Embed Size (px)

Citation preview

Local Government Taxation Reform in Tanzania:Poverty and Social Impact Analysis

Presentation prepared for Workshop on Ex-ante Poverty Impact Assessment of Macroeconomic Policies,

Washington DC, March 13-16, 2006Paul Francis, Africa Department, IMF and

Sabine Beddies, Social Development Department, World Bank

The Context

o tax reforms in 2003 and 2004

o abolition of development levy & “nuisance taxes”

o business licence fees radically reduced

o future financing of local government in Tanzania

o role of central versus local revenue

o creating tax-service delivery links

Poverty and Social Impact Analysis (PSIA)

“A PSIA is an assessment of the distributional impact of specific policy reforms on the well-being or welfare of different stakeholder groups, with particular focus on the poor and vulnerable.”

Objectives of the Tax Reform PSIA

TO EXAMINE:

o tax burden by social group, before & after reform

o tax burden by small businesses, before & after reform

o attitudes of stakeholders

o broader policy initiatives on fiscal policy in the context of decentralization

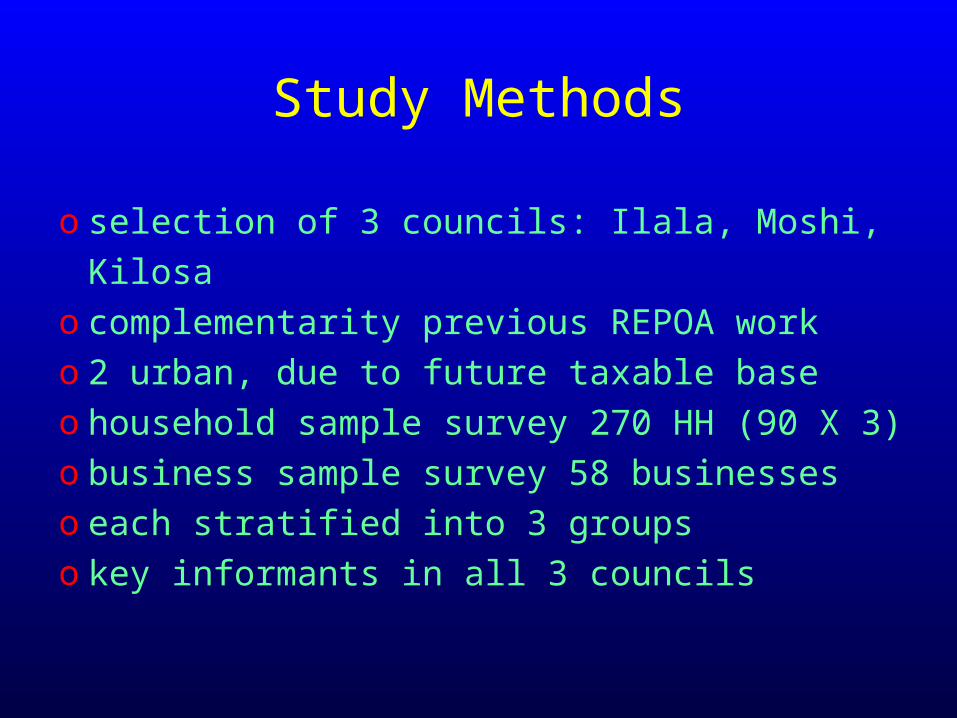

Study Methods

o selection of 3 councils: Ilala, Moshi, Kilosao complementarity previous REPOA worko 2 urban, due to future taxable baseo household sample survey 270 HH (90 X

3)o business sample survey 58 businesseso each stratified into 3 groupso key informants in all 3 councils

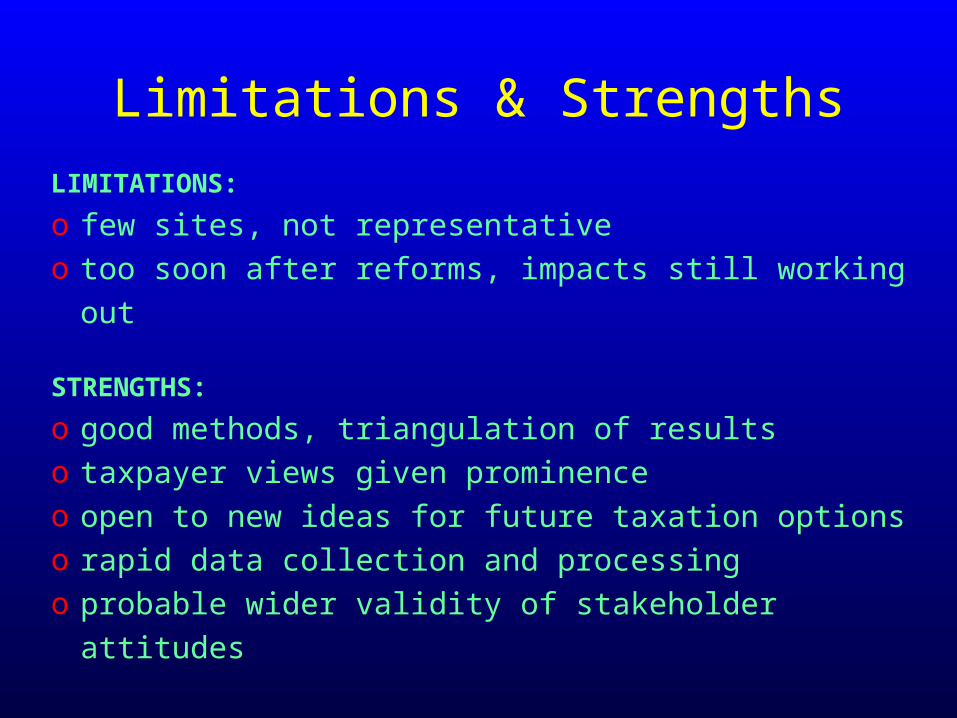

Limitations & Strengths

LIMITATIONS:

o few sites, not representativeo too soon after reforms, impacts still working out

STRENGTHS:

o good methods, triangulation of resultso taxpayer views given prominenceo open to new ideas for future taxation optionso rapid data collection and processingo probable wider validity of stakeholder attitudes

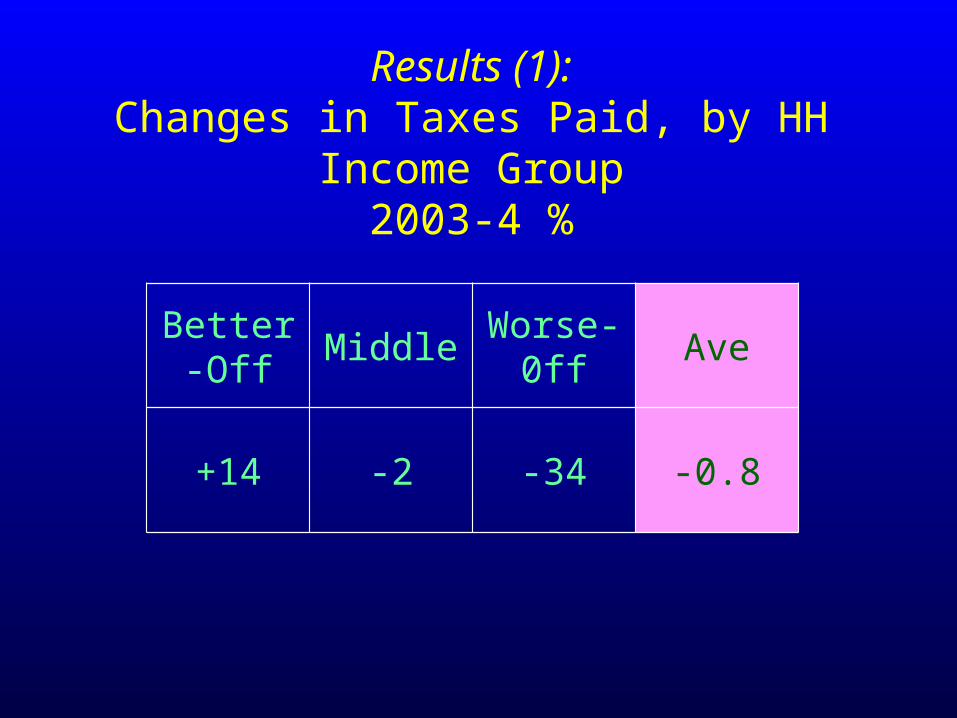

Better-Off

MiddleWorse-

0ffAve

+14 -2 -34 -0.8

Results (1):Changes in Taxes Paid, by HH Income

Group2003-4 %

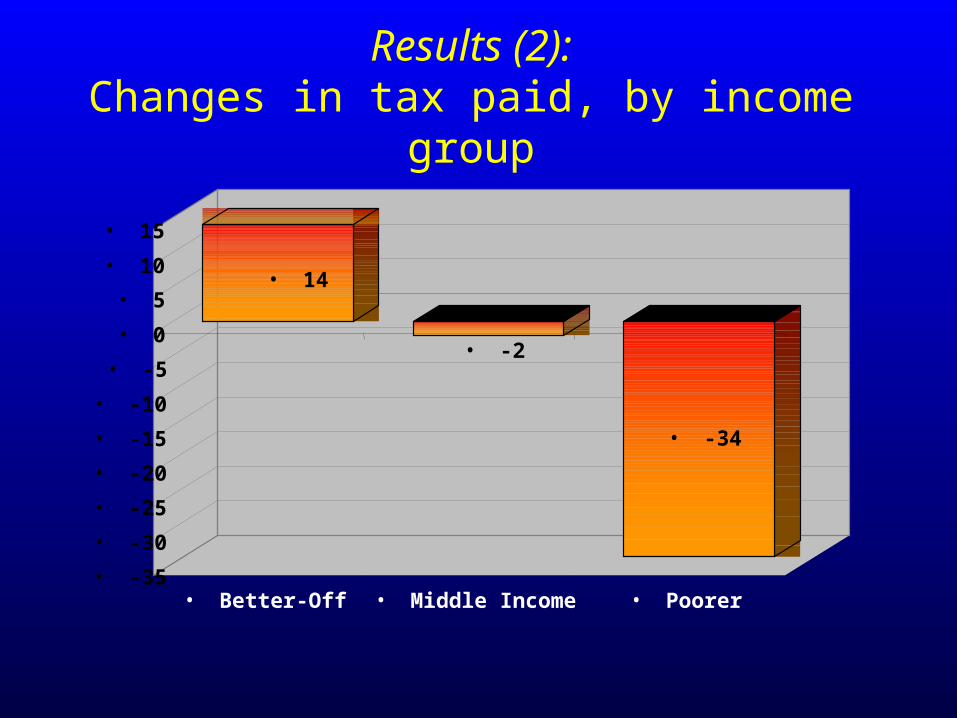

Results (2):Changes in tax paid, by income group

• 14

• -2

• -34

• -35

• -30

• -25

• -20

• -15

• -10

• -5

• 0

• 5

• 10

• 15

• Better-Off • Middle Income • Poorer

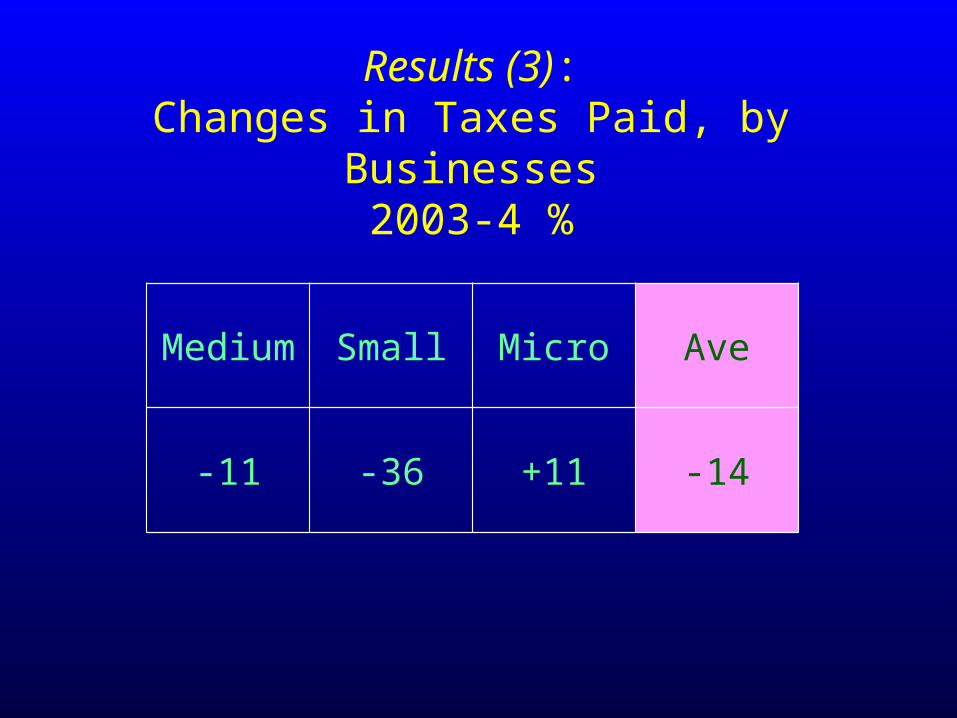

Medium

Small Micro Ave

-11 -36 +11 -14

Results (3):Changes in Taxes Paid, by Businesses

2003-4 %

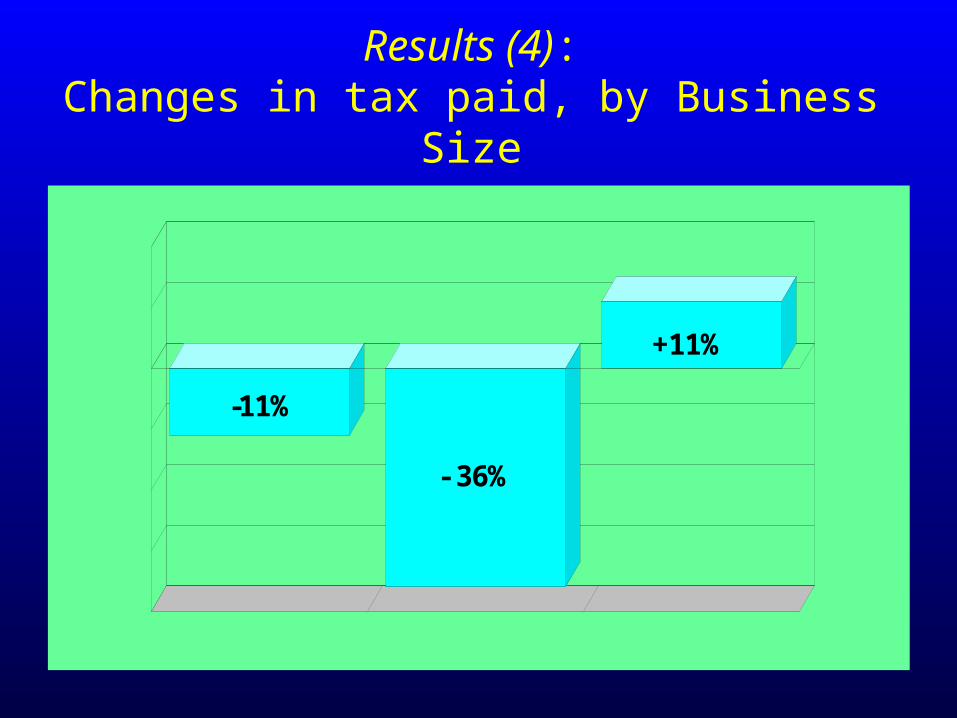

Results (4):Changes in tax paid, by Business Size

Medium Small Micro-40

-30

-20

-10

0

10

20

-11%

- 36%

+11%

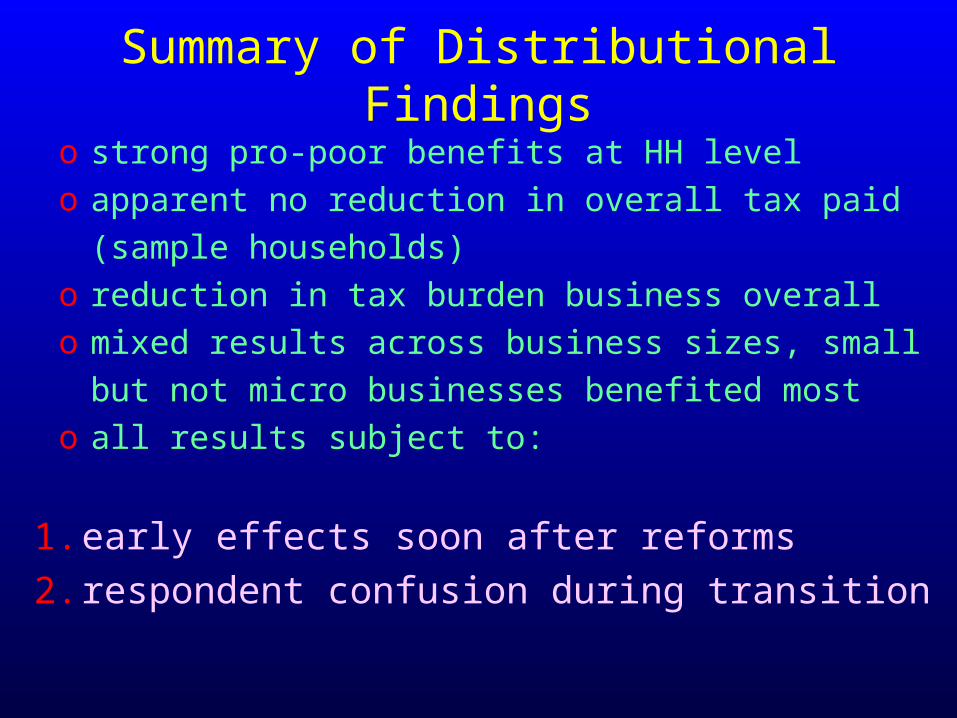

Summary of Distributional Findings

o strong pro-poor benefits at HH levelo apparent no reduction in overall tax paid

(sample households)o reduction in tax burden business overallo mixed results across business sizes, small

but not micro businesses benefited mosto all results subject to:

1. early effects soon after reforms2. respondent confusion during transition

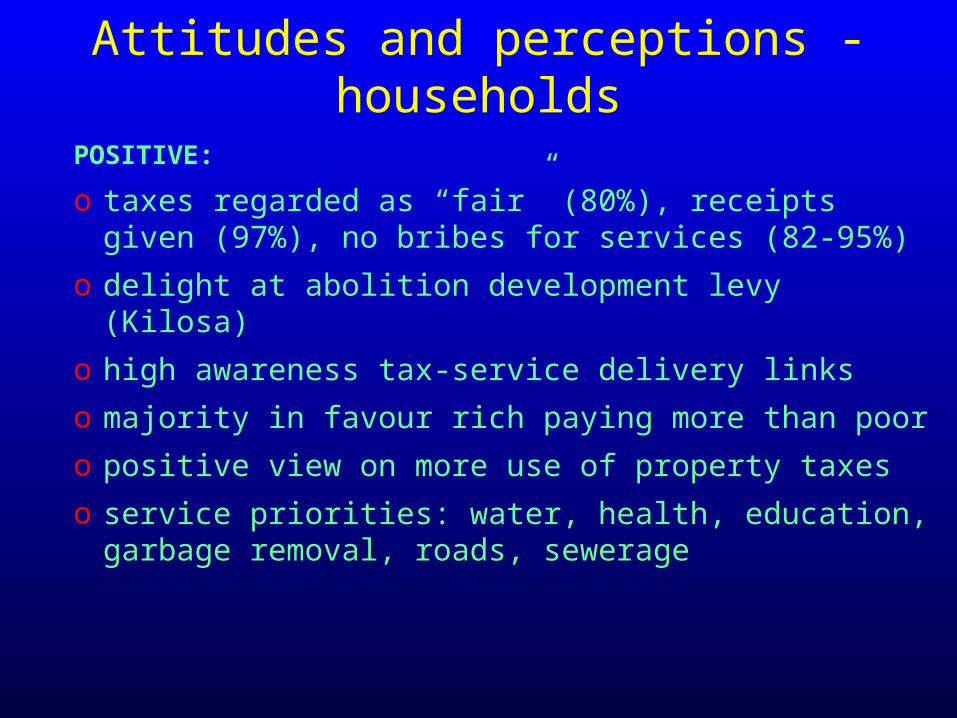

Attitudes and perceptions - households

POSITIVE:

o taxes regarded as “fair” (80%), receipts given (97%), no bribes for services (82-95%)

o delight at abolition development levy (Kilosa)

o high awareness tax-service delivery links

o majority in favour rich paying more than poor

o positive view on more use of property taxes

o service priorities: water, health, education, garbage removal, roads, sewerage

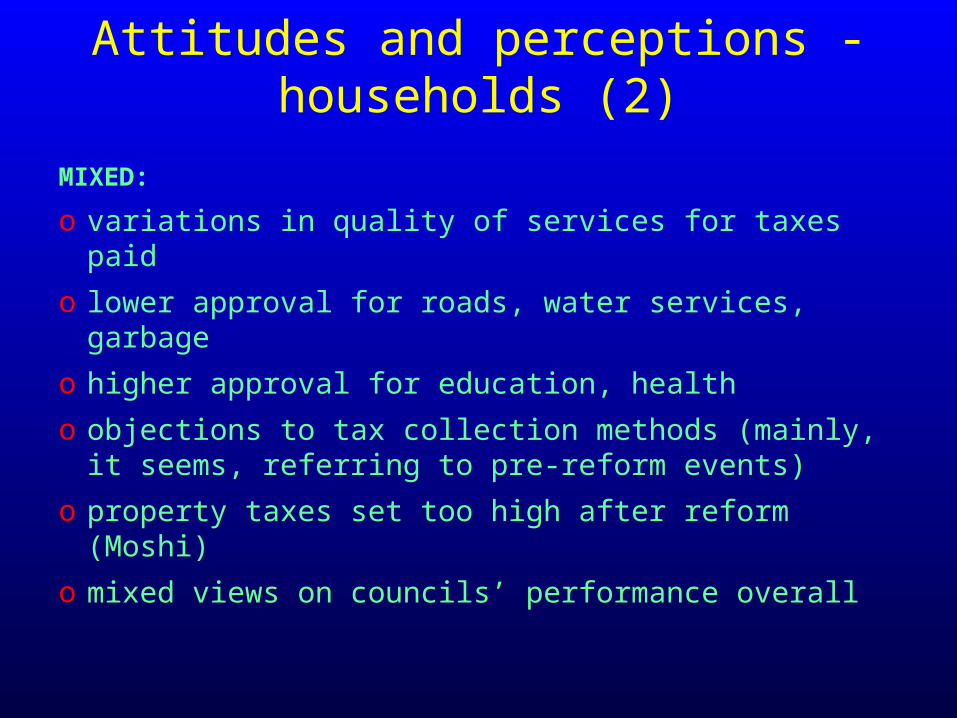

Attitudes and perceptions - households (2)

MIXED:

o variations in quality of services for taxes paid

o lower approval for roads, water services, garbage

o higher approval for education, health

o objections to tax collection methods (mainly, it seems, referring to pre-reform events)

o property taxes set too high after reform (Moshi)

o mixed views on councils’ performance overall

Attitudes and perceptions - Business

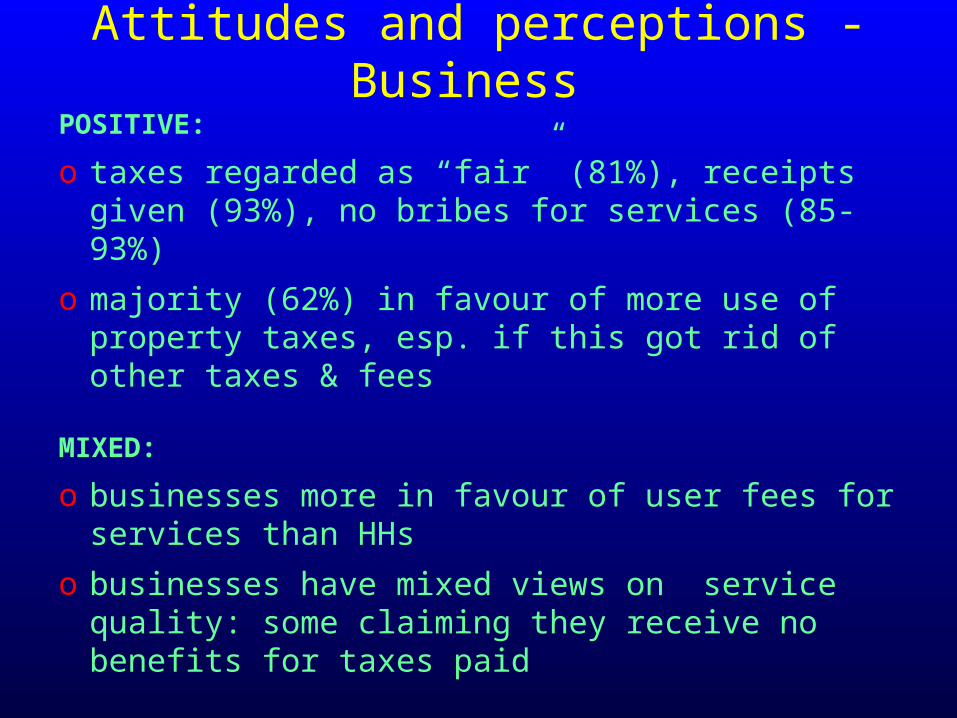

POSITIVE:

o taxes regarded as “fair” (81%), receipts given (93%), no bribes for services (85-93%)

o majority (62%) in favour of more use of property taxes, esp. if this got rid of other taxes & fees

MIXED:

o businesses more in favour of user fees for services than HHs

o businesses have mixed views on service quality: some claiming they receive no benefits for taxes paid

Views of Council Officials

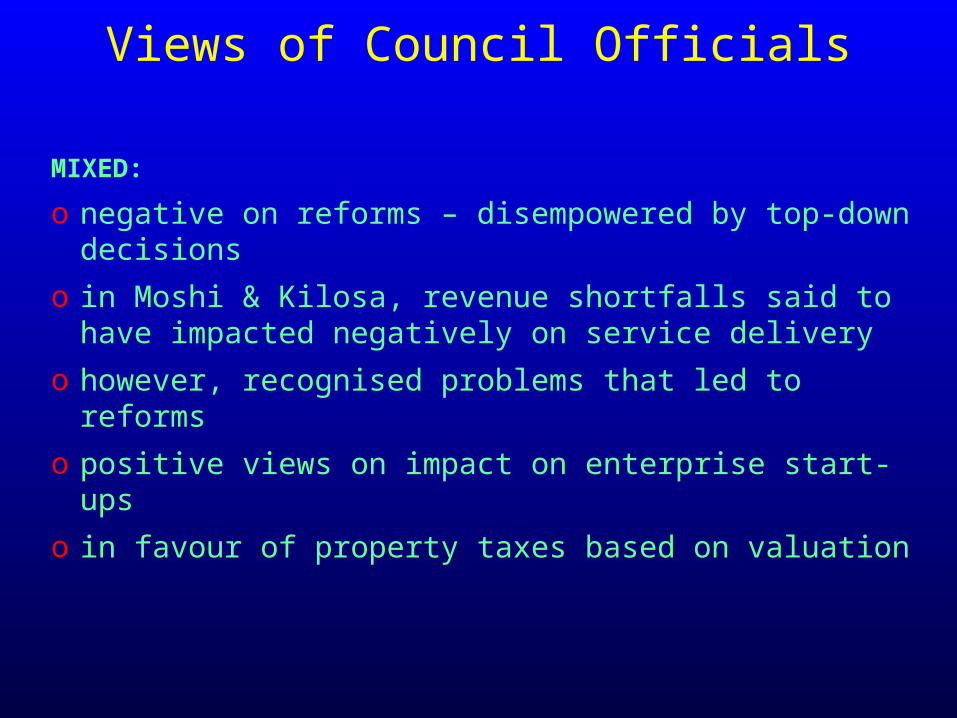

MIXED:

o negative on reforms – disempowered by top-down decisions

o in Moshi & Kilosa, revenue shortfalls said to have impacted negatively on service delivery

o however, recognised problems that led to reforms

o positive views on impact on enterprise start-ups

o in favour of property taxes based on valuation

Principles of Good Taxation

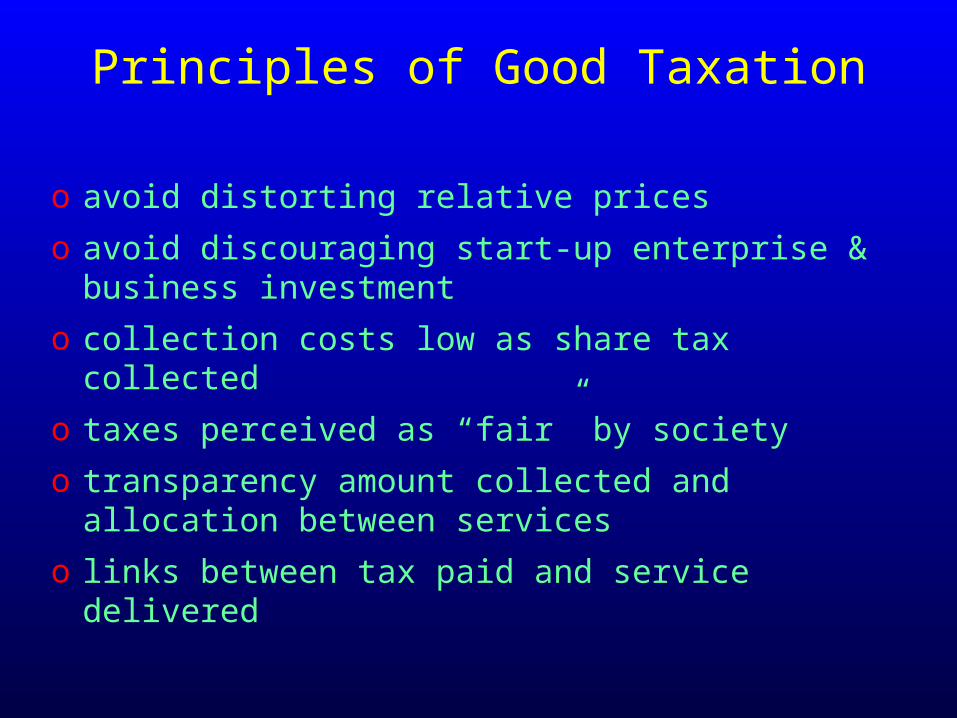

o avoid distorting relative prices

o avoid discouraging start-up enterprise & business investment

o collection costs low as share tax collected

o taxes perceived as “fair” by society

o transparency amount collected and allocation between services

o links between tax paid and service delivered

Post-Reforms Position

o considerable progress made with respect to these principles

o avoidance proliferation of new taxes critical

o in urban areas, property tax as means to avoid or cancel other taxes

o in rural areas, clarity about the purposes of local revenue and uses to which it can be put

o complementary role of user fees

Relying More on Property Taxes

“the taxation of real property is the superior route to creating a stable, predictable and sufficient revenue stream to provide the local governments with the bulk of their financial needs. Of all the options available, it is the most progressive and assured path.”

McCluskey et al. 2003

Conclusionso reforms were good for the poor and business

o further reductions in the revenue base of LGs should be avoided

o further studies: follow-on TZ/UG PSIA tax modeling work, GoT debates GSU local tax reform recommendations

o policy dialogue on holistic approach to future LG financing reform: service delivery expectations, share of cost between local and central governments, sustainable local tax regimes - all need to be jointly determined