Embed Size (px)

Citation preview

Liberty Holdings LimitedInvestor conference 20164 & 5 April

Thabo DlotiLiberty Group Chief Executive

3

Our purpose

4

Our group objectives to 2020 are clear and unchanged

Become the No. 1 provider in South Africa to the retail aspirational mid and affluent markets

Become the preferred partner for Standard Bank in all its African geographies

Leverage and ensure seamless transfer of core capabilities of the group to where the opportunities are

Vision: Liberty will be the trusted leader for insurance and investmentsin Africa and in other chosen markets

Being in Top 10 in Nigeria and Top 3 in Kenya and gaining significant growth and insurance market share in the rest of SSA

Become the preferred destination for asset flows destined for Africa

Accelerate growth and market share in the SA corporate market to become a Top 3 player through acquisitions

Liberty’s shares trading at a premium to sector average

5

Our anticipated Africa presence

Current Licensed Presence Anticipated 2020 footprint

8 Life licenses3 Short-term licenses9 STANLIB businessesHealth presence in 18 countries

• 4 Liberty licenses (includes Lesotho)• 10 Contracted license, Liberty

administration• 4 Contracted license, Third party

administration

15 Life licenses15 Short-term licenses10 STANLIB businessesHealth presence in 24 countries

• 12 Liberty licenses• 11 Contracted license, Liberty administration• 1 Contracted license, Third party

administration

6

Shifted the business to a new business model – from product houses to integrated value chain business for specific market segments

Ret

ail A

dvis

ory

DFS

(dire

ct s

ales

)

ECM

wor

ksite

sal

es

Cor

pora

teC

AL

STAN

LIB

Afric

a In

sura

nce

Hea

lth

Product push through channel

Overlapping end markets with little or no

segment focus

HNW & institutional funds

(international)

Individual Arrangements

Asset Management

Group Arrangements

Aspirational & affluent (SA)

Multinationals, Corporates,

SME’s, affinities,

(SSA)

Integrated value chain businesses… designed for specific segments

Product houses geared to fulfil propositions

7

We have unique capabilities to unlock these opportunities

• Strong relevant brand to the affluent market

• Strong distribution capability

• Attractive product set and product development capability

• Understanding of existing customers, their needs and buying behaviour

• Solid track record in the SME market

• Extensive African footprint and expertise

• Capability to serve companies in multiple geographies (e.g. healthcare)

• Insurance in a box

Individual Arrangements Group Arrangements Asset Management

• Multi-specialist franchise model with unique and strong investment propositions

• African footprint with expertise and product set

• Shared services platform leveraged across multiple geographies

• Offshore partners relationship and footprint – access to global investors

• Relationship with Standard Bank • Balance sheet management• Group functions to enable cost- and time-efficient operations

Group-wide

8

Life Insurance• In-country presence key to customer acquisition, servicing and risk management• Low cost operating model – competitive markets and/ or low price points• Market penetration versus market share acquisition – innovation, access and regulation• Standard Bank a key differentiator to access target customer segments

Health• Underwrite on Liberty licenses to capture additional margin and synergies• Cross sell to existing Health multinational client base • Expand health insurance offering to commercially viable target segments • Leverage health data for risk selection and management

We understand business imperatives required for success

9

STANLIB• A highly competitive market characterised by low fees in the pensions market

o Develop a suite of high margin products• Evolving demand profiles and expectations from institutional and retail investors results

in a need for diversified investment optionso Build additional distribution capacity

• The regulatory landscape may become increasingly stringent once reforms are implementedo Engage with regulators help influence policy changes that are supportive of the

industry

And Asset Management

10

IndividualArrangements

GroupArrangements

STANLIB Other 2015 Expectedlong-term rate

of return –SIP

67% 23%

How are we tracking against strategy ?

Our strategy has been to improve the quality of earnings, this has continued despite headwinds

Individual Arrangements• Good free cash generation• New generation products

are more capital efficient

Group Arrangements• Africa contribution growing

with footprint with better margins

STANLIB• New capabilities attracting

3rd party flows • Margin improvement

Contribution to operating earnings 2015 (Rm)

IndividualArrangements

GroupArrangements

STANLIB Other 2011 Expectedlong-term rate

of return –SIP

-2%

Contribution to operating earnings 2011 (Rm)

33% of Coreearnings

1 869225

629 49 2 772

1 379

2014/15 growth %

1 335 (38)

546 (75) 1 768

1 097

37% of Coreearnings

8% 2%

73% 31% -4%

11

9511 130

188

982

1 353

187

Agency BrokerConsultant

2013 2014 2015

Individual Arrangements, managed to model with focus on quality

• Decline in Agency force due to focus on improving productivity

• On-going growth of experienced advisers in tied channels maintains quality of sales

• Successful sales efforts and continued focus on retention initiatives in a tough environment

• Focus on quality new business volumes

• Good sales in STANLIB Linked Life Annuities and RAs

• New product launched – Liberty Agile with sales of R157m in first three months of launch

• Good returns on a higher asset base

• Positive risk and persistency variances

• On-going tight expense management and cost control

Focused distribution efforts maintains quality

Gross sales reflect difficult consumer environment

Solid earnings growth

22 414

25 21625 622

2013 2014 2015

1 467

1 689

1 869

2013 2014 2015

12

545551

579

2013 2014 2015

Asset Management

1. Excludes intergroup

• Continue to attract positive non-money market flows

• Money market flows are positive following improved sentiment

• Positive flows from group channels combined with improved retention benefitted cash flows

• Gaining traction in passives –R1bn mandates won.

• Margins benefited from a better flows mix

• Alternative capabilities, unlisted property (double digit returns) and infrastructure funds (50% return), have delivered superior returns

• Improved flows to own unit trusts via STANLIB LISP

• Strong growth in other African territories

• And good contribution to earnings

• REIT listed and secured $35m, target properties secured

Significant improvementin cash flows¹ (Rm)

South African margin growthfrom good inflows

Business continues toattract 3rd party flows

31 31

33

2013 2014 2015

13 527

2 1986 417

(13 738)

7 343

1 111

Non-moneymarket

Money market

2013 2014 2015Bps Rbn

13

78

90

105

68 68 71

2013 2014 2015Health Cover lives (000)

7 1727 270

7 810

2013 2014 2015

55%

2%

38%

5%

Brokerbancassurance

Group Arrangements, operational focus and expansion continues

• Improved diversification of sales volumes through multiple channels – a key focus

• Launched new market leading index tracking investment range

• Expanding consulting business

• Lower single premium sales • Stable Growth Fund top

performing fund of its kind• Improved service delivery to

umbrella fund customers• Total recurring premiums up 7%

in a challenging market

• Continue to see good contribution from the rest of Africa, aided by rand weakness

• Claims loss ratio is within target

Liberty Corporate expanded South African distribution channels

Liberty Corporate recurring gross insurance premiums supported by new product offerings

Increased focus on efficienciesand product offering in Health

Rm

14

Short term challenges are outweighed by the long term opportunity

In conclusion

Liberty is committed to capturing long term growth in Africa

1

2

Our core skills and strengths in insurance and investments combined with our footprint provides a competitive advantage

3

Questions

Private and confidential

Analyst Certification: This material is "non-independent research" and constitutes a "marketing communication" as defined in the UK FCA Handbook.It has not been prepared in accordance with the full legal requirements designed to promote independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research

Macroeconomic Update

East Africa will be the crown jewel in SSA; Take two

Jibran Qureishi

Regional East Africa Economist

4 April 2016

11

Commodity prices remain key transmission mechanism between globe and Africa

Hydro carbon exporters

Non-Oil Resources

Guinea

26%

86%

Botswana

27%

92%

Zambia

13%

73%

Rep ofCongo

74%%

76%

Cameroon

24%

51%

Nigeria

14.4%

97%

Gabon

66%

84%

Namibia

27%

39%

Angola

38%

97%

Cote d’Ivoire

20%

15%

LEGEND

Mining (% of GDP)

Fuel, Minerals & Metals (% of

Exports)

Ghana

17%

46%

SSA – contribution of extractive industries

Nigeria and Angola are particularly vulnerable to downside pressure on oil prices

Source: statistics agencies, central banks, Standar d Bank Research

* Nigeria contribution to GDP reflects Crude Oil in dustry in rebased national accounts

(South) Sudan

60%

78%

2

China’s new normal

Geography of commodities Chinese imports (USD bn)

PGM, Gold and other industrial metals in S.

Africa

Oil in Nigeria,

Sudan and Libya

Copper and Cobalt in

Zambia and the DRC

Bauxite and

alumina in Guinea

Gold in West Africa

Various other commodities,

including Uranium, Coal, and industrial

metals found throughout Africa

Less than USD100mnUSD100mn – USD500mnUSD500mn – USD1bnUSD1bn – USD4bn

USD4bn – USD10bn

More than USD10bn

Africa’s share of world commodities

And don’t forget agricultural potential

024681012

0

30

60

90

120

Sud

an

DR

C

Nig

eria

Mal

i

Tan

zani

a

Alg

eria

Moz

ambi

que

Ang

ola

Nam

ibia

Cot

e d'

Ivoi

re

Cultivable area Cultivated area Irrigation RHS

% of cultivated areaMn ha

0 25 50 75 100

PGMPhosphate

GoldChromiumMaganese

CobaltDiamonds

Bauxite

Reserves Mine production (2010)

Share of world total, %

3

SARB caught between a rock and a hard place?

What does the SARB do in this precarious situation?

-2

-1

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016f 2017f

4.8% average

2% average

1.1% average

GDP growth, annual percent

POOR GDP GROWTH BLIGHTS SA’S STATUS

Sources: Fitch, Moody’s, S&P, Standard Bank

Research

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

S&P

Moody’s

Fitch

B+

BB-

BB

BB+

BBB-

BBB

BBB+

A-

A

A+

B

B1

Ba3

Ba2

Ba1

Baa3

Baa2

Baa1

A3

A2

A1

B2

Non-investment grade

5

Major central banks have printed a lot of money but there’s been no inflation

The brown line is a rough estimate of global dollar liquidity – and it has been rising sharply since around 2000…

…and yet global inflation has fallen

But this is goods price inflation. Asset price inflation, like bond prices, stock prices and property prices have risen

6

Global debt still surgingGlobal debt now around 300% of GDP…

…or around USD200tr

0

50

100

150

200

250

Q4 2000 Q4 2007 Q4 2014

Financial Government Corporate Household

269% of GDP

299% of GDP

$ tr

246% of GDP

Source: McKinsey

7

What’s wrong with debt? Key points

Economic growth helps to pay off debt

But if nominal growth is less than the interest rate charged on debt, it is difficult to reduce the debt

In this example the sink stays full with debt

Source: Standard Bank Research

Interest rates

Growth

Debt

8

Are Democrats good for the dollar?Key points

Shaded areas represent Democrat presidents

The dollar tends to rise during Democrat presidency and fall when Republican president is in charge

Recessions have tended to occur during Republican presidencies, not Democrat

Political dangers – the US

For Trump

• Voters are railing against

government

• Sufficient finance

• Hard for Democrats to win the

presidency after a two-term

stint for Obama

• Obama’s popularity rating is

low

• Clinton supported by big

business, especially Wall Street

• Clinton is seen as an

‘untrustworthy’ candidate

Against Trump

• ‘Offended’ minorities dominate many swing

states

• Demographics – the US is becoming less

‘white’

• He’s offended the Republican Party

• Swing voters could align against him

• He’s not been strongly challenged on issues

• He’s seen as an ‘untrustworthy’ candidate

• He’s not attracted much negative

campaigning

Key points

High debt and modest growth are sowing the seeds of political fragmentation and disenchantment

One place we see this is in the US with the rise of Republican candidate Donald Trump

10

Who do you trust in the Brexit polling debate?Key points

Opinion polls show consistently different results depending on whether people are called on the telephone or fill in an online poll

What does this reflect?

Possibly people feel more pressurised to give an opinion on the telephone

It may also be because they feel they ‘should’ express a bias to remain

5

15

25

35

45

55

Remain Leave Undecided Remain Leave Undecided

Remain Leave Undecided Remain Leave Undecided

Internet polls Telephone polls

Source: Mori, Ipsos, ICM. Opinion polls Dec 1 st – Feb 19th

11

Currency forecastsKey points

Dollar seen firm –but volatile

The dollar’s long-term uptrend dating back to 2011 is seen coming to an end in the 1-2 year horizon

Source: Standard Bank Research

1 month 3 months 6 months 1 year 2 years

EUR/USD 1.10 1.15 1.05 1.00 1.20

USD/JPY 112 115 120 125 100

GBP/USD 1.43 1.35 1.30 1.33 1.50

USD/CNY 6.55 6.65 7.0 7.2 6.90

12

Key pointsKey points

Growth expected to expand by 5.7% y/y in 2016

Inflation depends largely on food inflation outlook

USD/KES likely to trade at levels around 107.0 by end of 2016

Consistency between monetary and fiscal policy needed

Kenya: Politics could take centre stage in the coming years

7580859095100105110115120

Dec-10 Sep-13 Jun-16

USD/KES

USD/KESUSD/KESUSD/KESUSD/KES

History Forwards Forecast

5.45

5.95

6.45

6.95

7.45

Jan-15 Apr-15 Jul-15 Oct-15

USDbn

FX ReservesFX ReservesFX ReservesFX Reserves

-15000.0

-10000.0

-5000.0

0.0

5000.0

10000.0

2008 2010 2012 2014f 2016f

USD m

Current Account DevelopmentsCurrent Account DevelopmentsCurrent Account DevelopmentsCurrent Account Developments

Trade balance ServicesIncome Transfers

-9.0

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

FY2011/12 FY2013/14 FY2015/16

% of GDP

Deficit incl. grantsDeficit incl. grantsDeficit incl. grantsDeficit incl. grants

13

FX reserves recover after financial outflows in 201 5

Source: KNBS; CBK; Standard bank research

Key pointsKey points

Balance of payment shock in 2015 was largely owing to financial account.

Reversal of financial flows began in Q4:15, albeit modestly.

When will equity market rebound?

CBK has a war chest with FX reserves being boosted by syndicated loan issuance as well as IMF precautionary facility at their disposal.

CBK has more than enough ammunition to ensure KES operates in an orderly manner.

5.45

5.65

5.85

6.05

6.25

6.45

6.65

6.85

7.05

7.25

7.45

Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15

USDbn

Financial

outflows

Boosted by

Eurobond

Boosted by

syndicated loan

14

Input costs have risen continuously in 2015 often t hanks to the weaker KES

Input prices PMI …Prices charged PMI

Sources: Markit; CfC Stanbic Bank

Drop in prices driven by

oil price reductions.

KES depreciation

15

SGR will be a silver bullet for the region

Source: Standard bank research

Key pointsKey points

SGR completion will provide a strong platform for the incumbent to demonstrate progress at pre-election rallies.

Intra East African trade will inevitably be boosted by the SGR.

Will be the catalyst for the industrialization process in the region.

Projected is mostly funded offshore.

16

Key pointsKey points

Magufuli has so far lived up to his nickname ‘tingatinga’ which means bulldozer.

Fiscal deficit inclgrants likely to be lower at 10.3% of GDP in FY15/16 as we suspect planned expenditure by the govt was lower due to delays in obtaining donor funding.

Tax collections been abysmal over the years. Magufuli, suspends TRA chief after TZS80bn couldn’t be accounted for.

Eurobond or private placement?

Credit rating delay?

Tanzania: Magafuli clamping down on spending

Magufuli has started well, but he must;

• Find a swift solution to the stalemate in Zanzibar.

• Hold the referendum vote for the new constitution.

• Fight corruption and continue his on-going house cleaning exercise.

• Sort out the petroleum act to boost FDI in the natural gas sector.

18

Key pointsKey points

Food prices are likely to mirror the trend in the rest of the region and rise in Q1:16.

Food stocks held by the National Food Reserve Agency (NFRA) have been falling since Dec 14. This is potentially a further upside risk to food prices.

The BOT increased the SMR ration to 10% from 8% and also lowered commercial banks prudential limit on foreign currency NOP, to 5.5% from 7.5% of core capital.

BOT will remain circumspect around the TZS and thus prefer to leave the policy stance unchanged.

Tanzania: Time for an inflation index rebase?

0.00

5.00

10.00

15.00

20.00

25.00

0

5

10

15

20

25

30

35

40

45

Jan-11 Jun-11 Nov-11 Apr-12 Sep-12 Feb-13 Jul-13 Dec-13 May-14 Oct-14 Mar-15 Aug-15

RHS Food inflation%

91-day Food inflation Headline inflation (y/y) Core inflation

Core inflation actually subsided in

period of extreme TZS

depreciation. Been trending

sideways since then.

19

Key pointsKey points

We expect GDP growth to register 5.4% y/y and 5.7% y/y in 2016 and 2017 respectively. This is up from an estimated 4.8% y/y in 2015.

Coffee productivity too low. South Sudan peace agreement remains in the balance?

C/A deficit probably eased to 7.7% of GDP in 2015.

USD/UGX likely to trade around 3700 by year end.

BOU likely to commence on a gradual easing cycle in H2:16.

Uganda: What next after elections?

1 800

2 300

2 800

3 300

3 800

4 300

4 800

Dec-10 Sep-13 Jun-16

USD/UGX

USD/UGXUSD/UGXUSD/UGXUSD/UGX

History Forwards Forecast

2 500.0

2 600.0

2 700.0

2 800.0

2 900.0

3 000.0

3 100.0

Jan-15 Apr-15 Jul-15 Oct-15

USDmn

FX ReservesFX ReservesFX ReservesFX Reserves

-4000

-3000

-2000

-1000

0

1000

2000

2004 2006 2008 2010 2012 2014 2016f

USDmn

Current Account DevelopmentsCurrent Account DevelopmentsCurrent Account DevelopmentsCurrent Account Developments

Trade Services Income

Transfers C/A

-7.5

-7.0

-6.5

-6.0

-5.5

-5.0

-4.5

-4.0

FY2010/11 FY2013/14 FY2016/17

% of GDP

Deficit incl. grantsDeficit incl. grantsDeficit incl. grantsDeficit incl. grantsInfrastructure

imports and drop

in FDI.

20

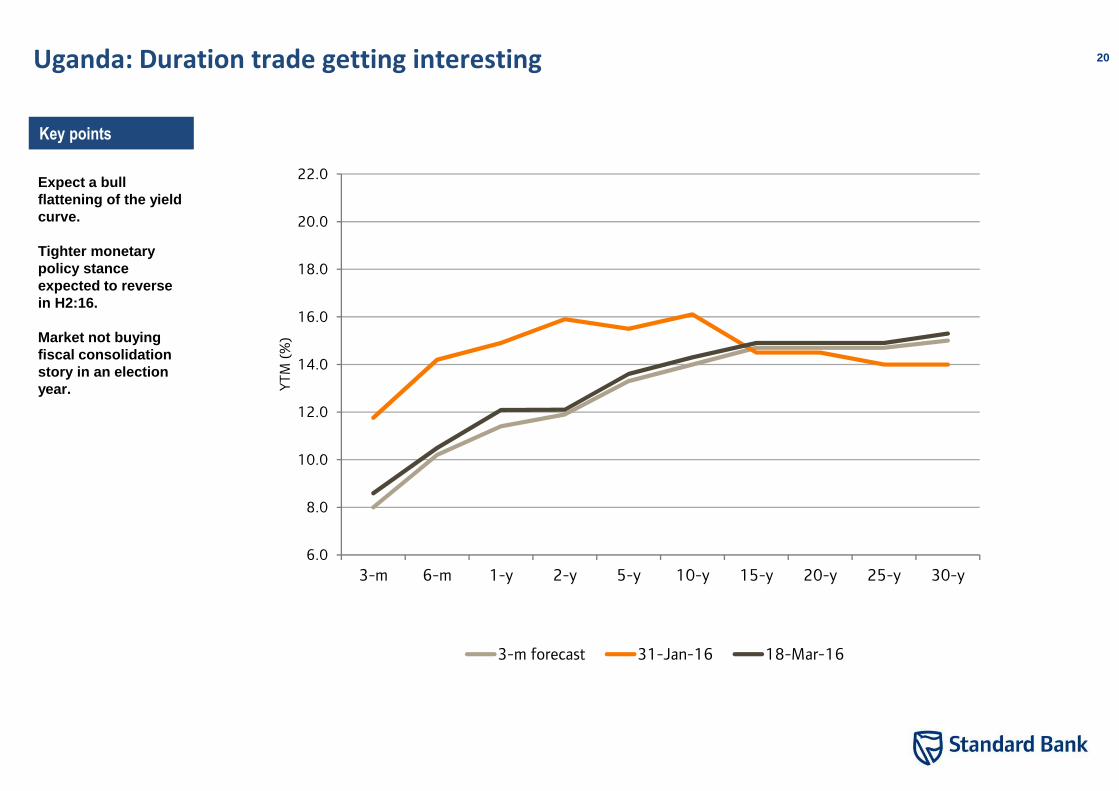

Key pointsKey points

Expect a bull flattening of the yield curve.

Tighter monetary policy stance expected to reverse in H2:16.

Market not buying fiscal consolidation story in an election year.

Uganda: Duration trade getting interesting

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

3-m 6-m 1-y 2-y 5-y 10-y 15-y 20-y 25-y 30-y

YTM (%)

3-m forecast 31-Jan-16 18-Mar-16

21

Key pointsKey points

By its own admission, the BOU believes the pass through effects of the weaker UGX, will increase core inflation.

BOU inflation forecasts are worrying. See 10% for core inflation in Q3:15.

Are they expecting further UGX weakness from a potential pre-election spending binge.

Money printing in 2011, admitted by BOU Governor.

Uganda: BOU’s concerns around core inflation

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Feb-06 Jan-08 Dec-09 Dec-11 Nov-13 Oct-15

%, y/y

Headline Food Core

22

Key pointsKey points

BOU consistently implies that macroeconomic instability in 2015 came about due to faster economic activity.

PSC and M3 growth not painting a true picture of this.

Soft GDP growth underscores our thoughts.

Uganda: Real output within target, contrary to what BOU thinks

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Jan-10 Sep-10 May-11 Jan-12 Sep-12 May-13 Jan-14 Sep-14 May-15

M3 y/y PSC y/y

UGX revaluation effects on

the two metrics.

23

Key pointsKey points

How sensible is the ‘overvaluation’ chatter in East Africa?

UGX REER reversing course.

Will this improve BOU’s tolerance for a stable and possibly a stronger UGX?

We think so.

No point in looking at trade weighted models without factoring in productivity.

Uganda: UGX not ‘overvalued’ anymore?

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Jan-10 Aug-10 Mar-11 Oct-11 May-12 Dec-12 Jul-13 Feb-14 Sep-14 Apr-15 Nov-15

UGX REER 5-y Avg

REER Depreciation

REER

Appreciation

24

Key pointsKey points

Service exports supported by tourism briefly in 2015.

Value benefitting from stronger USD, but volumes remain upsettingly low.

Numbers show South Sudan impact not as bad as thought.

Uganda: How reasonable is the UGX overvaluation paradigm?

0.0

50.0

100.0

150.0

200.0

250.0

300.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Goods exports Service exports

25

East African urbanisation plays to manufacturing se ctors competitive advantage

By 2050, 2/3 will live in cities African megacities will emerge

Sources: UN Habitat, Standard Bank Research

0%

25%

50%

75%

100%

1950 1975 2000 2020 2045

Rural population Urban population

Construction-related sales benefit

Electric lampsInsulated wires/cablesTaps & valvesAir conditionersStatic convertorsConstruction machinery

USD500mn

USD250mn

USD100mn USD50mn USD25mn

26

Divergence in growth is a dominant theme for Africa in 2016

Conclusion

� Commodity exporters (specifically metals, oil) will likely experience a marked slowdown in economic growth

– Financing of growth will prove challenging

– Pressure on currencies to depreciate

� Non-metals, non-oil exporters should fare much better

– Monetary policy independence

– Less pressure for currency depreciation

27Disclaimer

This material is non-independent research. Non-inde pendent research is a "marketing communication".

This material is "non-independent research". Non-independent research is a "marketing communication" as defined in the UK FCA Handbook. It has not been prepared in accordance with the full legal requirements designed to promote independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Additional information with respect to any security referred to herein may be made available on request. This material is for the general information of institutional and market professionals’ clients of Standard Bank Group (SBG) only. Recipients who are not market professionals or institutional investor customers of SBG should seek advice of their independent financial advisor prior to taking any investment decision based on this communication or for any necessary explanation of its content. It does not take into account the particular investment objectives, financial situation or needs of individual clients. Before acting on any advice or recommendations in this material, clients should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The information, tools and material presented in this marketing communication are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments, nor shall it, or the fact of its distribution, form the basis of, or be relied upon in connection with, any contract relating to such action. This material is based on information that we consider reliable, but SBG does not warrant or represent (expressly or impliedly) that it is accurate, complete, not misleading or as to its fitness for the purpose intended and it should not be relied upon as such. The information and opinions contained in this document were produced by SBG as per the date stated and may be subject to change without prior notification Opinions expressed are our current opinions as of the date appearing on this material only. We endeavour to update the material in this report on a timely basis, but regulatory compliance or other reasons may prevent us from doing so.

SBG or its employees may from time to time have long or short positions in securities, warrants, futures, options, derivatives or other financial instruments referred to in this material. Where SBG designates NON- INDEPENDENT Research to be a “marketing communication”, that term is used in SBG’s Research Policy. This policy is available from the Research Compliance Office at SBG. SBG does and seeks to do business with companies covered in its non-independent research reports including Marketing Communications. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

SBG has published a Conflicts of Interest Policy that is available upon request which describes the organisational and administrative arrangements for the prevention and avoidance of conflicts of interest. Further disclosures required under the FCA Conduct of Business Sourcebook and other regulatory bodies are available on request from the Research Compliance Department and or Global Conflicts Control Room, unless otherwise stated, share prices provided within this material are as at the close of business on the day prior to the date of the material. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of SBG. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of SBG or its affiliates.

SBG believes the information and opinions in the Disclosure Appendix of this report are accurate and complete. Information and opinions presented in the other sections of this communication were obtained or derived from sources SBG believes are reliable, but SBG makes no representations as to their accuracy or completeness. Additional information is available upon request. SBG accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to SBG.

The services, securities and investments discussed in this material may not be available to nor suitable for all investors. Investors should make their own investment decisions based upon their own financial objectives and financial resources and it should be noted that investment involves risk, including the risk of capital loss. Past performance is no guide to future performance. In relation to securities denominated in foreign currency, movements in exchange rates will have an effect on the value, either favourable or unfavourable. Some investments discussed in this marketing communication have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment, in such circumstances you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make them investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realize those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed.

28Disclaimer (continued)

This report is issued in Europe and approved as a financial promotion for the purposes of distribution in the UK by Standard Advisory London Limited 20 Gresham Street, London EC2V 7JE which is authorised by the Financial Conduct Authority (“FCA”). This report is being distributed in Kenya by CfC Stanbic Bank Limited; in Nigeria by Stanbic IBTC; in Angola by Standard Bank de Angola S.A.; in China by Standard Bank Limited; in Botswana by Stanbic Bank Botswana Limited; in Democratic Republic of Congo by Stanbic Bank Congo s.a.r.l.; in Ghana by Stanbic Bank Ghana Limited; in Hong Kong by Standard Advisory Asia Limited; in Isle of Man by Standard Bank Isle of Man Limited; in Jersey by Standard Bank Jersey Limited; in Madagascar by Union Commercial Bank S.A.; in Mozambique by Standard Bank s.a.r.l.; in Malawi by Standard Bank Limited; in Namibia by Standard Bank Namibia Limited; in Mauritius by Standard Bank (Mauritius) Limited; in Tanzania by Stanbic Bank Tanzania Limited; in Swaziland by Standard Bank Swaziland Limited; in Zambia by Stanbic Bank Zambia Limited; in Zimbabwe by Stanbic Bank Zimbabwe Limited; in UAE by The Standard Bank of South Africa Limited, Dubai branch.

In respect of the United States, this report is solely intended for distribution to US institutional investors that qualify as Major US Institutional Investors under Securities Exchange of 1934 Rule 15a-6.In jurisdictions where Standard Bank Group is not already registered or licensed to trade in securities, transactions will only be effected in accordance with the applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements.

Standard Bank Group Ltd Reg.No.1969/017128/06) is listed on the JSE Limited. SBSA is an Authorised Financial Services Provider and it also regulated by the South African Reserve Bank.

Copyright 2015 SBG. All rights reserved. This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Standard Bank Group Ltd.

Liberty Holdings LimitedInvestor conference 20164 April

Unlocking growth in AfricaSandile Hlophe, CE: Group Arrangements

3

Why Africa….

$1.4 trillionconsumer spending

1 billion15% of the world’s

population

$2.6 trillionEst. GDP in 2020

6 out of 10fastest growing

economies

128 millionAfricans buying consumer goods

5.5% GDPp.a. forecast to

2017

Sources: World Bank, IMF, Economist

4

Positive progress across the continent over last 10 years

Fundamentals remain positive• Growing population is increasing demand

• Increased urbanisation

• Improved political landscape

• Evolving regulatory frameworks

• Improved stock markets and oversight

Democracies are beginning to strengthen• Zambia, Nigeria, Kenya – democratic elections

Long-term policy decision making is positive• Regulatory reform and financial market stability remains key on government

agendas

• These are catalysts for growth and stability of the areas

Favourable market conditions for pensions and insurance business

5

Distinct regional growth trajectories

Western region is potentially the most significant opportunity but vulnerable to market volatility • Large and fast growing affluent consumer

market in Nigeria• Strong and increasing foreign investment

inflows• Significant commodity-based economy,

especially oil• Demand creates ‘Expensive’ entry premium• Planned risk-based capital requirements in

Nigeria and Ghana will improve prospects for well-capitalised insurers like Liberty

Southern region is more mature and expected to grow at a slower rate

• Stronger economies, highly resource dependent and linked to SA economy

• Low population growth rate expected over the next 50 years

• Power supply challenges

• Largely a market share strategy

Eastern region is an attractive opportunity with high growth expected in the near term• Regionalisation of EA

communities• Regulatory developments

create opportunities• Technology savvy consumers

and economy• Oil and gas deposits found

6

We have unique capabilities to unlock these opportunities …

• Extensive Africa footprint, expertise and product set

• Capability to serve multinationals and other large corporates in multiple geographies (e.g. healthcare)

• Solid track record in the SME market and partnering with Affinity groups

• Insurance in a box (life and short-term)

• Maximising current efficiencies and cross-selling opportunities

Life Insurance

• In-country presence key to customer acquisition and risk management

• Low-cost operating model

• Market penetration vs market share acquisition: innovation, regulation, access

• Standard Bank a differentiator to access target customer segments

• Leverage Johannesburg head office for scale and technical resources

Health

• Underwrite on Liberty licenses to capture margin and synergies

• Cross sell to existing Health multinational client base

• Expand health insurance offering to commercially viable target segments

• Leverage central processing for scale, technical resources, expertise

• Health data for risk selection and management

• Develop strategic partnerships with provider networks and other insurers to access all geographies

Short-term insurance

• Business in a Box

• Specialist underwriting including trade credit insurance, motor mechanical warranties, pay-as-go drive insurance, oil & gas

• Leverage skills and centre of excellence in Kenya

• Common IT platform

• Build scale through acquisitions & partnerships

• China opportunity

The business model to succeed

8

Key aspects of our insurance business model

Segment groupsFocus will vary by country, based on

commerciality

Commerciality of segments

• Customer value propositions developed per segment

• Multinational and Corporate clients provide scale

• Regulatory reform will make the corporate business opportunity incrementally more attractive and open to cost-efficient standardised solutions

• Market expansion will also be in the ‘bulk retail’ (worksite / affinities) markets. Customer relevance and affordable products are key to most markets with mainly low-income consumers

• Our ability to service seamlessly across jurisdictions will be a competitive advantage

Multinationals

Corporates

SMEs

Worksites and Affinities

9

• Liberty as an ingredient brand

• Technology• Enablement and

innovation • Scale of markets

facilitates opportunity

• Micro SMEs vs larger SMEs

• Access via intermediaries and partners

• Access and innovation to succeed

• Local relationships –brokers and clients

• Own sales team / consulting

• Expertise• Specialist needs

Capabilities are supported by distribution ability and efficiencies

Corporates SMEs Worksites and Affinities

• Footprint • ‘Local’ knowledge and

expertise• Consistency across

countries• Own sales team /

consulting• Expat solutions

Multinationals

• Business is ‘local’, supported centrally

• 80% standardisation/ 20% localisation

• Speed to market, operational risk management and economies of scale are enabled by a ‘business in a box’ approach

Operations and capability

• Embedded bancassurance and corporate business are low risk opportunities of entry

• Key opportunities, competitive landscape, and operating environment determine next phase of growth

• Greenfields growth and acquisitions are both available as options for entry into targeted jurisdictions

Market entry

• Match Standard Bank’s footprint• Entry method depends on

availability of suitable acquisitions, size of existing players and whether new licenses are being issued

• Use partner licenses where appropriate e.g. Francophone Africa

Expansion

10

Bancassurance, remains a key differentiator

Liberty’s strategy is to partner with the bank to build scale and customer base

11

The outlook informs our strategy

Current Licensed Presence Anticipated 2020 footprint

8 Life licenses3 Short-term licenses9 STANLIB businessesHealth presence in 18 countries

• 4 Liberty licenses (includes Lesotho)• 10 Contracted license, Liberty

administration• 4 Contracted license, Third party

administration

15 Life licenses15 Short-term licenses10 STANLIB businessesHealth presence in 24 countries

• 12 Liberty licenses• 11 Contracted license, Liberty administration• 1 Contracted license, Third party

administration

Progress so far…

13

Operating environment in 2015

We believe our strategy is sufficiently aligned to current trends and opportunities in the market

New businessesEconomic & Political environment• Political stability in all countries, although terrorism risk is

still a concern in Kenya;• Market volatility in Kenya from the end of April – equity

market fell 26% between April and October – short-term bond yields rose +700bps;

• Tanzania and Uganda macroeconomic fundamentals improved – inflation at single digits;

• Business confidence has fallen in Southern Africa; A possible downgrade of SA’s sovereign credit rating could affect the Southern region

• Currency depreciation and ratings downgrade in Zambia

Regulatory developments

• Progress in liberalising Bancassurance regulations in Kenya and Uganda;

• Enhanced importance around TCF and policyholder protection principles in Kenya and Swaziland;

• New regulations in Namibia around insurer prescribed assets and unlisted investments

• Higher scrutiny of tax and other regulatory compliance across geographies/borders, in growth markets of Kenya and Nigeria

Competitive Landscape• M&A and greenfield opportunities explored by SA insurers; • Renewed interest by European Insurers in the African

continent e.g. Prudential & AXA; • Kenya insurers looking to aggressively expand in the East

Africa region;• Underwriting margin pressure• Opportunities from the growth of Chinese and Indian FDI,

particularly in East Africa• Aggressive bonus declarations on deposit administration

business

14

Continued good progress on expanded footprint

Insurance• Gross earnings R152m • VNB R49m

Health (Liberty Health Cover)• CLR 63%• Lives covered R105 000

2009

Insurance• Gross earnings R42m • VNB R9m

Health (Liberty Blue)• CLR 78%• Lives covered 17 000

Licence and people

Additional business lines

Partners

2015

15

Key initiatives delivered in 2015Product Bancassurance

Affinity Partners Other Channels

• Unit-linked pensions products in Kenya• Education Plans• Launch of hospital cash plan in Botswana• SME Coupon Product• Legacy funeral plan launched in Kenya• Retail products Simple Life Plan and

Platinum Life Plan rolled out in Namibia, Swaziland, Botswana and Zambia

• Group Risk product launched in Zambia and Lesotho

• Credit life products launched in Zambia on back of Stanbic partnership

• Kenya Agency licence approved• Working closely with legislators and

regulators in Uganda on reform of insurance legislation

• Transactional channel rollout implemented in Botswana, Namibia and Swaziland

• Banking• Micro finance institutions• Unions• Medical aids• Funeral parlours• Churches• Police and defence forces• Partnership with top motor dealer in Kenya

to sell short-term insurance products

• Franchise model operational in Namibia and Botswana

• Underwriting health business on insurance licences

• Direct Sales Agents remuneration model;• Strategic insurers • Chinese speaking sales agents in East

Africa• Online sales & service platform in Kenya

Building for growth …

17

2016/2017 focus areas

Establish and integrate new businesses

Life

Short-term

Diversify channels

• Tier 2 brokers;• Bancassurance

− Transactional and institutional channels− Kenya and Uganda

• Additional affinities and worksites• Synergies between Liberty Africa Insurance, Health and

Corporate capabilities to enhance multinational, large corporate and SME propositions

• Partner with global insurers without an African footprint to target their multinational clients

• Develop a comprehensive SME proposition – taking into account economic structure in most African countries

• Short-term retail insurance capability in Kenya and Tanzania

• China business community and Chinese insurers

• Nigeria• Lesotho• Tanzania• Zimbabwe

• Botswana• Malawi• Namibia• Nigeria• Zimbabwe

Bulk up existing businesses• Acquisitions• Bolt-on acquisitions• Joint ventures• Stakeholder engagement programmes

• Unit-linked pensions products in Kenya;• Embedded products for Standard Bank in

Kenya, Uganda, Namibia and Botswana • New retail products (annuities) • Pension solutions for the continent

Product

18

Fundamentals are in place, however there are considerations

Political and Economic stability

• New governments – continued terrorist threats

• Currency volatility

Competition

• Impact on margins and risk management practices

• Availability of suitable acquisitions

• Price of acquisitions

Regulatory and tax environment

• Evolving bancassurance legislation

• Transfer pricing

• Governments need for tax revenues

• Introduction of risk based capital models

People

• Skills shortage across Sub-Sahara Africa

• Scale of operations makes succession planning difficult

• Not easy to expatriate

19

• Liberty is committed to capturing the long-term growth in Africa

• Strategic investments on the continent remain a focus

• The short-term challenges are outweighed by the long-term opportunity

• Our core skills and strengths in insurance and investments, and our on-the-ground presence gives us a competitive advantage

• Our bank partner remains a key differentiator for expansion and growth

• Effective and considered deployment of capital to chosen growth markets will drive shareholder value for the future

• Liberty is committed to working with equity partners and regulators to improve access and integrity of wealth solutions

• Stepped up stakeholder engagement to drive brand presence in Africa

In conclusion

Questions

Kenya Investor DayApril 2016

Seelan Gobalsamy

STANLIB Overview

A Leading Investment Business

Active asset managementMulti‐ManagerPassive asset management

We are a multi‐specialist investment company in 10 African countries with business partners in North America, United Kingdom, Europe, Middle East and Asia

R579bn(USD 37bn)Assets under management and administration

INVESTMENTS

31 December 2015

INSTITUTIONAL•10 of the top 20 JSE Companies•4 of the top 6 listed Insurers •R60bn – Parastatals, unions etc•R30bn ‐ Universities

OUR CUSTOMERS

RETAILMore than 500 000 across Africa.

OUR PEOPLE

100+ Investmentprofessionals

With over1500 yearsof collective investment experience

82 Raging Bull Awards92 Morningstar AwardsLevel 2 BBBEE StatusActive asset management

Multi‐ManagerPassive asset management

Asset Management Strategy

Our physical presence in 10 African countriesBest Asset Manager in Frontier Markets

Ghana – Alex Asiedu

Managing Director

Namibia – Brown Amuenje

Managing Director

Botswana – Moipone Lopang

Managing Director

South Sudan – Isaiah Malith

Managing Director

Uganda – Annette Rumanyika

Managing Director

South Africa – Seelan Gobalsamy

CEO, STANLIB

Managing Director

Swaziland – Mandla Ndlovu

Kenya – James Muratha

Managing Director

Lesotho – Kello Rametse

Managing Director

Managing Director

Tanzania – GeofreyMwakagenda

Our multi‐franchise model

Active Fund Management

Alternative Investments

Fixed Interest, Equity, Property and Multi‐Asset capabilities.

Passive Investments

Multi‐Manager Funds

OFFSHORE PARTNERS

Bonds

Cash and Multi‐asset

Equities

REST OF AFRICASOUTH AFRICA

Multi‐Specialist Franchise Model

STANLIB in the Rest of Africa

• High GDP growth rate• Increased political stability and pragmatic economic policy• It has a young, rapidly growing population• Emerging middle‐class• Urbanisation and increasing retail sector

Why are we passionate about Africa?

• Financial market reform attracted international investors• STANLIB offers traditional and alternative investment

options• In the traditional space, there is room for targeted product

development in specific segments• Alternatives focus on:

– Direct Property– Infrastructure– Private Equity

What do we offer Africa?

Closing

10

Leverage multi‐specialist investment capabilities to deliver consistent investment performance

Enhance our product range – alternatives and customised solutions

Build our international distribution capability – build capacity in local distribution

Invest in our people – truly Pan‐African investment professionals

1.

2.

3.

4.

Strategic Objective

Thank You

STANLIB’s Alternatives CapabilitiesKenya Investor Day

Amelia Beattie and Patrick Mamathuba04 April 2016

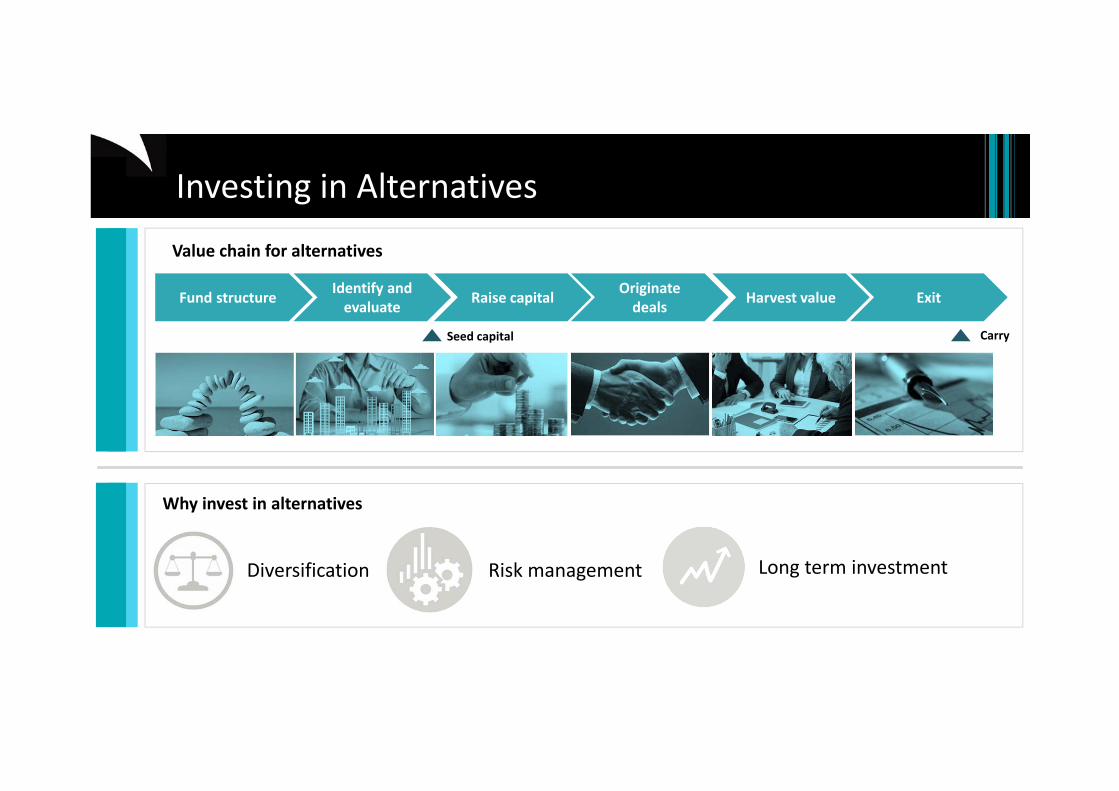

Alternatives overview

Value chain for alternatives

Diversification Risk management Long term investment

Investing in Alternatives

Why invest in alternatives

Fund structure Identify and evaluate Raise capital Originate

deals Harvest value Exit

CarrySeed capital

Alternatives investment team

Amelia Beattie

Patrick Mam

athu

ba

420+Years of collective

investment experience

Experience

Degrees includingMCom, MPhil, BCom(Hons), BAcc(Hons), BSc, BAcc, BCom,

BA(Hons), BA, MSc, PhD

CA (SA) CFA MBA

Qualifications

Direct Property Infrastructure Private Equity (Exeo Capital)

Liberty Property Portfolio

Alex Phakathi

Pan‐Africa Development Fund

Robe

rto Ferreira

Fahari Income‐REIT

Anton Bo

rkum

Ghana Income Fund

Neysa Harilal

Herm

an M

arais

Paul Nguru

Managing Partner Exeo Capital

Partner Exeo Capital

Gregg Babaya

Head of Infrastructure

MoyahaboMpanza

Andy

Louw

Principal Investment Analyst

Senior Partner Exeo Capital

Izak

Strauss

Direct Property Infrastructure Private Equity (Exeo Capital)

Direct property

6

INVESTMENT PHILOSOPHYTo be the Asset Manager of choice for investors with a long‐term investment appetite in quality real estate in carefully chosen economically growing nodes on the African continent

Strategic focus areas

LIBERTY PROPERTYPORTFOLIORemains a key focus area with dedicated investment team to drive investment returns for policyholders and match exposure needs

PAN AFRICA OFFERINGFocus dedicated efforts on building Pan African investment opportunities through creating quality stock in high growth areas

IN‐COUNTRY APABILITIESEnsure that we stay in touch with the market to offer investment solutions for investors to key opportunities and economically growing nodes

Making real estate accessible sustainably

DEVELOPMENT MANAGEMENTFocused property development team to provide development management and leasing management capabilities to grow the portfolio assets under management

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2010 2011 2012 2013 2014 2015Income return Capital growth CPI + 5%

Liberty Property Portfolio returns (gross) 2010 ‐ 2015

• 10.37% total return in 2015• Outperformed benchmark of CPI + 5%

Eastgate Shopping Centre

Promenade Shopping Centre

Liberty Midlands Mall

Liberty Property Portfolio

Sandton City

STANLIB Africa Direct Property Development Fund

Project Location Property Type

Estimated Size (m2)

Fund's Equity (millions)

Project Orca

Tema, Ghana Retail 20 064 $30.3

Project Honour

Lagos, Nigeria Office 44 000 $42.0

Total $ 165.3

Project Diamond

Oweri, Nigeria Retail 14 000 $10.0

Project Masai

Nairobi, Kenya Retail 13 000 $16.7

Project Audit

Accra, Ghana Office 10 200 $15.0

Project Sinatra

Asaba, Nigeria Retail 15 000 $18.6

Project West

Lagos, Nigeria Retail 20 000 $17.7

Project Nile

Kampala, Uganda Retail 13 600 $15.0

Pipeline of investment opportunities

• First listed Kenyan Property Fund (size of capital raise: KSH 3.6Bn)• Offering investors access to the following key benefits:

o A high quality, professionally managed property portfolio, which will yieldo Tax efficient dividend distributions plus capital gains within a regulated

environmento Diversification, transparent pricing, liquidityo Internal and external governance (IFRS reporting)

Trading price of Fahari Income‐REIT (KES)

1819202122232425

List Price Closing Price

Update on Inward Asset Transfers• Greenspan Mall transferred Feb‐16• Transfers of Signature International

and Bay Holdings are underway

Fahari Income‐REIT

Make a difference to peoples’ lives

Bring hope to the communities we serve

Make the planet a better place to live…and translate into creating real value

We build hospitals that provide 385 beds to the children and people of South Africa

Ghana – Meridian Square Mall

In Africa we convert barren land into income generating legacies

Our retail development in Athi River will create 893 construction jobs and 1,155 permanent jobs on completion

Infrastructure

MatureGrowthRamp UpConstructionGreenfield

Investment Stage of Life

Risk

level

Asset

value

Project Life

Multi fund strategy driven by investment life cycle

Yield Fund

PE Funds

Infrastructure strategy

Target project life cycle

Wind farms

Our investments generate a combined 340 MW of power

Solar

80 MW Wind Farm Combined 265MW Solar PV

Infrastructure Private Equity Fund I investments

Investors at final close CommitmentR’million

Commitment%

Total Fund commitments 1 189 100%

61%2%

37%Assets at marketvalueManagement fees &expensesAvailable funds

Investments as at 30/09/2015 Fund shareholding Cost (R’million)

Project Kalkbult 10% 63.5

Kouga Wind Farm 35% 169.2

Project Linde 10% 24.6

Project Dreunberg 20% 96.2

Project Kathu 12.5%˜ 223.0

Total investments 576.5

13%

40%

4%

17%

26%Project KalkbultKouga Wind FarmProject LindeProject DreunbergProject Kathu

Infrastructure Private Equity Fund I summary

Utilisation of funds

Breakdown on value basis

Private Equity

Retains distinct branding and management independence

A 50/50 partnership between STANLIB and the founders of Agrie Vie Private Equity

Introducing Exeo Capital

Sector focus:

Food and agribusiness Household goods manufacturing and distribution

Transport and logistics Specialised financial services

Media and e‐commerce Industrial services Healthcare Private education

Background

• Exeo Capital is a small, independent private equity firm based in Cape Town

• Currently manages Agri‐Vie Fund I ($100m) which achieved first close in 2008

• Invested in 13 deals across East Africa and SADC

• Agri‐Vie Fund I capital raised from 8 global institutional LP’s on three continents: Africa, Europe and North America

• Fund I target is to make 2.5‐3x initial investment and an IRR in USD of ~20%

• Currently raising capital for Agri‐Vie II – First close target $75 million and final close target $175 million

Experienced investors across East and Southern Africa

Agri‐Vie Fund II – pipeline for investments

ZambiaUgandaTanzaniaSouth Africa

RwandaMozambiqueKenyaGhana

$ millions

90

80

70

60

50

40

30

20

10

0Ethiopia

Investment focus:

4

6

2 22 2

2

2

1

Agri‐inputs and services

Storage and logistics

Food, beverage and fibre processing

Food ingredients

In‐closing

• Ability to offer our customers the full spectrum of alternative investments

• Critical to gaining flows in more lucrative asset classes, and driving future profitability

• Increased customer demand for this offering, alternatives industry CAGR of 12% since 1999 (SAVCA/KPMG, 2014)

• Growth is expected to accelerate driven by:

Regulatory changes that have increased the allocation that pension funds can make towards the asset class

Global capital is seeking higher returns in Africa and emerging markets

• Aligned to the Group’s Vision 2020 strategic intent of gaining flows destined for Africa

Concluding remarks

At STANLIB our alternative capabilities deliver real value

INVESTORS SHAREHOLDERS COMMUNITIESConsistently meet/exceed benchmark returns

Build sustainable earning streams

We change the lives of people we touch

Thank you.