Embed Size (px)

Citation preview

lines of business as described above. In the last several years they have made strategic changes to compete as a full service I.T. company providing software development, web based application development, and network development solutions which include server back up and hosting services. They have also moved their document storage business line into the growing electronic storage and back up line of business instead of just being a hard copy storage company. With what hard copy storage they still offer, they have developed their own software to help store the documents in a quickly and easily accessible manner which provides them with a competitive advantage over other companies. Job Creation/Retention: With the last PIDA loan received in 2014, the company promised to retain 60 full time jobs. This loan will require the creation of 6 full time employees within 6 years which matches the job creation ratio for PIDA. PIDA permits borrowing $50,000 for each full time job promised to be created within 3 years. Retained jobs may not be counted twice for a company, but jobs created with Commonwealth loan money can be later retained by Commonwealth money. In this case, the retained jobs remain part of the promise of this Borrower’s last PIDA loan and this PIDA loan must promise 6 full time jobs to be created without regard to the 60 full time jobs they have promised to retain by the last lending project.

DCED-PIDA-006 (02-15) COMMONWEALTH OF PENNSYLVANIA

DEPARTMENT OF COMMUNITY & ECONOMIC DEVELOPMENT

CENTER FOR BUSINESS FINANCING

EXHIBIT FSUMMARY OF TERMS AND CONDITIONS

Please complete a separate sheet for each PIDA credit facility being requested.

Borrower:

Co-Borrower:

Loan Amount:

Purpose: The proceeds of the PIDA loan will be used to finance

Interest: % computed on a 30 /360 basis.

Term: months.

Payments: Principal and interest will be paid beginning the first day of the second month after closing with

an amortization schedule provided to the Borrower at closing.

Collateral Security: Security for this Loan:

As part of each collateral description below identify the following:a. The type of asset securing the loan & legal name of entity or individual(s) holding title to the asset

b. The lien position in favor of the certified provider / PIDA

c. The name of any lien holder that will be senior to or sharing the lien position with the certified provider/PIDA along with their respective lien position

d. The filing amount / original loan amount associated with each lien holder and the current balance of thefinancing if payment has been made on the loan

Overall Project Loan to Value =

The above terms and conditions were approved by the Loan Review Committee / Corporation on the______ day of

________________ 20__ in which a quorum was present.

Signature: _________________________________ Name, Title: _________________________________

Attest: _________________________________

None

$300,000

machinery and equipment purchases.

2.00

60

monthly

79%

1. First lien on machinery and equipment purchased with the project. Value of Specific Collateral: $381,000 Valuation Method: Purchase Price per quotes/invoices Effective Date of Valuation: Date of quote or invoice 2. Taken as an abundance of caution, last lien on all business assets of and affiliates subject to all other current and future lien holders 3 Unconditional and unlimited guarantee of 4. Corporate guarantees of all affiliates including

5. Subordination of any shareholder or inter-affiliate debt.

17thOctober 17

Capital Region Economic Development Corporation

Melissa Stone, VP

PERSONAL CASH FLOW AND FINANCIAL STATEMENT

AFFILIATES AND EFFECT

FINANCIAL CONTROLS

STRENGTHS1)2)3)

CONCERNS1)

2)

3)

ATTACHMENTS1)2)3)4)

, the owner and sole personal guarantor adds strength to this request. His adjusted personal networth is approaching $1MM and his personal liqudiity is approaching $300,000. His personal cash flow is very strong as well leaving excess cash flow available to support the company over $100,000 each year. You will note that is providing a single named guarantee. His financial statemetn is accurately reflected in single name only despite his marriage to . They have a prenup in place which has retained 's single claim to many assets and cash flow.

is owned 100% by . The affilaited companies include which is the company through which business equipment leases are accounted; which holds

, the primary business location; and which holds another piece of real estate purchased for document storage. To address how interrelated these companies are, CREDC is lending to the eligilble entity, that being but requiring the corporate guarantees of all affiliated entities mentioned above. There is also affiliated related debt between companies. while we are requiring all of the entities to guarantee, we have gone one step further to also require that those specific affiliate related notes be subordinate to our loan in payment and collateral position.

The complexity of this business model and the affiliated entities requires a full time controller to be on staff. is the Controller for all companies. He has 30 years experience in accounting and controller roles from his start out of college doing 10 years at KPMG as a Sr Mgr to functioning as the Controller at Cleveland Brothers, Waggoner Construction and now .

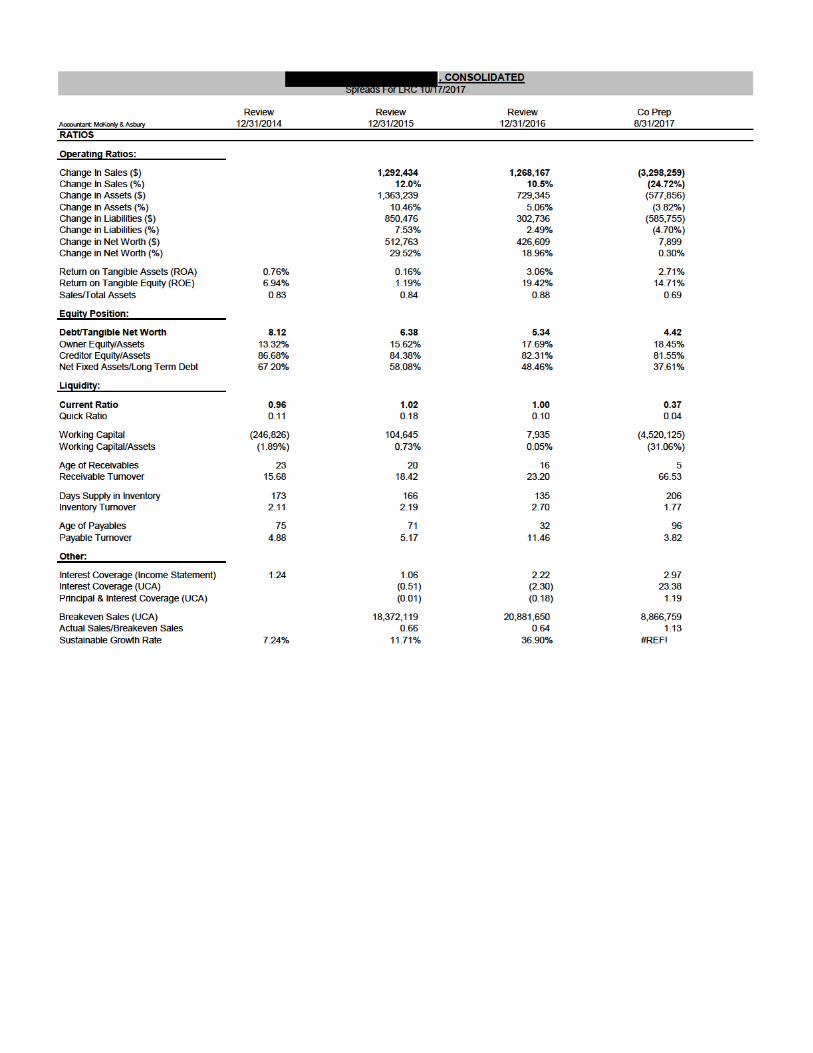

Growign revneues and net profit as a result of business strategy changesBusiness and global cash flow is strong for the past three years examined.1st lien position on equipment

Business in transition, however the past several years have shown that the new model has traction and is being managed appropriately.

Missing real estate collateral, but the remaining positions on real estate are subordinate where as our positionon this equipment is in sole first which gives us the ability to act quickly without consulting any other creditor involved.

Balance sheet ratios, however they are reflective of the emerging business model from one that was solely office equipment rental to a diversified business service company focusing on document retention and electronic solutions including an IT support desk and staffing company.

Personal Financial Summary, Personal Debt Schedule and Personal Cash FlowCompany debt schedule and DCRFinancial SpreadsCollateral Chart

Balance Payment

150,829$ 6,672$ 1,672,582$ 13,254$

58,000$ 3,462$ 20,072$ 624$ 18,491$ 571$ 15,422$ 459$ 19,916$ 446$ 13,277$ 477$

114,030$ 3,867$ Business assets and a vehicle78,863$ 2,595$ Business assets and a vehicle13,248$ 425$ 12,491$ 401$ 32,799$ 1,787$ 14,918$ 359$ 72,609$ 1,409$ 87,759$ 1,577$

1,269,754$ 15,524$ max payment - business assets786,919$ 4,806$ RE - 300,000$ 5,258$

TOTALS: 4,751,979$ 63,973$

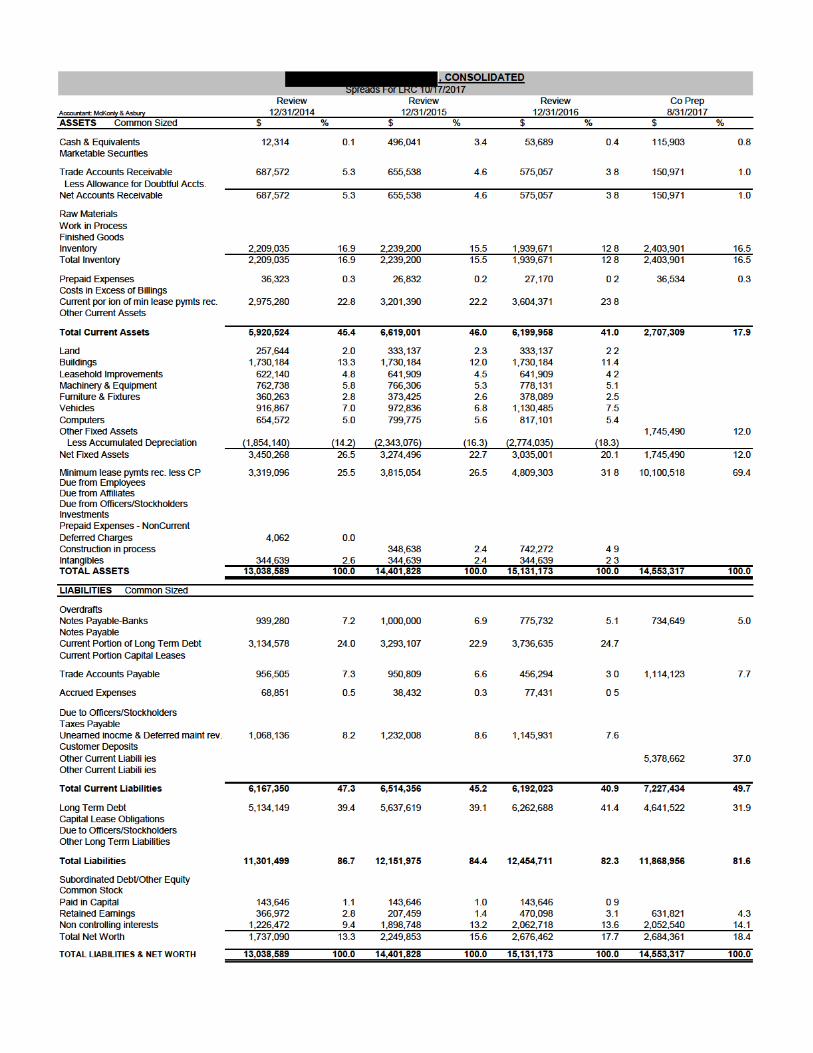

2014 2015 2016 2017 YTDGross Revenue 10,781,897$ 12,074,331$ 13,342,498$ 10,044,239$ Gross Profit 6,114,534$ 7,160,251$ 8,111,765$ 5,792,173$ Net Income 96,577$ 22,586$ 452,892$ 394,950$

Add Depr/Amort: 431,029$ 488,936$ 464,417$ 274,060$ Add Interest: 402,104$ 396,185$ 371,826$ 200,534$

Deduct: Distributions -$ (182,099)$ (190,253)$ -$ Add Bank Rent: 42,000$ 45,873$ 64,719$ 33,023$

Other adjustments: -$ -$ -$ -$ Other adjustments: -$ -$ -$ -$

Available CF 971,710$ 771,481$ 1,163,601$ 902,567$ DS: 767,676$ 767,676$ 767,676$ 511,784$

Coverage/ (Shortage) 204,034$ 3,805$ 395,925$ 390,783$ DSCR: 1.26:1 1:1 1.51:1 1.76:1

Notes:>

>

>

>

The largest note payable to M&T Bank of over $5MM is not refelcted in the debt service because of how the financials for this borrowing entity are preapred. The Borrower is and the note is a pre-approved commitment line to support the leasing activities of the company. What is reported on the income statement is not the total cash transaction. The M&T note funds the purchase of equipment which increases the liabiity due to M&T for this note, but also increases inventory which is an asset. When that equipment is leased, then the liability balance due to M&T is reduced with each and every lease payment made back to . The interest earned is top line revenue. And the interest paid on the M&T Note is interest expense.

Rent was added back because that was for the lease of property on St and the lease expired earlier this year, 2017. The space is not needed for that purpose any longer

There was an error in the foot note on the M&T Mortgage for …that monthly payment is corrected on this debt schedule

FNB of Mifflintown vehicle mat Sep 2020FNB of Mifflintown term matures jul 18Huntington vehicle matures Sept 2019Huntingtown vehicle matures Sept 2019FNB of Mifflintown term matures Aug 19FNB Mifflintown term matures July 2019Members 1st vehicle matures May 2019Ally Vehicle loan matreus Feb 2021Ally vehicle loan matures Dec 2019

COMPANY DEBT SCHEDULECreditor

EXISTING DEBT:

NEW SBF NOTEM&T mortgageFulton Bank equipment noteBMO Harris vehicles mat Feb 22FNB of Mifflintown vehicles mat aug 21

Rate/Term/Collateral

Cannon Equipment

vehicleSBF project equipement 1st lien

personal property and fixturesRE -

Nissan vehcicle loan Matures Oct 2019FNB vechicle loan, mat Oct 2019SBF loan mat Jan 2019M&T Bank mortgage loan mat Nov 2021M&T Bank term loan Matures Nov 2018

vehicle

multiple vehicleesmultiple vehicleesvehicleequipmentvehicle

COMPANY DEBT SERVICE COVEREAGE MODEL

vehicle

vehiclevehiclevehicle

Name:

Summary Balance Sheet 12/31/2016Cash & Equivalents 39,630$ Marketable Securities 225,000$ Personal Residence -$ Other Real Estate 745,000$ Cash Value Life Insurance -$ Other Investments 118,000$ Retirement Funds 265,522$ Closely Held Co's & N/R 3,360,068$ Personal Property 20,000$ Total Assets 4,773,220$

Current Payables -$ Mortgage(s) on Personal Residence -$ Other Mortgage Loans 373,300$ Other Term Debt 8,680$ Other Liabilities -$ Total Liabilities 381,980$

Net Worth 4,391,240$ Adjusted Net Worth 745,650$

Ratios 12/31/2016Liquid Assets/Total Assets 5.5%Equity in Personal Residence -$ LTV on Personal Residence #N/AEquity in Other Real Estate 371,700$ LTV on Other Real Estate 50.1%Debt to Worth 0.09xDebt to Adjusted Net Worth 0.51x

Notes:>

>

>

>

PERSONAL FINANCIAL STATEMENT SUMMARY

has also provided a personal guarantee on debt UNRELATED to and all consolidated related entities. These companies' financials are not being shared here. However, CREDC was part of the SBA 504 financing which supported those companies and can confirm that in real estate alone, those entities have asset values well exceeding that of the amount which has personally guaranteed.

The contingent liabilities balance which he has guaranteed related to and all consolidated related entities is $10.5MM. The total assets of consolidated and affiliated companies is $15.1MM or 1.4 times that of the debt.

Personally, his adjusted networth, which is the comparison of reasonably liquid assets to those matching liabilties is positive at $745K.

The contingent liabilities shown on 's PFS are all company related.

Name:

N/ABankruptcies 0

Satisfactories: 29Past Dues: 0

% Revolving Credit Available: 79%Transunion Fico Score: 807

Debt Service Monthly Annual UnpaidPayment Debt Svc. Balance

Mortgage Loans 3,233$ 38,796$ 373,300$ Auto & Other Installment Loans 1,097$ 13,164$ 8,680$ Credit Cards & Other Revolving Debt 15$ 180$ 885$ Business & Other Debt -$ -$ -$

Total Debt Service 4,345$ 52,140$ 382,865$

Mortgage LoansBank Monthly pymt Balance

#1 Orrstown Bank - Ave 808$ 77,900$ #2 Centric Bank - Ave 2,425$ 295,400$ #3 -$ -$ #4 -$ -$ #5 -$ -$

Auto & Other Installment LoansBank Monthly pymt Balance

#1 Land Rover loan 1,097$ 8,680$ #2 -$ -$ #3 -$ -$ #4 -$ -$ #5 -$ -$

Credit Cards & Other Revolving DebtBank Monthly pymt Balance

#1 PA Central FCU - personal line of credit $20,000 15$ 885$ #2 -$ -$ #3 -$ -$ #4 -$ -$ #5 -$ -$

Business & Other DebtBank Monthly pymt Balance

#1 -$ -$ #2 -$ -$ #3 -$ -$

PERSONAL DEBT SCHEDULE

10/15/17CREDIT REPORT SUMMARY

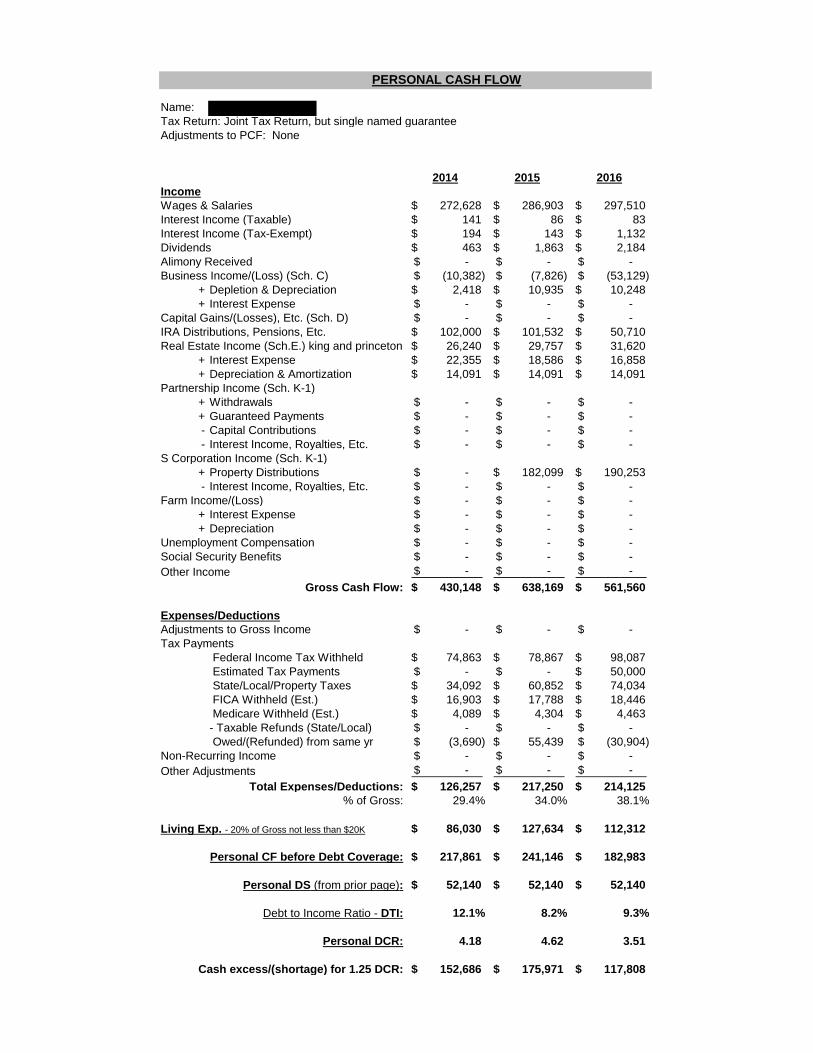

Name:Tax Return: Joint Tax Return, but single named guaranteeAdjustments to PCF: None

2014 2015 2016IncomeWages & Salaries 272,628$ 286,903$ 297,510$ Interest Income (Taxable) 141$ 86$ 83$ Interest Income (Tax-Exempt) 194$ 143$ 1,132$ Dividends 463$ 1,863$ 2,184$ Alimony Received -$ -$ -$ Business Income/(Loss) (Sch. C) (10,382)$ (7,826)$ (53,129)$

+ Depletion & Depreciation 2,418$ 10,935$ 10,248$ + Interest Expense -$ -$ -$

Capital Gains/(Losses), Etc. (Sch. D) -$ -$ -$ IRA Distributions, Pensions, Etc. 102,000$ 101,532$ 50,710$ Real Estate Income (Sch.E.) king and princeton 26,240$ 29,757$ 31,620$

+ Interest Expense 22,355$ 18,586$ 16,858$ + Depreciation & Amortization 14,091$ 14,091$ 14,091$

Partnership Income (Sch. K-1)+ Withdrawals -$ -$ -$ + Guaranteed Payments -$ -$ -$ - Capital Contributions -$ -$ -$ - Interest Income, Royalties, Etc. -$ -$ -$

S Corporation Income (Sch. K-1)+ Property Distributions -$ 182,099$ 190,253$ - Interest Income, Royalties, Etc. -$ -$ -$

Farm Income/(Loss) -$ -$ -$ + Interest Expense -$ -$ -$ + Depreciation -$ -$ -$

Unemployment Compensation -$ -$ -$ Social Security Benefits -$ -$ -$ Other Income -$ -$ -$

Gross Cash Flow: 430,148$ 638,169$ 561,560$

Expenses/DeductionsAdjustments to Gross Income -$ -$ -$ Tax Payments

Federal Income Tax Withheld 74,863$ 78,867$ 98,087$ Estimated Tax Payments -$ -$ 50,000$ State/Local/Property Taxes 34,092$ 60,852$ 74,034$ FICA Withheld (Est.) 16,903$ 17,788$ 18,446$ Medicare Withheld (Est.) 4,089$ 4,304$ 4,463$ - Taxable Refunds (State/Local) -$ -$ -$ Owed/(Refunded) from same yr (3,690)$ 55,439$ (30,904)$

Non-Recurring Income -$ -$ -$ Other Adjustments -$ -$ -$

Total Expenses/Deductions: 126,257$ 217,250$ 214,125$ % of Gross: 29.4% 34.0% 38.1%

Living Exp. - 20% of Gross not less than $20K 86,030$ 127,634$ 112,312$

Personal CF before Debt Coverage: 217,861$ 241,146$ 182,983$

Personal DS (from prior page): 52,140$ 52,140$ 52,140$

Debt to Income Ratio - DTI: 12.1% 8.2% 9.3%

Personal DCR: 4.18 4.62 3.51

Cash excess/(shortage) for 1.25 DCR: 152,686$ 175,971$ 117,808$

PERSONAL CASH FLOW

![Synthesis and physical properties of several aliphatic and ... · work on the acetylenic hydrocarbons is described in a previl)us paper [12] . The work described herein is the part](https://img.pdfslide.net/doc/110x75/5e50b182bc98a91e8e559c14/synthesis-and-physical-properties-of-several-aliphatic-and-work-on-the-acetylenic.jpg)