Embed Size (px)

Citation preview

LIVE IN L.A.

Your all access pass to complete Wealth Management

Strategic Planning with Corporate Class

Brent Steele, B. Comm, CA, CFP

Regional Vice-President, Wealth Planning

Goals of our session

• Talking to COIs• Practical considerations and planning opportunities

What an accountant sees at tax time

• Management fees • Relatively low corporate class distributions• Realized gain / loss on redemptions

But no idea of unrealized gain on account!

Tax Rates on Investment Income

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

Interest/Foreign Eligible Dividends Realized Capital Gains Unrealized Capital Gains

After-Tax Tax Rate

49.53%

33.85% 24.76%

50.47%

66.15% 75.24%

100%

2013 Top personal tax rates - Ontario

Why corporate class investment structures?

Desire by clients to:• Defer tax • Earn tax efficient investment income• Control the timing of when they pay tax

Business structures – cyclical businesses

Business Revenue Expenses Income Rate LiabilityCorporation A 150,000$ 200,000 (50,000)$ 25% -$ Corporation B 100,000$ 50,000 50,000$ 25% 12,500$ Corporation C 200,000$ 175,000 25,000$ 25% 6,250$

450,000$ 425,000 25,000$ 18,750$

Corporation ABCDivision A 150,000$ 200,000 (50,000)$ Division B 100,000$ 50,000 50,000$ Division C 200,000$ 175,000 25,000$

450,000$ 425,000 25,000$ 25% 6,250$

Multiple Corporations

One Corporation – Multiple Divisions

Investments - markets are cyclical

Source: United Financial

Investment structures

• Segregated holdings– Individual stocks, bonds, income trusts,

GICs, etc.

• Mutual fund trusts– Traditional pooled or mutual funds– Defined in paragraphs 132(6) & (7) of ITA

• Mutual fund corporation– A.K.A. corporate class– 131(8) of ITA

Similar tax consequences to the investor

Unique tax consequences to the investor

Segregated Holdings Mutual Fund Trusts "Corporate Class"

- stocks- bonds

- income trusts- term deposits - stocks - stocks

- T-bills - bonds - bonds- income trusts - income trusts- term deposits - term deposits

- T-bills - T-bills

Investor Investor Investor

Investment structures

Mutual fund trusts- Separate trusts

- Income maintains its form

Mutual fund corporation- Single corporation

- Dividends and capital gains only

What is corporate class?

• Taxation of a mutual fund corporation• Investor’s experience

How is a mutual fund corporation designed to work?

For illustrative purposes only

Taxable CapitalReturn Gains/(Losses)

Fixed income 20,000$ Fixed income (500)$ Cdn equity 2,500 Cdn equity (2,000) U.S. equity 2,250 U.S. equity 3,000

Foreign equity 3,250 Foreign equity 2,750 28,000$ 3,250$

Deductible Capital GainsExpenses Refund Mechanism

Fixed income 6,500$ (2,750)$ Cdn equity 7,000 S. 131(2) of ITAU.S. equity 7,000

Foreign equity 7,000 27,500$

Net income 500$ Distribution 500$ Dividend distribution to shareholders ortaxed inside mutual fund corporation

Capital gain distributionto shareholders

Typical diversified investment portfolio

40%

22%

20%18%

Income

Canadian Equity

U.S. Equity

Int'l Equity

Tax on typical diversified investment portfolio

Asset Portion of Return On Interest / Eligible Realized UnrealizedClass Portfolio Investment Other Dividends Cap Gains Cap Gains

Income 40% 4.99% 4.11% 0.14% 0.16% 0.59%Canadian Equity 22% 8.57% 0.41% 1.91% 0.99% 5.26%US Equity 20% 9.00% 1.81% 0.01% 0.13% 7.04%Int'l Equity 18% 9.25% 3.13% 0.00% 0.12% 6.00%

Portfolio Performance 7.34% 2.66% 0.48% 0.33% 3.88%

Portfolio investment 1,000,000$ 73,440$ 26,577$ 4,760$ 3,288$ 38,815$ Tax rates 46.41% 29.54% 23.21% 0.0%Tax liability 14,504$ 12,335$ 1,406$ 763$ -$ Average tax on performance 19.7%

Disclosure: Return on investment is based on projected hypothetical returns (pre-fees) for each mutual fund trust pool in the proposed portfolio asset mix and distributions are based on mutual fund trust pools averaged over the period from 2007 to 2012. Individual is in the top federal marginal tax bracket and resident in Ontario.

Tax on corporate class investment portfolio

$1,822 of tax versus $14,504 on non-corporate class structure

Difference of $12,682

Asset Portion of Return On Interest / Eligible Realized UnrealizedClass Portfolio Investment Other Dividends Cap Gains Cap Gains

Income 40% 4.99% 0.00% 0.55% 0.00% 4.44%Canadian Equity 22% 8.57% 0.00% 1.05% 0.00% 7.52%US Equity 20% 9.00% 0.00% 0.61% 0.00% 8.38%Int'l Equity 18% 9.25% 0.00% 0.25% 0.00% 9.00%

Portfolio Performance 7.34% 0.00% 0.62% 0.00% 6.73%

Portfolio investment 1,000,000$ 73,440$ -$ 6,168$ -$ 67,272$ Tax rates 46.41% 29.54% 23.21% 0.0%Tax liability 1,822$ -$ 1,822$ -$ -$ Average tax on performance 2.5%

Disclosure: Return on investment is based on projected hypothetical returns (pre-fees) for each Corporate Class share in the proposed portfolio asset mix and distributions are based on Corporate Class shares averaged over the period from 2011 to 2012. Individual is in the top federal marginal tax bracket and resident in Ontario.

Tax-deductible fees

$1,000,000 portfolio from previous example:

For illustrative purposes only

For illustrative purposes only

Non-Corp Subject Corp SubjectClass to Tax Class to Tax

Return on investment 73,440$ 73,440$

Interest 26,577 26,577 - - Dividends 4,760 138% 6,569 6,168 138% 8,512 Capital gains 3,288 50% 1,644 - 50% - Unrealized capital gains 38,815 67,272

Fees 1,000,000$ 2.32% (23,200) 1,000,000$ 2.32% (23,200)

Net inclusion (deduction) 11,590$ (14,688)$

Corporate Class: After-tax benefits

Corporate Class Structure – Benefits

• Ability to grow assets by deferring taxes• Opportunity to switch or rebalance among funds

without tax implications • Ability to receive tax-efficient capital gains or

Canadian dividends from traditional income funds• Opportunity to withdraw funds on a tax deferred

basis using return of capital versions of funds (T-Class)

• Ability to better control when taxes are paid

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Corporate Class Non-CorporateClass

FM V

A CB

Sample client – accumulation years• Age 40 to age 60• $25K/year for 20 years• Diversified portfolio averaging 5.3%• Income taxes are paid out of the portfolio $1,265,500

$1,094,300

For illustrative purposes only

Retirement years – Option #1

Match the cash flow over 25 years• Non-corporate class provides approximately

$41,350/year after-tax– After 25 years, account is $0

• Corporate class provides same $41,350/year after-tax– After 25 years, account has $1,568,000– Provides $1,210,000 on an after-tax basis

Retirement years – Option #2

Maximum cash flow over 25 years• Non-corporate class provides approximately

$41,350/year after-tax– After 25 years, account is $0

• Corporate class provides $66,550/year after-tax– After 25 years, account is $0

Corporate class inside an investment holdco

Corporate Class:Planning Opportunities

Corporate class planning tips

1. Corporate class may allow investors to use capital losses earlier– Significant portion of return on investment takes the form of

realized/unrealized capital gains, which can be fully offset by previous capital losses

2. Corporate class means that income splitting with investment dollars may no longer make sense.– Keep tax deduction with higher income-earning family member

3. Fee deduction may help offset high-tax corporate income– ABI > $500K and other forms of investment income

(eg. interest, foreign, rental income)4. Corporate class allows for even more efficient charitable donation planning

– Take advantage of 0% inclusion rate when donating marketable securities

– Bonus savings when donating securities through a corporation

Charitable donation planning using corporate funds (2013 Ontario rates)

$2M growth

$1M ACB

$1M 19 yrs $3M6%

Investment Holdco

Donate $30K cash:

- Capital gain of $20K

- Corp tax = $4,620

- CDA = $10K

Donate $30K in-kind:

- Capital gain of $20K

- Corp tax = $0

- CDA = $20K

Option #1 Option #2

For illustrative purposes only

Ideal clients for corporate class

• Personal or corporate clients subject to high tax rates on investment income

• Seniors looking for tax efficient retirement cash flow• Investors who want to hold a diversified portfolio and

want to rebalance over time• Investors looking for better control over when they

pay tax

Practical considerations and planning opportunities for advisors

Individuals – Don’t miss out on tax credits and deductions• Utilize dividend tax credit and management fee deduction – sometimes

the fact that a client paid no tax in a given year means we may have missed an opportunity.

– If a client has little other income and a large non-registered corporate class account, certain non-refundable tax credits (e.g. dividend tax credit, personal amount, age amount, medical expense tax credit) and other tax credits (e.g. donation credit) may go unused.

– Similarly, management fees that exceed other sources of income may create a non-capital loss or result in low tax brackets going unused.

– May be an opportunity to trigger unrealized gains on an annual basis to utilize above.

Individuals currently invested with a broker

• Brokerage accounts typically have heavy weighting in Canadian stocks.

• Canadian stocks often have significant portion of return in form of dividends which create a dividend tax credit – if client has no other income, can receive between $24,000 and $49,000 of eligible dividends tax-free depending on province of residence.

• Start the conversation from an investment perspective – if they are convinced they want an actively managed diversified portfolio, then without corporate class they will have interest and foreign income and capital gains from rebalancing.

• Canadian dividends are grossed up by 38% – potential impact on OAS claw back when net income exceeds $70,954 ($1 of dividend / $1.38 taxable / 20.7% clawback not 15%).

Prospective clients

Dealing with unrealized gain – compare tax cost of triggering gains on existing portfolio with “pay back period” of corporate class – Lower distributions and reduced capital gains with corporate class– Potential non-capital loss carries back for next 3 years if corporate class

management fees exceed other sources of income

Important line items on personal tax return– Taxable amount of dividends – line 120 and sch.4– Interest and other investment income – line 121 and 130, sch. 4– Carrying charges – line 221, sch. 4– Social benefits repayment (OAS claw back) – line 422

Trusts – practical considerations

• Need to review trust document (trust agreement for inter-vivos trusts / will or other document for testamentary trusts) to determine if corporate class is appropriate investment

– Are the income and capital beneficiaries different?

• If so, are capital gains treated as income or capital in the agreement?

• Default is that capital gains are capital for trust law purposes

– Given significant portion of return from corporate class can come in the form of capital gains, may favour capital beneficiaries over income beneficiaries

Trusts – practical considerations

• No ability to flow through losses (e.g. unused management fees) to beneficiaries

• Similar to individuals who may want to annually trigger unrealized gains to:– utilize non-refundable tax credits (e.g. dividend tax

credit)– utilize lower marginal tax brackets (testamentary

trusts only)– flow taxable income out to low income beneficiaries

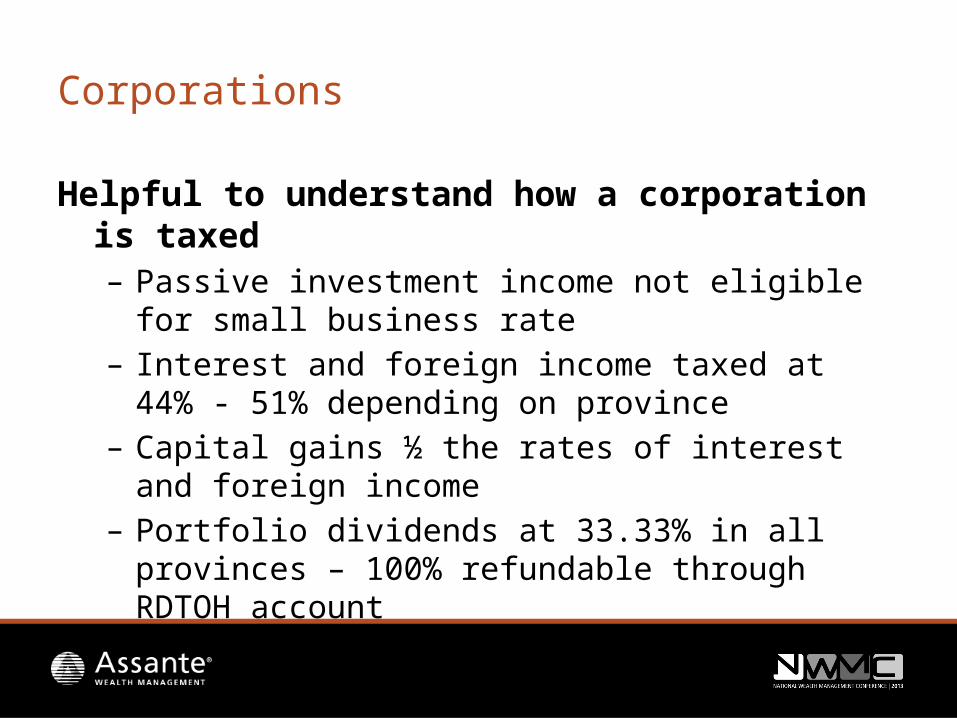

Corporations

Helpful to understand how a corporation is taxed– Passive investment income not eligible for small

business rate– Interest and foreign income taxed at 44% - 51%

depending on province– Capital gains ½ the rates of interest and foreign

income– Portfolio dividends at 33.33% in all provinces – 100%

refundable through RDTOH account

Corporate Tax Accounts of Interest

RDTOH – Refundable Dividend Tax on Hand account (temporary tax)

• Refundable portion of Part I tax assessed on investment income (26.67% Cdn/17.33% Foreign)

• Part IV tax on Canadian dividends received (33.33%)

Dividend Refund

• $1 from RDTOH for every $3 of taxable dividends paid

• All taxable dividends paid by a CCPC generate a dividend refund to the extent RDTOH exists

• $1 of dividend received from our corporate class will result in no corporate tax payable if distributed to the shareholder

RDTOH

Utilizing non-capital losses inside a corporation

• Unused tax deductible management fees inside a corporation create non-capital losses to carry forward.

• Opportunity exists to crystallize unrealized gains to use non-capital losses and create CDA.

– CDA created will allow for tax-free payment to the shareholder – consider where shareholder personally requires access to corporate investments.

• Alternatively, accountant may use current year or previous year’s non-capital losses to offset Part IV tax on dividend income (need to determine if it makes sense to use against this temporary tax).

• Can also carry back 3 years to offset previous gains (e.g. gains realized on transfer into corporate class).

T-Class – ideal clients

• First step – quantify gain that would be triggered on SWP without T-Class and corresponding tax payable

– Brand new clients have ACB = FMV, i.e. no gain

– Management fees reduce taxable income

• Additional income for seniors may trigger OAS clawback

• Individuals currently in a high tax bracket who expect to be in a lower tax bracket in the future will benefit from the deferral

• Individuals who intend to donate corporate class shares in the future

4

T-Class – corporate clients

T-Class inside a corporation is only beneficial in select circumstances – Eliminates corporate tax on SWP – but would tax deduction created by

management fees offset tax on gain without T-Class?– Are funds from SWP being retained inside corporation or being paid out to

the shareholder?– If funds are being paid out to shareholder, what if any personal tax is

payable?• Tax free withdrawals if shareholder loan exists, high PUC on shares

(limited circumstances), capital dividend account balance exists • Generally combined corporate and personal tax is less with regular

SWP vs. use of T-Class given CDA created with SWP

Thank you

For advisor use only

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise indicated and except for returns for periods less than one year, the indicated rates of return are the historical annual compounded total returns including changes in security value. All performance data assume reinvestment of all distributions or dividends and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Assante Wealth Management’s advisory services are offered through Assante Financial Management Ltd., Assante Capital Management Ltd. and Assante Estate and Insurance Services Inc. Assante Estate and Insurance Services Inc. is owned by Assante Financial Management Ltd. and Assante Wealth Management (Canada) Ltd. ®The Assante symbol and Assante Wealth Management are registered trademarks of CI Investments Inc., used under licence.