Embed Size (px)

DESCRIPTION

lg ratio

Citation preview

Financial Accounting

LG ElectronicsXZZV11D

Table Of Content

1

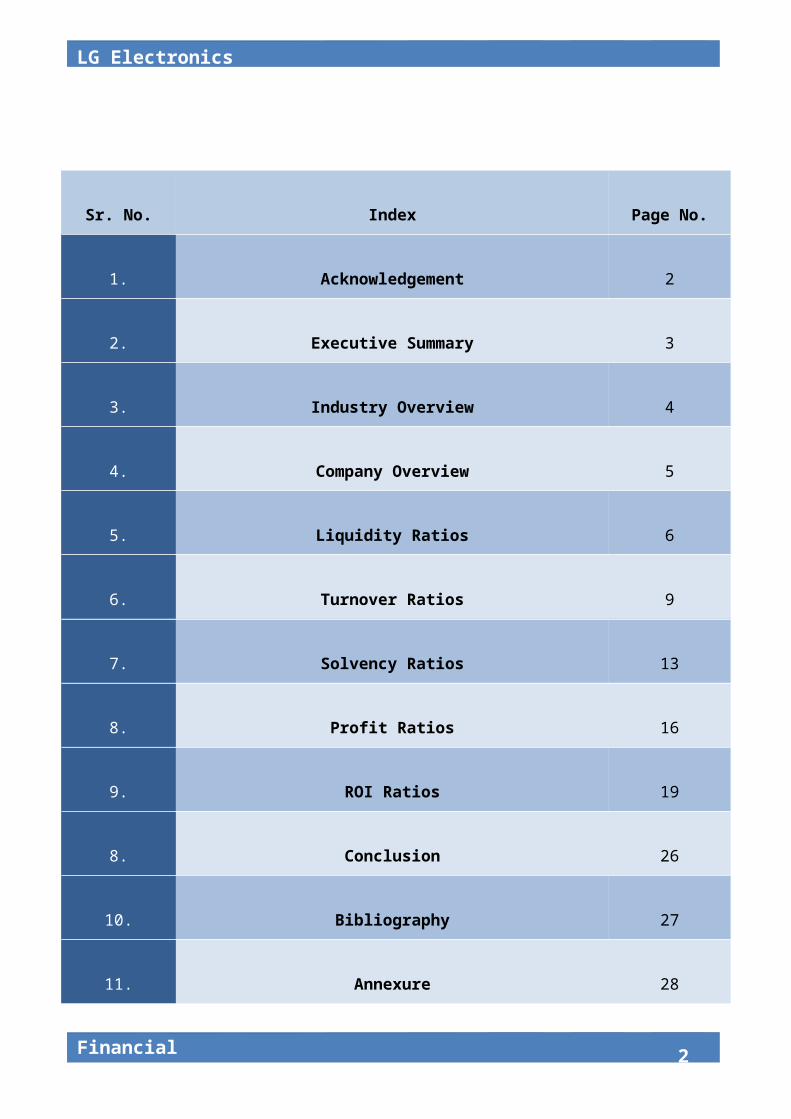

Sr. No. Index Page No.

1. Acknowledgement 2

2. Executive Summary 3

3. Industry Overview 4

4. Company Overview 5

5. Liquidity Ratios 6

6. Turnover Ratios 9

7. Solvency Ratios 13

8. Profit Ratios 16

9. ROI Ratios 19

8. Conclusion 26

10. Bibliography 27

11. Annexure 28

LG Electronics

Financial Accounting

Acknowledgement

I take this opportunity to express my profound gratitude and deep regards to my guide

Mrs.Meghna Dangi for her exemplary guidance, monitoring and constant encouragement

throughout the project.

I am obliged to my batch mates for the valuable information provided by them in their respective

fields. I am grateful for their cooperation during the period of my assignment.

2

Financial Accounting

LG ElectronicsXZZV33D

Executive Summary

LG Electronics’ brand recognition in the global consumer electronics market has increased

exponentially in the past two years. The company successfully achieved “Global Top 3” status in

almost every business area in the first quarter of this year. Much of this success can be attributed to

LG Electronics’ commitment to drive “Innovation” and “Globalization”.

LG Electronics is re-inventing its global procurement organization from highly decentralized to

center-led, establishing streamline procurement leadership across five business units (companies)

and eight regions. LGE’s procurement is currently comprised of 2,200 staff who are part of an

84,000-strong workforce in 115 operations globally, managing US$26 billion direct spend and

US$10 billion general spend, led by Tom Linton, Executive Vice President and Chief Procurement

Officer. The profitability of LG Electronics is heavily dependent on procurement’s performance

and efficiency since its spend represents 80 percent of revenues. LG Electronics procurement is re-

positioning the organization to a new level while maintaining its focus on high quality

manufacturing and becoming a global top brand.

3

LG Electronics

Financial Accounting

Industry Overview

The consumer electronics market is ever evolving with new products being made available on a

frequent basis. Also, the evolution of existing products serves to re-invent what is an already fully

functional product and gives the consumer the feeling that new technology is the new norm. For

example, televisions are entering a new era with the unveiling of the new ‘curved’ television

which gives the viewer a more ‘immersive experience’. This may re-invigorate what may be

considered a stagnating segment within the consumer electronics market and lead to an increase in

revenues.

Another interesting development within the market is the re-introduction of game consoles in

China. In 2000, the Chinese government placed a ban on the sale of foreign game consoles due to

their perception on the effect they have on the mental health of young people. The ban was finally

lifted in 2014, which means that retailers have the opportunity to enter a market, which was not

previously an option and will also have an overall positive effect on the consumer electronics

market as a whole.

Online retailing is also a major trend, which is becoming more prevalent within the industry.

Consumer electronics were traditionally purchased within electrical retailer showrooms so that the

consumer would have the opportunity to try the product before purchase. However, some retailers

have struggled to ‘close the deal’ with sites such as Amazon being able to offer the same product

at a significantly lower price. In recent years, traditional retailers have struggled with this threat of

competition and have led to them placing higher importance on their own online arm.

The global consumer electronics market had total revenues of $253.9bn in 2013, representing a

compound annual growth rate (CAGR) of 0.8% between 2009 and 2013.The Eastern European

markets showed particularly strong growth with CAGRs of 8.5% in comparison to Western

Europe which showed strong decline with compound annual rates of change (CARCs) of -7.8%

over the same period. The United States had the largest consumer electronic retail market in the

world with revenues of $90.5bn in 2013.

4

Financial Accounting

LG ElectronicsXZZV55D

Company Overview

LG is the brand that is Delightfully Smart. "Life's Good" slogan, and futuristic logo are a great

representation of what LG stand for.

Global, Tomorrow, Energy, Humanity and Technology are the pillars that this corporation is

founded on; with the capital letters L and G positioned inside a circle to center our ideals above all

else, humanity. The symbol mark stands for our resolve to establish a lasting relationship with, and

to achieve the highest satisfaction for our customers.

The letters "L" and "G" in a circle symbolize the world, future, youth, humanity, and technology.

Our philosophy is based on Humanity. Also, it represents LG's efforts to keep close relationships

with our customers around the world. The symbol mark consists of two elements: the LG logo in

LG Grey and the stylized image of a human face in the unique LG Red color. Red, the main color,

represents our friendliness, and also gives a strong impression of LG's commitment to deliver the

best. Therefore, the shape or the color of this symbol mark must never be changed.

LG logo is the fundamental visual expression used to identify LG. It expresses the quality and

sophistication that is the hallmark of our products. It is simple, modern and distinctive. Consistent

and proper usage of the logo is absolutely essential. The logo is symbolic of our steadfast

reputation for excellence; therefore, any variation of the logo diminishes the visual identity of LG

Electronics and its products.

LG have two versions of our logo: Corporate Logo and 3D Logo.

The updated 3D Logo retains the heritage and equity of the Corporate Logo, while aligning with

our new positioning. It was redrawn to strengthen the visual impact of our symbol mark and help

communicate our attributes.

5

LG Electronics

Financial Accounting

Ratio Analysis

Liquidity Ratios:

It is the ratio that measures a company’s ability to fulfill its short-term debt obligations or the

ability of a company to pay off its short-term liability, if and when they take a fall.

In case of Liquidity Ration, higher the ratio, higher is the margin of safety to pay off its current

liabilities and other short-term borrowings. Liquidity ration greater than 1, signposts its sound

financial health.

The liquidity ratios are an outcome of dividing cash and other liquid assets (current assets) by the

short-term borrowings (current liabilities). They show the number of times the short-term debt

obligations are covered by the cash and liquid assets. If the value is superior to 1, it means the

short-term obligations are abundantly covered.

The most common Liquidity Ratios are Current Ratio and Acid Test Ratio/Quick Ratio. Short-

term creditors, bankers, government agencies, Bankruptcy analysts and mortgage originators are

readily using the aforementioned ratios. Using these ratios they analyze and forecast the financial

wellbeing of a company and determine their stand accordingly.

6

Financial Accounting

LG ElectronicsXZZV77D

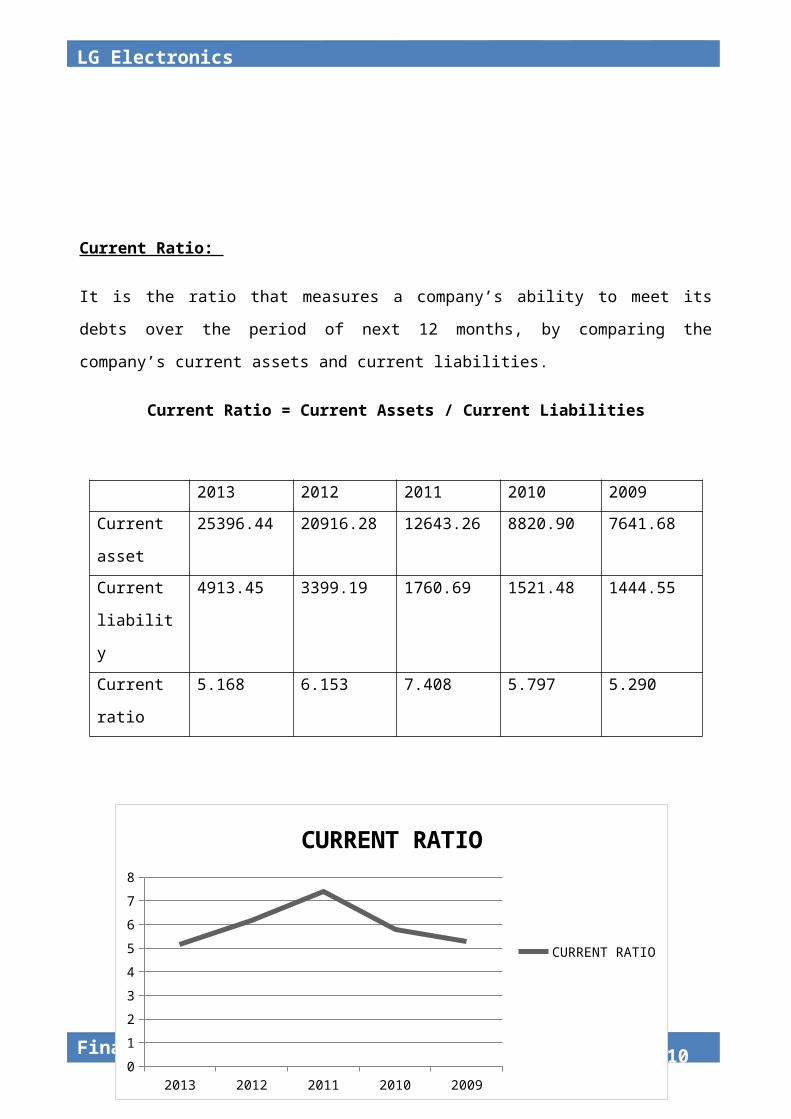

Current Ratio:

It is the ratio that measures a company’s ability to meet its debts over the period of next 12

months, by comparing the company’s current assets and current liabilities.

Current Ratio = Current Assets / Current Liabilities

2013 2012 2011 2010 2009

Current asset 25396.44 20916.28 12643.26 8820.90 7641.68

Current

liability

4913.45 3399.19 1760.69 1521.48 1444.55

Current ratio 5.168 6.153 7.408 5.797 5.290

Interpretation:

The current ratio shows the company’s ability to pay back its short term liabilities with is available

assets. Higher the ratio better is the safety level and payback condition of the company. The above

7

2013 2012 2011 2010 20090

1

2

3

4

5

6

7

8

CURRENT RATIO

CURRENT RATIO

LG Electronics

Financial Accounting

ratios show the gradual increase but after 2011 it decreases which is not a good sign and show that

the company’s capability has decreased. It is a negative sign.

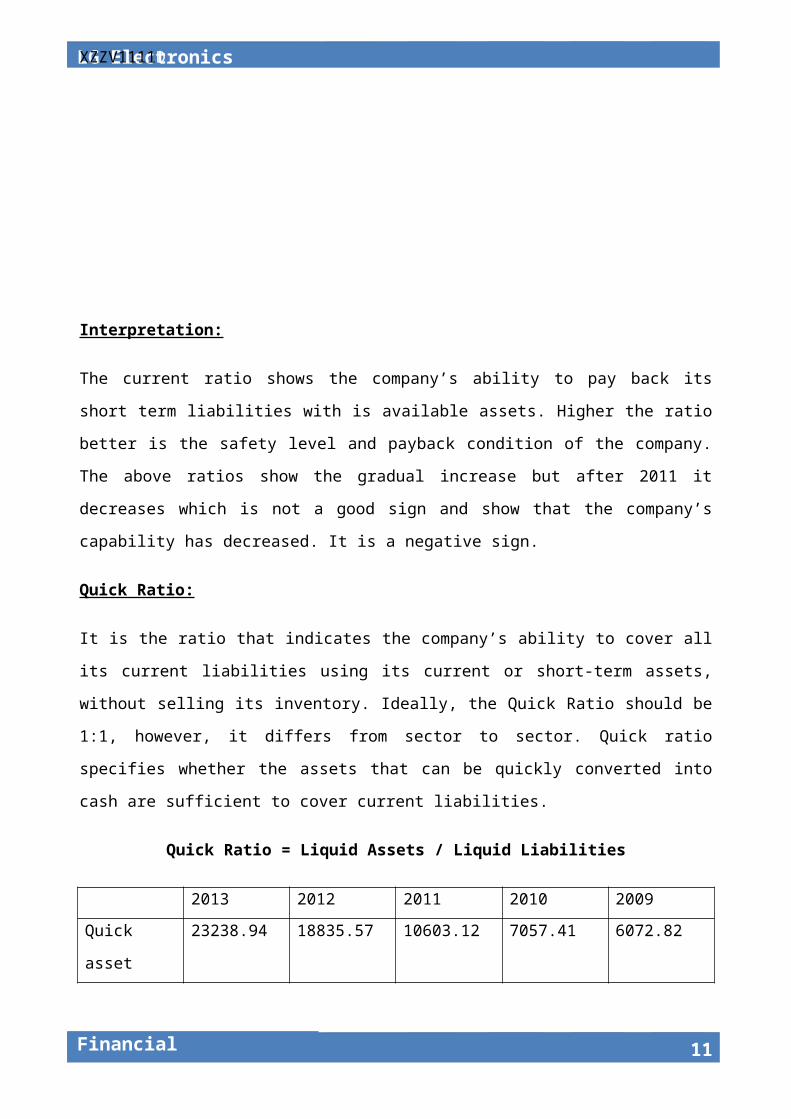

Quick Ratio:

It is the ratio that indicates the company’s ability to cover all its current liabilities using its current

or short-term assets, without selling its inventory. Ideally, the Quick Ratio should be 1:1, however,

it differs from sector to sector. Quick ratio specifies whether the assets that can be quickly

converted into cash are sufficient to cover current liabilities.

Quick Ratio = Liquid Assets / Liquid Liabilities

2013 2012 2011 2010 2009

Quick asset 23238.94 18835.57 10603.12 7057.41 6072.82

Current

liabilities

4913.45 3399.19 1760.69 1521.48 1444.55

Quick ratio 4.729 5.541 6.022 4.638 4.203

Interpretation:

2013 2012 2011 2010 20090

1

2

3

4

5

6

7

QUICK RATIO

QUICK RATIO

8

Financial Accounting

LG ElectronicsXZZV99D

Quick ratio is of more impact than current ratio, as inventory may not be immediately converted

into cash. The decreasing quick ratio is not good for the company. If the liquid ratio is very less

than the current ratio than it means that the current asset are highly dependent on the inventory.

Turnover Ratios:

Turnover ratios are also acknowledged as activity or efficiency ratios. It often refers to the

company’s ability to translate different accounts within their balance sheets into cash or sales.

Companies will normally try to turn their manufacture into cash or sales as fast as possible because

this will, in general, lead to greater revenues. Such ratios are frequently used when performing

fundamental analysis of the company.

There are various types of Turnover Ratios, namely: -

o Inventory turnover ratio

o Debtors turnover ratio

o Average collection period

o Total assets turnover ratio

o Fixed assets turnover ratio

o Capital employed turnover ratio

9

LG Electronics

Financial Accounting

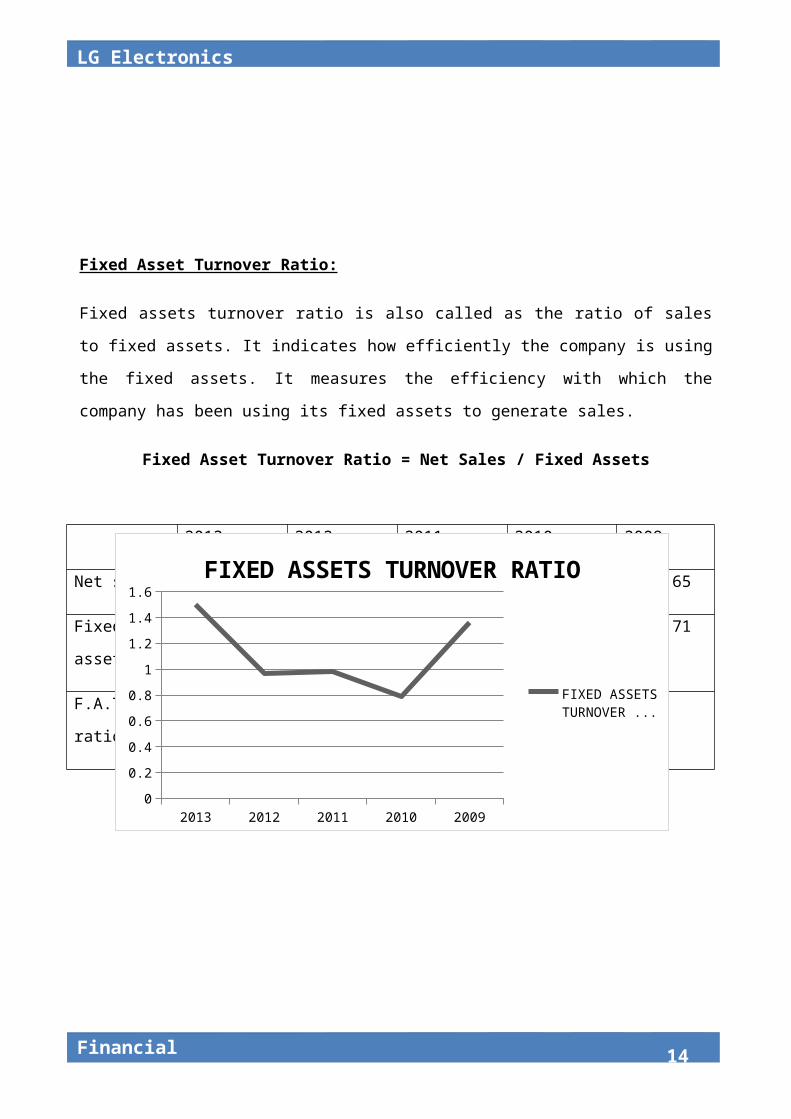

Fixed Asset Turnover Ratio:

Fixed assets turnover ratio is also called as the ratio of sales to fixed assets. It indicates how

efficiently the company is using the fixed assets. It measures the efficiency with which the

company has been using its fixed assets to generate sales.

Fixed Asset Turnover Ratio = Net Sales / Fixed Assets

Interpretation:

2013 2012 2011 2010 20090

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

FIXED ASSETS TURNOVER RATIO

FIXED ASSETS TURNOVER RA...

10

2013 2012 2011 2010 2009

Net sales 18157.28 12650.72 14409.69 9163.04 9753.65

Fixed assets 12095.96 13028.42 14568.28 11533.81 7177.71

F.A.T ratio 1.50 0.97 0.98 0.79 1.36

Financial Accounting

LG ElectronicsXZZV1111D

The higher fixed asset turn over ratio indicates the ability of the firm to achieve maximum sales

with the least investment in shares.as shown above it was high in 2009 fluctuated over the years

but is maximum in 2013.

Working Capital Turnover Ratio:

It is a metric equating the reduction of working capital to generate of sales over a given period.

This provides some useful information as to how effectively a company is using its working

capital to generate sales. A company utilizes its working capital to fund operations and acquire

inventory. These operations and inventory are then converted into sales revenue for the company.

The working capital turnover ratio is used to analyze the relationship between the money used to

fund operations and the sales generated from these operations.

Working Capital turnover Ratio = Net Sales / Working Capital

2013 2012 2011 2010 2009

Net sales 15157.28 12650.72 14409.69 9163.04 9753.65

Working capital 20482.99 17517.09 10936.57 7299.42 6197.13

W.C.T ratio 0.739 0.722 1.317 1.255 1.573

Interpretation:

11

2013 2012 2011 2010 20090

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

WORKING CAPITAL TURNOVER RATIO

WORKING CAPITAL TURNOVER RATIO

LG Electronics

Financial Accounting

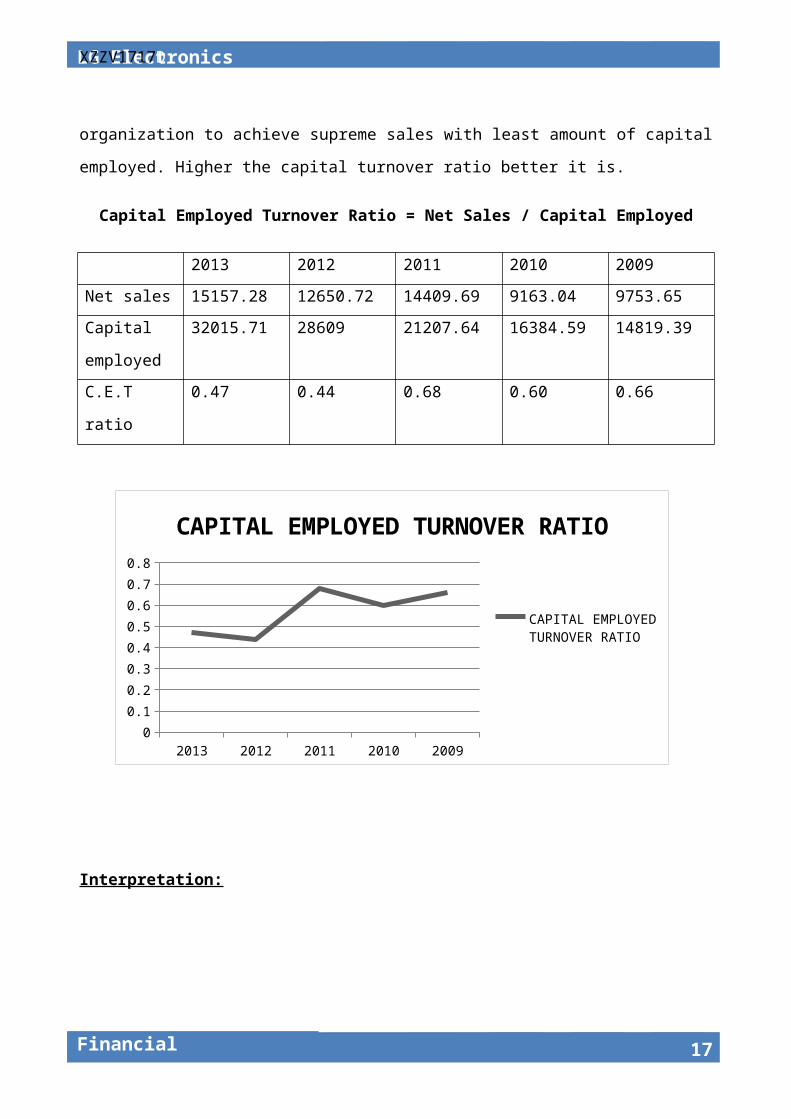

Capital Employed Turnover Ratio:

The capital employed turnover ratio reveals the association between the shareholders' investment

in the business and the turnover that the management has been able to generate from it. A high

capital turnover ratio designates the ability of the organization to achieve supreme sales with least

amount of capital employed. Higher the capital turnover ratio better it is.

Capital Employed Turnover Ratio = Net Sales / Capital Employed

2013 2012 2011 2010 2009

Net sales 15157.28 12650.72 14409.69 9163.04 9753.65

Capital

employed

32015.71 28609 21207.64 16384.59 14819.39

C.E.T ratio 0.47 0.44 0.68 0.60 0.66

Interpretation:

2013 2012 2011 2010 20090

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

CAPITAL EMPLOYED TURNOVER RATIO

CAPITAL EMPLOYED TURNOVER RATIO

12

Financial Accounting

LG ElectronicsXZZV1313D

Solvency Ratios

They measure the capacity of a company to compensate its long-term debt and the interest on it.

Solvency ratios help the business owner conclude the chances of the firm's long-term survival.

These ratios are of interest to long-term creditors and shareholders. These groups are concerned

with the long-term health and survival of business firms. Solvency ratios have to attest that

business can service their debt or pay the interest on their debt as well as pay the principal when

the debt matures.

13

LG Electronics

Financial Accounting

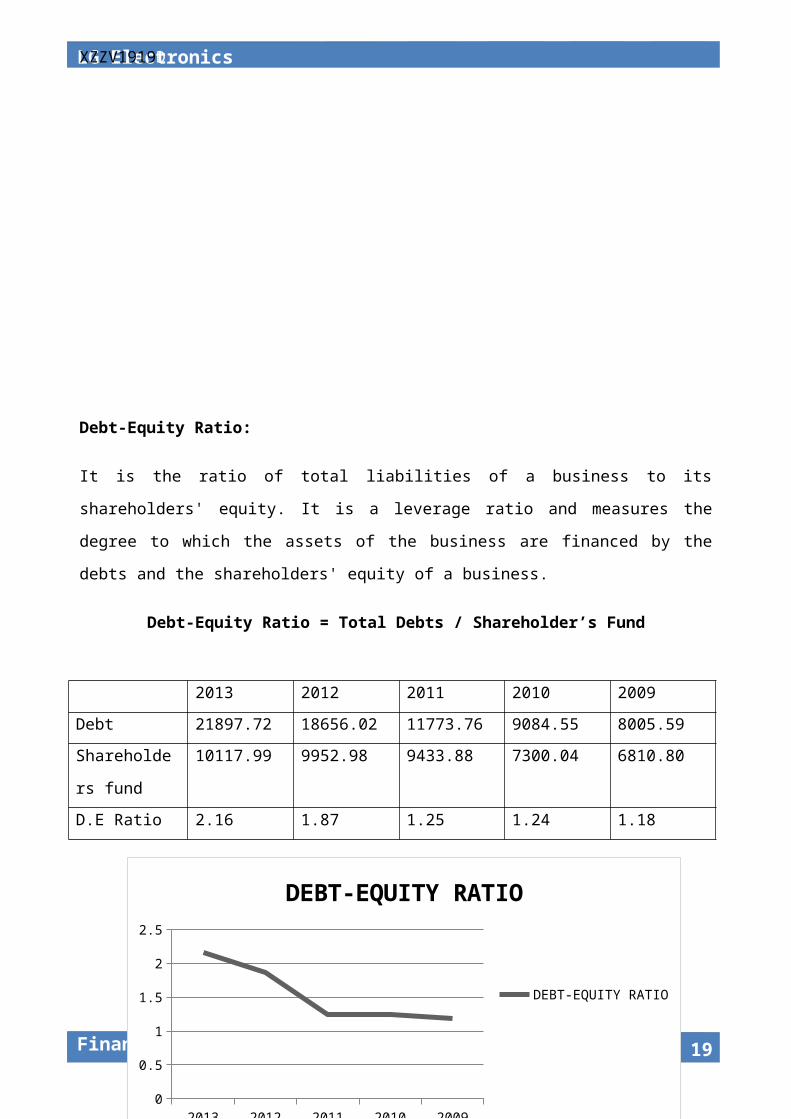

Debt-Equity Ratio:

It is the ratio of total liabilities of a business to its shareholders' equity. It is a leverage ratio and

measures the degree to which the assets of the business are financed by the debts and the

shareholders' equity of a business.

Debt-Equity Ratio = Total Debts / Shareholder’s Fund

Interpretation:

2013 2012 2011 2010 20090

0.5

1

1.5

2

2.5

DEBT-EQUITY RATIO

DEBT-EQUITY RATIO

14

2013 2012 2011 2010 2009

Debt 21897.72 18656.02 11773.76 9084.55 8005.59

Shareholders

fund

10117.99 9952.98 9433.88 7300.04 6810.80

D.E Ratio 2.16 1.87 1.25 1.24 1.18

Financial Accounting

LG ElectronicsXZZV1515D

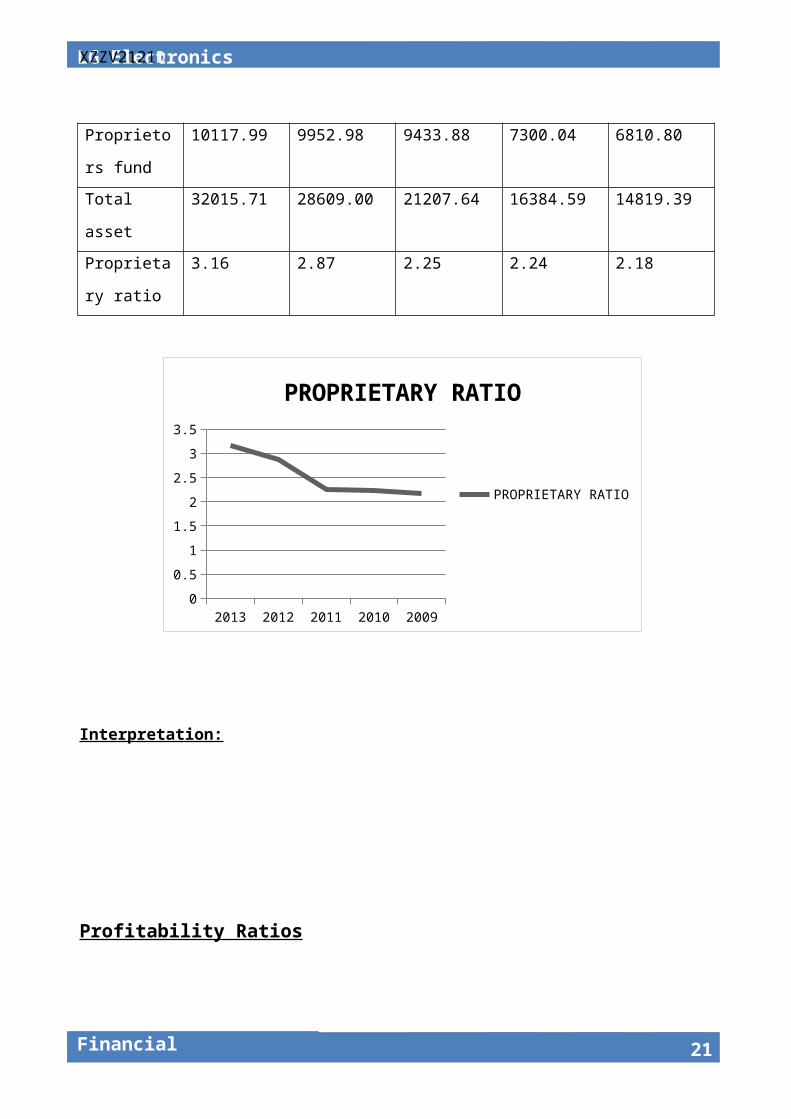

Proprietary Ratio:

Also known as Equity Ratio or the Net Worth to Total Assets Ratio, it is the ratio of shareholders'

funds to total assets. A high ratio indicates that the firm has adequate amount of equity to upkeep

the functions of the business.

Proprietary Ratio = Shareholders funds / Total Assets

2013 2012 2011 2010 2009

Proprietors

fund

10117.99 9952.98 9433.88 7300.04 6810.80

Total asset 32015.71 28609.00 21207.64 16384.59 14819.39

Proprietary

ratio

3.16 2.87 2.25 2.24 2.18

Interpretation:

15

2013 2012 2011 2010 20090

0.5

1

1.5

2

2.5

3

3.5

PROPRIETARY RATIO

PROPRIETARY RATIO

LG Electronics

Financial Accounting

Profitability Ratios

It is a measure of profitability, which measures a company's performance. Profitability is the

ability to make a profit, and a profit is what is left over from income earned after the company has

deducted all costs and expenses related to earning the income

Types of Profitability Ratios:

Common profitability ratios used in analyzing a company's performance include gross profit

margin (GPM), operating margin (OM), return on assets (ROA), return on equity (ROE), return on

sales (ROS), and return on investment (ROI).

16

Financial Accounting

LG ElectronicsXZZV1717D

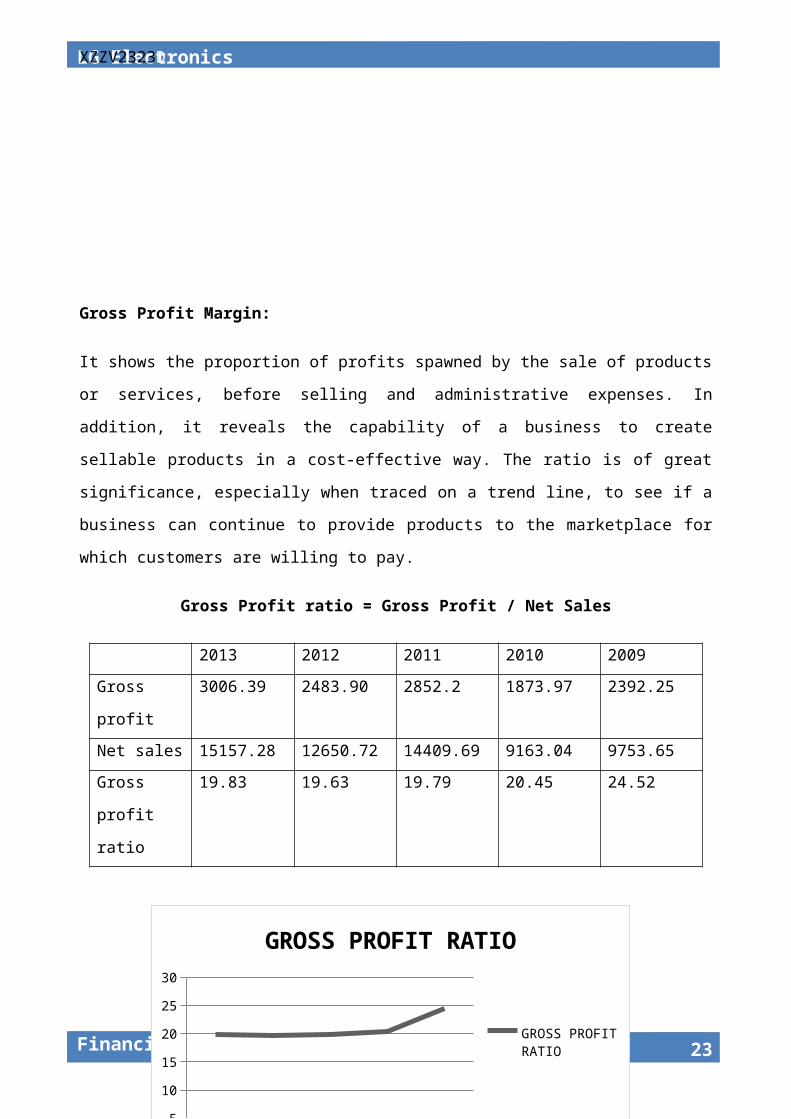

Gross Profit Margin:

It shows the proportion of profits spawned by the sale of products or services, before selling and

administrative expenses. In addition, it reveals the capability of a business to create sellable

products in a cost-effective way. The ratio is of great significance, especially when traced on a

trend line, to see if a business can continue to provide products to the marketplace for which

customers are willing to pay.

Gross Profit ratio = Gross Profit / Net Sales

2013 2012 2011 2010 2009

Gross profit 3006.39 2483.90 2852.2 1873.97 2392.25

Net sales 15157.28 12650.72 14409.69 9163.04 9753.65

Gross profit

ratio

19.83 19.63 19.79 20.45 24.52

17

2013 2012 2011 2010 20090

5

10

15

20

25

30

GROSS PROFIT RATIO

GROSS PROFIT RATIO

LG Electronics

Financial Accounting

Interpretation:

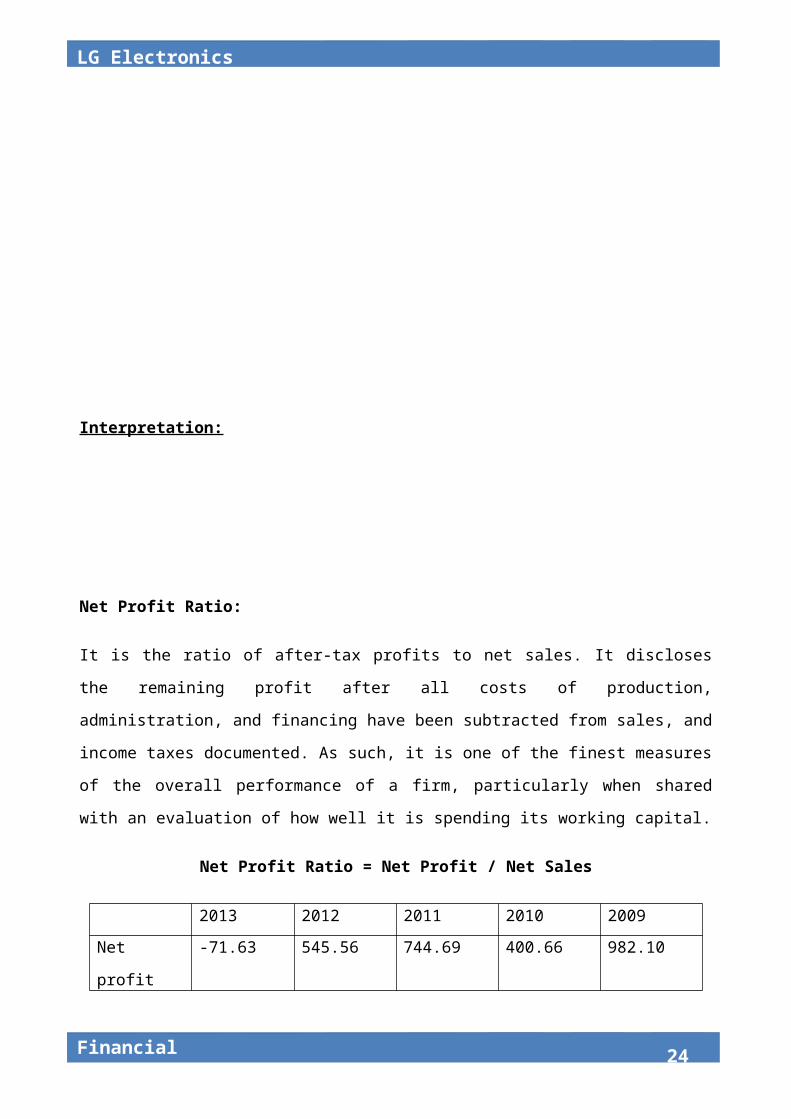

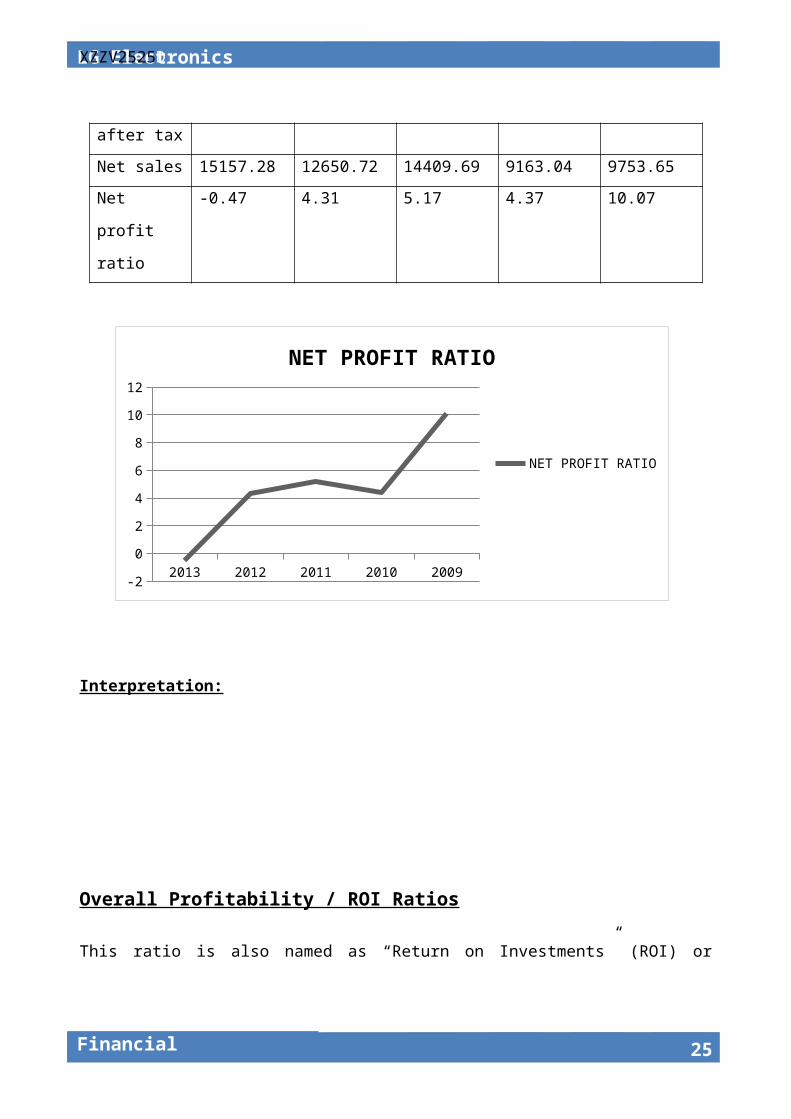

Net Profit Ratio:

It is the ratio of after-tax profits to net sales. It discloses the remaining profit after all costs of

production, administration, and financing have been subtracted from sales, and income taxes

documented. As such, it is one of the finest measures of the overall performance of a firm,

particularly when shared with an evaluation of how well it is spending its working capital.

Net Profit Ratio = Net Profit / Net Sales

2013 2012 2011 2010 2009

Net profit

after tax

-71.63 545.56 744.69 400.66 982.10

Net sales 15157.28 12650.72 14409.69 9163.04 9753.65

Net profit

ratio

-0.47 4.31 5.17 4.37 10.07

2013 2012 2011 2010 2009-2

0

2

4

6

8

10

12

NET PROFIT RATIO

NET PROFIT RATIO

18

Financial Accounting

LG ElectronicsXZZV1919D

Interpretation:

Overall Profitability / ROI Ratios

This ratio is also named as “Return on Investments” (ROI) or “Return on Capital Employed”

(ROCE). It shows the percentage of return on the total capital employed in the business. This ratio

processes the relationship between net profit before interest and tax and capital employed. The

objective of calculating this ratio is to find out how efficiently the long term funds supplied by the

creditors and the shareholders have been used.

19

LG Electronics

Financial Accounting

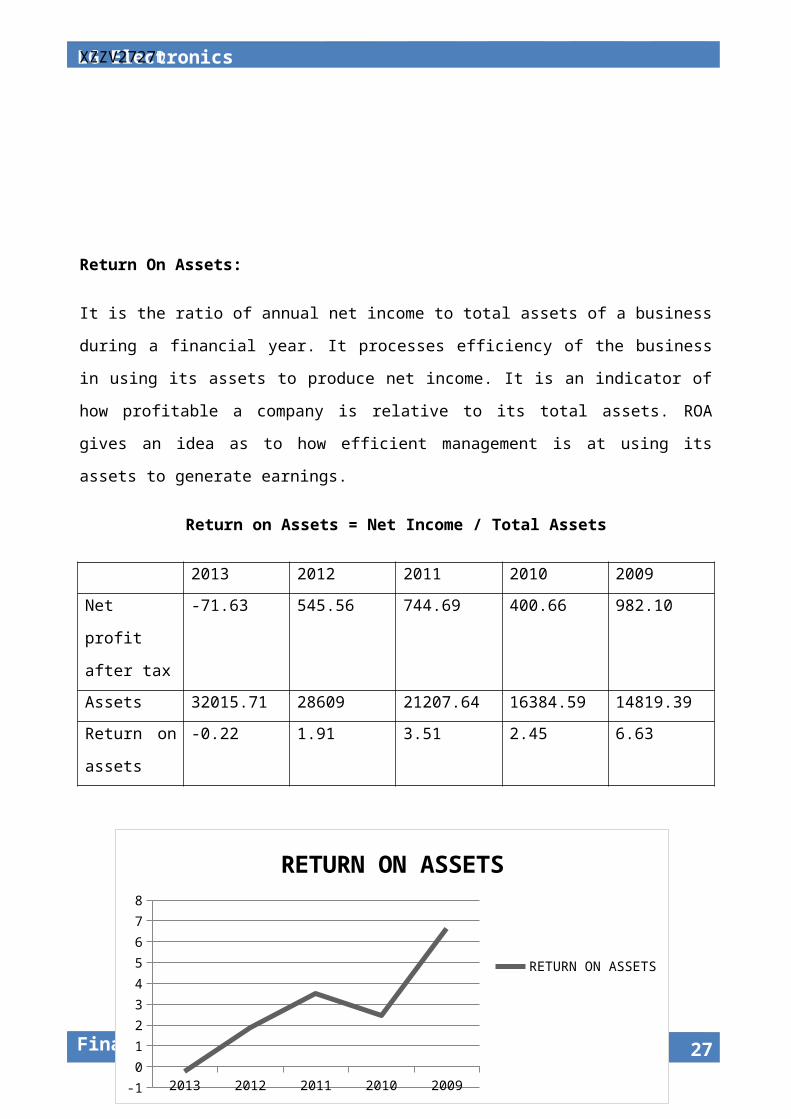

Return On Assets:

It is the ratio of annual net income to total assets of a business during a financial year. It processes

efficiency of the business in using its assets to produce net income. It is an indicator of how

profitable a company is relative to its total assets. ROA gives an idea as to how efficient

management is at using its assets to generate earnings.

Return on Assets = Net Income / Total Assets

2013 2012 2011 2010 2009

Net profit

after tax

-71.63 545.56 744.69 400.66 982.10

Assets 32015.71 28609 21207.64 16384.59 14819.39

Return on

assets

-0.22 1.91 3.51 2.45 6.63

2013 2012 2011 2010 2009-1

0

1

2

3

4

5

6

7

8

RETURN ON ASSETS

RETURN ON ASSETS

20

Financial Accounting

LG ElectronicsXZZV2121D

Interpretation:

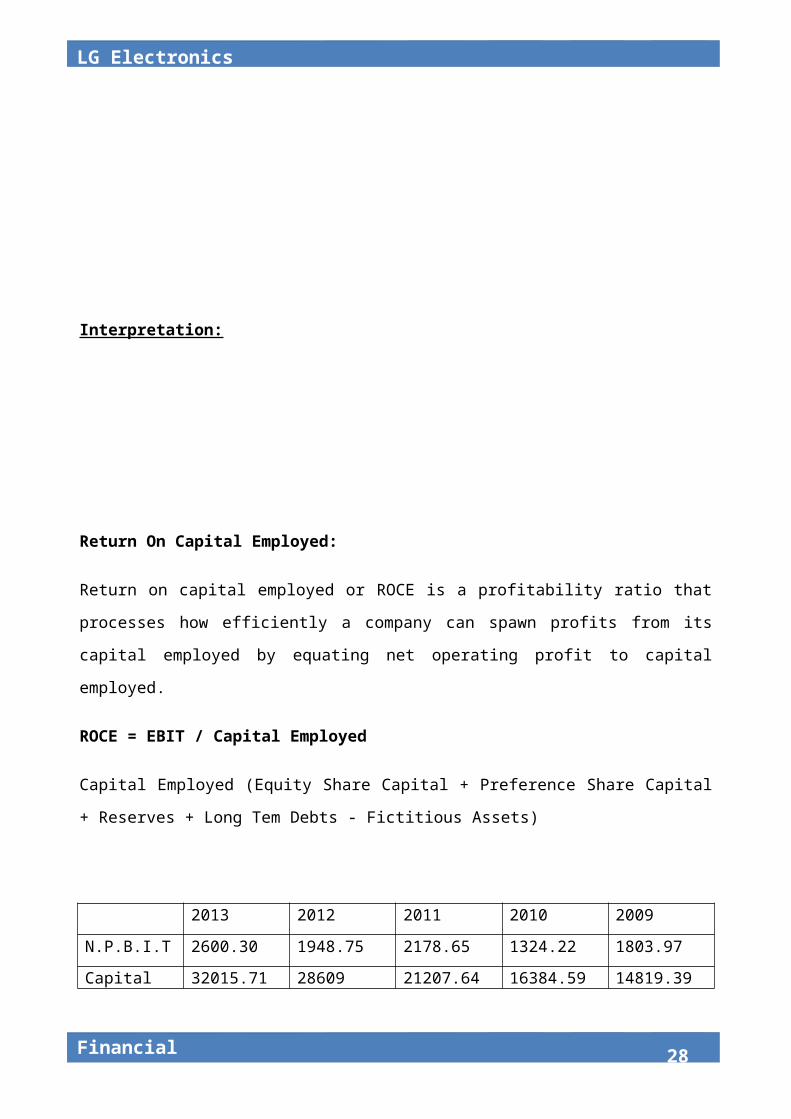

Return On Capital Employed:

Return on capital employed or ROCE is a profitability ratio that processes how efficiently a

company can spawn profits from its capital employed by equating net operating profit to capital

employed.

ROCE = EBIT / Capital Employed

Capital Employed (Equity Share Capital + Preference Share Capital + Reserves + Long Tem Debts

- Fictitious Assets)

2013 2012 2011 2010 2009

N.P.B.I.T 2600.30 1948.75 2178.65 1324.22 1803.97

Capital

employed

32015.71 28609 21207.64 16384.59 14819.39

ROCE 8.12 6.81 10.27 8.08 12.17

212013 2012 2011 2010 2009

0

2

4

6

8

10

12

14

ROCE

ROCE

LG Electronics

Financial Accounting

Interpretation:

Return On Equity:

This ratio determines the amount of net income reverted as a percentage of shareholders equity.

Return on equity processes a corporation's profitability by enlightening how much profit a

company creates with the money shareholders have invested.

ROE = (NPAT – Preference Dividend) / Equity Shareholder’s Fund

2013 2012 2011 2010 2009

N.P.A.T-

Preference

dividend

-74.4 542.18 740.08 396.98 978.42

Equity

shareholders

fund

10117.99 9952.98 9433.88 7300.04 6810.80

ROE -0.74 5.45 7.84 5.44 14.36

2013 2012 2011 2010 2009-2

0

2

4

6

8

10

12

14

16

ROE

ROE

22

Financial Accounting

LG ElectronicsXZZV2323D

Interpretation:

Earning Per Share:

EPS (Earning per Share) measures the profit earned per share by the shareholders. It is the portion

of a company's profit allotted to each outstanding share of common stock. Earnings per share

serves as a pointer of a company's profitability. Higher the value of EPS, higher is the

attractiveness of the stock to the investors.

EPS = (NPAT – Preference Dividend) / Total No. of Equity Shares Outstanding

2013 2012 2011 2010 2009

N.P.AT-

preference

dividend

-74.4 672.42 917.75 477.10 1055.75

No. of equity

shares o/s

49.6 37.35 46.51 27.30 24.66

EPS -1.50 18 19.73 17.47 42.80

23

2013 2012 2011 2010 2009-10

0

10

20

30

40

50

EPS

EPS

LG Electronics

Financial Accounting

Interpretation:

Dividend Payout Ratio:

It is the ratio that depicts the percentage of earnings paid back to the shareholders in the form of

dividend. The amount that is held back by the company is called retained earnings, which is used

for further development of the company.

DPR = Dividend per Share / EPS

2013 2012 2011 2010 2009

-200

-150

-100

-50

0

50

DIVIDEND PAYOUT RATIO

DIVIDEND PAYOUT RATIO

24

2013 2012 2011 2010 2009

D.P.S 2.77 3.38 4.61 3.68 3.68

E.P.S -1.50 18 19.73 17.47 42.80

Dividend pay

out ratio

-184.66 18.77 23.36 21.06 8.59

Financial Accounting

LG ElectronicsXZZV2525D

Interpretation:

Particulars 2013 2012 2011 2010 2009

Current ratio 5.168 6.153 7.408 5.797 5.290

Quick ratio 4.729 5.541 6.022 4.638 4.203

Fixed asset turnover ratio 1.50 0.97 0.98 0.79 1.36

Current asset turnover

ratio

0.71 0.60 1.139 1.038 1.276

Working capital turnover

ratio

0.739 0.722 1.317 1.255 1.573

Capital employed turn

over ratio

0.47 0.44 0.68 0.60 0.66

Debt equity ratio 2.16 1.87 1.25 1.24 1.18

Propriety ratio 3.16 2.87 2.25 2.24 2.18

Gross profit ratio 19.83 19.63 19.79 20.45 24.52

Net profit ratio -0.47 4.31 5.17 4.37 10.07

25

LG Electronics

Financial Accounting

Operating net profit ratio 19.83 19.63 19.79 20.45 24.52

Return on asset ratio -0.22 1.91 3.51 2.45 6.63

Return on capital

employed

8.12 6.81 10.27 8.08 12.17

Return on equity -0.74 5.45 7.84 5.44 14.36

Earning per share -1.50 18 19.73 17.47 42.80

Dividend payout ratio -184.66 18.77 23.36 21.06 8.59

Conclusion

26

Financial Accounting

LG ElectronicsXZZV2727D

References

27

LG Electronics

Financial Accounting

Annexures

28