Embed Size (px)

Citation preview

Life is a journey. Make it great.

43

Managing and growingyour wealth

KNOWLEDGE PATH CHOICEVISION

The financial resourcesfor the lifestyle you want

Growing your wealth for the lifestyle you want does not happen by chance. It results from careful planning and wise investment.

A sound financial plan is your first step to achieving your goals such as buying your first property, giving your kids a sound education, or retiring when you want to. While you build the resources to fulfill your life’s goals, you also want to ensure that your money continues to work hard for you even in varying economic situations.

Invest regularly to benefit from fluctuations

Good asset allocation helps grow your wealth steadily

Review your portfolio regularly

Grow your wealth with compound interest

Many people know how to build wealth simply by accumulating savings. But if you are unable to add value to your savings, the overall value of your assets will gradually be eroded by inflation, undermining all your efforts. It takes careful and considered planning to build wealth and overcome the effects of inflation.

Among seven Asian regions surveyed, Chinese people have the third strongest tendency to save. 48% of Chinese interviewees said that they would increase their rate of savings in the next six months. While savings and accumulating wealth are important, the key to adding value lies in consistent and sustainable wealth management.

Source: HSBC Asian Insurance Monitor 2011

China ranks the 3rd in the Asian region in saving for the future

67

61 2

4 53

74

96

12

6

6

14

61 48 41 33

5730

49

25

52474433

26

Increasesavings

Maintaincurrent level

Decreasesaving

Stop saving

Dollar-cost averaging may help manage market risk

65

4,000,0001,000,000 1,500,000 2,000,000 2,500,000 3,000,000 3,500,000500,0000

6000,000

6000,000

6000,000 1,514,900

684,085

179,646

2,883,261

Save HK$5,000 per month for 10 years and let it grow(Assuming 5% p.a.return)

10 years

20 years

30 years

40 years Total Savings

(RMB)

By investing fixed amounts regularly, you can take advantage of “dollar cost averaging”. This means that if you are buying funds, when the price rises, you buy fewer units and when the price drops, you buy more.

So over time, regardless of whether the price of the fund you are buying rises or falls, the average price you pay for each unit is likely to be lower than the market price. This may help increase the long-term return on your investment.

The graph above shows that for the 10 years from 2001 to 2010, the Hang Seng Index recorded an overall increase. However, there were sharp fluctuations, especially between 2003 and 2009, which had made many investors worried. If you had used dollar-cost averaging during that period to invest regular amounts in a tracking fund each month, you could have enjoyed potential capital gain with less volatility.

“Asset allocation” means diversifying and balancing the risk of your investments among different assets. A winning basketball team has a mix of three-point shooters, offensive players and defensive players. The same goes for a winning portfolio. Just as dollar-cost averaging may help smooth out the fluctuations in market prices, careful asset allocation diversifies your investments across different kinds of assets to ”smooth out” the rises and falls in different assets and create a more balanced portfolio for all market conditions.

Nothing in life stands still – especially not in today’s dynamic global economy. So no matter what investment strategy you use, it is important to review your portfolio regularly and adjust your mix of investments as needed.

As you progress through the different life stages, your responsibilities and priorities will change. Your appetite for risk may also change as you grow older. That is why it′s good to have a capable advisor you can turn to to help you adjust your asset allocation. Your Relationship Managers will be glad to support you and help you review your portfolio periodically, so you can make the right changes at the right time for the right reasons.

Most people understand that investing their capital can lead to potentially greater wealth. However, if you simply invest your money in equities and expect to double your earnings in a short time, the risk is much higher. It is also not easy to maintain the momentum of growing for the long-term.

Albert Einstein said, “The most powerful force in the universe is compound interest.” Indeed, an effective savings plan needs a longer period of time for the power of compound interest to work to your advantage.

For example, let’s say you save RMB 5,000 a month for 10 years – the total amount you accumulate is RMB 600,000. If you earn 5% interest each year on your savings, after 10 years you will have accumulated RMB 779,645 - almost RMB 180,000 more! By the 40th year, that sum will reach RMB 3,483,261.

That’s the power of compound interest, the force you want to harness to build your wealth for the long term. The longer you invest your capital, the better your results will be.

6000,000

年份

Average bidprice of atracking fund

HSI†

250

200

150

100

50

02001 2002 2003 2004 2005 2006

35,000

30,000

25,000

20,000

15,000

10,000

5,000

2007 2008 2009 2010 2011

Dollar-cost averaging*Defnition:buy more units when the price is lower and fewer units when the price is higherand may benefit from a lower average cost in the long run

the technique does not guarantee a profit or protect you from suffering a loss in a declining market.

†Source: AASTOCKS

HK% India% China% Singapore% Korea% Malaysia% Taiwan%

TimeCapital

Capital Gain

HSIUSD

*

KNOWLEDGE PATH CHOICEVISION KNOWLEDGE PATH CHOICEVISION

How to build your wealth over time

Plans to save innext 6 months

KNOWLEDGE PATH CHOICEVISIONKNOWLEDGE PATH CHOICEVISION

How to select the productsyou need to achieve your goals

Figuring out your needs in wealth growth will help you select the right products.

How to help reach your wealth goals

87

1 Dividends are not guaranteed.Investment involves risks. The income (if any) from investment choices may go down as well as up.Insurance policy owner shall take all the investment risk.

2

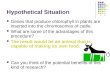

The path to growing your wealth effectively is to follow three principles: start early, be consistent and use the right tool for your needs at each stage of your life.

Start early

Be consistent

Use the right tool at the right time

Target Wealth

Irregular savingsbehavior

Start Late

Time

$

Regular saving

1

1

2

2

Many people stop their investment planning particularly during market downturns. By doing this, they often miss out on opportunities to invest at lower prices. If you stick to your plan and keep moving ahead consistently, you can spread your risks and grow your wealth for the long-term through dollar-cost averaging and careful asset allocation.

With good asset allocation and regular reviews of your portfolio with your Relationship Manager, you can adjust your portfolio to meet your needs at different stages of your life and in different market conditions. This helps you keep your momentum going to achieve your long-term financial goals.

The earlier you start investing, the sooner you can get the power of compound interest working for you to build value, earn even greater returns and make your money work harder for you.

Note: Please note that your savings returns may go down as well as up. The diagram and information shown are hypothetical and for illustration only. Please contact your Relationship Manager for professional advice.

Note: This document is not provided for sales purpose. The information shown in this document is hypothetical and for illustration only. It is not intended to constitute a recommendation or advice to any customers and is not intended as a substitute for professional advice. You should not act on any information in this document without seeking specific professional advice. Please contact your Relationship Manager for addressing your wealth management needs.

Secured wealth accumulation

Partially Withdrawal

Enhance potential returns

Flexibility

You will need your savings to have guaranteed returns.

You will need the flexibility to withdraw cash at important life stages.

You will need your money to work harder for you to counter the low-interest-rate environment.

You will need flexible payment and return ways to meet your needs at different times.

Your needs in wealth growth may include

33

Disclaimer:

This document has been distributed by HSBC Bank (China) Company Limited (the “Bank”). It is not

intended for anyone other than the recipient and should not be distributed by the recipient to any other

persons. It shall not be copied, reproduced, transmitted or further distributed.

Whilst every care has been taken in preparing this document, neither the Bank nor any other HSBC Group

member(s) makes any guarantee, representation or warranty or accepts any responsibility or liability as to

its accuracy or completeness. Except as specifically indicated, the expressions of opinion are those of the

Bank and/or the relevant HSBC Group member(s) only and are subject to change without notice.

The information contained in this document has not been reviewed in the light of your personal financial

circumstances. Neither the Bank nor any other HSBC Group member(s) is providing any financial or

investment advice. The information is not and should not be construed as an offer to sell or a solicitation

for an offer to buy any financial products, and should not be considered as investment advice.

Some of the information in this document is derived from third party sources as specified at the relevant

places where such information is set out. The Bank believes such information to be reliable but it has not

independently verified.