Embed Size (px)

Citation preview

f

Lifelong Learning Plan (LLP)

L / RC4112 (E) Rev. 17 canada.ca/taxes

– 1 –

NOTE: In th is publ icat ion, the text inser ted between square brackets represents the regular pr in t in format ion.

Is this guide for you? Use th is guide i f you want informat ion about par t ic ipat ing in the L i fe long Learning Plan (LLP).

The LLP al lows you to wi thdraw amounts f rom your regis tered ret i rement savings plans (RRSPs) to f inance t ra in ing or educat ion for you or your spouse or common- law par tner . You do not have to inc lude the wi thdrawn amounts in your income, and the RRSP issuer wi l l not wi thhold tax on these amounts.

Over your repayment per iod (general ly 10 years) , you have to repay to your RRSP or PRPP or both the amounts you wi thdrew under the LLP. Any amount that you do not repay when due wi l l be inc luded in your income for the year i t was due.

– 2 –

The def in i t ions sect ion on page 6 [4] g ives general explanat ions of the terms we use. Chapter 1 g ives in format ion on how the LLP works. Chapter 2 expla ins how to repay wi thdrawals under the LLP.

Our publ icat ions and personal ized correspondence are avai lable in brai l le , large pr int , e- text , or MP3 for those who have a v isual impairment . F ind more in format ion at canada.ca/cra-mult iple-formats or by cal l ing 1-800-959-8281 .

La vers ion f rançaise de ce guide est in t i tu lée RÉGIME D 'ENCOURAGEMENT À L 'ÉDUCATION PERMANENTE (REEP).

Unless otherwise stated, a l l legis lat ive references are to the INCOME TAX ACT and the INCOME TAX REGULATIONS.

– 3 –

Table of contents Page

Defin i t ions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . …6 [4]

Chapter 1 – Par t ic ipat ing in the LLP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 [5]

Who can par t ic ipate in the LLP? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 [6]

What condi t ions does the LLP student have to meet? . . . . . . . . . . . . . 16 [6]

How much you can wi thdraw . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21 [7]

When can you make LLP wi thdrawals? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 [7]

How to make an LLP wi thdrawal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 [7]

How the wi thdrawal f rom your RRSP af fects your RRSP/PRPP deduct ion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 [8]

What happens i f the LLP student leaves the educat ional program? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 [8]

Can an LLP wi thdrawal be cancel led. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 [9]

– 4 –

Page

How to cancel your LLP wi thdrawal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 [9]

Quest ions you may have . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 [10]

Chapter 2 – Repaying your wi thdrawals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40 [10]

When and how much to repay . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 [10]

How to make your repayments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 [12]

Contr ibut ions you cannot designate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47 [12]

Si tuat ions when the repayments have to be made in less than 10 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 [13]

Appendix – Ef fect of LLP on RRSP deduct ions . . . . . . . . . . . . . . . . . . . . . . . . 63 [15]

Onl ine serv ices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 [16]

My Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 [16]

– 5 –

Page

MyCRA – Mobi le app . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69 [16]

Electronic payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71 [16]

For more informat ion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71 [17]

What i f you need help? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71 [17]

Forms and publ icat ions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72 [17]

Tax Informat ion Phone Serv ice (TIPS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73 [17]

Teletypewri ter (TTY) users . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73 [17]

Serv ice compla ints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73 [17]

Repr isal complaint . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 [17]

Tax informat ion v ideos . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 [17]

– 6 –

Definitions These def in i t ions prov ide a general explanat ion of the terms that we use in th is guide.

Annuitant – general ly , an annui tant of an RRSP is the person for whom the plan provides a ret i rement income.

Common-law partner – a person who is not your spouse (see the def in i t ion of spouse on page 10 [4]) , wi th whom you are l iv ing in a conjugal re lat ionship, and to whom at least one of the fo l lowing s i tuat ions appl ies. He or she:

a) has been l iv ing wi th you in a conjugal re lat ionship and th is current re lat ionship has lasted at least 12 cont inuous months;

b) is the parent of your ch i ld by b i r th or adopt ion; or

c) has custody and contro l o f your ch i ld (or had custody and contro l immediate ly before the chi ld turned 19 years of age) and your chi ld is whol ly dependent on that person for support .

– 7 –

Note In th is def in i t ion, "12 cont inuous months" inc ludes any per iod you were separated for less than 90 days because of a breakdown in the re lat ionship.

Designated educational inst i tut ion – Designated educat ional inst i tut ions inc lude:

• Canadian univers i t ies, col leges, and other educat ional inst i tu t ions ;

• Canadian educat ional inst i tu t ions cer t i f ied by Employment and Socia l Development Canada (ESDC) prov id ing courses that develop or improve sk i l ls in an occupat ion, other than courses designed for univers i ty credi t ;

• Univers i t ies outs ide Canada where the student is enrol led in a course that lasts at least three consecut ive weeks and leads to a degree at the bachelor level or h igher ;

• Univers i t ies, col leges, or other educat ional inst i tu t ions in the Uni ted States that g ive courses at the post-secondary school level i f the student is l iv ing in Canada (near the border) throughout the year and commutes to that inst i tu t ion.

– 8 –

LLP balance – your LLP balance, at any t ime, is the tota l o f a l l e l ig ib le amounts you have wi thdrawn f rom your RRSPs under the LLP, minus the tota l o f a l l amounts you have repaid to your RRSP or PRPP or both or inc luded in your income.

LLP student – th is is the indiv idual whose educat ion you are f inancing under the LLP. I t can be you or your spouse or common- law par tner, but not your chi ld or the chi ld of your spouse or common- law par tner. You have to par t ic ipate in the LLP for the same LLP student each year unt i l the year af ter you have reduced your LLP balance to zero.

LLP withdrawal – th is is an amount you wi thdraw f rom your RRSPs under the LLP.

Part icipat ion period – your LLP par t ic ipat ion per iod star ts on January 1 of the year you make an e l ig ib le wi thdrawal f rom your RRSP and ends in the year your LLP balance is zero.

Pooled registered pension plan (PRPP) – a ret i rement savings p lan to which you or your employer or both can contr ibute. Any income earned in the PRPP is usual ly exempt f rom tax as long as i t remains in the plan.

– 9 –

Qualifying student – for the purposes of the LLP, for a month in a taxat ion year af ter 2016 means an indiv idual who in the month is enrol led in a qual i fy ing educat ional program as a fu l l - t ime student at a designated educat ional inst i tu t ion, and i f requested by the Min is ter has provided proof of enrolment by f i l ing a cer t i f icate in prescr ibed form issued by the designated educat ional inst i tu t ion and contain ing prescr ibed in format ion. I f the indiv idual is enro l led at an educat ional inst i tut ion cer t i f ied by the Min is ter of Employment and Socia l Development, the indiv idual is 16 years of age before the end of the year and is enrol led in the program to obta in sk i l ls for , or improved the indiv idual 's sk i l ls in , an occupat ion .

Repayment period – the repayment per iod star ts in the second, th i rd, four th, or f i f th year af ter the year of the f i rs t wi thdrawal and ends when the LLP balance is zero.

RRSP deduction l imit – the maximum amount you can deduct f rom contr ibut ions you made to your RRSP, PRPP or SPP or to your spouse's or common- law par tner 's RRSP or SPP for a year (exc luding t ransfers to your RRSPs of cer ta in types of qual i fy ing income). The calculat ion is based, in part , on your earned income in the previous year. PAs, PSPAs, PARs, and your unused RRSP

– 10 –

deduct ion room at the end of the prev ious year are a lso used to calculate the l imi t .

Specif ied pension plan (SPP) – a pension plan or s imi lar arrangement that has been prescr ibed under the INCOME TAX REGULATIONS as a "speci f ied pension plan" for purposes of the INCOME TAX ACT (current ly the Saskatchewan Pension Plan is the only arrangement prescr ibed to be a speci f ied pension plan) .

Spouse – a person to whom you are legal ly marr ied.

Chapter 1 – Participating in the LLP The Li fe long Learning Plan (LLP) a l lows you to wi thdraw up to $10,000 in a calendar year f rom your regis tered ret i rement savings p lans (RRSPs) to f inance fu l l - t ime t ra in ing or educat ion for you or your spouse or common- law par tner. You cannot par t ic ipate in the LLP to f inance your chi ldren 's t ra in ing or educat ion, or the t ra in ing or educat ion of your spouse's or common- law par tner 's chi ldren. As long as you meet the LLP condi t ions every year , you can wi thdraw amounts f rom your RRSPs unt i l January of the four th calendar year af ter the

– 11 –

year you made your f i rs t LLP wi thdrawal . You cannot wi thdraw more than $20,000 in tota l .

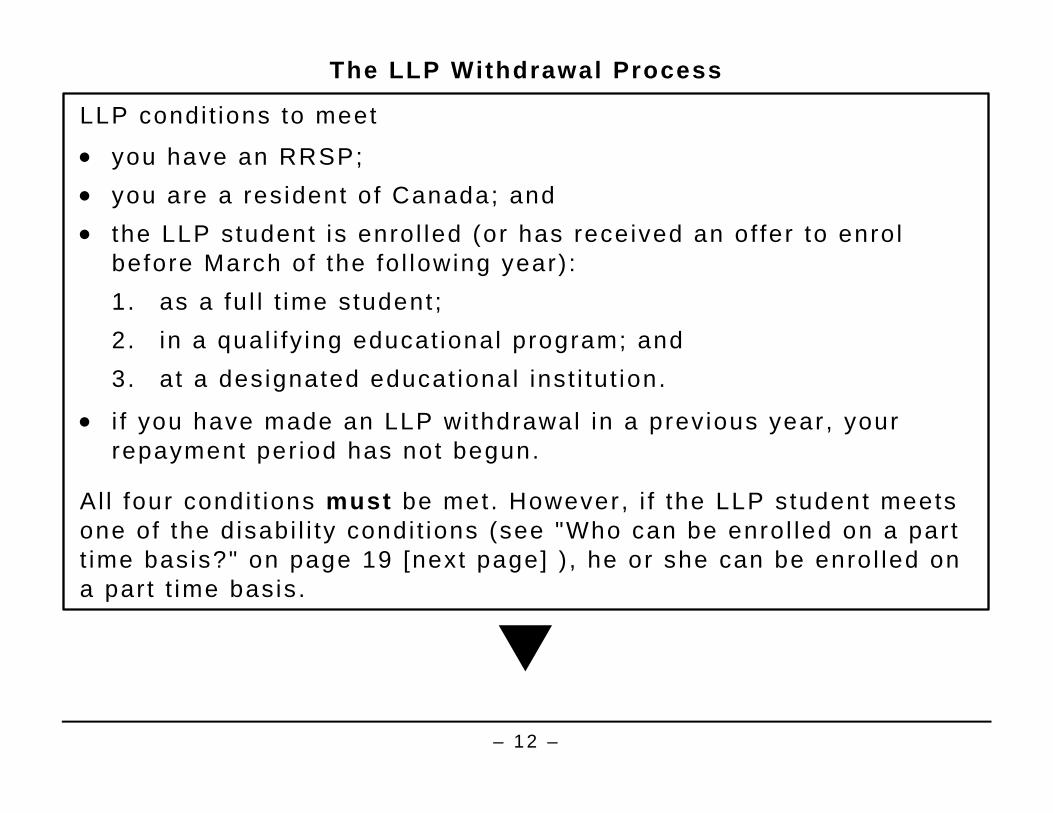

You cannot wi thdraw funds f rom an SPP or a PRPP under the LLP. However, SPP and PRPP contr ibut ions can be designated as an LLP repayment. You do not have to inc lude the wi thdrawn amounts in your income, and the RRSP issuer wi l l not wi thhold tax on these amounts. You have to repay these wi thdrawals to your RRSP or PRPP or both general ly wi th in 10 years. Any amount that you do not repay when i t is due wi l l be inc luded in your income for the year i t was due. This chapter expla ins the condi t ions that you and the LLP student have to meet to par t ic ipate in the LLP, and how to make an LLP wi thdrawal . The char t below summarizes the LLP wi thdrawal process.

– 12 –

The LLP Withdrawal Process

LLP condi t ions to meet

• you have an RRSP; • you are a resident of Canada; and • the LLP student is enrol led (or has received an of fer to enrol

before March of the fo l lowing year) : 1 . as a fu l l t ime student ; 2 . in a qual i fy ing educat ional program; and 3. at a designated educat ional inst i tut ion.

• i f you have made an LLP wi thdrawal in a prev ious year , your repayment per iod has not begun.

Al l four condi t ions must be met. However, i f the LLP student meets one of the d isabi l i ty condi t ions (see "Who can be enrol led on a par t t ime basis?" on page 19 [next page] ) , he or she can be enrol led on a par t t ime basis .

– 13 –

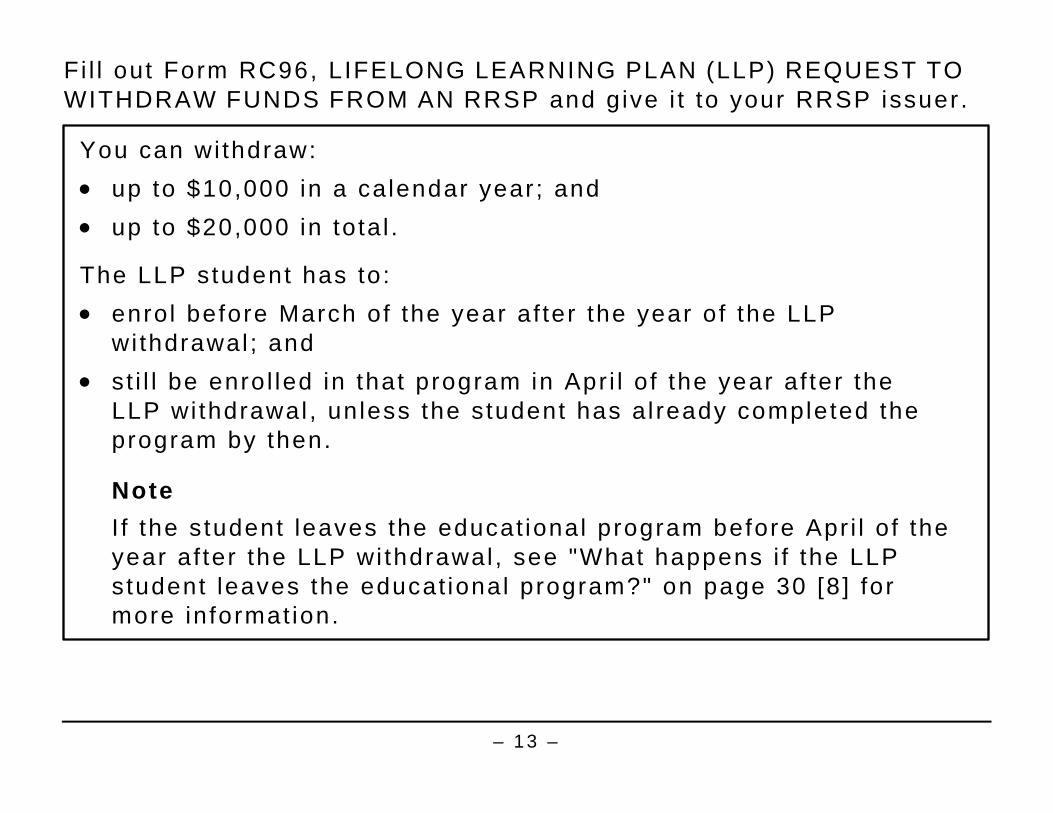

F i l l out Form RC96, LIFELONG LEARNING PLAN (LLP) REQUEST TO WITHDRAW FUNDS FROM AN RRSP and give i t to your RRSP issuer .

You can wi thdraw: • up to $10,000 in a calendar year ; and • up to $20,000 in tota l .

The LLP student has to: • enrol before March of the year af ter the year of the LLP

wi thdrawal ; and • s t i l l be enro l led in that program in Apr i l o f the year af ter the

LLP wi thdrawal , unless the student has al ready completed the program by then.

Note I f the student leaves the educat ional program before Apr i l o f the year af ter the LLP wi thdrawal , see "What happens i f the LLP student leaves the educat ional program?" on page 30 [8] for more in format ion.

– 14 –

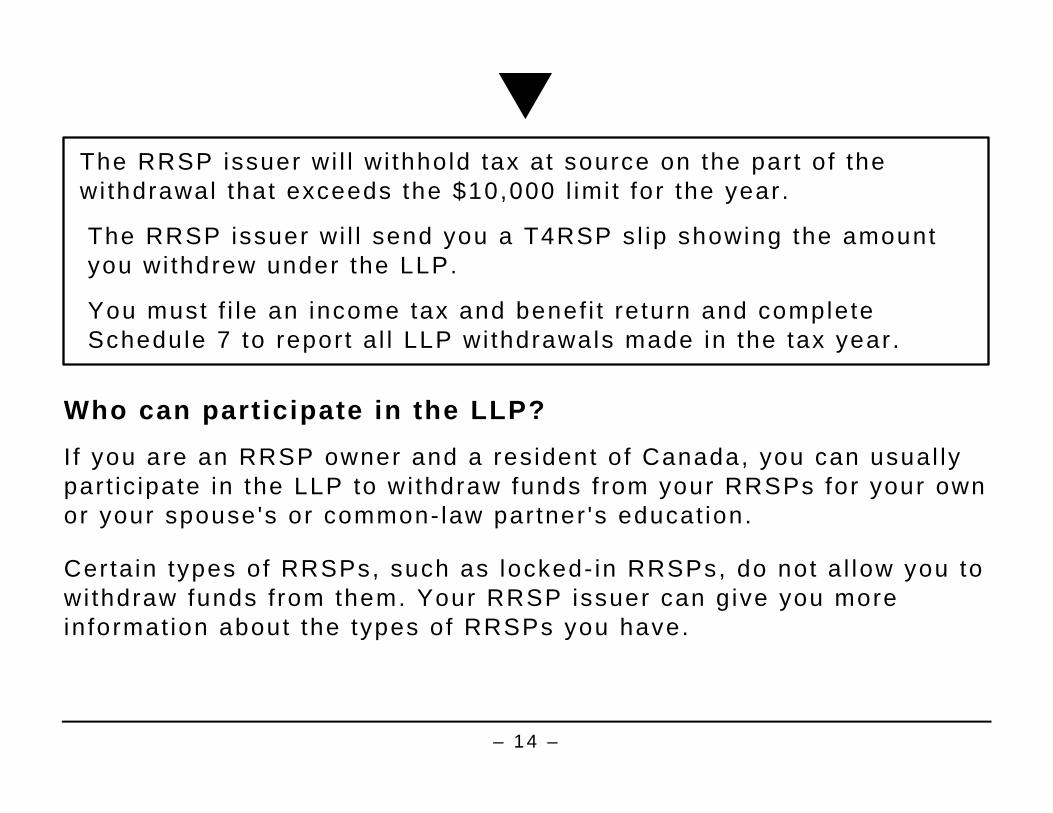

The RRSP issuer wi l l wi thhold tax at source on the par t o f the wi thdrawal that exceeds the $10,000 l imi t for the year .

The RRSP issuer wi l l send you a T4RSP s l ip showing the amount you wi thdrew under the LLP.

You must f i le an income tax and benef i t re turn and complete Schedule 7 to repor t a l l LLP wi thdrawals made in the tax year .

Who can participate in the LLP? I f you are an RRSP owner and a resident of Canada, you can usual ly par t ic ipate in the LLP to wi thdraw funds f rom your RRSPs for your own or your spouse's or common- law par tner 's educat ion.

Certa in types of RRSPs, such as locked- in RRSPs, do not a l low you to wi thdraw funds f rom them. Your RRSP issuer can give you more in format ion about the types of RRSPs you have.

– 15 –

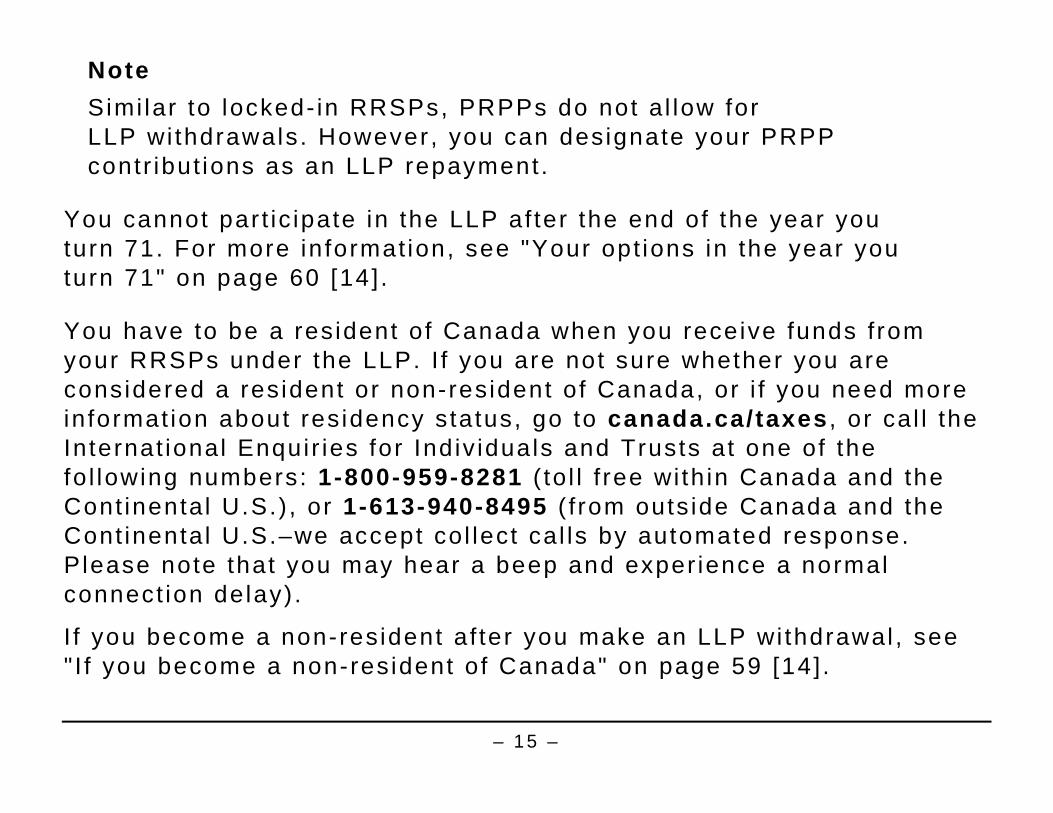

Note Simi lar to locked- in RRSPs, PRPPs do not a l low for LLP wi thdrawals. However, you can designate your PRPP contr ibut ions as an LLP repayment.

You cannot par t ic ipate in the LLP af ter the end of the year you turn 71. For more in format ion, see "Your opt ions in the year you turn 71" on page 60 [14] .

You have to be a resident of Canada when you receive funds f rom your RRSPs under the LLP. I f you are not sure whether you are considered a resident or non-resident of Canada, or i f you need more in format ion about residency status, go to canada.ca/taxes , or cal l the Internat ional Enquir ies for Indiv iduals and Trusts at one of the fo l lowing numbers: 1-800-959-8281 ( to l l f ree wi th in Canada and the Cont inental U.S.) , or 1-613-940-8495 ( f rom outs ide Canada and the Cont inental U.S.–we accept col lect cal ls by automated response. Please note that you may hear a beep and exper ience a normal connect ion delay) .

I f you become a non-resident af ter you make an LLP wi thdrawal , see " I f you become a non-resident of Canada" on page 59 [14] .

– 16 –

What conditions does the LLP student have to meet? The LLP student can be you or your spouse or common- law par tner. You cannot name your chi ld or the chi ld of your spouse or common-law par tner as an LLP student .

The LLP student must enrol on a ful l - t ime basis in a quali fying educational program a t a designated educational inst i tut ion .

I f the LLP student meets the d isabi l i ty condi t ions, the student can enrol on a par t - t ime basis (see "Who can be enrol led on a part - t ime basis?" on page 19 [on th is page]) . I f you are not sure whether the LLP student is enrol led on a fu l l - t ime basis , check wi th the educat ional inst i tut ion.

The educat ional inst i tu t ion determines when the student is considered to be enrol led in a program, and when the student is no longer enrol led. Usual ly , the student is considered to be enrol led when par t or a l l o f h is or her fees are paid.

I f the LLP student is not a l ready enrol led in a program, the student must have received a wr i t ten of fer f rom a designated educat ional inst i tut ion to enro l before March of the year af ter you wi thdraw funds

– 17 –

f rom your RRSPs under the LLP. A condi t ional wr i t ten of fer is acceptable.

I f you made an LLP wi thdrawal in a prev ious year , your repayment per iod has not begun.

You cannot par t ic ipate in the LLP i f the student has a l ready completed the program and is no longer enrol led.

What is a qual i fying educational program?

A quali fying educational program is an educat ional program of fered at a designated educat ional inst i tut ion.

The program must be:

• o f a technical or vocat ional nature designed to prov ide a person wi th sk i l ls for , or improve a person's sk i l ls in , an occupat ion, in the case where the program is at an educat ional inst i tu t ion cer t i f ied by Employment and Socia l Development Canada (ESDC), and

• a t a post-secondary school level , in any other case.

– 18 –

A l l programs must meet the fo l lowing condi t ions:

• last three consecut ive months or more; and

• requi re a s tudent to spend 10 hours or more per week on courses or work in the program. Courses or work inc ludes lectures, pract ical t ra in ing, and laboratory work, as wel l as research t ime spent on a post-graduate thesis . I t does not inc lude study t ime.

What is a designated educational inst i tut ion?

A designated educational inst i tut ion is a univers i ty , col lege, or other educat ional inst i tut ion. However, there are some di f ferences whether the inst i tu t ion is located in Canada or outs ide Canada. For more detai led in format ion see the def in i t ion of "designated educat ional inst i tut ion" on page 7 [4] . I f you are not sure whether a par t icular inst i tut ion qual i f ies as a designated educat ional inst i tu t ion, see Guide P105, STUDENTS AND INCOME TAX, or cal l 1 -800 -959 -8281 .

– 19 –

Who is a ful l - t ime student?

The educat ional inst i tu t ion determines who is a fu l l - t ime or par t - t ime student . The requirement that the student enro l as a fu l l - t ime student is separate f rom the qual i fy ing educat ional program requi rement. The qual i fy ing educat ional program requirement can be met by a person taking courses by correspondence or by a person enrol led in a d is tance educat ion program. Even i f the student is enrol led in a program that requires spending 10 hours or more per week on courses or work in the program, the inst i tu t ion may consider the student to be enrol led on a part - t ime basis. I f th is is the case, you cannot par t ic ipate in the LLP. The fo l lowing sect ion expla ins the only except ion to th is ru le.

Who can be enrol led on a part- t ime basis? An LLP student who meets one of the d isabi l i ty condi t ions can be enrol led on a part - t ime basis. The program in which the student is enrol led must s t i l l be a qual i fy ing educat ional program that usual ly requi res a student to spend 10 hours or more per week on courses or work in the program.

However, a s tudent who meets the d isabi l i ty condi t ions can spend less than 10 hours per week on courses or work in the program.

– 20 –

We consider the LLP student to meet the disabi l i ty condi t ions i f one o f the fo l lowing s i tuat ions appl ies:

• the student cannot reasonably be expected to be enrol led as a fu l l -t ime student because of a mental or physical impairment , and the student has submit ted a s igned let ter f rom a medical doctor , an optometr is t , a speech- language pathologis t , an audio logis t , an occupat ional therapist , a physiotherapist , or a psychologis t s tat ing th is ; or

• the student is ent i t led to the d isabi l i ty amount on l ine 316 of the student 's income tax and benef i t return for the year of the LLP wi thdrawal .

Note I f the student was al lowed the disabi l i ty amount on h is or her income tax and benef i t return for the prev ious year and st i l l meets the e l ig ib i l i ty requi rements for the d isabi l i ty amount , the student wi l l meet the d isabi l i ty condi t ion for the LLP. The student wi l l a lso meet th is condi t ion i f someone else c la imed the disabi l i ty amount for the student in the previous year and the student st i l l meets the el ig ib i l i ty requi rements for the d isabi l i ty amount . I f you have quest ions about the d isabi l i ty amount , ca l l 1 -800 -959 -8281 .

– 21 –

What happens if the LLP student does not enrol in the program in t ime?

I f the LLP student is not a l ready enrol led when you make the wi thdrawal , the student has to enro l in a qual i fy ing educat ional program before March of the year af ter you made the LLP wi thdrawal .

I f the LLP student does not enrol in the program in t ime, you have to cancel your LLP wi thdrawal .

For more informat ion, see "How to cancel your LLP wi thdrawal" on page 33 [9] .

How much you can withdraw Under the LLP, you can wi thdraw up to $10,000 f rom your RRSPs in a calendar year . This is your annual LLP l imit . The amount you wi thdraw is not l imi ted to the amount of tu i t ion or other educat ion expenses. Your spouse or common- law par tner can also wi thdraw up to $10,000 f rom thei r RRSPs under the LLP in the same year you do. For more informat ion, see "Can my spouse or common- law par tner and I par t ic ipate in the LLP at the same t ime?" on page 38 [10] .

– 22 –

You cannot wi thdraw more than $20,000 each t ime you par t ic ipate in the LLP. This is your total LLP l imit . You can par t ic ipate in the LLP again, s tar t ing the year af ter you br ing your LLP balance to zero.

I f you wi thdraw more than the annual LLP l imi t o f $10,000, the excess wi l l be inc luded in your income for the year of the wi thdrawal . The excess does not reduce your tota l LLP l imi t o f $20,000.

I f you wi thdraw more than the tota l LLP l imi t of $20,000, the excess wi l l be inc luded in your income for the year you exceed the tota l LLP l imi t .

When can you make LLP withdrawals? As long as the LLP student cont inues to meet the LLP condi t ions (see "What condi t ions does the LLP student have to meet?" on page 16 [6]) , you can keep wi thdrawing amounts f rom your RRSPs unt i l the ear l iest of the fo l lowing:

• the commencement of your repayment per iod, or

• January of the four th calendar year af ter the year you made your f i rs t LLP wi thdrawal .

– 23 –

You may not make addi t ional LLP wi thdrawals unt i l the year af ter your prev ious LLP balance is zero.

Example 1 Car los made LLP wi thdrawals of $10,000 in 2012 and $5,000 in 2013 because his spouse was at tending univers i ty . His spouse f i les income tax and benef i t re turns every year indicat ing she is enro l led in a fu l l - t ime program. Car los would l ike to wi thdraw another $5,000 in 2017. However, even though his spouse is s t i l l in school , he wi l l have to s tar t repaying his prev ious $15,000 wi thdrawals in 2017 and any 2017 wi thdrawal would be considered as inel ig ib le and taxable.

Example 2 Nadia made her f i rs t LLP wi thdrawal in 2015 for hersel f as the LLP student and completed the program the same year . She was not a s tudent in 2016 or in 2017. However, in 2017 she enrol led fu l l - t ime in a program beginning in January 2018 and would l ike to make another LLP wi thdrawal . Since Nadia wi l l have to star t repaying her 2015 wi thdrawal in 2017 (see char t "When to s tar t repaying your LLP wi thdrawals" on page 44 [10]) she cannot make another LLP wi thdrawal in 2017 nor in subsequent years unt i l the year af ter her f i rs t wi thdrawal has been fu l ly repaid.

– 24 –

Example 3 Angela made an LLP wi thdrawal of $5,000 in 2007 because her spouse was enrol led fu l l - t ime in a program that year . Her repayment per iod star ted in 2009 and she has been making a $500 repayment each year . In 2018, she decided to return to school and would l ike to make a wi thdrawal of $10,000. Such a wi thdrawal would not be e l ig ib le unless she made contr ibut ions to her RRSP or PRPP or both and chooses to fu l ly repay the remain ing $1,000 by making the designat ion in Par t B on Schedule 7 of her 2017 income tax and benef i t re turn. I f she does so, she could then star t a new par t ic ipat ion per iod beginning in 2018 and designate hersel f as the student .

How to make an LLP withdrawal To make an LLP wi thdrawal , use Form RC96, L IFELONG LEARNING PLAN (LLP) REQUEST TO WITHDRAW FUNDS FROM AN RRSP.

You have to f i l l out Form RC96 for each wi thdrawal you make. To get Form RC96, go to canada.ca/cra-forms .

– 25 –

F i l l out Par t 1 of Form RC96. You can name yoursel f or your spouse or common- law par tner as the LLP student in Par t 1. Af ter you f i l l out th is par t , g ive the form to your RRSP issuer , who wi l l f i l l out Par t 2.

Your RRSP issuer wi l l not wi thhold tax f rom the funds you wi thdraw i f you meet the LLP condi t ions. Your RRSP issuer wi l l send you a T4RSP sl ip , STATEMENT OF RRSP INCOME showing the amount you wi thdrew under the LLP in box 25. At tach th is s l ip to your income tax and benef i t re turn.

Fil ing an income tax and benefi t return

Star t ing in the year you make your f i rs t LLP wi thdrawal , you have to f i le an income tax and benef i t re turn every year unt i l you have repaid a l l your LLP wi thdrawals or inc luded them in your income. You have to send us an income tax and benef i t re turn even i f you do not owe any tax or you did not make a repayment to your RRSP.

Fi l l out Schedule 7, RRSP AND PRPP UNUSED CONTRIBUTIONS, TRANSFERS, AND HBP OR LLP ACTIV IT IES ( inc luded in your general income tax and benef i t package), and at tach i t to your income tax and

– 26 –

benef i t re turn to show the LLP wi thdrawals or the repayments made in the tax year. This wi l l he lp both you and us to keep t rack of them.

When you repor t a wi thdrawal on the Schedule 7, t ick Box 264 i f your spouse or common- law par tner is the student . I f you do not make th is ind icat ion we wi l l assume that you are the designated student . I f wi thdrawals are made in d i f ferent years, the student ind icated must remain the same or your wi thdrawal may be considered inel ig ib le.

How the withdrawal from your RRSP affects your RRSP deduction You can cont inue to contr ibute to your RRSP or PRPP or both and deduct your contr ibut ions f rom your income on your income tax and benef i t re turn af ter you have made an LLP wi thdrawal f rom your RRSP. However, you may not be able to deduct contr ibut ions you made before the wi thdrawal f rom your RRSP. The fo l lowing expla ins the restr ic t ions that apply.

I f you do not have an RRSP, you cannot set one up and then make an LLP wi thdrawal immediate ly . The contr ibut ion has to be in the RRSP

– 27 –

for 90 days before you can deduct i t f rom your income on your income tax and benef i t return.

I f you a l ready have an RRSP and you contr ibute to i t in the 89-day per iod before you make an LLP wi thdrawal , you may not be able to deduct the contr ibut ion f rom your income on your income tax and benef i t re turn even i f you repay th is amount to your RRSP under the LLP. I f the value of the RRSP r ight af ter the LLP wi thdrawal is more than or the same as the amount of the RRSP contr ibut ion, you can deduct the ent i re contr ibut ion. I f the value of the RRSP r ight af ter the LLP wi thdrawal is less than the amount of the RRSP contr ibut ion, you cannot deduct any or a l l o f the contr ibut ion.

– 28 –

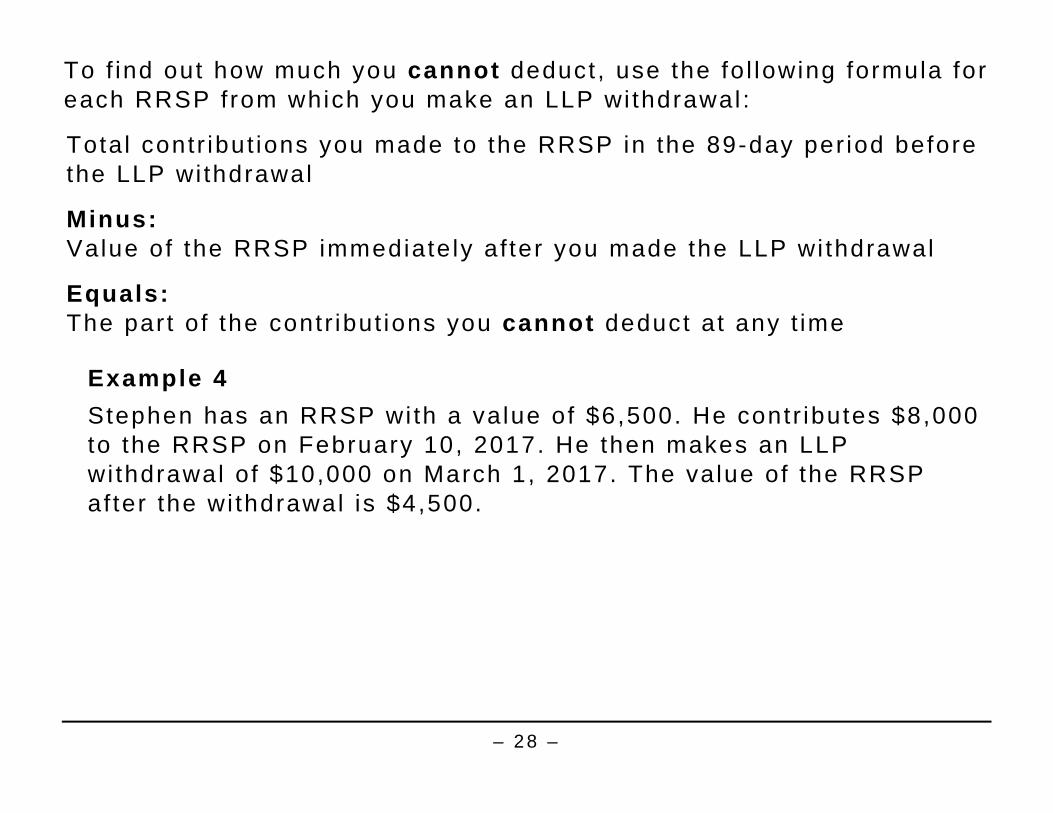

To f ind out how much you cannot deduct , use the fo l lowing formula for each RRSP from which you make an LLP wi thdrawal :

Total contr ibut ions you made to the RRSP in the 89-day per iod before the LLP wi thdrawal

Minus: Value of the RRSP immediate ly af ter you made the LLP wi thdrawal

Equals: The par t of the contr ibut ions you cannot deduct at any t ime

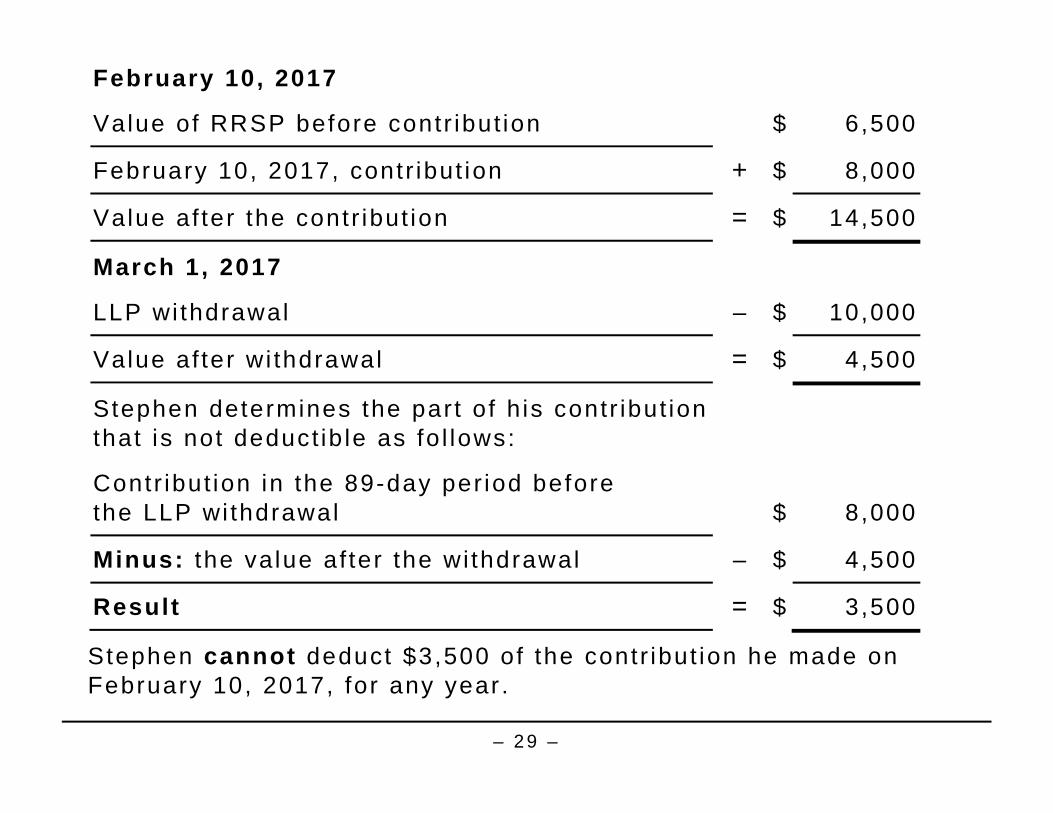

Example 4 Stephen has an RRSP wi th a value of $6,500. He contr ibutes $8,000 to the RRSP on February 10, 2017. He then makes an LLP wi thdrawal of $10,000 on March 1, 2017. The value of the RRSP af ter the wi thdrawal is $4,500.

– 29 –

February 10, 2017

Value of RRSP before contr ibut ion $ 6,500

February 10, 2017, contr ibut ion + $ 8,000

Value af ter the contr ibut ion = $ 14,500

March 1, 2017

LLP wi thdrawal – $ 10,000

Value af ter wi thdrawal = $ 4,500

Stephen determines the par t o f h is contr ibut ion that is not deduct ib le as fo l lows:

Contr ibut ion in the 89-day per iod before the LLP wi thdrawal

$

8,000

Minus: the value af ter the wi thdrawal – $ 4,500

Result = $ 3,500

Stephen cannot deduct $3,500 of the contr ibut ion he made on February 10, 2017, for any year .

– 30 –

Use the Appendix on page 63 [15] to determine the par t of contr ibut ions to your RRSP or PRPP or both that you or your spouse or common- law par tner made to your RRSP that are not deduct ib le for any year .

What happens if the LLP student leaves the educational program? For you to be able to repay the LLP wi thdrawals over a 10-year per iod, the LLP student usual ly has to e i ther :

• complete the program; or

• cont inue to be enrol led in the educat ional program at the end of March of the year af ter the LLP wi thdrawal .

I f the LLP student leaves the program before Apr i l o f the year af ter the wi thdrawal , you can st i l l make your repayments over a 10-year per iod i f less than 75% o f the student 's tu i t ion is refundable by the educat ional inst i tut ion.

I f the LLP student leaves the program before Apr i l o f the year af ter the wi thdrawal , and 75% or more of the LLP student 's tu i t ion is

– 31 –

re fundable, you have to cancel the LLP wi thdrawal . For more in format ion, see "How to cancel your LLP wi thdrawal" on page 33 [next page] . I f you do not cancel i t , the amount you wi thdrew wi l l be inc luded in your income for the year you wi thdrew i t .

We check the LLP student 's enrolment on l ine 328 of schedule 11 of thei r income tax and benef i t re turn for the year you make the wi thdrawal and for the fo l lowing year .

I f we cannot determine that the LLP student has cont inued in the program, we wi l l contact you to f ind out i f you st i l l meet the condi t ions to make the repayments over a 10-year per iod.

Example 5 In September 2017, George wi thdraws $1,000 f rom his RRSPs under the LLP. Ear l ier in the same month, he enrol led in a four-month col lege program and paid $750 in tu i t ion fees. George completes the program in January 2018. Therefore, he can repay h is LLP amounts over a 10 year per iod.

– 32 –

Note Specia l ru les apply i f the LLP par t ic ipant d ies. For more in format ion, see " I f the person who made the LLP wi thdrawal d ies" on page 54 [13] .

Can an LLP withdrawal be cancelled You can cancel your LLP wi thdrawal only i f one or more of the fo l lowing s i tuat ions apply:

• The LLP student was not enrol led in the qual i fy ing educat ional program when you made the wi thdrawal but had received wr i t ten not i f icat ion that he or she was ent i t led to enrol before March of the fo l lowing year and did not enrol in t ime.

• The LLP student le f t the program before Apr i l o f the year af ter the wi thdrawal , and 75% or more of the student 's tu i t ion was refundable.

• You became a non-res ident of Canada before the end of the year in which you made an LLP wi thdrawal .

– 33 –

A cancel la t ion payment is not considered an RRSP or PRPP contr ibut ion and therefore, must not be entered as a contr ibut ion in "Par t A – Contr ibut ions" of Schedule 7, RRSP AND PRPP UNUSED CONTRIBUTIONS, TRANSFERS, AND HBP OR LLP ACTIV IT IES, as you cannot c la im a deduct ion for th is amount on your income tax and benef i t re turn.

How to cancel your LLP withdrawal Step 1 – Repay the amount you wi thdrew f rom your RRSP. You can make your cancel la t ion payment to:

• the same RRSP you wi thdrew the funds f rom;

• any other of your RRSPs;

• a new RRSP.

You cannot make a cancel la t ion payment to your PRPP, SPP or spouse's or common- law par tner 's RRSPs or SPP. Your RRSP issuer wi l l g ive you a RRSP contr ibut ion (cancelat ion payment) receipt .

– 34 –

Note I f you do not repay al l the funds you wi thdrew, you have to inc lude the unpaid amounts in your income for the year they were wi thdrawn. I f we have a l ready assessed your income tax and benef i t re turn for that year , we wi l l reassess i t to inc lude the unpaid amount. We may a lso charge you in terest and penal t ies.

Step 2 – Send us a le t ter and include the fo l lowing:

• the informat ion about the RRSP owner ( th is is the indiv idual who made the RRSP wi thdrawal) :

– f i rs t name and in i t ia ls ;

– last name;

– socia l insurance number;

– mai l ing address;

– te lephone number.

• the year you made the wi thdrawal ;

• the amount wi thdrawn;

– 35 –

• the date you became a non-resident ( i f appl icable) ;

• the reason for the cancel la t ion:

– The LLP student was not enrol led in the qual i fy ing educat ional program when you made the wi thdrawal but had received wr i t ten not i f icat ion that he or she was ent i t led to enrol before March of the fo l lowing year and d id not enrol in t ime.

– The LLP student le f t the program before Apr i l o f the year af ter the wi thdrawal , and 75% or more of the student 's tu i t ion was refundable.

– You became a non-res ident of Canada before the end of the year in which you made an LLP wi thdrawal .

• the amount and date of the cancel la t ion payment; and

• the s ignature of the RRSP owner.

– 36 –

Step 3 – Send th is le t ter a long wi th your RRSP contr ibut ion (cancel la t ion payment) receipt to :

Canada Revenue Agency Pension Workf low Team Sudbury Tax Centre Post Of f ice Box 20000, Stat ion A Sudbury, ON P3A 5C1

Or

Canada Revenue Agency Pension Workf low Team Winnipeg Tax Centre Post Of f ice Box 14000, Stat ion Main Winnipeg, MB R3C 3M2

You cannot make your cancel la t ion payment i f the wi thdrawal d id not meet the LLP condi t ions when you made the withdrawal . One or more of the s i tuat ions l is ted above must apply for you to cancel your wi thdrawal .

– 37 –

Due date for cancel lat ion payment

I f you are a resident of Canada when you f i le your income tax and benef i t re turn for the year in which you made the LLP wi thdrawal , the due date for the cancel lat ion payment is December 31 of the year af ter the year you made the wi thdrawal .

I f you are a non-resident of Canada when you f i le your income tax and benef i t re turn for the year in which you made the LLP wi thdrawal , the due date for the cancel lat ion payment is whichever is earl ier :

• the date you f i le your income tax and benef i t re turn for the year you made the wi thdrawal ; or

• December 31 of the year af ter the year of the wi thdrawal .

Example 6 On May 3, 2017, Patr ick appl ies to three Canadian univers i t ies as a fu l l - t ime student. On July 12, 2017, Patr ick receives a wr i t ten of fer to enro l in a program at one of the univers i t ies. On July 13, 2017, he makes an LLP wi thdrawal of $10,000 f rom his RRSP. Since Patr ick wi thdrew the funds in 2017, he has to enrol in the program before March 1, 2018. I f he does not , Patr ick wi l l have to cancel the LLP

– 38 –

wi thdrawal by paying back the $10,000 to h is RRSP by December 31, 2018. Any amount he does not repay wi l l be inc luded in h is income for 2017.

Questions you may have

How often can I part icipate in the LLP?

There is no l imi t to the number of t imes you can par t ic ipate in the LLP over your l i fe t ime. Star t ing in the year af ter you br ing your LLP balance to zero, you can par t ic ipate in the LLP again and wi thdraw up to $20,000 over a new par t ic ipat ion per iod (def ined on page 8 [4] ) .

Can my spouse or common-law partner and I part icipate in the LLP at the same t ime?

Yes. You can do any of the fo l lowing:

• you can par t ic ipate in the LLP for yoursel f whi le your spouse or common- law par tner par t ic ipates in the LLP for h im or hersel f ;

• you can both part ic ipate in the LLP for e i ther of you; or

• you can par t ic ipate in the LLP for each other .

– 39 –

Each of you can wi thdraw up to the annual LLP l imi t o f $10,000 in a year and up to the tota l LLP l imi t o f $20,000 over the per iod you are par t ic ipat ing in the LLP.

Note: I f you are a l ready a part ic ipant in the LLP program and the student has been establ ished as e i ther yoursel f or your spouse or common-law par tner, you cannot make an addi t ional wi thdrawal for a d i f ferent s tudent .

Can I make LLP withdrawals from more than one RRSP?

You can make LLP wi thdrawals for you or your spouse or common- law par tner f rom more than one RRSP as long as you are the annui tant (p lan owner) of each RRSP. Your RRSP issuer wi l l not wi thhold tax on these amounts. Al though the maximum amount you can wi thdraw each t ime you par t ic ipate is $20,000, there is an annual wi thdrawal l imi t o f $10,000.

– 40 –

Note Simi lar to locked- in RRSPs, PRPPs do not a l low for LLP wi thdrawals. However, you can designate your PRPP contr ibut ions as an LLP repayment.

Can I make LLP withdrawals for other purposes?

As long as you meet a l l the LLP condi t ions when you make the wi thdrawal , you can use the funds you wi thdrew for any purpose.

Can I part icipate in the LLP and in the Home Buyers' Plan at the same t ime?

You can par t ic ipate in the LLP even i f you have not yet fu l ly repaid the wi thdrawn amounts f rom your RRSPs under the Home Buyers ' Plan (HBP). For more in format ion about the HBP, see canada.ca/home-buyers-plan .

Chapter 2 – Repaying your withdrawals Over a per iod of 10 years, you have to repay to your RRSP or PRPP or both the amounts you wi thdrew under the LLP. General ly , for each

– 41 –

year of your repayment per iod, you have to repay 1/10 of the tota l amount you wi thdrew, unt i l the LLP balance is zero.

When and how much to repay You wi l l receive an LLP STATEMENT OF ACCOUNT each year wi th your not ice of assessment or not ice of reassessment. This s tatement wi l l show the LLP wi thdrawals, your LLP balance, the amounts you have repaid to date, cancel la t ions, income inc lusions, and the amount you have to repay the fo l lowing year .

To v iew your LLP STATEMENT OF ACCOUNT onl ine, go to My Account at canada.ca/my-cra-account . To v iew the LLP STATEMENT OF ACCOUNT of someone who has author ized you on thei r behal f go to Represent a Cl ient at canada.ca/taxes-representat ives .

To determine when you have to s tar t repaying your LLP wi thdrawals, use the char t on the next page. The la test year you can star t repaying your LLP wi thdrawals is the f i f th year af ter your f i rs t LLP wi thdrawal . However, in most cases, you have to s tar t repaying your wi thdrawals before that year .

– 42 –

We determine when your repayment per iod star ts by checking i f the LLP student is a qual i fy ing student for at least three months dur ing the year . I f the LLP student does not meet th is condi t ion two years in a row, your repayment per iod usual ly s tar ts in the second of those two years. I f the LLP student cont inues to meet th is condi t ion every year , your repayment per iod star ts in the f i f th year af ter your f i rs t LLP wi thdrawal .

In some cases, the LLP student is not a qual i fy ing student for at least three consecut ive months in any calendar year . This can happen i f the program is shor t and the student star ts i t near the end of the year . In that case, your f i rs t repayment year is the second year af ter the year of your LLP wi thdrawal . I f the student is not a qual i fy ing student for three months in any year because the student le f t the program, see "What happens i f the LLP student leaves the educat ional program?" on page 30 [8] .

Example 7 Sarah makes LLP wi thdrawals f rom 2014 to 2017. She cont inues her educat ion f rom 2014 to 2019, and is a qual i fy ing student up to tax year 2017. Sarah's repayment per iod begins in 2019, s ince 2019 is the f i f th year af ter the year of her f i rs t LLP wi thdrawal .

– 43 –

The due date for her f i rs t repayment is March 1, 2020, which is 60 days af ter the end of 2019, her f i rs t repayment year

Example 8 Joseph makes an LLP wi thdrawal in 2016 for a qual i fy ing educat ional program he is enrol led in dur ing the same year . He is a fu l l - t ime student for f ive months of 2016. Joseph completes the educat ional program in 2017, and he is a fu l l - t ime student for f ive months in 2017. He is not considered a qual i fy ing student for 2018 or 2019. Joseph's repayment per iod begins in 2019.

Note Even i f you become bankrupt , you st i l l have to repay al l your LLP wi thdrawals to your RRSPs. I f you do not , you have to inc lude the requi red amounts in your income each year as they become due.

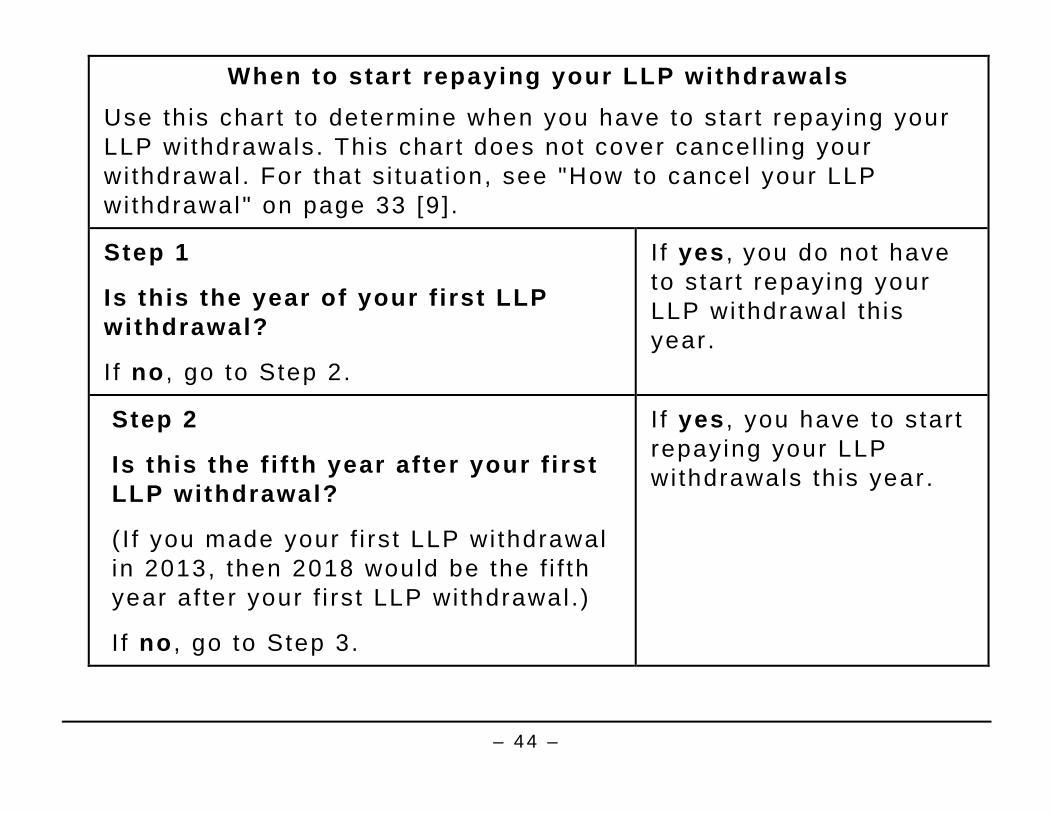

– 44 –

When to start repaying your LLP withdrawals Use th is char t to determine when you have to s tar t repaying your LLP wi thdrawals. This char t does not cover cancel l ing your wi thdrawal . For that s i tuat ion, see "How to cancel your LLP wi thdrawal" on page 33 [9] .

Step 1

Is this the year of your f irst LLP withdrawal?

I f no , go to Step 2.

I f yes , you do not have to s tar t repaying your LLP wi thdrawal th is year .

Step 2

Is this the f i f th year after your f irst LLP withdrawal?

( I f you made your f i rs t LLP wi thdrawal in 2013, then 2018 would be the f i f th year af ter your f i rs t LLP wi thdrawal . )

I f no , go to Step 3.

I f yes , you have to s tar t repaying your LLP wi thdrawals th is year .

– 45 –

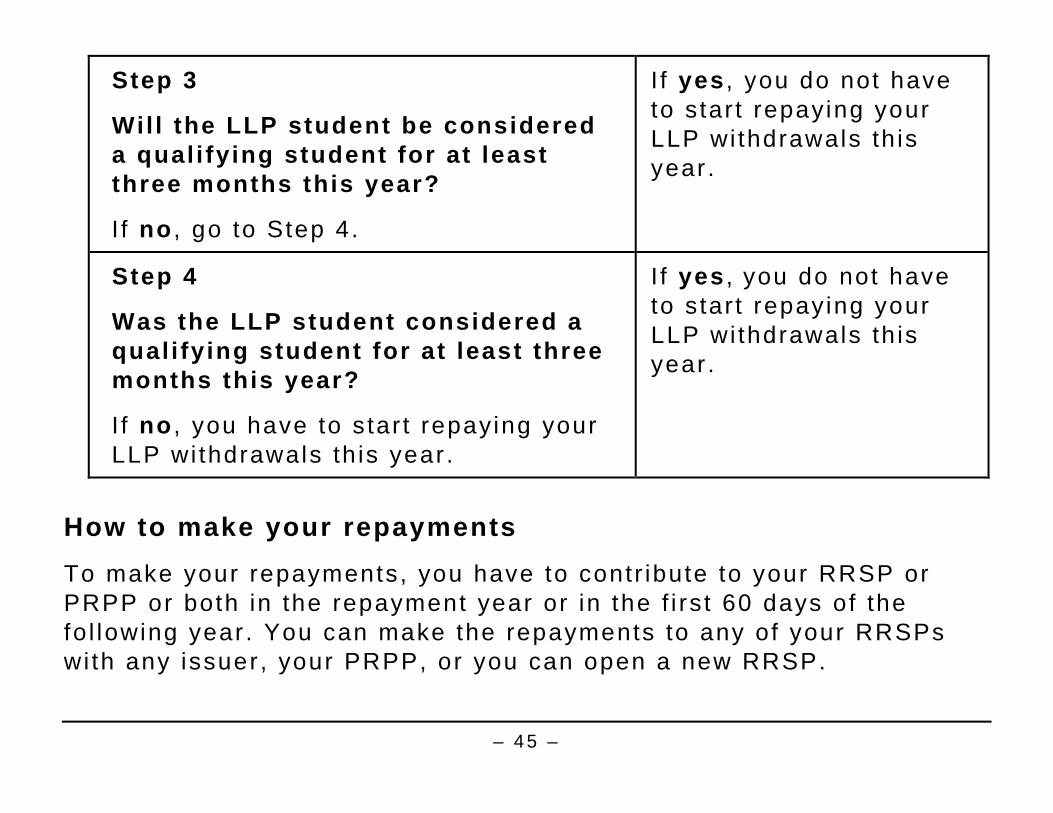

Step 3

Wil l the LLP student be considered a qual i fying student for at least three months this year?

I f no , go to Step 4.

I f yes , you do not have to s tar t repaying your LLP wi thdrawals th is year .

Step 4

Was the LLP student considered a qual i fying student for at least three months this year?

I f no , you have to s tar t repaying your LLP wi thdrawals th is year .

I f yes , you do not have to s tar t repaying your LLP wi thdrawals th is year .

How to make your repayments To make your repayments, you have to contr ibute to your RRSP or PRPP or both in the repayment year or in the f i rs t 60 days of the fo l lowing year . You can make the repayments to any of your RRSPs wi th any issuer , your PRPP, or you can open a new RRSP.

– 46 –

You have to designate your repayment for the year by complet ing Schedule 7, RRSP AND PRPP UNUSED CONTRIBUTIONS, TRANSFERS, AND HBP OR LLP ACTIV IT IES ( inc luded in your income tax and benef i t package), and f i le i t w i th your income tax and benef i t re turn for the repayment year .

You have to make your repayments to your RRSP or PRPP or both even i f your RRSP deduct ion l imi t is zero or a negat ive amount . We do not consider an amount you designate as a repayment under the LLP to be an RRSP contr ibut ion. Therefore, you cannot c la im a deduct ion for th is amount on your income tax and benef i t re turn.

Example 9 Betty has an LLP balance of $7,500. Her repayment per iod is f rom 2017 to 2026. For her f i rs t repayment year , she needs to repay $750, which is 1/10 of the amount she wi thdrew. Bet ty contr ibutes $6,000 to her RRSPs in 2017. To designate $750 as her 2017 repayment, she has to f i le Schedule 7 wi th her 2017 income tax and benef i t re turn. Betty can deduct the remain ing $5,250 she contr ibuted i f the RRSP deduct ion l imi t shown on her not ice of assessment for 2016 is at least $5,250.

– 47 –

Contributions you cannot designate Not a l l contr ibut ions you make to your RRSP or PRPP or both in the repayment year , or in the f i rs t 60 days of the fo l lowing year , can be designated as a repayment under the LLP.

You cannot designate contr ibut ions that :

• your employer made to your PRPP;

• you make to your spouse's or common-law partner 's RRSPs (or that he or she makes to your RRSPs);

• are amounts you t ransfer d i rect ly to your RRSPs f rom a regis tered pension plan, deferred prof i t shar ing plan, regis tered ret i rement income fund, speci f ied pension plan, PRPP, or another RRSP;

• are amounts you deducted as a re-contr ibut ion of an excess qual i fy ing wi thdrawal that you designated to have a prov is ional past serv ice pension adjustment approved;

• are amounts you designate as a repayment under the Home Buyers ' P lan (HBP) for the year ;

– 48 –

• are amounts you contr ibute in the f i rs t 60 days of the repayment year , that you:

– deducted on your income tax and benef i t re turn for the previous year ; or

– designated as a repayment for the prev ious year under the HBP or the LLP.

• are amounts you receive in the repayment year (such as ret i r ing a l lowances) that you inc lude in your income, designate as a t ransfer to your RRSP and deduct on your income tax and benef i t re turn for the year of receipt .

I f you want to repay earl ier

Any payments you make before the f i rs t repayment year reduce your f i rs t required repayment. For example, i f your f i rs t repayment year is 2018 and $1,000 is your required repayment and you make an ear ly repayment of $600 in 2017, your requi red repayment for 2018 is $400.

– 49 –

I f you repay less than the amount required I f you designate an amount less than the amount you have to repay, you have to inc lude the di f ference in your income on l ine 129 of your income tax and benef i t re turn. The amount you include in your income is equal to the amount you have to repay minus the amount you designate as a repayment for the year . The amount you inc lude in your income cannot be more than the resul t o f th is calculat ion. Your LLP balance is reduced by the amount you repay plus the amount you inc lude in income. I f you want to calculate the amount you have to repay for the next year , d iv ide your LLP balance by the number of years remain ing in your repayment per iod.

Example 10 Josée makes a $10,000 LLP wi thdrawal in 2015 for a four-month qual i fy ing educat ional program that f in ishes in the same year . For 2017, Josée's repayment is $1,000 ($10,000 ÷ 10) . Josée contr ibutes $700 to her RRSPs in 2017, and she f i les Schedule 7 wi th her income tax and benef i t return to designate the $700 as a repayment under the LLP. Josée has to inc lude $300 in her income on l ine 129 of her 2017 income tax and benef i t re turn.

– 50 –

She determined th is as fo l lows:

Amount she has to repay for 2017 $ 1,000

Minus: Amount she designates as a repayment on Schedule 7

–

=

$

$

700

Amount inc luded on l ine 129 300

She cannot c la im a deduct ion for the $700 contr ibuted to her RRSPs because she designated those contr ibut ions as a repayment under the LLP. In 2018, she wi l l have to repay $1,000 ($9,000 ÷ 9) .

– 51 –

I f you repay more than the amount required for a year

I f you repay and designate more than you have to repay for a year , the amount you have to repay in each of the fo l lowing years wi l l be less. The LLP STATEMENT OF ACCOUNT we send wi th your not ice of assessment or not ice of reassessment takes into account any addi t ional payments you make and te l ls you how much you have to repay for the next year . I f you want to calculate the amount you have to repay for the next year , d iv ide your LLP balance by the number of years le f t in your repayment per iod.

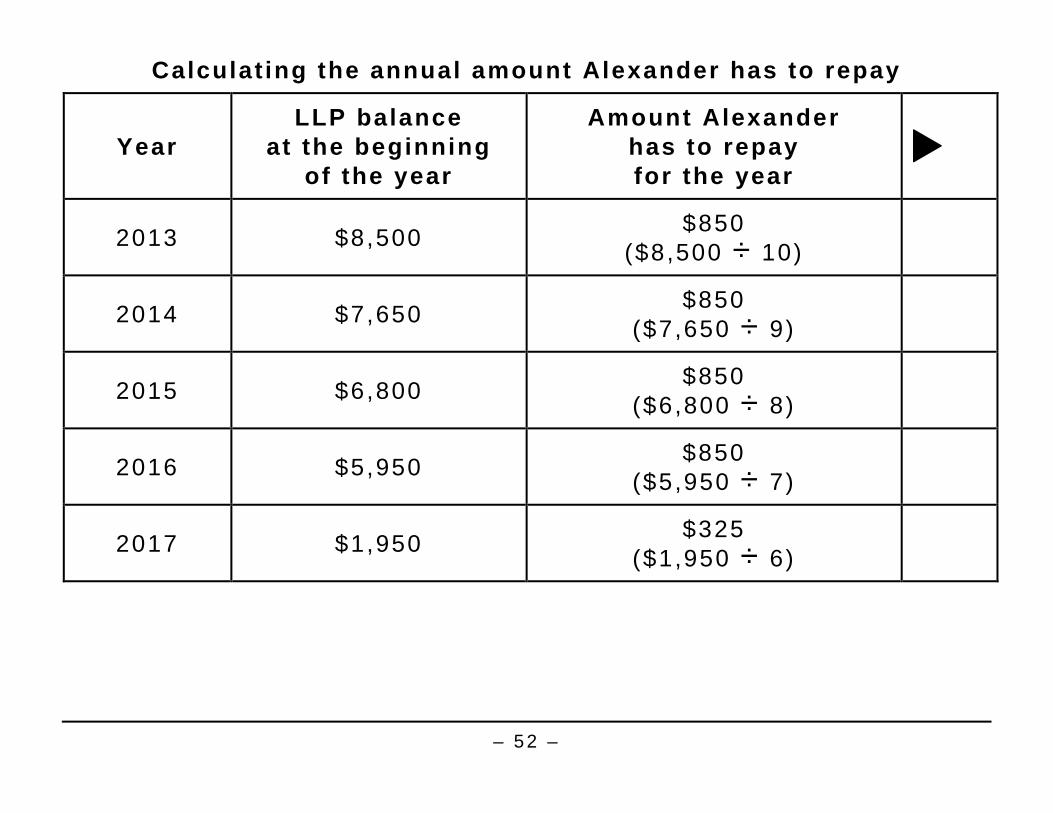

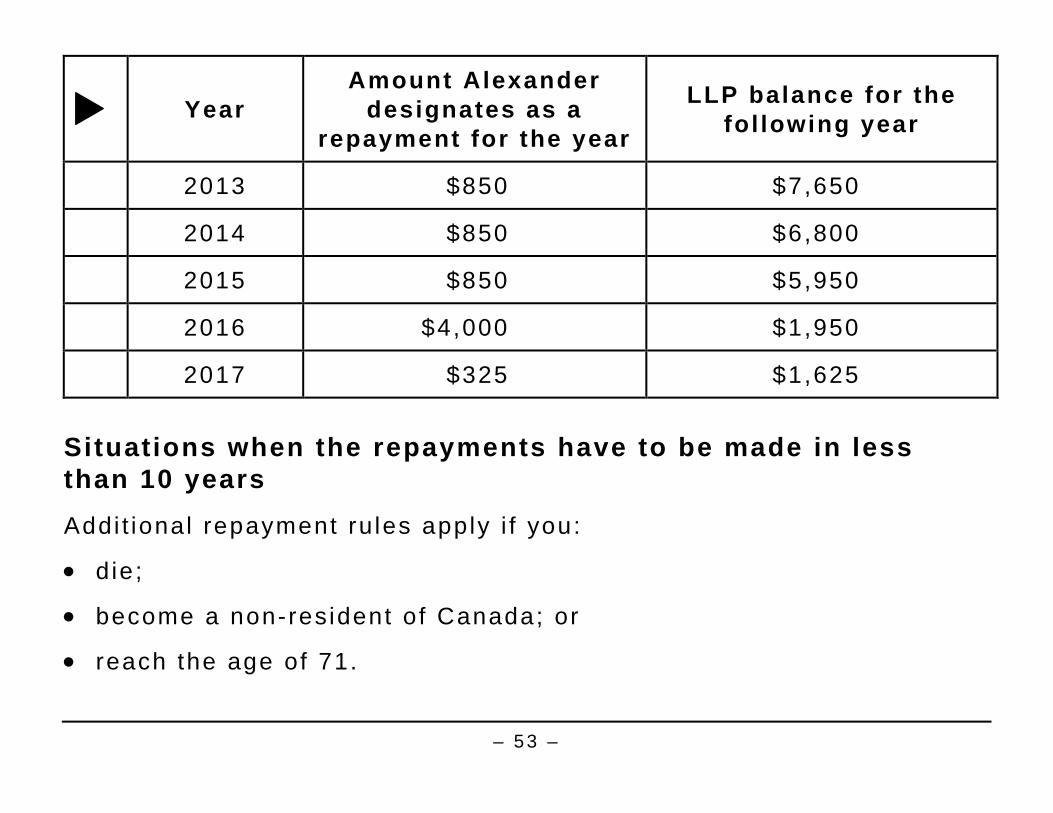

Example 11 Alexander 's repayment per iod began in 2013. His LLP balance was $8,500. Alexander 's repayment for 2013 was $850 ($8,500 ÷ 10) . He made the repayment for 2013, 2014, and 2015. In 2016, he received an inher i tance and decided to contr ibute $4,000 to h is RRSPs and designate that amount as a repayment under the LLP for 2016. He calculates the amount he has to repay for 2017 using the fo l lowing char t :

– 52 –

Calculat ing the annual amount Alexander has to repay

Year LLP balance

at the beginning of the year

Amount Alexander has to repay for the year

2013 $8,500 $850 ($8,500 ÷ 10)

2014 $7,650 $850 ($7,650 ÷ 9)

2015 $6,800 $850 ($6,800 ÷ 8)

2016 $5,950 $850 ($5,950 ÷ 7)

2017 $1,950 $325 ($1,950 ÷ 6)

– 53 –

Year Amount Alexander

designates as a repayment for the year

LLP balance for the fol lowing year

2013 $850 $7,650

2014 $850 $6,800

2015 $850 $5,950

2016 $4,000 $1,950

2017 $325 $1,625

Situations when the repayments have to be made in less than 10 years Addi t ional repayment ru les apply i f you:

• d ie;

• become a non-resident of Canada; or

• reach the age of 71.

– 54 –

I f the person who made the LLP withdrawal dies

Usual ly , i f the person who made the LLP wi thdrawal d ies, the legal representat ive (adminis t rator) has to inc lude the LLP balance in the deceased person's income for the year of death. I f the deceased person contr ibuted to an RRSP in the year of death, the representat ive can designate the contr ibut ions as a repayment under the LLP by complet ing Schedule 7, RRSP AND PRPP UNUSED CONTRIBUTIONS, TRANSFERS, AND HBP OR LLP ACTIV IT IES. This reduces the LLP balance that has to be inc luded in the deceased person's income.

Note An LLP student who dies may not have been the person who made the LLP wi thdrawal . I f th is is the case, the person who made the wi thdrawal makes the requi red LLP repayments over the usual 10-year per iod.

– 55 –

LLP elect ion on death

I f , a t the t ime the person who made the LLP wi thdrawal d ies, and the deceased had a spouse or common- law par tner who is a res ident of Canada, that spouse or common- law par tner can elect jo int ly wi th the deceased person's legal representat ive (adminis t rator) to make the repayments and to not inc lude the LLP balance in the deceased person's income. I f the surv iv ing spouse or common- law par tner is a lso the representat ive, he or she makes the e lect ion.

To make th is e lect ion, the surv iv ing spouse or common- law par tner and the deceased person's legal representat ive s ign a le t ter and at tach i t to the deceased person's income tax and benef i t re turn for the year of death. The le t ter should state that an elect ion is being made to have the surv iv ing spouse or common- law par tner make the repayments under the LLP, and to not have the income inclusion ru le apply to the deceased person. The deceased person's LLP balance then becomes the surv ivor 's LLP balance. The surv iv ing spouse or common- law par tner makes the repayments to h is or her own RRSP or PRPP or both.

– 56 –

Note I f th is e lect ion is made and the deceased person had not made a repayment for the year of death, no repayment wi l l be required for that year for the deceased.

I f the surviving spouse or common-law partner has no LLP balance of his or her own at the t ime the person who made the LLP withdrawal dies , the surv ivor is deemed to be the LLP student for the LLP balance taken over f rom the deceased person. The surv iv ing spouse or common- law par tner wi l l have to make repayments to h is or her RRSP over the normal 10 year repayment per iod, determined as though the year of h is or her f i rs t LLP wi thdrawal is the year the person d ied. For more informat ion on when the repayment per iod wi l l begin, see "When and how much to repay" on page 41 [10] and the char t on page 44 [11] .

I f the surv iv ing spouse or common- law par tner wants to make LLP wi thdrawals, the LLP balance taken over f rom the deceased person wi l l l imi t the amount he or she can wi thdraw.

The surv ivor 's to ta l l imi t wi l l be $20,000 minus the LLP balance taken over f rom the deceased person. The annual LLP l imi t for the year of

– 57 –

death wi l l be $10,000 minus the remain ing LLP balance of the deceased person.

Example 12 Isabel le d ied in 2017. At the t ime of death, she had an LLP balance of $7,200. Her repayment per iod began in 2016. Her husband Bruno is her adminis t rator ( legal representat ive) .Bruno decides to e lect to make the repayments. When he prepares Isabel le 's f ina l income tax and benef i t re turn for 2017, he does not inc lude her LLP balance in her income. Instead, he wr i tes a le t ter expla in ing that he is e lect ing to make his la te wi fe 's LLP repayments. He s igns the le t ter and at taches i t to her f ina l income tax and benef i t re turn. Bruno becomes an LLP par t ic ipant in 2017 having an LLP balance of $7,200.

I f Bruno is not a fu l l - t ime qual i fy ing student for at least three months in both 2018 and 2019, h is repayment per iod wi l l begin in 2019. He may choose to make repayments in 2017 or 2018, in which case they wi l l be appl ied to the balance to reduce or e l iminate the requi red repayment in 2019 and subsequent years. For more in format ion, see " I f you want to repay ear l ier" on page 48 [12] .

I f Bruno wants to par t ic ipate in the LLP in 2017 for h is own educat ion, h is to ta l LLP l imi t is now $20,000 minus the remain ing

– 58 –

LLP balance f rom Isabel le . As wel l , h is annual LLP l imi t for 2017 is $10,000 minus the remain ing LLP balance f rom Isabel le .

I f Bruno did not make the elect ion, he would have to inc lude $7,200 as income on l ine 129 of Isabel le 's f ina l income tax and benef i t re turn for 2017.

I f the surviving spouse or common - law partner already had an LLP balance of his or her own at the t ime the person dies, the deceased person's LLP balance is added to the surv ivor 's LLP balance. This may cause the surv ivor 's LLP balance to be more than the $10,000 annual l imi t or the $20,000 tota l l imi t . I f th is occurs, we wi l l not inc lude the excess in the income of e i ther the surv ivor or the deceased person. The surv iv ing spouse or common- law par tner has to repay the new balance over h is or her own repayment per iod.

Example 13 I rene d ied on June 10, 2017. At the t ime of her death, she had an LLP balance of $7,000 to be repaid. I rene 's common- law par tner Paul is the estate 's adminis trator ( legal representat ive) . He decides to make I rene's LLP repayments. He has his own LLP balance of $14,000, and his repayment per iod began in 2017.

– 59 –

Paul wi l l add I rene's LLP balance of $7,000 to h is own LLP balance of $14,000. However, Paul is only required to make a repayment of $1,400 in 2017 based on his own LLP balance of $14,000 at the beginning of the year . I f he pays only the requi red amount in 2017, h is min imum LLP repayment in 2018 wi l l be $2,177 ($19,600 ÷ 9) .

I f you become a non-resident of Canada

I f you become a non-resident of Canada after the year you made an LLP withdrawal , you have to inc lude your LLP repayable balance in income on your income tax and benef i t return for the year you become a non-res ident or repay that balance to your RRSP or PRPP or both. The due date for th is repayment is the earl ier o f the fo l lowing dates:

• before the t ime you f i le your income tax and benef i t re turn for the year that you become a non-resident ; or

• 60 days af ter you become a non-resident .

You have to designate your repayment for the year by complet ing Schedule 7 and f i l ing i t w i th your income tax and benef i t return for the year you become a non-res ident . I f you do not repay your LLP balance by the due date, you have to inc lude the unpaid amount in your

– 60 –

income for the year you became a non-resident . The amount is inc luded in your income for the per iod you were a resident of Canada.

I f you become a non-resident before the end of the year in which you make an LLP withdrawal , you have to cancel your LLP wi thdrawals by paying them back to your RRSP.

For more informat ion, see "How to cancel your LLP wi thdrawal" on page 33 [9] .

Your options in the year you turn 71 The year af ter you reach the age of 71, you wi l l not be able to repay any wi thdrawals to your RRSP or PRPP or both. This is because you cannot contr ibute to an RRSP or PRPP the year af ter you turn 71 years of age.

– 61 –

In the year you turn 71, you can choose one of the fo l lowing:

• repay your remain ing repayable balance to your RRSP or PRPP or both;

• make a par t ia l repayment to your RRSP or PRPP or both. Your remain ing repayable balance at the beginning of the year you turn 72 wi l l be d iv ided by the number of years remain ing in your repayment per iod, and that calculated amount wi l l be inc luded as income on l ine 129 of your income tax and benef i t return for each of those years; or

• make no repayment to e i ther your RRSP or PRPP. Your remain ing repayable balance at the beginning of the year you turn 71 wi l l be d iv ided by the number of years remaining in your repayment per iod, and that calculated amount wi l l be inc luded as income on l ine 129 of your income tax and benef i t re turn for each of those years.

Example 14 In 2010, at the age of 64, Henry made an LLP wi thdrawal of $9,000. His repayment per iod began in 2015. The requi red annual repayment is $900. In 2017, he reaches the age of 71. Henry 's LLP balance at the beginning of 2017 is $7,200 and he can choose to make an LLP repayment, or to inc lude $900 in h is income.

– 62 –

In 2017, Henry decides to contr ibute $3,000 to h is PRPP and to designate that amount as a repayment under the LLP. This leaves h im wi th an unpaid balance of $4,200 at the end of 2017. Henry wi l l have to inc lude $600 ($4,200 ÷ 7) in income for each year f rom 2018 to 2024. I f he d id not repay any par t o f the $7,200, he would have to inc lude $900 in income each year f rom 2017 to 2024. I f he repaid the ent i re $7,200, he would not have to inc lude any par t o f th is amount in h is income.

– 63 –

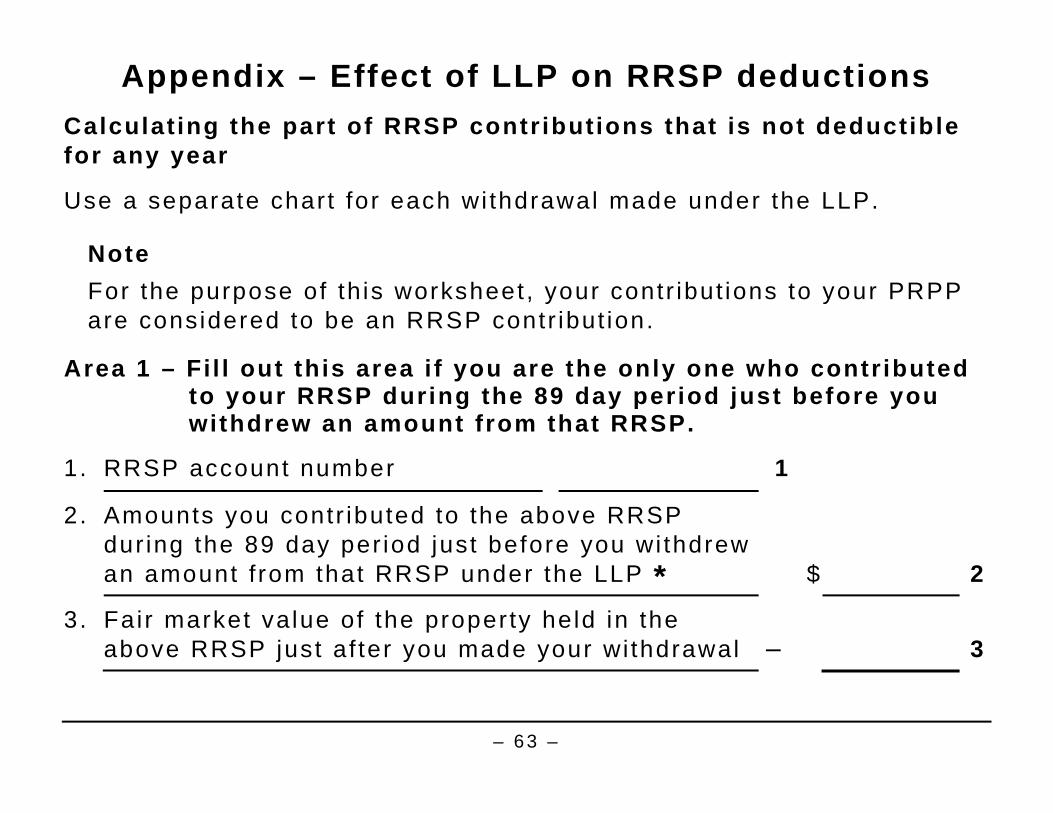

Appendix – Effect of LLP on RRSP deductions Calculat ing the part of RRSP contr ibutions that is not deductible for any year

Use a separate char t for each wi thdrawal made under the LLP.

Note For the purpose of th is worksheet , your contr ibut ions to your PRPP are considered to be an RRSP contr ibut ion.

Area 1 – Fi l l out this area i f you are the only one who contr ibuted to your RRSP during the 89 day period just before you withdrew an amount from that RRSP.

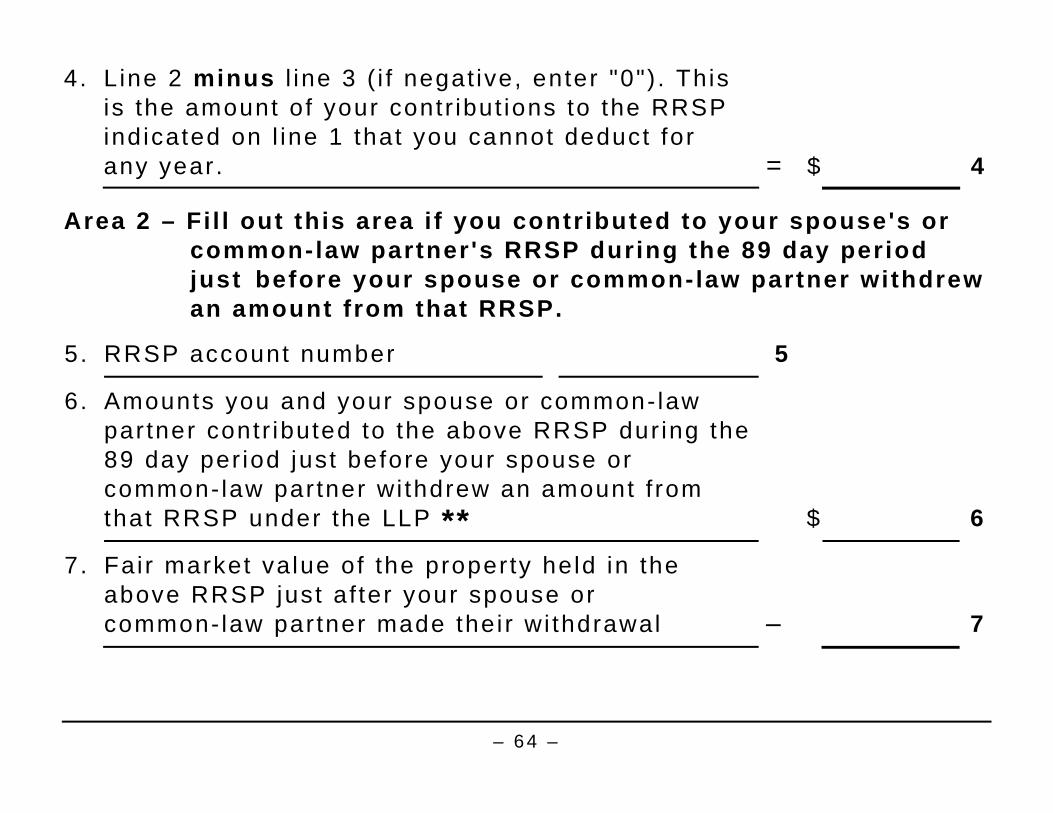

1. RRSP account number 1

2. Amounts you contr ibuted to the above RRSP dur ing the 89 day per iod just before you wi thdrew an amount f rom that RRSP under the LLP *

$

2

3. Fair market value of the proper ty held in the above RRSP just af ter you made your wi thdrawal

–

3

– 64 –

4 . L ine 2 minus l ine 3 ( i f negat ive, enter "0") . This is the amount of your contr ibut ions to the RRSP indicated on l ine 1 that you cannot deduct for any year .

=

$

4

Area 2 – Fi l l out this area i f you contr ibuted to your spouse's or common-law partner 's RRSP during the 89 day period just before your spouse or common-law partner withdrew an amount from that RRSP.

5. RRSP account number 5

6. Amounts you and your spouse or common- law par tner contr ibuted to the above RRSP dur ing the 89 day per iod just before your spouse or common- law par tner wi thdrew an amount f rom that RRSP under the LLP **

$

6

7. Fair market value of the proper ty held in the above RRSP just af ter your spouse or common- law par tner made thei r wi thdrawal

–

7

– 65 –

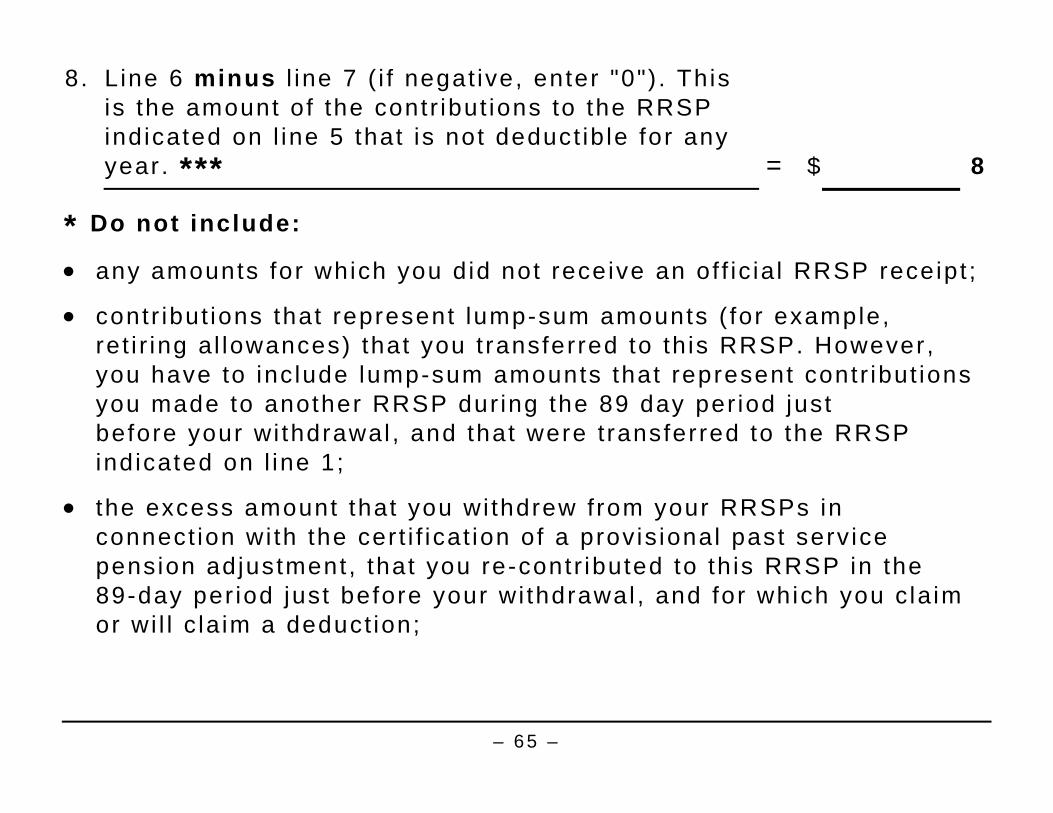

8 . L ine 6 minus l ine 7 ( i f negat ive, enter "0") . This is the amount of the contr ibut ions to the RRSP indicated on l ine 5 that is not deduct ib le for any year . ***

=

$

8

* Do not include:

• any amounts for which you did not receive an of f ic ia l RRSP receipt ;

• contr ibut ions that represent lump-sum amounts ( for example, ret i r ing a l lowances) that you t ransferred to th is RRSP. However, you have to inc lude lump-sum amounts that represent contr ibut ions you made to another RRSP dur ing the 89 day per iod just before your wi thdrawal , and that were t ransferred to the RRSP indicated on l ine 1;

• the excess amount that you wi thdrew from your RRSPs in connect ion wi th the cer t i f icat ion of a provis ional past serv ice pension adjustment , that you re-contr ibuted to th is RRSP in the 89-day per iod just before your wi thdrawal , and for which you c la im or wi l l c la im a deduct ion;

– 66 –

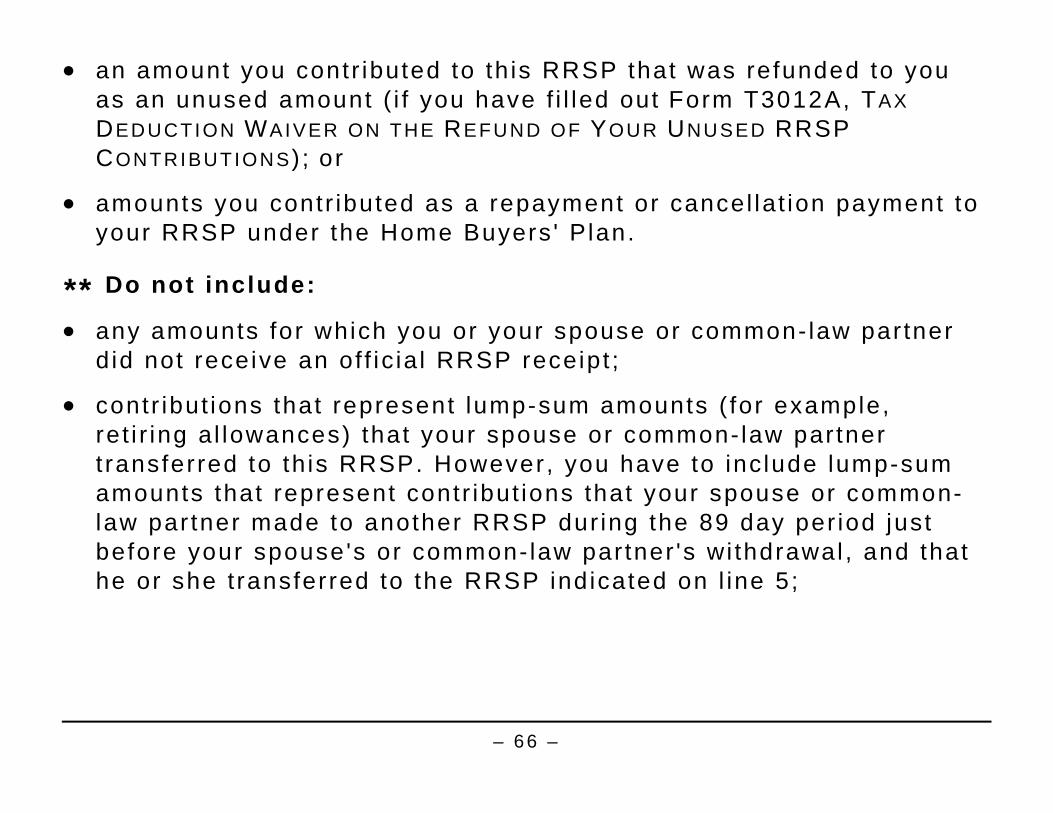

• an amount you contr ibuted to th is RRSP that was refunded to you as an unused amount ( i f you have f i l led out Form T3012A, TAX DEDUCTION WAIVER ON THE REFUND OF YOUR UNUSED RRSP CONTRIBUTIONS); or

• amounts you contr ibuted as a repayment or cancel lat ion payment to your RRSP under the Home Buyers ' Plan.

** Do not include:

• any amounts for which you or your spouse or common- law par tner d id not receive an of f ic ia l RRSP receipt ;

• contr ibut ions that represent lump-sum amounts ( for example, ret i r ing a l lowances) that your spouse or common- law par tner t ransferred to th is RRSP. However, you have to inc lude lump-sum amounts that represent contr ibut ions that your spouse or common-law par tner made to another RRSP dur ing the 89 day per iod just before your spouse's or common- law par tner 's wi thdrawal , and that he or she t ransferred to the RRSP indicated on l ine 5;

– 67 –

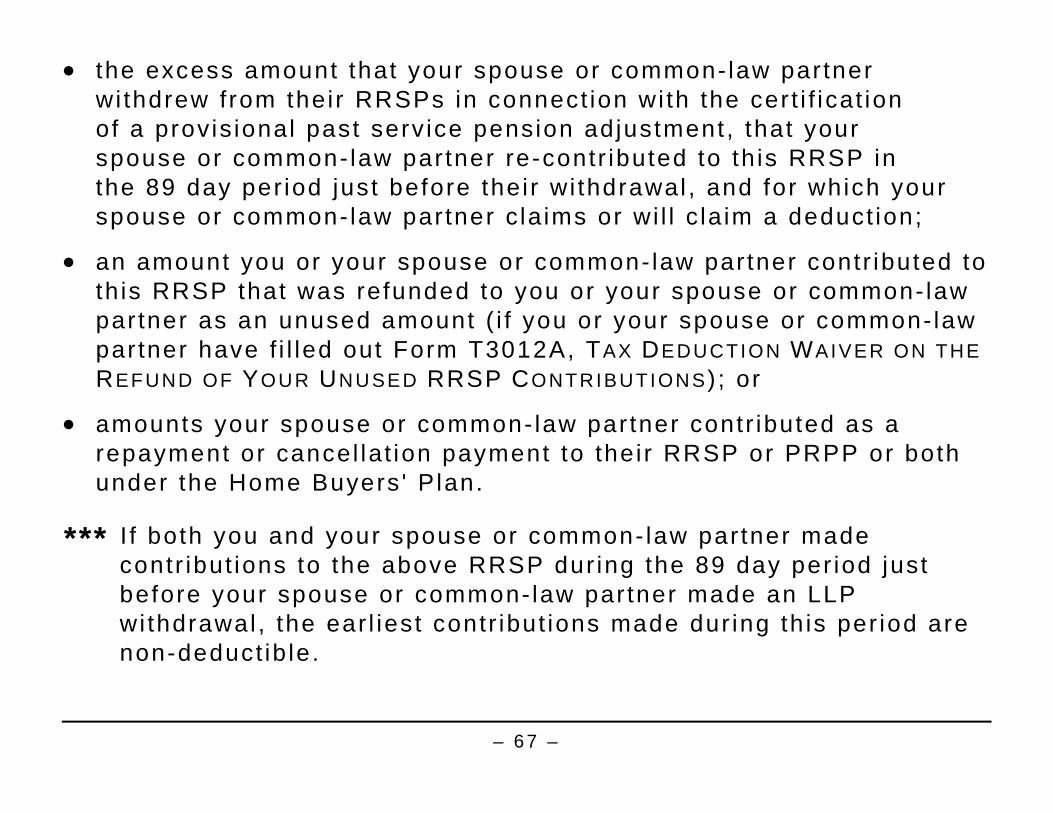

• the excess amount that your spouse or common- law par tner wi thdrew from their RRSPs in connect ion wi th the cer t i f icat ion of a provis ional past serv ice pension adjustment , that your spouse or common- law par tner re-contr ibuted to th is RRSP in the 89 day per iod just before thei r wi thdrawal , and for which your spouse or common- law par tner c la ims or wi l l c la im a deduct ion;

• an amount you or your spouse or common- law par tner contr ibuted to th is RRSP that was refunded to you or your spouse or common- law par tner as an unused amount ( i f you or your spouse or common- law par tner have f i l led out Form T3012A, TAX DEDUCTION WAIVER ON THE REFUND OF YOUR UNUSED RRSP CONTRIBUTIONS); or

• amounts your spouse or common- law par tner contr ibuted as a repayment or cancel lat ion payment to thei r RRSP or PRPP or both under the Home Buyers ' P lan.

*** I f both you and your spouse or common- law par tner made contr ibut ions to the above RRSP dur ing the 89 day per iod just before your spouse or common- law par tner made an LLP wi thdrawal , the ear l iest contr ibut ions made dur ing th is per iod are non-deduct ib le.

– 68 –

Online services

My Account The CRA's My Account serv ice is fast , easy, and secure.

Use My Account to :

• v iew your benef i t and credi t payment amounts and dates;

• v iew your not ice of assessment;

• change your address, d i rect deposi t in format ion, and mar i ta l s tatus;

• s ign up for account a ler ts ;

• check your TFSA contr ibut ion room and RRSP deduct ion l imi t ;

• check the status of your tax return;

• request your proof of income statement (opt ion 'C ' pr in t) ; and

• l ink between your CRA My Account and My Serv ice Canada Account .

– 69 –

How to register

For informat ion, go to canada.ca/my-cra-account .

Sign up for onl ine mail

Sign up for the CRA's onl ine mai l serv ice to get most of your CRA mai l , l ike your not ice of assessment onl ine.

For more informat ion, go to canada.ca/taxes-onl ine-mail .

MyCRA – Mobile app Use MyCRA throughout the year to:

• v iew the amounts and dates of your personal benef i t and credi t payments;

• check your TFSA contr ibut ion room;

• change your address, d i rect deposi t in format ion, and mar i ta l s tatus;

• le t us know i f a chi ld is no longer in your care;

• s ign up for onl ine mai l and account a ler ts ; and

– 70 –

• request your proof of income statement (opt ion "C" pr in t) .

Get t ing ready to f i le your income tax and benef i t return? Use MyCRA to:

• check your RRSP deduct ion l imi t ;

• look up a local tax preparer ; and

• see what tax f i l ing sof tware the CRA has cer t i f ied.

Done f i l ing? Use MyCRA to:

• check the status of your tax return; and

• v iew your not ice of assessment.

For more informat ion, go to canada.ca/cra-mobile-apps .

– 71 –

Electronic payments Make your payment using:

• your f inancia l inst i tu t ion 's onl ine or te lephone banking serv ices;

• the CRA's My Payment serv ice at canada.ca/my-cra-payment ; or

• pre-author ized debi t at canada.ca/my-cra-account .

For more informat ion on al l payment opt ions, go to canada.ca/payments .

For more information

What if you need help? I f you need more in format ion af ter reading th is guide, v is i t canada.ca/taxes or ca l l 1-800-959-8281 .

– 72 –

Electronic mailing l ists The CRA can not i fy you by emai l when new informat ion on a subject of in terest to you is avai lab le on the websi te. To subscr ibe to the e lectronic mai l ing l is ts, go to canada.ca/cra-email- l ists .

Forms and publications To get our forms or publ icat ions, go to canada.ca/cra-forms or cal l 1-800-959-8281 .

Guides

P105 Student and Income Tax

Forms

Schedule 7 RRSP and PRPP Unused Contr ibut ions, Transfers, and HBP or LLP Act iv i t ies

RC96 L i fe long Learning Plan (LLP) Request to Wi thdraw Funds f rom an RRSP

– 73 –

Tax Information Phone Service (TIPS) For personal and general tax in format ion by te lephone, use our automated serv ice, TIPS, by cal l ing 1-800-267-6999 .

Teletypewriter (TTY) users I f you have a hear ing or speech impairment and use a TTY cal l 1-800-665-0354 for b i l ingual assis tance.

I f you use an operator-assisted relay service , cal l our regular te lephone numbers instead of the TTY number.

Service complaints You can expect to be t reated fa i r ly under c lear and establ ished ru les, and get a h igh level of serv ice each t ime you deal wi th the CRA. See the TAXPAYER BILL OF RIGHTS.

I f you are not sat is f ied wi th the serv ice you received, t ry to resolve the matter wi th the CRA employee you have been deal ing wi th or cal l the te lephone number prov ided in the CRA's correspondence. I f you do not have contact in format ion, go to canada.ca/cra-contact .

– 74 –

I f you st i l l d isagree wi th the way your concerns were addressed, you can ask to d iscuss the matter wi th the employee's superv isor .

I f you are st i l l not sat is f ied, you can f i le a serv ice complaint by f i l l ing out Form RC193, SERVICE-RELATED COMPLAINT. For more in format ion and how to f i le a compla int , go to canada.ca/cra-service-complaints .

I f the CRA has not resolved your serv ice-re lated complaint , you can submit a complaint wi th the Off ice of the Taxpayers ' Ombudsman.

Reprisal complaint I f you bel ieve that you have exper ienced repr isal , f i l l out Form RC459, REPRISAL COMPLAINT.

For more informat ion about repr isal compla ints , go to canada.ca/cra-reprisal-complaints .

– 75 –

Tax information videos We have a number of tax in format ion v ideos for indiv iduals on topics such as the income tax and benef i t re turn, the Canadian tax system, and tax measures for persons wi th d isabi l i t ies. To watch our v ideos, go to canada.ca/cra-video-gal lery.