Embed Size (px)

DESCRIPTION

The turbulent times that we are currently experiencing will leave an indelible mark on our economic and social landscape. As well as helping to make a practical difference in the communities where we live, now is a critical time to think about the role that money plays in our lives and what the Christian faith has to say about the way that the economic system is structured.

Citation preview

HOW THE CHURCH CAN HELP

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:53 Page 1

2 LIFE BEYOND DEBT

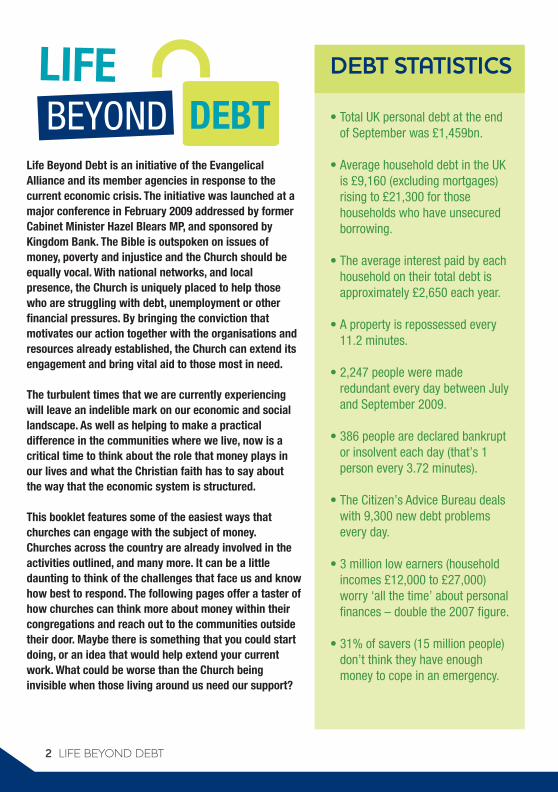

DEBT STATISTICS

• Total UK personal debt at the endof September was £1,459bn.

• Average household debt in the UKis £9,160 (excluding mortgages)rising to £21,300 for thosehouseholds who have unsecuredborrowing.

• The average interest paid by eachhousehold on their total debt isapproximately £2,650 each year.

• A property is repossessed every11.2 minutes.

• 2,247 people were maderedundant every day between Julyand September 2009.

• 386 people are declared bankruptor insolvent each day (that’s 1person every 3.72 minutes).

• The Citizen’s Advice Bureau dealswith 9,300 new debt problemsevery day.

• 3 million low earners (householdincomes £12,000 to £27,000)worry ‘all the time’ about personalfinances – double the 2007 figure.

• 31% of savers (15 million people)don’t think they have enoughmoney to cope in an emergency.

Life Beyond Debt is an initiative of the Evangelical

Alliance and its member agencies in response to the

current economic crisis. The initiative was launched at a

major conference in February 2009 addressed by former

Cabinet Minister Hazel Blears MP, and sponsored by

Kingdom Bank. The Bible is outspoken on issues of

money, poverty and injustice and the Church should be

equally vocal. With national networks, and local

presence, the Church is uniquely placed to help those

who are struggling with debt, unemployment or other

financial pressures. By bringing the conviction that

motivates our action together with the organisations and

resources already established, the Church can extend its

engagement and bring vital aid to those most in need.

The turbulent times that we are currently experiencing

will leave an indelible mark on our economic and social

landscape. As well as helping to make a practical

difference in the communities where we live, now is a

critical time to think about the role that money plays in

our lives and what the Christian faith has to say about

the way that the economic system is structured.

This booklet features some of the easiest ways that

churches can engage with the subject of money.

Churches across the country are already involved in the

activities outlined, and many more. It can be a little

daunting to think of the challenges that face us and know

how best to respond. The following pages offer a taster of

how churches can think more about money within their

congregations and reach out to the communities outside

their door. Maybe there is something that you could start

doing, or an idea that would help extend your current

work. What could be worse than the Church being

invisible when those living around us need our support?

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:53 Page 2

3LIFE BEYOND DEBT

managers of money. The aftermath of a seriousrecession, with its uncertainty and anxiety, seems acrazy time to speak of our stewardship of all Godhas given, of generosity (Haggai 1:3). Yet theprophet Haggai knew that fear of financial insecuritydrains us emotionally and spiritually. He would notallow God to be pushed to the margins, challengingIsrael to restore the temple. Jesus must be Lord ofour finances if he is Lord of all and if we are tospeak of financial freedom in our communities.

Faithful stewardship takes seriously threeaspects of our financial life.

Miraculous provision is made for a woman whosechildren have been seized by a creditor (2 Kings4:1-7). The law commands the cancellation ofdebts, generosity and the release of economicslaves every seven years (Dt 15:1-15). Jesus usesthe cancellation of unpayable debt as a picture offorgiveness (Matt 18:21-35). The Church isuniquely placed to offer the hope of life beyonddebt as well as practical and pastoral support inboth the congregation and the local community.

To speak with integrity the Church has to walkits talk! We are called to be more than good

Debt destroys lives, damages relationships, drives outjoy and lets in fear. No wonder the Bible speaks ofrelease for those shackled by debt!

THE TIMEIS NOW!

3. Lifestyle expectations

How do we plan, spend and save our money? Do our attitudes and lifestyle distinguish us from the

world around us? Is the gravitational pull of our possessions too strong?

1. Personal experiences

Are we struggling with personal debt? Do money worries weigh us down? Do we have skills or

experiences to share to set others free? Are we open to Bible teaching on wealth and possessions?

2. Scripture and spirituality

Whose money is it anyway? Everything comes from God so financial decisions are spiritual decisions.Free from both guilt and greed, we must receive with gratitude and give generously and joyfully.

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:53 Page 3

4 LIFE BEYOND DEBT

In the light of the growing economic crisisgripping the UK, the Church has a clearduty to listen to, and speak up for, thosemost affected. Following in the tradition ofthe Prophets, churches in the UK have longbeen at the forefront of calling for politicalchange to tackle the root causes of povertyand inequality.

A century ago, while William Booth was setting upthe Salvation Army, Seebohm Rowntree wasconducting groundbreaking research to shed lighton the root causes of poverty.

Twenty-five years ago, the churches led theway in challenging the social divisions of the1980s with the publication of ‘Faith in the City’and the establishment of Church Action onPoverty and the Church Urban Fund.

Make Poverty History showed that bymobilising public opinion within the churches andbeyond, we could put pressure on our politicalleaders to bring about policies which could makeglobal poverty history. Our task, and ourchallenge, is now to bring this hope back home.

As the economic crisis deepens it is criticallyimportant that churches understand the role thatthey can play, especially in their owncommunities. And also to hear from God how theycan be a voice to those in positions of politicalinfluence and responsibility, to challenge them toput first the needs of those suffering the effects ofpoverty, debt, homelessness and destitution.Oneexample of this is ‘Get Fair’, which bringstogether a broad alliance of churches andcharities with the simple message: ‘For the sakeof the thousands affected by risingunemployment, debt and damage to relationshipsand family life - it’s time to Get Fair’.

www.getfair.org.uk

The Evangelical Alliance is currently developing amajor report looking at the economic crisis in thelight of Biblical values

”

”

Our task as Christians isnot simply to pull peopleout of the river, but to askwho is throwing them intothe river in the first place(Jim Wallis)

in a time of crisisA prophetic voice

Our task as Christians isnot simply to pull peopleout of the river, but to askwho is throwing them intothe river in the first place(Jim Wallis)

”

”

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:53 Page 4

5LIFE BEYOND DEBT

In the current economic climatethe local church is ideallyplaced to reach out to its localcommunity, offering a range ofhelp to people who may besuffering financially.

Fortunately there are several Christian charitiesthat offer real hope here. For example literallymillions of people will be struggling with debtissues – many will not know where to turn andothers will have gone to fee-charging firms. Butthe expertise of Christian debt counsellors fromCommunity Money Advice [CMA] and ChristiansAgainst Poverty [CAP] is available in an everincreasing number of towns and cities andwhere they are not present people can get helpthrough Credit Action’s sister charity – theConsumer Credit Counselling Service [CCCS].

Credit Action [CA] also produces a range of guidesfor different groupings – such as Single Parentsand Students – which can prove to be thedifference between people being able to makeends meet or sinking into over-indebtedness. Theyalso produce a Redundancy Guide which isavailable in printed form but, like all their guides, itis also downloadable for free fromwww.creditaction.org.uk

Not many Christians realise that Jesus spokemore about money than virtually any othersubject. He knows how important money, or thelack of it, is in our every day lives.

It is therefore essential that not only do we asChristians handle our money with Jesus’ prioritiesand principles but that we offer help to those inour communities who are struggling. Here aresome ideas of going about this:

• Look at the information about CMA and CAP onthe following pages, and contact them to see ifthey have a debt counselling centre nearby. Ifnot consider setting up such a centre throughyour own church.

• If this is not feasible contact Credit Action fordetails of Consumer Credit Counselling Serviceand how you can help ‘hand-hold’ peoplethrough. 0800 027 4995

• Get people within your church trained on how tohelp those in the community with money andbudgeting. Credit Action can provide suchtraining.

• In either event think of ways you can publicisefree debt counselling by using posters or debtcards etc.

• Consider taking a range of CA guides fordistribution in your locality. For example, otherchurches have placed them in libraries anddoctors’ surgeries.

• Take both cards and booklets for giving away inchurch based groups like ‘mothers and toddlers’and youth groups.

• Educate your church – you can find out more onpage 8.

Whatever you decide to do by offering help in thisarea you could literally be a “Godsend” to many inyour community and be able to forge closer linkswith many people at the same time.

Money and Community

Engagement

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:53 Page 5

6 LIFE BEYOND DEBT

Community Money Advice andChristians Against Poverty bothoffer services for churchesseeking to establish debt advicecentres.

If you affiliate with CMA you will be running your ownindependent debt advice centre, so it is vital you have ateam committed to the work, and the backing of yourchurch or community centre leaders. CMA can then providetraining, guidance and practical support, both during yourset-up period and when you are up and running.

When the doors of an advice centre open, you will bemeeting and helping people whose lives are often tornapart by debt. Relationship breakdowns, loss of homes,addictions, shame, fear, anger and guilt, are all potentialconsequences of indebtedness. Your clients will bringvarious problems to you, from a fixed or low income clientwith relatively small debts, who can sometimes be helpedby claiming overlooked state benefits, through to well-paidexecutives who have lost a job or been trapped byborrowing tens of thousands of pounds on credit.

Undertaking debt advice work is a big commitment, butif you decide it is right for you, CMA can provide theexpertise to help you establish an effective, professionalservice, and you’ll become part of a family of over ninetycentres across England and Wales that share your vision.

The rewards? Seeing people who have been crushed byfear start to find hope again; seeing people, who have beentrapped by debt released and enabled to manage moneywell in the future; seeing lives transformed.

You are life savers. I didn’t knowwhat to do or where to go and wasready to do something stupid. You haveshown me that my life is worth living

Mr D. CMA Client

“ “Practical action you can take

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 6

7LIFE BEYOND DEBT

Sarah’s StoryWe were in really dreadful debt. We had nomoney at all and struggled to do day to daythings such as feeding our four year olddaughter, Kayleigh. We were trying to pay backmore than we had coming in.

A friend introduced us to Andy Jackson fromChristians Against Poverty (CAP) Bracknell, andfrom that moment on everything changed –literally everything.

We were given a budget, which meant wecould afford to feed Kayleigh and get her thenew clothes that she needed.

We could suddenly do all the things that aparent is meant to do for their child. We could eatas well, which was amazing for us because wehad been living on toast.

Andy got me a place at ‘Sparklers,’ which isthe mother and toddler group at CAP’s partnerchurch in Bracknell. I’m a very nervous personso I brought a really close friend, Carly, alongwith me. It was wonderful and we started goingall the time. Then Carly asked me if I wanted togo to church with her and her partner, John, onSunday. I agreed and came to an event called‘The Xmas Factor’ where J. John was speaking.It really spoke out to me. During the appeal, Ifound myself standing up wanting to ask Jesusinto my life.

I was so impacted by the words and it allseemed so right. Then, at Easter, I got baptisedalong with Carly and John, which was fantastic!

In May, life got really hard when our son wasstillborn. I was devastated, but the church neverleft us. Other friends in my life have come andgone, but friends from church stuck by usthrough thick and thin and made us see that wecould actually make it through. With their helpand prayers we have done.

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 7

8 LIFE BEYOND DEBT

With around 2,350verses on wealthand possessions –compared, it isoften said, toaround 500 verseseach on faith andprayer – it isinteresting that thechurch is so silenton the subject!

Those verses speak in many different voices.They tell of the goodness and abundance ofGod’s gifts, challenging greed and thetemptation to find identity in acquiring evermore stuff. The Bible speaks of release for thepoor, for those in debt and challenges us togratitude and contentment, reminding us thatGod is the ultimate owner of all we have and ofthe responsibility entrusted to us in wealth.

If we are to offer hope to those in debt in ourcongregations and communities we must breakthe sound of silence. We must give peoplepermission to speak about money and tounderstand the richness of what the Bible hasto say in the churches’ preaching, teaching andpastoral ministry.

The Sound Of Silence...

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 8

9LIFE BEYOND DEBT

1.�

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

Visit: www.stewardship.org.uk/money

Churches must:• Be faithful to the breadth and depth ofbiblical teaching on money andpossessions. Talk money when the Bibledoes, not over-spiritualising the texts ormaking them serve our lifestyle choices.

• Connect the spiritual life with how wehandle money and its power in our lives(Luke 16:10). Money talk should be anormal part of preaching, teaching,discipleship, mentoring and spiritualdirection.

• Give people permission to talk aboutmoney, to share their hopes, fears andjoys. Leaders must preach with honesty,humour, sensitivity and vulnerability asthose on a shared journey, not expertswho have reached a destination.

• Address money holistically: spendingand saving; the wise use of credit; and thedangers of debt. Simple financial planning,budgeting and money managementshould sit easily in our teaching ministrywith prayer or spiritual gifts.

• Teach the grace of generosity and thediscipline of giving as the hallmark orlitmus test of authentic discipleshiparound money. Giving talk must not beconstrained by the annual stewardshipcampaign or the capital appeal.

• Support clergy and leaders in thispreaching and teaching ministry, knowingthat they struggle with the same concernsas their congregations.

• Establish simple systems of pastoraland practical care for those who areburdened by debt or facing the financialimpact of circumstances.

Money Makeover12 steps to better looking finances!

Allocate time: money management does notjust happen!Develop a plan: know what you want money toachieve for you.Talk: communicate with your partner and olderchildren. Don’t be too afraid, too embarrassed ortoo proud to ask for help or take advice.Prepare a budget: know what comes in, whatgoes out – and deal with the difference. Makesure you receive benefits you are entitled to.Think cash: You may use Direct Debits or acredit for big ticket items but use cash as muchas you can to control the variables: all the smallthings that mount up!Review regularly: a budget is only useful if wecheck out how we are doing. Be aware of the pressures: our kids,advertising, our expectations, our peers.Spend less than you earn: sounds obvious butit takes effort and practice. Pay bills on time: again obvious, but we can beso busy, so anxious or just out of control – andthat costs us money. Find a system that worksfor you.Do your research: stay on top of your costs andlook for ways of saving and increasing income. Get help if you are in debt: don’t wait, don’tdelay, don’t despair – but don’t think it will goaway. It won’t. Expect the unexpected: stay alert, have anemergency fund if you can.

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 9

10 LIFE BEYOND DEBT

Sometimes as Christians we often don’tlike to hear the harder messages Jesusspoke. We like to focus on the Jesus whois our friend, who carries our burdens,who comforts and protects.

But what about the Jesus who called us to denyourselves to follow him (Luke 9:23)? The Jesuswho loved the rich young ruler, but wasn’t going tomake his message more palatable by telling theman that he didn’t actually have to sell everythingand give it to the poor (Mark 9:21)? The Jesuswho tells us to seek first God’s kingdom and thatstuff like food and clothing will follow (Matthew6:33)? Did he just say this to make life difficultand miserable for his followers?

Even though we live in a world today wheremany people in the West own more than they everhave before, the idea that possessions don’t equalhappiness was just as true in the first century as itis today. Jesus knew full well the hold thatpossessions can have on people’s lives.

Take, for example, the rich young rulermentioned earlier: his identity was so tied up inhis belongings that he could not give them up,despite the promise of treasure in heaven. Howtrue is this for people today? We allow ourselvesto be defined by the status symbols that are ourcars, the size of our houses, the exotic locations ofour holidays.

Simplify your life

Could you Simplify your life? Find out more at: www.simplify.org.uk

We may declare otherwise but these things canquickly become more important to us than putting God first. We fail to take seriously Jesus’words, ‘Do not store up for yourselves treasureson earth… but store up for yourselves treasuresin heaven… for where your treasure is, thereyour heart also will be.’ Jesus didn’t say thatmoney and possessions are inherently wrong.Rather, our use of them needs to be directedtowards putting God first, making him ourtreasure rather than our belongings. So, forexample, in Luke 8:3 we see that Jesus relied onthe wealth of women to support his ministry.Jesus certainly knew how to enjoy a celebratoryfeast for a special occasion with friends, and hedoesn’t want us to stop enjoying life either.

Our culture has become so tied to itspossessions that we no longer realise the holdthey have over us. Perhaps, too, we are so usedto having what we want whenever we want itthat we have lost the value of a feast – of savingsome things for special occasions. Taking time tore-evaluate how we use our money andbelongings might turn out to be releasing. Wemay realise what we can do without and how wecan more effectively use what we do have forGod’s purposes. With the money we save we canbe generous, providing support for people weknow who are in debt, or helping to resourceministries that offer a helping hand.

We might just find that this isn’t aboutdogmatic asceticism, a desire to take all the funout of life, but that actually in simplifying ourlifestyles, we discover more about what Jesusmeant when he said he had come to give us lifein all its fullness, life that finds its identity firstand foremost in him, and not in what we own.

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 10

11LIFE BEYOND DEBT

Credit unions are financial co-operativesowned and controlled by their members. Theyoffer savings and great value loans plus they arelocal, ethical and know what their memberswant. Many credit unions now offer a range ofservices including current accounts, benefitsdirect and ISAs.

Because credit unions have a ‘common bond’which determines who can join, this bringscommunity into financial transactions. You arelending to, or borrowing from, people you are inrelationship with. This is often based on an areawhere people live or who you work for.www.abcul.coop

Money ministries – a preventativeapproach: If a debt advice centre is toomuch, can you consider a ‘money ministry’in your church? A money ministry stressesprevention as well as cure. It focuses onbudgeting – a key step for those in debt anda key skill for all. Stewardship offersPersonal Budget Coach training. A moneyministry also addresses good moneymanagement and rich Biblical perspectiveon money through preaching resources andcourses. Stewardship can provide detailsand resources to equip your money ministry.www.stewardship.org.uk/money

Charity foodbanks across the UK arefeeding an increasing number of people infinancial difficulty as the recession continuesto bite. The response of churches andcommunities to this growing need has enabledUK foodbanks to feed over 24,000 people inthe last year.

The Trussell Trust’s foodbank network hasexperienced a 71% growth in the number ofpeople fed compared to 2008, and an evengreater increase in enquiries from churcheswanting to set up foodbanks in their own town. www.trusselltrust.org

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 11

Useful websiteswww.simplify.org.ukwww.stewardship.org/recessionwww.creditaction.org.ukwww.crownuk.org www.fsa.gov.uk

Debt helpCCCS: 0800 027 4995Full details of how to set-up a debt advicecentre are available through Community Money Advice or Christians Against Poverty.Christians Against Poverty: www.capuk.org Community Money Advice:www.communitymoneyadvice.com Citizens Advice Bureau:www.adviceguide.org.uk

Find out more

www.eauk.org/lifebeyonddebtwww.stewardship.org.uk/money

Books to readYour Money and your life – Keith TondeurYour Money Counts – Mark Lloydbottom60 Minute Debt Buster – Katie ClarkeThe Money Secret – Rob ParsonsThe Money Revolution – John Preston

Resources‘The Bible & Money’ Bible Study (Jubilee Centre)Quidz In (Care for the Family) Seasons of Giving (Stewardship)Crown Financial Ministries

If you or your church would likecopies of this booklet to distributeplease [email protected]

LifeBeyondDebt-A5 Howard:Layout 1 02/12/2009 16:54 Page 12