Embed Size (px)

Citation preview

LESSON 1: INTRODUCTION

Economics: An Introduction

Economics deals with the problem of scarcity. If society’s resources are abundant and

unlimited rather than scarce, then there would be no problem to study. Society would simply

produce anything and everything it needs at any point in time and everyone would have as

much of everything he desires. But this is not the case, for there is a basic and continuing

problem of scarcity that man and society are confronted with. Scarcity alone does not explain

completely the economic problem. Paired with a shortage of resources are the multiple

wants and desires of human beings.

Human beings have multiple wants and desires, resources have alternative uses. Scarce

resources need to be allocated among different needs. If human beings have only one

requirement (say food), coping with scarcity would require only how to get the most food out

of existing resources. However, since men need many more material items other than food,

there arises the problem of determining the optimum use of resources to satisfy competing

needs.

To summarize, scarcity of resources plus multiplicity of human wants equals economics. It is

obvious to anyone that, at any given time, at least some resources (e.g. land or capital) are

scarce and that human wants are almost unlimited. Thus, it is hard to deny the importance of

economics both today and in the future.

Definition:

1. Economics is the study of how societies use scarce resources to produce valuable

commodities and distribute them among different people.

2. Economics may be defined as a science that deals with the activities of man in

obtaining wealth for the satisfaction of his wants.

3. Economics is the art of making a living.

4. Economics is the proper allocation and efficient use of available resources for the

maximum satisfaction of human wants.

5. Economics is the branch of social science that deals with the production and

distribution and consumption of goods and services and their management.

6. Economics is the science that deals with the production, distribution, and consumption

of wealth, and with the various related problems of labor, finance, taxation, etc. (Webster's

New World)

7. Economics is the study of choice and decision-making in a world with limited

resources.

8. Right and prudent administration of assets, Public wealth, set of services and

economic interests.

9. The study of the choices people make to cope with scarcity.

10. Economics is the study of how to use our limited resources to satisfy our unlimited

wants as fully as possible.

Division of Economics:

Microeconomics is that branch of economics that deals with the economic behavior of

individual units such as consumers, firms and the owners of the factors of production, for

example, the price of rice, the number of workers of PLDT, the income of Mr. Dorig, etc.

Micro means small, thus microeconomics deals with the study of the small units of the

economy.

Macroeconomics is that branch of economics that deals with the economic behavior of the

whole economy such as government, business and household. Examples of macroeconomic

studies are national income, employment and inflation.

Microeconomics and macroeconomics are closely related, for example, compared with the

human body, the microeconomic units are the heart, kidney, lungs and other parts. The

macroeconomic unit is the human body. A defect in part of the human body affects the whole

body. The same is true in the operation of economics.

History of Economics:

It has started to be known when Adam Smith’s book Wealth of Nations was published in 1776.

Prior to that, economics has been integrated into other fields such as religion, philosophy

and political science. That book became the bible of economics for more than a century.

Adam Smith was responsible for the recognition of economics as a separate body of

knowledge. Economics have been as old as mankind. It started when God drove Adam and

Eve away from the Garden of Eden. Economic thoughts appeared in biblical teachings,

philosophy and politics. The primitive people invented ways and means of food gathering

and hunting. Such art of making a living among the ancient tribes represented a form of

economics.

The word “economics” has been derived from the Greek word oikonomia. It means

household management. The housekeeper has to see to it that there is enough food, clothing

and shelter; that the house is kept in order; that the necessary duties and responsibilities are

performed by the members of the household; and that their products are distributed

according to necessity. To the ancient Greeks, the term oikonomos applied more on the

proper management of the city-states. As a science, economics emerged only in 1776

Basic Economics Problem:

1. What goods and services to produce and how much?

A society must determine how much of each of the many possible goods and services it will

make, and when they will be produced. Will we produce frozen pizzas or shirts today? A few

high-quality shirts or many cheap shirts? Will we use scarce resources to produce many

consumption goods (like frozen pizzas)? Or will we produce fewer consumption goods and

more investment goods (like pizza-making machines, which will boost production and

consumption tomorrow.

2. How to produce the goods and services?

It has to do with production and technology. As a general rule, goods and services must be

produced in the most efficient manner. This means maximum output with minimum input

without sacrificing quality. The application of modern technology has increased output and

decreased cost of production. The use of advanced technology will create more

unemployment.

3. For whom are the goods and services?

One key task for any society is to decide who gets to eat the fruit of the economy’s efforts.

How is the national product divided among different households? Are many people poor and

a few rich? Do high incomes go to managers or workers or landlords? Do the sick or elderly

eat well, or are they left to fend for themselves?

Economic System Model:

Economic system is a set of economic institutions that dominates a given economy.

An institution is a set of rules of conduct, established ways of thinking, or ways of doing

things.

The purpose of an economic system is to solve the basic economic problems. The main goal

of economic system is high standard of living for all its citizens.

1. Capitalism

Here, the factors of production and distribution are owned and managed by private

individuals or corporations. We can use different terms like market economy, free-enterprise

economy, or laissez faire economy for capitalism. The essential characteristics of capitalism

are:

Private property

Economic freedom

Free competition

Profit motive

2. Communism

It is the opposite of capitalism. The factors of production and distribution are owned and

managed by the state. It is also known as the command economy or classless economy. The

essential characteristics of communism are:

No private property

No economic freedom

Presence of central planning

No free competition

No profit motive.

3. Socialism

It is a combination of capitalism and communism. The major industries are owned and

managed by the state while the minor industries belong to the private sector.

How to Judge a Economic System:

The vital criteria to judge an economic system is as follows:

1. Abundance

2. Growth

3. Stability

4. Security

5. Efficiency

6. Justice and equity

7. Economic freedom

The Goals of Economics:

1. Economic growth

2. Full employment

3. Price stability

4. Economic freedom

5. Equitable distribution of wealth and income

6. Economic security

LESSON 2: THEORY OF WANTS

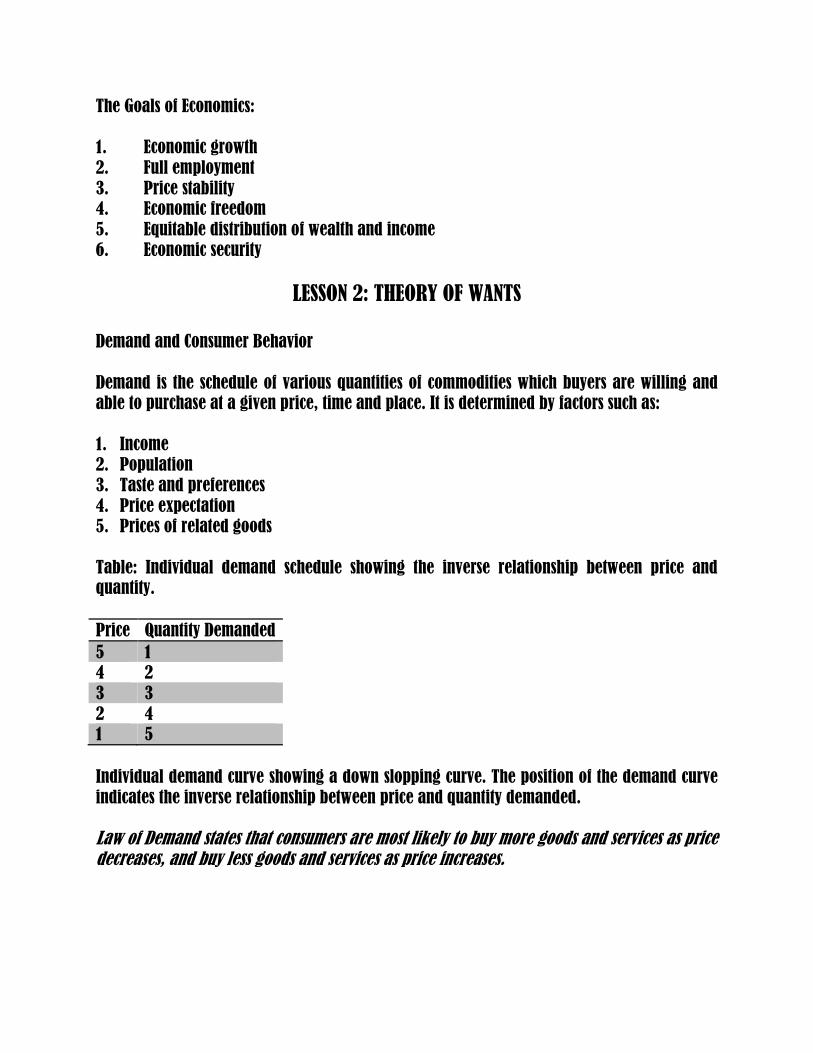

Demand and Consumer Behavior

Demand is the schedule of various quantities of commodities which buyers are willing and

able to purchase at a given price, time and place. It is determined by factors such as:

1. Income

2. Population

3. Taste and preferences

4. Price expectation

5. Prices of related goods

Table: Individual demand schedule showing the inverse relationship between price and

quantity.

Price Quantity Demanded

5 1

4 2

3 3

2 4

1 5

Individual demand curve showing a down slopping curve. The position of the demand curve

indicates the inverse relationship between price and quantity demanded.

Law of Demand states that consumers are most likely to buy more goods and services as price decreases, and buy less goods and services as price increases.

Validity of the Law of Demand

The law of demand states: as price increases, quantity demanded decreases, and as price

decreases, quantity demanded increases. Such theory is only true if the assumption of ceteris

paribus is applied. It means “all other things equal or constant.” The law of demand is

correct if the determinants of demand are held constant. That is there is no change in

income, taste or population.

Elasticity of Demand

Demand elasticity refers to the reaction or response of the buyers to changes in price of

goods and services. There are five types of demand elasticity to price changes of goods and

services:

1. Elastic demand. A change in price results to a greater change in quantity demanded. For

example, a 10% change in price (increase or decrease) creates a 20% change in quantity

demanded (increase or decrease). This means that the buyers are very sensitive to price.

2. Inelastic demand. A change in price results to a lesser change in quantity demanded. For

example, a 20% change in price creates a 5% change in quantity demanded. This means

that buyers are not sensitive to price change.

3. Unitary demand. A change in price results to an equal change in quantity demanded. For

example, a 10% change in price results to a 10% change in quantity demanded.

4. Perfectly elastic demand. Without change in price, there is an infinite change in quantity

demanded. Such situation occurs in a purely competitive market.

5. Perfectly inelastic demand. A change in price creates no change in quantity demanded.

Determinants of Demand Elasticity

1. Number of good substitutes. Demand is elastic for a product with many substitutes. An

increase in the price of such product induces the buyers to look for good substitutes.

2. Price increase in proportion to income. If the price increase has very little effect on the

income or budget of the buyers, demand is inelastic. But if the price increase involves a

substantial amount in proportion to the income of consumers, demand is elastic.

3. Importance of the product to the consumers. Luxury goods are not very important to

majority of the people. On the other hand, the essential goods are very important to

people. Rice is important to Filipinos, Electricity is important to factory owners and

gasoline is important to transportation industry. All of these are inelastic.

Theory of Consumer Behavior

1. Law of diminishing marginal utility. The law states that as the amount of the good

consumed increases, the marginal utility of that good tends to diminish. Marginal utility

refers to the additional satisfaction of a consumer whenever he consumes one more unit

of the same good. For example, the first unit of a good like ice cream gives you a certain

level of satisfaction or utility. Now imagine consuming a second unit. Your total utility

goes up because the second unit of the good gives you some additional utility. What about

adding a third or fourth unit of the same good? Eventually if you eat enough ice cream,

instead of adding utility, it makes you sick. This leads us to the fundamental economic

concept of marginal utility.

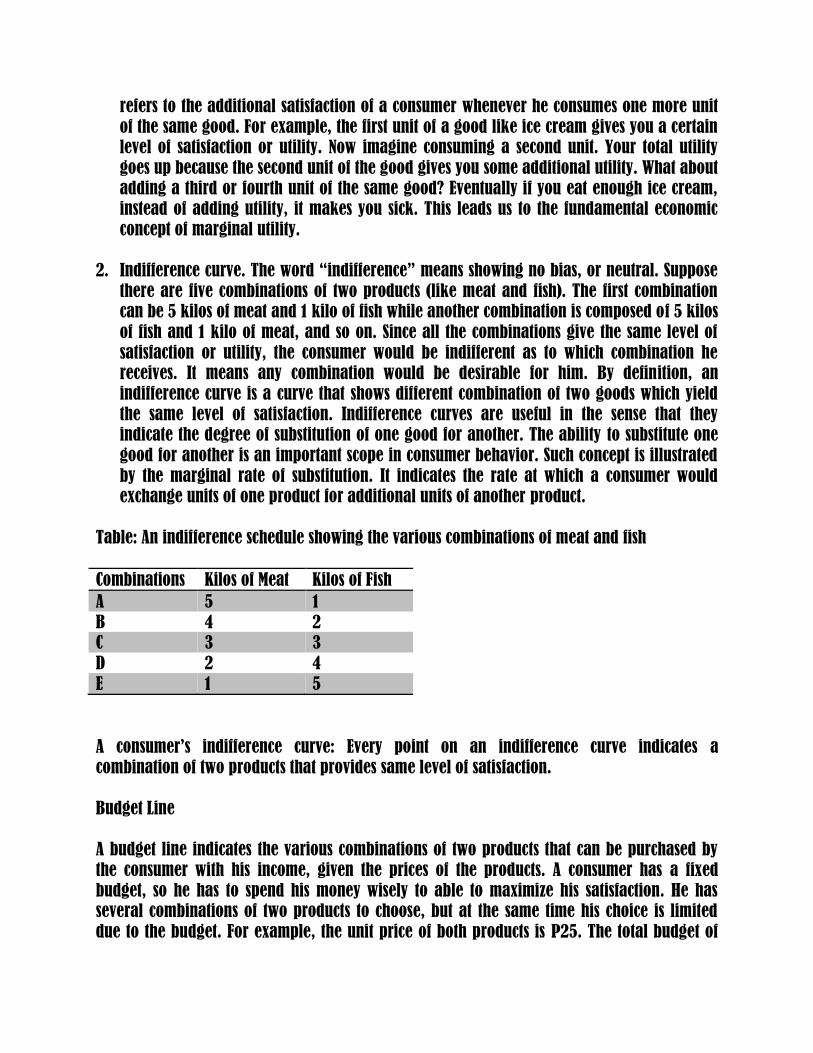

2. Indifference curve. The word “indifference” means showing no bias, or neutral. Suppose

there are five combinations of two products (like meat and fish). The first combination

can be 5 kilos of meat and 1 kilo of fish while another combination is composed of 5 kilos

of fish and 1 kilo of meat, and so on. Since all the combinations give the same level of

satisfaction or utility, the consumer would be indifferent as to which combination he

receives. It means any combination would be desirable for him. By definition, an

indifference curve is a curve that shows different combination of two goods which yield

the same level of satisfaction. Indifference curves are useful in the sense that they

indicate the degree of substitution of one good for another. The ability to substitute one

good for another is an important scope in consumer behavior. Such concept is illustrated

by the marginal rate of substitution. It indicates the rate at which a consumer would

exchange units of one product for additional units of another product.

Table: An indifference schedule showing the various combinations of meat and fish

Combinations Kilos of Meat Kilos of Fish

A 5 1

B 4 2

C 3 3

D 2 4

E 1 5

A consumer’s indifference curve: Every point on an indifference curve indicates a

combination of two products that provides same level of satisfaction.

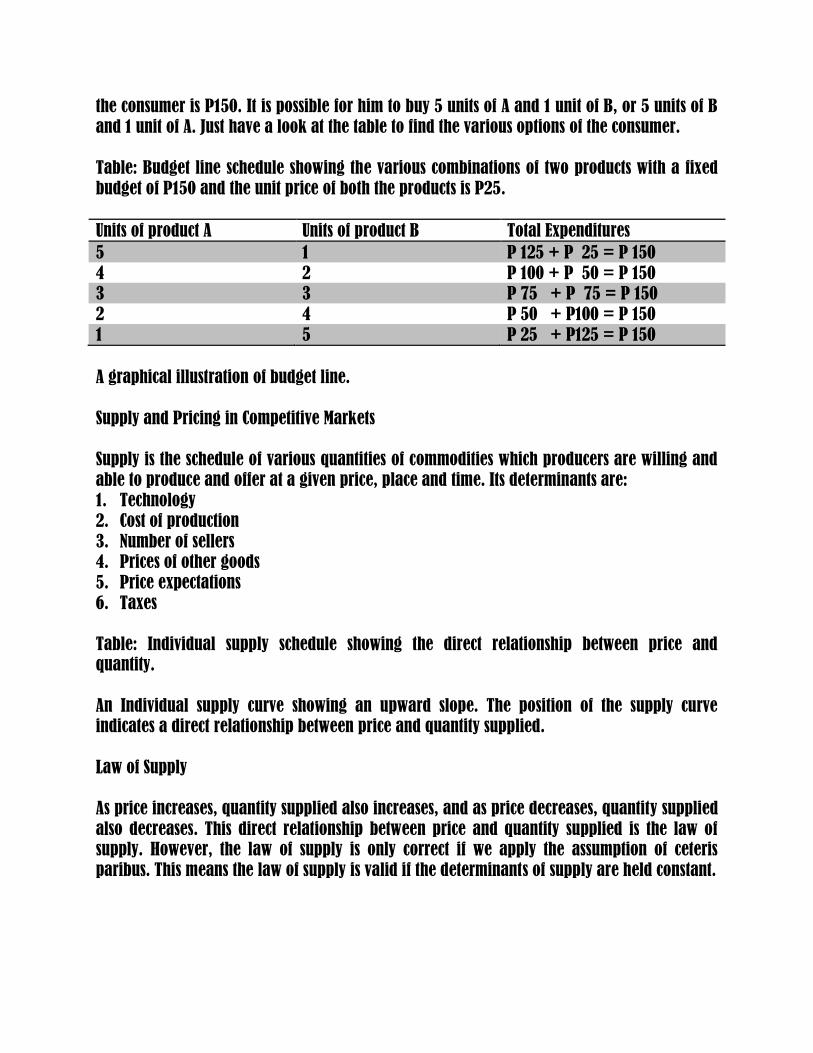

Budget Line

A budget line indicates the various combinations of two products that can be purchased by

the consumer with his income, given the prices of the products. A consumer has a fixed

budget, so he has to spend his money wisely to able to maximize his satisfaction. He has

several combinations of two products to choose, but at the same time his choice is limited

due to the budget. For example, the unit price of both products is P25. The total budget of

the consumer is P150. It is possible for him to buy 5 units of A and 1 unit of B, or 5 units of B

and 1 unit of A. Just have a look at the table to find the various options of the consumer.

Table: Budget line schedule showing the various combinations of two products with a fixed

budget of P150 and the unit price of both the products is P25.

Units of product A Units of product B Total Expenditures

5 1 P 125 + P 25 = P 150

4 2 P 100 + P 50 = P 150

3 3 P 75 + P 75 = P 150

2 4 P 50 + P100 = P 150

1 5 P 25 + P125 = P 150

A graphical illustration of budget line.

Supply and Pricing in Competitive Markets

Supply is the schedule of various quantities of commodities which producers are willing and

able to produce and offer at a given price, place and time. Its determinants are:

1. Technology

2. Cost of production

3. Number of sellers

4. Prices of other goods

5. Price expectations

6. Taxes

Table: Individual supply schedule showing the direct relationship between price and

quantity.

An Individual supply curve showing an upward slope. The position of the supply curve

indicates a direct relationship between price and quantity supplied.

Law of Supply

As price increases, quantity supplied also increases, and as price decreases, quantity supplied

also decreases. This direct relationship between price and quantity supplied is the law of

supply. However, the law of supply is only correct if we apply the assumption of ceteris

paribus. This means the law of supply is valid if the determinants of supply are held constant.

Elasticity of Supply

Supply elasticity refers to the response of the sellers/ producers to price change of goods.

There are five types of elasticity of supply or types of responses of producers to price changes:

1. Elastic supply. A change in price results to a greater change in quantity supplied. This

means that producers are very responsive to price change. For example, with a 10%

increase in price, they increase their quantity supplied by 20%.

2. Inelastic supply. A change in price results to a lesser change in quantity supplied. This

shows that producers have very weak response to price change.

3. Unitary supply. A change in price results to equal change in quantity supplied.

4. Perfectly elastic supply. Without change in price, there is an infinite change in quantity

supplied.

5. Perfectly inelastic supply. A change in price has no effect on quantity supplied.

Determinant of Supply Elasticity

The determinant of supply elasticity is the time involved in the ability of producers to

response to price changes. If it takes a short time to produce the products to take an

advantage of an increase in price, then supply is elastic. On the other hand, if it takes a long

time to produce the products, then supply is inelastic. Agriculture or farm products are highly

inelastic.

The Law of Supply and Demand

The law of supply and demand states that when supply is greater than demand, price

decreases. When demand is greater than supply, price increases. When supply is equal to

demand, price remains constant. This is the market price or the equilibrium price. It means

that both sellers and buyers have mutual agreement.

LESSON 3: ANALYSIS PRICE SYSTEM

Analysis of the Price System

One favorable argument for the price system is its efficiency in distributing goods and

services. On the part of the producers, they tend to produce those products that give them

maximum profits. On the other hand, the consumers are inclined to purchase those products

that provide them maximum satisfaction. In the process of free competition, the best methods

of production and marketing are developed and used in order to increase output and reduce

unit cost of production. Thus the goal of profit maximization becomes attainable. At the same

time, the welfare of the consumers is enhanced because they are the beneficiaries of quality

products at low prices.

Another argument in favor of price system is the presence of personal freedom. Producers

are free to produce any product to satisfy their own economic interests as long as those do

not conflict with legal and moral traditions. Other freedoms include the free choice of

workers or employees. Employees are also free to choose their employers. Buyers are also

free to purchase any product that gives them maximum satisfaction.

Criticisms against the Price System

As a matter of fact, the free competition does not exist long enough. Self-interests of

businessmen force them to drive away their rivals through competition. Another strategy is to

merge their companies for market advantage. The small ones find it difficult to compete with

the big ones. In the process of competition, the big companies become the price leaders.

Another case against the price system is the unfair distribution of goods and services. Only

the very few rich can have a decent life under the price system. Moreover, social goods like

anti-pollution, rural electrification, irrigation, or highways cannot be allocated efficiently

through the price system. Usually these require a huge financing, and yet the returns of

investment take a long time and profits may not be attractive. Hence, only the government is

willing to undertake such projects.

The Role of the Government

Keeping in mind the limitations of the price system, the government has to regulate and

supervise production, distribution and consumption of goods and services. The government

provides incentives in the production of goods and services that greatly contribute to the

socio-economic development of the country. The government interferes in the allocation of

the goods and services in order to protect the welfare of the poor. At the same time, the

government has to control the consumption of goods and services that are wasteful and

detrimental to the growth of the economy. In developing countries, the role of the

government is more active. Infrastructures like roads, bridges, communication facilities,

electrification, schools and hospitals have to be set up. These speed up the process of

economic growth. Economic growth means more employment, production and income. And

this situation leads to the high standards of living.

LESSON 4: PRODUCTION Production

Production is the creation of goods and services to satisfy human wants. The factors of

production are called the inputs of production, and the goods and services that have been

created by the inputs are called the outputs of production. The factors of production are

classified as fixed factor (fixed input) and variable factor (variable input). A fixed factor

remains constant regardless of the volume of production. In case of variable factor, it

changes in accordance with the volume of production. The process of transforming both fixed

and variable inputs into finished goods and services is called the theory of production. The

technical relationship between the application of inputs and the resulting maximum

obtainable output is known as the production function.

Kinds of Utilities in Production

Form Utility. Utility could be increased in a certain commodity by changing its form. Raw

materials are indeed useful, but they could be made more useful by reshaping them. Trees in

the forest serve man in one way or another, but they are of little use to him unless the

lumberman cuts them down and saws them into boards. Fresh fish can satisfy our want for

food better if it is properly cooked to suit our taste. Coal and iron extracted from the bowels

of the earth keep us warm and provide us with the raw materials for our tools and

machinery. Lumbering, fishing, mining, all of these so-called extractive industries create

form utility. Agriculture is another industry that creates form utility. The farmer, by careful

preparation and fertilization of the soil, produces all sorts of crops.

Place Utility. Goods can be made more desirable by moving them about. Matter in the wrong

place is dirt, but in the right place it is wealth. After harvesting the crop, it is of little use to

the farmer unless it is brought to town and sold to the people who consume it.

Possession Utility. The rice in the granary of the farmer, after satisfying his needs for that

commodity will not be as useful as when it is brought to market and sold to the final

consumers. Similarly, an automobile in the shop of the dealer is not as useful as in the hands

of the person who needs a car. The selling of the rice or of the car is an activity that creates

what is known as possession utility.

Time Utility. Time is an important factor that influences the utility of goods. There are some

utilities that cannot be kept for a long time and wait to satisfy the maximum need for them.

During the mango or lansones season, great quantities of these fruits go to waste or

command a very low price. They can be more useful when they are preserved in their natural

state for consumption after the harvest season. Fish does not keep long after being taken off

the water; it is a very perishable commodity. The same may be said of meat, vegetables and

other commodities. The development of cold storage and refrigeration has partly solved the

problem of preserving these perishable commodities until such time as they are more useful.

Service Utility. Production is not only confined to material goods but also to immaterial goods

or services. There are many persons who never handle material goods but are considered

productive because they create certain utilities by rendering valuable and necessary services

to the community; they are engaged in service production. The people engaged in the so-

called learned professions and those who render personal services create service utility. The

services of professors, lawyers, doctors, priests and ministers, singers, dancers, government

officials and also those of servants, cooks, waiters, and housemaids are included in service

production.

Economic Costs

1. Total cost – is the sum total cost of production. It is composed of wages, rents,

interests and normal profits.

2. Fixed cost – is a kind of cost that remains constant regardless of the volume of

production. Even if there is no production, there is still cost. Examples are the expenditures

on machines and buildings.

3. Variable cost – is a kind of cost that changes in proportion to volume of production. If

there is no production, there is no cost. More production means more costs. Examples are

wages and raw materials.

4. Average cost – is also called unit cost. It is equivalent to total cost divided by quantity.

AC =TC

Q

5. Marginal cost – is the additional or extra cost brought about by producing one

additional unit. It is obtained by dividing change in total cost by change in quantity.

MC= ΔTC

ΔQ

6. Explicit cost – is also called expenditure cost. These are payments to the owners of the

factors of production like wages, interests, electric bills, and so forth.

7. Implicit cost – also called non-expenditure cost. The factors of production belong to

the users.

8. Opportunity cost – is a foregone opportunity or alternative benefit.

Short Run and Long Run Period

Short run refers to a period of time that is too short to allow an enterprise to change its plant

capacity, yet long enough to allow a change in its variable resources.

Long run refers to a period of time that is long enough to permit a firm to alter all its

resources or inputs

Economies of Scale

Economies of scale may be classified as internal and external economies of scale. Internal

economies of scale are the factors inside the firm that contribute to the efficiency of the firm.

Examples of such factors are division of labor, human resource development, managerial

specialization, proper use of machines and equipment, favorable management policies,

effective utilization of by-products, and modern techniques of production. External

economies of scale refers to those factors that are outside the firm, but they contribute to the

efficiency of the firm in terms of increased output and decreased unit cost of production.

Examples are government policies, electrification, and transportation and communication

facilities.

Appropriate Techniques of Production

Labor-intensive technology means more labor inputs and less capital inputs. Capital-intensive

technology means more machines and less labor. Poor countries should use labor-intensive

technology and advanced countries should use capital-intensive technology.

Conclusion

In the production of goods and services one must always consider the type of products that

one is to produce, for whom the products are to be produced , how are these products to be

produced and how long will it take to produce the products. Thus one must take into

consideration the cost of producing the product , the techniques in production, the length of

time and the utility of the products that are to be produced.

References:

1. Principles of Macroeconomics by Case and Fair

2. Economics by Samuelson and Nordhaus

3. Principles of Economics by Roberto Medina

LESSON 5: BUSINESS ORGANIZATION Business Organizations

The main economic activity is production. Almost all production activity is done by

specialized organizations.

There are different forms of business organizations, from very simple to complex. The choice

of a form of business organization depends on one’s resources, objectives, and perceptions.

There are three most common forms of business organizations in a capitalist economy. These

are single/sole proprietorship, partnership and corporation.

Single/sole proprietorship.

This is the oldest and simplest form of business organization. It is also the easiest to put up.

This is owned and usually managed by one person.

Advantages:

1. It is easy to form and dissolve. It requires a small capital and there are no legal

papers needed except the usual business license from the Department of Trade and Industry

and a business permit from the city/municipal government.

2. All profits belong to the business owner. This is the greatest advantage to the

entrepreneur as there is no one else to share the profit with.

3. The owner is the boss. He makes his own decisions and executes them the way he

likes. For example, he can change his business hours, products, prices, or style of

management.

4. Tax advantage and less government regulation. Usually the owner pays only the

income tax. The government regulation is almost nil. The only time the sole proprietor deals

with the government is when he pays the license, permit, and tax.

Disadvantages:

1. Unlimited liability. In case of business loss, the owner assumes all the financial

obligations. He is liable to the extent of his personal properties including saving.

2. Lack of stability. If the owner dies, it is the end of the business unless members of the

family or relatives can continue the business.

3. Limited amount of capital. Sometimes the proprietor meets difficulty in securing the

capital for a large scale enterprise. Unless the proprietor has large resources of his own, this

proves a distinct disadvantage.

4. Difficulties of management. The owner assumes the responsibility for such diverse

tasks as purchasing, merchandising, extending credits, financing, employing personnel, and

so forth. He may be capable of handling some of these functions but not all.

Partnership

Article 1967 of the Civil Code defines partnership as an organization where “two or more

persons bind themselves to contribute money, property, or industry to a common fund with

the intention of dividing the profits among themselves. There are two types of partners:

general and limited. The liability of a general partner extends up to his personal properties

while a limited partner is only liable to the extent of his contribution in the business.

Advantages:

1. It is easy to organize. The partnership is much easier to form than a corporation. The

legal requirements include articles and by-laws of partnership to be submitted to the SEC,

verification of business name with SEC, registration of business name with the Bureau of

Commerce, Bureau of Internal Revenue for a TIN (tax identification number), business permit

from the city/municipal hall and a registration of employees with SSS.

2. Availability of more capital and credit. Partners can pool their resources – properties,

equipment, and others – and use these for security in obtaining bank loans. Suppliers are

more willing to extend more credit to a partnership than to a single proprietorship.

3. The partners get all the profits. This stimulates them to improve their business.

4. More and better knowledge and skills. Each partner contributes his knowledge and

skills to the organization. It is said that two heads are better than one. This kind of

combination provides better management in terms of planning, decision-making, and

implementation compared with sole proprietorship.

Disadvantages:

1. Unlimited liability. Each general partner is personally responsible for all the debts of

the business.

2. Lack of stability. In most of the cases the partnership is terminated by the death,

withdrawal, or legally declared insanity of any of the partners.

3. Management disagreement. If the management do not work in unity, conflicts arise.

Suspicion or distrust may crop up among the partners. Such negative attitude and unfair

often takes place.

4. Idle investment. It is easy to invest money in partnership, but sometimes it is difficult

to get it out. For example, when a partner decides to leave the organization, the remaining

partners may not buy his share. And if the leaving partner decides to sell his share to an

outsider, the problem might arise that the existing partners may not agree

Kinds of Partnerships:

1. Universal-refer to all present property or to all profits

2. Particular- has for its objects determinate things their use or fruits, or specific

undertakings, or the exercise of a profession or vocation

3. General- liabilities of partners extend to their individual properties after the assets

have been exhausted

4. Limited-at least one general partner and the others are limited partners

Kinds of Partners:

1. General-liable for partnership obligations to the extent of their private properties

2. Limited-those who cannot be held for partnership obligations

3. Capitalist- contributes money or property

4. Industrial- contributes expertise, ,skills and services

5. Managing-administers the operation and manages the business directly

6. Liquidating-handles affairs of dissolution of the business

7. Ostensible-publicly makes known his connection with the partnership

8. Secret-identity is not publicly made known

9. Dormant- both a secret and silent partner

10. Nominal- partner in name only

Corporation

It is an artificial being created by operation of law, having the right of succession, and the

powers, attributes, and properties expressedly authorized by law or incident to its existence.

The shares or certificates of ownership of a corporation are called stocks. The owners of

stocks are called stockholders or shareholders. There are two types of corporations: private

or close corporation and open corporation.

Advantages:

1. Limited liability. The stockholders have a limited liability. In case the corporation

becomes a failure, the creditors can lay their claim on the assets of the corporation and not

on the assets of the stockholders.

2. Easy to raise capital. A corporation can sell shares of stock to the public for addition

funds.

3. Perpetual life. The life of a corporation does not end with the withdrawal or death of

key owners. It can exist for 50 years and is subject to renewal.

4. Specialized management. A corporation can hire professionals. It has funds to develop

its human resources.

Disadvantages:

1. Difficult to organize. Sometimes it requires the services of a lawyer and an accountant

to prepare the legal documents. The legal requirements include submission of articles of

incorporation and by-laws to SEC, registration with BIR and DOLE, acquisition of a business

permit from city/ municipal hall and a license from the DTI. It also has to get approval from

other agencies like Central Bank, Food and Drug Administration and many others depending

on the nature of the products and services.

2. Strictly regulated and supervised by the government. Corporations have to submit

their financial reports every year to concerned government agencies. They have to comply

with government laws, policies and regulations. Government regulation and supervision on

corporations are close compared with the other forms of business organizations.

3. Some corporations are socially irresponsible. They sell substandard goods and pollute

the environment.

4. Formal and impersonal employer-employee relationship. A corporation has several

layers of management. The top management seldom or do not associate with the workers or

clerks of the corporation.

Cooperatives

The cooperative code defines a cooperative as a duly registered association of persons, with

a common bond of interest, who have voluntarily joined together to achieve a lawful

common social or economic end, making equitable contributions to the capital required and

accepting a fair share of the risks and benefits of the undertaking in accordance with the

universally accepted principles of cooperation, which include the following:

1. Open and voluntary membership

2. Democratic control

3. Limited interest on capital

4. Division of net surplus

5. Cooperative education

6. Cooperation with other cooperatives

Objectives of Cooperatives.

1. To encourage savings among members;

2. To generate funds and extend credit to the members for productive purposes;

3. To encourage among members systematic production and marketing;

4. To provide goods and services and other requirements to the members;

5. To develop expertise and skills among its members;

6. To acquire lands and provide housing benefits for the members;

7. To promote and advance the economic, social, and educational status of the

members; and

8. To establish, own, lease, or operate cooperative banks, cooperative wholesale and

retail complexes, insurance and agricultural/industrial processing enterprises, and public

markets.

Types of Cooperatives

1. Credit cooperative. Create funds in order to grant loans for productive purposes.

2. Consumer’s cooperative. Procures and distributes commodities to its members and

non-members.

3. Producer’s cooperative. Undertake joint production in agriculture and industry.

4. Marketing cooperative. Engages in the supply of production inputs to members and

markets their products.

5. Service cooperative. Undertakes medical and dental care, hospitalization,

transportation, insurance, housing, labor, electric light and power, communication, and

other services.

6. Multipurpose cooperative. Combines two or more of the business activities of different

types of cooperatives.

Conclusion

The study of the four types of business organization provided a significant guide on the

individual as regards the advantages and disadvantages of each type. Such knowledge gives

the individual the benefit of determining which business organization may be most useful in

producing the goods and providing the services to people in society.

The notes are taken from the books:

1. Management by Feliciano Fajardo.

2. Business organization and management by Gutierrez, Pura and Garcia.

LESSON 6: MACROECONOMICS CONCEPTS Macroeconomic Concepts

Macroeconomics is the study of the behavior of the economy as a whole. It examines

the overall level of a nation’s output, employment, and prices.

Fundamental concerns of macroeconomics policy:

1. Why do output and employment sometimes fall, and how can unemployment be

reduced?

2. What are the sources of price inflation, and how can it be kept under control?

3. How can a nation increase its rate of economic growth?

All market economies show patterns of expansion and contraction known as business

cycles. During business-cycle downturns, such as the recession, production of goods and

services fall, and millions of people lose their jobs. For much of the postwar period, one key

goal of macroeconomic policy has been to use monetary and fiscal policy to reduce the

severity of business-cycle downturns and unemployment.

Sometimes countries experience periods of high unemployment, which persist even

when their economies are expanding. Macroeconomics examines the sources of such

unemployment and after diagnoses, can even suggest possible remedies such as reforming

labor market institutions through reducing the incentives not to work or increase wage

flexibility. The lives of millions of people depend upon whether macroeconomics can find the

right answers to these questions.

When it comes to second question, economists have learned that high rates of price

inflation have a corrosive effect on market economies. A market economy uses prices as a

yardstick to measure economic values and as a way to conduct business. During periods of

rapidly rising prices, the yardstick loses its value: people become confused, make mistakes,

and spend much of their time worrying about inflation eating away their incomes. That’s why

macroeconomics has increasingly emphasized price stability as a key goal.

When taking under consideration question three, the macroeconomics is also

concerned with the long-run prosperity of a country. Over a period of decades and more, the

growth of a nation’s productive potential is the central factor in determining the growth in its

real wages and living standards. Over the past years, rapid growth in Asian countries such as

Japan, South Korea, and Taiwan sent average incomes for their citizens soaring. Countries

want to know the ingredients in a successful growth recipe. Does running a big budget deficit

or a big trade deficit have harmful long-run effects on growth? What is the role of investment

in physical capital, in research and development, and in human capital? Should the

government nourish key industries through subsidies and industrial policy, or does a hands-

off policy work better? A complication in considering the three central issues is that there are

inevitable tradeoffs among these goals. Reducing the budget deficit may mean accepting

slower growth in the short-run. Increasing the rate of growth of output over the long run may

require greater investment in knowledge and capital; this investment lowers current

consumption of food, clothing and recreation. Of all the macroeconomic dilemmas, the most

agonizing is the choice between low inflation and low unemployment. There are no simple

formulas for resolving these dilemmas, and macroeconomics differ on the proper approach

to take when confronted with high inflation, rising unemployment, or stagnant growth. But

with sound macroeconomic understanding, at least the inevitable pain that comes from

choosing the best route can be minimized.

The Theory of Economic Growth

Economic growth is the product of economic development. Economic development is a

progressive process of improving human conditions, such as the reduction or elimination of

poverty, unemployment, illiteracy, inequality, disease and exploitation. As a process, it

involves the interaction of economic and non-economic factors. Economic growth is the

increase in the volume of goods and services produced by an economy. It is generally a

factor in an increase in the income, of a nation. It is conventionally measured as the percent

rate of increase in real gross domestic product, or GDP.

Stages of economic growth

One theory in determining the stages of economic growth is based on exchange

systems. That is from barter economy to money economy, and finally to a credit economy.

Another approach is based on the dominant productive sectors of the economy. According to

this theory as stated by British economist Colin Clark, there are three stages of economic

growth:

1. Agriculture is the main source of employment and income.

2. Manufacturing industry becomes the major economic activity as a country develops.

3. Service industries grow to be the dominant feature of the economy as a country

further develops.

Another theory of classifying the stages of growth is the doctrine of Rostow, an

American economic historian. In his book Stages of Economic Growth, the transition of a

country’s economy from underdevelopment to development passes through several stages

such as:

1. Traditional society

2. Pre-conditions for take-off

3. Take-off

4. Drive to maturity

5. Age of high mass consumption

Some economic growth models:

1. Ricardian model. - Here the key factor is land. This means agriculture is the first

priority in the attainment of economic growth.

2. Harrod-Domar. - The key factor in this model is physical capital like machines,

buildings, equipment, and so forth. According to this model, the input is capital, and its

efficiency is determined by the number of output it can produce.

3. Kaldor model. - Here the key factor is technology, which is embodied in physical

capital. Japan is an example which has achieved economic growth through technology.

Inflation

There is inflation when there is a rising general level of prices. Increase in prices is

inflation or we can say that it is decrease in the value of money. Demand for goods and

services decrease when prices increase. Inflation creates more inflation. When prices keep on

increasing, people are inclined to spend their money before it loses its value. Inflation

encourages more consumption and less saving.

Types of inflation:

1. Demand-pull inflation. - This type of inflation occurs when demand for goods and

services exceed supply. This is based on the law of supply and demand. Another cause of

demand – pull inflation is the excess money supply. When money supply increases without

corresponding increase in production of goods and services, prices rise.

2. Cost-push inflation. - An increase in the cost of production results to an increase in

prices. Cost increases whenever there is an increase in wages, oil prices, or prices of raw

materials.

3. Structural inflation. - This view explains that the inability of some sectors of our

economy to response immediately to demand for goods and services. When supply cannot

meet demand, prices increase. If there are no obstacles or constraints (financial, physical or

institutional), whenever prices rise, producers are encouraged to enter the market. This

increases supply, and therefore prices fall. However, there are instances where supply cannot

be increased, at least in a short period. Since supply falls, prices of such scarce products rise.

And this is inflation for such particular products.

LESSON 7: BUSINESS CYCLES Business Cycles

Understanding the business cycles will be useful in understanding the phases which an

economic system undergoes to bring about the use of the resources.

Phases of the business cycles

1. Prosperity: This is the peak of the business cycle. There is full employment, and the

national output is at full capacity. Output can no longer be increased because productive

resources are at full capacity or fully employed.

2. Recession: Both production and employment are falling down.

3. Depression: Both production and employment are at their lowest levels. Under such

condition, no businessman is willing to invest because the demand for goods and services is

also at its lowest point.

4. Recovery: Both production and employment rise towards full employment

Business Cycle Theories

1. Exogenous theory: Forces outside the economic system create the business cycles.

Examples of these forces are wars, political developments, natural disasters, or major

innovations. Typhoons and floods can easily wipe out in a week's time the output of an

agricultural country. Civil wars have destroyed the economies of all countries which have

been afflicted with said human misunderstandings or greediness for political powers among

the leaders.

2. Endogenous theory: Forces within the economic system cause the fluctuations in the

economy. Examples are accelerators, multipliers, innovations or monetary policies.

Full employment

When there is an available job for every person who is willing and able to work, it is full

employment.

Theories of employment

1. Classical theory of employment states that employment increases at lower wages.

Employers are willing to hire more workers at lower wages because it is more profitable.

Keynes did not agree with such theory. He said that during depression, workers are willing to

accept any wage but could not find jobs. He argued that high wage could not be the main

cause of unemployment.

2. The Keynesian theory of employment - which is the modern theory of employment -

states that employment is determined by aggregate or total demand for goods and services.

Unemployment and its types

Disguised unemployment is a situation where individuals are actually working but they do

not contribute to production.

Types of Unemployment

1. Frictional unemployment is caused by interruptions in production for technical

reasons, or when workers are temporarily laid off due to renovation works.

2. Structural unemployment: A change in technology renders the skills and talents of

some workers obsolete.

3. Cyclical unemployment: This is caused by the fall of business activities in the economy.

When aggregate demand decreases, production declines. Some workers have to be laid off.

4. Seasonal unemployment: During slack periods, many workers in farming and

construction are laid off.

Conclusion

The concepts of recovery, recession, expansion, depression are terms we have encountered

since time immemorial. These concepts dealt with how we have attained levels of growth in

relation to the employment and unemployment of our resources. As we understand the

concepts, we are also made aware of the different effects of the same in our society

Reference

1. Principles of Macroeconomics by Case and Fair

2. Economics by Samuelson and Nordhaus

LESSON 8: MEASURING NATIONAL OUTPUT AND INPUT

Measuring National Outputs & Income

Gross National Product - It is the total market value of all final goods and services produced

by citizens in one year.

The real economic achievements of any country are measured by the number of goods and

services its citizens have produced in a given year. If we depend on the market value of final

goods and services, it is not most of the time accurate because of price fluctuations. In case of

inflation (high prices), the market value of GNP naturally increases. In case of deflation (low

prices), the market value of GNP is low.

GNP at current prices is money GNP. It is obtained by multiplying the number of final

products and services by prevailing market prices. It is expressed as: P X Q = GNP.

Measuring GNP

GNP can be measured in at least two different ways, both of which yield the same result. One

way of measuring the GNP is from the buyer's point of view, or in terms of aggregate

demand. Also known as the expenditure approach to measuring GNP, this method calculates

the value of the GNP as the sum of the four components of GNP expenditures: consumption,

investment, government purchases, and net exports.

The expenditure method accounts for the source of the monetary demand for products and

services. The largest component, consumption, includes the value of all the goods and

services purchased by consumers during the year. The investment category includes the

production of buildings and equipment as well as the net accumulation of inventories.

Financial investments, which involve only transfer payments rather than the production of

capital goods, are not counted. Government purchases include only expenditures for goods

and services, not transfer payments such as Social Security. Net exports include the value of

all goods produced in the country but sold abroad, minus the value of goods produced

abroad and imported into the country.

Since every transaction involves a buyer and a seller, the GNP can also be calculated from the

seller's point of view, which focuses on where money payments go. The method, also known

as the income approach, measures GNP as the sum of all the incomes received by all owners

of resources used in production. Such income payments are known as factor payments,

because they are paid to various factors involved in the production of goods and services.

These include employee compensation, rental income, proprietary income, corporate profits,

interest income, depreciation, and indirect business taxes.

Employee compensation includes all payments relating to labor, including fringe benefits

and taxes paid on labor. Rental income is paid for the use of capital goods. Proprietary

income represents payments to owners of business firms. Corporate profits are earned by the

shareholders of a business. Interest income is received for lending financial resources.

Depreciation is a charge against assets used in production. The indirect business tax refers to

sales tax, which represents part of the payments for goods and services that are not paid to

any of the income recipients.

The measurement of GNP is fairly complex and follows a set of rules that, while generally

agreed upon, may nevertheless appear somewhat arbitrary. For example, housing is treated

in a manner that protects GNP calculations from changes in the rate of home ownership. All

occupant-owned housing, as opposed to rental housing, is treated in the GNP accounts as if

rented. Thus, the rental value of occupant-owned housing is included as a service in the GNP

along with the rental value of houses that are actually rented.

GNP measures the value of final products and services, so it is necessary to avoid double-

counting the many intermediary products that are bought and sold in the economy. Products

and services are counted as part of the GNP when they reach their final form.

Some important final products are actually excluded from the GNP. Many household activities

are excluded, as are all illegal goods and services. In the case of housework, the services of a

hired maid are considered part of the GNP, but not if the same services are performed by a

member of the household. The exclusion of domestic chores has a greater effect on the

calculation of the GNP of lesser-developed countries, where households may produce their

own food and clothing to a greater extent.

The treatment of government expenditures also affects GNP calculations. All government

expenditures are considered final; there is no attempt to categorize them as intermediate

and final. The effect of this rule is an upward bias in the GNP. In addition, all government

expenditures are considered as current consumption rather than as investments; they are

measured only once, in the year in which they occur. Finally, government goods and services,

which are usually not sold in the marketplace, are valued at cost in the GNP.

Limitations of GNP

1. It does not show the allocation of goods and services among the members of society. It

only shows the number of goods and services produced by citizens in a given period. An

increase in GNP does not necessarily mean that the economic and social welfare of the

masses has improved. In a society where there is a widespread mal-distribution of wealth, an

increase in GNP only benefits the very rich who own the productive resources.

2. GNP accounting in less developed countries in understated. There are many economic

transactions especially in the rural areas that are not registered in the market. For example,

backyard poultry, fishing and other small-scale income-producing activities whose products

are only intended for family consumption. Only market transactions are reflected in the GNP.

3. The evils of economic growth like pollution, congestion and dirty environment are not

reflected in the GNP. The cost of such destruction to the health of human beings, and to the

balance of nature is very high. And this is not subtracted from the GNP.

4. GNP only measures the number of goods and services but not the quality of goods and

services. Needless to say, quality is an important feature as it affects the well-being of people.

5. Income or products from illegal sources are not included in the GNP. Examples are

gambling, unlicensed money lending, and narcotics business.

Price Index

When newspapers tell us “inflation is rising,” they are really reporting the movement of a

price index. A price index is a measure of the general price level; more precisely, it is a

weighted average of the prices of a number of goods and services. The most important price

indexes are the consumer price index, the GDP deflator, and the producer price index.

The Consumer Price Index (CPI)

In economics, a Consumer Price Index (CPI, also retail price index) is a statistical measure of

a weighted average of prices of a specified set of goods and services purchased by wage

earners in urban areas. It is a price index which tracks the prices of a specified set of

consumer goods and services, providing a measure of inflation. The CPI is a fixed quantity

price index and a sort of cost-of-living index.

The CPI can be used to track changes in prices of all goods and services purchased for

consumption by urban households. User fees (such as water and sewer service) and sales and

excise taxes paid by the consumer are also included. Income taxes and investment items (like

stocks, bonds, life insurance, and homes) are not included.

For example assume that consumers buy three commodities: food, shelter, and medical care.

Using 1995 as the base year, we reset the price of each commodity at 100 so that differences

in the units of commodities will not affect the price index. This implies that the CPI is also 100

in the base year. [= (0.20 X 100) + (0.50 X 100) + (0.30 X 100)]. Next, we calculate the

consumer price index. Suppose that in 1996 food prices rise by 2 percent to 102, shelter

prices rise 6 percent to 106, and the medical care prices are up 10 percent to 110. We

recalculate the CPI for 1996 as follows:

CPI (1996)

= (0.20 X 102) + (0.50 X 106) + (0.30 X 110)

= 106.4

In other words, if 1995 is the base year in which the CPI is 100, then in 1996 the CPI is 106.4.

Gross Domestic Product

It is the total market value of all final goods and services produced within the territories of a

country in one year. Incomes derived from investments or wealth in foreign countries is

excluded. In a country whose economy is dominated by multinational corporations or

foreigners, the GDP is bigger than GNP.

GDP is used for many purposes, but the most important one to measure the overall

performance of an economy.

LESSON 9: INTERNATIONAL TRADE International Trade and Theory of Comparative Advantage

International trade refers to exchange of goods and services between one country and other

countries. Because of geographical conditions and technological monopoly, countries

produce various products, and no one country can create all kinds of products. With free

international trade, countries can exchange their goods with one another. Hence, each

country has the opportunity to purchase all the goods and services from other countries

which it cannot produce.

Free international trade appears more in theory. For economic and political reasons, there

have been trade barriers on the movement of goods and services among countries.

Bases of International Trade

1. Distribution of economic resources. The distribution of natural resources, labor and

capital goods among countries is not even. When a top Japanese government official saw the

United States, he said God has not been fair in the distribution of natural resources. The

arable land of Japan is only about 15 percent of its total land area. And during winter, half of

this is covered with snow. Countries which have abundant skilled labor are most efficient in

the production of labor-intensive goods.

2. Technological efficiency. All other things being equal, a country which has the most

efficient technology can produce goods at the lowest price, with the best quality, and the

highest quantity. Difference in technological efficiency results to difference in quality and

price of products.

The Importance of International Trade

International economics is concerned with allocation of economic resources among

countries. Such allocation is done in the world markets by means of free trade; the best

products are produced and sold in a free competitive market. One fundamental principle in

international trade is that one should buy goods and services from a country which has the

lowest price, and sell his goods and services to a country which has the highest price. This is

good for the buyers and the sellers. Another thing is that no country in the world can be

economically independent without a decline in its economic growth. Even the richest

countries buy raw materials for their industries form the poor countries.

Barriers to International Trade

In theory, free trade benefits everybody and every country. It has been said that tariffs and

other trade barriers only encourage inefficiency, restrict commerce, and reduce the general

standard of living. But the theory of free trade came from a world which is no longer

relevant with existing realities.

During the time of Adam Smith, Great Britain was the leading industrial power, and was

greatly benefited from free trade. Free trade prospered because there were abundant world

markets and only a few key countries. Former Harvard professor Henry Kissinger pointed out

that today’s world economy, by contrast, contains many trading nations of widely different

cultural backgrounds with great variations in labor costs and standards of living, each

claiming sovereign control over its economic decisions. In such conditions, competition

becomes more ruthless and its impact more drastic.

Other Arguments for Trade Barriers

1. Military self-sufficiency. There is a need to protect industries which manufacture goods

and materials for national defense and security. Strategic military goods are not sold to

enemies.

2. Local standard of living. To a country with a high standard of living, it is argued that

tariffs are needed to protect such living standard. The inflow of cheap foreign products will

reduce the prices of the local goods, and ultimately wages and the level of living will also

fall.

3. Local employment. It is contended that be restricting imports, the level of employment

rises. This will stimulate production in the local economy in view of the absence of foreign

competition. Of course, more production requires more workers.

Exchange Rates

A foreign exchange is the price of foreign money relative to the local money. For example, the price of $1 is ₱53. In other words it requires 53 units of our peso to buy 1 unit of U.S.

dollar. Under a floating exchange rate, the price of a dollar relative to our peso is

determined by the market forces of demand and supply. This means exchange rate between the dollar and the peso fluctuates. In case the price of a dollar increases, let us say to ₱55 to

$1, then the dollar has appreciated and the peso has depreciated. Depreciation can also be

called currency devaluation. Strictly speaking, devaluation refers to the increase of price of

gold relative to a currency. For example, one ounce of gold is worth $60. Supposing it has

become $600, this means the value of the U.S. dollar has decreased 10 times.

An exchange rate can be overvalued or undervalued. The value of a U.S. dollar relative to

peso is determined by the demand and supply of dollars. Supposing the real market value of a dollar is ₱53. If the official rate of the government (Central Bank) is ₱50, then our peso is

overvalued. Overvalued because it requires only ₱50 and not ₱53 to buy a dollar. It is

cheaper to buy goods and services from a country with undervalued currency than from the

one with an overvalued currency.

Determinants of Exchange Rates

Without government restrictions or regulations on the buy and sell of dollars, the price of the

dollar is determined by market forces such as:

1. Relative income changes. An increase in the purchasing power of the Filipinos tends to

raise the imports of the U.S. goods. This means demand for U.S. dollars also increases. As a

result, the price of the dollar rises, and the value of our peso depreciates. Conversely, a rise

in the purchasing power or real income of the Americans tends to increase imports of

Philippine goods. Such situation increases the value of the peso relative to the dollar,

because the supply of dollars in the Philippines increases.

2. Relative price changes. In case prices of goods and services are much higher in the

Philippines than in the United States, Filipinos are inclined to buy from the United States

because of cheaper prices. This results to a greater demand for dollars, and so its price

increases. This means the value of the peso declines. On the other hand, a fall in the prices of

goods in the Philippines increases demand for Philippine products from the U.S. residents.

This reduces the exchange rate of the dollar.

3. Relative interest rates. Supposing interest rates are higher in the Philippines than in

the United States. These attract U.S. investments and reduces Filipino investments in the U.S.

These results to an increase in the supply of dollars in the Philippines while the demand for

dollars declines. So, the exchange rate of dollar falls.

Trade Protection for the Less Developed Countries

The theory of free trade is basically based on the concept of comparative advantage.

Industrial countries should sell finished products while agricultural countries should sell raw

materials. In this case, the agricultural countries will have no chance to industrialize their

economies which is the best way to achieve high economic growth. Agricultural economies

have remained poor because the prices of their products in the world markets are low while

those of the industrial countries are high.

The most widely used trade barriers are tariffs and import quotas. A tariff is an excise tax on

imported goods while an import quota limits the number of goods to be imported. Nations

built trade barriers to give their infant industries a chance to develop and grow. During the

formative industrial development of United States, Germany, Canada, and other countries in

Western Europe, they protected their infant industries against the industrial goods of Great

Britain.

Conclusion

The word had indeed become smaller due to the development in technology. This is most

true in the field of telecommunication and transportation. Thus the relations among

countries have become more intense. In this regard, the most important concern remains to

be economic. The exchange of goods and services would always be a major concern for

counties have different needs and different levels of productivity responsible for different

products. Thus the knowledge of international trade remains crucial in order that individual

players in the international scene or market may be guided accordingly

References:

1. Principles of Economics by Roberto G. Medina

2. Principles of Macroeconomics by Karl E. Case and Ray C. Fair

3. Economics by Feliciano Fajardo

Questions:

1. What are the bases of international trade?

2. What are the barriers to international trade

3. What is exchange rate?

4. What are the factors that affect exchange rates?

LESSON 10: FISCAL POLICY Fiscal Policy

Fiscal policy refers to the revenue and expenditure measures of the public budget. By fiscal

policy we mean the process of shaping taxation and public expenditure to help dampen the

swings of the business cycle and contribute to the maintenance of a growing, high-

employment economy, free from high or volatile inflation. In formulating fiscal policies, the

voters, the President and his cabinet (executive branch) and the legislative body (congress or

general assembly) are involved. In a true democratic society, the welfare of the people is

promoted through the budget. The most important needs of the economy and the people are

given top priority. However, in not a few cases, political interests of government officials are

the first considerations. For instance, many government projects appear immediately before

the election time.

The objectives of fiscal policy are:

1. Provision for social goods

2. Equitable distribution of wealth and income

3. Maintain high employment

4. Ensure price stability; and

5. Sustain a satisfactory rate of economic growth

6.

The national budget contains specific provisions for the funding of projects and programs

geared toward the attainment of the aforementioned policy objectives. The budget is focused

towards the promotion of the welfare of the poor masses. It is the President of the Republic,

together with the cabinet members, who prepare the national budget. The proposed budget

is submitted to the legislature for discussion and approval.

Discretionary Fiscal Policy

A discretionary fiscal policy is one in which the government changes tax rates or spending

programs, usually by passing new legislation. The principal weapons of discretionary fiscal

policy are public works, other capital programs, public-employment projects, and changes in

tax rates.

Public works include creating jobs, building hospitals, schools, and roads as well as other

infrastructures needed for a growing economy. Other public works investments, such as

electrification, proved enormously beneficial to underdeveloped areas, and transportation

projects.

At the other extreme from highly capital-intensive, long-duration public works projects are

public-employment projects. The idea behind these programs is simple: If the problem is

high unemployment, why not just create jobs directly? Public-employment projects are

designed to hire unemployed workers for a short time in public jobs, after which people can

move to regular jobs in the private sector.

A third approach to discretionary fiscal policy is making temporary changes in income taxes.

Tax cuts can keep disposable incomes from falling and prevent an economic decline from

snowballing into a deep recession. Varying tax rates can be used to either stimulate or

restrain an economy. Many advocates of discretionary stabilization policy see varying tax

rates as the ideal fiscal weapon. Once taxes have been changed, consumers react quickly; a

tax cut is spread widely over the population, stimulating spending on consumption goods and

including an economic upturn.

Shortcomings of Fiscal Policies

Many government programs and projects are very good. They are always intended for the

good of the people, especially the poor masses. However, when it comes to results, it is

already different. Such projects are not properly managed or implemented. Either the

implementers or managers are inefficient or some very powerful groups have hampered the

success of such programs for economic or business reasons. For example, the land reform

program in most of the less developed countries is a failure.

Fiscal policy is very effective during economic depression. The government has to spend more

money on public works in order to create employment. This results to more income and

consumption that stimulate the private sector to produce goods and services. And this is the

beginning of economic recovery. However, during a period of economic boom, the

government finds it politically difficult to increase taxes and reduce government

expenditures. Many people do not understand why the government should increase taxes and

reduce government expenditures at the time when the economy is prosperous. They do not

know that such fiscal measures are designed to prevent inflation.

Fiscal Functions

There are three major fiscal functions:

1. Allocation function. Private goods like rice, soap, or cake are allocated in the market.

Those who have the money and they are willing to acquire such goods can purchase them.

They just exchange their money with such goods. However, in the case of most social goods it

is not efficient to allocate them through the market system. For example, Ayala avenue is a

public or social good. If all those who use the street, including pedestrians, have to pay, then

there would be a great delay in the movement of persons and transportation facilities.

Another example is the anti-malaria or anti-pollution project in a community. It is not

economically feasible to exclude those houses that do not like to buy the project. Whether

they pay or not they get the benefits of the project. So, there is no need to sell the project to

the community. If it is the felt need of the community, then the government should clean the

community through health and sanitation programs. Such programs are funded by taxes paid

by the people. The government also sells private goods at a lower price, and in many

countries in Europe and America, such goods are even free for those who cannot afford to

buy them in the market. They are given free food, clothing and shelter, medicare and

education. In the Philippines, there are also goods and services sold by the government at a

lower price or even free. But these are limited due to our inadequate financial resources.

2. Distribution function. The issue of the fair distribution of wealth and income has been

a problem from ancient times to modern times. Some economists believe that just distribution

of wealth and income is only for politicians, philosophers and poets. In economics, income

distribution is determined by the prices of factor ownership, like land, labor, capital, and

entrepreneurship ability. This economic theory appears good but in countries where there is

no just distribution of the factors of production, only very few have high incomes while the

great masses have very low incomes. In less developed countries, most of the peoples own

only labor. Because of very limited economic activities, there is a surplus of labor supply.

Thus, wages are very low. This means most people in countries live below poverty line. Social

reforms fight for distributive justice. They claim that the productive resources of society

should be fairly distributed among its members. If this is done, the gap between the rich and

poor is narrowed. Economic opportunities are available to all regardless of religion, race or

belief. Such situations exist only in the richest countries of the world. Even a poor country,

through its fiscal policies can contribute to distributive justice. Progressive taxation is a good

example. This is based on the ability to pay.

3. Stabilization function. One goal of fiscal policy is the attainment of economic stability.

When there are no problems of unemployment and inflation, then the economy is said to be

stable. The government through the fiscal tools of taxation, borrowings, and expenditures

can minimize or eliminate the problems of unemployment and inflation. The government

should give top priority to projects which are very efficient in generating jobs and incomes

for the people. Such productive projects do not only reduce unemployment but also inflation

rate. More supply of goods means lower prices. This is the law of supply and demand. In the

same manner, taxation can help in reducing inflation rate. If the kind of inflation is caused

by oversupply of money in relation to the number of goods available in the economy, the

solution of the government is increase taxes in order to reduce the disposable income of the

buyers. Most individuals are not happy about such fiscal policy. They believe that taxes

should be lowered during inflation because their purchasing power falls. What they do not

understand is that when there is an oversupply of money, demand for goods and services

increases. Since supply is limited, prices go up. The tax increase should only be temporary

just enough to control the demand for goods and services while efforts are being done by the

government in increasing supply of goods and services.

LESSON 11: TAXATION General Principles of Taxation

Taxation is a means of raising funds for the operations of the government, especially its

public services.

Taxes are very important as they constitute the life of our economy and society. It is not

possible for a government to exist permanently if it has no funds. Most of our programs and

projects are financed by tax revenues. The rest are funded by local and foreign loans.