Embed Size (px)

Citation preview

- By Aditya Gupta

Roll no. 857

B.B.A LLB (Hons.)

VI Semester

The Beginning

The Bank was started by a group of social workers and

labour movement activists, 1964, with a small share

capital of Rs. 5,000.

In a short period of time Abhyudaya Co-op. Credit

Society got converted into an Urban Co-op. Bank.

Finally in June 1965, Abhyudaya Co-op. Bank Ltd. was

established with the motto of "Prosperity through Co-

operation".

As on 31st March 2013, the bank has 1.51 lakh members and more than 16.66 lakh

depositors.

Bank has achieved substantial growth in all perspectives reflecting an overall growth

of 20.64% in business mix & total business mix of the bank has reached over Rs.

13145 Crore.

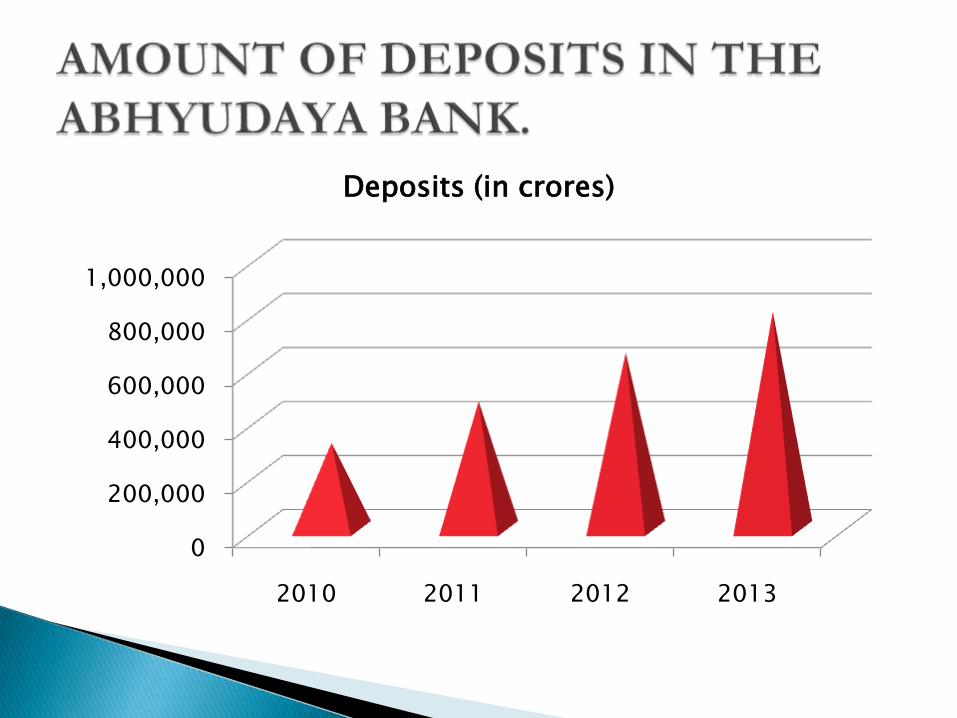

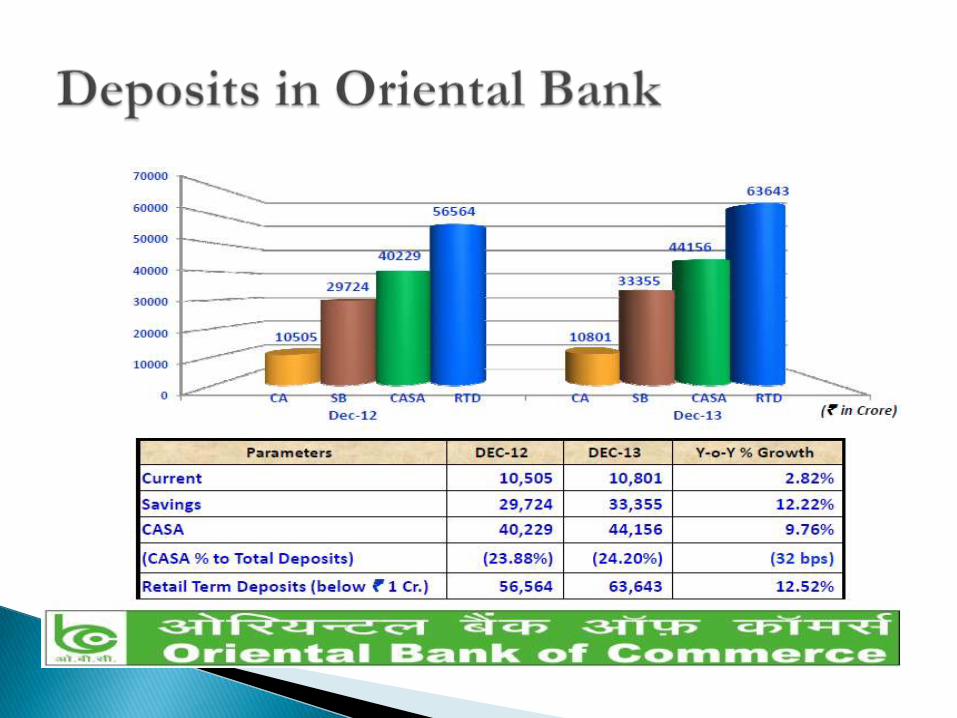

As on 31st March 2013, Bank’s Deposits have reached upto Rs. 8036.40 Crore with

rise of 23.27% while Advances have reached upto Rs. 5108.88Crore.

Paid up Capital and Reserves have amounted to Rs. 970.08 Crore and Investments

are to the tune of Rs. 3428.00 Crore.

For the F.Y. 2012-13, the Net Profit of the Bank after tax/provision stood at Rs.

91.22 Crore.

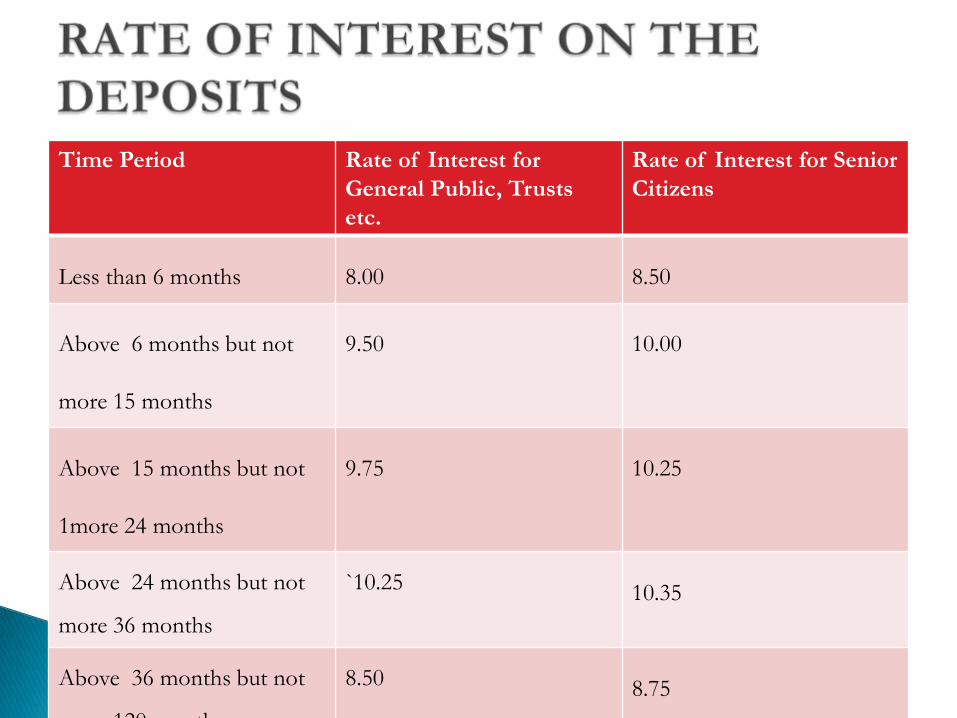

Time Period Rate of Interest for

General Public, Trusts

etc.

Rate of Interest for Senior

Citizens

Less than 6 months 8.00 8.50

Above 6 months but not

more 15 months

9.50 10.00

Above 15 months but not

1more 24 months

9.75 10.25

Above 24 months but not

more 36 months

`10.25 10.35

Above 36 months but not

more 120 months

8.50 8.75

0

200,000

400,000

600,000

800,000

1,000,000

2010 2011 2012 2013

Deposits (in crores)

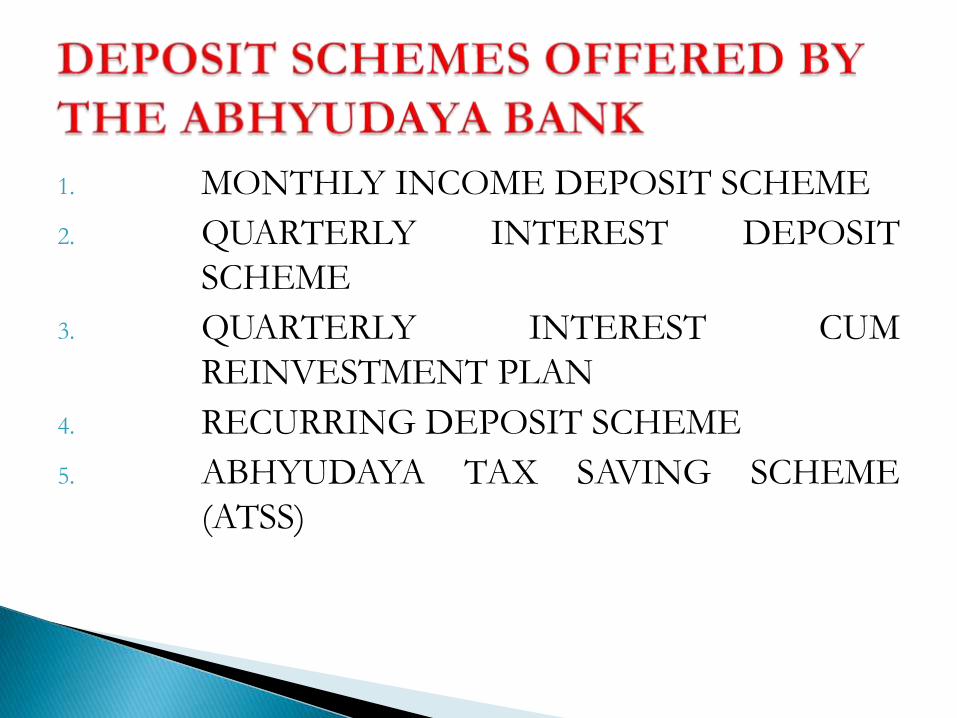

1. MONTHLY INCOME DEPOSIT SCHEME

2. QUARTERLY INTEREST DEPOSIT

SCHEME

3. QUARTERLY INTEREST CUM

REINVESTMENT PLAN

4. RECURRING DEPOSIT SCHEME

5. ABHYUDAYA TAX SAVING SCHEME

(ATSS)

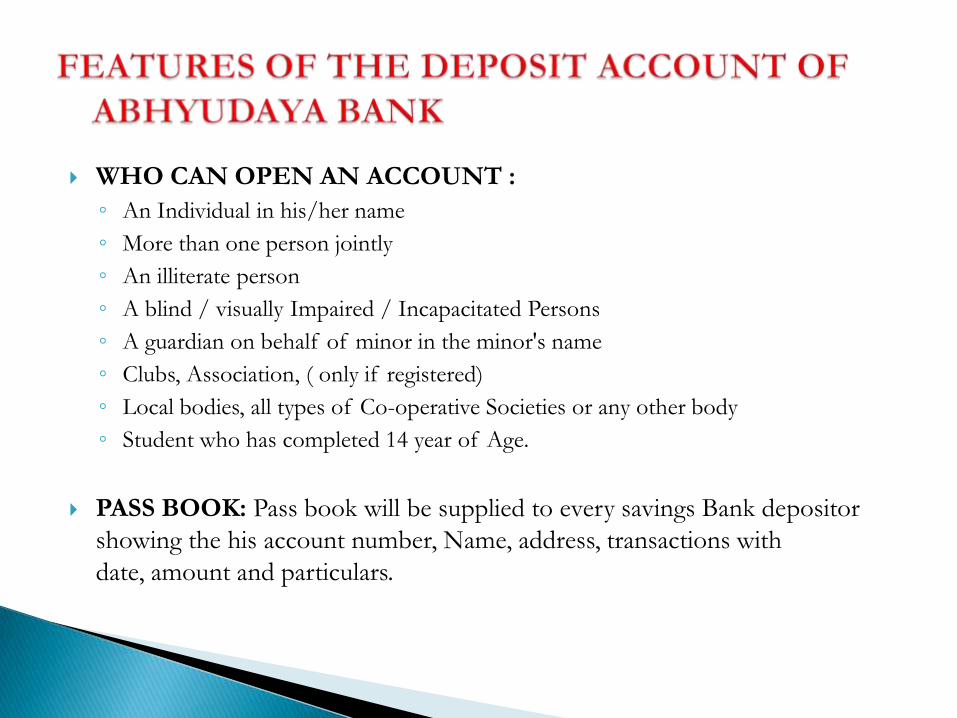

WHO CAN OPEN AN ACCOUNT :

◦ An Individual in his/her name

◦ More than one person jointly

◦ An illiterate person

◦ A blind / visually Impaired / Incapacitated Persons

◦ A guardian on behalf of minor in the minor's name

◦ Clubs, Association, ( only if registered)

◦ Local bodies, all types of Co-operative Societies or any other body

◦ Student who has completed 14 year of Age.

PASS BOOK: Pass book will be supplied to every savings Bank depositor

showing the his account number, Name, address, transactions with

date, amount and particulars.

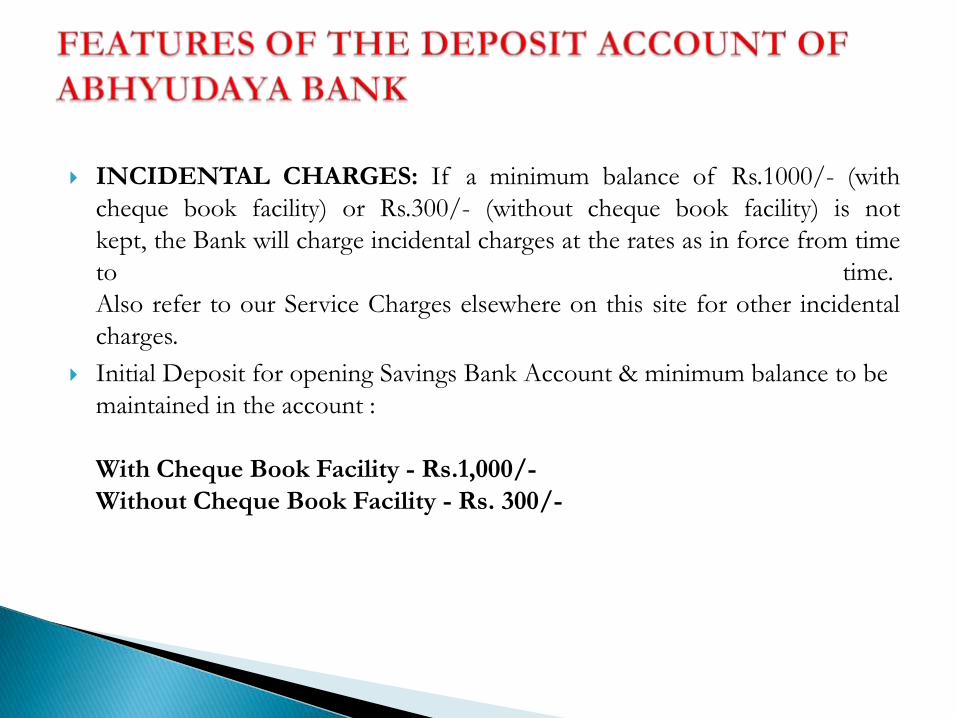

INCIDENTAL CHARGES: If a minimum balance of Rs.1000/- (with

cheque book facility) or Rs.300/- (without cheque book facility) is not

kept, the Bank will charge incidental charges at the rates as in force from time

to time.

Also refer to our Service Charges elsewhere on this site for other incidental

charges.

Initial Deposit for opening Savings Bank Account & minimum balance to be

maintained in the account :

With Cheque Book Facility - Rs.1,000/-

Without Cheque Book Facility - Rs. 300/-

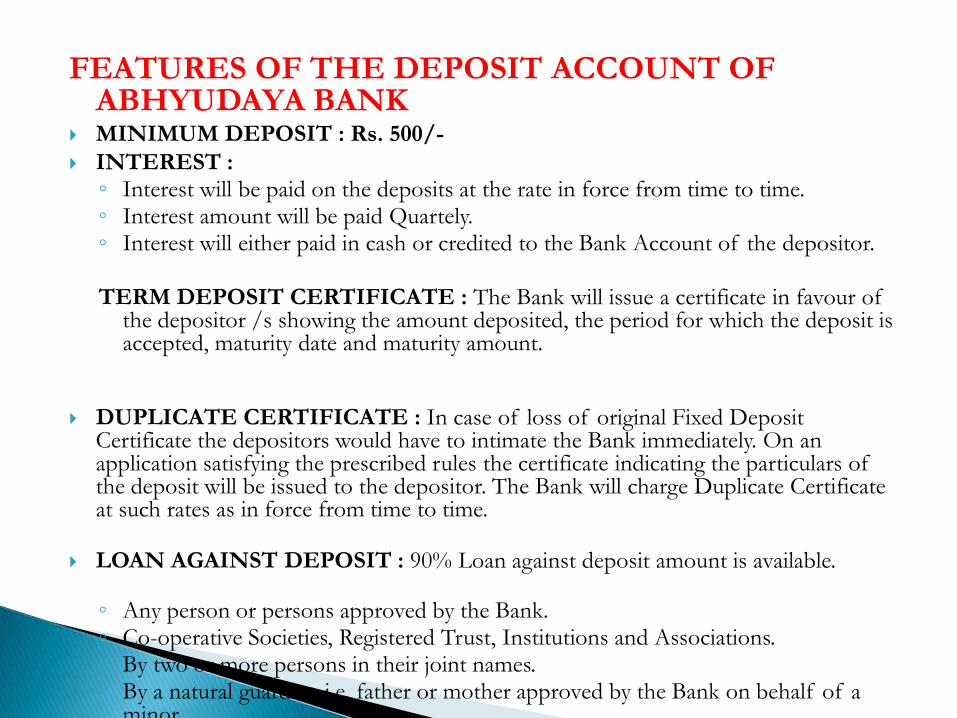

FEATURES OF THE DEPOSIT ACCOUNT OF ABHYUDAYA BANK

MINIMUM DEPOSIT : Rs. 500/-

INTEREST :◦ Interest will be paid on the deposits at the rate in force from time to time.◦ Interest amount will be paid Quartely.◦ Interest will either paid in cash or credited to the Bank Account of the depositor.

TERM DEPOSIT CERTIFICATE : The Bank will issue a certificate in favour of the depositor /s showing the amount deposited, the period for which the deposit is accepted, maturity date and maturity amount.

DUPLICATE CERTIFICATE : In case of loss of original Fixed Deposit Certificate the depositors would have to intimate the Bank immediately. On an application satisfying the prescribed rules the certificate indicating the particulars of the deposit will be issued to the depositor. The Bank will charge Duplicate Certificate at such rates as in force from time to time.

LOAN AGAINST DEPOSIT : 90% Loan against deposit amount is available.

◦ Any person or persons approved by the Bank.◦ Co-operative Societies, Registered Trust, Institutions and Associations.◦ By two or more persons in their joint names.◦ By a natural guardian i.e. father or mother approved by the Bank on behalf of a

minor.

ORIENTAL BANK OF COMMERCE : AN

INTRODUCTION

Established by Late Rai Bahadur Lala Sohan Lal in 1943.The bank was

nationalised on 15 April 1980. Within a decade the bank turned into one of

the most efficient and best performing banks of India.

The bank has progressed on several fronts crossing the Business Mix mark

of 2 lac crores as on 31 March 2012 making it the 7th largest Public Sector

Bank in India, achievement of 100% CBS, reorienting of lending strategy

through Large & Mid Corporates and establishment of new wings

viz., Rural Development and Retail & Priority Sector.

The Bank has to its utmost credit lowest staff cost with highest

productivity in the Indian banking industry.

VISION STATEMENT

"TO BE A CUSTOMER FRIENDLY PREMIER BANK COMMITTED TO

ENHANCING STAKEHOLDERS VALUE“

MISSION STATEMENT

Provide quality, innovative services with state-of-the-art technology in line

with customer expectations.

Enhance employees’ professional skills and strengthen cohesiveness.

Create wealth for customers and other stakeholders.

Time Period Rate of Interest for

Deposit less than 1 Cr.

Rate of Interest for

Deposit more than 1 Cr.

Less than 6 months 8.75 9.00

Above 6 months but not

more 15 months

9.00 9.00

Above 15 months but not

1more 24 months

9.00 9.25

Above 24 months but not

more 36 months

`9.00 9.00

Above 36 months but not

more 120 months

8.75 8.75

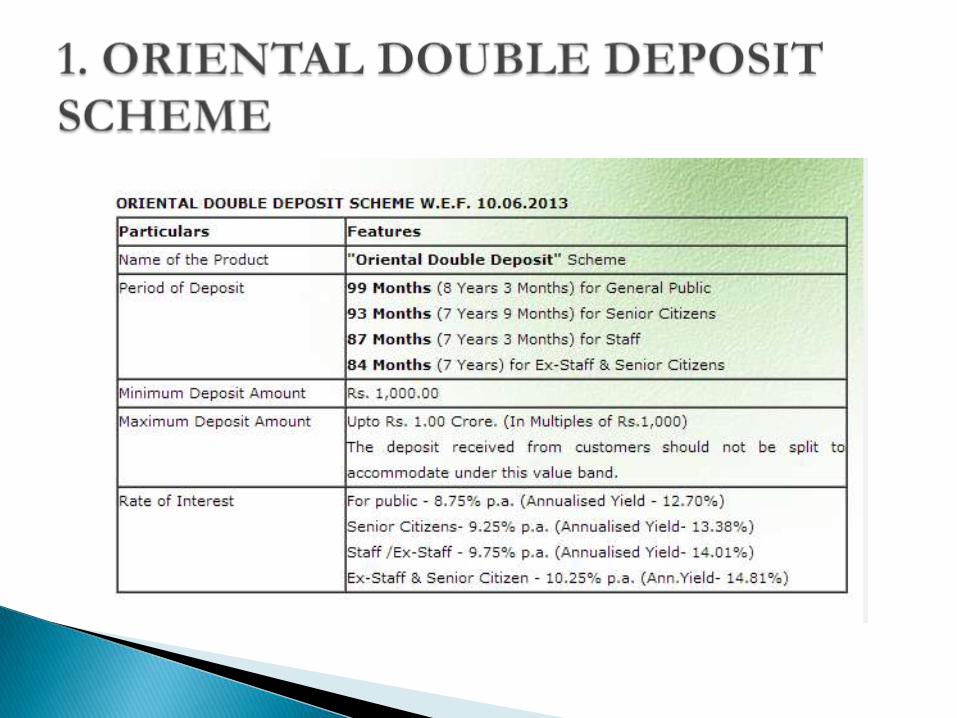

1. ORIENTAL DOUBLE DEPOSIT

SCHEME

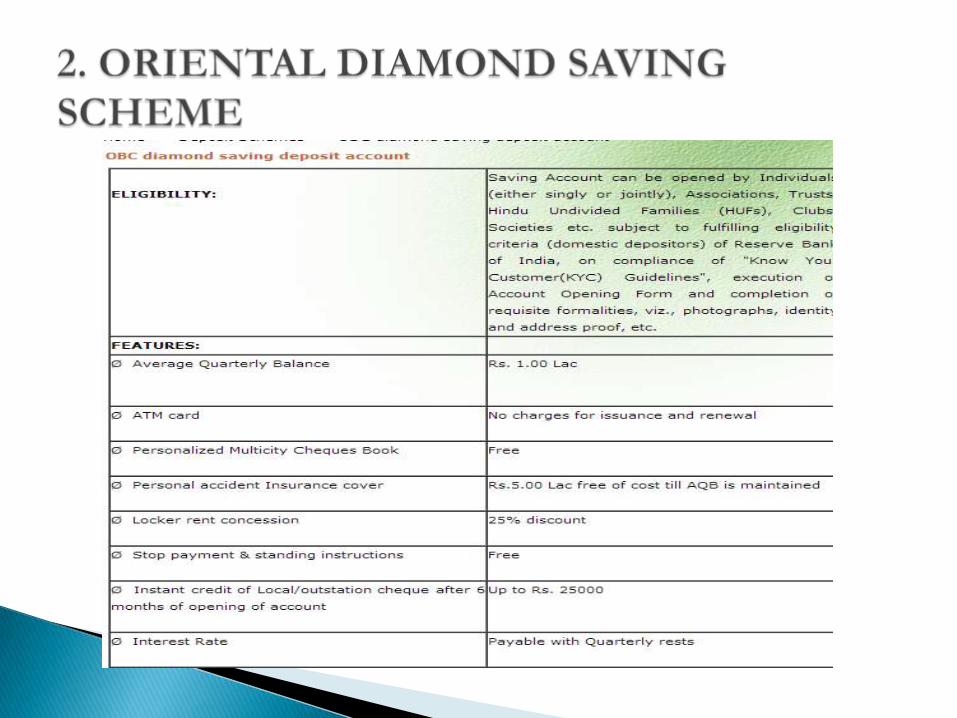

2. ORIENTAL DIAMOND SAVING

SCHEME

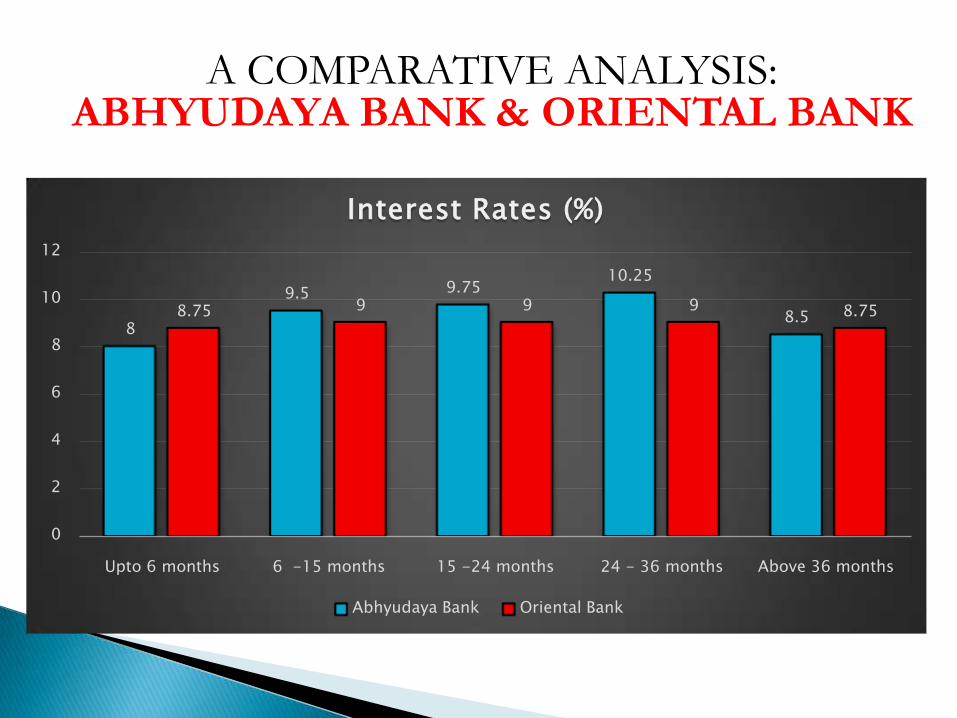

A COMPARATIVE ANALYSIS:ABHYUDAYA BANK & ORIENTAL BANK

8

9.5 9.7510.25

8.58.75 9 9 9 8.75

0

2

4

6

8

10

12

Upto 6 months 6 -15 months 15 -24 months 24 - 36 months Above 36 months

Interest Rates (%)

Abhyudaya Bank Oriental Bank

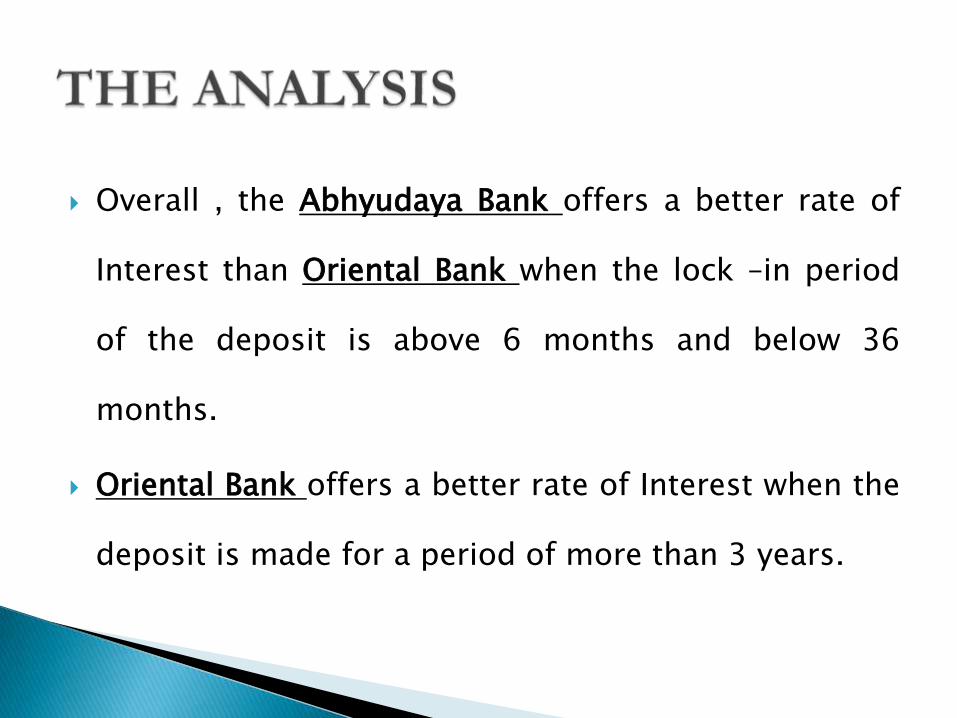

Overall , the Abhyudaya Bank offers a better rate of

Interest than Oriental Bank when the lock –in period

of the deposit is above 6 months and below 36

months.

Oriental Bank offers a better rate of Interest when the

deposit is made for a period of more than 3 years.

Abhyudaya Bank offers a high rate of Interest to

Senior citizens. Oriental bank does not offer any such

incentives.

However, Oriental Bank offers more deposit schemes

than the Abhyudaya Bank, giving investors the

opportunity to invest according to their requirements.