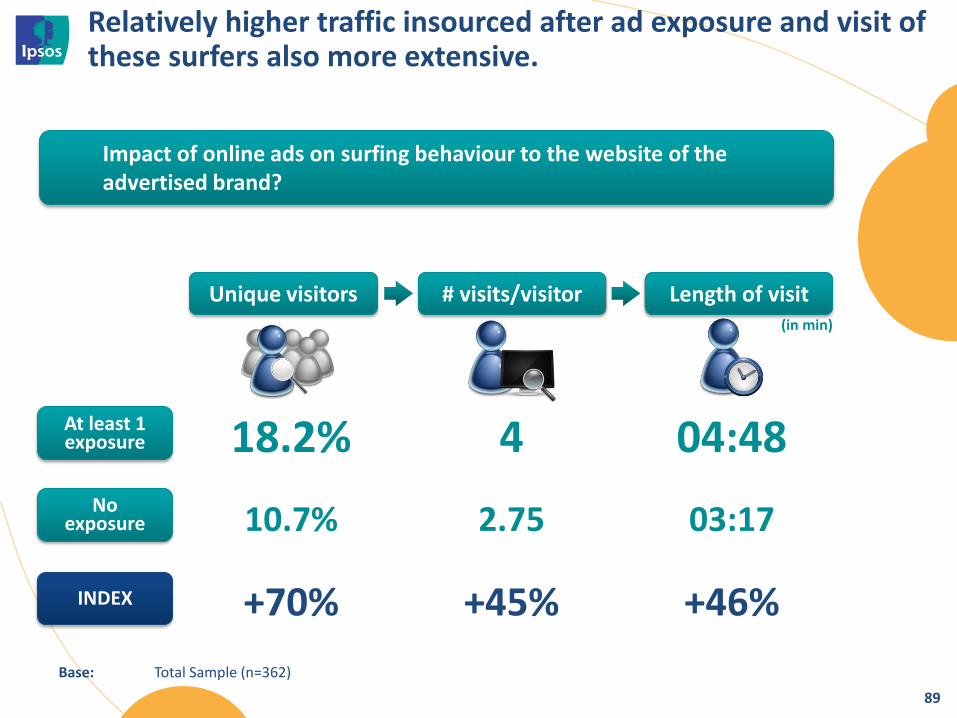

ING online campaign for free online account

18.2% 4 04:48

10.7% 2.75 03:17

+70% +45% +46%

89

Unique visitors # visits/visitor Length of visit

At least 1 exposure

No exposure

INDEX

Relatively higher traffic insourced after ad exposure and visit of these surfers also more extensive.

(in min)

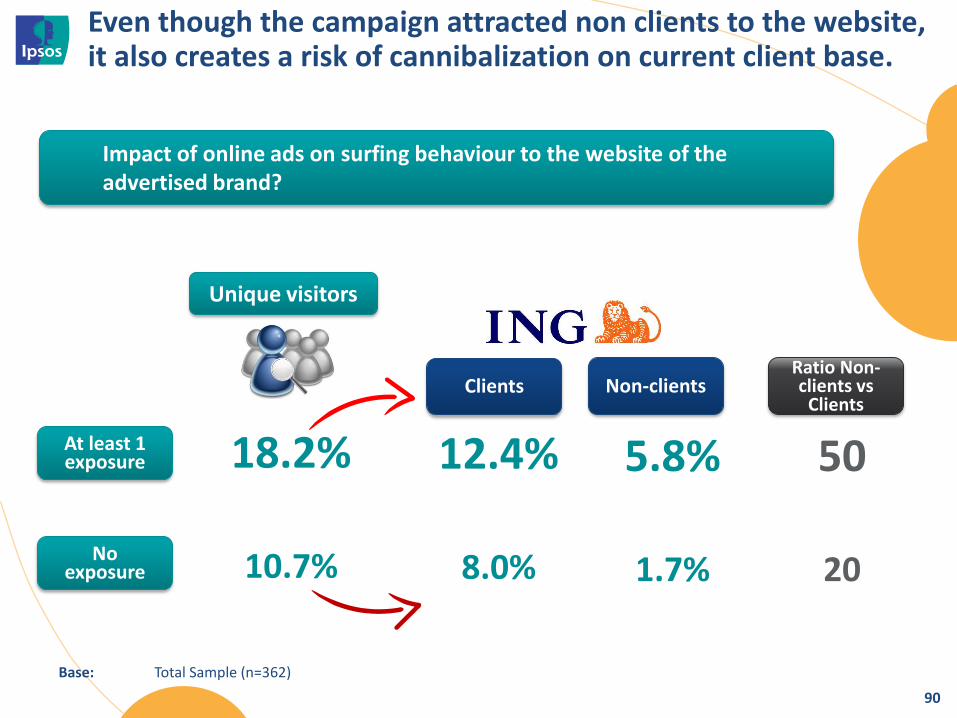

Impact of online ads on surfing behaviour to the website of the advertised brand?

Base: Total Sample (n=362)

18.2%

10.7%

90

Unique visitors

At least 1 exposure

No exposure

Even though the campaign attracted non clients to the website, it also creates a risk of cannibalization on current client base.

Impact of online ads on surfing behaviour to the website of the advertised brand?

Clients Non-clients

12.4%

8.0%

5.8%

1.7%

50

20

Ratio Non-clients vs

Clients

Base: Total Sample (n=362)

91

screens meet the

93

THEN ONE SCREEN FRONT AND CENTER

THEN ONE SCREEN FRONT AND CENTER

94

NOW SCREENS SURROUND US

of this world view

gain insight & understanding

created equal

screens are all important, but not

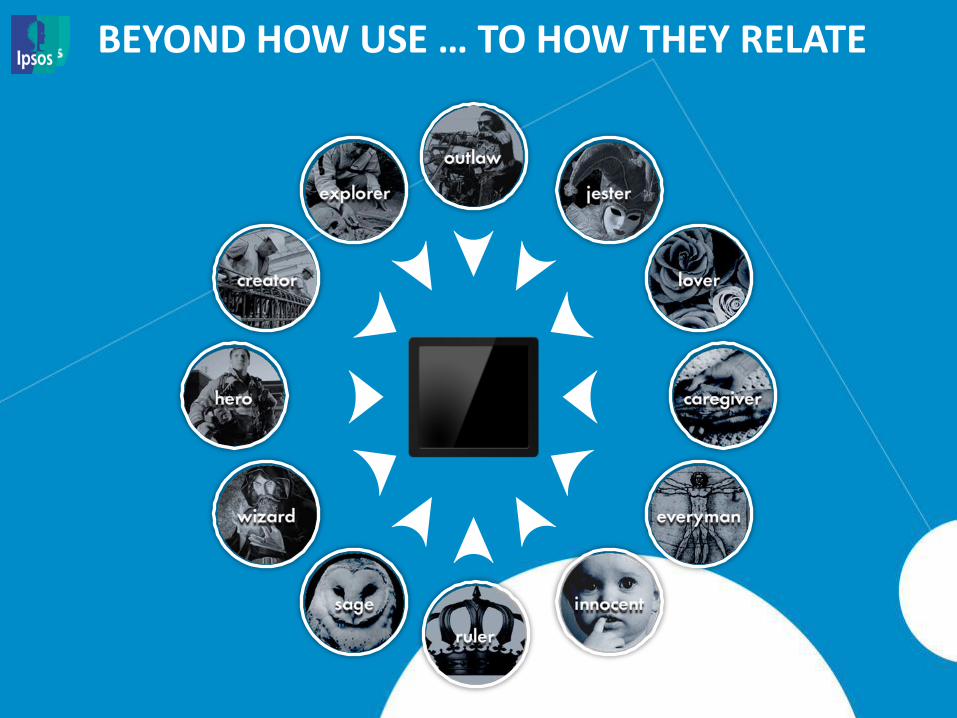

BEYOND HOW USE … TO HOW THEY RELATE

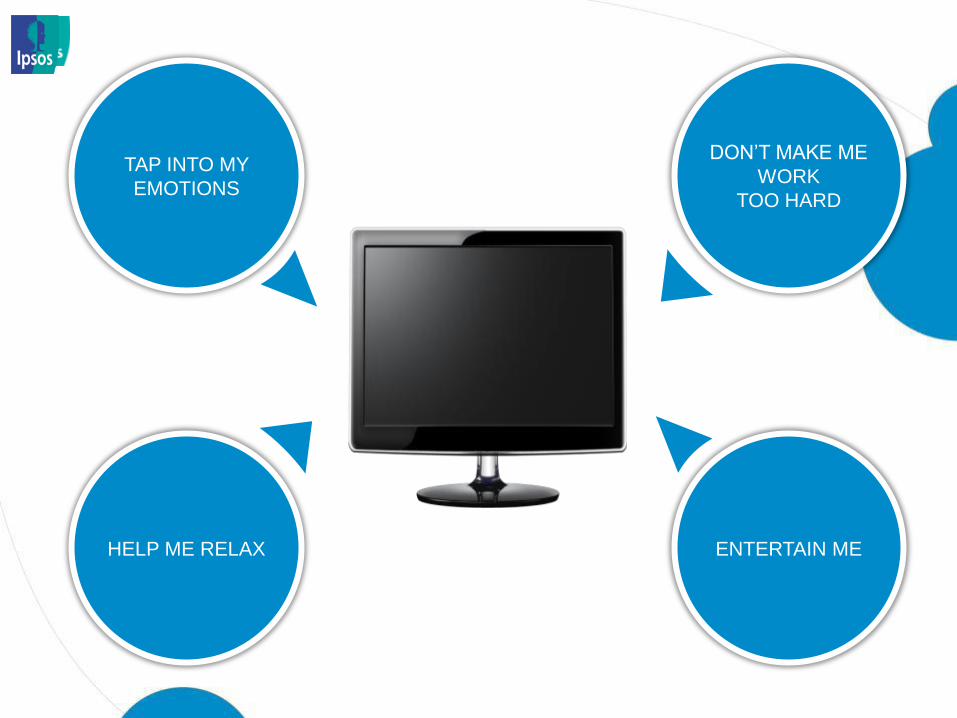

television the

TAP INTO MY

EMOTIONS

DON’T MAKE ME

WORK

TOO HARD

ENTERTAIN ME HELP ME RELAX

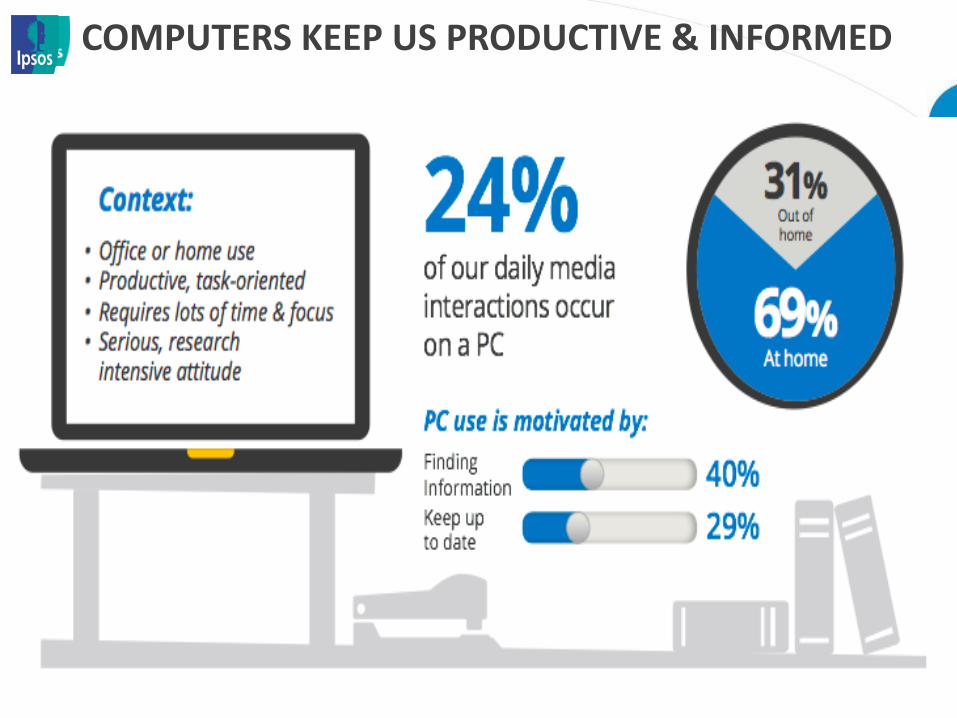

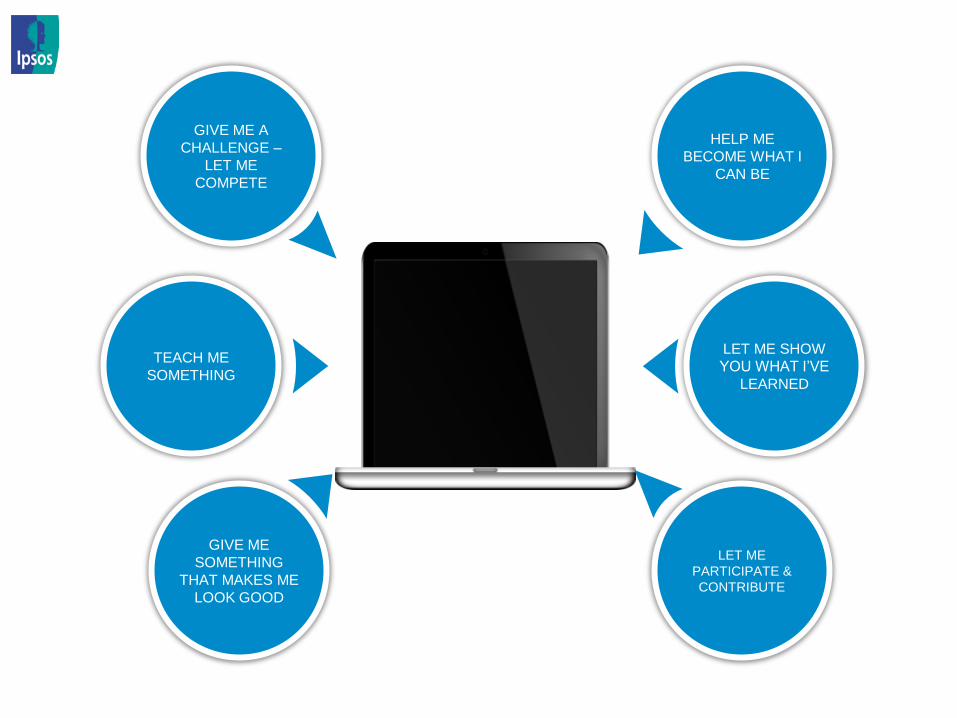

computer the

COMPUTERS KEEP US PRODUCTIVE & INFORMED

GIVE ME A

CHALLENGE –

LET ME

COMPETE

TEACH ME

SOMETHING

LET ME SHOW

YOU WHAT I’VE

LEARNED

HELP ME

BECOME WHAT I

CAN BE

LET ME

PARTICIPATE &

CONTRIBUTE

GIVE ME

SOMETHING

THAT MAKES ME

LOOK GOOD

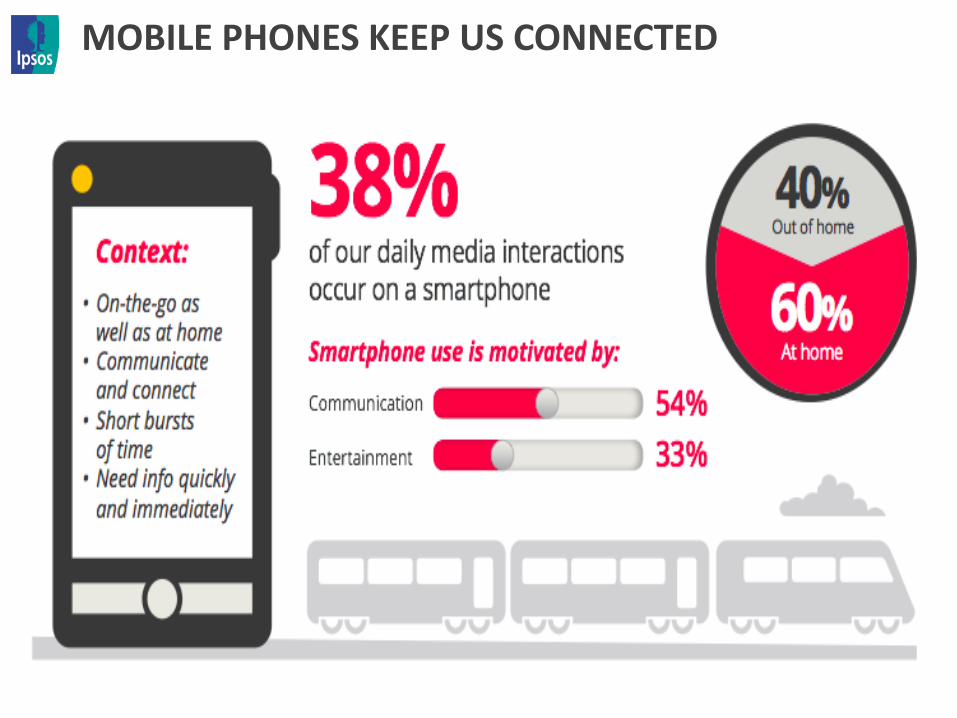

mobile the

MOBILE PHONES KEEP US CONNECTED

MAKE ME FEEL

LIKE I BELONG

HELP ME FIT IN

HELP ME MAKE

THE MOST OF

MYSELF

MUST KNOW ME

PERFECTLY

SURPRISE ME KEEP ME ON

TOP OF MY LIFE

the

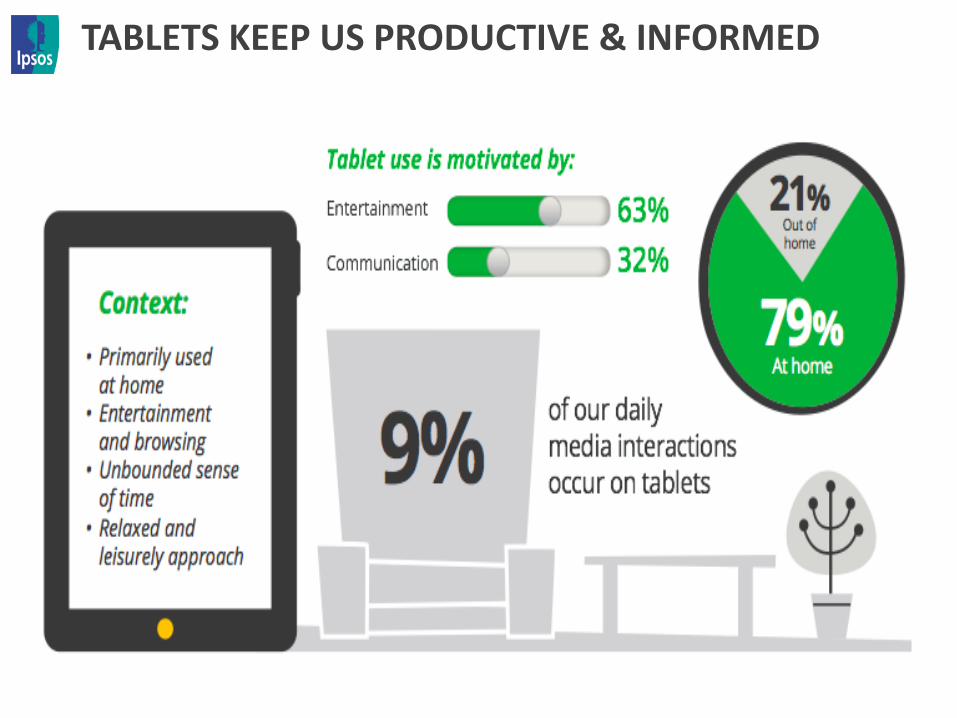

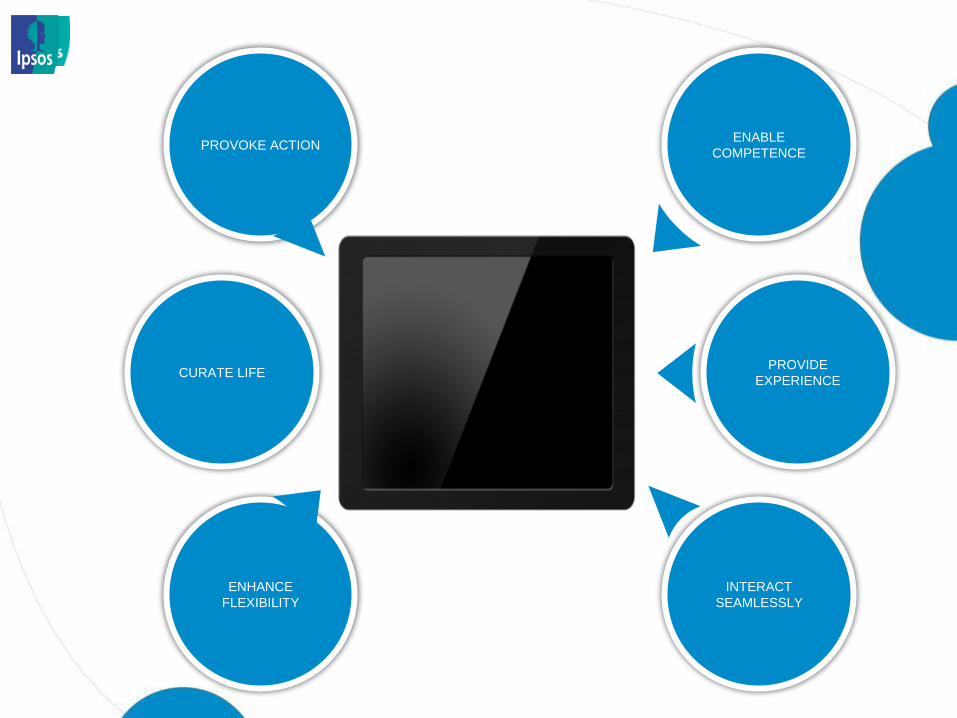

tablet

TABLETS KEEP US PRODUCTIVE & INFORMED

PROVOKE ACTION

CURATE LIFE PROVIDE

EXPERIENCE

ENABLE

COMPETENCE

INTERACT

SEAMLESSLY

ENHANCE

FLEXIBILITY

screens the four

EVERYMAN LOVER WIZARD

SAGE

SCREEN RELATIONSHIPS AREN’T MONOGAMOUS

the code has not been

cracked

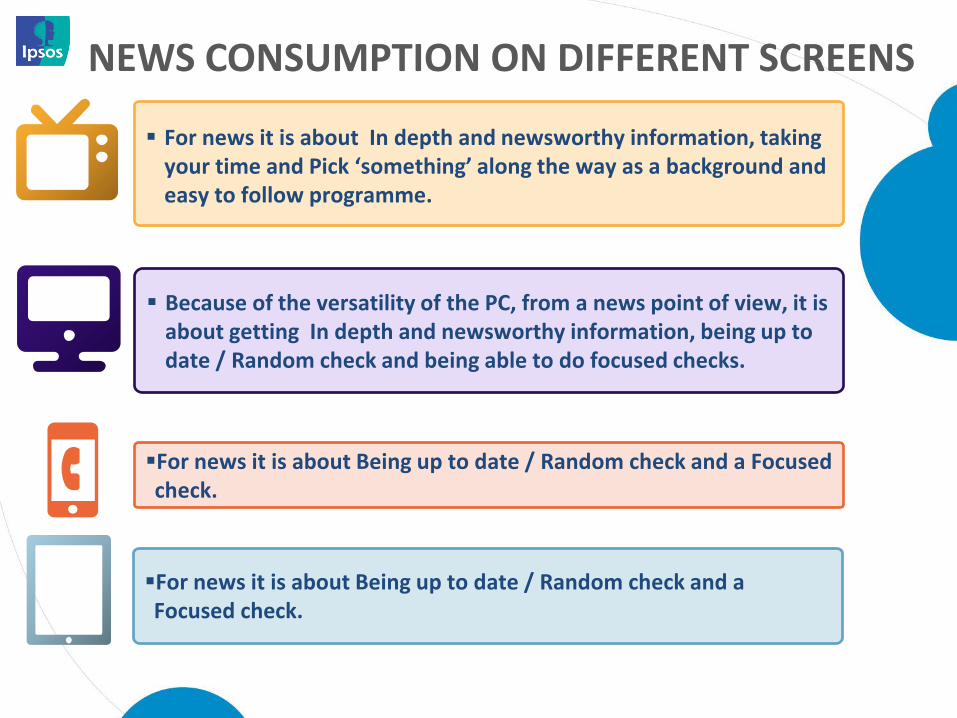

NEWS CONSUMPTION ON DIFFERENT SCREENS

For news it is about In depth and newsworthy information, taking your time and Pick ‘something’ along the way as a background and easy to follow programme.

Because of the versatility of the PC, from a news point of view, it is about getting In depth and newsworthy information, being up to date / Random check and being able to do focused checks.

For news it is about Being up to date / Random check and a Focused check.

For news it is about Being up to date / Random check and a Focused check.

SCREEN RESONANCE

INSPIRE HER The TV screen has the

most emotional relationship with her,

and where she is most open to influence.

TEACH HER The PC screen is the where she plans her

shopping, and is in her functional steps of finding the deals.

BE THERE The mobile screen is

the most intimate relationship and one she depends on real time as needs arise.

122

OUR MOBILE PLANET

Understanding the Mobile Consumer

Ipsos/Google - 05/2013

123

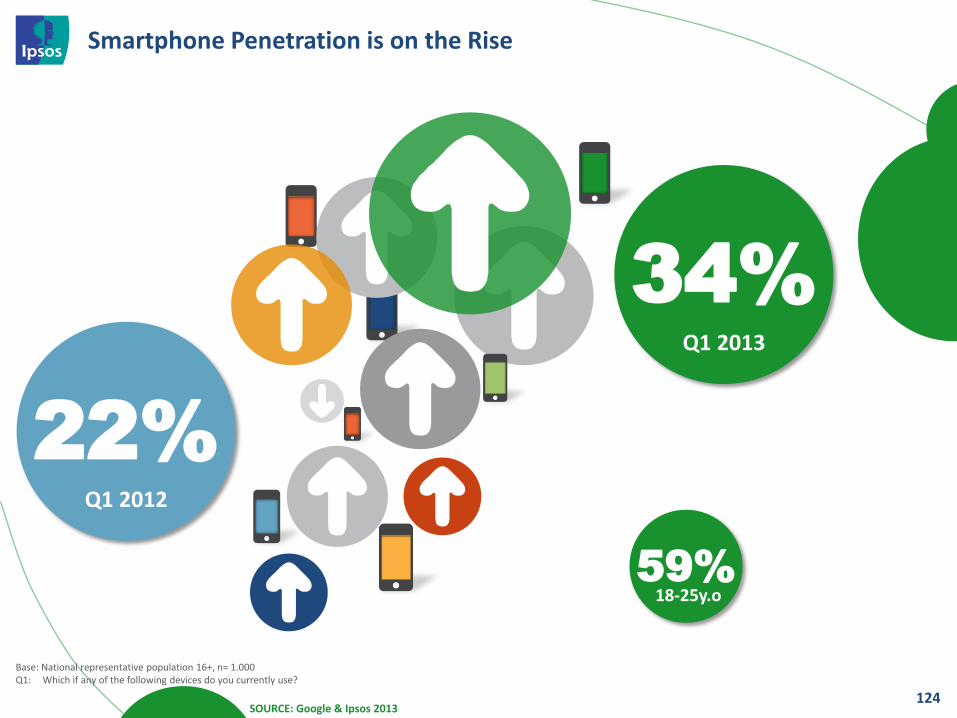

Smartphone Penetration is on the Rise

124

22%

Base: National representative population 16+, n= 1.000 Q1: Which if any of the following devices do you currently use?

SOURCE: Google & Ipsos 2013

Q1 2012

34% Q1 2013

59% 18-25y.o

Smartphones are a Central Part of Our Daily Lives

125

Have used their smartphone to go online every day in the past 7 days

54%

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q18: Thinking about the last seven days, on how many days were you online with ...?

SOURCE: Google & Ipsos 2013

Smartphones are Always On, Always with You

126

77% Don’t leave home without their device

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q52: To what extent do you agree to each of these statements?, Top2 Boxes; scale from 5 – completely agree to 1 – completely disagree. "I don’t leave house without my smartphone"

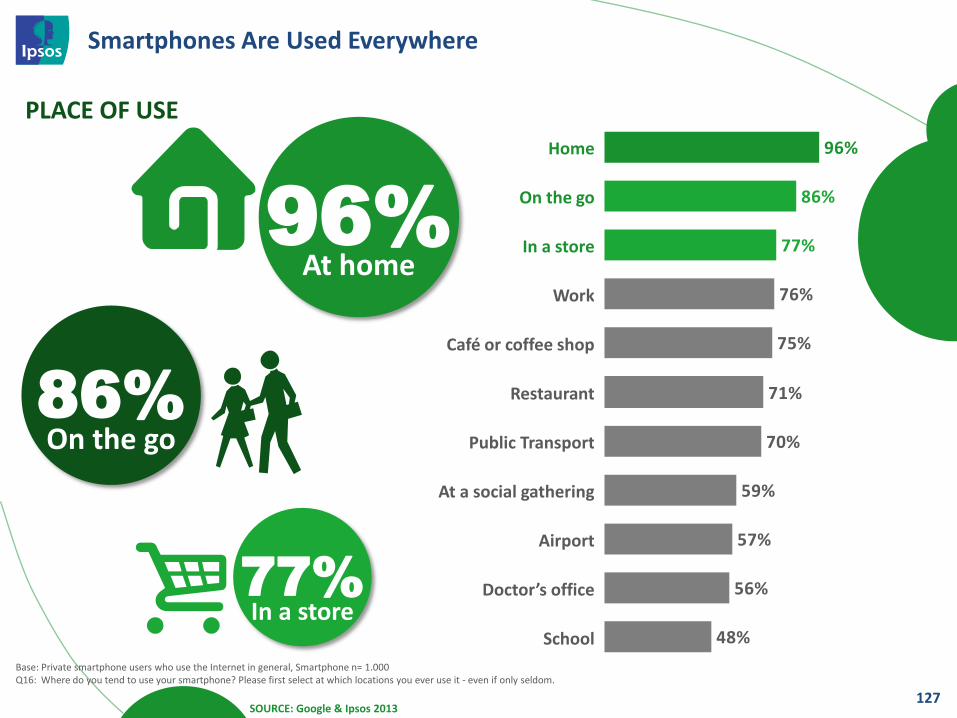

Smartphones Are Used Everywhere

127

76%

75%

71%

70%

59%

96%

86%

77%

48%

56%

57%

Home

On the go

In a store

Work

Café or coffee shop

Restaurant

Public Transport

At a social gathering

Airport

Doctor’s office

School

96% At home

86% On the go

77% In a store

PLACE OF USE

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q16: Where do you tend to use your smartphone? Please first select at which locations you ever use it - even if only seldom.

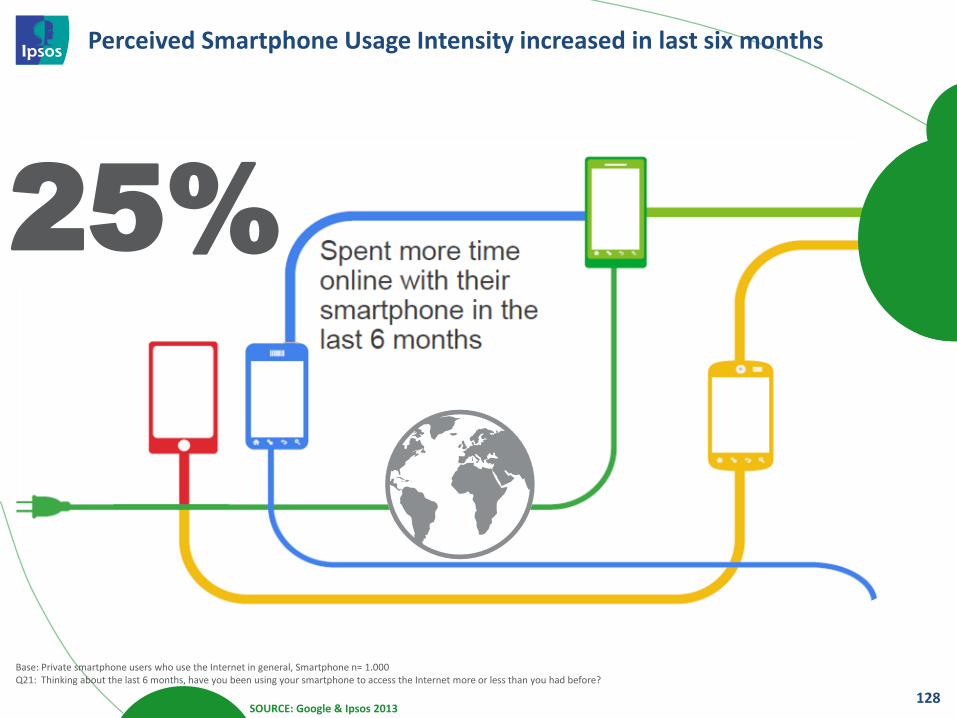

Perceived Smartphone Usage Intensity increased in last six months

128

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q21: Thinking about the last 6 months, have you been using your smartphone to access the Internet more or less than you had before?

SOURCE: Google & Ipsos 2013

25%

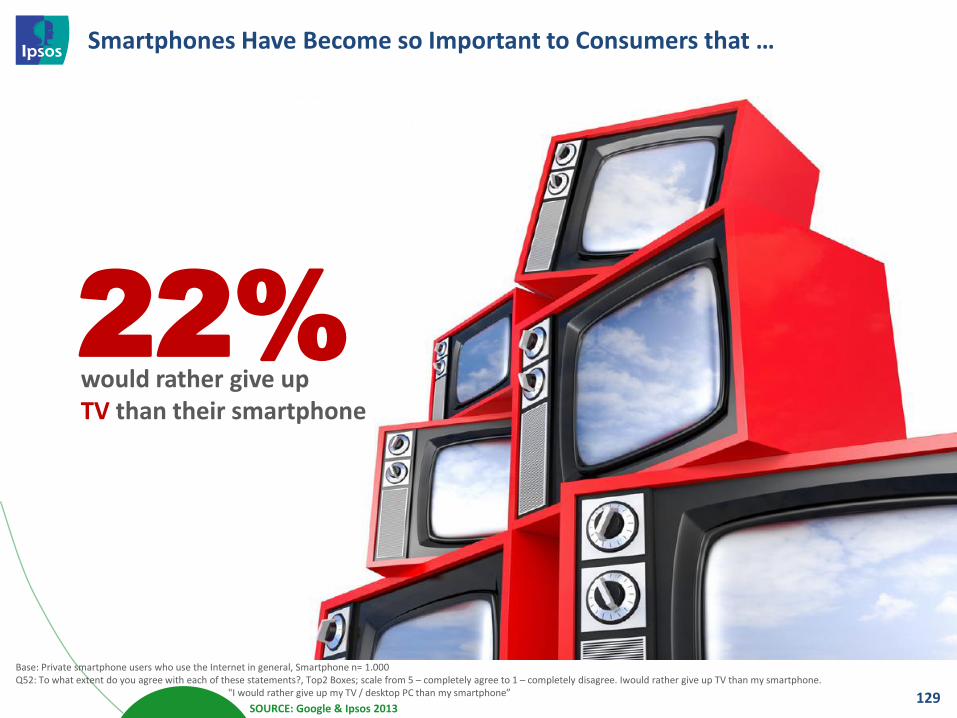

Smartphones Have Become so Important to Consumers that …

129

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q52: To what extent do you agree with each of these statements?, Top2 Boxes; scale from 5 – completely agree to 1 – completely disagree. Iwould rather give up TV than my smartphone. "I would rather give up my TV / desktop PC than my smartphone”

SOURCE: Google & Ipsos 2013

would rather give up TV than their smartphone

22%

130

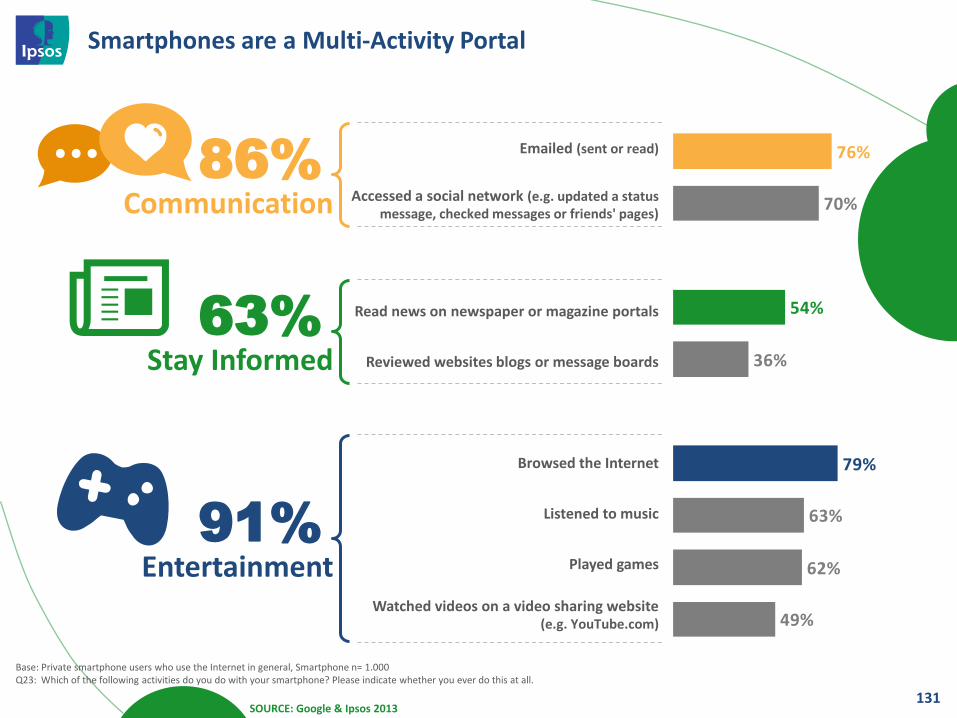

Smartphones are a Multi-Activity Portal

131

70%

36%

63%

79%

54%

76%

49%

62%

Emailed (sent or read)

Accessed a social network (e.g. updated a status message, checked messages or friends' pages)

Read news on newspaper or magazine portals

Reviewed websites blogs or message boards

Browsed the Internet

Listened to music

Played games

Watched videos on a video sharing website (e.g. YouTube.com)

Communication

Stay Informed

Entertainment

86%

63%

91%

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q23: Which of the following activities do you do with your smartphone? Please indicate whether you ever do this at all.

25

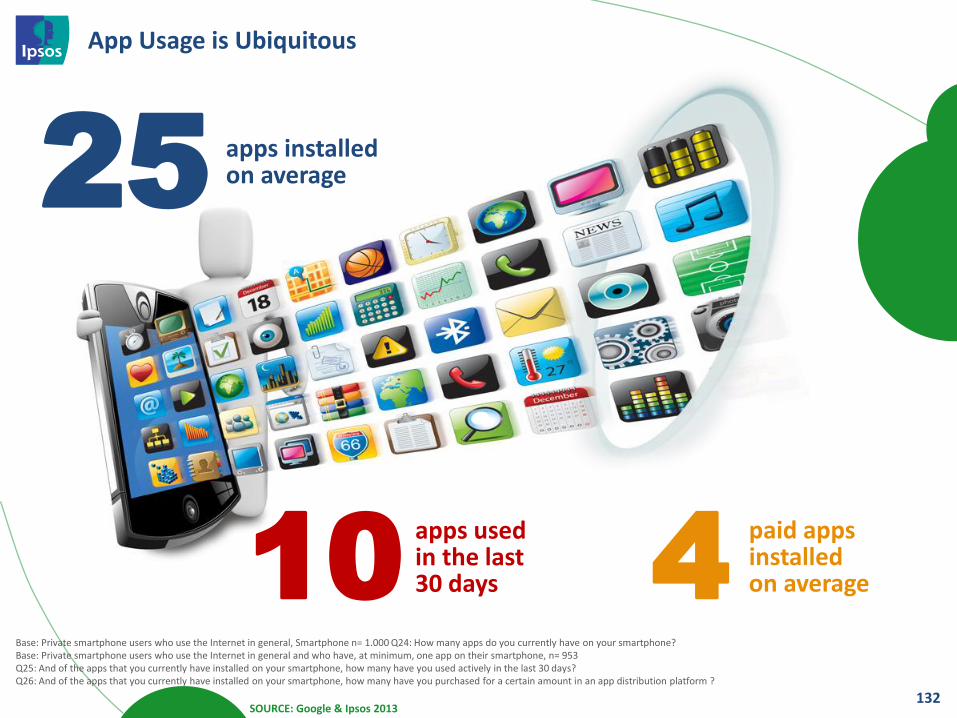

App Usage is Ubiquitous

132

apps installed on average

apps used in the last 30 days

paid apps installed on average 10 4

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q24: How many apps do you currently have on your smartphone? Base: Private smartphone users who use the Internet in general and who have, at minimum, one app on their smartphone, n= 953 Q25: And of the apps that you currently have installed on your smartphone, how many have you used actively in the last 30 days? Q26: And of the apps that you currently have installed on your smartphone, how many have you purchased for a certain amount in an app distribution platform ?

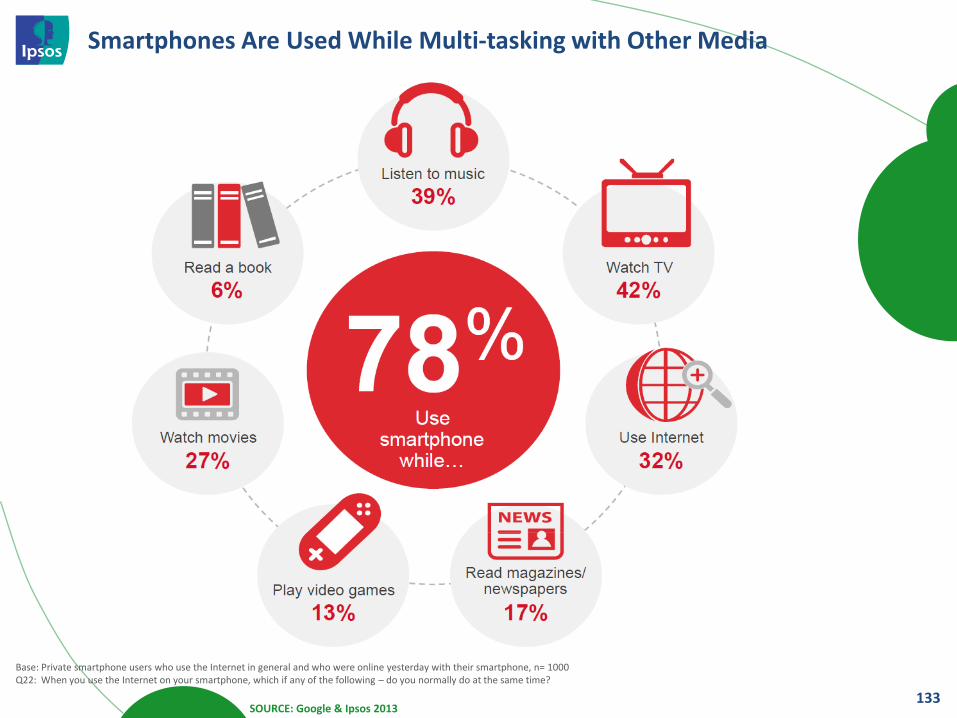

Smartphones Are Used While Multi-tasking with Other Media

133 SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general and who were online yesterday with their smartphone, n= 1000 Q22: When you use the Internet on your smartphone, which if any of the following – do you normally do at the same time?

134

135 SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q51a: And where were you when you researched for products or services with your smartphone?

have researched a product or service on their phone

66%

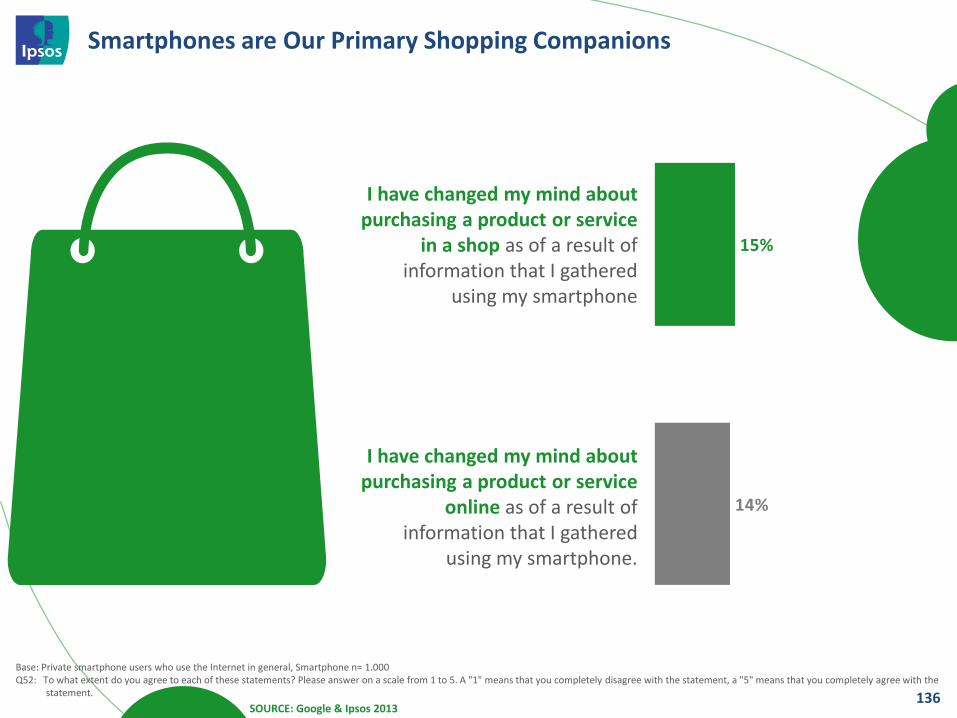

Smartphones are Our Primary Shopping Companions

136 SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q52: To what extent do you agree to each of these statements? Please answer on a scale from 1 to 5. A "1" means that you completely disagree with the statement, a "5" means that you completely agree with the statement.

I have changed my mind about purchasing a product or service

in a shop as of a result of information that I gathered

using my smartphone

I have changed my mind about purchasing a product or service

online as of a result of information that I gathered

using my smartphone.

14%

15%

Smartphones Are an Emerging Point of Purchase

137

of smartphone users have purchased a product or service on their smartphone

16%

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q44: Have you ever purchased a product or service over the Internet on your smartphone? By product or service we mean everything that you can buy excluding apps

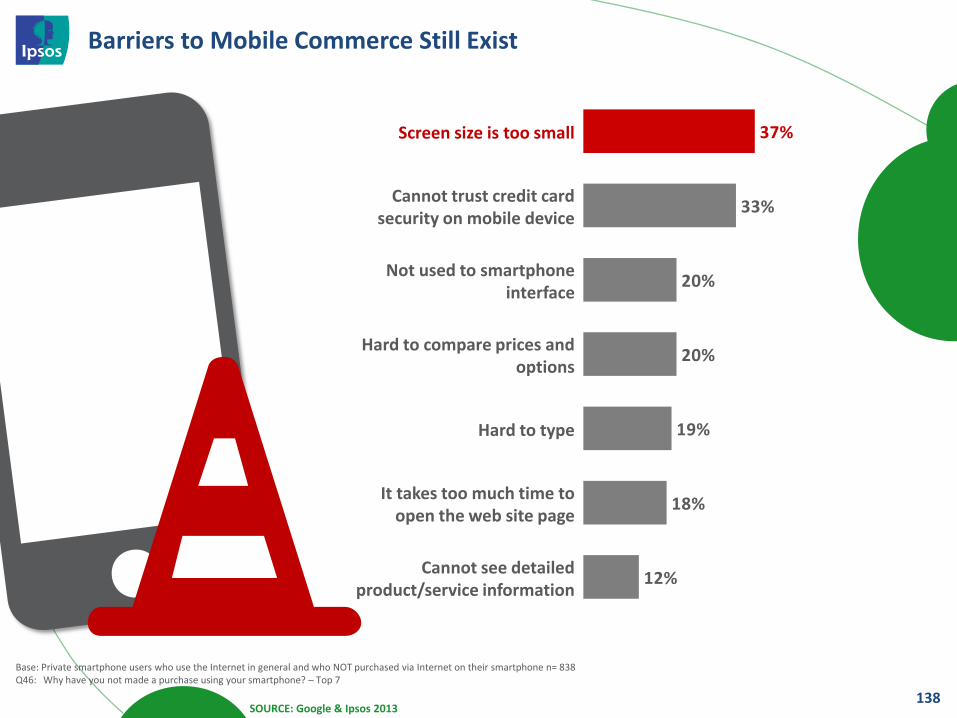

Barriers to Mobile Commerce Still Exist

138

33%

20%

19%

18%

12%

20%

37%Screen size is too small

Cannot trust credit card security on mobile device

Not used to smartphone interface

Hard to compare prices and options

Hard to type

It takes too much time to open the web site page

Cannot see detailed product/service information

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general and who NOT purchased via Internet on their smartphone n= 838 Q46: Why have you not made a purchase using your smartphone? – Top 7

139

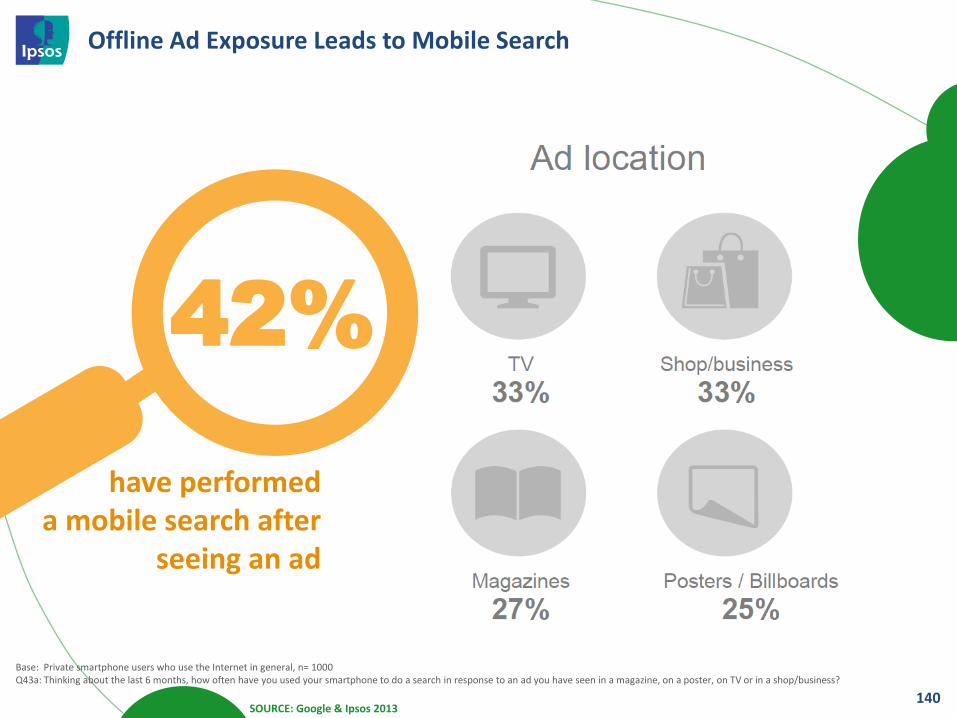

Offline Ad Exposure Leads to Mobile Search

140

have performed a mobile search after

seeing an ad

42%

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, n= 1000 Q43a: Thinking about the last 6 months, how often have you used your smartphone to do a search in response to an ad you have seen in a magazine, on a poster, on TV or in a shop/business?

141

84% of smartphone

users notice mobile ads

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general, Smartphone n= 1.000 Q41: How often do you notice advertising when you are using the browser or an app on your smartphone? (Ever)

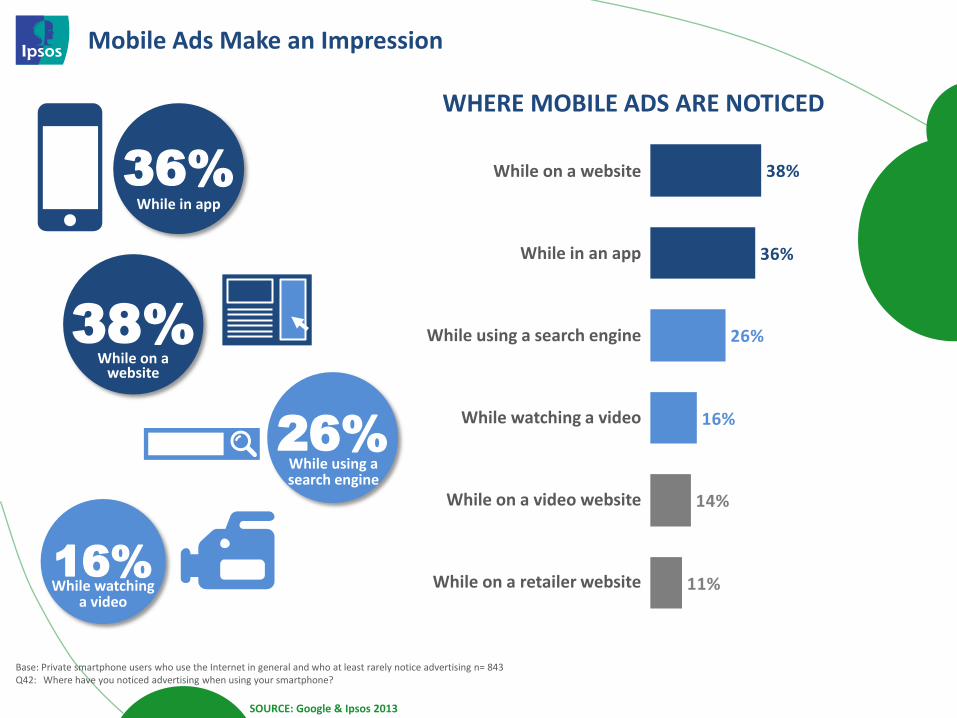

Mobile Ads Make an Impression

14%

11%

38%

36%

26%

16%

While on a website

While in an app

While using a search engine

While watching a video

While on a video website

While on a retailer website

WHERE MOBILE ADS ARE NOTICED

36% While in app

38% While on a

website

16% While watching

a video

26% While using a search engine

SOURCE: Google & Ipsos 2013

Base: Private smartphone users who use the Internet in general and who at least rarely notice advertising n= 843 Q42: Where have you noticed advertising when using your smartphone?

In Summary

143

• Consumers spent more and more time online consuming content through different devices

• Consumers have unlimited access to information (not all of this information is under ypur control)

• Smartphone penetration is booming, and the smartphone has taken in an important place in consumers life

Internet penetration

is higher than ever

144

• Understand the relationship between a “screen” and your consumer

• Every “screen” has its personality, adapt your communication to it and make information relevant

• Gather insights in the digital path to purchase

• Acknowledge the impact of comparing products and services, on professional comparison websites or user generated fora and blogs

• Provide relevant information in every step of the digital journey

Relevance is KEY

145