Embed Size (px)

DESCRIPTION

LNG World Shipping’s coverage of the global LNG shipping industry is the best there is. The journal covers the full length of the LNG maritime transport chain, from offshore developments at the upstream end, through conventional LNG carriers and terminals, to small-scale LNG at the consumer end. Six issues are published each year, each containing in-depth profiles of ships and operators, fleet statistics, summary of key international news and the views of leading industry figures. “LNG World Shipping is the number one publication for the LNG shipping industry and the most informative and up to date source of information for all things LNG and shipping!” - Duncan Gaskin, Bestobell LNG Valves Each bi-monthly issue features complete and exclusive listings of the world’s LNG carrier fleet, expert analysis of key market developments, and authoritative features about ship technology and the commercial markets served by LNG carriers. Profiles of ships, operators, regions, equipment, service

Citation preview

May/June 2016 www.lngworldshipping.com

The ship-shore interface:LNG shipping’s weakest link

FSRUs: a story of growth

Europe ramps up its LNG imports

“Oversupply of LNG has to find new markets – and small-scale and bunkering are two

of the most promising places where this LNG can go”

Dag Lillevedt, chief executive, Fuelgarden, see page 9 of supplement

Safety Meansthe World to Us

GasLog’s reputation has been earned as one of the world's leading owners, operators and managers of LNG Carriers.

As each ship leaves port we are keenly aware of our responsibility toward ensuring the safe passage of our people, our cargoes

and our environment.

Our attention to detail is a reflection of our company's valuesand a demonstration of our dedication.

www.gaslogltd.com

contentsMay/June 2016

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

08

13

16

18

Comment 5 Australia industry summit finds the international LNG community in a sadder,

wiser mood

Analysis6 Thirteen things we’ve learned from the new International Group of LNG

Importers (GIIGNL) annual LNG report

8 Europe is emerging as a critical LNG-import market, as it seeks to cut its

dependence on piped gas from Russia and to diversify its energy sources. Mike

Corkhill reports

Conference13 LNG World Shipping’s forthcoming London conference will discuss the ship-

shore interface, the weakest point in the LNG supply chain

Operations16 As more ports start to import, export and supply LNG as marine fuel, escort

tugs will become ever more important in mitigating risk. Selwyn Parker reports

Exports 18 Plans by Mozambique and Tanzania to tap and export their vast gas reserves

may create a new LNG hotspot in east Africa. Diana Taremwa Karakire reports

Cargo handling21 Mike Corkhill reports on how US researchers are assessing the risks of methane

leakage during LNG bunkering in the drive to gut greenhouse-gas emissions

Offshore24 New buyers of LNG are turning to floating storage and regasification units

(FSRUs) as the fastest, cheapest way to import. Karen Thomas reports on a

growing LNG business

Infographic26 Your exclusive LNG World Shipping guide, showing the world FSRU fleet

and the import markets that will drive demand for new offshore terminals

contentsMay/June 2016

Editor: Karen Thomast: +44 20 8370 1717e: [email protected]

Consultant Editor: Mike Corkhillt: +44 1825 764 817e: [email protected]

Sales Manager: Ian Powt: +44 20 8370 7011e: [email protected]

Production Manager: Richard Neighbourt: +44 20 8370 7013e: [email protected]

Subscriptions: Sally Churcht: +44 20 8370 7018e: [email protected]

Korean Representative: Chang Hwa Park Far East Marketing Inc t: +82 2730 1234 e: [email protected] Japanese Representative: Shigeo Fujii Shinano Co Ltd t: +81 335 846 420 e: [email protected]

Chairman: John LabdonManaging Director: Steve LabdonFinance Director: Cathy LabdonOperations Director: Graham HarmanEditorial Director: Steve MatthewsExecutive Editor: Paul GuntonHead of Production: Hamish DickieCorporate Portfolio Manager: Bill Cochrane

Published by:Riviera Maritime Media LtdMitre House 66 Abbey RoadEnfield EN1 2QN UK

www.rivieramm.com

ISSN 1746-0603 (Print)ISSN 2051-0616 (Online)

©2016 Riviera Maritime Media Ltd

Total average net circulation: 4,000Period: January-December 2015

A member of:

Disclaimer: Although every effort has been made to ensure that the information in this publication is correct, the Author and Publisher accept no liability to any party for any inaccuracies that may occur. Any third party material included with the publication is supplied in good faith and the Publisher accepts no liability in respect of content. All rights reserved. No part of this publication may be reproduced, reprinted or stored in any electronic medium or transmitted in any form or by any means without prior written permission of the copyright owner.

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

Subscribe from just £299Subscribe now and receive six issues of LNG World Shipping every year and get even more:• supplements: LNG Carrier Lifecycle Maintenance, Small-Scale LNG, Offshore LNG and Ballast Water Treatment Technology• access the latest edition content via your digital device• free industry yearplanner including key dates• access to 'web address' and its searchable archive.Subscribe online: www.lngworldshipping.com

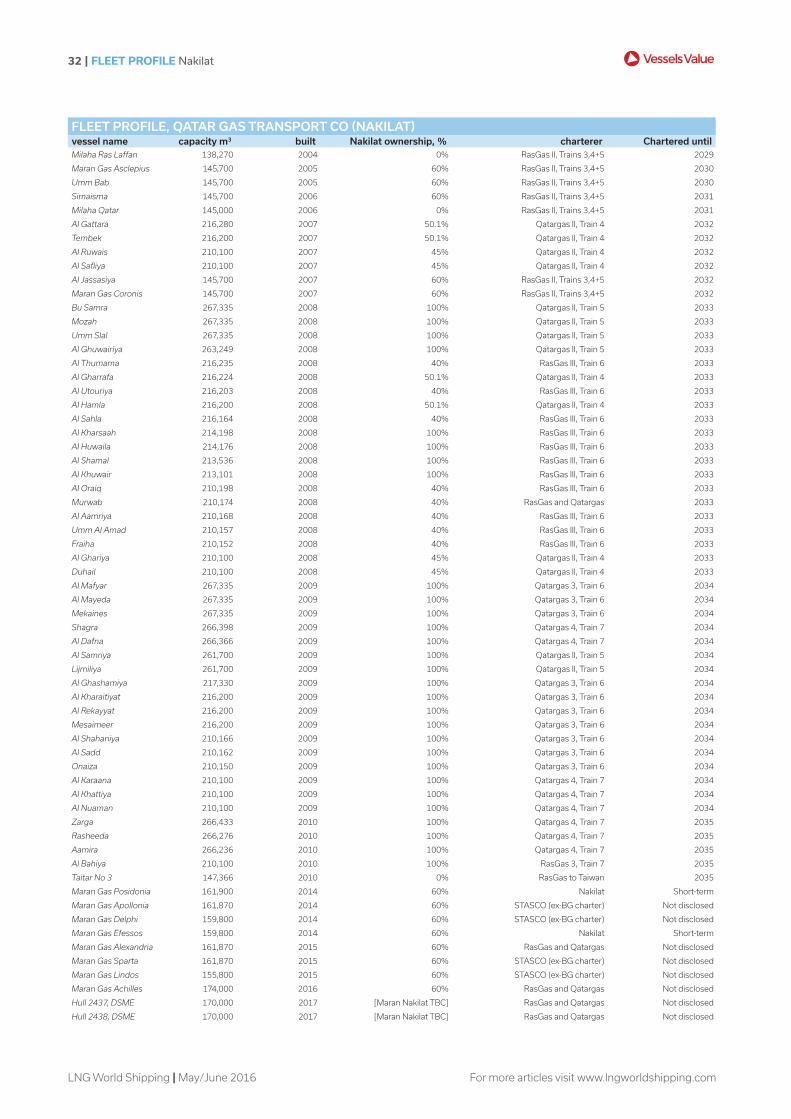

Fleet profile 31 VesselsValue senior data editor Craig Jallal explains why Qatari state-owned

LNG giant Nakilat will look to its partners when it needs additional capacity

Best of the web33 A digest of some of the most popular stories this spring on

LNGworldshipping.com

Ship-to-shore35 Innovation in ship-to-shore transfer

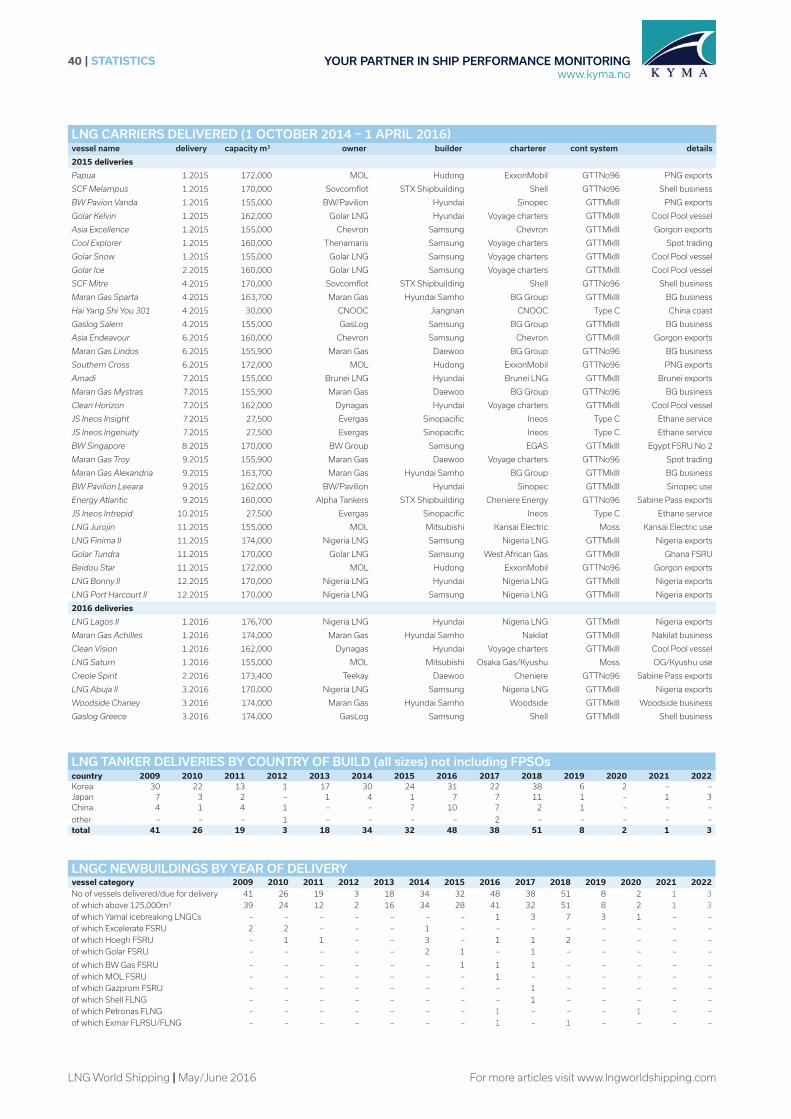

Statistics36 Your exclusive LNG World Shipping guide to the global LNG fleet, orders

and deliveries

Viewpoint44 Parker Bestobell Marine market-development manager Duncan Gaskin

explains how the company has developed cryogenic valves to meet FSRUs’

very specific needs

Coming upThe next bimonthly issue of LNG World Shipping is the June-July magazine.

This issue will cover:

• Analysis – as Russia’s Yamal LNG project moves closer to fruition, we examine

prospects for a new trade lane to Asia via the northern sea route and how this

may affect polar shipping and demand for ice-class carriers

• Technology – innovation in cargo-handling plant and equipment

• Profile – how shipmanagement companies are reshaping their businesses to

adapt to volatile markets

• Supplement – lifecycle maintenance. Our annual report on LNG-carrier repairs

and maintenance will cover the opportunities and challenges facing the top

yards in this competitive market segment. We will report back on the year’s

most innovative projects and talk to companies promoting a shift towards

condition-based maintenance.

Follow LNG World Shipping on Twitter @LNGkaren

Keep up with the latest international LNG shipping news at

www.lngworldshipping.com

Front cover, image © Antwerp Port Authority

MARINE DESIGN FOR LNGC, FSRU AND FPSO

Fuel gas systems for ME-GI diesel engines

No vibrations due to elimination of unbalanced forces and moments

Maximum reliability and availablity supported by unique piston sealing technology, robust marine standard design and advanced diagnostic solution

Best operation flexibility due to warm and cold gas operation capabilities and side stream gas delivery to auxiliary engines and reliquefaction systems

Suitable for BOG suction temperatures down to –160 °C at best efficiency

With our global organization and local service centers we can offer you the full range of services and top performing compressor components

→ www.recip.com/LNGC

1ST CHOICE FUEL GAS COMPRESSION

LABY®-GI

YOUR BENEFIT: LOWEST LIFE CYCLE COSTS

04_LabyGI_210x297_RA_LNG_Industry_RZ.indd 1 29.02.16 19:19

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

COMMENT | 5

Karen Thomas, Editor

A fter three years in the planning, Perth in Western Australia last month played host to LNG18 – the latest iteration of an event that

every three years brings together the most senior players in the gas-producing, shipping, importing, technical and service industries.

Three years ago, at LNG17, the mood was one of optimism, buoyed by the boom in Asian demand, and the new wave of floating and land-based production projects, from the US to Australia, and from the Russian Arctic to east Africa.

Fast-forward three years, and demand growth for LNG has slowed among Asia’s mature importing economies just as that first wave of projects has come to market. For LNG shipping, that means surplus capacity as new tonnage ordered against the expected

demand boom hits the market.Little wonder that this year’s gathering found

delegates in a sadder, wiser mood. Speaker after speaker urged the industry to innovate – and to work together to find smarter ways to improve efficiency and cut costs.

The message is that the LNG industry must work to achieve the growth it expects – and that none of us can take that growth for granted.

This reality check has been a while coming.“Ten years ago, we were told in Europe

that we stood on the brink of great expansion, great volume growth – a Golden Age for European gas,” IHS Energy chief strategist Michael Stoppard told the conference.

“It didn’t quite work out like that. Ten years

later, we have found gas demand down by almost one-fifth.

“We believed in Europe that the demand growth would come automatically, that the environmental and economic case was so compelling that we didn’t need to listen to our customers. We didn’t need to engage in public opinion. We didn’t need to advocate to policymakers.”

It will take a united effort to promote and demonstrate the advantages of liquefied natural gas. There is growing consensus that LNG’s build-it-and-they-will-come approach is out of step with today’s depressed markets.

And as world governments turn their attention to COP21 climate targets, the industry must work harder to persuade the wider public that LNG offers a safe, clean and cost-effective alternative to traditional fossil fuels.

Cheniere Marketing president Meg Gentle urged the industry to encourage new importers, in particular those that will need floating storage and regasification units (FSRUs).

Meanwhile, credibility is everything in today’s tough markets. Pavilion Energy chairman Tan Sri Mohd Hassan Marican warned that safety remains paramount, particularly at the ship-shore interface, as the LNG supply chain lengthens to take in more, smaller players. Just one major incident will push the industry’s ambitions back by ten or 15 years, he warned.

“We should never assume our success in this business,” Mr Stoppard concluded. “We really have to work hard at it.” LNG

Ten years ago, we were told in Europe that we stood on the brink of great expansion, great volume growth – a Golden Age for European gas

LNG GETS A REALITY CHECK

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

5.1 2 5.2 315.0- 0 5.0-1-1.5-2-2.5-3-3.5-45- 5.4-MT

South Korea

Lithuania

Puerto Rico

Dubai

Argentina

Singapore

Greece

Pakistan

Japan

Netherlands

Israel

Belgium

France

USA

Canada

Italy

Thailand

United Kingdom

Jordan

Egypt

Mexico

Sweden

Dominican Rep.

Spain

Malaysia

Indonesia

Portugal

Brazil

Kuwait

India

Taiwan

Turkey

China

Chile

LNG IMPORTS: 2015 Vs 2014 ↑

Total LNG imported, 2015: 245.2 mta, annual 2.5% increase239.2 mta LNG imported 2014, 1% annual increase

↑117 LNG-import terminals 2015110 LNG-import terminals 2014

↑34 importing countries, 201530 importing countries, 2014

↑777 mta, total regasification capacity, 2015751 mta, total regasification capacity, 2014

—19 exporting countries, 201519 exporting countries, 2014

↓68.4 mta spot/short-term traded LNG, 28% of total LNG traded69.6 mta spot/short-term traded LNG 2014, 29% of total LNG traded

↑308 mta total nameplate

liquefaction capacity, 2015298 mta total nameplate

liquefaction capacity, 2014

↑280,945m3 total capacity

demolished, 2015269,300m3 demolished, 2014

↑6 LNG carriers laid up,

year-end 20155 LNG carriers laid up,

year-end 2014

↓New LNG carriers

delivered, 2015: 33New LNG carriers delivered,

2014: 34

↑764,088m3 total capacity

laid up, 2015637,203m3 laid up, 2014

—3 LNG carriers demolished, 2015

3 LNG carriers demolished, 2014

13 THINGS WE LEARNED FROM THIS YEAR’S GIIGNL REPORT

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

5.1 2 5.2 315.0- 0 5.0-1-1.5-2-2.5-3-3.5-45- 5.4-MT

South Korea

Lithuania

Puerto Rico

Dubai

Argentina

Singapore

Greece

Pakistan

Japan

Netherlands

Israel

Belgium

France

USA

Canada

Italy

Thailand

United Kingdom

Jordan

Egypt

Mexico

Sweden

Dominican Rep.

Spain

Malaysia

Indonesia

Portugal

Brazil

Kuwait

India

Taiwan

Turkey

China

Chile

LNG IMPORTS: 2015 Vs 2014 ↑

Total LNG imported, 2015: 245.2 mta, annual 2.5% increase239.2 mta LNG imported 2014, 1% annual increase

↑117 LNG-import terminals 2015110 LNG-import terminals 2014

↑34 importing countries, 201530 importing countries, 2014

↑777 mta, total regasification capacity, 2015751 mta, total regasification capacity, 2014

—19 exporting countries, 201519 exporting countries, 2014

↓68.4 mta spot/short-term traded LNG, 28% of total LNG traded69.6 mta spot/short-term traded LNG 2014, 29% of total LNG traded

↑308 mta total nameplate

liquefaction capacity, 2015298 mta total nameplate

liquefaction capacity, 2014

↑280,945m3 total capacity

demolished, 2015269,300m3 demolished, 2014

↑6 LNG carriers laid up,

year-end 20155 LNG carriers laid up,

year-end 2014

↓New LNG carriers

delivered, 2015: 33New LNG carriers delivered,

2014: 34

↑764,088m3 total capacity

laid up, 2015637,203m3 laid up, 2014

—3 LNG carriers demolished, 2015

3 LNG carriers demolished, 2014

13 THINGS WE LEARNED FROM THIS YEAR’S GIIGNL REPORT

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

8 | ANALYSIS

EUROPE GENERATES SOLID LNG DEMAND

Europe’s net LNG imports surged in 2015, climbing 15.8 per cent on-year to reach 37.6 million tonnes (mt), due to a

combination of increased regional demand for gas, declining local gas production and a fall in the number of reload cargoes at European import terminals.

Another determinant was the dramatic slowdown in what was once rapidly growing demand for LNG in Asia. LNG follows the path of least resistance and, with Asian storage tanks now full, gas sellers have turned to European terminals as destinations for more of their cargoes.

In the face of weak global gas demand European LNG prices are at the same low levels as those in Asia and not much different to the cost of pipeline deliveries. The purchase of

additional LNG cargoes is enabling European utilities to lessen their dependence on piped gas deemed to be geopolitically sensitive, notably from Russia.

Qatar and Nigeria are the leading examples of exporters reorienting their cargo flows because they no longer command the premium Asian buyers paid for additional LNG cargoes following the Japanese tsunami in March 2011. When shipping costs are factored in, Europe is now a more attractive LNG market than it has been for several years.

According to the International Group of Liquefied Natural Gas Importers (GIIGNL), Qatar shipped 21.1mt of LNG to Europe in 2015, 20 per cent more than a year earlier. Nigerian exports to the region were 5.45mt, 26 per cent ahead of 2014.

Cheap and plentiful LNG boosts European customers keen to diversify their limited gas-supply portfolios. Mike Corkhill reports

The Baltic is following the example of the Mediterranean and becoming a busy LNG carrier zone, but with the emphasis on small-scale

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

ANALYSIS | 9

Big winnersIn terms of increased import volumes, the UK, Spain, Italy and Belgium were Europe’s big winners in 2015. The UK remained the region’s top LNG buyer, its 10.08mt in net imports 20 per cent up on the previous year.

Qatar supplied the UK with 96 per cent of its LNG in 2015 and most of the emirate’s cargoes were discharged at South Hook LNG terminal in South Wales, in which Qatar Petroleum holds a controlling stake.

Net Spanish LNG imports last year totalled 8.8mt, an 11.7 per cent on-year increase resulting from a widespread drought that reduced hydroelectric output. Huelva, Barcelona and Sagunto are the busiest of Spain’s six receiving terminals.

Turkish potentialCargo purchases by Turkey, Europe’s third-largest LNG importer, totalled 5.35mt in 2015, a 1.8 per cent drop on the previous year. Qatar, Algeria and Nigeria are the country’s principal suppliers and Norway and Trinidad provide occasional shipments.

Turkey is one of the world’s fastest-growing power markets and uses gas for more than 50 per cent of its electricity generation. It relies on imports to meet virtually all its gas needs, of which Russian pipeline deliveries account for nearly 60 per cent of the volume it buys from other nations.

Political tensions between the two countries have increased in recent months, prompting Turkish interest in diversifying energy sources and boosting LNG imports through its Aliaga and Marmara receiving terminals.

In December 2015 Turkey and Qatar reached preliminary agreements on the possible development of a third terminal and the sale of LNG under a new term contract. Turkey is also looking to the US as a possible future source of LNG.

Neck and neckFrance is Europe’s fourth-largest LNG importer, by the smallest of margins over Italy. France’s 4.35mt of imports in 2015 were down 4.5 per cent on-year, whereas Italy’s 4.32mt represented a 32 per cent increase. The busiest of Italy’s three import facilities is the RasGas-controlled offshore Adriatic LNG terminal.

France’s lower imports in 2015 are attributed to higher purchases of Norwegian piped gas and increased storage drawdowns. However, inbound French LNG is set for a boost with the opening of the country’s fourth receiving terminal, the EDF-operated Dunkirk facility near the Belgian border, this coming June.

Dunkirk has the capacity to process 9.4 mta of LNG, which is enough, through its links to the gas grids of France and Belgium, to meet about 20 per cent of the two countries’ annual gas consumption. The terminal also has the ability to reload cargoes and

Europe’s net LNG imports surged nearly 16 per cent last year to reach 37.6 million tonnes

possible LNG bunkering and tank truck loading roles are being investigated.

French state utility EDF holds 60 per cent of Dunkirk’s capacity rights and its recent purchase contracts include two deals with Cheniere Energy for output from the recently commissioned Sabine Pass liquefaction complex.

Under the first, Dunkirk will receive 26 Sabine Pass cargoes between 2016 and 2018 and the second covers the purchase of up to 24 LNG cargoes over the 2017-2018 period. Dunkirk is also the most likely destination for the latter tranche, or at least the bulk of it.

France’s other terminals, all operated by the Engie affiliate Elengy, are Montoir at St Nazaire and Fos Tonkin and Fos Cavaou, both in the industrial port of Fos, close to Marseilles. Built to handle Medmax ships of up to 75,000m3 carrying cargoes from Algeria, Fos Tonkin has been in service since 1972 and Elengy is set to make a decision on the facility’s post-2020 future by 2017.

Benelux flexibilityBesides Europe’s Big Five importers, six European Union (EU) nations each received under 2mt of LNG in 2015. Belgium’s Fluxys facility in Zeebrugge was the busiest of the facilities handling smaller volumes, accommodating net imports of 1.9mt, some 89.7 per cent more than the previous year.

Zeebrugge supplements its regasification activities with cargo reloads and road tanker loadings. Last year Fluxys re-exported 0.83mt of LNG using both conventional-sized and small coastal LNG carriers and its LNG tank-truck consignments are now approaching 2,000 annually.

The range of operations at the terminal is set to widen again.

Fluxys has won a 20-year contract to tranship up to 8 mta of Yamal LNG, from Yamal’s fleet of dedicated icebreaking LNGCs to conventional gas ships for onward distribution to the final customer. A fifth in-ground storage tank, of 180,000m3, is being built at Zeebrugge to assist with this work.

Fluxys is also constructing a multipurpose second jetty, for commissioning this year, to accommodate both LNG cargo discharges and loadings as well as ships in the size range 2,000-217,000m3. The smaller gas vessels utilising the terminal will include a 5,100m3 tanker which is set to be the industry’s first purpose-built LNG bunker vessel on delivery to NYK/Engie later in 2016.

The neighbouring Gate terminal at Rotterdam in the Netherlands recorded net imports of 0.63mt in 2015, up by 50 per cent on the previous year. Amongst the factors boosting Benelux interest in LNG purchases is the falling output from the Dutch Groningen gas field.

Gate is seeking to enhance its hub role, as is Zeebrugge. Gate is building a breakbulk facility adjacent to its main terminal to facilitate the

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

distribution of smaller volumes of LNG around Europe’s busiest port and its hinterlands.

Like Zeebrugge, Gate will also have its own LNG bunker vessel. The 6,500m3 gas tanker being built for Shell for 2017 delivery will load at the Gate breakbulk facility and fuel LNG-powered vessels in Rotterdam and the surrounding area.

Greece in transitionGreece began importing LNG in February 2000, at its Revithoussa terminal on a small island west of Athens that in 2015 handled 0.45mt, an 18.4 per cent increase on-year.

DEPA, Greece’s state-owned gas utility, is upgrading Revithoussa through the provision of a third in-ground tank to boost the terminal’s storage capacity by 73 per cent. Additional modifications, due for completion by the end of 2016, will permit the berthing of vessels of up to 266,000m3 and increase the terminal’s regas capacity by 40 per cent, to 4.7 mta.

Greece, like Turkey, depends on imports for virtually all its gas, some two-thirds of which comes from Russia by pipeline via Bulgaria and Turkey. Greece is keen to reduce this dependence through increased purchases of LNG.

In addition to the Revithoussa expansion two FSRU-based terminals have been proposed, in Thrace in northeastern Greece, to broaden gas supply choices for the country and its neighbours in southeastern Europe. The Copelouzos Group has put forward a 1.9 mta project for Alexandroupolis

close to the Turkish border whereas DEPA is promoting Aegean LNG, based on a 2.6 mta FSRU in the port of Kavala.

Croatia is also looking to ease its reliance on Russian pipeline gas and to fast-track LNG imports using an FSRU. European Union subsidies are being mooted for the proposed floater as part of a drive to serve customers in central Europe.

Baltic breakthroughThe Baltic Sea is also poised for a major increase in LNG carrier traffic, although the emphasis will be on smaller vessels. Lithuania and Sweden recently became the first two Baltic countries to import LNG.

Sweden’s breakthrough is a great advertisement for small-scale LNG. Between them, the Scandinavian nation’s two coastal distribution terminals, at Nynäshamn and Lysekil, received 290,000 tonnes of LNG in 2015, not far short of the 320,000 tonnes that neighbouring Lithuania imported via its 170,000m3 FSRU.

Poland is set to become the third Baltic Sea LNG importer when its 3.7 mta Swinoujscie terminal opens for business this summer.

Elsewhere, Gazprom is set to take delivery of an FSRU in 2017 that will bring LNG to the Russian enclave of Kaliningrad.

Finland, meanwhile, has three small-scale receiving terminals under construction, at Pori, Tornio and Hamina, for commissioning in 2016, 2017 and 2018. LNG

10 | ANALYSIS

Buying additional LNG cargoes allows European utilities to cut their dependence on piped gas that is geopolitically sensitive, notably from Russia

Revithoussa's jetties are being modified to enable it to handle Q-max LNG carriers

The Future is ClearME-GI dual fuel done right

MAN B&W MC/MC-C Engines MAN B&W ME/ME-C/ME-B Engines MAN B&W ME-GI/ME-C-GI/ME-B-GI Engines

The new ME-GI generation of MAN B&W two-stroke dual fuel ‘gas injection’ engines are characterised by clean and efficient gas combustion control with no gas slip. The fuel flexibility and the inherent reliability of the two-stroke design ensure good longterm operational economy. Find out more at www.mandieselturbo.com

Pub/Issue LNG World Shipping_November

Size B: 216 x 303 T: 210 x 297 L: 190 x 277

File Name RRR

Client FMC

www.fmctechnologies.com

#RethinkReinventReimagine

Copyright © FMC Technologies, Inc. All Rights Reserved.

Discover the upside in this down cycle.We are aggressively helping operators reduce capital investments and improve returns by transforming the way we all do business. By working with us to rethink, reinvent and reimagine field developments, you can dramatically reduce overall costs. We will leverage a new generation of standardized equipment and innovative tech- nologies to squeeze unnecessary cost and time from the value chain. Talk to us today. Because it’s clearly time for a change.

Rethink.Reinvent. Reimagine.SM

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

Ship-shore interface CONFERENCE | 13

LNG World Shipping will host its Ship-Shore Interface Conference in London, UK on 11-12 May. This year's event will scrutinise the point in the supply chain where workloads are at their most intense and where the risks are greatest

LNG’S WEAKEST LINK – WHY SAFETY IS EVERYTHING AT THE SHIP-SHORE INTERFACE

For the LNG industry, the equivalent to the coalface is when the gas carrier is in the terminal zone. Compared with the relatively relaxed workaday routines of life at sea, activities

reach peak intensity at the ship-shore interface.History and risk analysis have shown that if anything is going to go

wrong in the LNG supply chain, the chances are that it will occur when the ship is in the port approaches or berthed at the terminal jetty.

At the ship-shore interface the LNG carrier has to negotiate often traffic-laden port waters whose approach channels pose navigational challenges. At the same time, the ship and terminal must both work to a finely tuned and pre-agreed game plan that can accommodate a full range of possible emergencies while cargo is being transferred across the jetty at rates of up to 12,000m3 per hour.

FLEXIBILITY The industry’s ship-shore interface focus has taken on new dimensions in recent years, reflecting increasingly flexible LNG trading patterns and the extension of the LNG supply chain upstream and downstream.

The traditional ship-shore interface involves a conventional-size carrier at a regularly visited shore terminal but the rising popularity of spot and short-term cargoes and less stringent charterparty requirements governing destination ports mean that ships today are calling at more terminals than ever before.

Similarly, each terminal is handling more LNG carriers of varying types and sizes than before.

The floating receiving terminal is now also an integral part of LNG activities and floating LNG production will also become a new feature of the logistics chain.

Floating terminals have brought new LNG carrier interface options into play, many requiring innovative technologies to be developed to ensure safe operations.

Growing interest in the natural gas option from energy customers remote from the grid and with limited volume requirements is spurring interest in small-scale LNG, notably in the form of coastal gas carriers and regional distribution terminals.

The use of LNG as marine fuel is another small-scale market driver. The multiple solutions available to LNG bunkering logistics planners are opening up new ship-shore interface scenarios.

DIALOGUEThe ship-shore interface has been a central theme for LNG World Shipping since the magazine’s inception. This year’s conference builds on the publication’s inaugural conference two years ago, bringing together the key players – the ship operators, charterers and terminal operators, equipment suppliers, service providers and enforcement authorities – that play a pivotal role in safe cargo transfers and smooth port turnarounds.

The 2016 conference provides a dedicated space in which LNG carrier and terminal operators will discuss the business and operational challenges that arise at their common interface. This year, with the scope of proceedings extended to encompass floating terminals, small-scale operations and LNG bunkering, the vital commitments made by both equipment suppliers and service providers will come under special scrutiny.

Communications systems, equipment and emergency-response planning come into sharp focus. Fluxys Belgium/E Manderlier

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

14 | CONFERENCE Ship-shore interface

SIGTTO LEADA measure of the importance of the ship-shore interface to the LNG industry is the fact that more than 20 titles in the technical publications portfolio of the Society of International Gas Tanker and Terminal Operators (SIGTTO) cover some aspect of the subject. The total goes up to 30 if we include training-related documents.

SIGTTO leads the industry in disseminating best practice and providing technical support for the liquefied gas shipping and terminal sectors. The exemplary safety record that LNG ships have maintained over the past 50 years owes much to the society’s commitment to ship-shore interface issues.

The point at which ships and terminals connect remains under the SIGTTO microscope. Four currently convened society working groups are preparing new publications that relate to the ship-shore interface.

Two topics that interest SIGTTO are the LPG ship-shore interface and the emergency-response roles of support vessels in protecting gas carriers and terminals. Both topics are on the agenda at this year’s LNG World Shipping conference.

SIGTTO’s LPG group is identifying possible causes of LPG and chemical gas cargo ship-shore interface-related incidents and will update the association’s original document on the subject, which dates from 1997. It behoves the gas shipping industry to share its experiences so that new participants learn lessons quickly and efficiently rather than learning them the hard way.

SIGTTO members recognised the importance of terminal support craft in mitigating emergency situations back in 2012, prompted by the increasing diversification of the LNG supply chain. This led to the preparation, by a number of support vessel, gas tanker and terminal operators among the society’s membership, of guidance that reinforces the effectiveness of such vessels in maintaining high safety standards at gas terminals.

SHARING EXPERIENCELike every terminal, every terminal emergency will have its own specific characteristics, and there is much to be gained from discussion and a cross-fertilisation of ideas across the industry. Many lessons are learned

the hard way and it behoves the gas-shipping industry to share its experiences and thus to fast-track the learning curves of new participants.

Delegates to the LNG World Shipping Ship-Shore Interface Conference 2016 will have the opportunity to discuss, among other topics, the emergency release system mechanisms of cargo transfer equipment. This is an issue taking on added significance in light of today’s extending LNG supply chains and the advent of LNG bunkering.

Other focal points at the two-day event include vessel mooring arrangements, ship-shore communication links and training for ship and terminal staff. LNG carrier mooring incidents have declined with the widespread use of high modulus polyethylene (HMPE) fibre ropes but, as the recent injury to an officer on the Q-max vessel Zarga at the South Hook terminal in Wales showed, accidents can still occur when these ropes are used.

Training remains a critical first line of defence and the gas shipping safety regime has benefited from the introduction of crew competence standards in recent years. The application of such standards to new fields of gas carrier and terminal activity poses challenges, as the upcoming conference will highlight.

Proceedings at the Ship-Shore Interface 2016 event will be in the capable hands of conference chairman Bernhard Schulte Shipmanagement corporate expert, liquefied gas Chris Clucas. LNG

The 2016 LNG World Shipping Ship-Shore Interface conference takes place at London’s Millennium Gloucester Hotel on May 11-12. Visit our website to f ind out who is speaking and which topics they will cover: http://bit.ly/LNGship-shoreIFACE

As the LNG supply chain extends, so does the ship-shore interface safety and training regime

Many lessons are learned the hard way and it behoves the gas shipping industry to share its experiences

BSM_VHP_100x297_lng1_Layout 1 15/01/2016 13:34 Page 1

Stand 3105 - Hall 3

Meet us at:

®

FERRYL 202 STANDARD ANTICORROSIVE GREASE

Superior Greasefor LNG Mooring Wires

1955 - 2015

Specialised in high quality products for the shipping industry for 60 years,

Ferryl products can withstand the harsh conditions at sea.

With global availability, Ferryl’s wire-rope grease offers superior adhesion and

ultimate rust protection of mooring wires.

VGPCOMPLIANT

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

16 | OPERATIONS Escort Tugs

TUGS FOR TOUGH TERMINALST

he steady growth in LNG terminals around the world is

boosting demand for tug boats specifically adapted to handle gas carriers in often challenging ports, many of them with long approach channels.

These tugs are operating in facilities from Australia to the Baltic Sea as increasingly international procedures in terms of safety and risk-mitigation come into play, and in most cases the vessels’ crews are specially trained.

One of the latest ports to welcome LNG-carrying vessels is Poland's Swinoujscie on the Baltic Sea. In February the LNG terminal used customised harbour-escort tugs built by Turkey’s Bogazici Shipping to successfully berth a Qatargas–owned Q-flex vessel to load the terminal’s commissioning cargoes.

Swinoujscie is the biggest LNG terminal in northern, central and eastern Europe and presents significant challenges. It has a 3km breakwater and an unloading jetty with a single berth able to handle methane carriers with a capacity of anything from 120,000m3 to – in the case of Q-flex size vessels – 217,000m3.

When full commercial operations start later this year, the tugs, which Spain’s Cintranaval-Defcar group designed for Bogazici, will be handling vessels delivering 1 million tonnes a year (mta) of LNG.

And as terminal operator Polskie LNG president Jan

Chadam pointed out at the time of the inaugural berthing, there is no room for mistakes in an enterprise with such high stakes. “The receiving terminal’s potential makes us an important player in energy independence in the whole region,” he said.

DemandsWhen it comes to handling LNG carriers, port operators are pushing designers and shipyards to higher specifications and performance. Smit Lamnalco business development manager Andrew Brown points out that safety is paramount in the case of the five new Robert Allan-designed

RAstar 3400 escort tugs it is introducing to the port of Gladstone in Australia.

“These tugs are high-powered and are ideally suited for escort operations in areas exposed to weather and sea, such as many new LNG terminals, where a high standard of seakeeping is required.”

In Gladstone, tug crews must routinely deal with difficult close-quarter situations. Access to the port is through narrow channels on the Queensland coast, buffeted by winds of more than 40 knots that kick up waves of up to 3m.

Lamnalco’s LNG-customised tugs comply with Australian Maritime Authority safety

regulations, among the toughest in the world. “These vessels represent a unique development in terminal escort tug design,” says project director Ali Gurun from the vessels’ Turkish builder Sanmar shipyard.

Although the Society of International Gas Tanker and Terminal Operators (SIGTTO) says LNG-approved tugs are not greatly different in principle from standard ones, the differences are nevertheless important. For instance, Smit Lamnalco had its Gladstone RAstar 3400s customised – they boast a sponsoned hull configuration and foil-shaped escort skegs that work together to greatly reduce the roll motion and accelerations to less than half that of conventional tugs of comparable size.

StabilityAs the designer’s executive chairman Robert Allan explains, the stability provided by the bigger and more powerful escort-class tug is a vital element in working with LNG carriers. “By definition, it must be designed to handle a much more unique set of operational demands [than a conventional harbour tug].

“Thus it has a different hull form and very different kind of winch capable of ship-handling and towing. Many [standard] escort tugs are more than capable of handling LNG carriers, if suitably equipped, and we

Tug boat designers, builders and crews must rise to new challenges as LNG terminals proliferate around the world. Selwyn Parker reports

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

Escort Tugs OPERATIONS | 17

have designed many of these for more exposed terminals.”

Whether an escort or harbour tug, any tug handling LNG carriers must also exert the softest possible touch on these vessels’ typically thin-skinned hulls. In technical terms, the contact pressure is 14 tonnes/m2, which experts say is extremely low.

An elaborate fendering system provides the necessarily gentle push. On the bow is an upper row of cylindrical fenders with a diameter of 1,000mm and a lower level of 450mm deep W-shaped fenders, while another cylindrical fender of 600mm diameter protects the stern.

Standard safety procedures focus particularly on the reduction of the risk of explosion. As well as the installation of a gas detection system, all ventilation dampers on the Lamnalco tugs can be remotely closed.

The system that remotely controls the gas-tight dampers has a two-tiered alarm set at lower explosion limits of 20 per cent and 40 per cent.

On the deck the

towing winches, navigation lights, outside lights and emergency-stop buttons are explosion-proof. The fire-fighting capability has FiFi 1 certification and the tugs have extra foam-carrying capacity.

In another example of the trend towards international safety standards, the latest Bogazici-built tug at work in the Swinoujscie terminal features similar safety equipment to that installed on the Lamnalco vessels.

Mixed-use portsIn the growing number of mixed ports, most tugs are expected to fulfil a dual role. As LNG towage company Svitzer’s chief technical officer Kristian Brauner points out, its fleet in Darwin in Australia will have

to deal with all the port’s other operational requirements as well as the demands of LNG.

“While we needed a tug with escort notation and emergency towage capability, we also required whole-of-port tugs with full FiFi, pollution control and oil recovery capabilities,” he says.

This is increasingly the case in other mixed-used ports such as Milford Haven, Rotterdam and Singapore, where LNG and conventional terminals sit side by side.

At Darwin, Svitzer has just commissioned two smaller RAstar 2800 tugs, all-purpose versions to service the Ichthys LNG project starting up in late 2017.

These tugs have the standard safety features such as gas-detection systems but no customisation for LNG

carriers. “Our crew don’t handle any LNG and the tug is only connected to the carriers by the towline while the crew remains on board,” Svitzer explains.

Personnel on these tugs need no special LNG training. “It’s not required because [LNG carriers] are similar to a fuel tanker in terms of hazard and safety issues,” says Svitzer.

In such locations the true escort tug may not in fact be suitable. As Robert Allan says: “In many instances they are too large and even too powerful to be ideal for more routine ship-handling.”

Meanwhile SIGTTO guidelines issued in September are dictating procedures and influencing training. Lamnalco, for instance, uses the guidelines to train crews on simulators in Singapore. SIGTTO specifies that tugs with escort capability must be employed at terminals in exposed locations and with long approach channels.

Crews are being trained for accident scenarios that include loss of containment, collision, grounding and incursion of unauthorised vessels into the gas-exclusion zone.

All are among the “top events”, in official language, in which support craft play a vital risk-mitigating role. Another for which they must be prepared is a gas carrier floating away from its jetty because the mooring lines have failed.

As Smit Lamnalco’s Andrew Brown maintains, crew preparedness counts. “In an emergency, support vessels provide the first line of defence,” he says.

In future, the world will see LNG-fuelled tugs able to operate anywhere in a port. As SIGTTO notes, class and IMO regulations are pending for operating – and training – tugs powered by LNG or other fuels with a low flashpoint. LNG

“In an emergency, support vessels provide the first line of defence” – Andrew Brown, Lamnalco

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

18 | EXPORTS East Africa

East Africa keeps faith with LNG

Tanzania and Mozambique are home to East Africa’s

largest natural reserves, with a combined capacity of nearly 250 trillion cu feet (tcf ). In recent years, both countries have moved to develop these vast fields but slow government regulation has at times hampered progress, as has inadequate infrastructure and weak international prices.

Italy’s Eni and US-based Anadarko Petroleum are developing straddling reservoirs in the Rovuma Basin off the northern coast of Mozambique. The partners hope to deliver LNG from the 24 tcf reservoir by 2020.

Eni has discovered some 85 tcf of natural gas in Mozambique and Anadarko has unearthed some 75 tcf, enough to transform the country into a world-class producer of natural gas. Last year, the partners reached key milestones, including selecting a contractor for the initial onshore development, estimated to cost US$15 billion.

The project in Mozambique comprises two LNG-processing trains. Anadarko says the partners have so far reached long-term offtake sales contracts for more than 8 million tonnes a year (mta).

The majors felt the location of the project on the east African coast would be ideal for large LNG facilities,

built to export gas to Asia’s energy-hungry markets. Now, however, with the emergence of a global supply glut, questions remain over the project’s final investment decision.

Oil and gas companies worldwide have been delaying big development projects after the sharp fall in oil prices, to which the price of Asia’s long-term LNG-supply contracts remains tied. However, Anadarko maintains that, with

many projects on hold due to low global prices, “now is the time to move forward” with low-cost projects in areas such as Mozambique.

Meanwhile, plans have been finalised to acquire land for building an LNG plant along Tanzania’s Indian Ocean coast. Some 55 tcf has been discovered in the country so far. Developing these resources will transform the Tanzanian economy over the next 10 years into a middle-income nation, according to the country’s central bank.

Today, Tanzania produces around 300 million ft3 of natural gas to fire electricity plants. However, state energy company Tanzania Petroleum Development Corp predicts that this could more than triple

by 2020, enabling the country to export liquefied gas to regional and Asian markets.

Shell’s recent acquisition of the BG Group raises the prospect that developing these resources may gather pace.

BG’s partners in Tanzania LNG include Statoil, Exxon Mobil and Ophir Energy. They plan to build an onshore LNG export terminal in partnership with state-run Tanzania Petroleum Development Corp, to start in the early 2020s.

Despite the unfriendly business environment, however, KPMG Africa senior manager energy and natural resources Jean Githinji believes that “government flexibility can keep projects going”.

Critics have blamed government indecision for holding back projects such as Tanzania LNG. Earlier this year, however, Tanzania’s recently elected president John Magufuli pledged to speed up government decisions on key investment projects.

This year has brought more indications that things may have started to move at last. In February, Tanzania announced that it had secured 2,070 hectares of land for the project.

This removes a major hurdle for the long delayed LNG-production plant.

Analysts believe that both countries’ projects remain competitive. KPMG Africa International Development Advisory Services associate director Mark Essex says that although low oil and LNG prices “challenge the economics of greenfield LNG projects”, the schemes in Tanzania and Mozambique “appear highly cost-competitive and well placed to supply Asia”. LNG

Tanzania and Mozambique plan to develop and export their vast gas reserves – but progress so far has been slow. Diana Taremwa Karakire reports

Mozambique has enough gas in the offshore Rovuma Basin to become a world-class exporter. Eni

Tanzania and Mozambique “appear highly cost-competitive and well placed to supply LNG to Asia” – KPMG Africa director Mark Essex

SOLUTION FIVE

ENERGY EFFICIENCY

WE Drive™ Shaft Generator Motor

Shaft Generator Motor

Shaft Generator Motor

Shaft Generator Motor

Shaft Generator

Hybrid Machinery

Hybrid Machinery

Ship wide DC Bus Power Distribution

DC-link Power Distribution

Boost Mode

Take Me Home

WE Drive™

WE Drive™

WE Drive™

Economical Operations Hybrid Machinery Efficient Power Distribution Hybrid DC Machinery

WE Drive™

SOLUTION FOUR

SOLUTION THREE

SOLUTION TWO

SOLUTION ONE

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

CARGO HANDLING | 21

US RESEARCHERS ASSESS LNG BUNKERING METHANE-LEAK RISK

CO2 accounts for about 82 per cent of all greenhouse gas emissions from human activities in the US

T he battle to reduce greenhouse gas (GHG) emissions from ships is

heating up – as the workload of IMO’s Marine Environment Protection Committee’s indicates – and LNG-powered vessels can be a powerful tool in the maritime community’s drive to comply with tightening international regulation of ship atmospheric pollution.

Combustion of natural gas produces lower carbon dioxide (CO2), sulphur oxides (SOx), nitrogen oxides (NOx) and particulate matter than burning the same amount of oil fuel on an energy-equivalency basis.

In fact, the emissions signature of LNG meets all

current, pending and proposed standards laid down for controlling ship air pollution. However, LNG has a potential environmental downside.

LNG processed for carriage by sea and use as bunker fuel is, typically, 95 per cent methane, a potent greenhouse gas due to its ability to trap radiation and, hence, promote global warming.

On a volume basis CO2 accounts for about 82 per cent of all greenhouse gas emissions from human activities in the US, whereas methane is responsible for 9 per cent. However, in a tonne-for-tonne comparison, methane has an impact on climate change 25 times

greater than CO2.Although methane emissions volumes are relatively small, escapes of natural gas have a disproportionately high global warming potential (GWP) quotient.

In recent years scientists have been trying to better understand the sources and volumes of methane emissions, including those across the oil and gas supply chain.

In 2015 the US recognised the potential detrimental impact and introduced the first legislation to control methane escape.

Work has expanded to encompass the risks that LNG-powered ships present, namely methane leakage

during LNG-bunkering and the passage of unburned methane through gas-burning engines, a process called slip.

StudiesResearchers in the US have just completed a study to determine the net effect of methane leakage and slip on LNG-fuelled ships’ GHG impact. Their work at the University of Delaware and the Rochester Institute of Technology adopted a total-fuel-cycle approach in an analysis on behalf of the US Maritime Administration (MARAD).

Bunkering ships that are not LNG carriers is comparatively new but will grow, not least in the US. It can take various

22 | CARGO HANDLING

Basic principle of PBCF effectAs the flows accelerated down after the blade trailing edges are blocked and

rectified to a straight ship-stream by the fins of the PBCF, the hub vortex

will be eliminated.

The PBCF has been developed and commercialized in 1987 by the corporate

group centered in Mitsui O.S.K. Lines, Ltd..

PBCF is the originated device to be focused in the recovery of energy from

the flow out energy in propeller hub vortex.

Research and development on the PBCF started in 1986, and sales began the

following year. Since then, an increasing number of shipowners, mainly in

Japan, began to adopt the system.

By 2006, the 19th year since the start of sales, the PBCF had been ordered

for 1,000 vessels. Since then, it has gained worldwide recognition by vessel

owners and operators, and the number of ships adopting it has doubled in

just five years, reaching the 2,000 vessels milestone in 2011, and now exceeding

the 3,000 milestone in just four year.

without PBCF

hub vortex

E-mail:[email protected] URL:http://www.pbcf.jp/

5% fuel saving experiences on 3,000 vesselsadopted by more than 200 owners and operators.

with PBCF

forms, including truck-to-ship, ship-to-ship and terminal-to-ship operations, and using interchangeable portable tank containers as LNG bunker units.

Opportunities exist for methane leaks from various elements of the bunkering system.

In its own investigative work, ABS has adopted a risk-assessment framework in considering LNG leakage during bunkering, which the MARAD study embraced.

ABS has identified four initiating events that can give rise to methane emissions: leaks from LNG pumps, pipes, hoses and tanks; inadvertent disconnection of hoses; overfilling or over-pressuring vessel fuel tanks; and external impact.

ABS also outlines 22 prevention and mitigation safeguards that minimise the frequency and volume of bunkering leaks.

Methane slipBut when it comes to the process of burning LNG to provide propulsion, various factors cause unburned hydrocarbon to pass through an engine and into the atmosphere.

Slip emissions occur because of poor combustion of the gas under very lean methane/air mixtures, variations in flame propagation dynamics and the blow-by of unburned methane during cylinder valve operations.

However, not all engines are equal when it comes to the amount of hydrocarbon they allow to pass through them untouched.

The three most popular engines found on LNG-powered ships are:(a) lean-burn, spark-ignited engines operating on the Otto cycle (b) diesel dual-fuel (DDF) compression-ignited engines, that operate like lean-burn

types on the Otto cycle but with diesel cycle injection to ignite the methane/air mixture(c) diesel-injected, compression-ignited engines that operate with natural gas on the diesel cycle.

Rolls-Royce and Mitsubishi make the first type, which can produce lower downstream CO2 emissions than DDF engines at similar air-fuel ratios. Lean-burn units can also operate on a much thinner fuel-air mixture and at higher compression ratios using advanced spark timing but are also more prone to slip than compression-ignition engines.

DDF engines typically use a port-injected, air/methane mixture, ignited by diesel cycle injection and show a flame propagation like that in Otto cycle combustion. These engines, including Wärtsilä’s

four and two-stroke units, produce lower methane slip than lean-burn gas equivalents.

Combustion in high-pressure, gas-injection diesel cycle engines on the other hand uses diffusion-controlled pilot fuel ignition, as in conventional diesel engines.

MAN’s ME-GI units are examples of these two-stroke engines, which provide high reliability, high thermal efficiency, good fuel flexibility and a level of methane slip that can be negligible.

However, high-pressure gas-injection engines fail to reduce NOx emissions to meet IMO Tier III demands.

That means they require an exhaust-gas recirculation (EGR) scrubber system or a selective catalytic reduction system, sometimes both, to comply.

As a general rule, methane slip occurs only in the Otto

CARGO HANDLING | 23

cycle mode, including in dual-fuel engines, but not in the diesel cycle mode.

Methane slip tends to be greater at lower engine loads and depends on the composition of the gas and the engine speed.

All makers of gas-burning engines are working to minimise methane slip.

Manufacturers are developing combustion-chamber technologies to improve the combustion process, using catalysts to oxidise unburned methane and optimising turbocharging arrangements.

One area of investigation is the use catalysts in after-treatment systems to oxidise methane, but this technology needs further development.

Key findingsThe MARAD study highlights the need to consider more than just the combustion engine to minimise methane emissions.An examination of the full LNG-bunkering supply chain is vital.

Two key findings emerged from the research.

First, methane slip is a key factor in determining whether an LNG propulsion system will improve or worsen GHG emissions compared with the burning of conventional fuels. Ships using compression-ignited LNG systems – whose methane slip is low – produce low GHG emissions compared with vessels burning conventional fuels, even allowing for a certain amount of methane leakage during routine bunkering.

However, spark-ignited LNG engines cause more methane slip and can negate the recognised environmental advantages of the LNG system. This is true even when there are no bunkering leakages.

MARAD’s second important finding is how routine bunkering leakages can have a disproportionate impact on overall GHG emissions due to the high

volume of natural gas throughput and methane’s high GWP.

For example, a 1 per cent methane leakage during bunkering operations leads to a 10 per cent increase in net GHG emissions.

For a compression ignition engine a 1 per cent bunkering leakage cut the net GHG emissions advantages of LNG

from a benefit of 14.9 per cent to 6.7 per cent compared with low-sulphur diesel fuel.

MARAD’s study found that reducing leakage in frequently recurring bunkering processes has substantial benefits on total-fuel-cycle GHG impacts.

Researchers identified several stages in the bunkering process where

leakage can be reduced and they recommended further investigation to look more closely at these areas.

Low natural gas prices mean that the economic value of this methane loss may not be significant. However, the environmental opportunity costs are also very important. LNG

Onshore or Offshore, Insist on Zeeco.

Experience the Power of Zeeco.™

Burners • Flares • Thermal Oxidisers • Vapour Control Rentals • Aftermarket: Parts, Service & Engineered Solutions

Explore our global locations at Zeeco.com/global

Zeeco Europe LimitedThe Woolfox Building

Great North Road, Rutland LE15 7QT+44 (0) 1780 765077

©Zeeco, Inc. 2016

Built for the job. Marine and offshore applications operate in harsh and isolated environments. That’s why you need dependable vapour recovery and combustion systems, low-NOx burners, flares, and control systems purpose-built to withstand both the elements and the process demands.

Don’t trust your mission-critical systems to anyone but a proven expert. From high-efficiency, low emission boiler burners and hurricane-proof flare pilots to full turnkey solutions, Zeeco understands every aspect of combustion equipment for your ship, FPSO, LNGC, FLNG, FSRU, or offshore platform.

Choose Zeeco. We engineer the advanced combustion systems that keep you in compliance, keep people safe, and keep ships and terminals running smoothly.

Global experience. Local expertise.

A ZEECO Utility Flare Installed on the World’s First Operating FLNG.Photo Courtesy of Exmar.

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

24 | OFFSHORE FSRUs

FSRUS OPEN LNG TO NEW IMPORTERSLower gas prices, more supply and excess capacity add up to one segment of the LNG market that is doing rather nicely, thank you. Karen Thomas reports

As Australia ramps up its LNG exports and as the US switches from importing to exporting, analysts expect a resulting supply glut – and a new incentive to new players

to import this ever-cheaper commodity.Consultancy Wood Mackenzie estimates that new projects

will deliver a combined 125 million tonnes a year (mta) to market, including 10-17 mta this year. Meanwhile, the cost of buying LNG on the spot market has fallen by half in the last 12 months.

That spells bad news for energy companies’ returns on

investment – but for prospective buyers, there is more than enough cheap gas coming to market and a surplus of idle LNG carriers to deliver or store it. The International Gas Union (IGU) predicts an increase in LNG-importing countries from fewer than 30 two years ago to nearly 50 by 2025.

Building land-based import terminals can be expensive and time-consuming, and can run into regulatory obstacles. So, for many prospective LNG buyers, floating storage and regasification units (FSRUs) present a cheap, quick and straightforward alternative, at around US$300 million to build, or as little as US$80 million to convert, according to broker Poten & Partners.

GROWTH MARKETLast year, new importers Egypt, Pakistan and Jordan opted for FSRUs – and the trend looks set to gather momentum.

According to the annual report of the 2015 International Group of Liquefied Natural Gas Importers (GIIGNL), the live FSRU fleet comprised 23 vessels with a combined capacity at year-end of nearly

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

FSRUs OFFSHORE | 25

3.5 million m³. The orderbook stands at eight vessels, three to be delivered this year and five next year.

LNG World Shipping has identified nearly 30 operating and confirmed FSRU-based projects worldwide and nearly 40 at the proposal stage.

US-based Excelerate owns nine FSRUs, has an LNG carrier it deploys for storage and holds four options at Daewoo Shipbuilding and Marine Engineering (DSME). Golar LNG has seven FSRUs, a converted LNGC acting as a floating storage unit (FSU) off Jamaica and takes delivery of its eighth – unfixed – FSRU next year.

Norway-based Höegh LNG has six FSRUs on the water, another fixed to the Penco-Lirquen import project in Chile and one unfixed FSRU, all part of its plans to expand this fleet to at least 12 by 2019. The Chile project has gained new urgency now that Höegh has decided not to enter the floating LNG (FLNG) production segment.

Elsewhere, a fourth established player, OLT, is importing LNG to Italy via FSRU.

New entrants are already circling, however. BW Gas entered the market last year, when it dispatched the 170,000m³ BW Singapore to Egypt, chartered as a second floating import terminal to EGAS.

BW has now exercised its option on a second FSRU newbuilding but where it will deploy Hull 2118, the company has yet to say. The LNG transporter has been linked to a plan by UK-backed First Gas to station an FSRU off Yuzhny in Ukraine. And now at least three new players are about to enter the market.

BIGGEST VESSELMitsui OSK takes delivery this year of the largest FSRU to hit the water, at 263,000m³. Hull 2419 will produce up to 4 mta when it replaces the 145,000m³ Höegh LNG-owned GDF Suez Neptune off Uruguay in November.

Next year, Gazprom will take delivery of the world’s first ice-class FSRU, having commissioned the 174,000m³ newbuilding to import up to 3.6 mta through Russia’s Baltic enclave at Kaliningrad.

Teekay LNG has ordered a floating storage unit (FSU) for the Bahrain LNG build-own-operate-transfer (BOOT) joint venture with Samsung C&T and Gulf Investment Corp (GIC). It is converting ME-GI engine LNG carrier Hull 2461 into a 174,000m³ FSU to be moored off Hidd for 20 years.

Teekay has also been linked to talks with India’s Swan Energy to station a 5 mta FSRU off Pipavav in Gujarat.

In a second proposed Gujarat import project at Jafarabad, Belgium-based Exmar, which has suffered setbacks to its FLNG ambitions this year, is negotiating with Swan Energy to supply a 4.5 mta FSRU.

And in April Fox Petroleum announced that it has signed a Memorandum of Understanding to position an FSRU at Karawar in Karnataka State and to invest US$1.05 in import infrastructure.

The energy-hungry Indian subcontinent is emerging as a prospective FSRU hotspot, with at least 11 such projects under discussion, from Gwadar in Pakistan’s Baluchistan region to Moheshkhali Island in the far south of Bangladesh.

Monaco-based GasLog furthered its plans to enter the FSRU space by hiring Bruno Larsen in March to head this business. He will present his growth strategy to the board in May.

Other reports have linked China National Offshore Oil Corp (CNOOC) and other shipping and energy compatriots to the FSRU market. Poten says shipowners there are “looking at buying old carriers for conversion and chartering them out to city

gas distributors, given attractively low valuations of US$18-20 million... “Converted FSRUs are attractive to independent Chinese LNG importers that are at the mercy of the country’s three major importers, which can deny third-party deliveries, even when a tanker is en route, because of storage constraints.

“FSRUs could [also] be competitive against high tolling fees for third-party access, currently sought by state-owned onshore terminal operators.”

NEW PROJECTSThe consensus holds that FSRU projects will grow significantly in number over the next few years – but how fast? Excelerate Energy chief executive officer Rob Bryngelson suggests a rate of four or five projects a year, a mix of smaller and larger FSRUs.

Consultancy Douglas-Westwood predicts a near doubling of the world fleet to 2022, growth in Asia and western Europe in particular increasing the number to 55 vessels. The LNG World Shipping FSRU project list shows the Indian subcontinent as generating most interest in new ventures, with at least nine projects under discussion in India, one new venture in Pakistan and one in Bangladesh.

Otherwise, the global spread of projects is even, with six proposed ventures apiece in Asia, Africa, Latin America and Europe. Those of particular interest in the coming months include Croatia, which is about to decide whether to develop Krk LNG as a land-based or FSRU-based project.

In Brazil, Golar LNG is moving into the midstream LNG market. It has the exclusive right to supply an FSRU to a new combined-cycle power plant there in whose development it also has a stake.

Golar is likely to convert one of its tri-fuel diesel-electric (TFDE) newbuildings for that project. Chief executive Gary Smith has pledged to step up the company’s conversion programme to reduce Golar’s exposure to the “disappointing” spot market.

So which countries are likely to join the LNG-importers' club next? The top contenders include Chile, where Höegh will soon deliver Hull 2685 and Ghana, where West Africa Gas (WAGL) has chartered the 170,000m³ Golar Tundra on a five-year contract to 2021, with options.

In Bahrain, the Teekay-led FSU venture plans a 2018 start date, as do the Gazprom venture in Kaliningrad, the New Fortress Energy FSU project in Jamaica and the Swan Energy/Teekay LNG terminal in Pipavav.

At least one Indian project will come to market within the next two years, while in the UK, Excelerate has agreed to station an FSRU off Teesside and Port Meridian Energy plans to set up a 6 mta STL-buoy project in Morecambe Bay.

Watch this space. LNG

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

THE GLOBAL FSRU FLEET

TOP

FSRU newcomers(orderbook)

Research: Karen Thomas, Mike Corkhill

Infographic: Richard Neighbour

© LNG World Shipping, April 2016

EXCELERATE ENERGY Experience Excelsior Excellence Express Exemplar Exquisite Explorer Expedient Excelerate

59

GOLAR LNG Golar Winter Golar Spirit Golar Freeze Nusantara Tegas Satu Golar Igloo Golar Eskimo Golar Tundra Golar Arctic (FSU) Hull 2189

7+1

HÖEGH LNG Höegh Grace GDF Suez Neptune Independence Höegh Gallant PGN FSRU Lampung GDF Suez Cape Ann Hull 2685 Hull 2552 ordered HHI, Feb 2016 (TBC)

6+2+1 (unconfirmed)

BW GAS BW Singapore Hull 2118

1+1OLT FSRU Toscana

1

Mitsui OSK 1

Teekay LNG 1 (FSU)

Gazprom 1

Exmar 1 (barge)

LIVE FLEET+ORDERBOOK

Existing Proposed

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

THE GLOBAL FSRU FLEET

TOP

FSRU newcomers(orderbook)

Research: Karen Thomas, Mike Corkhill

Infographic: Richard Neighbour

© LNG World Shipping, April 2016

EXCELERATE ENERGY Experience Excelsior Excellence Express Exemplar Exquisite Explorer Expedient Excelerate

59

GOLAR LNG Golar Winter Golar Spirit Golar Freeze Nusantara Tegas Satu Golar Igloo Golar Eskimo Golar Tundra Golar Arctic (FSU) Hull 2189

7+1

HÖEGH LNG Höegh Grace GDF Suez Neptune Independence Höegh Gallant PGN FSRU Lampung GDF Suez Cape Ann Hull 2685 Hull 2552 ordered HHI, Feb 2016 (TBC)

6+2+1 (unconfirmed)

BW GAS BW Singapore Hull 2118

1+1OLT FSRU Toscana

1

Mitsui OSK 1

Teekay LNG 1 (FSU)

Gazprom 1

Exmar 1 (barge)

LIVE FLEET+ORDERBOOK

Existing Proposed

LNG World Shipping | May/June 2016 For more articles visit www.lngworldshipping.com

28 | FSRU infographic

EXISTING AND PLANNED FLOATING STORAGE AND REGASIFICATION (FSRU) PROJECTS WORLDWIDE, MAY 2016

Region Project name/location parties involved plan details

North America San Pedro de Macoris, Dominican Republic

BW Gas 1 mta FSRU/ FSU from 2016

South America Buenaventura, Colombia Government of Colombia barge-based option

South America Recife, Brazil Ebrasil is seeking a FSRU from 2019

South America Rio Grande do Sul, Brazil Bolognesi Group talks with Excelerate Energy

South America Suape, Brazil Bolognesi Group intends to import 2 mta from 2017

South America Sergipe, Brazil GenPower and Golar LNG joint venture. Golar LNG exclusive right to provide the FSRU

South America Mejillones, Chile Gas Atamaca talks with Golar LNG seeking a 1.5 mta FSRU for 15 years

South America GNL Penco, Concepcion Bay, Chile Cheniere/Australis looking for FRU to import 4.2 mta from 2017

South America San Vicente Bay, Chile ENAP wants to charter a 2 mta FSRU

Africa Dakar, Senegal Senelec, Mitsui and Nebras Power FSRU to be stationed near Dakar, capacity TBC

Africa Abidjan, Ivory Coast Petroci/Benin Electricity/Volta River Authority seeking a 2 mta FSRU or FSU for 10-year charter

Africa Ghana 1000, Takoradi, Ghana TBC

Africa Cotonou, Benin Gasol wants to import up to 1.2 mta into Benin, Togo and Ghana from 2016

Africa Walvis Bay, Namibia Xaris Energy/Excelerate Energy

Africa Adabiya, Egypt EGAS wants to charter its thrid FSRU/cross-check with above

Africa Saldanha Bay, South Africa IPP/Dept of Energy up to three FSRUs for 2018-2019 start. Karen Breytenbach, DoE

Europe Morecambe Bay, UK Port Meridian Energy 6 mta STL-buoy project

Europe Marsaxlokk, Malta Enemalta plans to charter an FSU

Europe Aegean LNG, Kavala, Greece DEPA plans to charter a 2.7 mta FSRU

Europe Alexandroupolis, Greece Prometheus Gas proposed 1.9 mta FSRU

Europe Yuzhny, Ukraine First Gas preliminary agreement with BW Gas for 1.4 mta FSRU

Europe Krk, Croatia Government of Croatia 2.4 mta FSRU or land-based terminal

Middle East Beirut, Lebanon Ministry of Energy tender relaunch planned for 1.3 mta FSRU

Indian subcontinent Karachi, Pakistan Government of Pakistan tender launch, January 2016

Indian subcontinent Gwadar, Pakistan Interstate Gas Systems/government of China FSRU option, TBC

Indian subcontinent Jafarabad, Gujarat Swan Energy/Exmar 4.5 mta FSRU

Indian subcontinent Swan LNG, Pipavav, India Swan Energy/Teekay LNG 5 mta FSRU, 2018

Indian subcontinent Mumbai India Gas Solutions 5 mta FSRU

Indian subcontinent Karwar, Karnataka, India Fox Petroleum 7.6 mta FSRU

Indian subcontinent Kakinada, India APGDC, Shell, Engie 5 mta FSRU

Indian subcontinent KG LNG, Kakinada, India VGS 4.5 mta, FSU or FSRU

Indian subcontinent Port of Kolkata Port of Kolkata and Excelerate 4 mta FSRU, 25 years

Indian subcontinent Krishnapatnam, Andhra Pradesh Petrogas 5 mta FSRU

Indian subcontinent H-Energy East Coast, Digha, India Hiranandani Group 8 mta FSRU

Indian subcontinent Moheshkhali Island, Bangladesh Petrobangla and Excelerate Energy 5 mta FSRU, 15 years

Asia Batangas, Philippines Shell 4 mta

Asia Philippines, TBC HiLoad LNG/Vires Floating regas dock (FRD)

Asia Cilamaya, West Java, Indonesia Pertamina 600,000 tonne FSRU

Asia Cilacap, Central Java, Indonesia Pertamina; Central Java FSRU 1.2 mta-1.6 mta FSRU

Asia Son My, Vietnam Petrovietnam 3 mta FSRU from 2020

Asia Thi Vai, Vietnam Petrovietnam 1 mta FSRU from 2017

Asia Gulf of Martaban, Myanmar Government of Myanmar 2.7 mta, Yangon FSRU

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

infographic FSRU | 29

CONFIRMED FLOATING STORAGE AND REGASIFICATION UNITS (FSRUS) AND FLOATING STORAGE UNITS (FSUS), APRIL 2016

Region Project name/location Vessel name Capacity, m3 owner charterer

Central America Aguirre Offshore GasPort, Puerto Rico TBC 150,900 Excelerate Energy Puerto Rico Electric Power Authority

South America Cartagena, Colombia Höegh Grace 170,000 Höegh LNG Sociedad Portuaria El Cayao

South America Pecém, Brazil Golar Spirit 129,000 Golar LNG Partners Petrobras

South America Bahia, Brazil Golar Winter 138,000 Golar LNG Partners Petrobras

South America Guanabara Bay, Rio de Janeiro, Brazil Experience 173,400 Excelerate Energy Petrobras

South America various Excelsior 138,000

South America GNL del Plato, Montevideo, Uruguay GDF Suez Neptune 145,000 Höegh LNG Gas Sayago

South America GNL del Plato, Montevideo, Uruguay Hull 2419 263,000 Mitsui OSK Gas Sayago

South America Bahia Blanca GasPort, Argentina Exemplar 150,900 Excelerate Energy YPF

South America GNL Escobar, Argentina Expedient 150,900 Excelerate Energy YPF

South America Penco-Lirquen, Chile Hull 2685 170,000 Hoegh LNG Penco-Lirquen

Caribbean Montego Bay, Jamaica Golar Arctic (FSU) 140,650 Golar LNG New Fortress Energy

Africa Tema, Ghana Golar Tundra 170,000 Golar LNG Partners West Africa Gas Ltd

Africa Ain Sokhna, Egypt Hoegh Gallant 170,000 Hoegh LNG EGAS

Africa Ain Sokhna, Egypt BW Singapore 170,000 BW Shipping EGAS

Europe Teesside, UK TBC Excelerate Energy

Europe Livorno, Italy FSRU Toscana 137,500 OLT Offshore LNG Toscana

Europe Kaliningrad, Russia Hull 2854 174,000 Gazprom Gazprom

Europe Klaipeda, Lithuania Independence 170,000 Höegh LNG Klaipedos Nafta

Middle East Hadera Gateway, Israel Excellence 138,000 Excelerate Energy Israel Electric

Middle East Aqaba, Jordan Golar Eskimo 160,000 Golar LNG Jordan LNG

Middle East Mina al-Ahmadi, Kuwait Golar Igloo 170,000 Golar LNG Kuwait National Petroleum

Middle East Jebel Ali, Dubai Golar Freeze 125,000 Golar LNG Dubai Supply Authority

Middle East Jebel Ali, Dubai Explorer 150,900 Excelerate Energy Dubai Supply Authority

Middle East Hidd, Bahrain Hull 2461 (FSU) 174,000 Teekay LNG Bahrain LNG

Indian subcontinent Port Qasim, Karachi, Pakistan Exquisite 150,900 Excelerate Energy Engro

Asia Tianjin, China GDF Suez Cape Ann 145,000 Hoegh LNG Partners Engie, sublet to CNOOC

Asia Lampung, Sumatra, Indonesia Lampung FSRU 170,000 Hoegh LNG Partners Perusahaan Gas Negara

Asia West Java, Indonesia Nusantara Regas Satu 125,000 Golar LNG Partners Nusantara Regas

Asia Bali, Indonesia FSU 26,000 JSK Group PT Pelindo Energi Logistik

Asia Bali, Indonesia FRU JSK Group PT Pelindo Energi Logistik

Unfixed Express 150,900 Excelerate Energy

Unfixed Excelerate 138,000 Excelerate Energy

Introducing the re-engineered Maritime Protection nitrogen system

• Unique system design with one of the smallest footprint in the market

• Fully automated control and monitoring system protects the membranes from potential damage and costly repairs

Wilhelmsen.com/technicalsolutions0

0.5

1m

1.5 m

PART OF THE SIMS PUMP COMPANY

Eliminate Corrosion Forever

THE PROVEN NAMEIN IMPELLER TECHNOLOGY

High T/C Levels? Minimize your time in yard for Special Surveys

Repair WBT coatings on voyage prior to SS Prepare for CAP surveys; - easier CAP 1 and

2 ratings Keep yard stays to a minimum

www.msi.no — [email protected] — T (47) 64 93 30 03

The “Voyage Repair” Specialists

Ballast Tank Upgrades Coating Inspectors Deck Upgrades Steel Inspectors Hull / Superstructure UHP Blasting Brazil Spray painting Norway Marine Scaffolding Singapore Steel repairs Gdynia SPS Overlay Nigeria

For more articles visit www.lngworldshipping.com LNG World Shipping | May/June 2016

Qatar Gas Transport Co (Nakilat): a story of growth

Qatar Gas Transport Company Ltd (Nakilat) could make an interesting case study at business school on how to successfully develop, implement and control a secure

shipping supply chain.Nakilat was formed in 2004 to deliver the 77 million tonnes

per annum (mta) of LNG that Qatar’s state-owned gas-producing companies RasGas and Qatargas planned to export. It secured 25-year contracts to ship the LNG from these producers and embarked on a huge LNG carrier newbuilding programme, said to have cost about US$11 billion.

As of April, the Nakilat-controlled fleet comprised 63 wholly or part-owned LNG carriers with a total capacity of 13 million m3 and a current value of US$11 billion, according to VesselsValue.com. The vessels are reported to be on 25-year charters, with ten-year options, to RasGas and Qatargas.

To maximise exports, Nakilat chose the largest membrane containment system designs in three size ranges: the Q-Max, at around 260,000m3; the Q-Flex, around 216,000m3; and large LNG carriers of around 150,000m3.

Q-Max and Q-Flex ships are said to be expensive to operate, due to the twin engine design, but since September, Nakilat has been testing the 2010-built Rasheeda, whose twin diesel engines have undergone a retrofit with MAN’s ME-GI dual-fuel propulsion system that can run on LNG.

Nakilat wholly owns all the Q-Max ships and holds a majority share of 16 of the Q-Flex types. Management and operation of these 31 vessels is a joint exercise with Shell International Trading and Shipping Company Ltd (STASCO) under a 12-year deal that started in 2008.

Under this agreement, STASCO is transferring its technical and LNG shipmanagement knowledge to Nakilat. This handover of expertise has already seen success in the case of four Nakilat

VLPG carriers now entirely managed by Nakilat Shipping Qatar, a wholly owned subsidiary. The remaining 36 LNG carriers in the Nakilat-controlled fleet are owned and operated by a small group of third parties, with Nakilat holding a significant share in the joint ventures of 43 per cent on aggregate, with buy-out options to purchase full control.

One of the major partners is Angelicoussis Shipping, which, through Maran Gas Maritime, has 15 LNG carriers chartered out to Qatari gas companies. Although Nakilat itself is no longer ordering LNG carriers – the last one was delivered in 2010 – the fleet available to Nakilat continues to expand through Maran Gas, which has 13 on order, with at least two said to be earmarked for Nakilat charters.

This highlights Nakilat’s future direction, relying on partners such as Maran Gas to provide the swing supply.