Embed Size (px)

Citation preview

Dominic de Vries

Leveraging Patents Financially

GABLER RESEARCH

Dominic de Vries

Leveraging Patents Financially A Company Perspective

With a foreword by Prof. Dr. Cornelius Herstatt

RESEARCH

Bibliographic information published by the Deutsche Nationalbibliothek

The Deutsche Nationalbibliothek lists this publication in the Deutsche Nationalbibliografi e;

detailed bibliographic data are available in the Internet at http://dnb.d-nb.de.

Dissertation Hamburg University of Technology, 2011

1st Edition 2011

All rights reserved

© Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2011

Editorial Offi ce: Marta Grabowski | Jutta Hinrichsen

Gabler Verlag is a brand of Springer Fachmedien.

Springer Fachmedien is part of Springer Science+Business Media.

www.gabler.de

No part of this publication may be reproduced, stored in a retrieval system

or transmitted, in any form or by any means, electronic, mechanical, photo-

copying, recording, or otherwise, without the prior written permission of the

copyright holder.

Registered and/or industrial names, trade names, trade descriptions etc. cited in this publica-

tion are part of the law for trade-mark protection and may not be used free in any form or by

any means even if this is not specifi cally marked.

Cover design: KünkelLopka Medienentwicklung, Heidelberg

Printed on acid-free paper

Printed in the Netherlands

ISBN 978-3-8349-3176-4

Foreword

Together with other intangible assets, patents constitute essential value and competitive

factors for companies, particularly companies in technology-intensive sectors. Patents’ legal

and economic value is beyond question, while their quantitative valuation remains

challenging due to a lack of efficient and reliable methods. In practice, the valuation of

patents is therefore often limited to qualitative appraisals and “strategic” assessments.

This dissertation’s point of departure is the observation that the value of patents and patent

portfolios are often accounted for indirectly, but not based on qualitative valuations in

corporate financing. In this study, Dominic de Vries investigates whether and to what extent

patents may contribute to corporate financing and which factors may be relevant for it. Thus,

he observes the high importance of patents for innovative companies on the one hand and the

difficult utilization of these valuable assets for corporate financing on the other, placing his

focus on this discrepancy. Based on an empirical study, he addresses his set of research

questions within the German industry. As a result, Dominic de Vries provides descriptive and

partially explanatory findings and translates these into hypotheses. In the process, he chooses

an explorative, survey-based research approach, which he combines with a large-scale

empirical study.

In my view, the overall findings of his research are interesting and enriching for academics as

well as practitioners. The distinction of the findings concerning company size clusters allows

for a differentiated insight into corporate finance practice. Another interesting finding is that,

to date, mostly traditional financing instruments have been used to involve patents as

economic assets.

I consider Dominic de Vries’s dissertation a recommendable contribution in every respect.

Univ. Prof. Dr. Cornelius Herstatt

Hamburg, July 2011

Preface

Intellectual property (IP) is a key factor for the creation of value across industries and its

importance is widely recognized. However, measures of the value of IP assets are mostly

limited to qualitative appraisals, due to difficulties and deficiencies of quantitative valuation

methods. As a result, the value of IP, subsumed as intangible assets in reporting standards, is

not adequately represented in the range of corporate financing. Based on expert interviews

and a large-scale survey across technology-intensive industries in Germany, the objective of

this thesis is to find out how patents might contribute to the external access of companies to

financial sources. Within the class of IP assets, I focus on patents, since these are fungible

rights and form a large part of a company’s technological capital. As one of the first in-depth

empirical studies, this thesis explores the actual relevance of and identifies the main influence

factors for companies to leverage patents financially across industry and company size

clusters, and provides an analytical model with the influence factors to analyze the financial

utilization of patents. I therefore seek to contribute to a better theoretical understanding and to

facilitate the practical applicability of patents to external financing instruments.

I wrote this thesis as a research associate at the Institute for Technology and Innovation

Management at the Hamburg University of Technology. I am grateful to Prof. Dr. Cornelius

Herstatt for his supervision and academic support as well as the valuable and pleasant time at

his Institute. Besides allowing me a broad thesis development scope, he also supported me

throughout in many ways. I thank Prof. Dr. Matthias Meyer for his second advisory role,

interest and kind support. I also thank Prof. Thomas J.C. Matzen for the extremely interesting

and inspiring time as his assistant. This time as doctoral candidate was one of professional

and personal enrichment.

Furthermore, I appreciate the contribution of the experts and interview partners who provided

time, valuable insights, and substantial input for my empirical study. My kind thanks to all my

colleagues at the Institute for the company and their valuable advice and support for my work.

Finally, I thank my family for keeping me grounded and my friends Frank and Florian for the

great time and extraordinary fellowship over the years.

Dominic de Vries

Hamburg, July 2011

Outline

Foreword .................................................................................................................................. VPreface ................................................................................................................................... VIIOutline ..................................................................................................................................... IXList of Abbreviations .............................................................................................................. XIList of Figures ...................................................................................................................... XIIIList of Tables ......................................................................................................................... XV 1 Introduction ...................................................................................................................... 1

1.1 Purpose and objective ................................................................................................. 11.1.1 The increasing relevance of intellectual property .............................................. 11.1.2 Challenges in leveraging intellectual property financially ................................. 31.1.3 Research objectives ............................................................................................ 6

1.2 Introduction of central concepts and thesis focus ...................................................... 91.2.1 Introduction of key concepts and definitions ..................................................... 91.2.2 Thesis focus ...................................................................................................... 111.2.3 Thesis structure ................................................................................................ 14

2 The economics of patents ............................................................................................... 16

2.1 The concept of patents and patenting trends ............................................................ 162.1.1 The concept of patents ...................................................................................... 162.1.2 Patenting trends ................................................................................................ 19

2.2 Asset characteristics of patents ................................................................................ 202.2.1 Motives and barriers to patent .......................................................................... 212.2.2 Patents as value drivers .................................................................................... 262.2.3 Patents as value indicators ................................................................................ 292.2.4 Patents as 'assets per se' .................................................................................... 322.2.5 Patents compared to tangible assets ................................................................. 33

2.3 The value question ................................................................................................... 362.3.1 The value distribution of patents ...................................................................... 362.3.2 How to assess the value of patents ................................................................... 38

2.4 The liquidity question ............................................................................................... 412.4.1 The external acquisition and exploitation of patents ........................................ 422.4.2 The external acquisition of patents ................................................................... 432.4.3 The external exploitation of patents ................................................................. 472.4.4 Markets for technology .................................................................................... 522.4.5 Evolving patent-based business models ........................................................... 58

2.5 Synopsis of the economics of patents ...................................................................... 61 3 Patents as financial assets .............................................................................................. 63

3.1 The perception of patents in financial statements .................................................... 633.2 How to leverage patents financially ......................................................................... 67

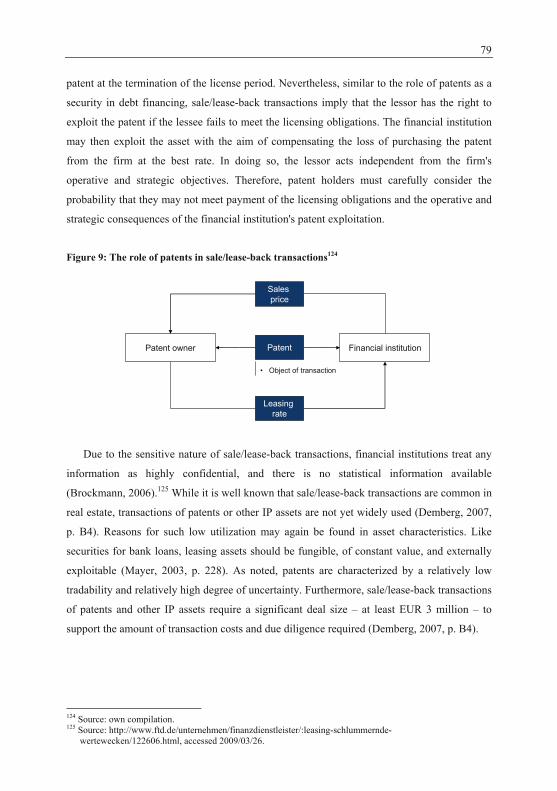

3.2.1 The role of patents in equity transactions ......................................................... 693.2.2 The role of patents in debt financing ................................................................ 723.2.3 The role of patents in sale/lease-back transactions .......................................... 773.2.4 The role of patents in patent funds ................................................................... 80

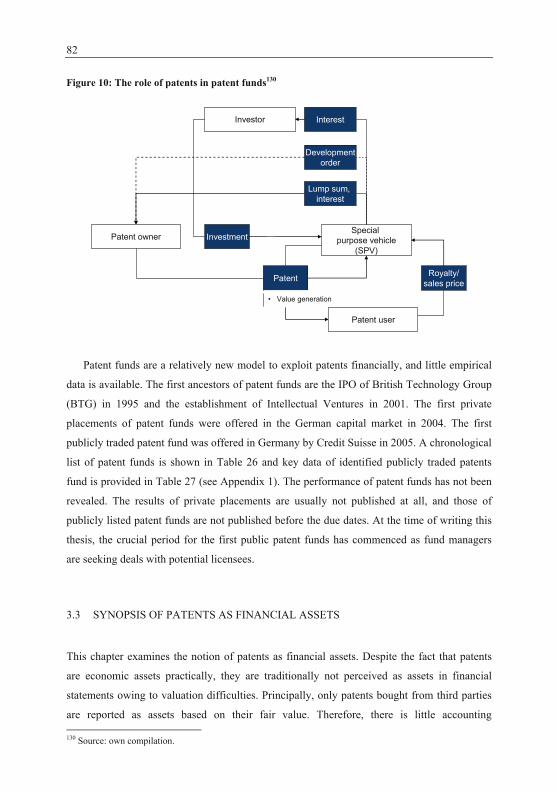

3.3 Synopsis of patents as financial assets ..................................................................... 82

X

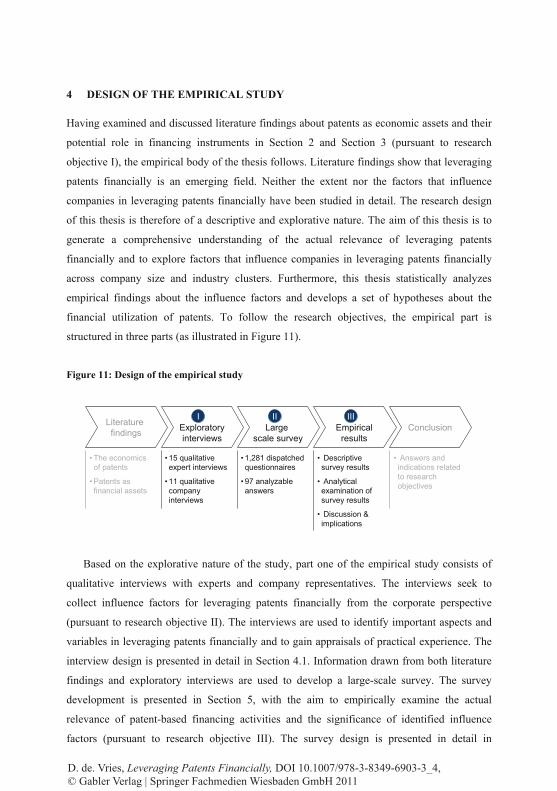

4 Design of the empirical study ........................................................................................ 844.1 Exploratory interviews ............................................................................................. 854.2 Large-scale survey .................................................................................................... 874.3 Statistical measures and methods ............................................................................. 89

5 Development of the survey ............................................................................................ 92

5.1 Asset characteristics of patents reconsidered ........................................................... 925.2 Endogeneous financial exploitability of patents ...................................................... 945.3 Actual extent and potential of leveraging patents financially .................................. 975.4 Influence factors for companies to leverage patents financially .............................. 98

5.4.1 Financial influence factors ............................................................................... 985.4.2 Asset-related influence factors ....................................................................... 1035.4.3 Managerial influence factors .......................................................................... 105

6 Descriptive results of the empirical study .................................................................. 107

6.1 Description of the survey sample ........................................................................... 1076.2 Asset characteristics of patents .............................................................................. 111

6.2.1 Patent use and patent management trends ...................................................... 1116.2.2 The value and valuation of patents ................................................................. 114

6.3 Endogenous financial exploitability of patents ...................................................... 1186.4 Actual extent and potential of the financial utilization of patents .......................... 1206.5 Influence factors for companies to leverage patents financially ............................ 123

6.5.1 Financial influence factors ............................................................................. 1246.5.2 Asset-related influence factors ....................................................................... 1266.5.3 Managerial influence factors .......................................................................... 128

6.6 Summary of major descriptive findings ................................................................. 129 7 Analytical examination of the survey results ............................................................. 133

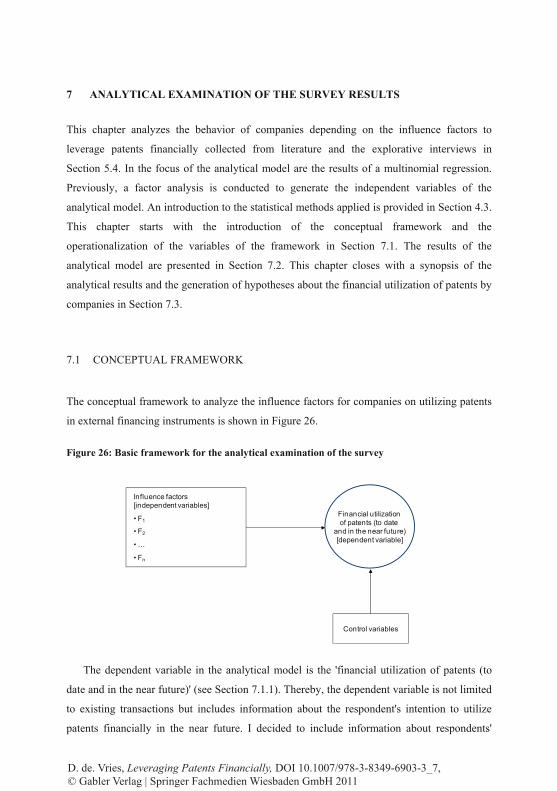

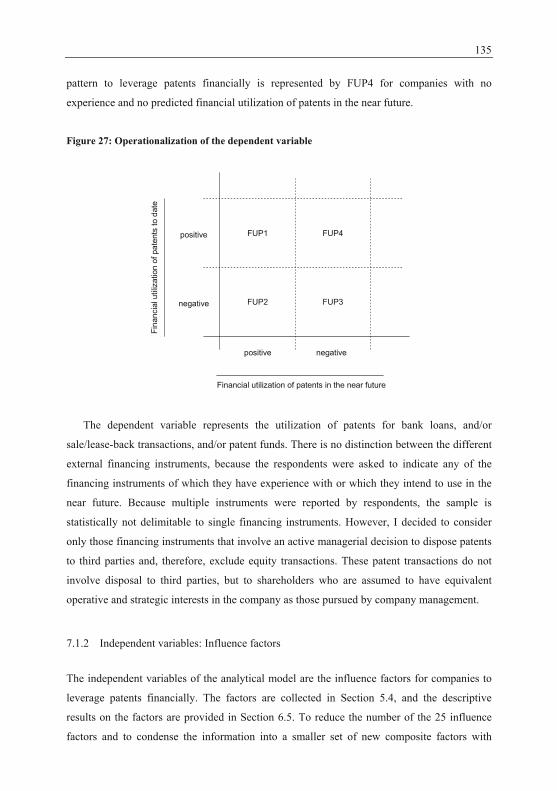

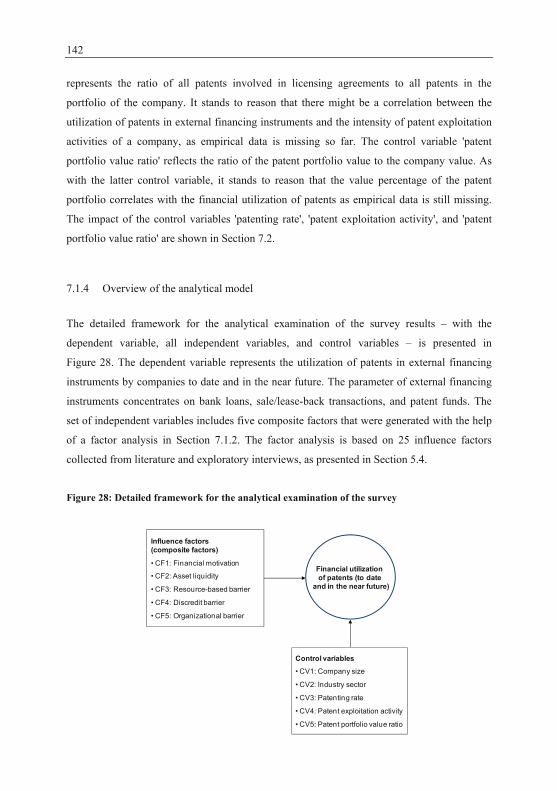

7.1 Conceptual framework ........................................................................................... 1337.1.1 Dependent variable: Financial utilization of patents ...................................... 1347.1.2 Independent variables: Influence factors ........................................................ 1357.1.3 Control variables ............................................................................................ 1407.1.4 Overview of the analytical model .................................................................. 142

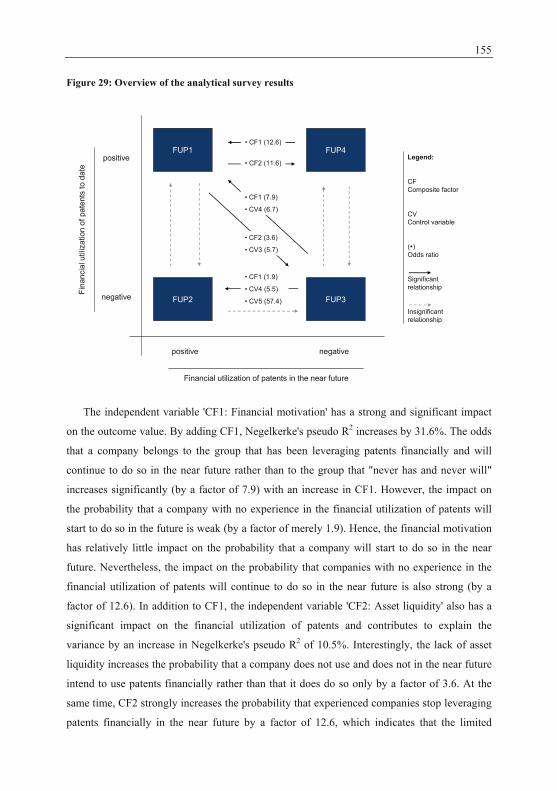

7.2 Analytical result of the empirical study and generation of hypotheses .................. 1437.3 Synopsis of the analytical survey results ................................................................ 154

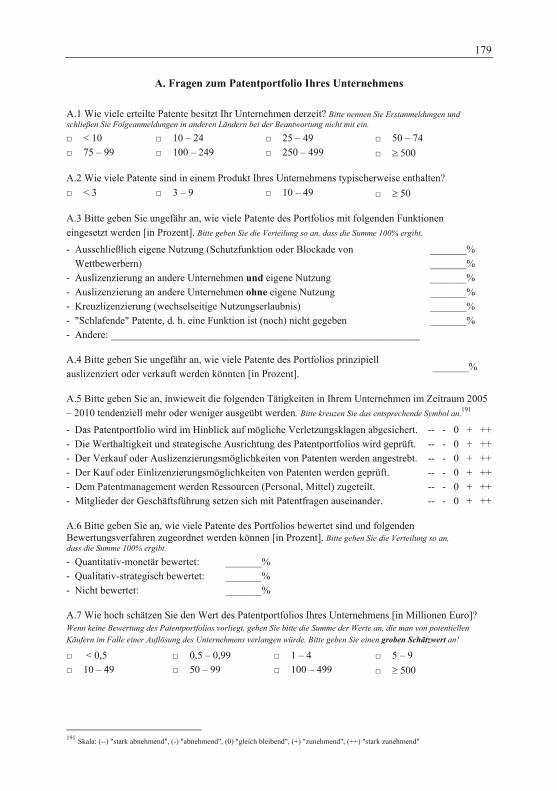

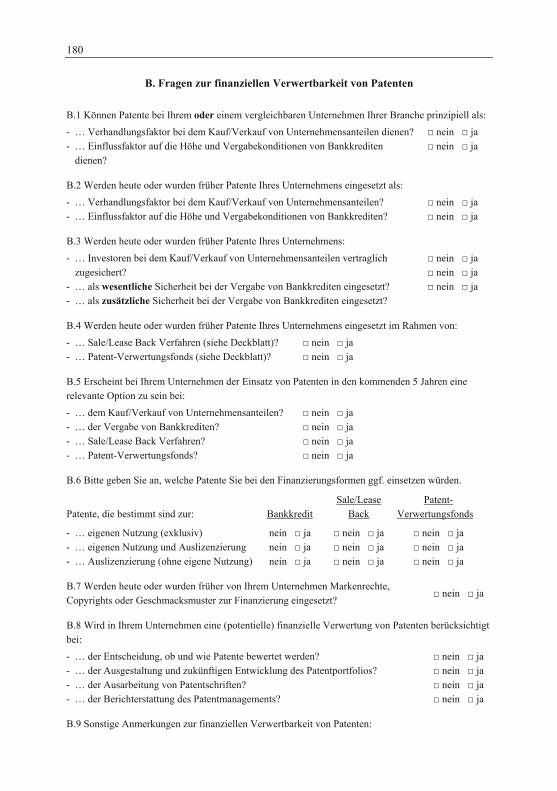

8 Discussion and implications ......................................................................................... 157 9 Conclusion ..................................................................................................................... 171 Appendix 1: General information on the concept of patents ........................................... 173Appendix 2: Questionnaire .................................................................................................. 178Appendix 3: Information on descriptive results of the empirical study .......................... 183Appendix 4: Information on the analytical examination of survey result ...................... 194 List of references .................................................................................................................. 197

List of Abbreviations

BaFin Bundesanstalt für Finanzdienstleistungsaufsicht (Federal Financial Supervisory

Authority)

BCBS Basel Committee on Banking Supervision

BilMoG Bilanzmodernisierungsgesetz (Balance Modernization Act)

BGB Bürgerliches Gesetzbuch (German Code of Civil Law)

CDAX Composite Deutscher Aktien Index (Composite German Stock Index)

CEO chief executive officer

CF cash flow

CFO chief financial officer

DAX Deutscher Aktienindex (German Stock Index)

DCF discounted cash flow

DPMA Deutsches Patent- und Markenamt (German Office for Patents and Registered Brand Names)

EPC European Patent Convention

EPO European Patent Office

EU EUR

European Union Euro

FASB Financial Accounting Standards Board (US)

FDA Food and Drug Administration (US)

GDP gross domestic product

HGB Handelsgesetzbuch (German Commercial Code)

IAS International Accounting Standards

IASB International Accounting Standards Board

ICT information and communication technology

IFD IFRS

Initiative Finanzstandort Deutschland International Financial Reporting Standards

IP intellectual property

IPO initial public offering

IPR intellectual property rights

JPO JPY

Japan Patent Office Japanese Yen

JV joint venture

M&A merger & acquisition

MNC multinational corporation

N/K not known

XII

OECD OEM

Organization for Economic Co-operation and Development original equipment manufacturer

PatG Patentgesetz (Patent Act)

R&D research and development

RDFO research and development financial organization

RoI return on investment

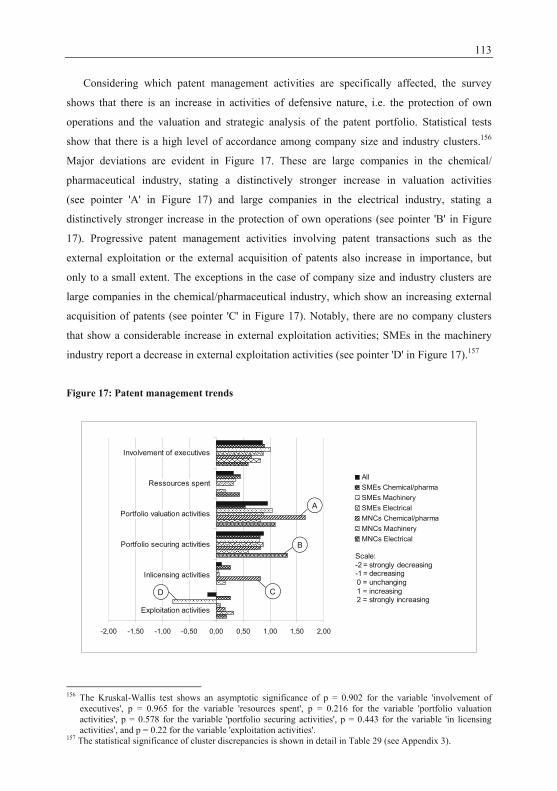

SME small and medium-sized enterprises

SolvV Solvabilitätsverordnung (Solvability Decree)

S&P Standard & Poor's

SPV special purpose vehicle

SWORD stock warrants of balance-sheet research and development

UK United Kingdom

US USD

United States of America United States Dollar

USGAAP United States Generally Accepted Accounting Principles

USPTO United States Patent and Trademark Office

VC venture capital

WIPO World Intellectual Property Organization

List of Figures

Figure 1: Illustration of the thesis focus ................................................................................... 11

Figure 2: Thesis structure ......................................................................................................... 14

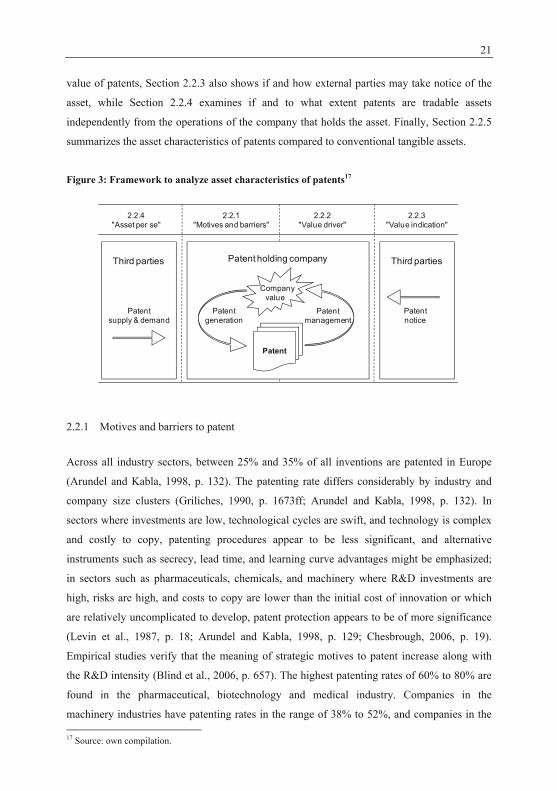

Figure 3: Framework to analyze asset characteristics of patents ............................................. 21

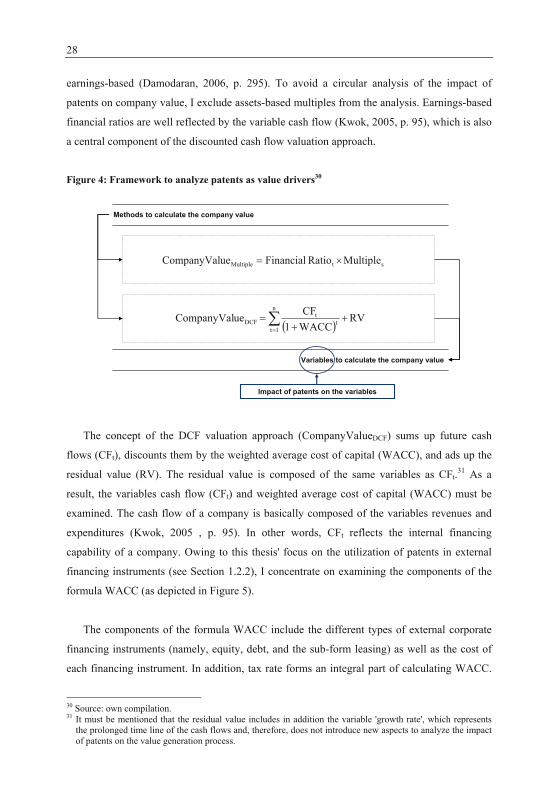

Figure 4: Framework to analyze patents as value drivers ........................................................ 28

Figure 5: WACC variables ....................................................................................................... 29

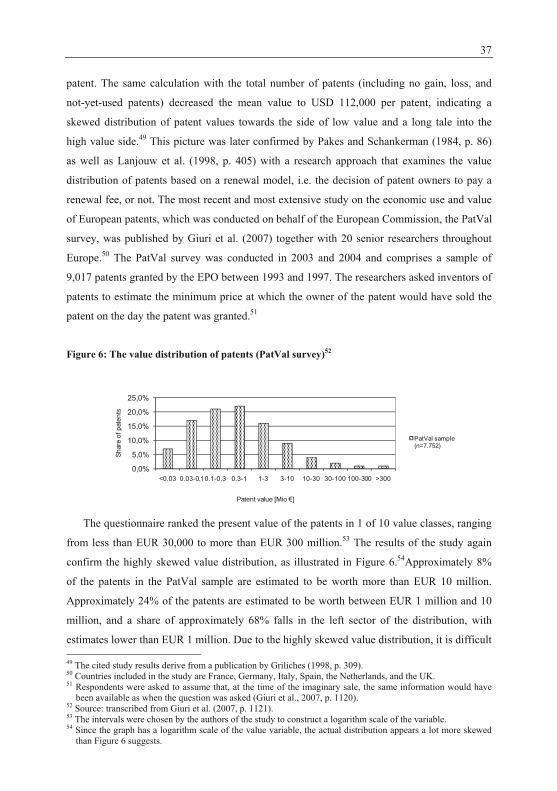

Figure 6: The value distribution of patents (PatVal survey) .................................................... 37

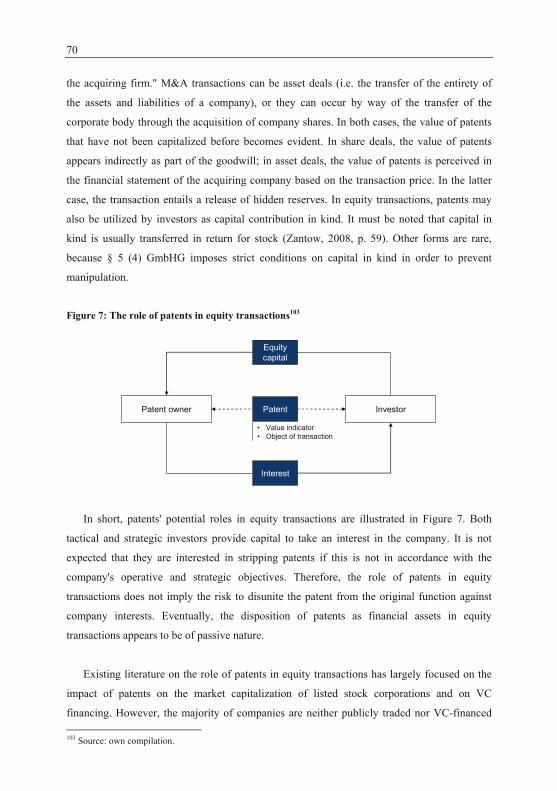

Figure 7: The role of patents in equity transactions ................................................................. 70

Figure 8: The role of patents in the acquisition of bank loans ................................................. 74

Figure 9: The role of patents in sale/lease-back transactions ................................................... 79

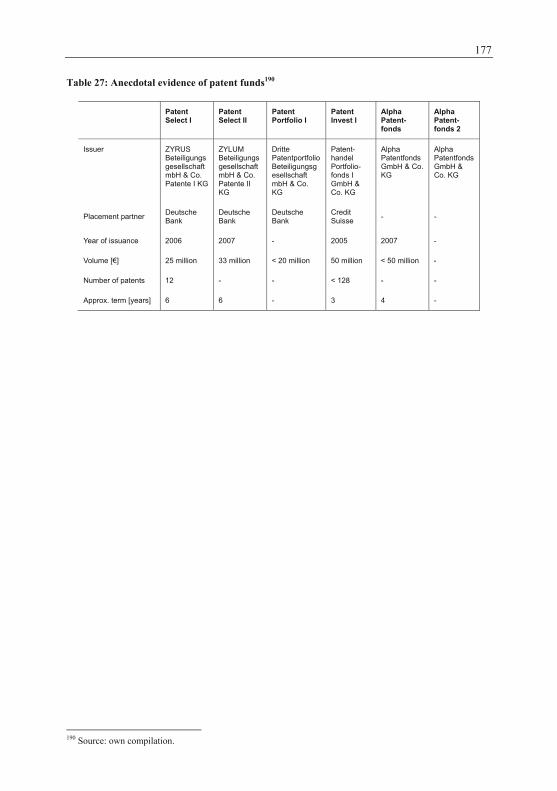

Figure 10: The role of patents in patent funds ......................................................................... 82

Figure 11: Design of the empirical study ................................................................................. 84

Figure 12: Patent disposition matrix ........................................................................................ 96

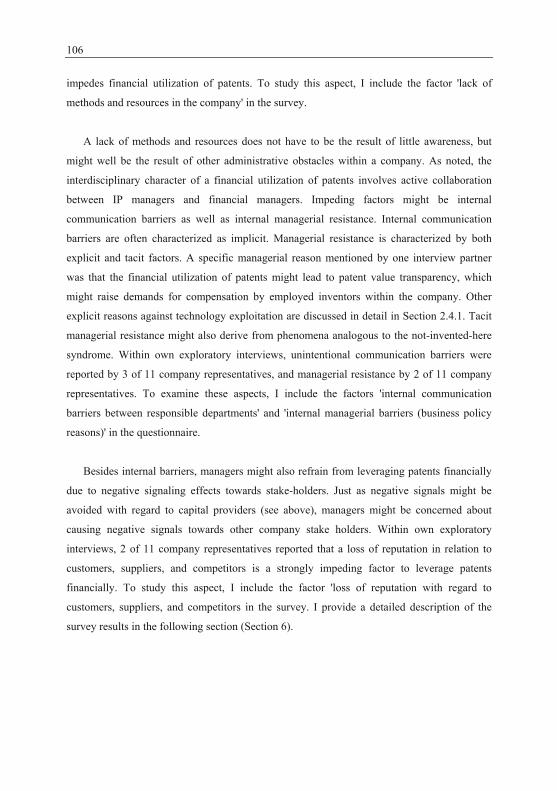

Figure 13: Overview of respondents' field of responsibility .................................................. 108

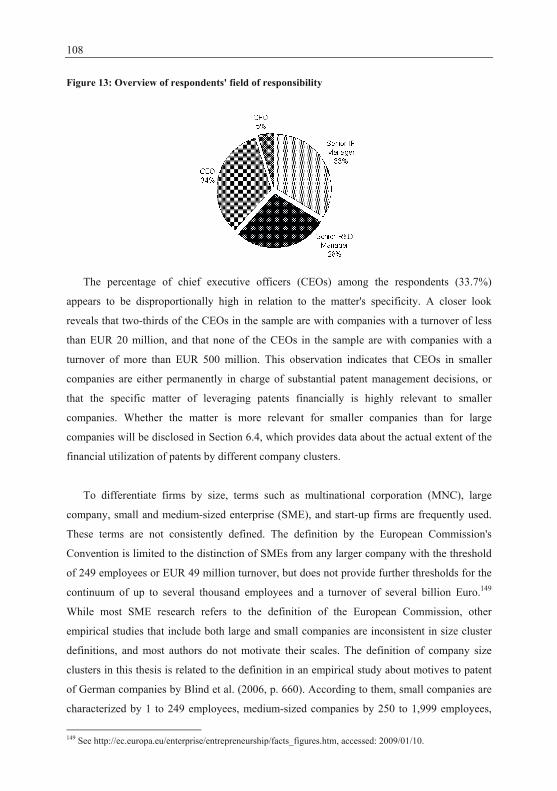

Figure 14: Distribution of company size clusters ................................................................... 109

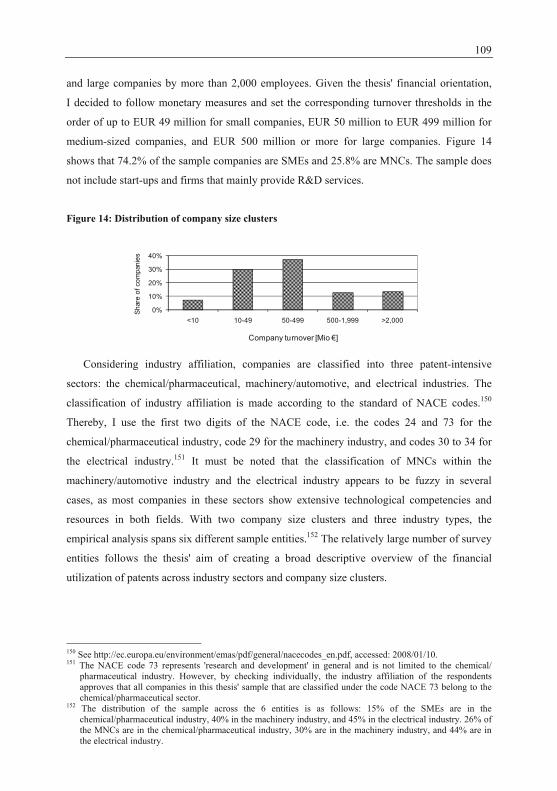

Figure 15: Distribution of industry affiliation ........................................................................ 110

Figure 16: Distribution of patent portfolio size clusters ........................................................ 110

Figure 17: Patent management trends .................................................................................... 113

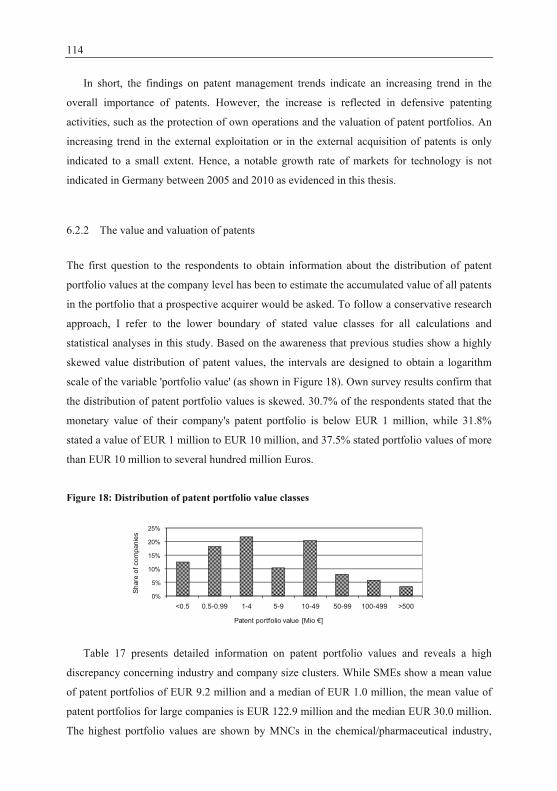

Figure 18: Distribution of patent portfolio value classes ....................................................... 114

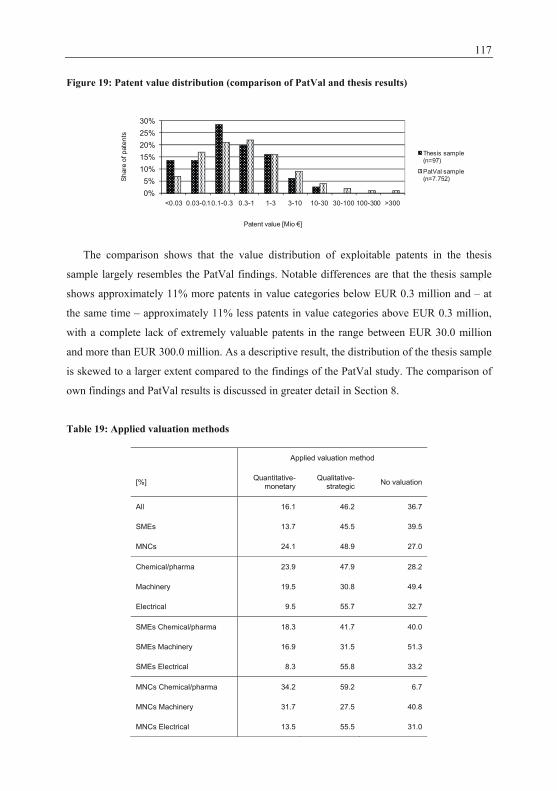

Figure 19: Patent value distribution (comparison of PatVal and thesis results) .................... 117

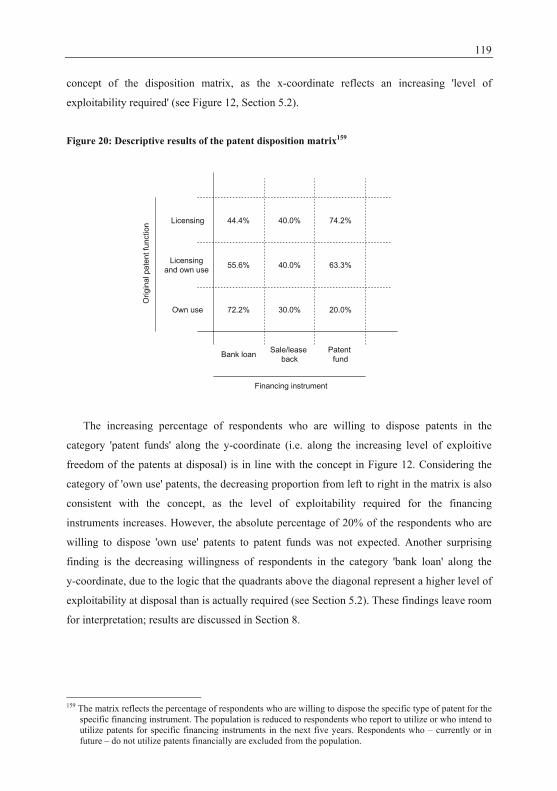

Figure 20: Descriptive results of the patent disposition matrix ............................................. 119

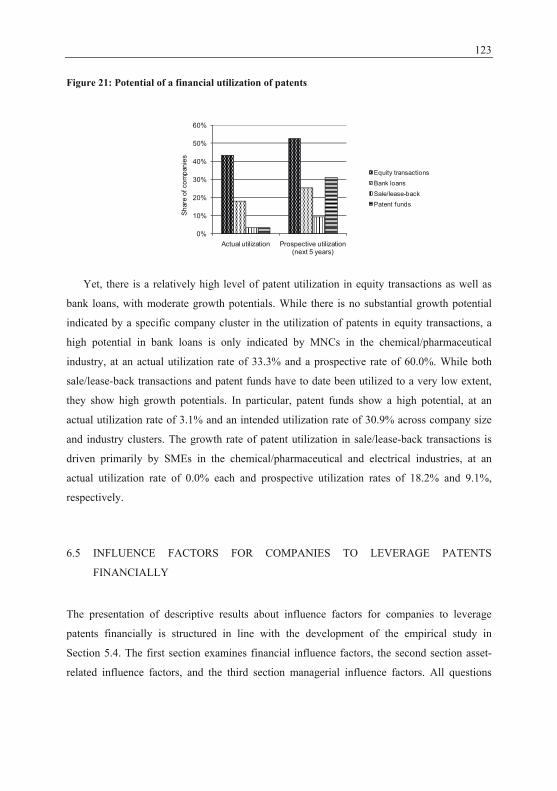

Figure 21: Potential of a financial utilization of patents ........................................................ 123

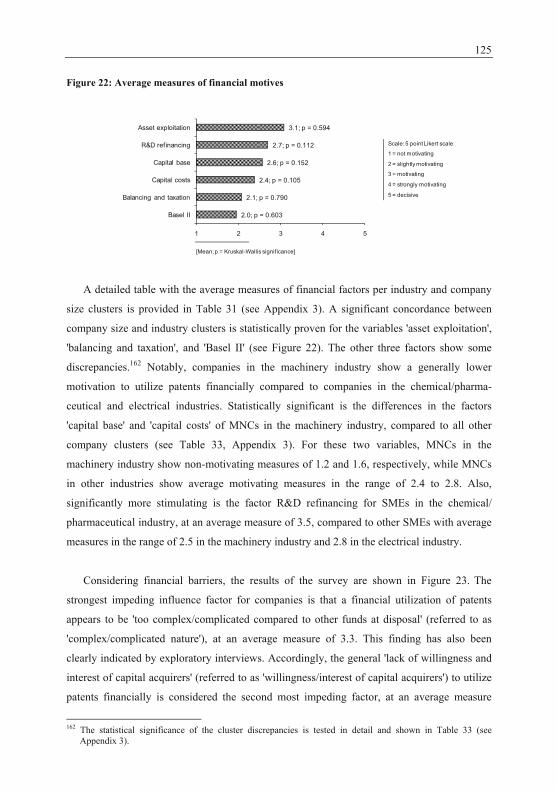

Figure 22: Average measures of financial motives ................................................................ 125

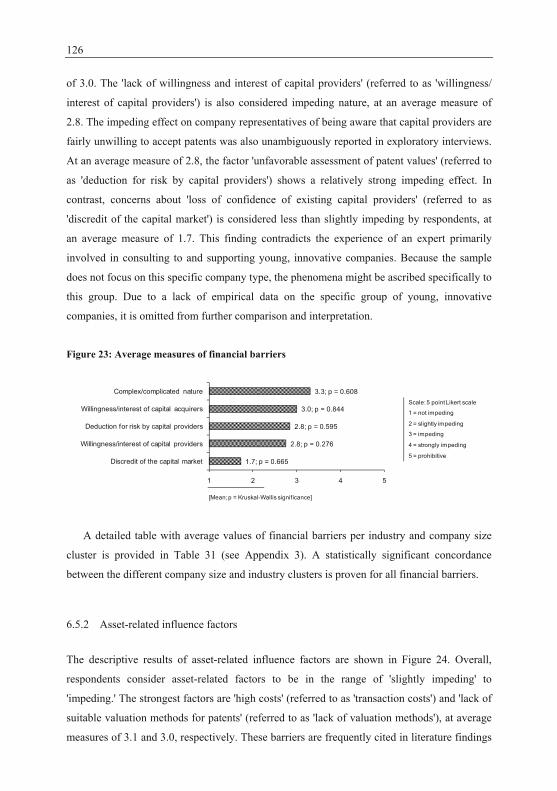

Figure 23: Average measures of financial barriers ................................................................ 126

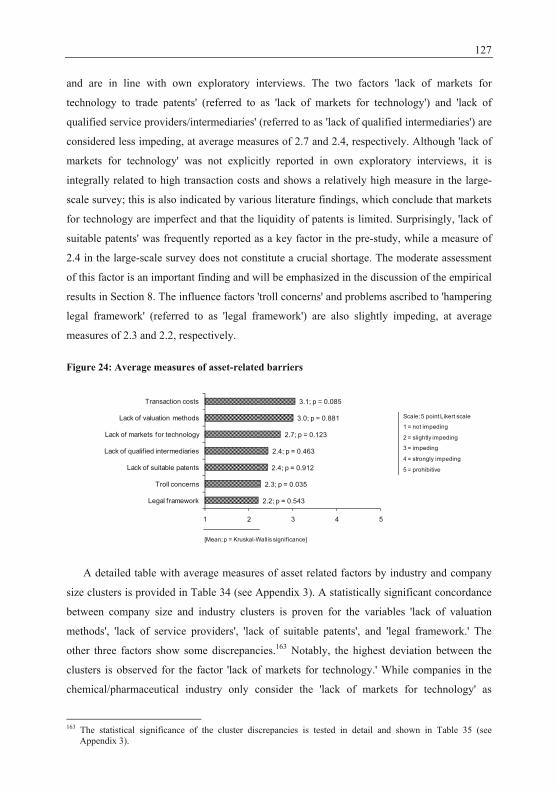

Figure 24: Average measures of asset-related barriers .......................................................... 127

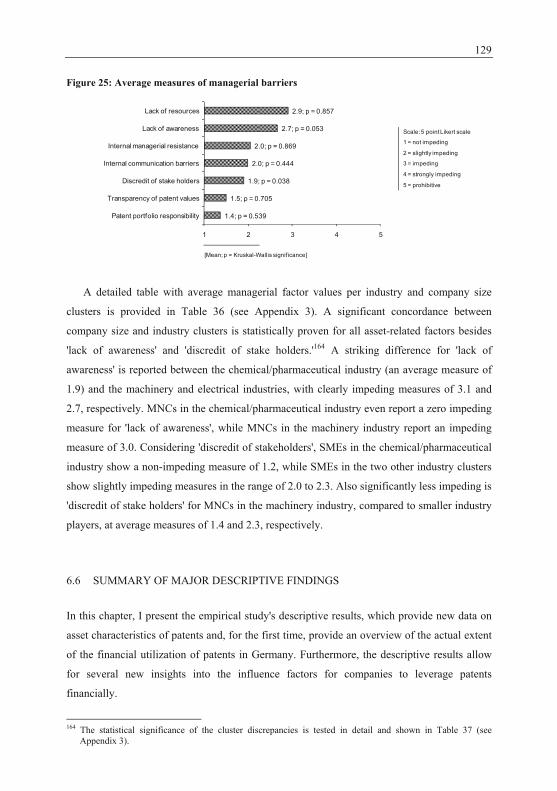

Figure 25: Average measures of managerial barriers ............................................................. 129

Figure 26: Basic framework for the analytical examination of the survey ............................ 133

Figure 27: Operationalization of the dependent variable ....................................................... 135

Figure 28: Detailed framework for the analytical examination of the survey ....................... 142

Figure 29: Overview of the analytical survey results ............................................................. 155

List of Tables

Table 1: Existing literature on leveraging patents financially .................................................... 7

Table 2: Patent statistics at DPMA and EPO in 2006 .............................................................. 19

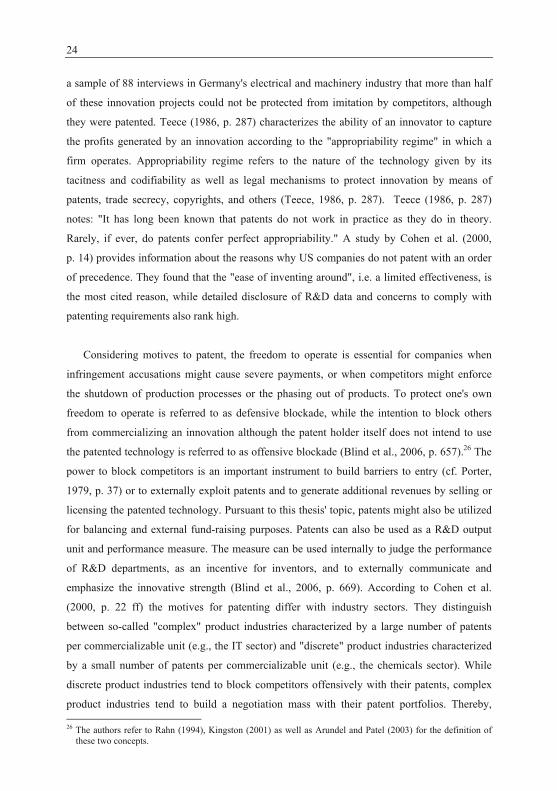

Table 3: Motives and barriers to patent .................................................................................... 22

Table 4: Overview of patent charges in the triad EU, US, and Japan (2003) .......................... 23

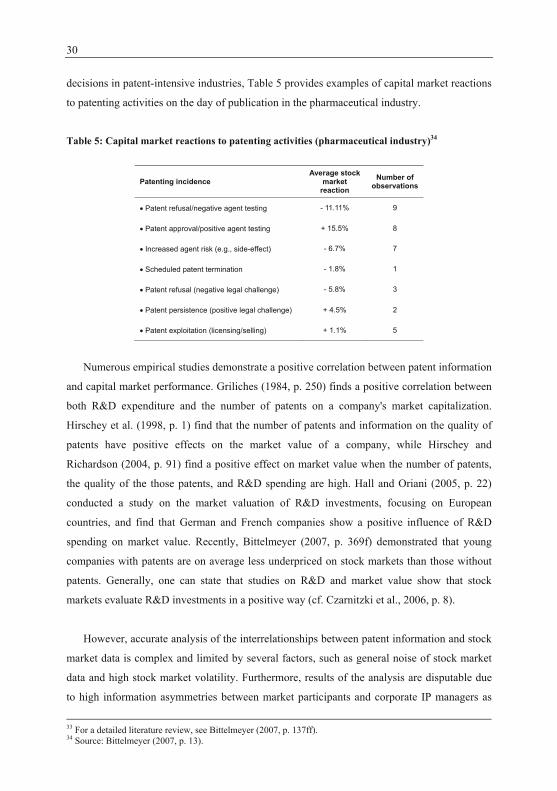

Table 5: Capital market reactions to patenting activities (pharmaceutical industry) ............... 30

Table 6: Patents compared to tangible assets ........................................................................... 34

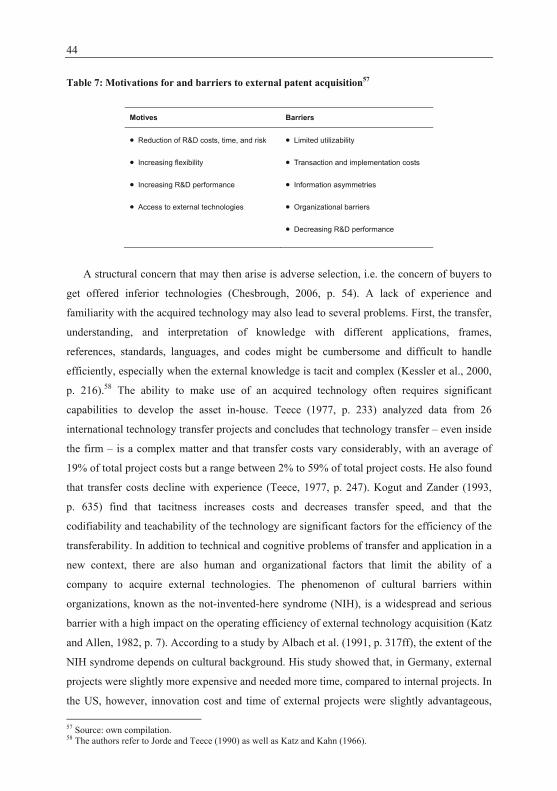

Table 7: Motivations for and barriers to external patent acquisition ....................................... 44

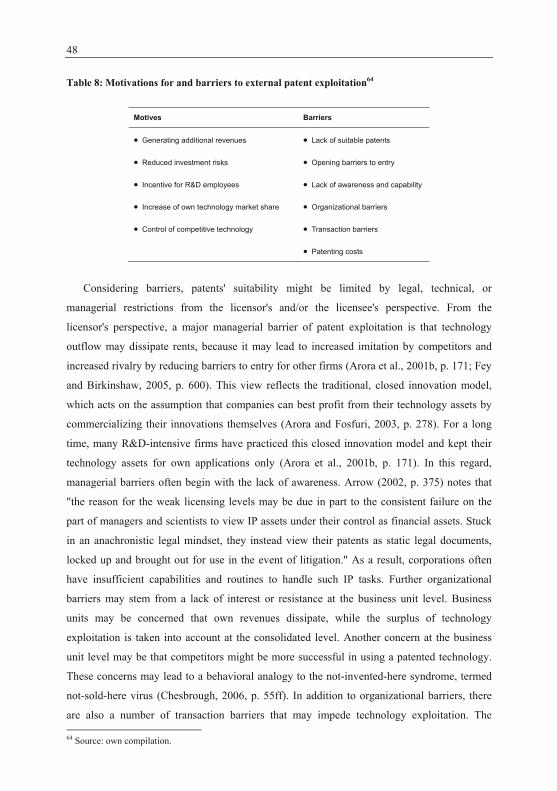

Table 8: Motivations for and barriers to external patent exploitation ...................................... 48

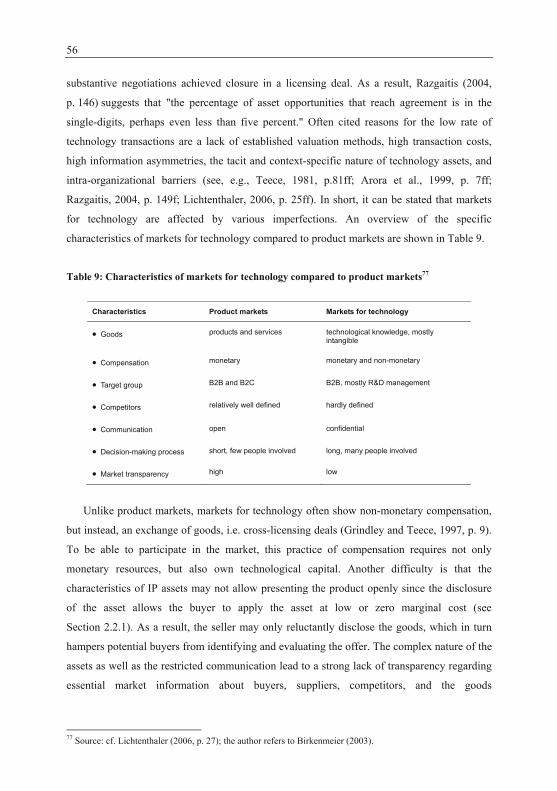

Table 9: Characteristics of markets for technology compared to product markets .................. 56

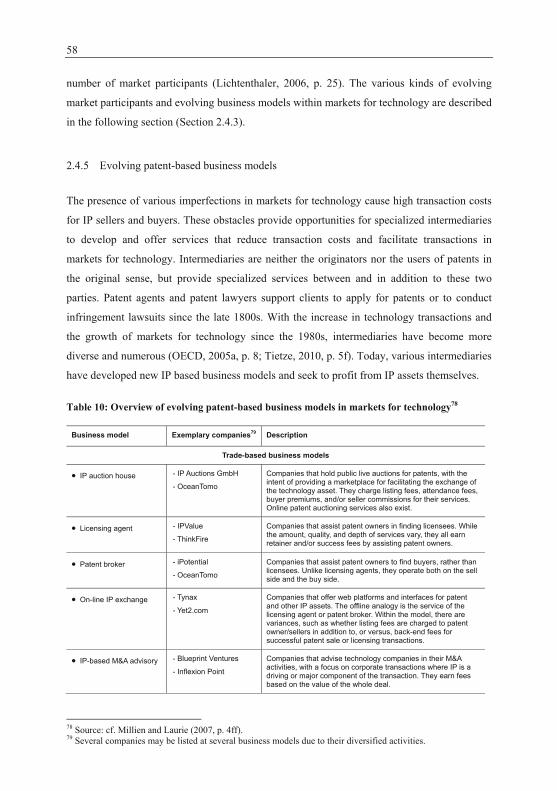

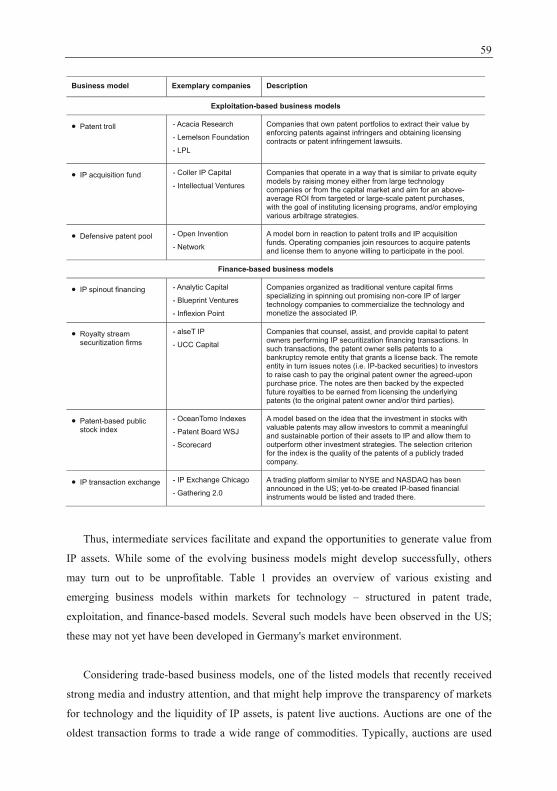

Table 10: Overview of evolving patent-based business models in markets for technology .... 58

Table 11: Capitalization of development expenditures (automotive industry, 2007) .............. 66

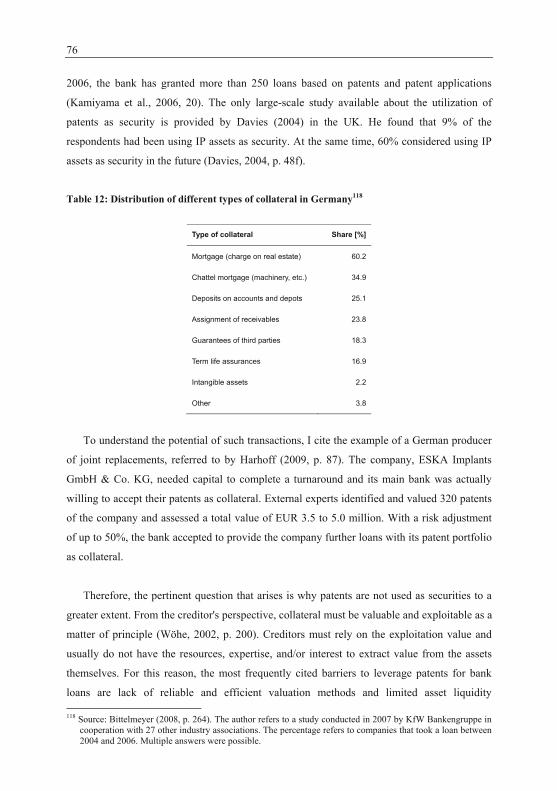

Table 12: Distribution of different types of collateral in Germany .......................................... 76

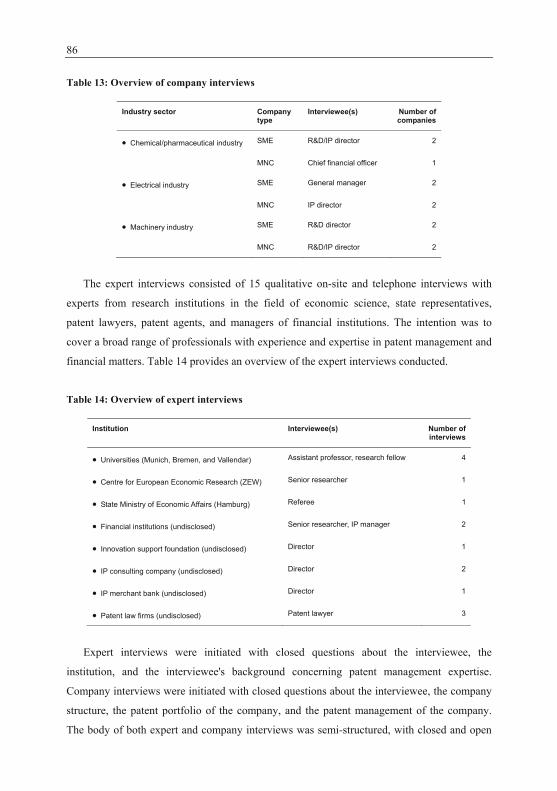

Table 13: Overview of company interviews ............................................................................ 86

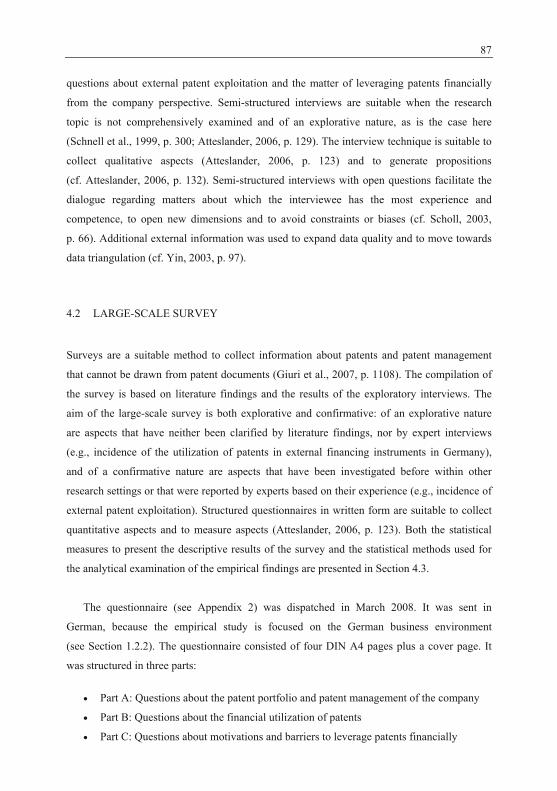

Table 14: Overview of expert interviews ................................................................................. 86

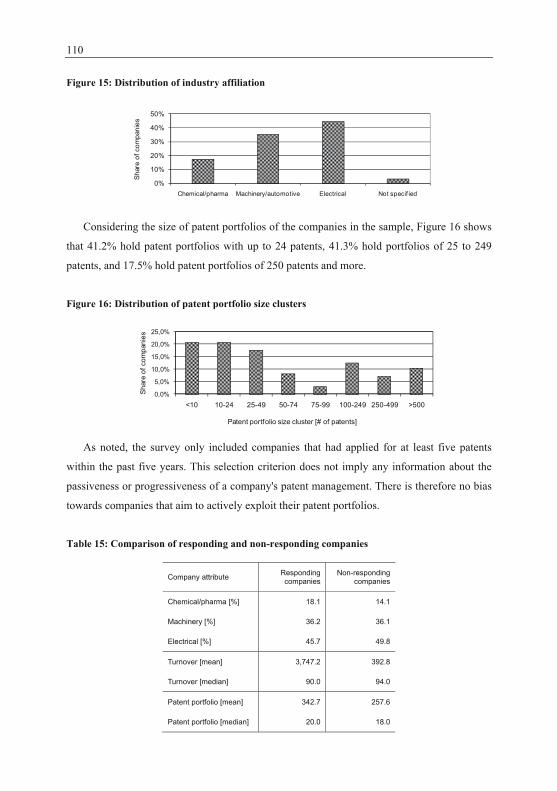

Table 15: Comparison of responding and non-responding companies .................................. 110

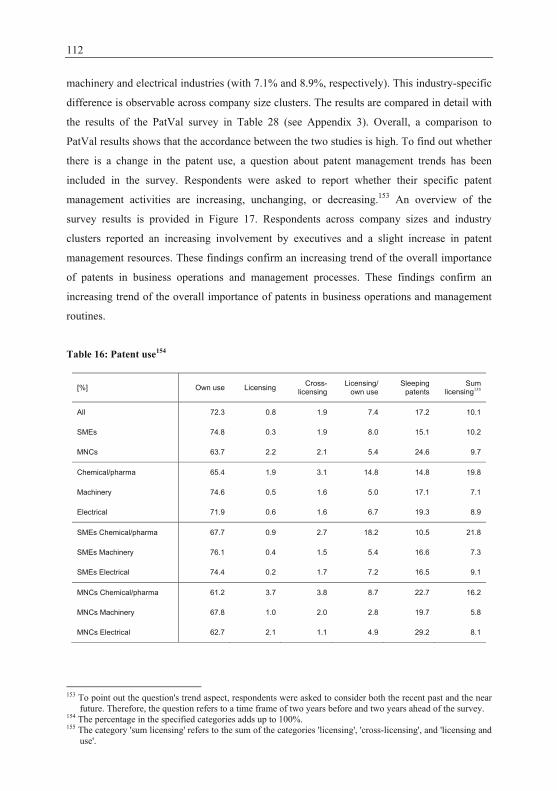

Table 16: Patent use ............................................................................................................... 112

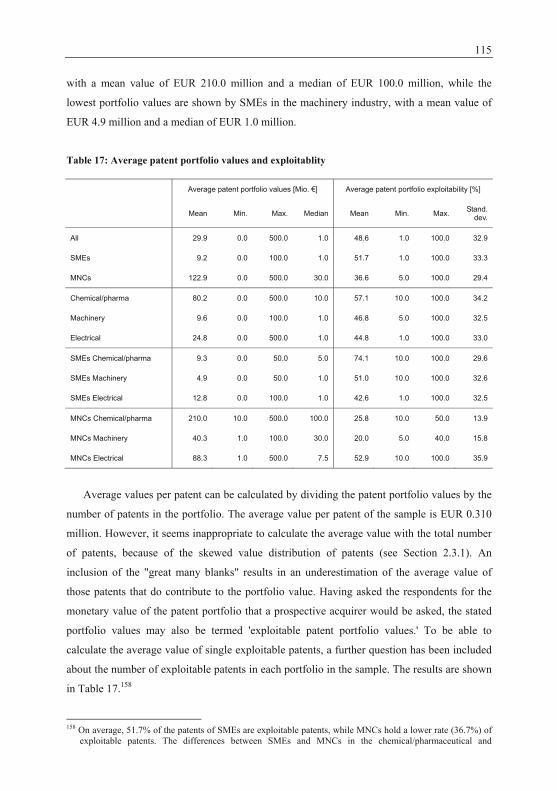

Table 17: Average patent portfolio values and exploitablity ................................................. 115

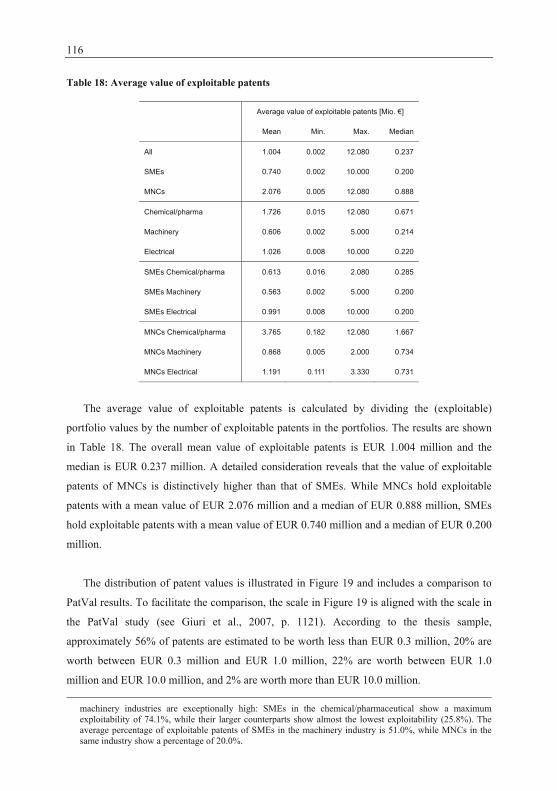

Table 18: Average value of exploitable patents ..................................................................... 116

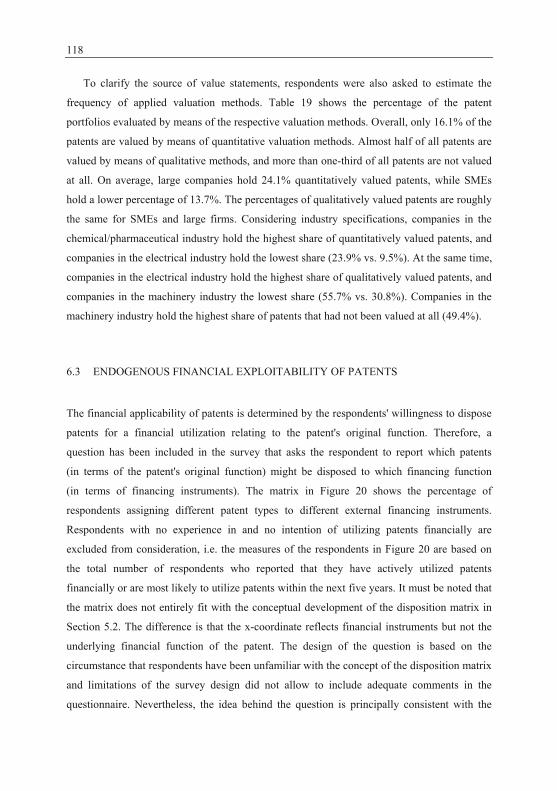

Table 19: Applied valuation methods .................................................................................... 117

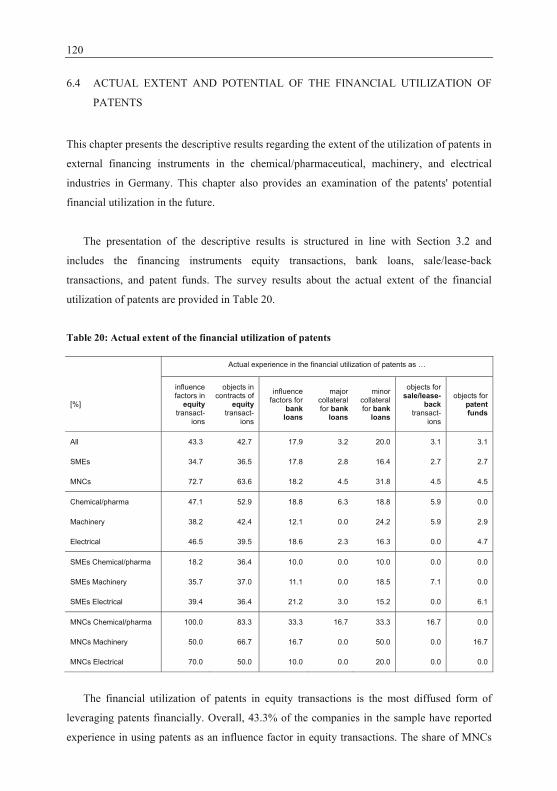

Table 20: Actual extent of the financial utilization of patents ............................................... 120

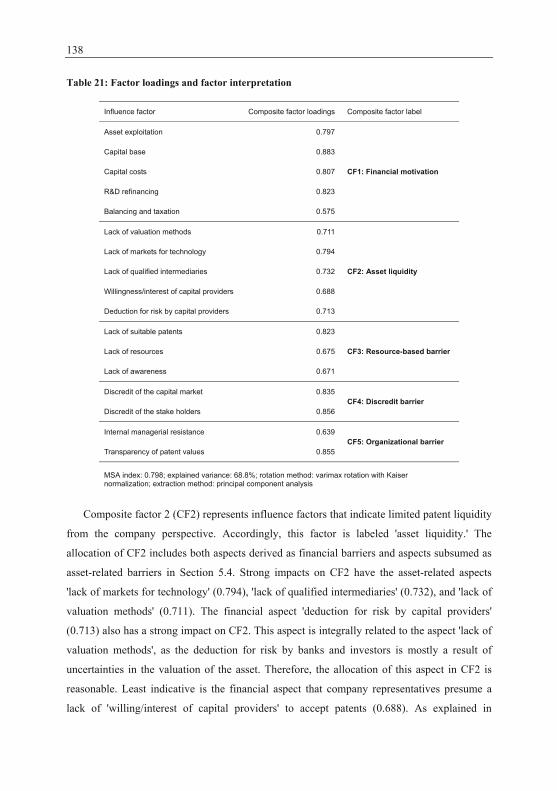

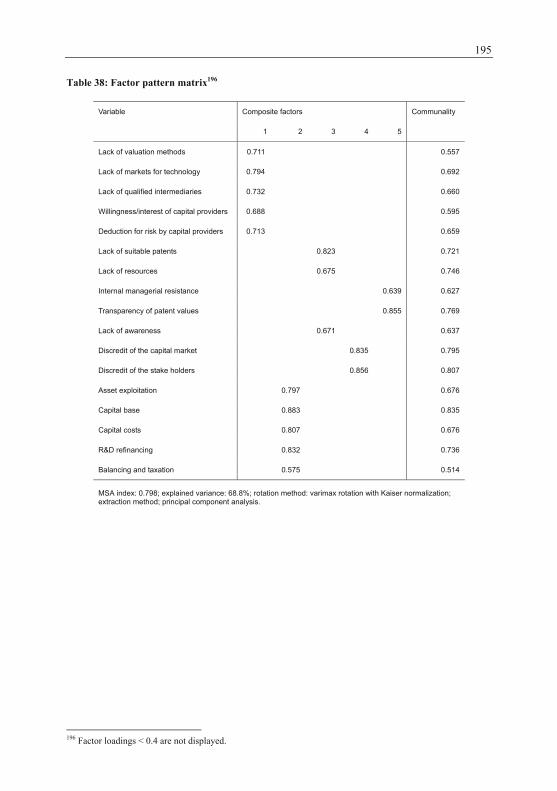

Table 21: Factor loadings and factor interpretation ............................................................... 138

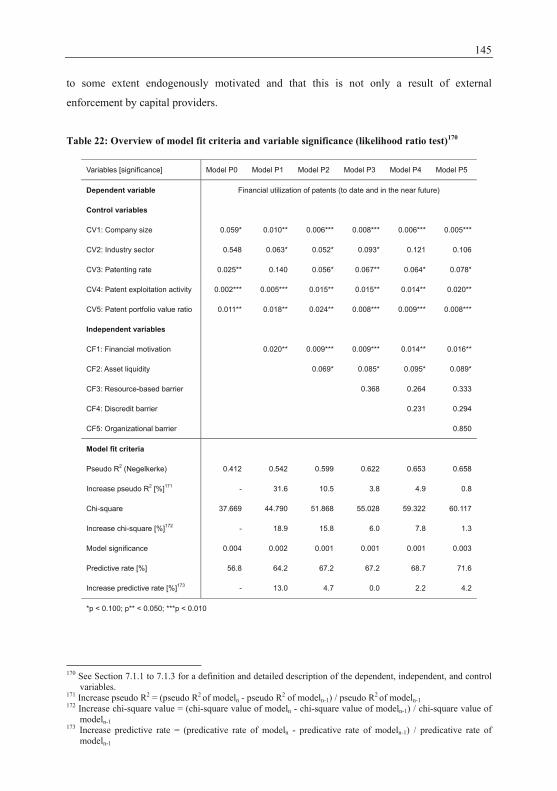

Table 22: Overview of model fit criteria and variable significance (likelihood ratio test) .... 145

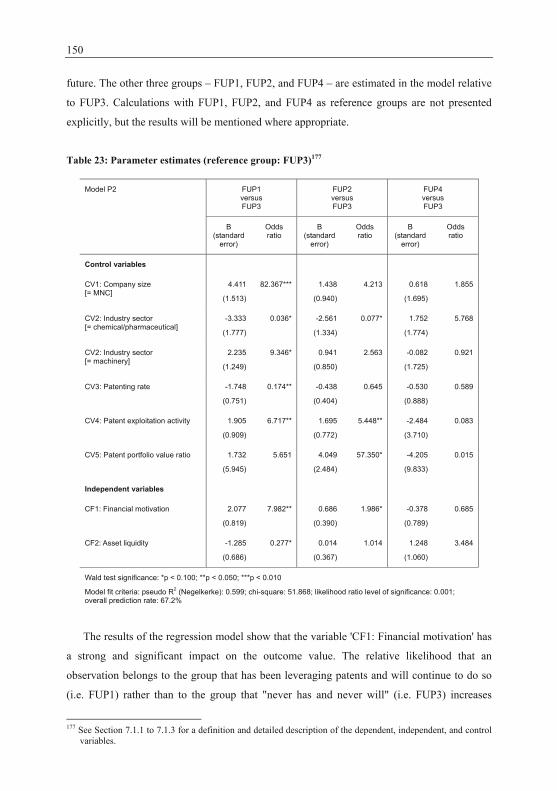

Table 23: Parameter estimates (reference group: FUP3) ....................................................... 150

Table 24: Anecdotal evidence of funds based on innovative company measures ................. 174

Table 25: Anecdotal evidence of external patent exploitation ............................................... 175

Table 26: History of patent funds ........................................................................................... 176

Table 27: Anecdotal evidence of patent funds ....................................................................... 177

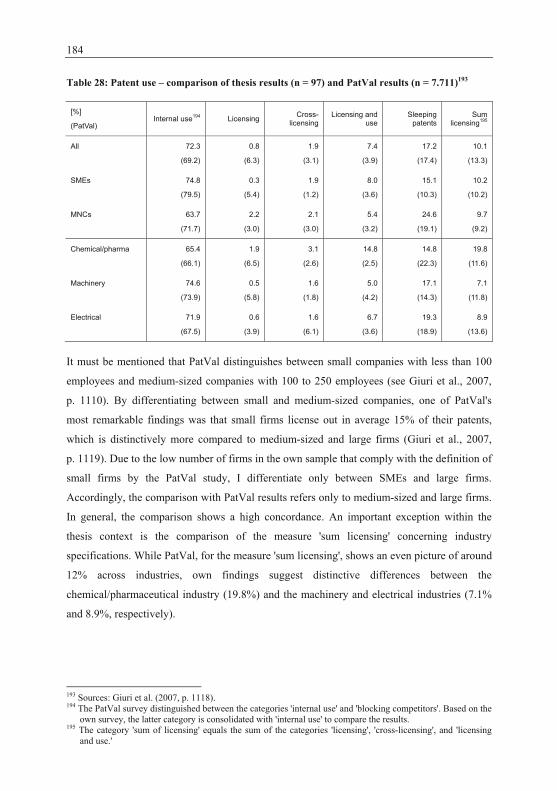

Table 28: Patent use - comparison of thesis results (n = 97) and PatVal results (n = 7.711) 184

Table 29: Company cluster discrepancies in patent management trends ............................... 185

Table 30: Feasibility of and prediction to leverage patents financially ................................. 186

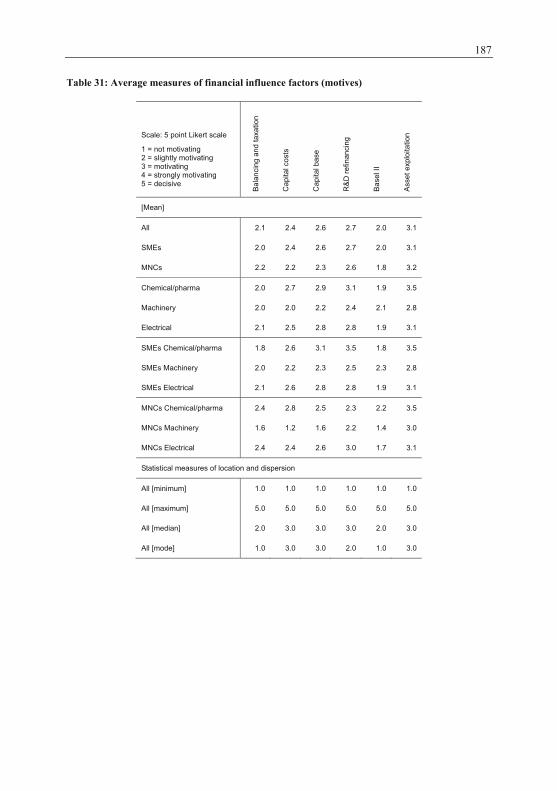

Table 31: Average measures of financial influence factors (motives) ................................... 187

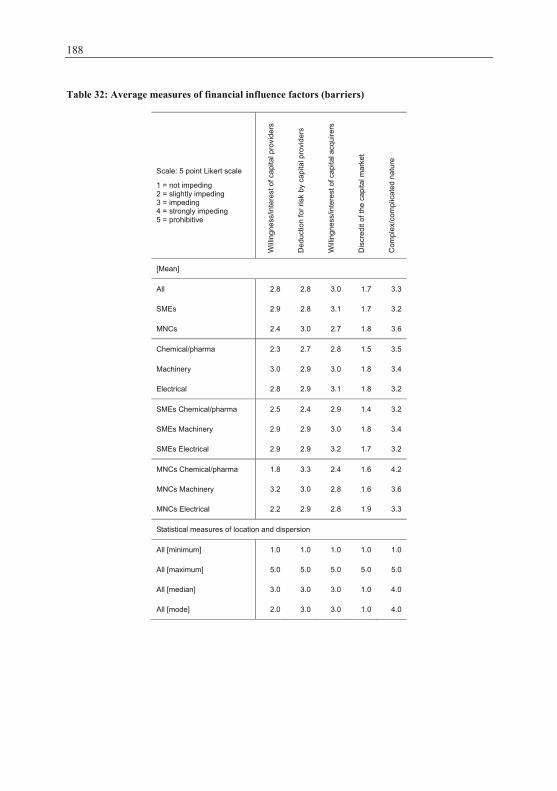

Table 32: Average measures of financial influence factors (barriers) ................................... 188

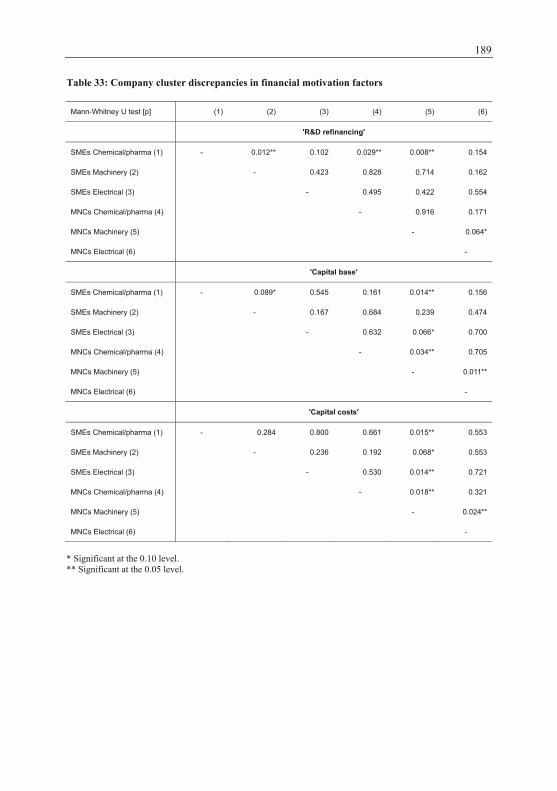

Table 33: Company cluster discrepancies in financial motivation factors ............................. 189

XVI

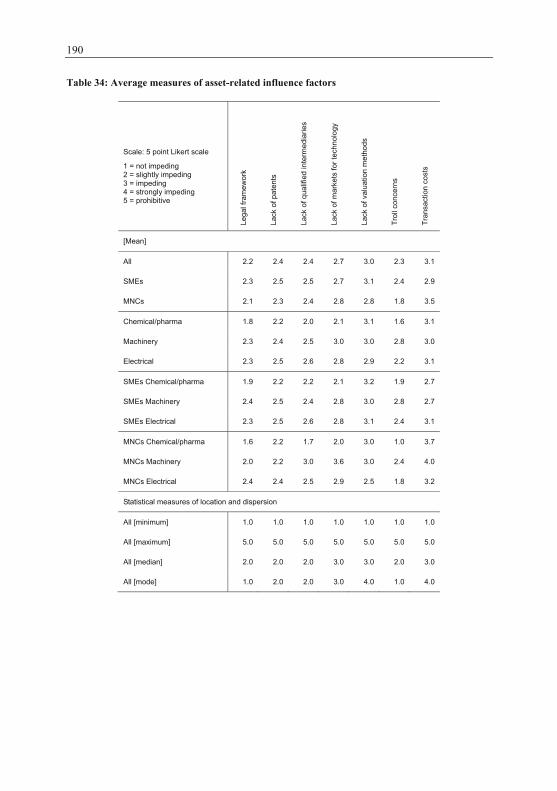

Table 34: Average measures of asset-related influence factors ............................................. 190

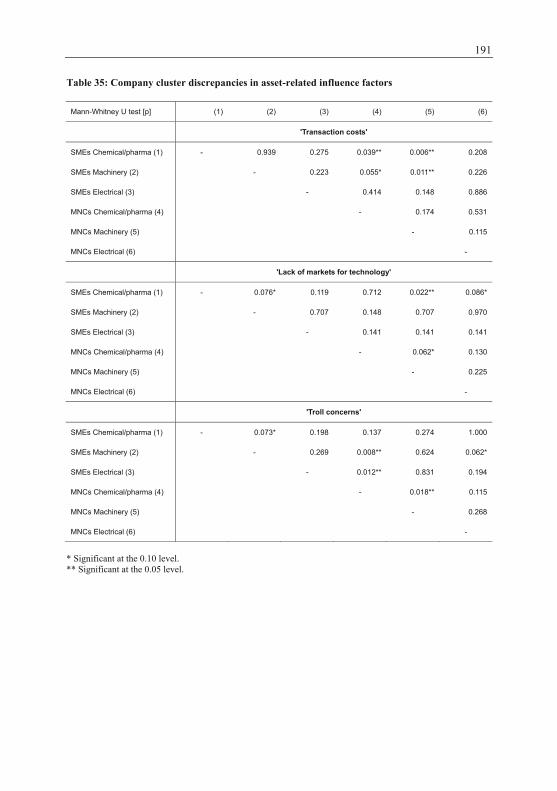

Table 35: Company cluster discrepancies in asset-related influence factors ......................... 191

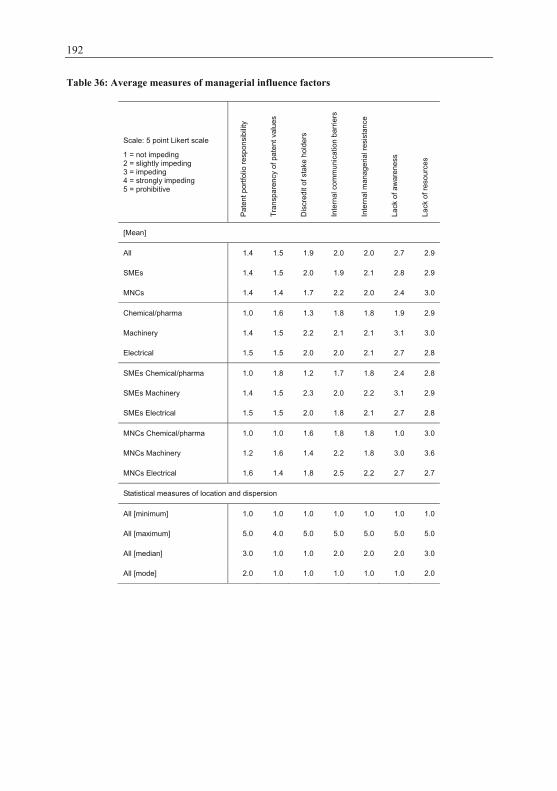

Table 36: Average measures of managerial influence factors ............................................... 192

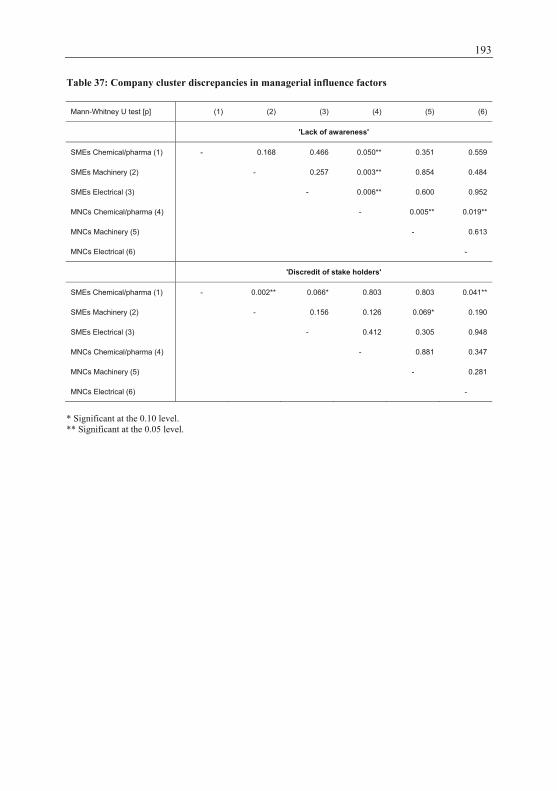

Table 37: Company cluster discrepancies in managerial influence factors ........................... 193

Table 38: Factor pattern matrix .............................................................................................. 195

1 INTRODUCTION "Corporate America is wasting a staggering USD 1 trillion in underutilized patent assets.

Given the pressures on companies these days to maximize shareholder returns, this

underutilization of technology assets represents either a stinging myopia regarding

intellectual property or the greatest opportunity to be handed to chief financial officers in a

generation" (Rivette and Kline, 2000, p. 143).

1.1 PURPOSE AND OBJECTIVE

This thesis explores the essential role of intellectual property (IP) assets for the creation of

economic value, the challenges and difficulties for market participants to leverage these assets

financially, and the chasm between them. Both the critical role of IP for the creation of

economic value and the challenges to leverage IP financially are reviewed in Sections 1.1.1

and 1.1.2, to derive the research objectives of the thesis in Section 1.1.3.

1.1.1 The increasing relevance of intellectual property

The importance and economic value of IP has increased considerably in developed countries

in the past (see, e.g., Granstrand, 1999, p. 8f; OECD, 2005a, p. 3). This increasing importance

is based on the shift from a labor-driven, industrial economy to a knowledge-based economy.

Economic scholars refer to the shift as a transformation towards "intellectual capitalism", i.e.

a capitalist, knowledge-intensive economy in which intellectual capital dominates capital

values, investments, and profit sources (Granstrand, 1999, p. 322). Accordingly, investments

in intellectual assets increased significantly since the 1980s and measure up to the levels of

investments in tangible assets in many OECD countries since the late 1990s (Nakamura,

2001, p. 2; OECD, 2006, p. 11). In line with the higher investments in IP, an increasing share

of the market value of companies is based on their intellectual assets (Kamiyama et al., 2006,

p. 6). By now, intangible capital constitutes the major percentage of corporate market values

of both old and new-economy companies (cf. Lev, 2003, p. 2). While, in 1982, intangibles

accounted, on average, for about 40% of corporate value (Kamiyama et al., 2006, p. 22), it is

estimated that in 2002, intangible assets accounted for 75% of the market value of US firms

(Kaplan and Norton, 2004, p. 4), indicating a major shift within two decades.

D. de. Vries, Leveraging Patents Financially, DOI 10.1007/978-3-8349-6903-3_1, © Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2011

2

This trend is enforced by the global division of labor. While man-hour-intensive

manufacturing activities associated with tangible assets are transferred to low-wage countries,

knowledge-intensive activities associated with intangible assets are concentrated in developed

countries. At the same time, however, the share of manufacturing output in GDP has remained

largely unchanged in developed countries. The confluence of a decreasing manufacturing

labor share and a stable or even growing manufacturing output in OECD countries is the

result of an increasing productivity (cf. Economist, 2005, p. 69), which can be ascribed to

investments in R&D, know-how, and other intangible assets (cf. Griliches, 2000, p. 15). Thus,

confronted with competition from low-wage countries with increasing manufacturing labor

shares, firms in OECD countries are investing in knowledge intensive activities to create

comparative advantage (OECD, 2005b, p. 5). The crucial role of IP for business performance

and economic growth in OECD countries is emphasized in various official economic reports

(see, e.g., OECD, 2006, p. 5). The Oxford Dictionary of Finance and Banking, for instance,

notes that "intangible assets are increasingly seen as the key to competitive advantage and the

market value of a firm" (Smullen and Hand, 2005, p. 213).

Some executives are staying abreast of this structural change and increasingly attach

importance to the active and strategic management of IP assets and the optimization of their

IP portfolios so as to increase value creation (Kamiyama et al., 2006, p. 6; PwC, 2007, p. 5).

Studies about IP management activities have traditionally shown fairly defensive patenting

activities to prevent copying, to block competitors, and to prevent lawsuits. Within the past

decades, several studies have also shown a development of patent management activities

towards a more active external acquisition and exploitation of IP assets (see, e.g., Kamiyama

et al., 2006, p. 7), to generate additional revenues and develop IP units from cost centers to

profit centers (Chesbrough, 2006, p. 25). By being managed as business assets, IP assets are

increasingly traded as economic goods and may also be utilized as financial assets, besides

being applied purely as legal assets inside the firm.

Based on this development, firms may leverage their IP assets financially to a greater

extent and utilize them to access additional external sources of financing (cf. Kamiyama et al.,

2006, p. 20). However, several studies indicate that the key economic role of IP assets in

OECD countries is not reflected in an equally important role in corporate financing (see, e.g.,

KfW, 2006, p. 145; Klawitter and Hombrecher, 2004, p. 1213). I address reasons for this

3

incongruity in the following section (Section 1.1.2), which outlines the difficulties in dealing

with intangible assets financially.

1.1.2 Challenges in leveraging intellectual property financially

Traditional accounting and reporting standards and their application in management decision

processes, financial instruments, and tax regulations are based on tangible assets as value

drivers and measures of economic performance. Measuring and quantifying IP assets in

economic terms is difficult due to their complex asset characteristics. Therefore, traditional

accounting and reporting systems cannot deal with the structural changeover to a knowledge-

based economy and fall short in an adequate coverage of intangibles and their economic

impact (Lev, 2003, p. 1). The systematic academic examination and discussion of intangible

assets and their economic impact only started in the 1980s; scholars only began to alert

managers, investors, and policy-makers since the early 1990s about the structural change and

the increasing impact of intangible asset on corporate value and growth (cf. Lev, 2003, p. 1).

Due to the failure in providing adequate reporting of intangibles, the value assigned to a

company by accountants and the value assigned to it by market participants often differ. This

is frequently seen in merger and acquisition (M&A) transactions with high discrepancies

between the reported balance sheet value and the purchasing price of equity, or in high

discrepancies between balance sheet values and market capitalization. For instance, as of the

end of 2000, Microsoft Corp. had only USD 1.9 billion in property and equipment, although

its market capitalization was about USD 328 billion (Blair and Wallman, 2001, p. 1).

The reporting gap emerges from the fact that most intangibles are not perceived as assets

in a company's financial statement, although intangibles may have already been adding value

to the firm for several years. According to HGB, intangibles can be capitalized only to a very

limited extent, which is based on HGB's principle of prudence and creditor protection,

according to the rule that assets and income will not be overstated and liabilities and charges

will not be understated. Until the recent commencement of BilMoG in 2010, intangibles were

capitalized only if they were bought in return for payment from a third party and self-

developed intangibles were not capitalized at all. As a result, a company's equity ratio might

have dropped although it might have created value. Eventually, financial key figures might

have shown a negative development when in fact the company was investing in intangibles.

With the commencement of BilMoG, the regulations of the HGB to some extent align with

4

the International Accounting Standards (IAS), which – in contrast to the HGB principle of

prudence and creditor protection – are designed to reflect a company's success potential to

investors. Therefore, the development costs of some self-developed intangibles can be put on

the asset side of the balance sheet, under certain restrictions.1 This may close the reporting

gap to a certain extent, but does not constitute a solution for providing adequate reporting

information. With current reporting standards, the failure in providing adequate information

about intangible assets causes a number of essential economic problems (cf. Chan et al., 2001,

p. 2454; Hall, 2003, p. 29; Lev, 2003, p. 2; Hofmann, 2005, p. 3ff); these include:

inappropriate rating and due diligence processes

systematic biases in managerial decisions

systematic biases in investor decisions

excessive cost of capital for intangible intensive investments

abnormally high volatility of stock prices and excessive insider trading gains

The significant impact of these failures has led to calls for additional information from the

investment community and financial institutions, who would "welcome improvements in

disclosures about the identity, source, and life of both purchased and internally generated

intangible assets" as articulated, for example, by the American Institute of Certified Public

Accountants (AICPA, 1994, p. 83). An increasing number and particularly intangible

intensive companies tend to provide supplementary information, such as voluntary

publications and investor relation, albeit on an unsystematic basis and with great

discrepancies between companies, sectors, and countries (Gelb, 2002, p. 457; OECD, 2006,

p. 19; PwC, 2007, p. 46). Considering the design of information, systematic and conceptual

approaches have different origins. Hiroyuki Itami was a pioneer in 1980 with his work on

invisible assets in the management in Japanese corporations. His findings were published in

English in 1987 (Itami, 1987) at the same time as Sveiby and Riesling's (1986) work on

knowledge management and human capital. Also at the same time, Johnson and Kaplan

(1987, p. 2) introduced their work on the inadequacy of the contemporary accounting system,

noting that it "treats many cash outlays as expenses in the period in which they are made even

though these outlays will benefit future periods." Based on the awareness that intangibles

have an important impact on company growth that is not represented by the contemporary

accounting system, Kaplan and Norton (1992) developed the Balanced Scorecard, with the 1 A detailed description of the handling of intangibles, according to HGB, before and after the commencement of the BilMoG as well as their handling according to IAS is provided in Section 3.1.

5

aim of providing performance measures that take these value drivers into account. Related

tools subsequently developed by economists and practitioners are the Intangible Asset

Monitor (Sveiby, 1997), the Skandia Navigator (Edvinsson and Malone, 1997), and the

Technology Broker (Brooking, 1996). In addition, many companies and organizations have

developed their own reporting tools and measures for their own use (Blair and Wallman,

2003, p. 458). However, Blair and Wallman (2003, p. 458) note that some of the measures

being used "to show the linkages among the intangible factors that contribute to the

performance […] have gained a certain prominence and have apparently proved to be useful

management tools in individual companies. None, however, is being used consistently by a

large enough group of firms to provide useful cross-sectional or time-series data, or even

reasonable benchmarks that one company could use to compare its performances with that of

another. So far, at least, the information generated by these efforts is still ad hoc and situation

specific." Similarly, concerning observations of internal reporting practices, Lev (2003, p. 2)

notes that these non-standardized measures are not adequate for resource allocation or

investment decisions. Even though official institutions, academics, and practitioners are

engaged in various efforts such as PRISM2 to address the problem, state-of-the-art intellectual

capital reporting has a number of barriers and shortcomings.3 In short, Lev (2003, p. 2)

concludes that "both managers and investors are at a very early stage of grappling with the

management, valuation, and reporting of intangibles."

The potential to leverage IP assets financially might be a matter of great interest to the

financial community, including private equity firms, investment banks, and commercial

banks. Investors would benefit from more realistic corporate valuations, and creditors would

benefit from more realistic risk assessments and could enhance their average yield per loan as

well as their overall market potential (Hofmann, 2005, p. 4). Moreover, Hofmann (2005,

p. 12) from Deutsche Bank Research notes that "an ever larger number of prospering

companies owe their success precisely to their intangible assets. Lenders unable to extend

credit to such businesses on the basis of these assets are closing the door on large part of the

credit market of the future." Some banks are thus beginning to take certain IP assets such as

patents into account in rating procedures, to deal with patents as major collateral, and to

develop other patent-based financing instruments such as IP securitization (Kamiyama et al.,

2006, p. 20). A number of trade journals have drawn the picture of a rapidly evolving field of

IP finance (e.g., Lucier and Milani, 2005). However, larger banks do not thoroughly analyze 2 PRISM is a project initiated by the European Union (see http://www.euintangibles.net, accessed: 2008/08/04). 3 See, e.g., Guimon (2005, p. 32f) for an overview of specific barriers and shortcomings.

6

IP (Hall, 2003, p. 36; Kamiyama et al., 2006, p. 20); a 2006 German study indicates that the

current volume of IP exploitation in the capital market is negligible (KfW, 2006, p. 146).

As a result, companies with high ratios of intangibles are confronted with serious

disadvantages in their ability to raise external capital. This difficulty applies both at the

company and project levels. A 2006 study shows that about a quarter of exploitable patents in

technology-based companies in Germany are lying idle (IW, 2006, p. 20). Particularly in

smaller companies, these patents are kept on hold, primarily due to the difficulty of attracting

external funds (IW, 2006, p. 23). Typically, young technology-based companies with limited

revenues, tangible assets, and track records are strongly dependent on the ability to leverage

their IP assets financially. Other established companies with valuable IP portfolios may also

benefit from the ability to leverage their IP assets financially. Based on the presumably

marginal contribution of IP assets to access external financial sources and on the high

potential of companies to benefit from leveraging their IP assets financially, I will now

describe the objectives of this thesis in the following section (Section 1.1.3).

1.1.3 Research objectives

Detailed information about the financial utilization of IP assets across technology-intensive

industry sectors and company size clusters does not exist for the German market environment.

The introduction to this thesis points out the significant role of IP assets and the high potential

to leverage them financially in a technology-driven economy, although it is assumed that the

actual utilization of IP assets for financial purposes is limited. Therefore, it is of great

economic concern for both capital seekers and capital providers to understand the economic

factors that determine the financial utilization of IP assets, and to recognize the actual extent

and potential possibilities of this (cf. Aho, 2006, p. 25; KfW, 2006, p. 145).

Due to the broad variety of IP assets, I will concentrate on specific assets. While the focus

of this thesis is described in greater detail in Section 1.2.2, it has to be mentioned here that

this thesis concentrates on patents. Patents are at the forefront of being leveraged financially,

because they are fungible and constitute a large part of a company's technological capital.

Owing to the increasing importance of the topic, there has been much research on patents and

patent management over the past two decades. For a long time, however, the role of patents as

financial assets was disregarded by both academics and by practitioners. Literature about

7

leveraging patents financially is rare, and very few studies examine the financial utilization of

patents in detail. Table 1 presents an overview of identified publications.

An overview of existing literature shows that information about the financial utilization of

patents is fragmented, and that comprehensive studies about the financial impact of patents

are mostly limited to venture capital financing. Besides this, there is rich research on the value

relevance of patent information in the capital market (see, e.g., Griliches et al., 1991; Deng et

al., 1999; Hirschey and Richardson, 2004; Hall et al., 2007). Because the impact of patent

information on the stock market performance of publicly tradable companies is only indirectly

associated with the financial utilization of patents, existing literature is not explicitly referred

to in Table 1. In short, it can be stated that most of the existing empirical findings on the

relationship between corporate financing and IP assets are based on stock market valuation

and venture capital financing. Hence, the financial utilization of patents is limited to a sub-

sample of firms and financing instruments.

Table 1: Existing literature on leveraging patents financially4

Author (year) Subject matter Type of data source (sample)

Company focus

Geographical scope

Czarnitzki and Kraft (2002)

the impact of innovation (in terms of patents, among others) on credit ratings and company value

databases (5,305 observations)

manufact-uring sector

Germany

Hall (2003) intangibles and credit risk analysis banks and rating agencies (14 interviews)

not supplied European Union

Baum and Silverman (2004)

selection criteria (among others, patents) in venture financing

(204 qualitative datasets)

bio-tech start-ups

Canada

Davies (2004) the financial utilization of IP assets companies and intermediaries (301 surveys)

SMEs Great Britain

Bittelmeyer (2007) patents as indicators in the capital market

databases (288 IPOs and 589 CDAX firms)

publicly tradable companies

Germany

Mann and Sager (2007)

the role of patents for venture capital financing

databases (1,089 datasets)

bio-tech and software start-ups

United States

Bittelmeyer et al. (2008)

the utilization of intangible assets as loan security

companies (4,300 surveys)

SMEs Germany

Haeussler et al. (2009)

the role of patents in venture capital financing

companies (280 surveys)

bio-tech companies

Germany, Great Britain

4 Source: own compilation.

8

The aim of this thesis is to provide a comprehensive and detailed analysis of the actual

extent of and influence factors on leveraging patents financially in the case of established

companies across industry sectors, company sizes, and company type clusters, from a

corporate perspective. The objectives of this thesis are:

I. to demonstrate the role of patents as financial assets and to describe prevalent

patent-based financing instruments from a corporate perspective based on literature

findings

II. to derive influence factors for leveraging patents financially from a corporate

perspective based on literature findings and expert interviews

III. to empirically examine the relevance of patent-based financing activities as well as

the significance of identified influence factors across company size clusters and

patent-intensive industry sectors based on an extensive survey

IV. to derive hypotheses about leveraging patents financially from a corporate

perspective based on empirical findings

This study is of a descriptive and explorative nature, due to the matter's emerging status.

This thesis conducts empirical research that prepares the ground for a set of hypotheses. The

results of the study should serve as a foundation for both practitioners and academics, to

enable a more comprehensive financial handling of patents, particularly in technology-driven

economies.

9

1.2 INTRODUCTION OF CENTRAL CONCEPTS AND THESIS FOCUS

Due to the complexity of key concepts in this thesis and the vastness of the research topic,

Section 1.2.1 defines frequently used terms, while Section 1.2.2 describes the focus of this

thesis. Finally, Section 1.2.3 provides an overview of the thesis structure.

1.2.1 Introduction of key concepts and definitions

Key concepts that are frequently used in the thesis are intangible asset, intellectual property,

intellectual property right, patent, and innovation. To avoid inaccuracies and

misinterpretation, I will now define these concepts and describe their use in this thesis.

Tangible and intangible assets comprise all value generating elements in a company

(Smith and Parr, 2000, p. 15). Tangible assets have a physical substance5, while intangibles

are nonmaterial assets that can neither be seen nor touched. There are various definitions of

intangibles. The International Accounting Standards Board (IASB) defines intangibles as

"identifiable non-monetary assets without physical substance held for use in the production or

supply of goods and services, for rental to others, or for administrative purposes."6 Intangibles

can be divided into relational capital (organizational capital, goodwill, and reputation), human

capital (competencies) and intellectual property rights (trademarks, copyrights, and patents)

(Granstrand, 2007, p. 16).

An intangible asset is referred to as intellectual property (IP) when it is legally secured

and enforceable against third parties (Smith and Parr, 2000, p. 27; Lev, 2001, p. 5). As any

other form of property, IP can be bought, sold, licensed, and traded. The term intellectual

property right (IPR) refers to the assignment of the property right through patents, copyrights,

and trademarks, which usually provide an exclusive right over the use of an intellectual asset

for a certain period of time.7 A property right is a social construct and must be distinguished

5 Tangible assets are generally categorized into physical capital (plant, equipment, machinery, etc.) and financial

capital (money, securities, etc.) (Granstrand, 2007, p. 16). 6 Source: http://www.iasplus.com/standard/ias38.htm, accessed: 2008/08/04. 7 Source: http://www.wto.org/english/tratop_e/trips_e/intel1_e.htm, accessed: 2010/05/08;

http://www.oecd.org/dataoecd/8/61/2376087.pdf, accessed: 2010/05/08.

10

from the underlying intellectual asset in the sense that the property right is transferable and

can be dealt with as an economic good in itself (Granstrand, 1999, p. 18).

The thesis focuses on patents.8 Patents are defined by the United States Patent and

Trademark Office (USPTO) as "the grant of a property right to the inventor […] to exclude

others from making, using, offering for sale, or selling the invention."9 It must be noted that a

patent is a negative right, i.e. a patent does not grant the right to make, use, offer, or sell an

invention, but it grants the right to exclude others from doing so.10 To be granted, a patent

application must fulfill three criteria: it must be new, involve an inventive step, and be

capable of industrial application (§§ 1 - 5 PatG). The patent application must describe the

invention in a detailed enough way to enable others to use it. The patent application is

published by the Patent Office. Patents are only valid in the country that granted them. The

general term of a patent is 20 years from the date on which the application was filed (the

priority date), provided that the maintenance fees for the patent are paid (§§ 16, 17, 20 PatG).

If, during this time, the patent is commercially exploited by others without authorization, the

patent holder may go to court and sue the infringer. The court may then stop the infringer

from using it through an injunction and the court may also claim against the infringer for

damages. Therefore, the value of a patent right is essentially based on its use as a means for

litigation (Granstrand, 2007, p. 161). The term patent is usually used in a broad sense,

including the right to commercialize the invention in the form of the legal document itself as

well as the invention and the know-how needed to apply and commercialize it. To draw a

clear distinction between concepts, I will refer to patents in this thesis as pure legal

documents, unless otherwise stated.

Other closely related terms frequently associated with patents and (new) technologies are

the terms invention and innovation. While invention basically refers to novel ideas of

technologies in a rudimentary form (e.g., sketches or prototypes), it does not imply a

successful application, whereas innovations imply that an invention has successfully been

transformed into marketable technologies or products (Granstrand, 1999, p. 58; Verburg et al.,

2006, p. 139). Innovations may be patented, or not.

8 With patents, I refer to both patent applications and granted patents. Distinctions will be used where necessary. 9 Source: http://www.uspto.gov/patents/resources/general_info_concerning_patents.jsp#heading-2, accessed:

10/06/04. 10 The distinction between an entitlement and a negative right can be explained by patents for drugs, which do

not automatically entitle the holder to sell it as a medicine unless national health authorities have also authorized this, independently from the question as to whether or not the drug is patented (Granstrand, 2007, p. 159).

11

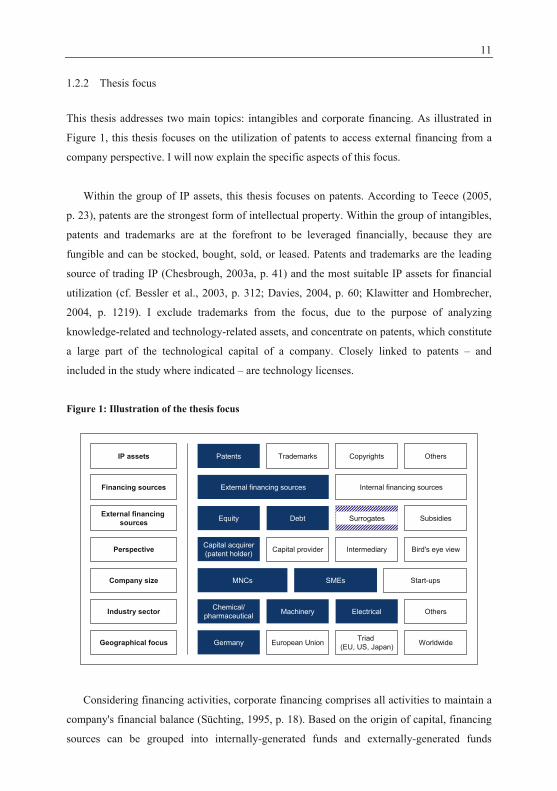

1.2.2 Thesis focus

This thesis addresses two main topics: intangibles and corporate financing. As illustrated in

Figure 1, this thesis focuses on the utilization of patents to access external financing from a

company perspective. I will now explain the specific aspects of this focus.

Within the group of IP assets, this thesis focuses on patents. According to Teece (2005,

p. 23), patents are the strongest form of intellectual property. Within the group of intangibles,

patents and trademarks are at the forefront to be leveraged financially, because they are

fungible and can be stocked, bought, sold, or leased. Patents and trademarks are the leading

source of trading IP (Chesbrough, 2003a, p. 41) and the most suitable IP assets for financial

utilization (cf. Bessler et al., 2003, p. 312; Davies, 2004, p. 60; Klawitter and Hombrecher,

2004, p. 1219). I exclude trademarks from the focus, due to the purpose of analyzing

knowledge-related and technology-related assets, and concentrate on patents, which constitute

a large part of the technological capital of a company. Closely linked to patents – and

included in the study where indicated – are technology licenses.

Figure 1: Illustration of the thesis focus

Company size

Industry sector

Financing sources

IP assets

Geographical focus

Patents

Internal financing sources

Start-ups

Trademarks Copyrights Others

External financing sources

External financing sources

SMEsMNCs

Chemical/pharmaceutical Machinery Electrical Others

Germany European Union Triad (EU, US, Japan) Worldwide

Equity Debt SubsidiesSurrogates

Perspective Capital acquirer(patent holder) Capital provider Intermediary Bird's eye view

Considering financing activities, corporate financing comprises all activities to maintain a

company's financial balance (Süchting, 1995, p. 18). Based on the origin of capital, financing

sources can be grouped into internally-generated funds and externally-generated funds

12

(Süchting, 1995, p. 22; Wöhe, 2002, p. 27). Internal funds may be generated, for example,

through the creation of capital (retained earnings) or by the redeployment of capital (through

depreciation, rationalization, and other instruments) (Süchting, 1995, p. 22f ; Wöhe, 2002,

p. 13ff). Concerning leveraging IP assets financially, internal financial sources are the

commercialization of IP assets and the optimization of IP portfolios to cut the expenses for IP

activities. Both aspects have been the topic of numerous studies in recent years (see, e.g.,

Lichtenthaler, 2006, p. 40ff). This thesis does not seek to contribute to the large body of

research on external patent commercialization, but to specifically examine the utilization of

patents within external financing instruments. The external exploitation of patents to generate

additional revenues is only partially included in this thesis in order to analyze the distinction

and preferences of companies in the financial utilization of patents. First and foremost, the

objective of this thesis is to analyze the utilization of patents in external financing

instruments, i.e. the acquisition of capital from sources outside the company by means of

patents. In contrast to internally-generated funds, these instruments are characterized by an

inflow of capital at the start of financing activity, which involves the payback of the capital at

a later stage (Schneider, 1990, p. 1986). External financing instruments can basically be

categorized into equity financing and debt financing (Süchting, 1995, p. 22), both of which I

examine in detail. Furthermore, I examine the role of patents as financial assets in the

surrogate instrument sale/lease-back transaction. The classification of sale/lease-back is not

consistent in the financing literature. Because leasing has elements of loan agreements and

can be considered as a sub-form of debt financing (Wöhe, 2002, p. 15; Zantow, 2008, p. 315),

sale/lease-back transactions may equally be categorized as a sub-form of debt financing. I also

examine how patents can be leveraged in patent funds. Patent funds are a relatively new

model that cannot be classified within the scheme of financing instruments in Figure 1.

Nevertheless, for patent holders, the utilization of patents in patent funds is one way to

acquire external capital, which is aligned with the context of this thesis.

An important distinction from certain other studies is that this thesis does not concentrate

on how patents can be used to finance innovation projects, i.e. how development activities

based on certain proprietary rights can be financed with the help of these assets. Instead, this

thesis examines if and how existing and valuable patent portfolios of established companies

are leveraged financially. I also decided not to examine financing instruments relevant only

for specific companies. I do not examine the role of patents in accessing subsidies and

exclude financing instruments of large corporations that are not available to smaller

13

companies, due to a lack of financial volume, such as the issuing of securities in the capital

market (cf. Gräfer et al., 1998, p. 202; Zantow, 2008, p. 138). I also exclude financially

engineered products traded in capital markets, such as asset-backed instruments.

This thesis is designed to generate an understanding of how patents can be leveraged

financially across company size classes and industry clusters. Nevertheless, certain limitations

are also drawn concerning industries and company size. Considering industry sectors, I

concentrate on patent-intensive sectors. Arundel and Kabla (1998, p. 133f) analyzed the

patenting rate in different industry sectors. They found that the most patent-intensive

industries are the pharmaceutical industry, with a patenting rate of 74% of innovations, and

the chemical industry, with 57%. Companies in the machinery industry (and closely related

industries such as fabricated metal products) show patenting rates in the range of 38% to 52%;

companies in the electrical industry (and closely related sectors such as office and computing

equipment or precision instruments) show similar patenting rates between 43% and 56%. In

other industries, they found rather low patenting rates, for instance, in the basic metals

industry (14%) or the textile industry (a mere 8%). I focus on patent-intensive industries,

namely the chemical, pharmaceutical, machinery, and electrical industries, including closely

related sectors. Section 6.1 provides a systematic differentiation and a detailed description of

examined industry classes. Concerning company size clusters, this thesis includes all

company types, rather than concentrating on particularities of specific size clusters, such as

the role of patents for start-ups and venture capital financing. This thesis analyzes the

financial utilization of patents by all types of companies with valuable patent portfolios.

I also seek to avoid systematic distortions and noise from differing legal and economic

factors, which may influence financial and patent management behavior. To eliminate the

influence and noise of differing country-specific factors as far as possible, the study focuses

on firms within one country (cf. Ernst, 2001, p. 148). This thesis concentrates on the German

business environment, concerning the importance of IP with relatively high and lasting patent

application numbers compared to other countries. In 2009, with 25,107 or about 18% of all

patent applications worldwide, Germany ranked second behind the US (32,966), with Japan

third (19,933) (EPO, 2010, p.52f). The German business and legal environment is at the

center of investigation and is referred to throughout, unless otherwise stated. Nevertheless,

Germany's legal environment is integrated into the European Union (EU), and the German

business environment is strongly influenced by internationalized companies and foreign trade

14

regulations. Patent applications by German companies often extend German borders. Data and

information from other geographical regions will therefore be used, where indicated. This will

comprise primarily the so-called triad of the EU, the US, and Japan.

Finally, I must mention that IP and financing are both complex areas that involve a broad

range of academic disciplines, including engineering expertise, legal matters, macroeconomic

theories, tax matters as well as the broad field of policies and regulations. These are

considered along general lines within this thesis, but need to be examined in greater detail by

experts in the various fields.

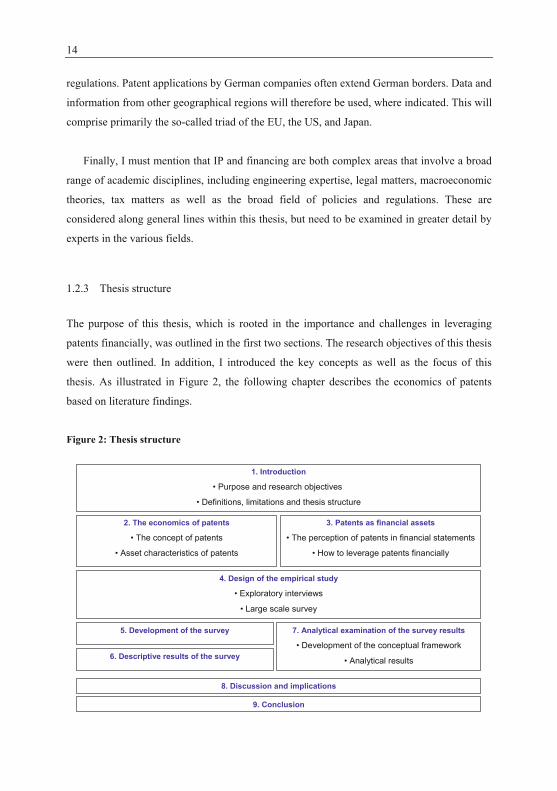

1.2.3 Thesis structure

The purpose of this thesis, which is rooted in the importance and challenges in leveraging

patents financially, was outlined in the first two sections. The research objectives of this thesis

were then outlined. In addition, I introduced the key concepts as well as the focus of this

thesis. As illustrated in Figure 2, the following chapter describes the economics of patents

based on literature findings.

Figure 2: Thesis structure

2. The economics of patents

• The concept of patents

• Asset characteristics of patents

1. Introduction

• Purpose and research objectives

• Definitions, limitations and thesis structure

4. Design of the empirical study

• Exploratory interviews

• Large scale survey

8. Discussion and implications

3. Patents as financial assets

• The perception of patents in financial statements

• How to leverage patents financially

7. Analytical examination of the survey results

• Development of the conceptual framework

• Analytical results

5. Development of the survey

6. Descriptive results of the survey

9. Conclusion

15

Chapter 2 provides an understanding of patents as economic assets and to distinguish

important characteristics of patents concerning financial utilization. Chapter 3 explicitly

describes patents as financial assets. First, I summarize the perception of patents as assets in

financial statements according to German reporting standards; then I clarify in Chapter 3

different roles of patents in different external financing instruments. The empirical study in

Chapter 4 is designed to explore the actual financial utilization of patents and factors that

influence the financial utilization of patents from a company perspective. The statistical

methods used for the empirical study are also introduced at this point. In Chapter 5, the first

step of the empirical study is the generation of the questionnaire for the large-scale survey

based on the literature findings and exploratory interviews with experts and company

representatives. The results of the large-scale survey are described in Section 6 with basic

statistical measures. These comprise a description of the data sample, new indications about

asset characteristics of patents, the actual financial utilization of patents by patent-intensive

companies, and factors that influence these companies in the financial utilization of patents.

Because there is little insight from prior studies about the financial utilization of patents in

patent-intensive industries in Germany, the descriptive results serve as a starting point to

design the analytical examination of the survey results. Chapter 7 develops the analytical

framework to examine the factors that influence the financial utilization of patents and

operationalize these factors for the analytical examination. I then present the results of the

analytical examination. Both the descriptive survey results and the analytical examination of

the empirical study are discussed in Chapter 8 concerning the research objectives. In addition,

implications are provided in this chapter for managers and policy-makers. Chapter 9 draws a

conclusion and provides an outlook for potential future research on leveraging patents

financially.

2 THE ECONOMICS OF PATENTS

"Many commentators believe that intellectual property, especially patents, will represent the

most significant wealth of the next century" (Ely, 1992, p. 6).

2.1 THE CONCEPT OF PATENTS AND PATENTING TRENDS

I will now discuss the concept of patents (Section 2.1.1) at the macro-economic level and will

provide a description of EPO statistics in the subsequent section (Section 2.1.2) to highlight

the development of patenting activities by market actors.

2.1.1 The concept of patents

The intellectual property rights system enables private ownership of intellectual capital

(Granstrand, 2007, p. 19). The concept of a patent system stimulates innovations by providing

a temporary monopoly for the inventor and, at the same time, by facilitating R&D on new

processes or products by publishing and disseminating detailed technical information about

the invention in the form of the patent itself that might otherwise remain secret (Griliches,

1990, p. 1663). The concept of patents, which stimulates innovations by granting a temporary

monopoly right, is based on specific characteristics of IP assets that otherwise barely allow for

profitable revenues on investments in IP assets. In general, IP assets are irreversibly produced

and transferred as well as reusable and reproducible at no or low cost. Therefore, the value

creation of IP assets is usually characterized by large initial investments with small variable

costs in application (Granstrand, 2007, p. 154). Teece (2005, p. 22) notes that "[…]

knowledge has aspects of what economists refer to as a public good – when consumption by

one individual does not reduce the amount left for another. This is especially true for

scientific knowledge. […] However, the distinction erodes quickly as one move towards

industrial knowledge and away from scientific knowledge. While multiple uses need not take

away from knowledge – indeed it may well be augmented – the economic value may well

decline with simultaneous use by multiple entities. […] Imitators can dramatically lower the

market value of knowledge by augmenting its supply in the market." Therefore, the objective

of patent systems is to sustain the economic value of technological knowledge and to enable

companies to refund investments in innovations, producing a high risk-reward ratio by

temporarily granting a monopoly right.

D. de. Vries, Leveraging Patents Financially, DOI 10.1007/978-3-8349-6903-3_2, © Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2011

17

If the patent protection model is considered for a single, isolated invention, the concept

seems convincing. Mansfield (1986, p. 173) notes, in this context, that "the patent system is at

the heart of our nation’s policies toward technological innovation." However, the patent

system is both complex and controversial (see Andersen and Konzelmann, 2008, p. 13).11

Several studies suggest that patent systems are an ineffective tool to encourage innovative

activities and may even impose disincentives (see, e.g., Bessen and Meurer, 2008, p. 26).

Hence, intellectual property rights may – in contrast to their conceptual motivation – even

hamper technological progress. This critique is primarily grounded on the following three

aspects:

technological factors

market participants' behavior

institutional inadequacy

Considering technological factors, monopoly rights may hamper innovative

developments, mostly in so-called "complex product industries", i.e. technological fields that

are complex and where technological developments are cumulative and interactive processes

with many cross-links (Hunt, 1999, p. 17f; Levin et al., 1987, p. 7). Especially high-

technological fields are characterized by interdisciplinary R&D processes and typically

interact with each other in complex and interdependent ways. At the same time, more generic

technologies12 emerge, i.e. more multiproduct technologies are developed (Granstrand, 1999,

p. 334). In addition, sources of new technologies and the number of cross-links within the

patent landscape increase with an increasing number of corporations investing in

internationalized R&D activities. As a result, new businesses become more reliant on an

increasing number of patents (Granstrand, 1999, p. 334). Companies are confronted with an

IP assembly problem by being required to develop not only their own IP assets, but also to

gather an increasing number of licenses from others so as to be able to commercialize new

products and services. As Shapiro (2001, p. 120) notes, "our patent system is in fact creating a

patent thicket, a dense web of overlapping intellectual property rights that a company must

hack its way through in order to actually commercialize new technologies." Considering

11 There are alternative concepts to patent systems in practice, which have been analyzed to some extent. For

instance, Wright (1983, p. 691ff) analyzes the choice between patents, prize, and direct contracting for research services, while Mansfield (1985, p. 97ff) conducted an empirical analysis of R&D tax credits and allowances in Canada to increase company-financed R&D activities.

12 Technologies are generic when a cascade of successive technologies emerges from them (Granstrand, 2007, p. 284).

18

market participants' behavior, the increasing importance and value of IP assets and the general

shift towards "intellectual capitalism" (see Section 1.1.1) leads to an increasing number of

market participants who intensify the use of the patent system as a competitive business tool.

Large corporations progressively develop patent portfolios to strengthen their bargaining and

retaliation power or to exercise patent strategies to delude competitors (Granstrand, 1999,

p. 335). Consequently, asymmetries in bargaining power between new and old firms, small

and large firms, and between industrial sectors are likely to increase (Granstrand, 1999,

p. 335), and patent management skills are likely to evolve into a competitive factor. At the

same time, opportunities to exploit patent values as well as to abuse the patent system arise.

With increasing opportunities to exploit patent values, new patent-based business models

evolve. On the one hand, these business models create value by means of a more effective and

more efficient application and exploitation of patents. On the other hand, new exploitation-

based business models might have destructive effects. Particularly, the litigation-based

business models of so-called patent trolls raise concerns.13 Another concern arises from

institutional inadequacies. According to Granstrand (1999, p. 334), "the changing character of

technology creates misfits between technology and the legal framework designed to foster it.

It is an inherent tendency that changes in legislation lag behind changes in technology."

Contemporary technology such as, for example, software and biotechnology are developing

swiftly and challenge patent systems concerning the protection of IP assets (Granstrand, 1999,

p. 334).

In short, with cumulative innovations and an increasing number of cross-links between IP

assets and actors in technological fields, the patent system may have the effect of slowing

down and hampering innovation and diffusion, and its workings may be too slow to be able to

protect the IP assets of fast-developing high-technology fields (Granstrand, 1999, p. 334;

Shapiro, 2001, p. 120), although patent systems are designed to stimulate investments in

innovation activities and constitute an essential instrument for companies to develop new

products and to bring them successfully to market.

13 Patent trolls are usually small and specialized firms with legal and technological expertise, and concentrate on

patent extortions.

19

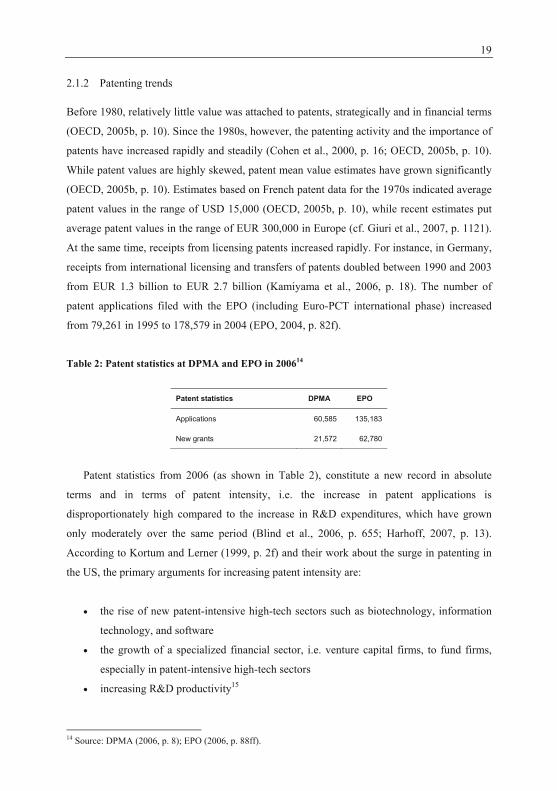

2.1.2 Patenting trends Before 1980, relatively little value was attached to patents, strategically and in financial terms

(OECD, 2005b, p. 10). Since the 1980s, however, the patenting activity and the importance of

patents have increased rapidly and steadily (Cohen et al., 2000, p. 16; OECD, 2005b, p. 10).

While patent values are highly skewed, patent mean value estimates have grown significantly

(OECD, 2005b, p. 10). Estimates based on French patent data for the 1970s indicated average

patent values in the range of USD 15,000 (OECD, 2005b, p. 10), while recent estimates put

average patent values in the range of EUR 300,000 in Europe (cf. Giuri et al., 2007, p. 1121).

At the same time, receipts from licensing patents increased rapidly. For instance, in Germany,

receipts from international licensing and transfers of patents doubled between 1990 and 2003

from EUR 1.3 billion to EUR 2.7 billion (Kamiyama et al., 2006, p. 18). The number of

patent applications filed with the EPO (including Euro-PCT international phase) increased

from 79,261 in 1995 to 178,579 in 2004 (EPO, 2004, p. 82f).

Table 2: Patent statistics at DPMA and EPO in 200614

Patent statistics DPMA EPO

Applications 60,585 135,183

New grants 21,572 62,780

Patent statistics from 2006 (as shown in Table 2), constitute a new record in absolute

terms and in terms of patent intensity, i.e. the increase in patent applications is

disproportionately high compared to the increase in R&D expenditures, which have grown

only moderately over the same period (Blind et al., 2006, p. 655; Harhoff, 2007, p. 13).

According to Kortum and Lerner (1999, p. 2f) and their work about the surge in patenting in

the US, the primary arguments for increasing patent intensity are:

the rise of new patent-intensive high-tech sectors such as biotechnology, information

technology, and software

the growth of a specialized financial sector, i.e. venture capital firms, to fund firms,

especially in patent-intensive high-tech sectors

increasing R&D productivity15

14 Source: DPMA (2006, p. 8); EPO (2006, p. 88ff).

20

a shift in R&D management towards more applied activities and thereby towards more

patentable R&D outputs

changes in the regulatory and administrative environment towards stronger patent

protection

According to Blind et al. (2006, p. 655), more complex and comprehensive patent

strategies may also have increased the patent intensity. Results of empirical studies do not

provide a clear picture of the significance of the factors underlying the surge in patenting

(Blind et al., 2006, p. 655). Various studies referring to researchers and practitioners show

that a general trend can be observed, from a rather passive and defensive (i.e. protection-

oriented) patent management towards more active and offensive (i.e. exploitation-oriented)

patent management activities. For instance, an OECD publication (Kamiyama et al., 2006,

p. 7) summarizes that a tendency can be observed, from patent applications that secure the

freedom to operate and set barriers to entry towards activities, to patent applications that

generate additional revenues and use patents as a leveraging point in negotiations as part of

business management and strategy. Eventually, this trend may have a self-enhancing effect,

because IP managers are confronted with an increasing patent management intensity within

their competitive environments, which also forces them to intensify their own activities (Blind

et al., 2006, p. 658).16 This indicates how independent patenting dynamics have become over

time and how the strategic dimension of patent management activities is increasingly

detached from R&D management in the narrow sense (Blind et al., 2006, p. 658). To

understand the overall trend of the increasing economic importance and value of patents, the

next section (Section 2.2) examines patents as economic assets in greater detail.

2.2 ASSET CHARACTERISTICS OF PATENTS

To understand patents as economic assets, the following section (Section 2.2.1) examines why

companies patent or not. Subsequently, Section 2.2.2 explains in detail how patents may add

value to a company. As illustrated in Figure 3, the company-internal belongings are relevant

not merely to understand the asset characteristics of patents. To understand the economic

15 For this argument, the authors refer to Arora and Gambardella (2008, p. 364) who argue that increasing R&D