Embed Size (px)

Citation preview

m i l l e r & c h e v a l i e r Chartered

Anti-Money Laundering Compliance Overview

Michael L. Burton

James G. Tillen

Miller & Chevalier Chartered

May 18, 2005

2

WHAT IS MONEY LAUNDERING?

“Process by which one conceals the existence, illegal source, or illegal application of incomes, and disguises that income to make it appear legitimate”

Money laundering represents between 2 and 5 percent of global gross domestic product ($800 billion to $2 trillion annually)

3

THE U.S. ANTI-MONEY LAUNDERING FRAMEWORK

Money Laundering Control Act

Bank Secrecy Act

USA PATRIOT Act

4

MONEY LAUNDERINGCONTROL ACT (“MLCA”)

Transfers of money derived from specified (“predicate”) offenses

Transactions with proceeds of specified offenses

Similar to mail fraud and wire fraud

5

PREDICATE OFFENSES

Literally hundreds of predicate offenses

Traditional organized crime offenses: murder, arson, robbery, extortion, drug trafficking, RICO, etc.

White collar crimes: fraud and other financial crimes

Violations of international regulatory regimes: FCPA, export control violations, customs violations, foreign law (e.g., currency controls) (note: PATRIOT Act additions)

6

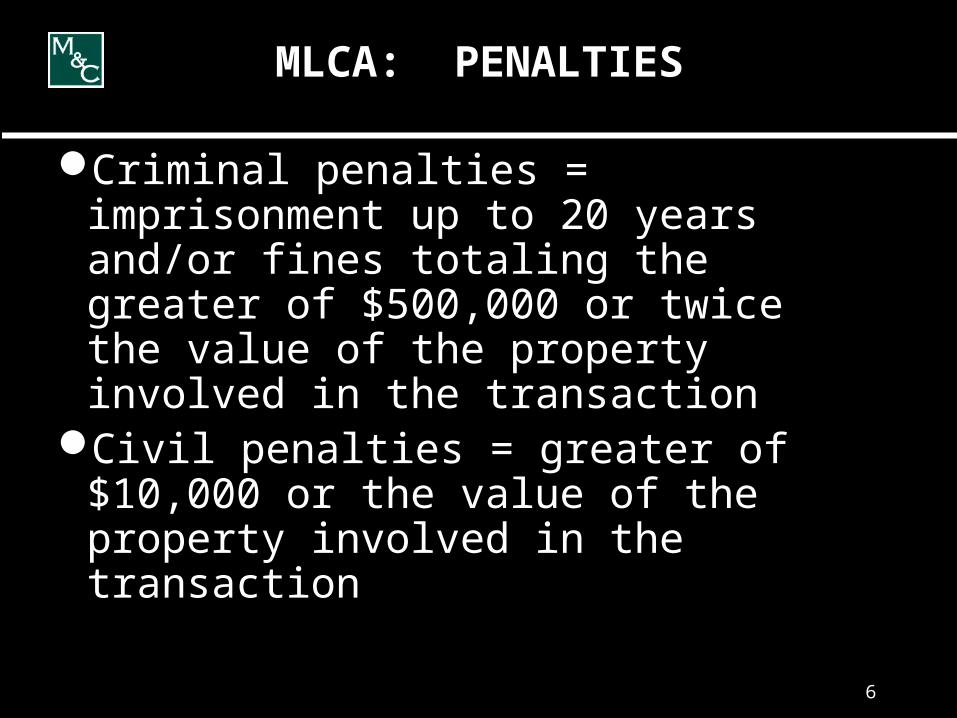

MLCA: PENALTIES

Criminal penalties = imprisonment up to 20 years and/or fines totaling the greater of $500,000 or twice the value of the property involved in the transaction

Civil penalties = greater of $10,000 or the value of the property involved in the transaction

7

BANK SECRECY ACT (“BSA”)

Reporting and record-keeping obligations for “financial institutions”

Pre-PATRIOT Act generally targeted only activities of banks

PATRIOT Act expanded definition of “financial institutions”

Suspicious transaction reporting requirements for certain financial institutions

Cash reporting (>10K) for non-financial trades and business

8

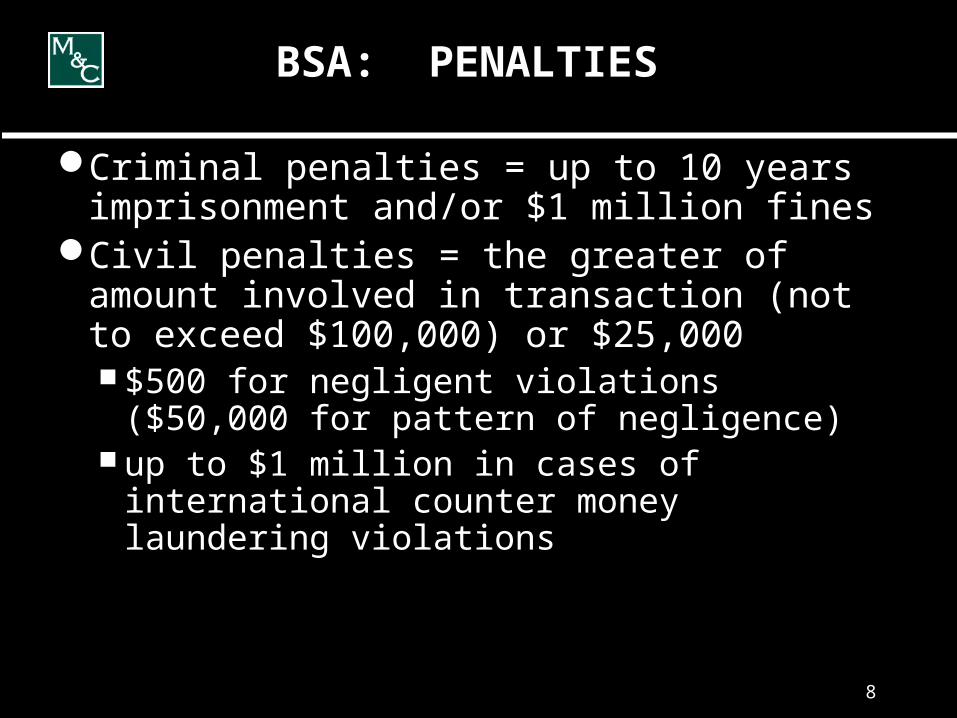

BSA: PENALTIES

Criminal penalties = up to 10 years imprisonment and/or $1 million fines

Civil penalties = the greater of amount involved in transaction (not to exceed $100,000) or $25,000 $500 for negligent violations ($50,000 for

pattern of negligence) up to $1 million in cases of international

counter money laundering violations

9

BSA: FINANCIAL INSTITUTIONS

Financial institutions (including PATRIOT Act additions)

an insured bank (as defined in the Federal Deposit Insurance Act)

a commercial bank or trust companya private bankeran agency or branch of a foreign bank in the U.S.any credit uniona thrift institutionan SEC-registered broker/dealera securities or commodities broker/dealer (including

introducing brokers)

10

BSA: FINANCIAL INSTITUTIONS(cont’d)

an investment banker or investment companya currency exchangean issuer, redeemer, or cashier of traveler’s checks,

checks, money orders, or similar instrumentsan operator of a credit card systeman insurance companya pawnbrokera loan or finance companya travel agencya licensed money-sender or others that engage in the

business of transferring money

11

BSA FINANCIAL INSTITUTIONS (cont’d)

a telegraph companya business engaged in vehicle salesa real estate brokera casinothe U.S. Postal Service and other U.S. government

agencies carrying out similar functionsany futures commission merchant, commodity trading

advisor, or commodity pool operator registered, or required to register under the Commodity Exchange Act (added by the PATRIOT Act)

12

BSA FINANCIAL INSTITUTIONS (cont’d)

a dealer in precious metals, stones, or jewels

others designated by regulation

13

RECENT U.S. ANTI-MONEY LAUNDERING DEVELOPMENTS: USA PATRIOT ACT

Passed on October 26, 2001

Expanded BSA requirements to many more financial institutions

Expanded predicate offenses to include violations of international regulatory regimes

14

PATRIOT ACT AMENDMENTSTO BSA

Prohibits and regulates certain types of accounts relationships with financial institutions

Expanded suspicious activity reporting requirements

Expanded requirements for anti-money laundering compliance programs

15

Anti-money laundering (“AML”) compliance program – 4 required elements:

Internal policies, procedures, and controls Designated compliance officer Ongoing training program for employees Independent audit function to test the program

PATRIOT ACT AMENDMENTSTO BSA (cont’d)

16

On February 21, 2003, Treasury issued a notice of proposed rulemaking, which would require dealers in precious metals, stones, or jewels to implement an AML compliance program

Sought public comment on rulesNo action by Treasury for past two yearsIn March 2005, FinCEN issued its 2004 Annual

Report; noted that it planned to finalize rules this year

PROPOSED AML COMPLIANCE PROGRAM FOR DEALERS

17

PROPOSED AML COMPLIANCE PROGRAM FOR DEALERS (cont’d)

Applies to “dealers”: person engaged in business of purchasing and selling jewels, precious metals, or precious stones who, during the prior year: Purchased more than $50,000 jewels, metals, or

stones; or Received more than $50,000 in gross proceeds

from transactions in jewels, metals, or stones

18

PROPOSED AML COMPLIANCE PROGRAM FOR DEALERS (cont’d)

Exceptions to definition of dealer: Retailer, i.e., a person engaged in sales to the

public other than a retailer who, during the prior year, purchases more than $50,000 in jewels, metals or stones from non dealers

Persons who engage in transactions for purposes of fabricating finished goods that contain minor amounts of jewels, metals, or stones

19

PROPOSED AML COMPLIANCE PROGRAM FOR DEALERS (cont’d)

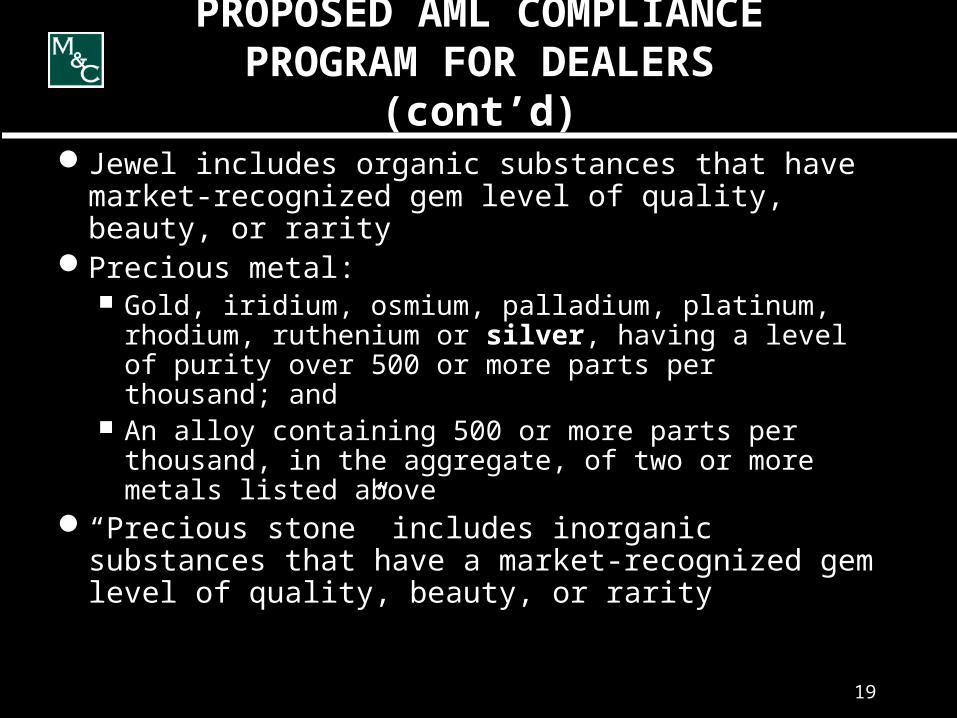

Jewel includes organic substances that have market-recognized gem level of quality, beauty, or rarity

Precious metal: Gold, iridium, osmium, palladium, platinum, rhodium,

ruthenium or silver, having a level of purity over 500 or more parts per thousand; and

An alloy containing 500 or more parts per thousand, in the aggregate, of two or more metals listed above

“Precious stone” includes inorganic substances that have a market-recognized gem level of quality, beauty, or rarity

20

PROPOSED AML COMPLIANCE PROGRAM FOR DEALERS (cont’d)

Program requirements: Approved by Senior Management and in writing Incorporate policies that address the entity’s risk Incorporate policies to identify transactions that

may involve use of the dealer to facilitate money laundering an terrorist financing

Reflect BSA requirements (noted that only reporting of cash transactions currently apply to dealers)

21

KEYS TO MONEYLAUNDERING PREVENTION

“Know-your-customer” (KYC) principles Customer and counterpart identification Customer and counterpart due diligence Screening against government lists (i.e., OFAC)

Transactional alertness Screen transactions for red flags

Payment restrictions Limit or prohibit cash transactions

22

KEYS TO MONEY LAUNDERING PREVENTION: RED FLAGS

Purchases or sales that are unusual for customer or supplier

Unusual payment methods, such as large cash transactions or payments from third parties

Attempts by customer or supplier to maintain high degree of secrecy

Purchases or sales that are not in conformity with standard industry practice

23

RED FLAGS (cont’d)

Counterpart is reluctant to provide adequate identification information when making a purchase

Counterpart provides inaccurate identification information

Transactions that appear to be structured to evade reporting requirements (e.g., a series of transactions under $10,000)

Counterpart presence in NCCT or country that is the subject of advisories issued by FinCEN

24

COMPLIANCE BASICS

Make the commitmentIdentify the risksDevelop compliance systems to manage risksImplement compliance processesDesignate compliance “gatekeepers”Train personnelMonitor compliance – people, paper, process

25

CONTACT INFORMATION

Michael L. Burton

James G. Tillen

Miller & Chevalier Chartered

202-626-5800 (main)

![C L GOLCHHA & ASSOCIATES [ CHARTERED ACCOUNTANTS ] Firm Profile Presentation CHARTERED ACCOUNTANTS C L GOLCHHA & ASSOCIATES](https://img.pdfslide.net/doc/110x75/5697c0301a28abf838cdac32/c-l-golchha-associates-chartered-accountants-firm-profile-presentation.jpg)