Embed Size (px)

Citation preview

Lucknow Residential Real Estate Overview

July 2012

2

TABLE OF CONTENTS

1. Executive Summary 3

2. Lucknow Fact File 4

3. Lucknow Real Estate 7

4. Micro Trends 10

5. Trans-Gomti Region - Zone 1 11

6. Trans-Gomti Region - Zone 2 13

7. Cis Gomti Region - Zone 3 15

8. Central Lucknow 17

9. Cis Gomti Region - Zone 5 19

10. Location Attractiveness Index 20

11. Disclaimer 21

3

The Lucknow Residential Real Estate Overview, July 2012, offers a comprehensive insight into the key macro andmicro trends evolving in the Lucknow residential realty markets. The ICICI Home Finance Company Research teamundertook a detailed city survey and elucidated below are the key findings of the report.

On the basis of geographical location and development history, the report has broadly classified the city into twoparts, Old Lucknow and New Lucknow. Old Lucknow was established during the 'Nawab' era and is typicallydotted with old-cramped developments. However, New Lucknow which has emerged only a few decades ago, isreplete with planned development and adequate social infrastructure. New Lucknow demonstrates high realestate potential and has been the focal point of our study.

Lucknow real estate market is currently a buyer's market and is largely driven by end users. Our estimatessuggest 40% investor participation in New Lucknow and we anticipate some rise in these numbers in the future.

The market is primarily driven by bureaucrats, politicians, public/government servants, some private sectoremployees and original inhabitants of Lucknow who have now migrated outside, yet wish to have a base inLucknow. Huge demand also flows in from surrounding cities on account of aspirations to enjoy better amenitiesand opportunities amiss in other cities of Uttar Pradesh.

Lucknow real estate markets have been stable with a slight upward bias. During the FY 2011-12 average priceappreciation in certain locations has been in the range of 8 - 15%.

A recent CRISIL report titled 'Real(i)ty Next-Beyond the top 10 cities of India’, stated that Lucknow is one of thenext top ten cities with enormous real estate potential. The builders exude positive market sentiment in the longrun, which is supported by the fact that many outside developers of repute have expressed interest in establishingtheir projects in the city.

The city's radial expansion has given way to new growth corridors on the real estate development map, especiallyalong the highways that connect with neighboring cities such as Kanpur, Rae Bareli, Hardoi, Sitapur, Faizabadand Sultanpur. The real estate markets along these regions have recently witnessed some traction and manyknown developers have launched their projects along these locations. Moreover, focus on the supportinginfrastructural development is also gaining ground.

While locations in Central Lucknow such as Mall Avenue and Jopling Road are old prime zones offering propertiesin the range of INR 3,500 - 6,500/sft., Gomtinagar and its extensions are new niche locations with properties in theprice bracket of INR 2,000 - 4,000/sft. on offer. Many good projects by known developers spread across Gomtinagar,Rae Bareli Road, Sultanpur Road, Faizabad Road, Hardoi Road and Jankipuram have evoked a good responsein the market.

The recent political change has brought a sense of optimism amongst market players. With the revival of LIDA(Lucknow Industrial Development Authority), there are plans to focus on Industrial and IT growth in the city. Suchdevelopments, once materialized, will provide the much needed impetus to the market demand.

Lucknow being the state capital, has emerged as a key center of business and financial activities for entire UttarPradesh. Government offices and BFSI sector are key segments which have witnessed growth in the city. Moreover,the Telecom sector has also emerged as a user of space in the city. MG Road (Mahatma Gandhi Road) atHazratganj is the Central Business District (CBD) housing the main government and BFSI sector offices. Gomtinagarzone (esp. Vibhuti Khand and Vipin Khand) is emerging as a Secondary Business District (SBD). Faizabad Road,Mahanagar and Aliganj also witnessed some amount of commercial activity.

The organised retail market activity has paced-up in the city, especially in the last 4-5 years. While MG Road andHazratganj are the most prominent shopping high-streets in Lucknow, Aminabad and Chowk are typical old retaildestinations famous for 'Chikankari' works of small-scale industries. Moreover, Mahanagar, Indiranagar andGomtinagar also have shopping arcades in various pockets. Organized retail is booming in the city and a numberof malls (located in Hazratganj, Gomtinagar and Alambagh) have obtained a decent response. Sahara mall(Hazratganj), East End mall, Zee mall, Riverside mall (Gomtinagar) and Phoenix United mall (Alambagh) areoperational malls witnessing decent foot-falls.

EXECUTIVE SUMMARY

4

City Overview

Lucknow Metropolis, the state capital of Uttar Pradesh, traditionally known for its rich cultural heritage and distinctetiquette is now emerging as one of the fastest growing non-metropolitan cities. Shedding its old image of a city famousonly for its unique styles of embroidery like 'Chikan' and 'Lakhnawi Zardozi', it is today a centre of modern technology,with a high level of investment, institutional development and progressive outlook. It is witnessing an economic boomwhich is reflected in the pace of real estate development in the city. Today, Lucknow is an amalgamation of culturedgrace and newly acquired pace.

Geographical Location

The city is geographically located at 26.50 N and 80.50 E in the Northern Gangetic plains, around 123 metres above sealevel. The present metropolitan area of Lucknow is envisaged to be 3091.40 sq km. The River Gomti flows through thecity, dividing the whole city diagonally into trans-Gomti and cis-Gomti regions. Some of the tributaries of this river arethe Kukrail, Loni and Beta. The Sai river flows from the south of the city. Lucknow witnesses diverse climatic conditions,with hot-humid summers from April to June (maximum temperature 470 C) and cool-dry winters from December toFebruary (minimum temperature 200 C).

Surrounding Towns and Cities

The city is surrounded by towns and villages like Malihabad, Kakori, Mohanlalganj, Gosainganj, Chinhat and Itaunja. Itis bounded by the Barabanki district in the east and the Sitapur district in the north. To the north west of the city is Hardoidistrict, while south-east and south-west are bounded by Rae Bareli and Unnao districts respectively.

Economy and Demographics

As per the provisional census 2011, the population of Lucknowhas seen a decadal growth of 25.79% and currently stands at4,588,455. This includes 2,407,897 males and 2,180,558 females.The district has a literacy rate of 79.33 %; male and female literacyare at 84.27% and 73.33% respectively. The sex ratio of Lucknowhas witnessed an increase of 2.03% over the decade and currentlystands at 906 females per 1000 males. The service sector formsthe main economic base of the city. Government departmentsand the public sector undertakings are the principal employers ofthe salaried middle-class. Liberalisation has created many moreopportunities and the service sector and self-employedprofessionals are burgeoning in the city.

History

Lucknow traces its origin to the Suryavanshi dynasty of Ayodhya in ancient times and derives its name from Lakshman,brother of Lord Rama, the hero of the Indian epic 'Ramayana'. The city came into eminence only during the 18thcentury. In 1732, Mohammad Shah, one of the later kings of the once powerful Mughal dynasty, appointed MohammadAmir Saadat Khan, a Persian adventurer of noble lineage, to the vice royalty of the area known as Awadh, of whichLucknow was a part.

At the time of the first war of independence in 1857, the city suffered a lot of damages, vestiges of which are still evidentin the dilapidated buildings. The old past was replaced with new developments during the British period. Postindependence, Lucknow replaced Allahabad as the capital of Uttar Pradesh.

LUCKNOW FACT FILE

Census 2011 Key Highlights

Description 2011 2001Actual Population 4,588,455 3,647,834Male 2,407,897 1,932,317Female 2,180,558 1,715,517Population Growth 25.79% 32.03%Area Square Km. 2,528 2,528Density/Square Km. 1,815 1,443Sex Ratio (females per 1000 males) 906 888Average Literacy Rate 79% 69%Male Literacy Rate 84% 76%

Female Literacy Rate 74% 60%

Source: Census 2011

5

Administrative Framework

Lucknow is the political and administrative capital of Uttar Pradesh. The city elects members to the Lok Sabha as wellas the Uttar Pradesh Vidhan Sabha (State Assembly). Lucknow has two Lok Sabha constituencies named Lucknowand Mohanlalganj.

The city is under the jurisdiction of a District Magistrate/Collector, who is an IAS officer. The Collector is in charge ofproperty records and revenue collection for the Government. The Collector oversees the national elections held in thecity and is also responsible for maintaining law and order.

The civic amenities of the city are managed by the Lucknow Municipal Corporation with executive power vested in theMunicipal Commissioner. The Corporation comprises elected members (corporators elected from the wards directlyby the people) with the City Mayor as its head. An Assistant Municipal Commissioner oversees each ward foradministrative purposes.

Existing and Upcoming Infrastructure

Lucknow has experienced immense infrastructural development in the past two decades. The development has acquiredpace during the last decade in terms of organised and planned development of roadways, entertainment zones, goodeducational institutions and other public amenities. Recently the city's central commercial hub, Hazratganj has undergonea makeover which gives it a near international look.

While New Lucknow, the part of the city that started to develop at a much later stage, has good infrastructural facilitiessuch as well-planned road networks, water and sanitation facilities, presence of organized retail and other socialamenities, the Old Lucknow region, that constitutes the older parts of the city established during the 'Nawab' era,suffers from unsatisfactory basic facilities. Lucknow being an eligible city in JNNURM (Jawaharlal Nehru NationalUrban Renewal Mission) is expected to witness improved infrastructure in the future.

Road Connectivity

There are four national highways and four state highways in the city:

National Highways State Highways

NH 24 connects Delhi SH 25 connects Hardoi

NH 25 connects Bhopal via Jhansi SH 36 connects Rae Bareli

NH 28 connects to Makama (Bihar) SH 56 connects Sultanpur

NH 56 connects to Varanasi SH 40 connects Mohaan.

Numerous bridges across Gomti river have been constructed to offer improved connectivity. Hardinge Bridge (nearImambara), Iron Bridge (at Daliganj), University Bridge and Nishaathganj Bridge are old bridges providing connectivityprimarily in the older part of the city. Gomti Barrage, Gandhi Setu and Ambedkar Park bridge are a set of parallelbridges providing good connectivity in the new part of Lucknow.

Initiatives have been taken to provide good intra and inter-city road connectivity.

Amar Shaheed Path is an elevated road, conceptualized in 2001, with the main aim to ease the traffic flow on the cityroads by providing a diversion to the long distance vehicles. Hence, traffic from Kanpur to Rae Bareli, Sultanpur andFaizabad, or vice versa will not have to enter the city. Apart from improving the inter-city links, the road will considerablybenefit the connectivity amongst all key locations and growth corridors within the city limits. The road starts at FaizabadRoad passes through Sultanpur Road (near Gomtinagar extension), Rae Bareli Road and ends at Kanpur road, spanninga stretch of approximately 23 km. It will also pass through many upcoming developer projects.

Other chief roads are the upcoming Lucknow-Kanpur Expressway and existing outer ring road.

LUCKNOW FACT FILE

6

Railway and Airway Connectivity

Lucknow is well-connected by rail and air routes to different parts of India. The main railway station is located atCharbagh. Further, there are 13 other railway stations within the city limits.

Chaudhary Charan Singh International Airport at Amausi, is located approximately 20 km from the city center. A newintegrated terminal has become operational from June 02, 2012, while the old terminal has been shut for repairs. The20,000 sq.m three-tier building, which can accommodate around 650 passengers at a time, is equipped with the latesttechnology, duty-free shops, cyber cafes, snack bars and shopping arcade.

Lucknow is directly connected by air with New Delhi, Patna, Kolkata, Mumbai and Hyderabad. International destinationsinclude Dubai, Muscat, Sharjah, Jeddah, Riyadh and Kathmandu (Nepal). During Haj, special flights are also operatedfrom Lucknow.

Lucknow Metro

The Lucknow Metro project is still in the planning stage. It would be built and operated by Lucknow Metro Rail Corporation.As per the proposed plan, the phase-I of the Lucknow Metro will constitute two lines and an extension line.

The proposed three corridors are:

North-South Corridor

This will connect Amausi airport to Munshipulia. This corridor is expected to have 21 stations.

Gomtinagar Link

Trains coming from the Airport Terminal will be diverted towards Gomti Nagar at the Indira Nagar Trisection (PolytechnicCrossing).

East-West Corridor

This will connect Lucknow railway station at Charbagh to Vasantkunj on Hardoi Road. This corridor is expected to have12 stations.

Focus on Industrial Development

Lucknow Industrial Development Authority (LIDA), constituted in 2005, is set to revive post a period of dormancy. LIDApossesses approximately 350 acres of land and is expected to acquire additional acres to boost the industrial developmentin the city.

An Information Technology park is planned on approximately 32 acres of land under LIDA, at Amausi Industrial area onthe Kanpur Road. It has been decided to develop the park on the 'walk to work' concept. Apart from office spaces,service apartments would also be set-up exclusively for employees of IT businesses. The anchor developer would berequired to develop IT towers and all requisite public amenities, in order to attract big IT companies for establishingtheir businesses. For the IT park, there are approximately 350 proposals from industrialists and the decision onapplications and allotment process is expected to start in near future. Nearly 25 acres of land has been sanctioned fordisaster management and training centre of the Indo-Tibetian Border Police. It has also been decided to develop anIndustrial corridor between Lucknow and Kanpur.

LUCKNOW FACT FILE

7

Short Term (10 - 12 months) Average appreciation of 8 - 10%

Long Term (50 - 60 months) 10 - 15% YoY average appreciation in capital valuewith an upward bias on a conservative note.

The above analysis pertains to the new and upcoming part of the city (referred to as New Lucknow in the report), wheredevelopmental activities indicate a promising real estate potential in the future. An average capital appreciation of 8 -10% is expected in the Lucknow residential real estate markets in the short term (10 - 12 months). However, over alonger span of 50 - 60 months, the market is expected to yield a year-on-year appreciation of 10 - 15% on a conservativenote.

This analysis is based on the past market trends, present builder/buyer sentiments and the enormous future real estatepotential. With the recent change in political scenario of the state, a sense of optimism prevails across the market.There are anticipations of certain key steps that would directly/indirectly boost the realty sector in the city. The revival ofLIDA, the plans of an upcoming industrial/IT corridor and a positive approach towards investments from outside the cityhave provided the impetus for growth in the real estate markets.

The upward bias over a five-year horizon is also based on the estimate that 40% of the current activity in New Lucknowis driven by investors and this is expected to intensify in the future. We analyzed the past price trends in certainlocations of New Lucknow, as depicted in the graphs illustrated in the later part of the report. We observed that pricesover the last one year (Q1-2011 to Q1-2012) have appreciated to the tune of 8 - 30%, while over a span of the last fiveyears, year-on-year appreciation ranged from 8 - 39%.

The real estate market of Lucknow is considered to be one of the most upcoming Tier-II markets on account of thehuge metamorphosis that the city is undergoing. While we analyze this outlook in the report, it is interesting to note thecontrasting nature of the two parts located within the same city but separated by river Gomti. These pockets havedifferent real estate dynamics driving them.

A Glimpse of Residential Development in Lucknow

On the basis of geographical location and development history, Lucknow city can be divided into Old and NewLucknow.

Old Lucknow, spread out in the cis-Gomti region, was established in the 'Nawabi' era. A major part of Old Lucknowis dotted with unplanned residential developments fraught with old architecture, heritage monuments, grosslyinadequate infrastructure, water and sanitation issues. The region is home to a number of handicraft factories forZardozi and Chikan embroidery work. People from varying socio-economic groups, ranging from wealthy establishedfamilies to families below poverty line reside here. There are hardly any multi-storied builder developments in thiscluster.

New Lucknow lies in the trans-Gomti region, with the exception of certain prime localities around Hazratganj (inCentral Lucknow) that are located in the cis-Gomti region. This part started to develop at a much later stage,therefore is equipped with well-planned roads, modern architecture and an organised social infrastructure. Whilethe real estate landscape is dotted with independent houses, the trend of apartment/floor establishments byreputed builders is now being witnessed.

Lucknow over the years has witnessed a radial growth, greater along the Faizabad Road and also along the roadsleading to other neighboring cities, hence carving out newer locations on the real estate development map.

Market Sentiment

The Lucknow real estate market is currently a 'buyer's market'. It is largely 'end-user' driven, with some investmentactivity prevalent in the new emerging locations. In New Lucknow, the investor participation is approximately 40%which is expected to escalate in the future. While investors are predominantly long-term investors, short termspeculation is still at a very nascent stage.

LUCKNOW REAL ESTATE

8

The investor base in the city includes bureaucrats, polititians and government officials, businessmen and alsomigrants who wish to own a second home in the city. Moreover, demand also flows in from residents of other citiesin Uttar Pradesh like Faizabad, Gonda, Bahraich, Sultanpur, Unnao, Sitapur, Barabanki, Allahabad, Kanpur andVaranasi, who aspire for an upgradation in living standards. The recent political change has created a sense ofoptimism amongst the market players, who are anticipating certain developments that will foster the real estatesector. The successful implementation of plans to develop an industrial and IT corridor may furnish the muchdesired impetus to the market demand that will further boost supply absorption and market liquidity.

A recent CRISIL report titled 'Real(i)ty Next - Beyond the top 10 cities of India', stated that Lucknow is one of thenext top ten cities with enormous real estate potential. The builders exude positive market sentiment in the longrun which is supported by the fact that many outside developers of repute have expressed interest in establishingtheir projects in the city. Developers show interest in Tier-II and Tier-III cities like Lucknow because of better profitmargins due to lower land costs.

The real estate market of Old Lucknow is predominantly end-user driven with very limited investment opportunities.The old colonies like Rakabganj, Chowk, Rajabazaar, Rajajipuram have been densely populated on account ofeasy availability of low priced real estate. It may be surprising to know that despite the underdeveloped infrastructure,property prices in several parts of Old Lucknow like Chowk are at par with the average prices prevailing in primelocalities like Gomti Nagar. The key reason is the high demand by owners willing to further expand their traditionalestablishments in these areas, amidst lack of fresh supply. Moreover, a number of wealthy business families thatreside here, possess huge potential spending power. Hence, this high demand and low supply, coupled with goodspending capability leads to property price escalations.

Independent Houses vs. Builder Developments

Lucknow is a city where people have been particularly attached to land. Most parts of the city are dotted withplotted/independent houses style development. While private developers have ventured into the city more than 3decades ago, offering planned plotted developments, their presence has paced-up in the last 5-6 years (especiallymulti-storied developments). Big real estate developers like DLF and Emaar MGF have recently forayed into theLucknow market while some known builders such as Rohtas, Eldeco, Unitech and Parsvnath have already beenoffering projects in the city. While the lure of land plots/independent houses is still rampant, migration to buildersocieties has been witnessed particularly on account of better amenities and security. Most builder projects in thecity offer a diverse product mix (comprising land plots, villas and floors), as per estimated demand.

Migration from Independent Houses to multi-storied Apartments

The city is undergoing a transition, wherein the appetite for plots/independent houses has seen some changetowards a taste for multi-storied developments. This is on account of diminishing supply of land plots within thedesired budget and lucrative amenities in builder developments. Moreover, the Lucknow Development Authorityhas not announced schemes for independent houses and plots for a long time and the schemes that have comeof late, offered apartment floors (in Gomtinagar and Jankipuram). This further leads to migration from independenthouses to apartments. This migration has been more prevalent in the niche areas like central Lucknow (JoplingRoad, Gokhale Marg), New Hyderabad and Gomti Nagar.

Land Acquisition by Private Developers

The developers buy land parcels that are sold or auctioned by the government authorities (Lucknow DevelopmentAuthority, Uttar Pradesh Housing and Development Board) or farmers. This phenomenon is visible in the developing/upcoming parts of the city like Faizabad Road, Gomti Nagar Extension, Rae Bareli Road and Hardoi Road.

There are several old 'kothis' erected over huge land parcels at various locations within the city. These kothis aregenerally old and dilapidated and many owners are offloading these properties. Builders are either purchasingthese kothis and reconstructing apartments or entering into a joint-development model with the owners whereinbuilders construct their project and share profits with the original owner. This trend is prevalent in developed areaslike Central Lucknow, New Hyderabad, Dalibagh, etc.

LUCKNOW REAL ESTATE

9

Investment Scenario in Lucknow/Growth corridors

After rigorous analysis it has been observed that certain locations in Lucknow have seen a sharp property pricegrowth to the tune of 25-50% in the past 2-3 years.

The locations that are considered hot-spots for investment are mainly in the trans-Gomti region. Locations suchas Gomtinagar, Indiranagar, Jankipuram and their extensions are certain growth corridors within the city.

However, as the city has been expanding radially, the highways connecting with surrounding cities such as Sitapur,Faizabad, Sultanpur, Rae Bareli, Kanpur and Hardoi have gained prominence in terms of infrastructural developmentand market activity. While infrastructure development is underway at these locations, mega projects by manyreputed developers like DLF, Ansals, Sahara, Eldeco and Unitech are under-construction and many new projectsare in the pipe-line.

Factors boosting Real Estate in Lucknow

The residential real estate in Lucknow has witnessed a rapid growth during the past few years. Key factorscontributing to the growth are:

1) Lucknow's position as the state capital and the second largest city of Uttar Pradesh. The city is the only largeurban centre amidst a number of small towns in the surrounding districts, making it an attractive destination.

2) Growing per capita income of state, coupled with positive aspirations of middle-class. The state's per capitaincome in FY 2011 stood at a moderate level of INR 26,211. Per capita income of Uttar Pradesh in FY 2006was INR 14,115 and has shown a progressive trend each year.

3) Improving infrastructure in terms of road networks, good educational institutions and organized retail. Creationof employment opportunities by the public and private sector companies is an added factor.

4) Availability of land at affordable prices when compared to metros, has led private developers to venture intothe market.

5) Presence of reputed private developers like DLF, Rohtas, Eldeco, Halwasiya, Emaar MGF, Ansals, Unitechand Sahara in the form of various mega projects with world class social amenities is slowly and graduallychanging the face of residential real estate in the city.

6) Lucknow's eligibility under JNNURM.

7) The proposed Metro in the city is another reason for the boom.

However, issues like slums mushrooming in almost all the parts of city, water-sanitation issues and pollution of theriver Gomti are a few causes of concern.

Supply vs Demand of Private Builder Developments

The current supply and demand ratio of builder developments is almost proportionate. However, how this ratio willfare in the future is debatable because a large number of units will find their way into the market. Developers feelthat this ratio will remain stable as supply will be released in various phases, in consonance with the increasingdemand. Moreover, if IT/ITeS grows as per predictions, the new employee base is expected to provide the muchneeded impetus to the market demand. This will enable faster absorption across all product mixes.

LUCKNOW REAL ESTATE

10

MICRO TRENDS

After analyzing the macro-trends of Lucknow real estate, we now delve deeper and analyze the micro-trends.

Methodology: For this analysis, we have divided the Lucknow real estate market into five zones on the basis ofgeographical location and the growth stimulators driving them. We have considered the trans and cis-Gomti regionsseparately. Each of these is further divided into two parts, while central Lucknow in the cis-Gomti region is consideredas a separate zone. Therefore, there are a total of 5 zones. The analysis of each zone is as follows:

11

Major Locations: Gomti Nagar Phase I, II and Extension, Indira Nagar, Chinhat, Faizabad Road, Rabindra Palli.

Key Highlights:

Gomti Nagar belt has emerged as a prime location in the city, with a fair mix of commercial, residential and retaildevelopments. Segregated into various phases and sectors, the landscape is dotted with the presence ofindependent houses and premium apartments. Many reputed developers are foraying into this location. Thecommercial/retail catchments, good social infrastructure and close proximity to CBD has enabled property priceappreciation to the tune of 6-10% over the last one year.

Faizabad Road, a road that connects Lucknow to Faizabad, has demonstrated active growth and is expected togrow further in the near future. The micro-market witnesses the presence of many educational institutions, residentialtownships and commercial/retail establishments (Nissan, Volkswagen, Toyota showrooms, Metro Cash & Carryto name a few). Recently Spencer's retail store started operations on this road. The market players anticipatemore consolidation activities (small players exiting to big players) to take place at this location. The residentialproperties along this road fall in the price band of INR 2,000 - 2,500/sft.

Chinhat, Deva Road: This is in close proximity to the Islamic shrine 'Deva Shareef'. The Tata automobile factorylocated in this area is the main growth driver for residential real estate here. The capital values are in the priceband of INR 2,000 - 2,500/sft.

Organized retail developments include the Zee mall, East End mall and Riverside mall in Gomti Nagar. Thefamous Taj Group's hotel is also located in the Gomtinagar region.

Growth Stimulators:

Many financial institutions, public/private sector companies and corporates like the Reserve Bank of India, Passportoffice, LDA office, Tata Consultancy Services, NTPC, Hindustan Times are located in Gomtinagar. The newpremises of U.P. High Court-Lucknow Bench are also under construction in this area. Moreover, the entire regionis in close proximity to the CBD. Maximum operational malls in the city are located in this region.

Good road connectivity owing to existing and upcoming wide roads, highways, bridges and flyovers. ShaheedPath touches Gomtinagar extension.

Well-developed social infrastructure in terms of hospitals (eg. Sahara, Ram Manohar Lohiya Hospital), reputededucational institutions (eg. Jagran School-Dainik Jagran's initiative, Jaipuria school and Institute of Management,Homeopathic Medical College) and other social amenities like shopping arcades, malls and multiplexes.

TRANS-GOMTI REGION - ZONE 1

Price Trends in Trans-Gomti Locations of Lucknow*

*Assuming 100 as the base for Q1-2008Source: ICICI Property Services Group

80

100

120

140

160

180

200

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Ind

ex

Gomti Nagar Indira Nagar Faizabad Road

12

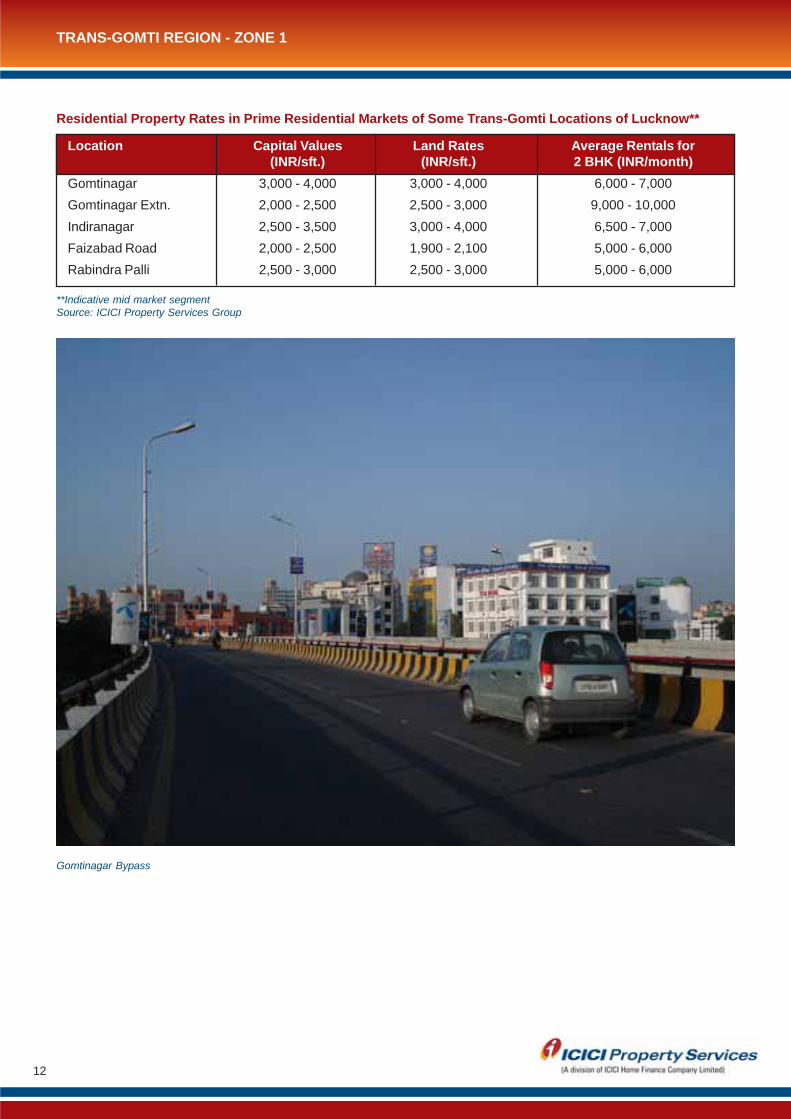

Residential Property Rates in Prime Residential Markets of Some Trans-Gomti Locations of Lucknow**

Location Capital Values Land Rates Average Rentals for(INR/sft.) (INR/sft.) 2 BHK (INR/month)

Gomtinagar 3,000 - 4,000 3,000 - 4,000 6,000 - 7,000

Gomtinagar Extn. 2,000 - 2,500 2,500 - 3,000 9,000 - 10,000

Indiranagar 2,500 - 3,500 3,000 - 4,000 6,500 - 7,000

Faizabad Road 2,000 - 2,500 1,900 - 2,100 5,000 - 6,000

Rabindra Palli 2,500 - 3,000 2,500 - 3,000 5,000 - 6,000

**Indicative mid market segmentSource: ICICI Property Services Group

TRANS-GOMTI REGION - ZONE 1

Gomtinagar Bypass

13

Major Locations: Sitapur Road, Janakipuram and extension, Aliganj, Niralanagar, Mahanagar and Daliganj.

Key Highlights:

These micro-markets typically comprise of independent houses. Re-development of old properties to builderapartments is prevalent in some of these locations.

Aliganj typically constitutes residences of government officials and coaching institutes. Head office of the SaharaIndia Group is located in Aliganj. The property prices in Aliganj and Niralanagar micro-markets have witnessed anappreciation in the range of 9-10% over the last one year.

While Aliganj, Niralanagar and Mahanagar are planned colonies that were developed more than 30-40 years ago,Jankipuram and Sitapur Road are comparatively new upcoming developments. Jankipuram is one of the locationswhere LDA recently offered apartment schemes. Properties in the price band of INR 2,000 - 4,000/sft can bewitnessed across these locations.

Aliganj, Niralanagar and Mahanagar predominantly witness transactions in the secondary markets. Of late, nomajor activity has been seen in these markets. However, construction of independent houses, private builderdevelopments and LDA apartments is rampant in Jankipuram and its extensions.

Major developers in the Jankipuram area include Sahara and SAS.

Growth Stimulators:

Presence of commercial catchments in Mahanagar and Aliganj coupled with good connectivity with the CBD hasdriven residential demand in these areas.

Presence of institutional buildings like Geographical Survey of India, Public Service Commission of Uttar Pradesh,Central Government Office Building Complex, Institute of Engineering and Technology and New Campus ofLucknow University. Moreover, adjoining Daliganj are the well-known Lucknow University campus and IsabellaThoburn College.

Well-developed public infrastructure offering good education facilities, presence of reputed hospitals and variousshopping arcades.

TRANS-GOMTI REGION - ZONE 2

*Assuming 100 as the base for Q1-2008Source: ICICI Property Services Group

Price Trends in Trans-Gomti Locations of Lucknow*

80

100

120

140

160

180

200

220

240

260

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Ind

ex

Janakipuram Scheme of LDA

Aliganj Chowk

Mahanagar

Nirala Nagar

14

Residential Property Rates in Prime Residential Markets of Trans-Gomti Locations of Lucknow**

Location Capital Values Land Rates Average Rentals for(INR/sft.) (INR/sft.) 2 BHK (INR/month)

Sitapur Road 2,000 - 3,500 1,500 - 2,000 4,000 - 5,000

Jankipuram and Extn. 2,000 - 2,500 2,000 - 2,500 5,000 - 6,000

Vikas Nagar 2,500 - 3,500 2,500 - 3,500 6,000 - 7,000

Nirala Nagar 3,000 - 3,500 3,000 - 3,500 6,000 - 7,000

Aliganj 3,000 - 3,500 3,000 - 3,500 6,000 - 7,000

Mahanagar 3,000 - 4,000 3,000 - 4,000 6,000 - 7,000

**Indicative mid market segmentSource: ICICI Property Services Group

TRANS-GOMTI REGION - ZONE 2

Parivartan Chowk

15

Major Locations: Kanpur Road, Rae Bareli Road, Sultanpur Road, LDA Colony, Ashiana Colony, South City,Vrindavan Upnagari, Alambagh.

Key Highlights:

Lucknow cantonment lies between the Rae Bareli Road and the Sultanpur Road. Since major portions of the areabelonged to the defence ministry, the area adjoining the Lucknow cantonment did not witness much developmentin the past. It was post the establishment of S.G.P.G.I (Sanjay Gandhi Post Graduate Institute of Medical Sciences)on Rae Bareli Road that urban residential development acquired pace.

Rae Bareli Road: This growth corridor has witnessed some traction of late and the residential projects locatedhere have evinced good response from the buyers. There are many government aided projects planned near thisroad. The road is well-connected with other parts of the city through the Shaheed Path.

Sultanpur Road houses many private educational institutions. The road is well-connected with other parts of thecity through the Shaheed Path. Several private developers have forayed into this area to develop residentialprojects. Currently, residential properties along this road are available in the price range of INR 2,000 - 3,000/sft.

Kanpur Road, a road between two main cities, is yet to evolve. However, with the recent political shift, the regionis believed to witness focused developmental activities to unlock the huge potential that the location is believed topossess. The region is primarily an industrial area and there are plans to set up an IT corridor in this region. Theestablishment of IT companies and corporates in the city will provide the much required impetus to the marketdemand. Project launches along this road by private developers, are anticipated.

This cluster also hosts the Vrindavan Upnagri, one of the biggest residential townships developed by Uttar PradeshAwas evam Vikas Parishad. The residential properties in this township fall in the price band of INR 2,000 - 3,000/sft.

Organised retail: Phoenix United Mall is located in the heart of Alambagh. It is strategically located in closeproximity to Lucknow's Amausi International Airport and the Charbagh Railway Station, along the Kanpur Road.

Major developers present in this area include Ansal and Unitech.

Growth Stimulators:

Good road connectivity with other parts of the city as well as neighbouring cities. Close proximity to Lucknowairport. Connectivity through Shaheed Path to various key locations within the city.

Industrial and IT corridor planned near Kanpur Road.

Decent social infrastructure and presence of reputed hospitals.

Presence of organized retail (Phoenix Mall) and commercial developments in various parts of this cluster.

CIS-GOMTI REGION - ZONE 3

Price Trends in cis-Gomti Locations of Lucknow*

*Assuming 100 as the base for Q1-2008Source: ICICI Property Services Group

50

100

150

200

250

300

350

400

450

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Ind

ex

LDA Colony

Kanpur Road

Ashiana

Sharda Nagar Scheme

Alambagh

16

Residential Property Rates in Prime Residential Markets of Cis-Gomti Locations of Lucknow**

Location Capital Values Land Rates Average Rentals for(INR/sft.) (INR/sft.) 2 BHK (INR/month)

Kanpur Road 1,500 - 2,000 1,500 - 2,000 4,000 - 5,000(very less supply)

Rae Bareli Road 2,200 - 3,000 1,500 - 2,500 4,000 - 5,000

Sultanpur Road 2,000 - 3,000 1,000 - 2,000 NA

Vrindavan Upnagari 2,000 - 3,000 2,000 - 3,000 5,000 - 6,000

Ashiyana Colony 2,500 - 3,500 2,500 - 3,500 6,000 - 7,000

Alambagh 2,000 - 3,000 2,500 - 3,500 5,000 - 6,000

South City (Unitech) 2,000 - 3,000 2,000 - 3,000 6,000 - 7,000

**Indicative mid market segmentSource: ICICI Property Services Group

CIS-GOMTI REGION - ZONE 3

New Lucknow Airport

17

Major Locations: Hazratganj, Jopling Road, Wazir Hasan Road, Mall Avenue, Aminabad, New Hyderabad, Kai-ser Bagh, Meenabagh (Commercial Area) and Aishbagh (Industrial Area).

Key Highlights:

Hazratganj is said to be the heart of Lucknow. It is a prime commercial and retail zone of the city. Many governmentoffices, private offices and financial institutions are located in this micro-market. Vidhan Sabha is located in thispart. Another commercial center is Aminabad, which is in close proximity to the old part of the city.

Mall Avenue, Jopling Road and Gokhale Marg are niche residential localities surrounding the CBD and arelandscaped with prime bungalow style or premium multi-storied developments. This micro-market is a seller'smarket, on account of mitigating residential supply. Hence, the high rates in these areas cannot be compared withthe rates in other locations of Lucknow. The property prices range from INR 3,500 - 6,500/sft.

Sahara Mall, located in this cluster is the pioneer mall in the city. This mall attracts maximum foot-falls.

Major developers present in this area include Eldeco, SAS and Halwasiya.

Growth Stimulators:

Presence of reputed financial institutions, corporate offices, excellent social infrastructure, niche residential localitiesand connectivity to various parts of the city are the growth drivers of this region.

Close proximity to all key areas of the city, on account of its central location.

Good connectivity to both trans and cis-Gomti regions of the city through roads and highways.

Presence of organized retail (Sahara Mall).

Lucknow Golf Club, one of the premier clubs of Lucknow, is located midway Hazratganj and Gomti Nagar.

CENTRAL LUCKNOW

Price Trends in Central Lucknow*

*Assuming 100 as the base for Q1-2008Source: ICICI Property Services Group

80

100

120

140

160

180

200

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Ind

ex

Hazratganj Gokhale Marg New Hyderabad

18

Residential Property Rates in Prime Residential Markets of Central Lucknow**

Location Capital Values Land Rates Average Rentals for(INR/sft.) (INR/sft.) 2 BHK (INR/month)

Hazratganj 3,500 - 4,500 4,000 - 5,000 9,000 - 10,000

Jopling Road/ 4,000 - 6,500 4,000 - 5,000 9,000 - 10,000Gokhale Marg (very less supply)

Mall Avenue 3,500 - 4,500 4,000 - 5,000 9,000 - 10,000

Aminabad 2,000 - 3,000 2,000 - 3,000 5,000 - 6,000

New Hyderabad 3,000 - 4,000 3,000 - 4,000 7,000 - 8,000

Paper Mill Colony 2,000 - 4,000 2,000 - 2,500 7,000 - 8,000 (Metro City)

**Indicative mid market segmentSource: ICICI Property Services Group

CENTRAL LUCKNOW

Hazratganj

19

Major Locations: Hardoi Road, Alambagh, Rajajipuram, Chowk, Thakurganj and other locations of old Lucknowcity.

Key Highlights:

Major parts of this region consist of old developments like Chowk, Rajajipuram, Thakurganj and Rakabganj. Thispart of Lucknow is saturated, except for certain upcoming areas like Hardoi Road and IIM Road.

Hardoi Road/IIM Road is a growth corridor and many known developers have been venturing into this part todevelop residential projects. The premier management institute 'Indian Institute of Management, Lucknow' islocated near Hardoi Road. Both government authorities and private developers have planned residential projectsin this area. Main developers present in this area include Sahara and Eldeco.

While Alambagh and its adjoining areas are primarily commercial zones, Chowk is a mix of residential andcommercial developments and is the centre for 'Chikan' and 'Zardozi' embroidery. Rajajipuram is one of theplanned colonies of old Lucknow. Many heritage monuments and famous 'Imambaras' are located in Chowkmaking it often frequented by tourists.

The entire old Lucknow belt predominantly witnesses secondary market transactions. However, primary markettransactions can be seen in the Hardoi Road belt.

CIS-GOMTI REGION - ZONE 5

Residential Property Rates in Prime Residential Markets of Cis-Gomti Locations of Lucknow**

Location Capital Values Land Rates Average Rentals for(INR/sft.) (INR/sft.) 2 BHK (INR/month)

Hardoi Road/IIM Road 1,500 - 2,500 1,500 - 2,500 5,000 - 6,000

Rajajipuram 2,000 - 3,000 2,000 - 3,000 5,000 - 6,000

Chowk 2,000 - 3,000 2,000 - 3,000 5,000 - 6,000

**Indicative mid market segmentSource: ICICI Property Services Group

Vidhan Sabha

20

Source: ICICI Property Services Group

LOCATION ATTRACTIVENESS INDEX

Location Attractiveness Index

Explanatory Note: While Central Lucknow and Gomtinagar show greys/blues on almost all parameters(which is positive), the maroon boxes indicate high residential property prices. Out of the short-listedlocations while Central Lucknow, Gomtinagar, Indiranagar and Aliganj are established prime localities,Rae Bareli Road, Faizabad Road, Sitapur Road, Hardoi Road and Kanpur Road are emerging corridorswitnessing traction.

Good / Low cost

Above Average

Average / Medium Cost

Below Average

Bad / High Cost

Infrastructure(connectivity, roads,markets, schools)

Residential Cost

Proximity to OrganisedRetail

Proximity to CommercialDevelopment

Future InfrastructureDevelopment

Future EmploymentGeneration

Gomti-nagar

Indiranagar

CentralLucknow

Jankipuram Aliganj

RaeBareliRoad

HardoiRoad

KanpurRoad

SitapurRoad

FaizabadRoad

GomtinagarExtn.

21

ANALYST

DEEPIKA SRIVASTAVAssistant Manager - ResearchICICI Property Services [email protected]

For any further queries, please e–mail us at [email protected]

or

For more on our research reports & periodicals please log on to www.icicihfc.com

ICICI HFC DISCLAIMERS & DISCLOSURES

The information set out in this document has been prepared by ICICI HFC Ltd. based upon projections which havebeen determined in good faith by ICICI HFC Ltd. There can be no assurance that such projections will prove to beaccurate.

ICICI HFC Ltd. does not accept any responsibility for any errors whether caused by negligence or otherwise or forany loss or damage incurred by anyone in reliance on anything set out in this document. The information in thisdocument reflects prevailing conditions and our views as of this date, all of which are subject to change. In preparingthis document we have relied upon and assumed, without independent verification, the accuracy and completenessof all information available from public sources or which was provided to us or which was otherwise reviewed by us.Past performance cannot be a guide to future performance.

No reliance may be placed for any purpose whatsoever on the information contained in this document or on itscompleteness. The information set out herein may be subject to updating, completion, revision, verification andamendment and such information may change materially.

This document is being communicated to you solely for the purposes of providing our views on current markettrends. This document is being communicated to you on a confidential basis and does not carry any right of publicationor disclosure to any third party. By accepting delivery of this document each recipient undertakes not to reproduceor distribute this presentation in whole or in part, nor to disclose any of its contents (except to its professionaladvisers) without the prior written consent of ICICI HFC Ltd., who the recipient agrees has the benefit of thisundertaking.

The recipient and its professional advisers will keep permanently confidential information contained herein and notalready in the public domain. This document is not an offer, invitation or solicitation of any kind to buy or sell anysecurity and is not intended to create any rights or obligations. Nothing in this document is intended to constitutelegal, tax, securities or investment advice, or opinion regarding the appropriateness of any investment, or a solicitationfor any product or service. The use of any information set out in this document is entirely at the recipient's own risk.