Embed Size (px)

Citation preview

Living Benefits Business Solutions

Reducing the financial risk of disability

What are the odds of disability?

Number of Business Owners

Age 2 3 4 5

30 66 (23) 80 (32) 88 (40) 93 (48)

35 63 (22) 78 (31) 86 (39) 92 (47)

40 60 (21) 75 (30) 84 (38) 90 (45)

45 55 (20) 70 (29) 80 (37) 87 (43)

50 49 (19) 63 (27) 74 (34) 81 (40)

(probability of death in brackets)

Source: 1985 Commissioner’s Disability Table A (Experience Table) CIA 86-92 Aggregate Mortality Table

The % probability of at least one long-term disabilitylasting at least 90 days before age 65

How long do disabilities last?

Age % DisabledAverage duration

25 44% 2.4 years

30 42% 3.2 years

35 40% 3.4 years

40 37% 3.9 years

45 33% 4.2 years

50 28% 4.7 years

Percentage of people who will become disabled for at least 90 days prior to age 65 and average duration of disability

Source: 1985 Commissioner’s Disability Table A (CIDA), blended 50/50 male/female and 50/50 accident/sickness

What are the chances of being disabled for life?

Age Male Female

30 2.90% 4.18%

50 13.61% 15.44%

Chances of being disabled for life if already disabled at least 90 days.

Source: 1985 Commissioner’s Disability Table A (Experience Table)

Expenses continueExpenses continue

Disability and your business – revenue and expenses

30 60 90 120 180 365

$

Days

Savings /Revenue

Onset ofDisability

Disability and your business – workload and staff

Workload continues

Staffing decreases

Knowledge, expertise and goodwill decrease

Disability and your business – decision making

Owner 1

Owner 2

??

Disabled owner

Disability and your business – new conflicts of interest

EmployeesEmployees

Other ownersOther owners

ClientsClients

FamilyFamily

RecoveryRecovery

CreditorsCreditors

SuppliersSuppliers

BusinessBusiness

Disabled Owner

Where will the money come from?

Who decides when the owner is permanently disabled?

Will the owner relinquish his/herinterest in the business?

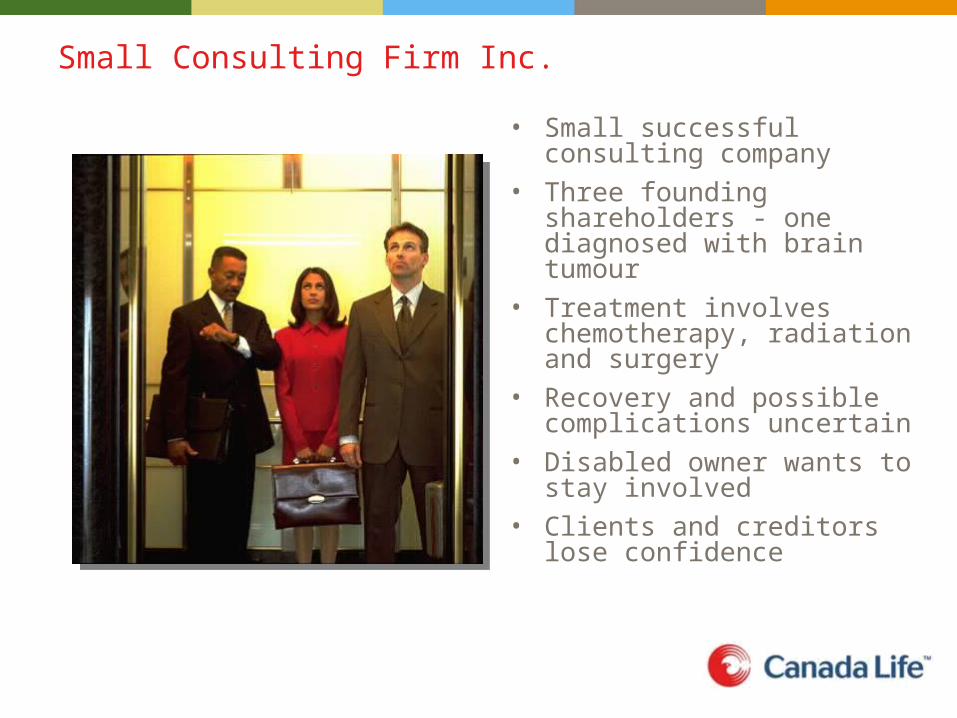

Small Consulting Firm Inc.

• Small successful consulting company

• Three founding shareholders - one diagnosed with brain tumour

• Treatment involves chemotherapy, radiation and surgery

• Recovery and possible complications uncertain

• Disabled owner wants to stay involved

• Clients and creditors lose confidence

Small Consulting Firm Inc.

• Business losing money – need to cut salaries. Who to cut?

• Six months later, other owners want to move on.

• Owners discuss purchase and disabled owner not willing to take reduced purchase price.

• Call the bank for loan to buy out - disabled owner a major concern. Not granted.

Small Consulting Firm Inc.

• One year later – have hired replacement. At 18 months, business back on track.

• At two years, owner still disabled. Business making profit. Wants to hold interest.

• Disabled owner’s family financially challenged. Wants full value + of ownership. Threatening, but can’t afford legal action.

• What can they do? How?

Fair market value

• “The amount at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of the relevant facts.”*

*Black’s Law Dictionary, sixth edition

Disability and your business – choices you must make

1. Do nothing

2. Dissolve the business

3. Buy out the disabled owner’s share

i. When?

ii. How much?

iii. Where will you get the money?

a. Cash flow?

b. Loan?

4. Insurance funded buy/sell agreement.

Disability insurance buy/sell plan

• Protection against potentially costly and unproductive drain on the business with a fixed business expense

• Suppliers and creditors may be reassured - business owners have a plan with appropriate funding

• Demonstrates sound business management and may help attract quality employees

Disability insurance buy/sell plan

• Can provide disabled owner fair market value for their share of business

• Policy wording provides clear definition of disability

• 365 or 720 day waiting period

Some Disability Buy/Sell structures – purchase by business

OwnerOwner

BusinessBusiness

Disabledowner

Disabledowner

Canada LifeCanada Life

$

$ Shares / ownership interest

Some Disability Buy/Sell structures – cross purchase

OwnerOwner

BusinessBusiness

Disabledowner

Disabledowner

Canada LifeCanada Life

$

$

Shares / Ownership interest

Some Disability Buy/Sell structures – trust

OwnerOwner

BusinessBusiness Disabledowner

Disabledowner

Canada LifeCanada Life

$

Shares / Ownership interest

TrusteeTrustee

$OwnerOwner

DI Buysell Structure - Considerations

• Capital Gain/Loss on sale

• Capital Dividend Account not available

• Adjusted cost base

• Premium imbalance

What are the costs?

Buy/Sell Plan Monthly Premium Potential Financial Impact of Disability

John, 40 years old.

$250,000 Buy/Sell Plan, 365 Day Waiting Period

$118.40 Salary to disabled owner

$100,000

Jane, 40 years old.

$250,000 Buy/Sell Plan, 365 Day Waiting Period

$158.90 Business valuation $15,000

Legal and accounting fees

$10,000

Lost revenue $150,000

Lost market value of business

$250,000

Total $277.30 Total $525,000

Source: Canada Life Buy/Sell Plan premium. Occupation class 5 non-smokers. (Zoom 9.1)

The Solution

• Disability insurance funded buy/sell agreement

• Non-cancellable buy/sell funding

• Clear definition of disability

• Third party to decide disability, triggering agreement

• Minimize disputes among shareholders / partners

Additional considerations

• Maximum buy/sell coverage is $1,000,000 per business owner

What can you do when value ofIndividual ownership interestexceeds $1,000,000?

Possible solution

Critical illness funded buy/sell agreement

• Coverage up to $2,000,000*

• Note – technical considerations of agreement may be different from disability buy/sell

• Payment at 30 days from diagnosis, not 365 or 720 days

• Structural considerations may vary, terms need to be negotiated between the parties

*Subject to underwriting. Other inforce disability or critical illness coverage would be considered in determining how much additional coverage is available.

Business Expenses

Personal Expenses

Disability and your business – covering the risks

30 60 90 120 180 365

$

Days

Savings /Revenue

Onset ofDisability

Salaries, rent, phones, leases, interest, legal fees, accounting fees, business taxes, utilities, business insurance…

Mortgage, groceries, vehicles, clothing, utilities, taxes, monthly bills, medical expenses..

Overhead Expense Plan

Key Person Plan

Individual Disability

Bu

y / Se

ll lump su

m

Business expensesSTOP

Business expensesSTOP

Personal expensescontinue

Personal expensescontinue

Critica

l Illness

lump su

m

The Big Picture

30 60 90 120 180 365

Individual Disability

Bu

y / Se

ll Lum

p S

um

Overhead Expense Plan

$

Business liabilitiesSTOP

Business liabilitiesSTOP

Personal liabilitiescontinue

Personal liabilitiescontinue

Keyperson Plan

Critica

l Illness lu

mp

sum

Days

Savings /Revenue

Onset ofDisability

Keyperson Disability Reimbursement Plan

Source: Canada Life Keyperson Plan

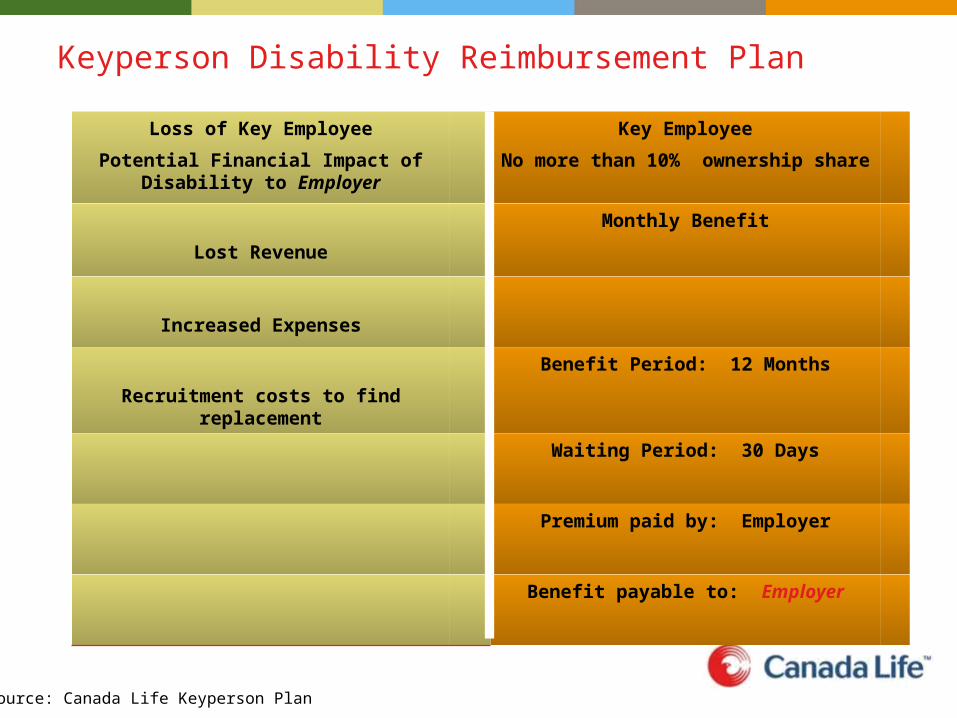

Keyperson Disability Reimbursement Plan

Loss of Key Employee

Potential Financial Impact of Disability to Employer:

Lost Revenue

Increased Expenses

Recruitment costs to find replacement

Source: Canada Life Keyperson Plan

Keyperson Disability Reimbursement Plan

Loss of Key Employee

Potential Financial Impact of Disability to Employer

Key Employee

No more than 10% ownership share

Lost Revenue

Monthly Benefit

Increased Expenses

Recruitment costs to find replacement

Benefit Period: 12 Months

Waiting Period: 30 Days

Premium paid by: Employer

Benefit payable to: Employer

Source: Canada Life Keyperson Plan

Business Needs: Living Benefits

• Individual Disability Income

• Personal expenses (monthly income replacement)

• Overhead Expense

• Reimbursement of business expenses

• DI Buysell

• Funding for disability buyout agreement

• Keyperson Disability Reimbursement

• Monthly benefit to help company adjust to loss of key person

• ‘Grouped’ Critical Illness

• Individual CI plans for 2+ employees

• Wage Loss Replacement Plan

• Individual DI for 2+ employees

Living Benefits: Smoker?

• How many:

• Cigars?

• Cigarillos?

• How much:

• Chewing tobacco?

Turn a smoker into a non-smoker

For DI and CI only

• Must not have smoked cigarettes or used marijuana within the past 12 months

• All other forms of tobacco use will be considered non-smoker

• No quantity limitations

• Cigar, pipe, cigarillos

“Premier Value” Premium Reduction: 10%

• Employees or active owners of the same business or professionals sharing office space and expenses

• At least 3 applications must be submitted at the same time

Thank You