Embed Size (px)

Citation preview

Lessons & Contentious Issues from Cats and Claims

Speaker

• Dr Allan Manning, Managing Director LMI Group

RIMS 2016 Business Interruption Paper

- SYNOPSIS

• Problems and errors in the policy drafting phase can have a massive effect on the actual payout of a claim compared to that which was expected

• This paper outlines the lessons learned from recent claims

Quick History Lesson

• The Industrial Special Risks Policy was introduced from the United Kingdom in the early 1970’s.

• I believe it was a plagiarized document from the start

• Reason for this hypothesis – Situation/Premises

Increase in Cost of Working

$1,000,000

Item 1 – Loss of Gross Profit/Income

Item 1(a) As a result of a reduction in Turnover

Item 1(b) As a result of an Increase in cost of

working

Typical Wording – Increase in Cost of Wording

• The additional expenditure necessarily and reasonably incurred for the sole purpose of avoiding or diminishing the reduction in turnover which, but for that expenditure, would have taken place during the indemnity period in consequence of the damage, but not exceeding the sum produced by applying the rate of gross profit to the amount of the reduction thereby avoided.

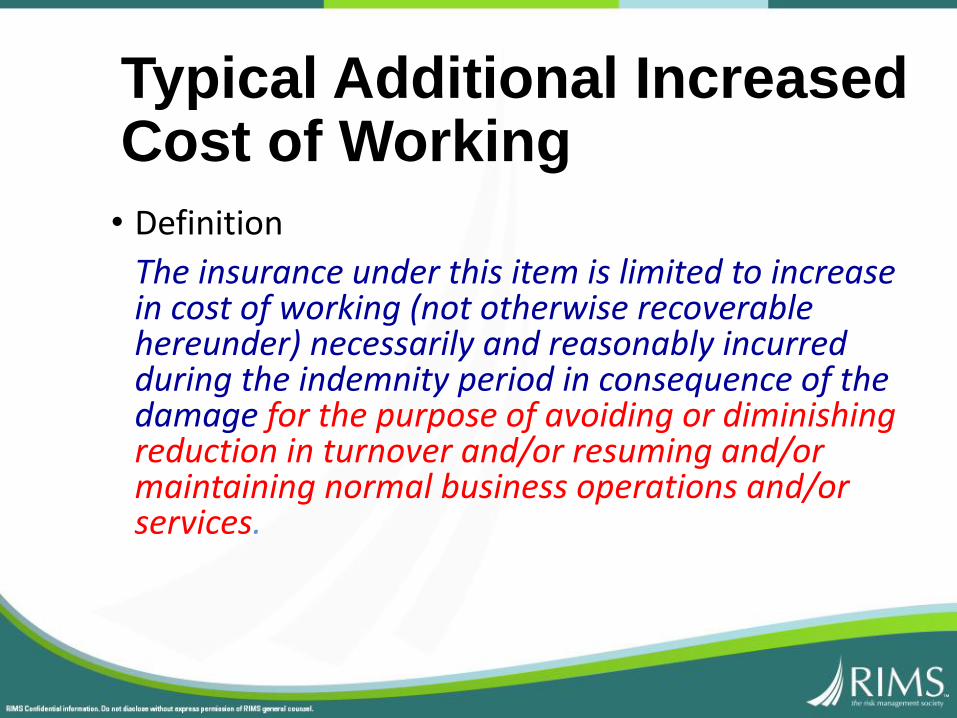

Typical Additional Increased Cost of Working

• Definition

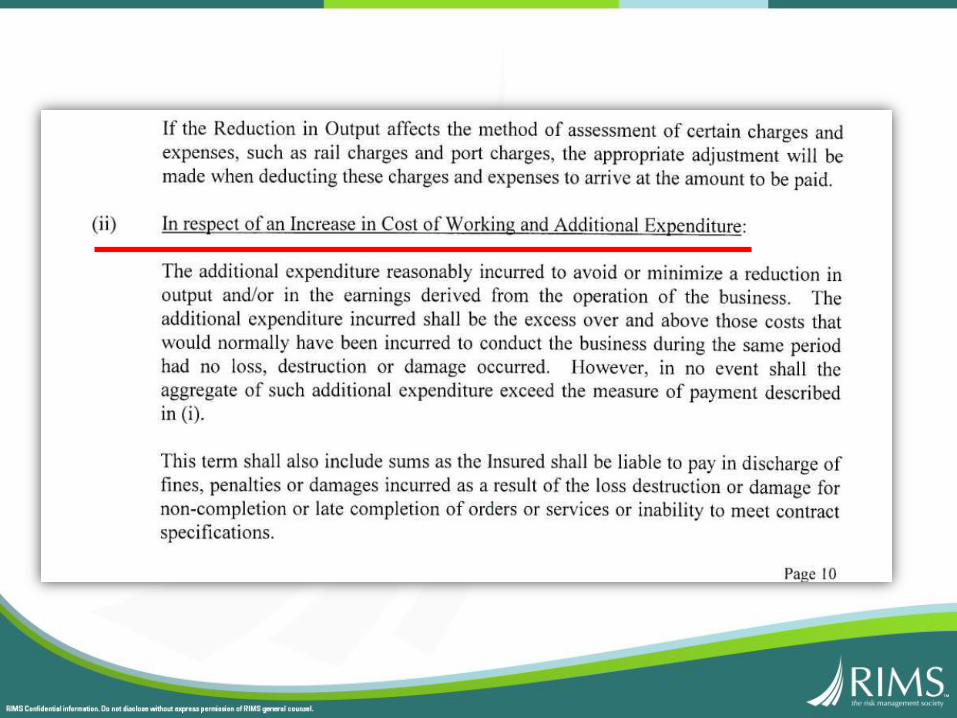

The insurance under this item is limited to increase in cost of working (not otherwise recoverable hereunder) necessarily and reasonably incurred during the indemnity period in consequence of the damage for the purpose of avoiding or diminishing reduction in turnover and/or resuming and/or maintaining normal business operations and/or services.

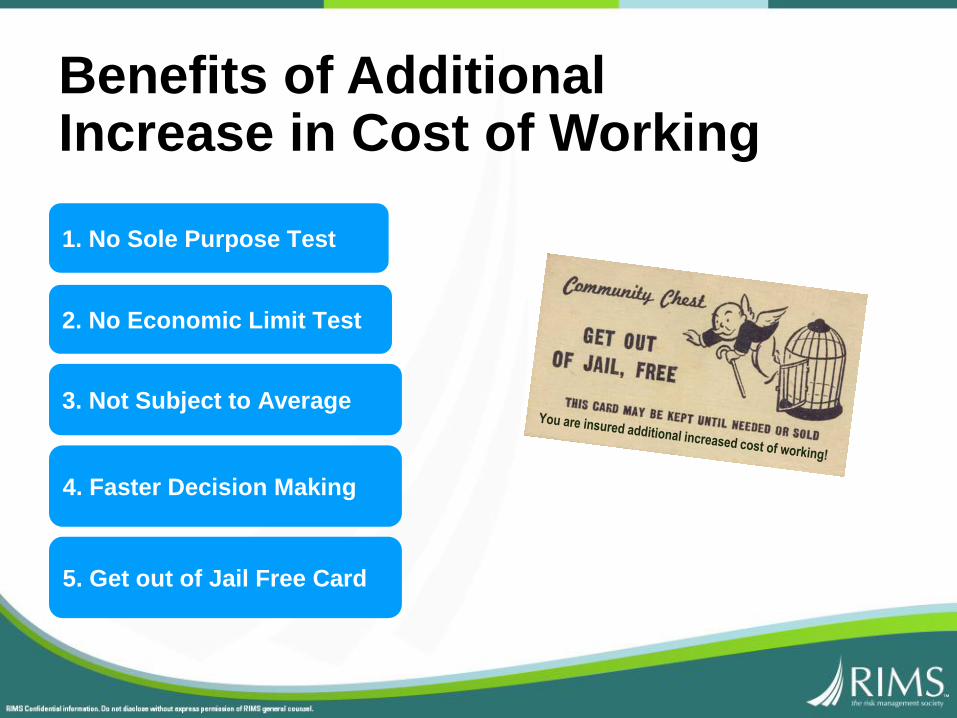

Benefits of Additional Increase in Cost of Working

1. No Sole Purpose Test

2. No Economic Limit Test

3. Not Subject to Average

4. Faster Decision Making

5. Get out of Jail Free Card

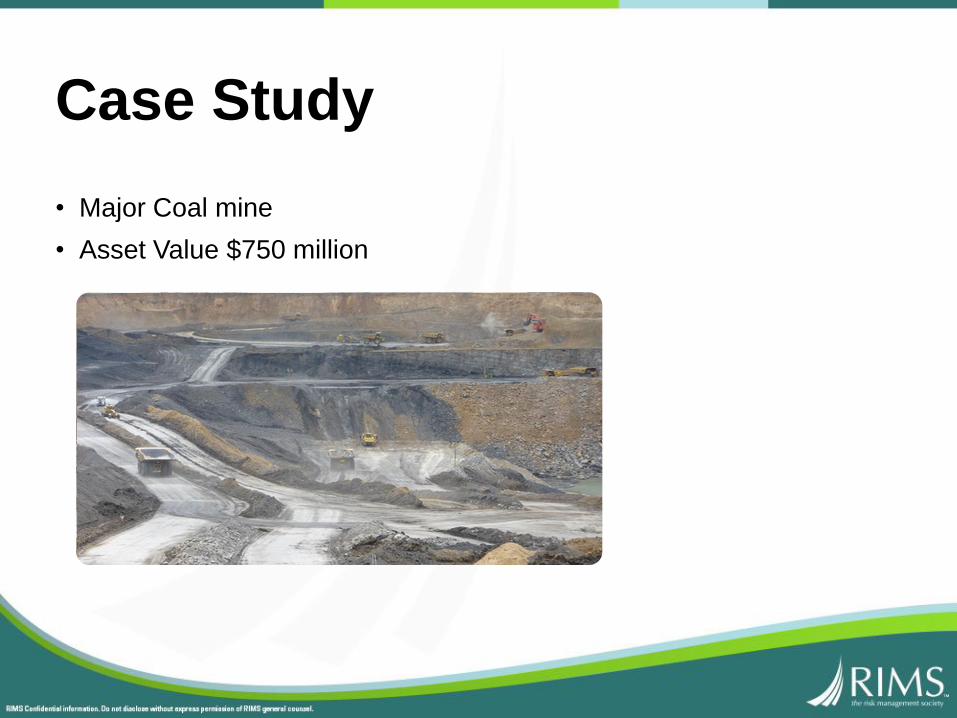

Case Study

• Major Coal mine

• Asset Value $750 million

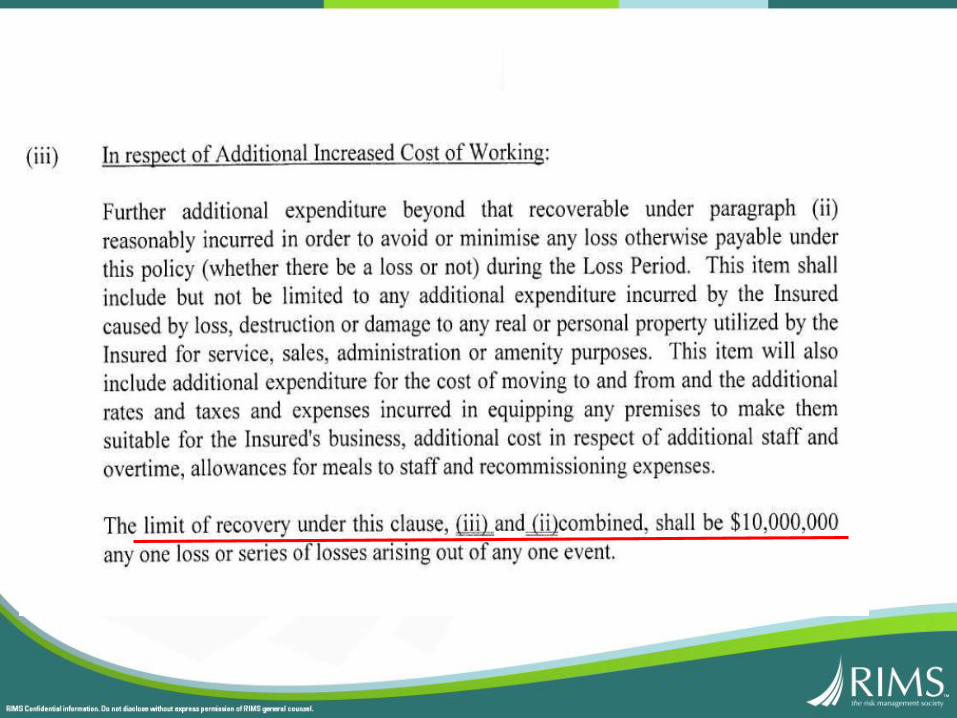

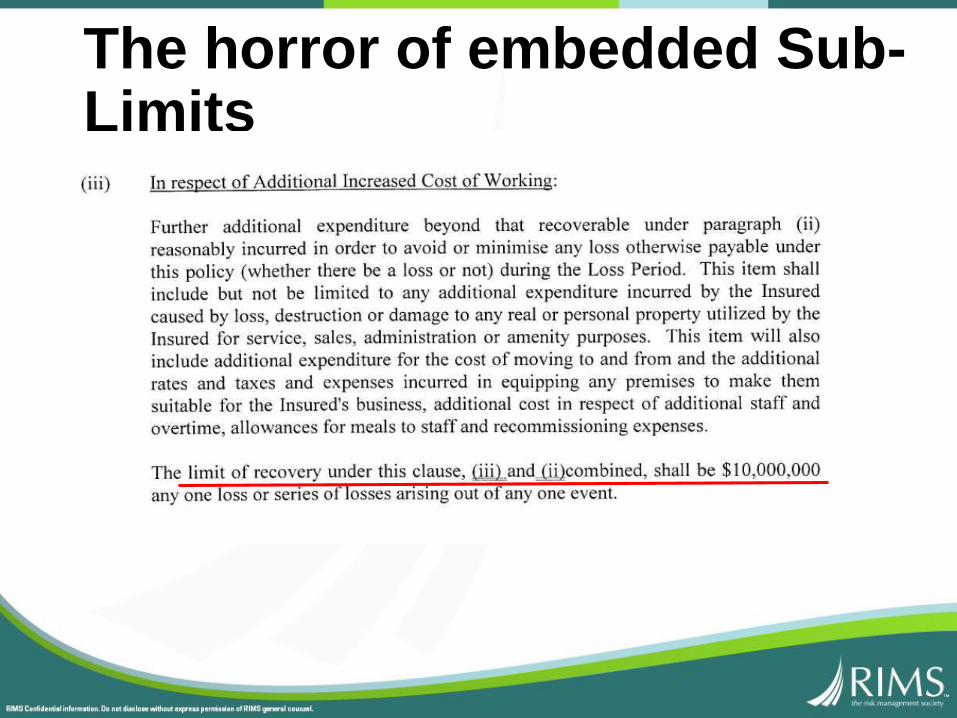

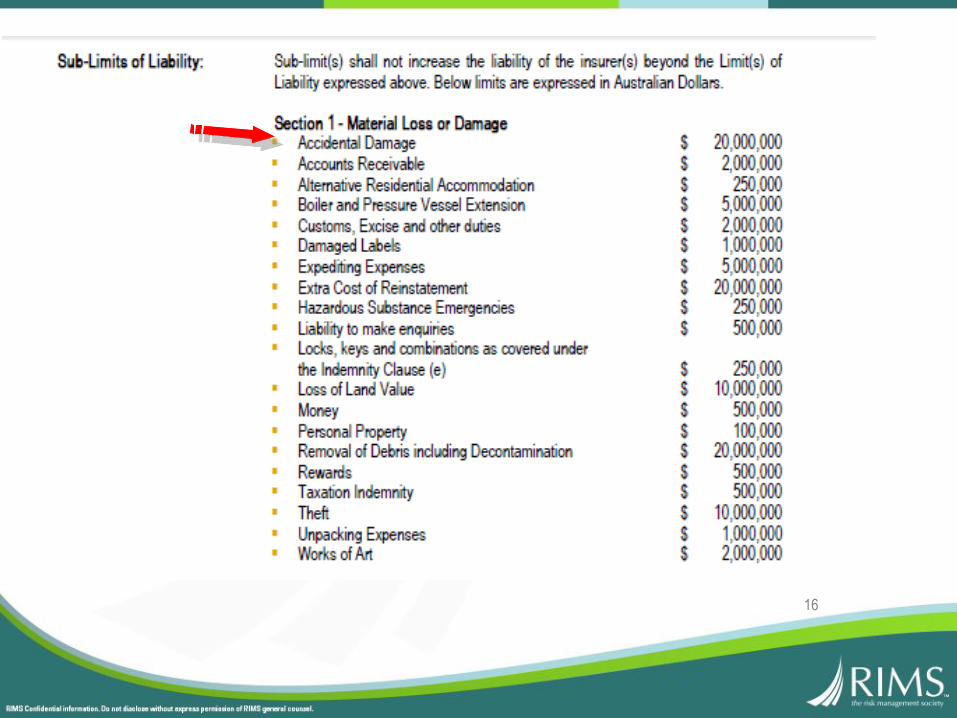

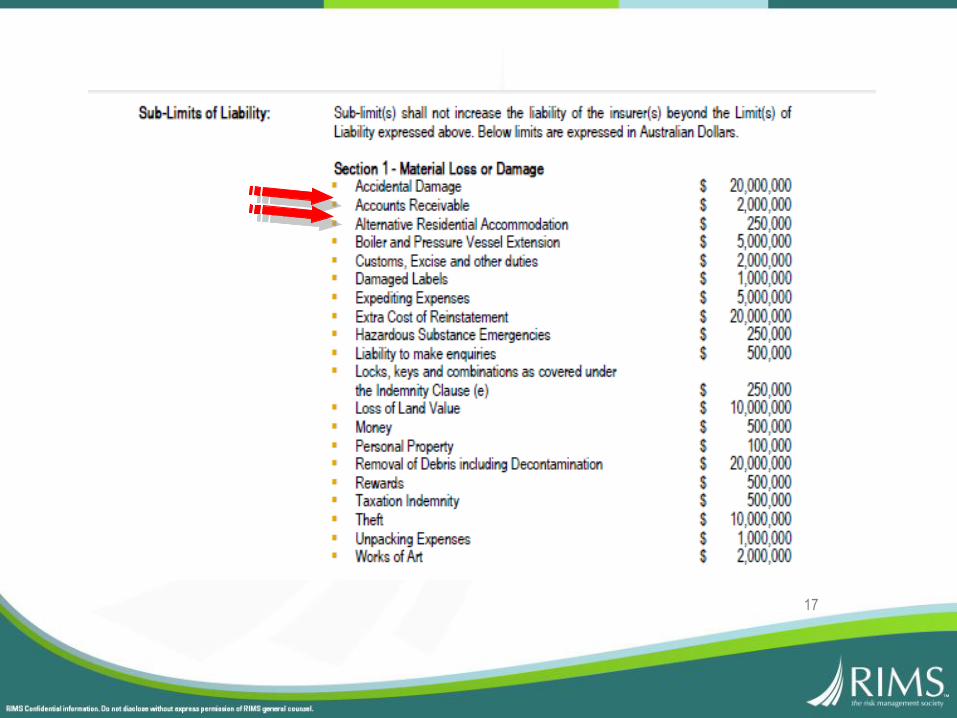

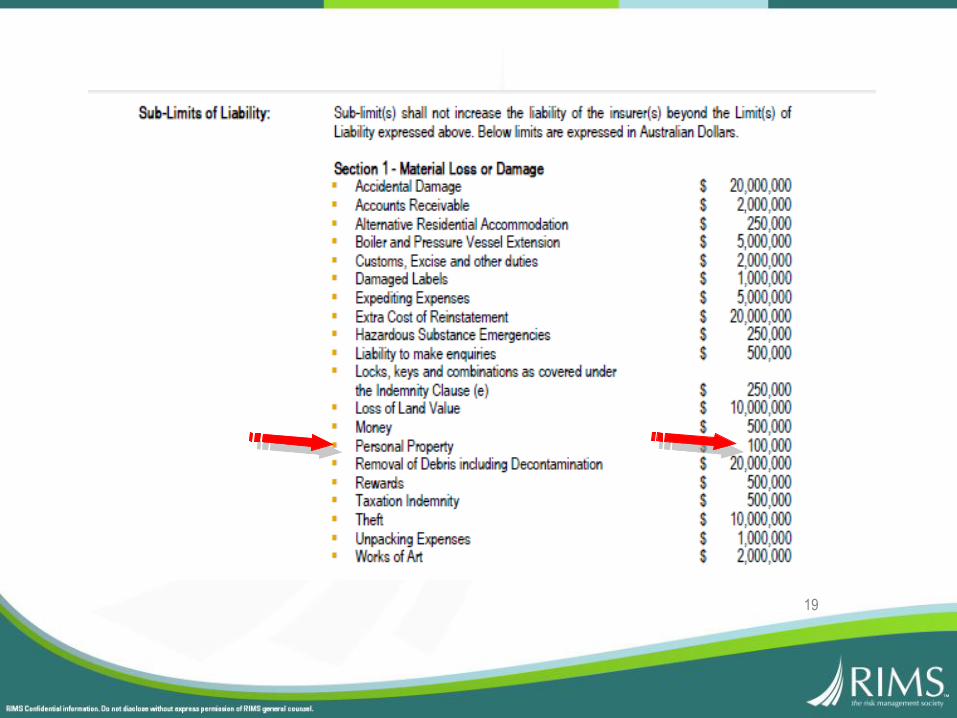

Sub-Limits

• Removal of Debris - $10,000,000

• Cost - $90,000,000

• Additional Increase in Cost of Working -$10,000,000

• or so you would think from reading the Schedule but -

The horror of embedded Sub-Limits

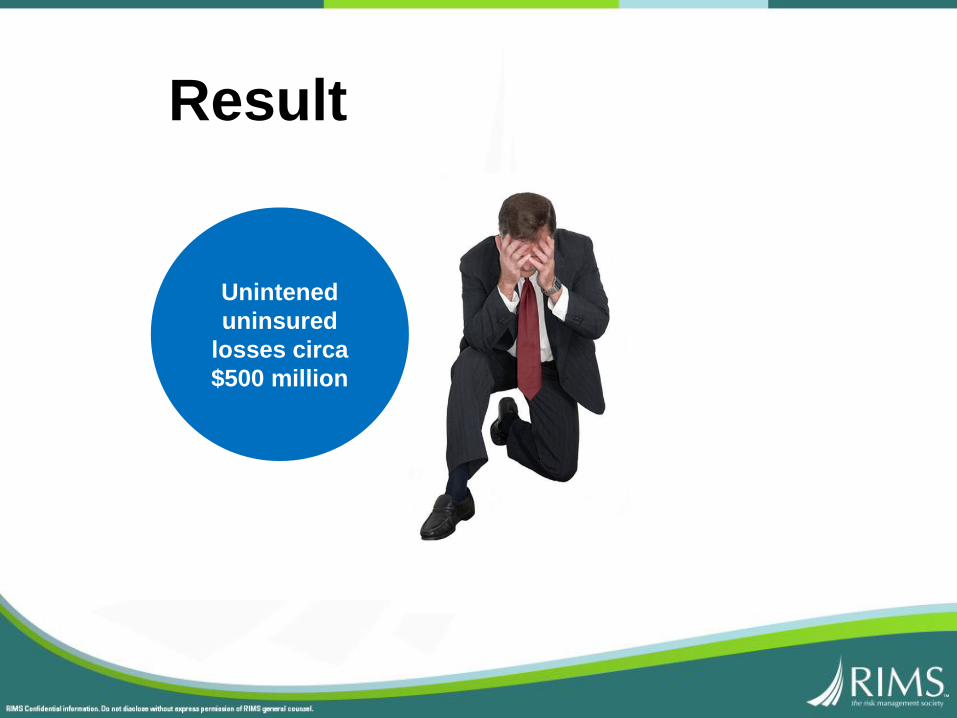

Result

Unintened

uninsured

losses circa

$500 million

Basic Wording Unchanged but Endorsement upon

Endorsement

16

17

18

19

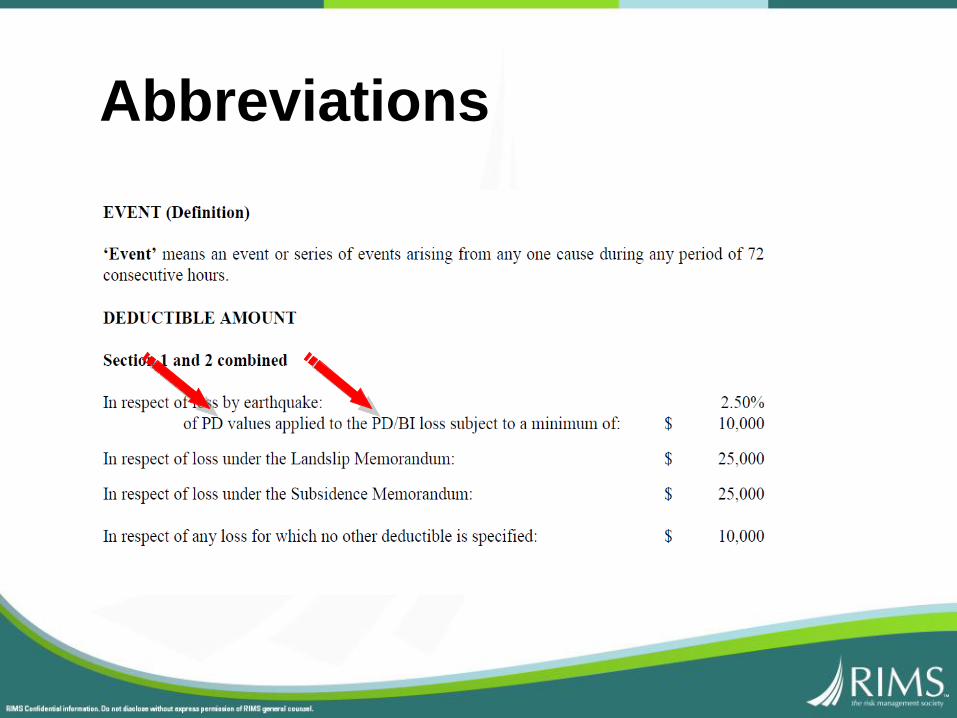

Abbreviations

Great care required when modifying the wording

• Beaconsfield Mine Collapse April 25, 2006.

• Decision of Victorian Court of Appeal -Allstate Exploration NL v QBE Insurance (Australia) Ltd [2008] VSCA 148

Civil Authority Clause

Notwithstanding anything contained herein to the contrary, the Property Insured under this Policy is also covered against the risk of loss, destruction or damages arising from the actions of any civil authority during a conflagration or other catastrophe and for the purposes of preventing, minimising or retarding same and shall also include the closure of any Premises/Operations by any civil authority due to the operation of a peril insured against.”

A comment from court

Clause 23 was inserted at the request of an insurance broker acting as agent of the joint venturers, however this evidence was not relied upon in submissions before the court. His honour found that nothing turned upon this fact although it may explain why the language of clause 23 did not sit comfortably with the rest of the policy. The circumstances that clause 23 may have been written by a person different from the author of the rest of the document, in this case, assisted neither party.

Caution is required

• Anyone adding clauses to pre existing insurance contracts need to ensure that their intentions take account of the structure in to which the additions are made.

• This will reduce as much as possible, ambiguities and uncertainties

Short but very important Clause

Note: The Limit of Liability and Sub-Limits of Liability apply in excess of any applicable Deductible

General Area Damage and the Adjustments

Clause

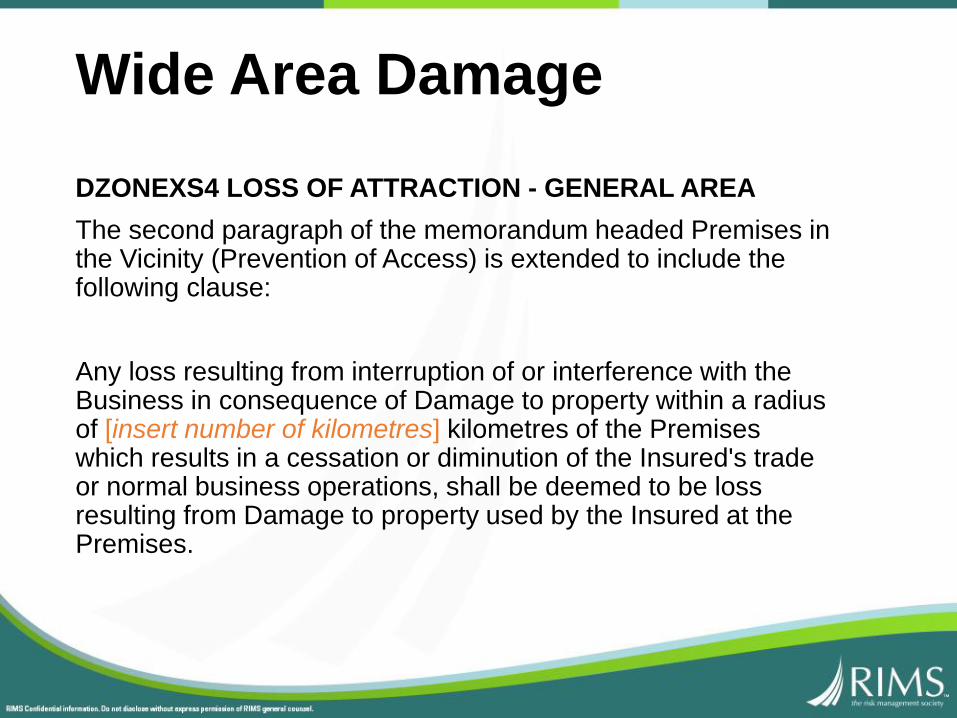

Wide Area Damage

DZONEXS4 LOSS OF ATTRACTION - GENERAL AREA

The second paragraph of the memorandum headed Premises in the Vicinity (Prevention of Access) is extended to include the following clause:

Any loss resulting from interruption of or interference with the Business in consequence of Damage to property within a radius of [insert number of kilometres] kilometres of the Premises which results in a cessation or diminution of the Insured's trade or normal business operations, shall be deemed to be loss resulting from Damage to property used by the Insured at the Premises.

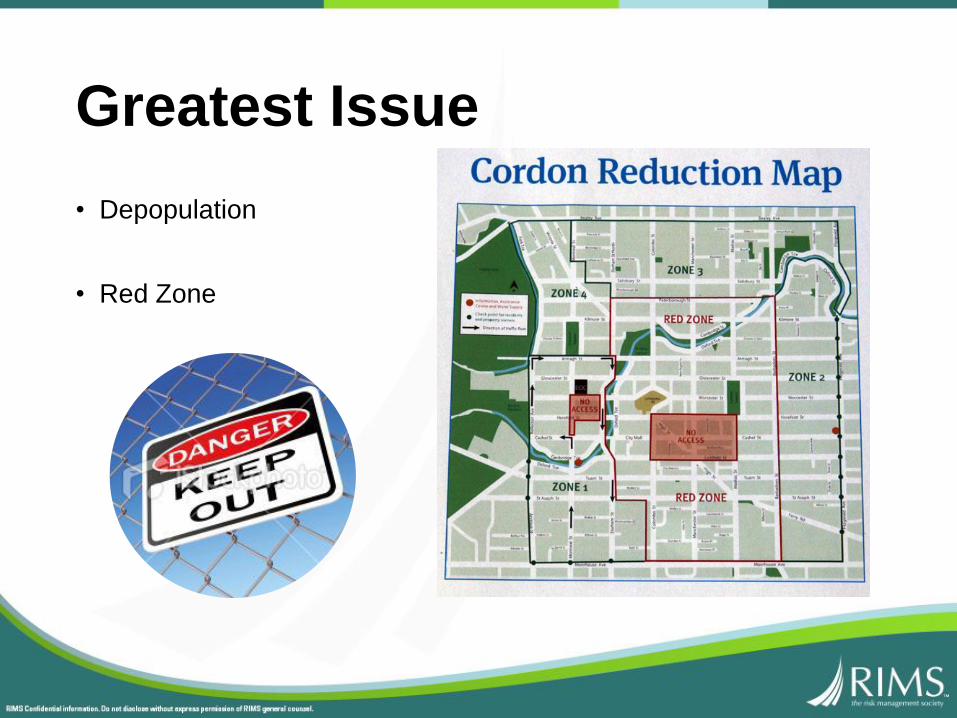

Depopulation & Repopulation

Greatest Issue

• Depopulation

• Red Zone

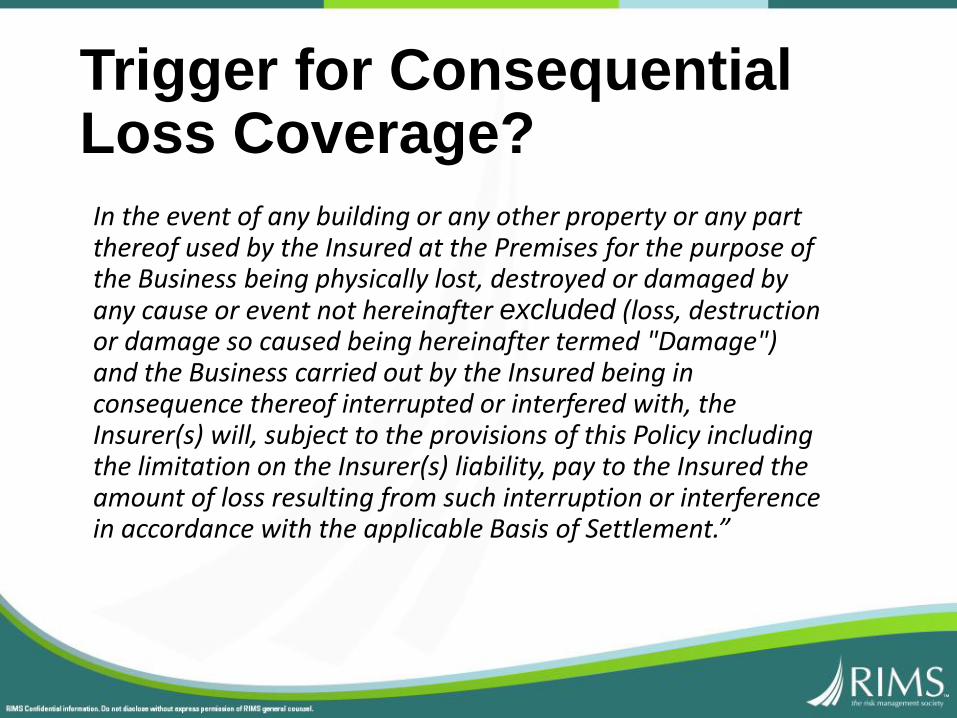

Trigger for Consequential Loss Coverage?

In the event of any building or any other property or any part thereof used by the Insured at the Premises for the purpose of the Business being physically lost, destroyed or damaged by any cause or event not hereinafter excluded (loss, destruction or damage so caused being hereinafter termed "Damage") and the Business carried out by the Insured being in consequence thereof interrupted or interfered with, the Insurer(s) will, subject to the provisions of this Policy including the limitation on the Insurer(s) liability, pay to the Insured the amount of loss resulting from such interruption or interference in accordance with the applicable Basis of Settlement.”

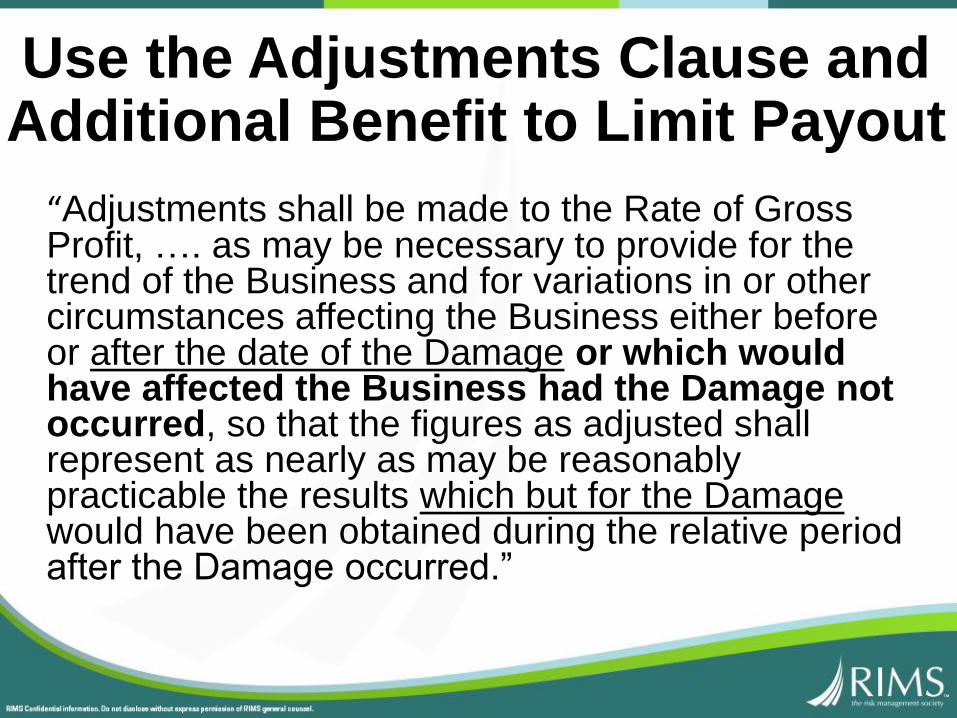

Use the Adjustments Clause and Additional Benefit to Limit Payout

“Adjustments shall be made to the Rate of Gross Profit, …. as may be necessary to provide for the trend of the Business and for variations in or other circumstances affecting the Business either before or after the date of the Damage or which would have affected the Business had the Damage not occurred, so that the figures as adjusted shall represent as nearly as may be reasonably practicable the results which but for the Damage would have been obtained during the relative period after the Damage occurred.”

“But for” Test

• Much cited

Orient-Express Hotels Ltd v Assicuraziomi Generali SpA.

[2010]; and

• Prudential v ColletonEnterprises [1992]

Compare to Mining Losses out of Australia result of Floods

Time Deductibles

• Difficult and time consuming to calculate

• Period of time (hours v business hours)

• Where shut down over many hours

• Not when Increase in Cost of Working Made but rather allocate to the period(s) is the investment benefiting

Time for a new Wording?

• A wording written 29 years ago

• Not easy to read

• With nearly 600 published endorsements

• Hiding to nothing!

This [ISR] policy is made up of a jumble of ill-assorted documents expressed in that distinctive style which insurance companies have made their own.”

Mason, J. (1974)

Guardian Assurance Company v Underwood Constructions Pty Ltd (1974) ALJR 307 at 308

ISR books

Learning Objectives

• Learning Objective 1

• Ensure ALL Sub-Limits are listed in the one place on the Policy Schedule

• Learning Objective 2

• Review the adequacy of Sub-Limits every renewal and when any major change to the risks

• Learning Objective 3

• Understand the Endorsements and ensure they marry in with the base wording – absolutely no abbreviations.

Dr Allan Manning of the LMI Group