Embed Size (px)

Citation preview

M2M & Telematics

A market opportunity

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Lars Odlén MSc, MBA 20 years in product & process development 8 years of wireless M2M Led M2M developments in several industries Extensive international business experience

M2M SystemTelematics Consultancy

What happens in the wireless world ?What happens in the wireless world ?

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

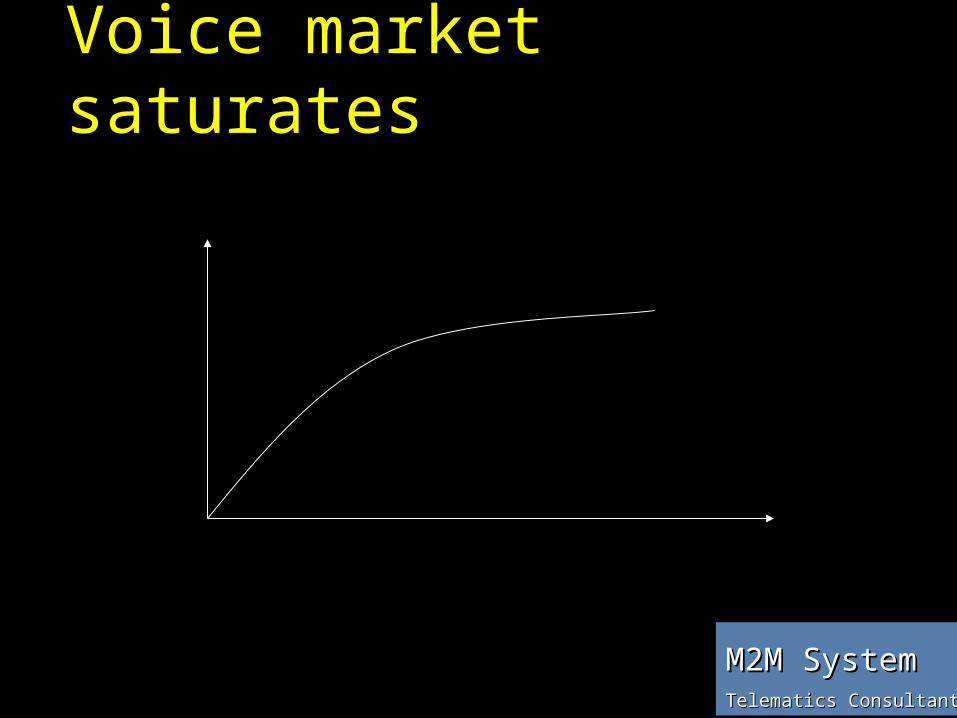

Voice market saturates

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

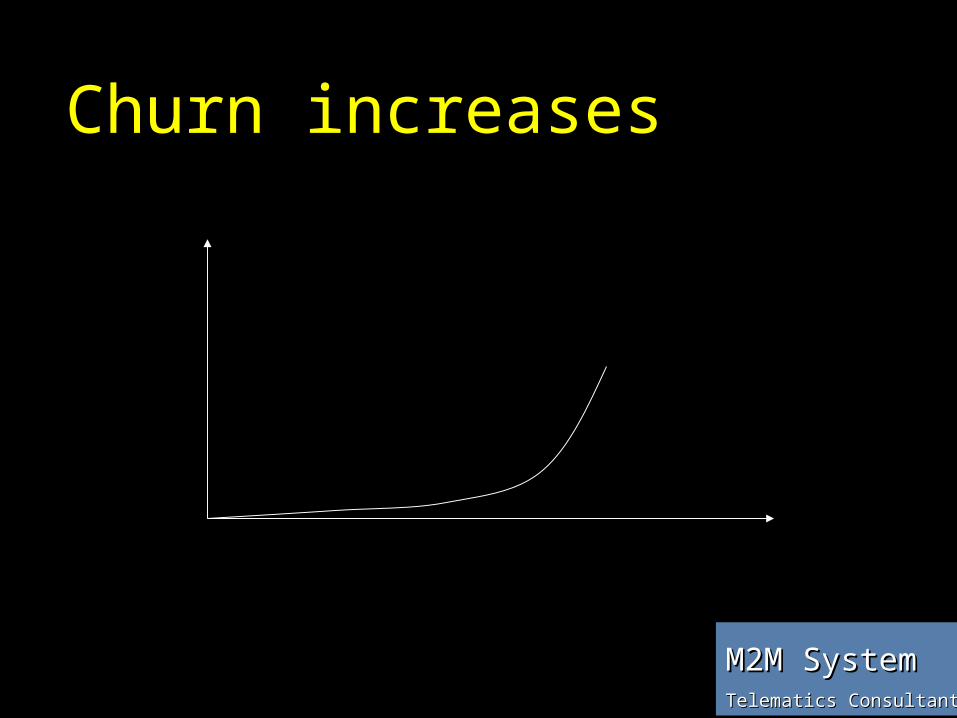

Churn increases

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

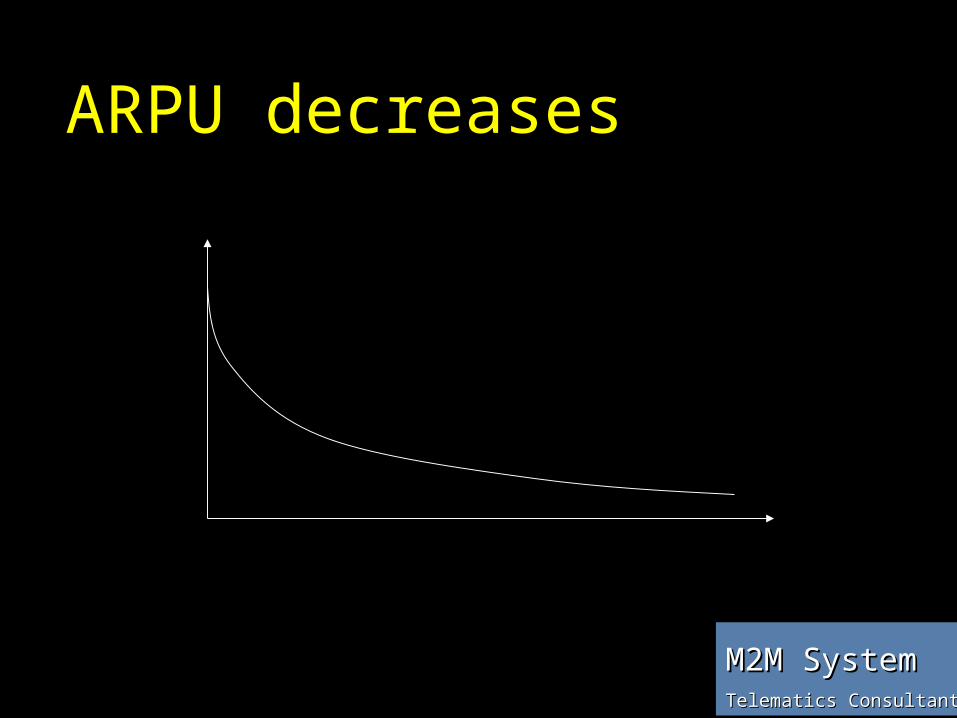

ARPU decreases

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

3G mobile-phone woes

The introduction of third-generation faces technical and financial difficulties.

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

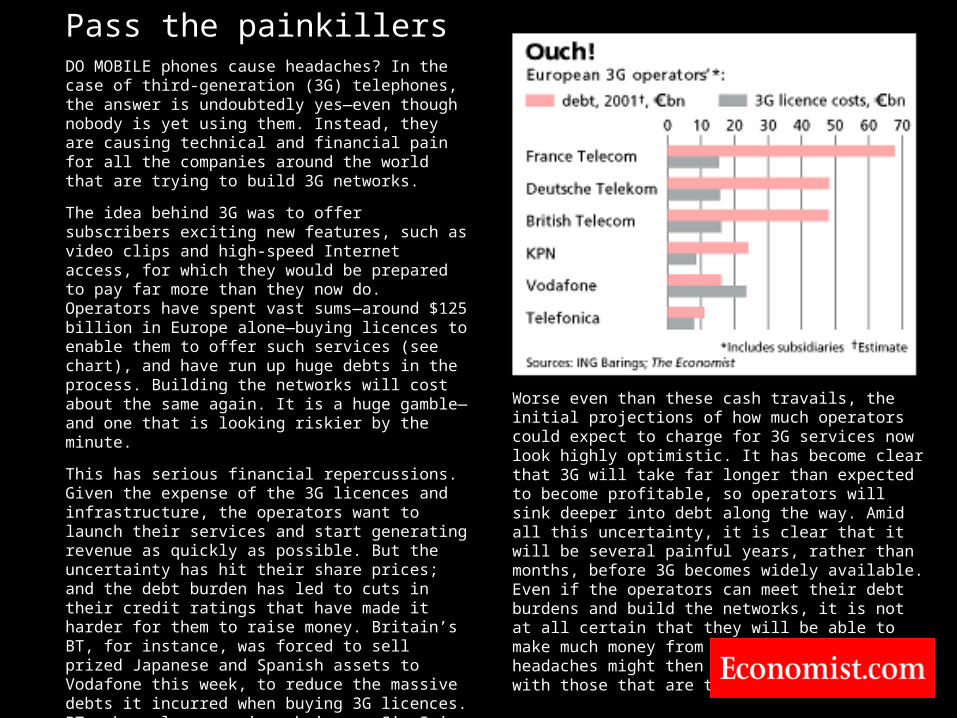

Pass the painkillersDO MOBILE phones cause headaches? In the case of third-generation (3G) telephones, the answer is undoubtedly yes—even though nobody is yet using them. Instead, they are causing technical and financial pain for all the companies around the world that are trying to build 3G networks.

The idea behind 3G was to offer subscribers exciting new features, such as video clips and high-speed Internet access, for which they would be prepared to pay far more than they now do. Operators have spent vast sums—around $125 billion in Europe alone—buying licences to enable them to offer such services (see chart), and have run up huge debts in the process. Building the networks will cost about the same again. It is a huge gamble—and one that is looking riskier by the minute.

This has serious financial repercussions. Given the expense of the 3G licences and infrastructure, the operators want to launch their services and start generating revenue as quickly as possible. But the uncertainty has hit their share prices; and the debt burden has led to cuts in their credit ratings that have made it harder for them to raise money. Britain’s BT, for instance, was forced to sell prized Japanese and Spanish assets to Vodafone this week, to reduce the massive debts it incurred when buying 3G licences. BT, whose long-serving chairman, Sir Iain Vallance, stood down last week, now plans a huge rights issue that may further upset its long-suffering shareholders.

Worse even than these cash travails, the initial projections of how much operators could expect to charge for 3G services now look highly optimistic. It has become clear that 3G will take far longer than expected to become profitable, so operators will sink deeper into debt along the way. Amid all this uncertainty, it is clear that it will be several painful years, rather than months, before 3G becomes widely available. Even if the operators can meet their debt burdens and build the networks, it is not at all certain that they will be able to make much money from them. Today’s headaches might then seem mild compared with those that are to come.

What the future might hold No market growth SOW (Share of wallet) not increasing All playes offer same Mobile communication becomes a comodity Mobile com just another utility Customers wants more for less Technology migration require heavy

investments ARPU likely to decrease

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

When the future looks uncertain, why not rely on the past

- You have a GSM network- You have spare capacity

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Additional revenues •Now•Without investment•Without cost

Without investments

Without investments

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Your future subscribers might not be persons, but machines

Telematics

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

By 2005 there will be more machines communicating than people

NTT DOCOMO President Keiji Tachikawa

For the UK market this equals +100 million £ per annum, at almost no marginal cost (1p/msg, 200 msg/yr)

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

There is a finite number of peopleThere is a finite number of people

butbut

An ever growing number of machinesAn ever growing number of machines

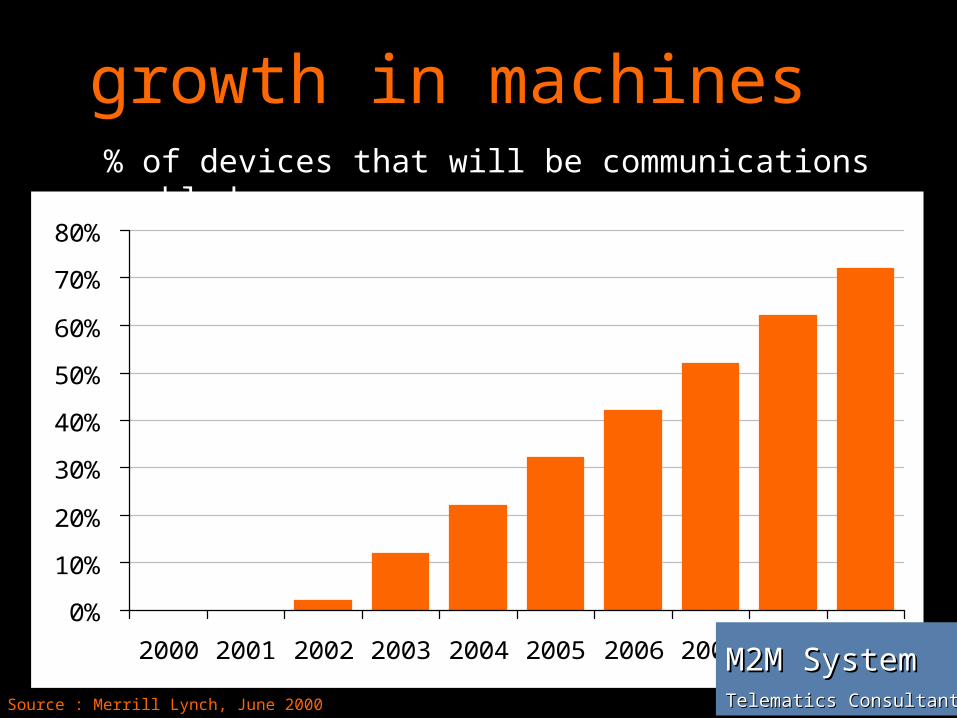

growth in machines% of devices that will be communications enabled

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source : Merrill Lynch, June 2000

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

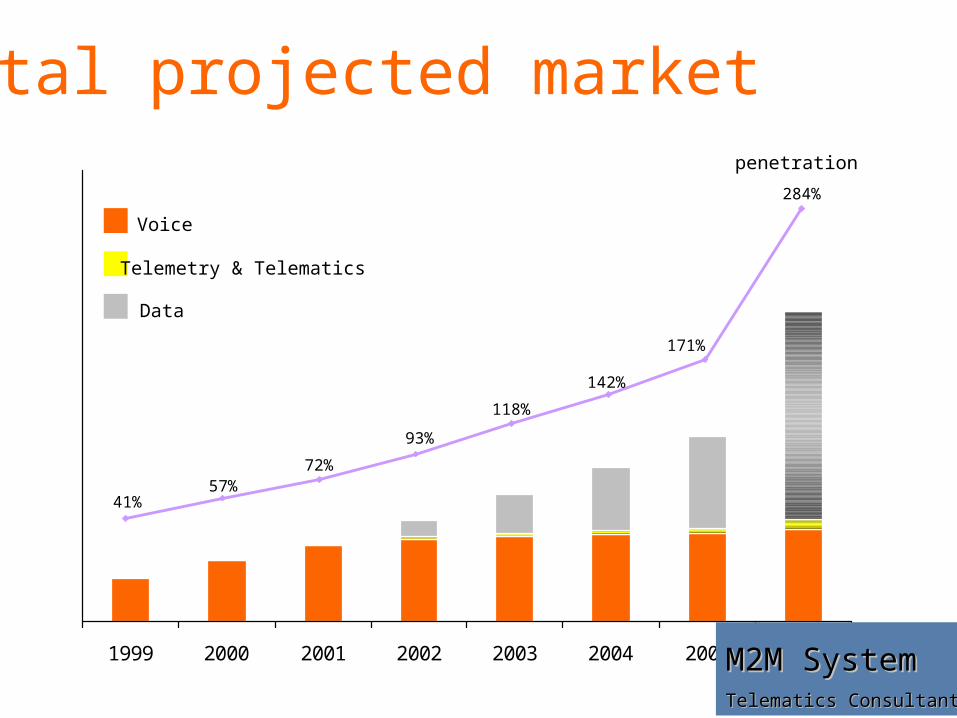

1999 2000 2001 2002 2003 2004 2005 2009

total projected market

Voice

Telemetry & Telematics

Data

penetration

41%57%

72%

93%

118%

142%

171%

284%

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

recognising the opportunity within the next ten years, telemetry in its

various guises will reach into all areas of industry i.e. food, retail, leisure engineering and transport

invasive as mobile voice currently is today

Eventually everything will be connected

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

a glimpse into the future

telecom will pervade all aspects of life

human to human

human to machine

machine to machine

machine to human

communication

interaction

transaction

control

building the connected worldM2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

What is Telematics The fourth phase of the IT revolution All devices communicate Geography becomes irrelevant Enables ”Business in real time” A Productivity driver Drives re-engineering and new business

models

A new tool for mankind

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

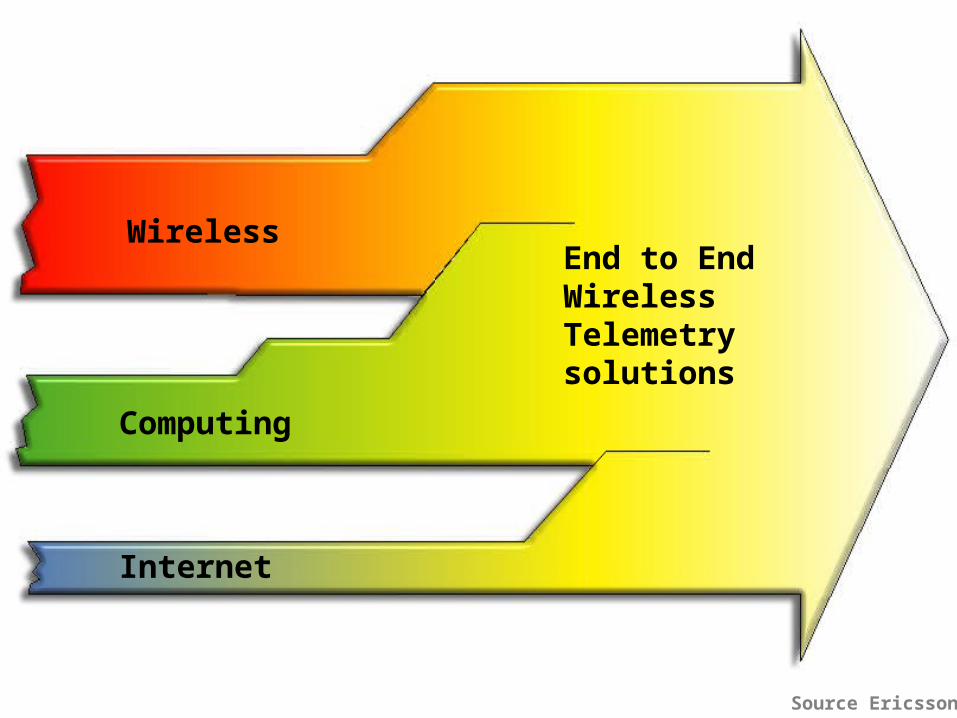

Computing

End to End Wireless Telemetry solutions

Internet

Wireless

Source Ericsson

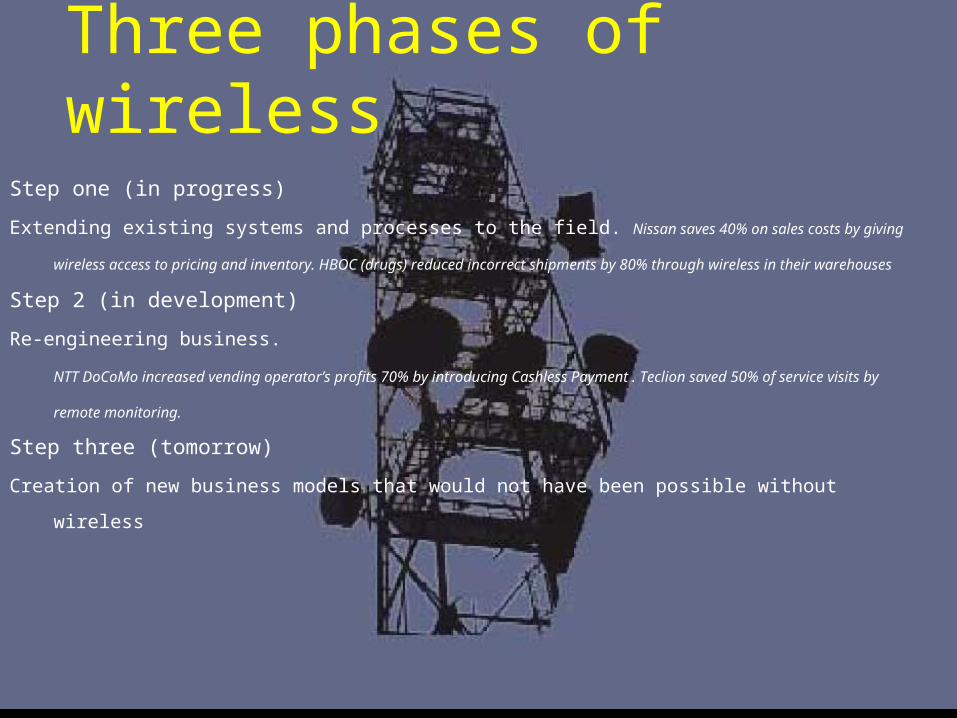

Three phases of wireless Step one (in progress)

Extending existing systems and processes to the field. Nissan saves 40% on sales costs by

giving wireless access to pricing and inventory. HBOC (drugs) reduced incorrect shipments by 80%

through wireless in their warehouses

Step 2 (in development)

Re-engineering business.

NTT DoCoMo increased vending operator’s profits 70% by introducing Cashless Payment . Teclion

saved 50% of service visits by remote monitoring.

Step three (tomorrow)

Creation of new business models that would not have been possible without wireless

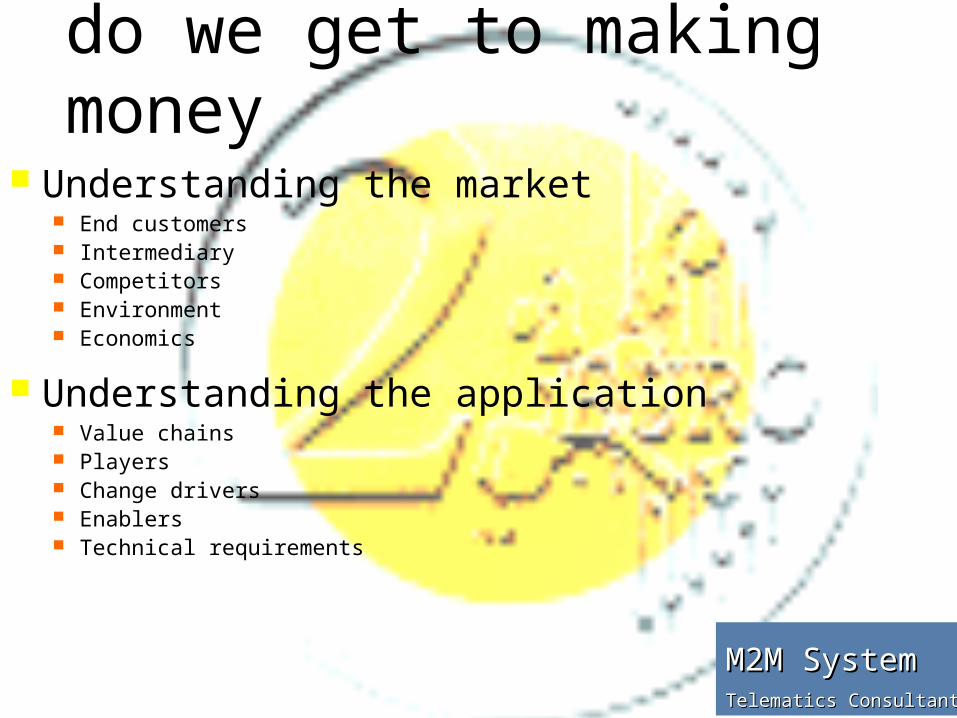

Understanding the market End customers Intermediary Competitors Environment Economics

Understanding the application Value chains Players Change drivers Enablers Technical requirements

Sounds great, but how do we get to making money

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

understanding who has to be involved

It's like a teamIt's like a team

the different players and the the different players and the interaction between them is referred to interaction between them is referred to as "the value chain"as "the value chain"

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

the value chain

supplier systems

integrator

service

supplier

network

operatorend user

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

the value chain it's very complex many interested parties a lack of standards specialists and ways of working are

specific to particular vertical markets however overall framework is similar in

all markets

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

What can an operator do?

Help others play !

Competitors

Vend

ing

Vend

ing

Secu

rity

Secu

rity

Au

tom

oti

ve

Au

tom

oti

ve

Au

tom

ati

on

Au

tom

ati

on

Uti

litie

sU

tilit

ies

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Opportunity

Vend

ing

Vend

ing

Secu

rity

Secu

rity

Au

tom

oti

ve

Au

tom

oti

ve

Au

tom

ati

on

Au

tom

ati

on

Uti

litie

sU

tilit

ies

Generic middleware platformGeneric middleware platform

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

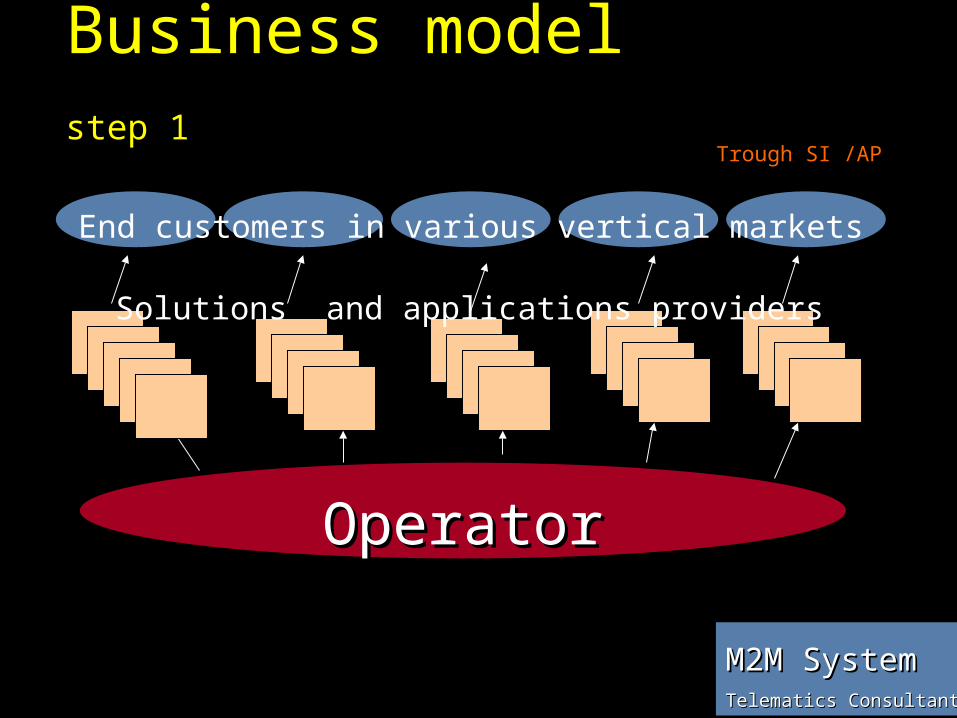

Business model step

1

End customers in various vertical markets

OperatorOperator

Solutions and applications providers

Trough SI /AP

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

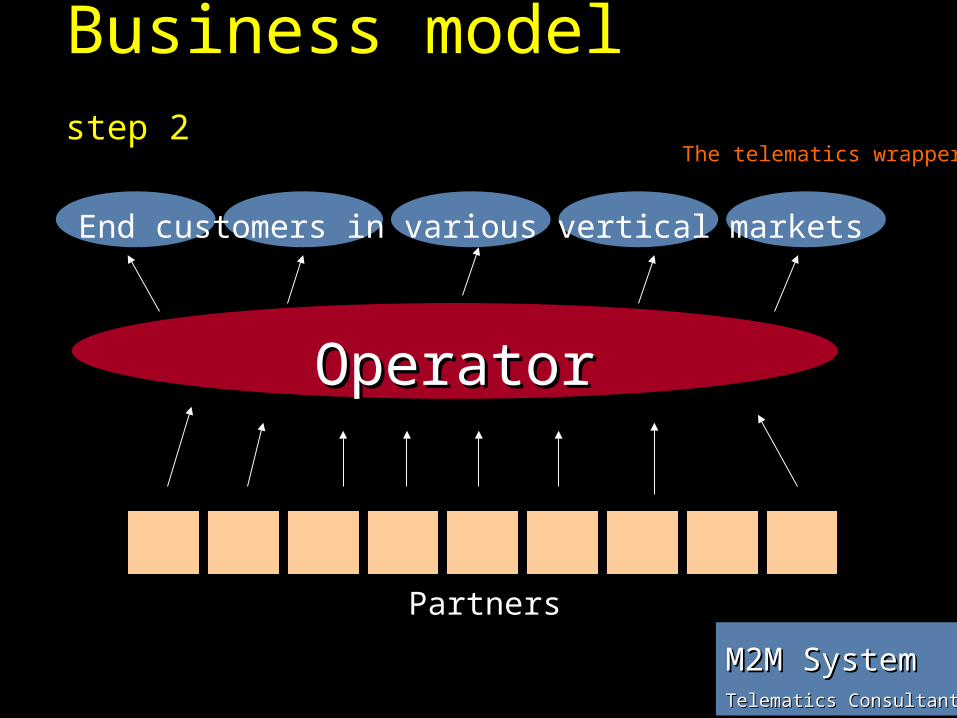

Business model step

2

End customers in various vertical markets

OperatorOperator

Partners

The telematics wrapper

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

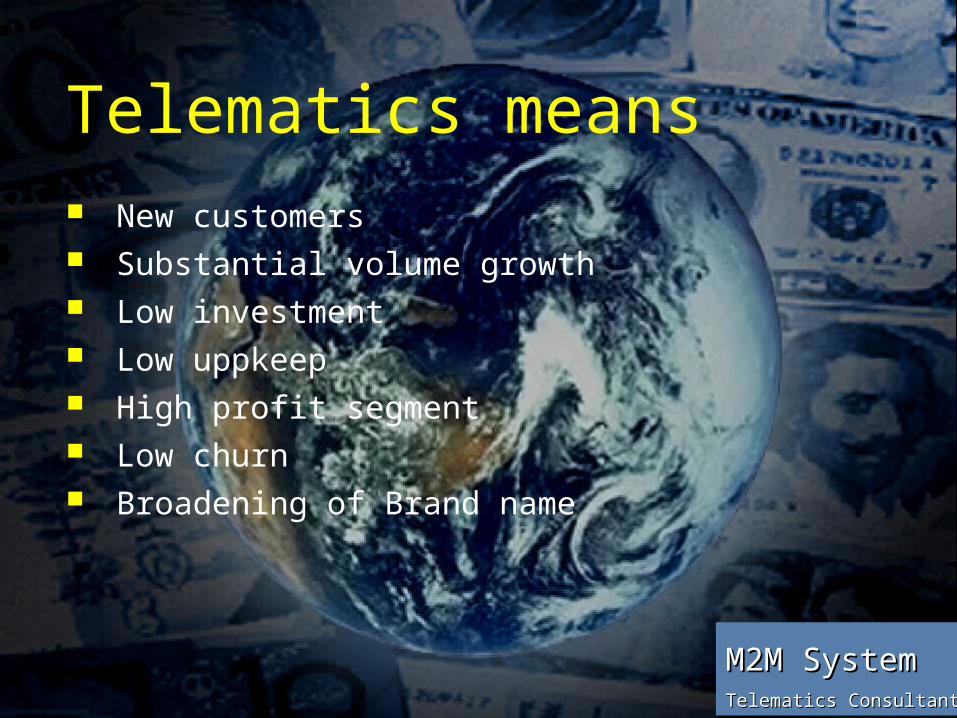

Telematics means New customers Substantial volume growth Low investment Low uppkeep High profit segment Low churn Broadening of Brand name

CASES

CasesCases

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Case Operator

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Developing a telemetry managed

solution

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

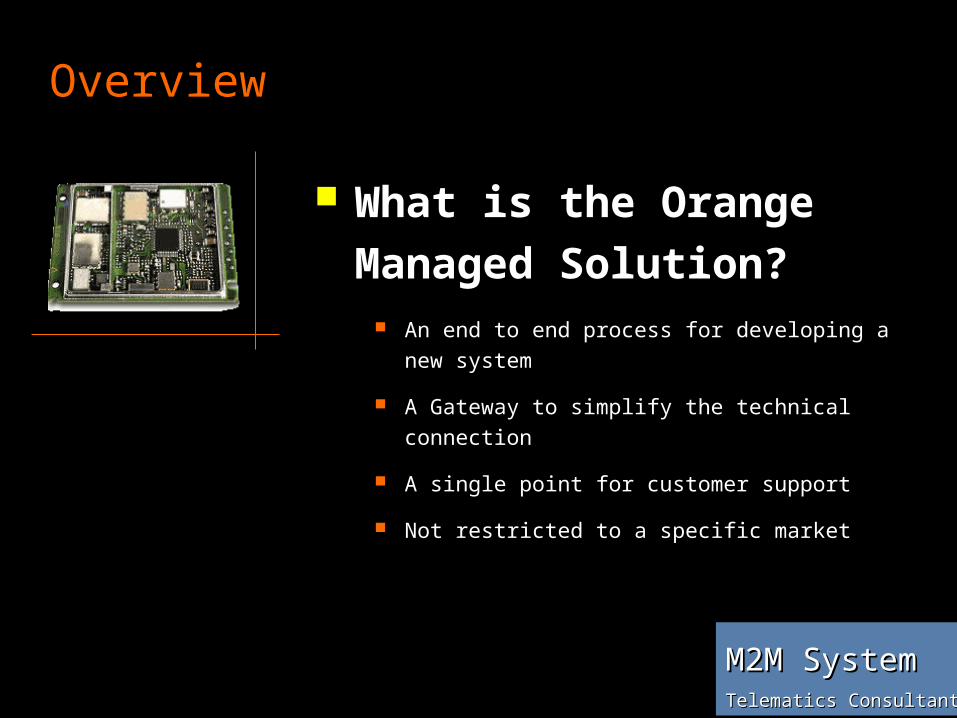

What is the Orange Managed Solution?

An end to end process for developing a new system

A Gateway to simplify the technical connection

A single point for customer support

Not restricted to a specific market

Overview

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

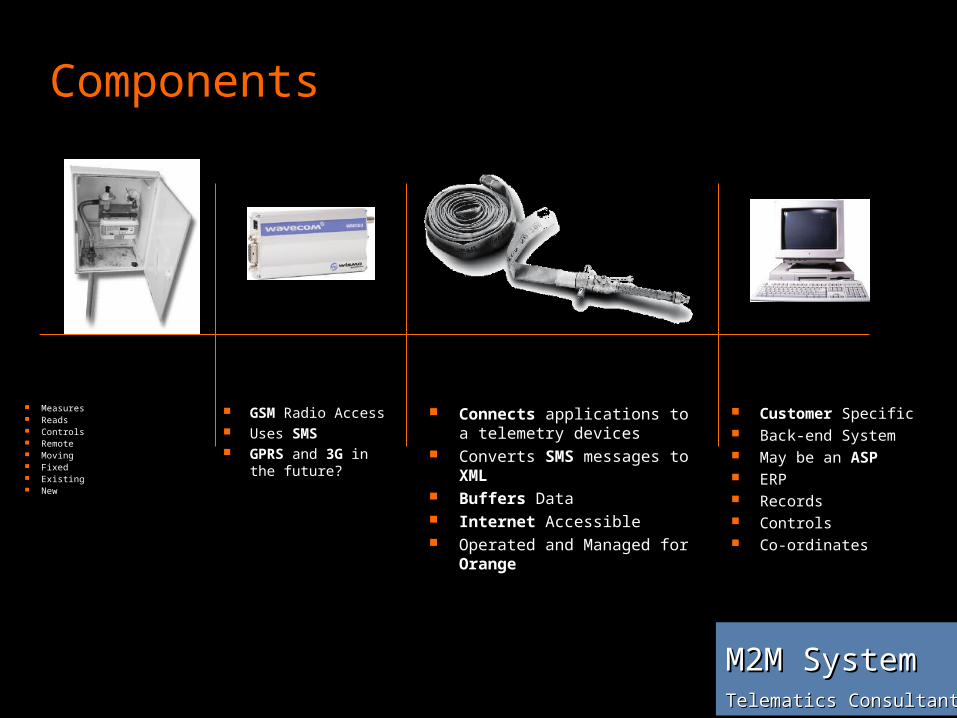

Components

Device Modem Managed GatewaySoftware Measures Reads Controls Remote Moving Fixed Existing New

GSM Radio Access Uses SMS GPRS and 3G in

the future?

Connects applications to a telemetry devices

Converts SMS messages to XML

Buffers Data Internet Accessible Operated and Managed for

Orange

Customer Specific Back-end System May be an ASP ERP Records Controls Co-ordinates

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

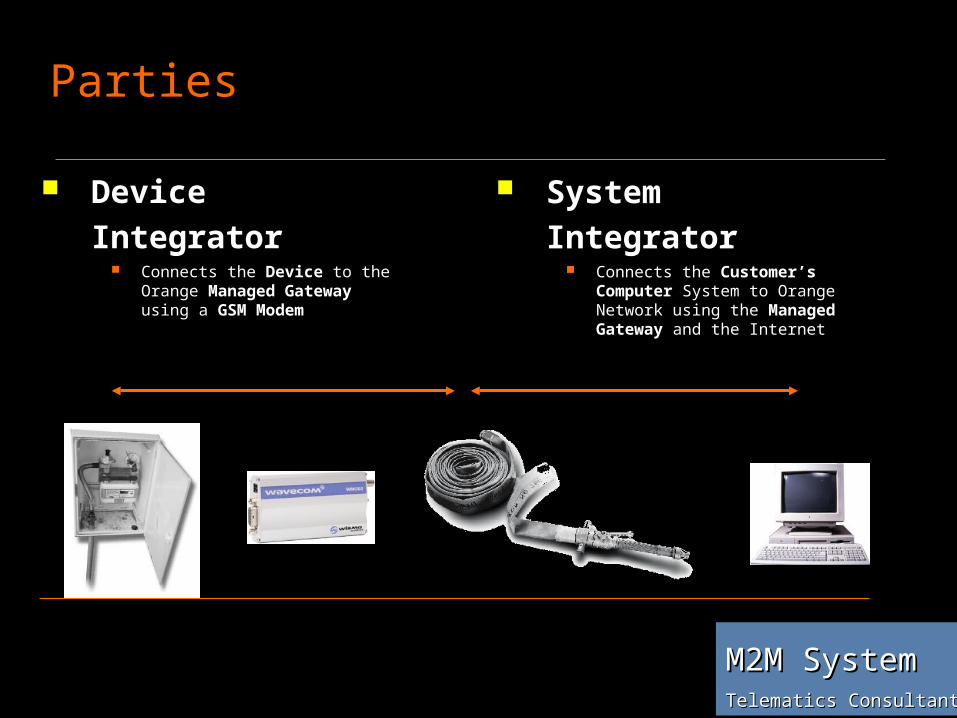

Parties

Device Integrator

Connects the Device to the Orange Managed Gateway using a GSM Modem

System Integrator

Connects the Customer’s Computer System to Orange Network using the Managed Gateway and the Internet

Device Modem Managed GatewaySoftwareM2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

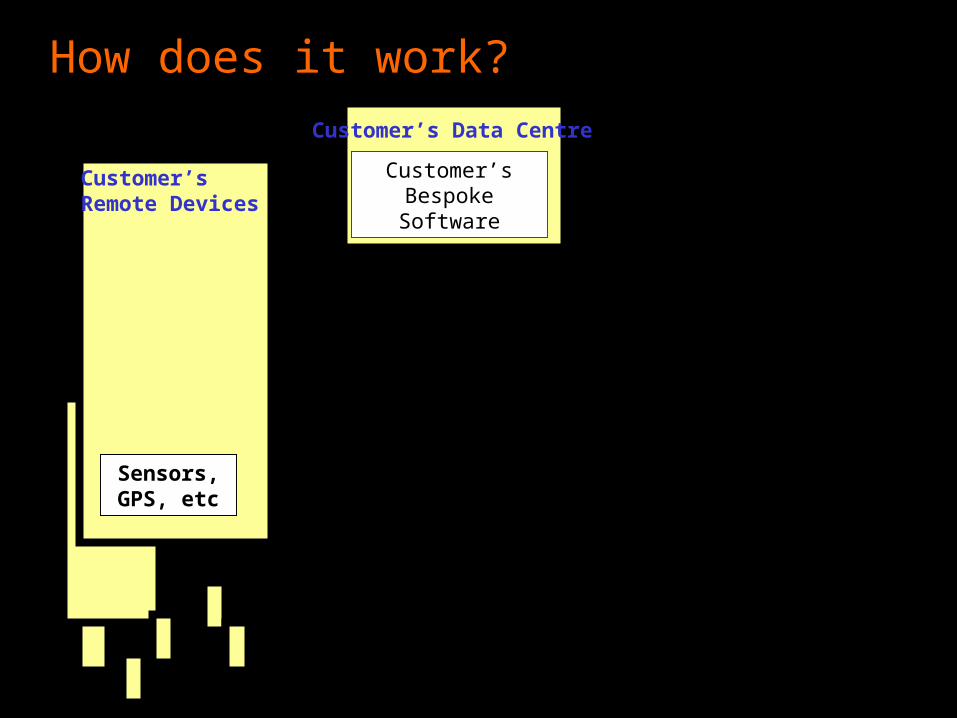

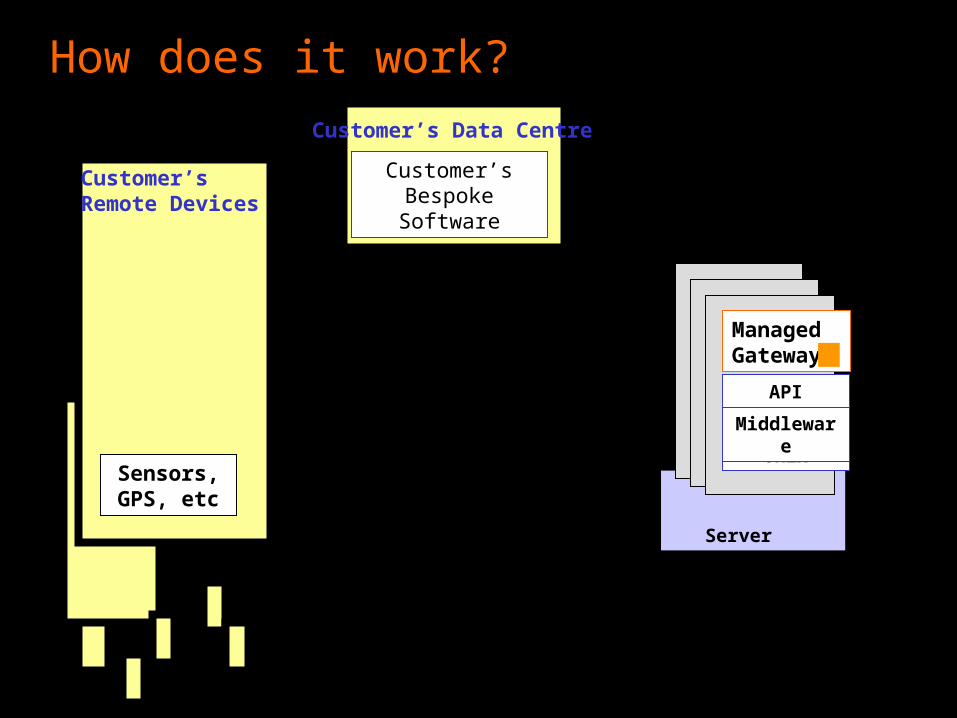

Customer’s Data Centre

Customer’sRemote Devices

Customer’sBespoke Software

Sensors, GPS, etc

How does it work?

OrangeManaged Gateway

Customer’s Data Centre

Customer’sRemote Devices

Customer’sBespoke Software

Customer Support

Managed Gateway

Unix

Middleware

API

Server Farm

Sensors, GPS, etc

How does it work?

Customer’s Data Centre

Customer’sRemote Devices

Customer’sBespoke Software

GSM Modem+ SIM

DeviceIntegration

System Integratio

n

Sensors, GPS, etc

How does it work?

OrangeManaged Gateway

Customer Support

Managed Gateway

Unix

Middleware

API

Server Farm

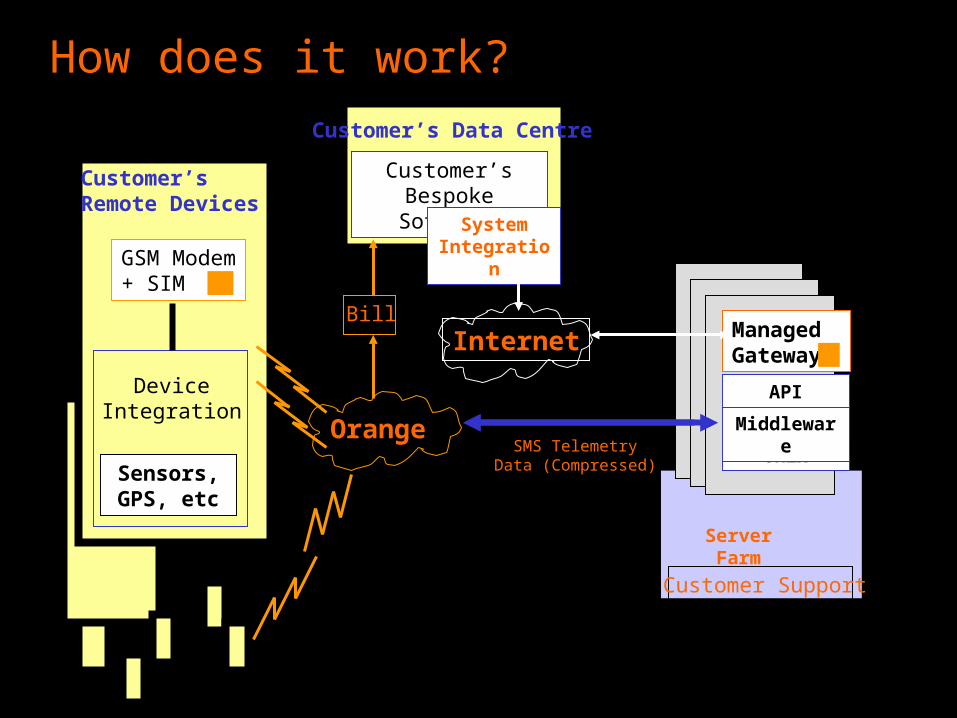

Internet

Orange

Customer’s Data Centre

Customer’sRemote Devices

Bill

Customer’sBespoke Software

GSM Modem+ SIM

DeviceIntegration

System Integratio

n

Sensors, GPS, etc

How does it work?

Orange Managed Gateway

Customer Support

Managed Gateway

Unix

Middleware

API

Server Farm

SMS TelemetryData (Compressed)

System Integration

Device Integration

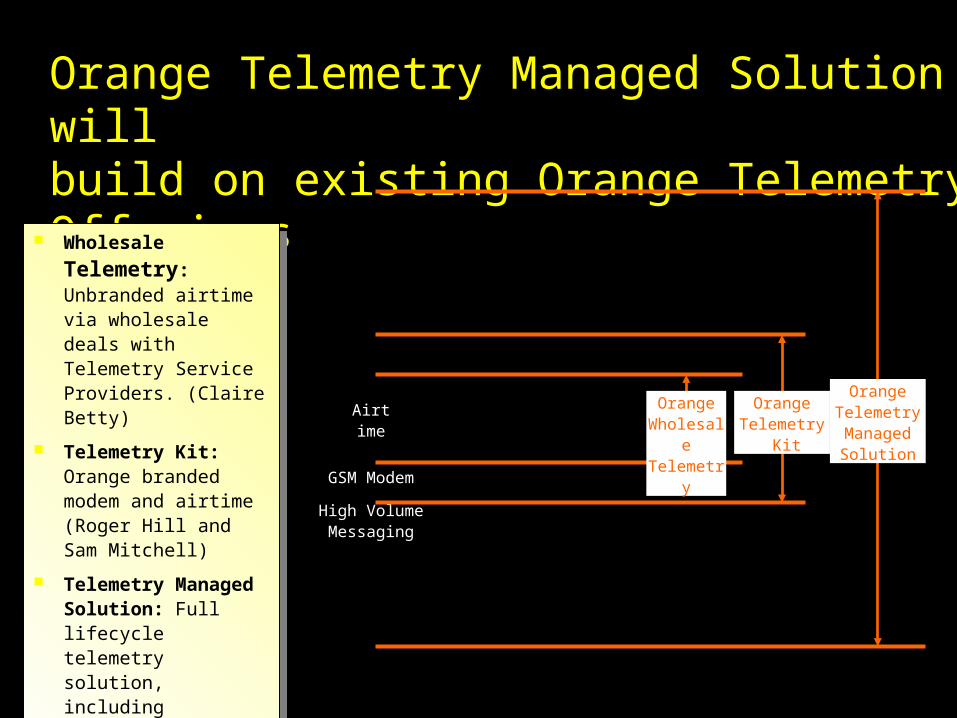

Orange Telemetry Managed Solution will build on existing Orange Telemetry Offerings

Airtime

GSM Modem

High VolumeMessaging

OrangeWholesal

eTelemetr

y

OrangeTelemetry

Kit

OrangeTelemetryManagedSolution

Wholesale

Telemetry: Unbranded airtime via wholesale deals with Telemetry Service Providers. (Claire Betty)

Telemetry Kit: Orange branded modem and airtime (Roger Hill and Sam Mitchell)

Telemetry Managed Solution: Full lifecycle telemetry solution, including monitoring, integration, and hardware.

Wholesale

Telemetry: Unbranded airtime via wholesale deals with Telemetry Service Providers. (Claire Betty)

Telemetry Kit: Orange branded modem and airtime (Roger Hill and Sam Mitchell)

Telemetry Managed Solution: Full lifecycle telemetry solution, including monitoring, integration, and hardware.

Reduced development time

Scalable, High performance messaging

Reduced message latency

No single point of failure

Removes complexities of modem hosting

Flexible, horizontal approach

Easy Migration path from SMS to GPRS

End to End monitoring and support

Base for ASP development

Advantages

Orange will be a ‘One Stop Shop’ for new telemetry products

Reduced product development time

Quicker customer connection

Not restricted to specific industries

Easy Migration path from SMS to GPRS

End to End monitoring and support

Built using ‘Off the Shelf’ technology

Designed for the b2b marketplace

Key Features

Case Lift service

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

What is the biggest saving in lift service?

Not to visit the lift !

Unmanned visits Need based service intervals Preventive maintenance

Reduces annual service visits by 50%

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

GSM based monitoring/alarm

system

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

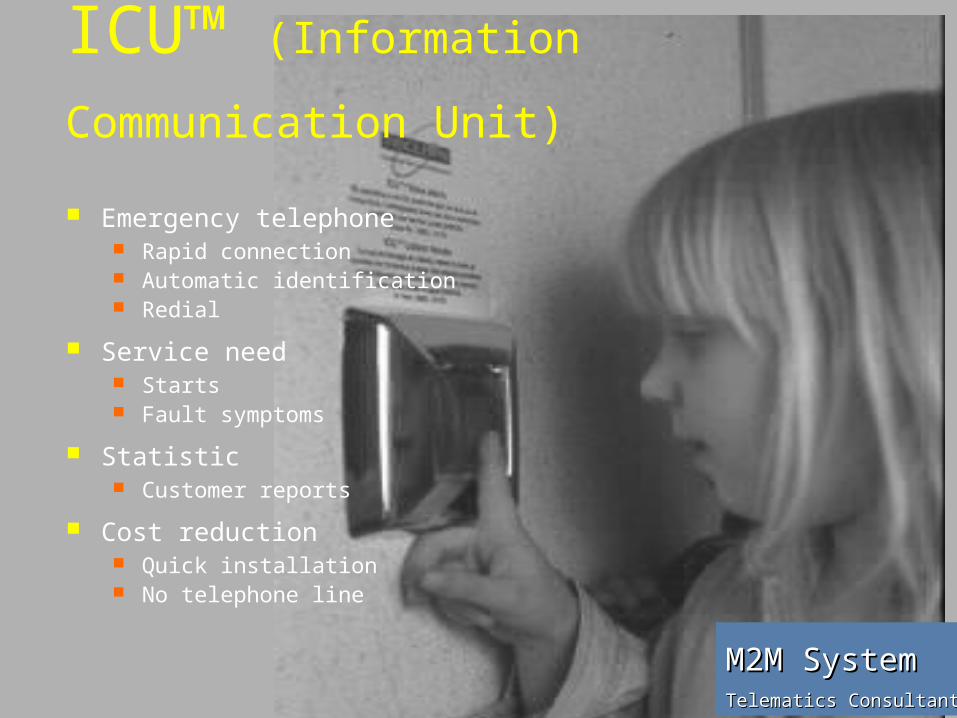

Emergency telephone Rapid connection Automatic identification Redial

Service need Starts Fault symptoms

Statistic Customer reports

Cost reduction Quick installation No telephone line

ICU™ (Information Communication

Unit)

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

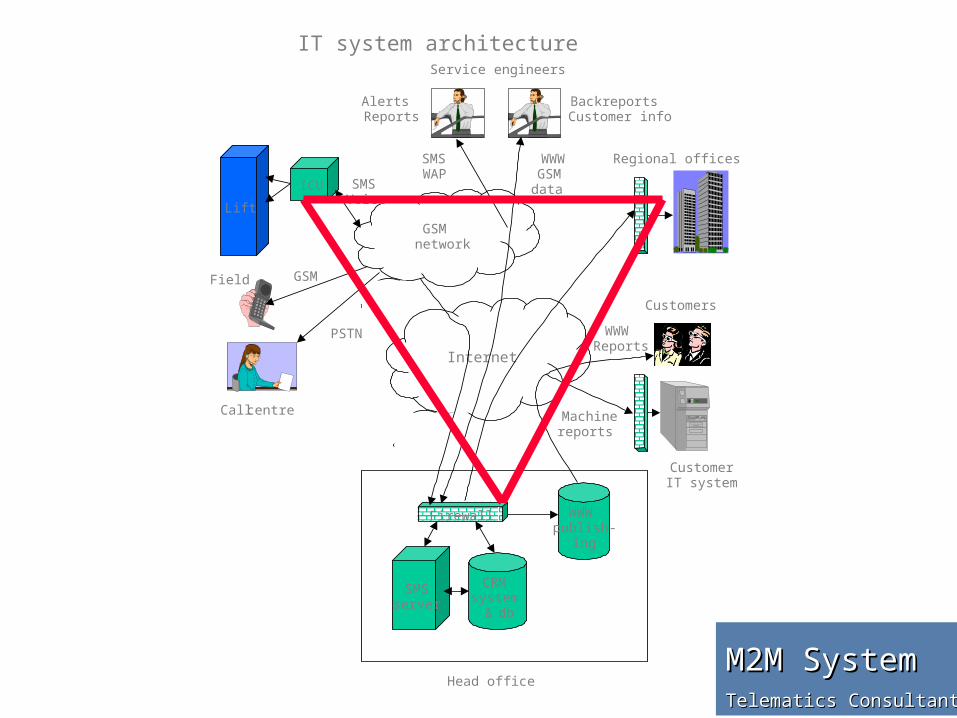

IT system architecture

Lift

ICU

GSMnetwork

Internet

CRM system

& db

WWW publish-

ing

Firewall

Call centre

PSTN

GSMField

Service engineers

Customers

WWWReports

WWWGSMdata

SMSWAP

AlertsReports

BackreportsCustomer info

Regional offices

Head office

SMSVoice

Machinereports

CustomerIT system

SMSserver

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

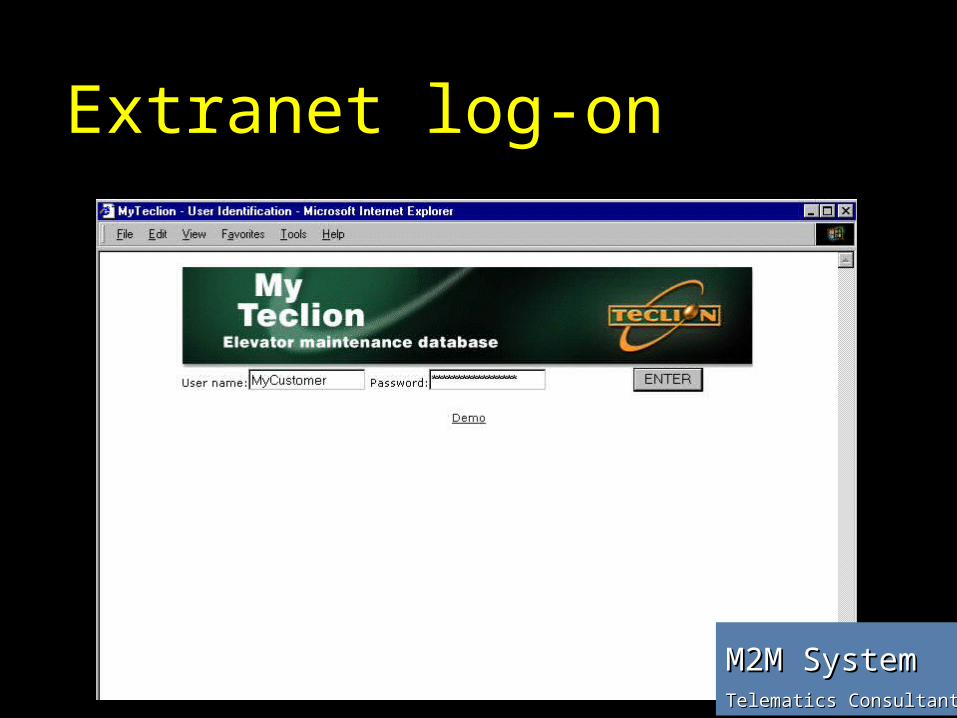

Extranet log-on

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

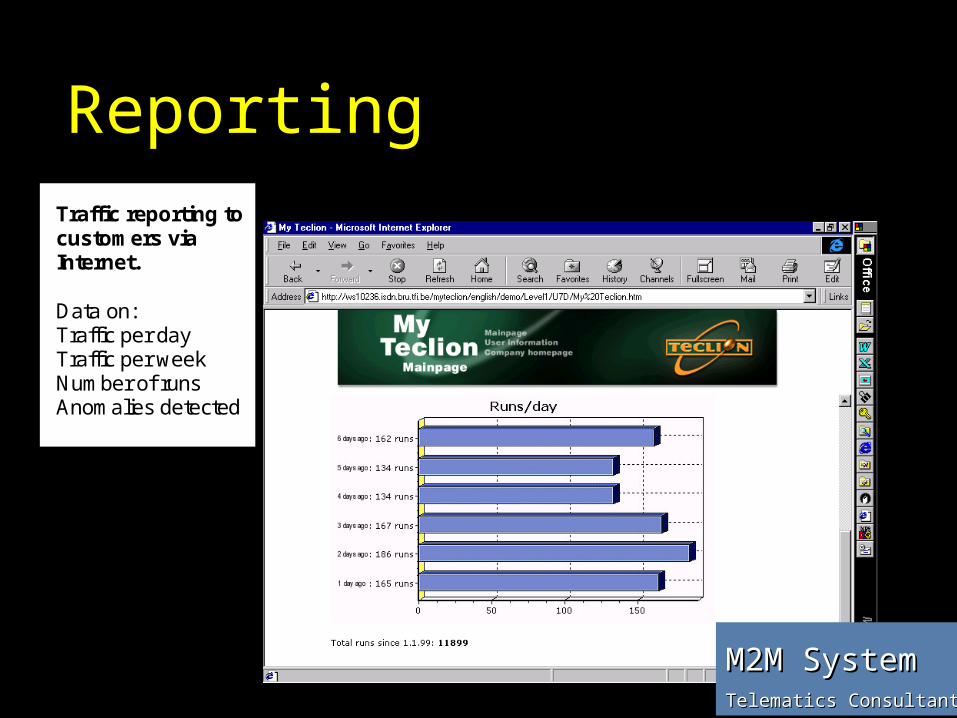

ReportingTraffic reporting tocustomers viaInternet.

Data on:Traffic per dayTraffic per weekNumber of runsAnomalies detected

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

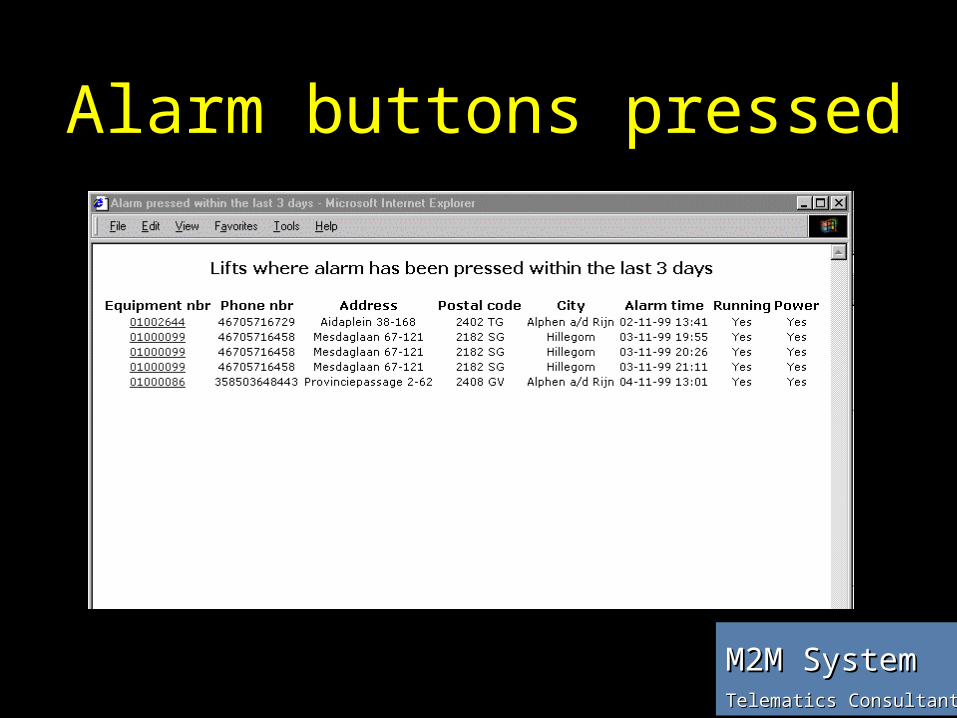

Alarm buttons pressed

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

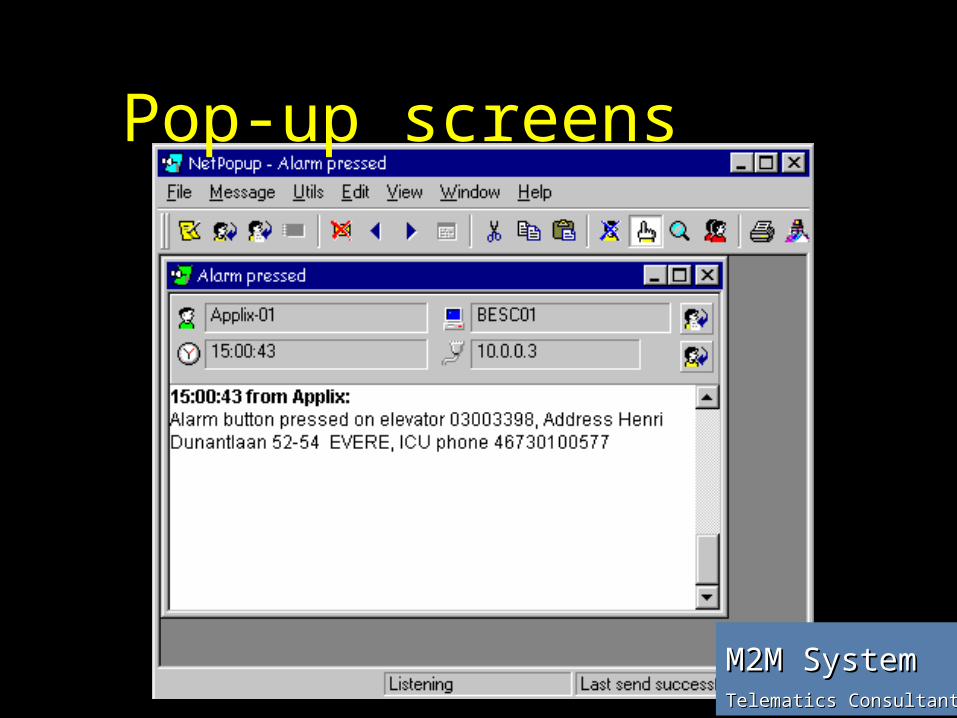

Pop-up screens

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

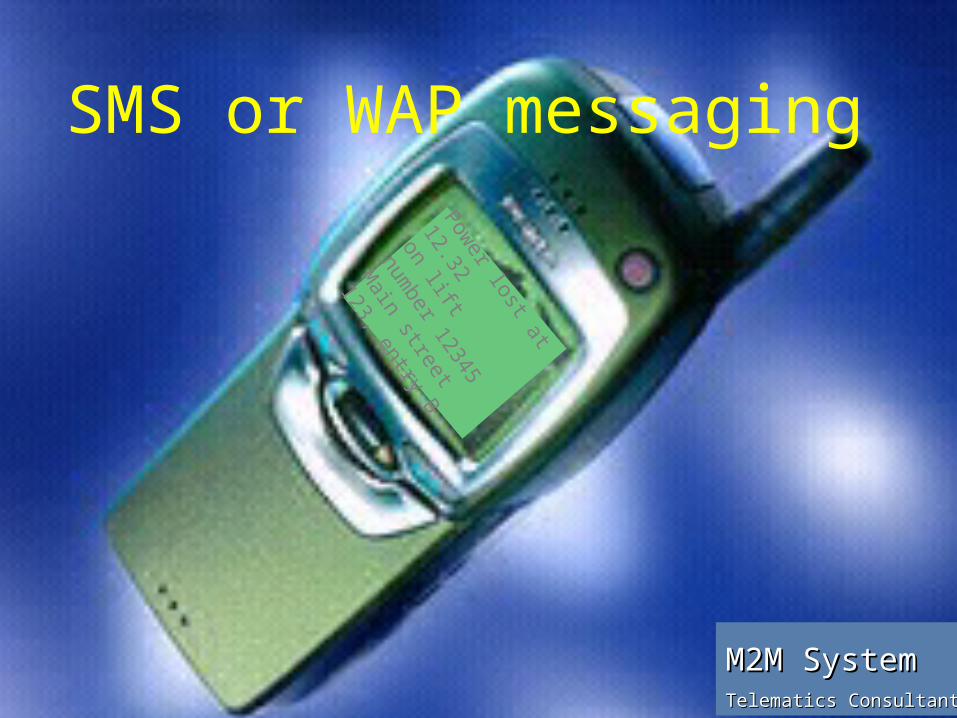

Power lost at

12.32

on lift number

12345

Main street 123,

entry B

SMS or WAP messaging

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

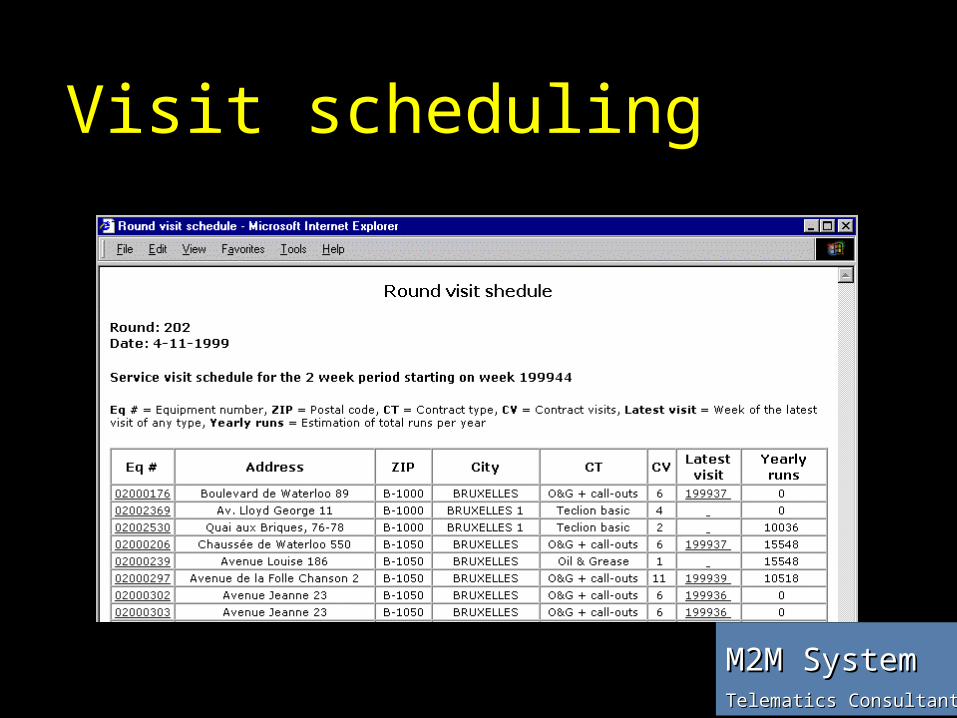

Visit scheduling

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Networking Virtually present Self managed Empowered Knowledgeable Access to information and support Quality built into the process Need based actions Producing results,

not time

Tomorrow is already here

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Service organisationCase lift service

Doubled productivity Reduced call outs to half Increased customer satisfaction Doubled profitability Less churning More motivated workforce

Result

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Case Gaming

Problem Cash shrinkage

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Case Gaming

Monitor cash box Desired effect: No cash shrinkage

Side effects Uptime Fetching profile Games preferred

Cash handling cost

Solution

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Transforming IT structuresCase Copiers

Countries are pretty independent The way they run service vary Their IT systems also vary We have left them alone as long as they

made profit But now the market gets tougher And we need one IT system for Europe

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Case copiers con’t The problem is that some countries are quite

advanced Sweden, for example, have an AS400 system

that they have been developing for ten years There is nothing on the market as good as

that So they would never accept a new system But we need to change...

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

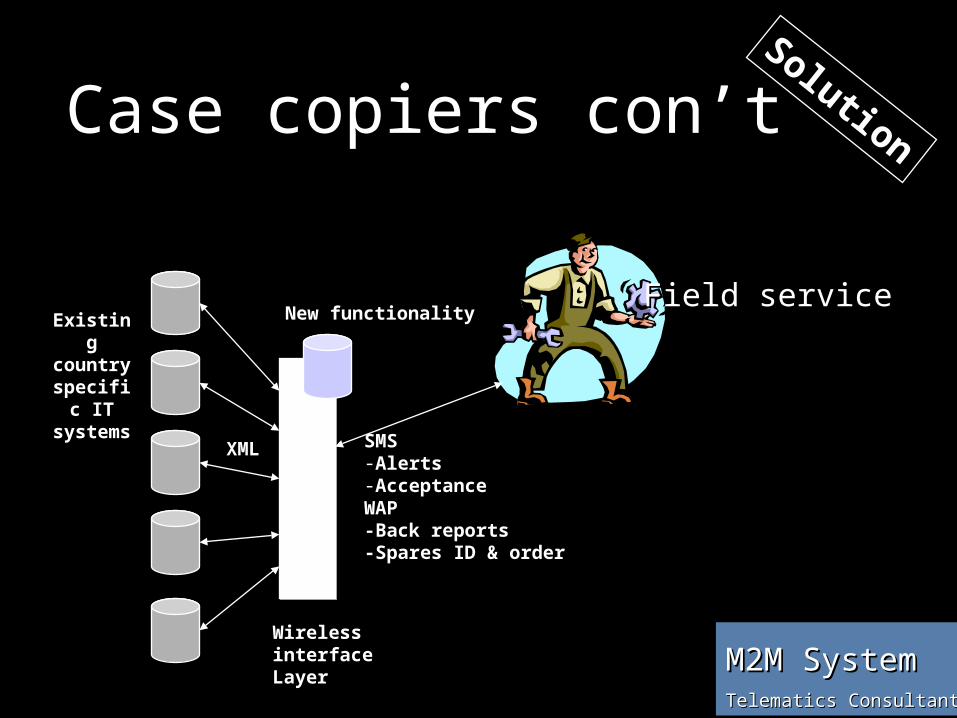

Case copiers con’tSolution

Existing country specific

IT systems

ASPASP

Wireless interface Layer

XML SMS -Alerts-AcceptanceWAP-Back reports-Spares ID & order

New functionalityField serviceField service

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

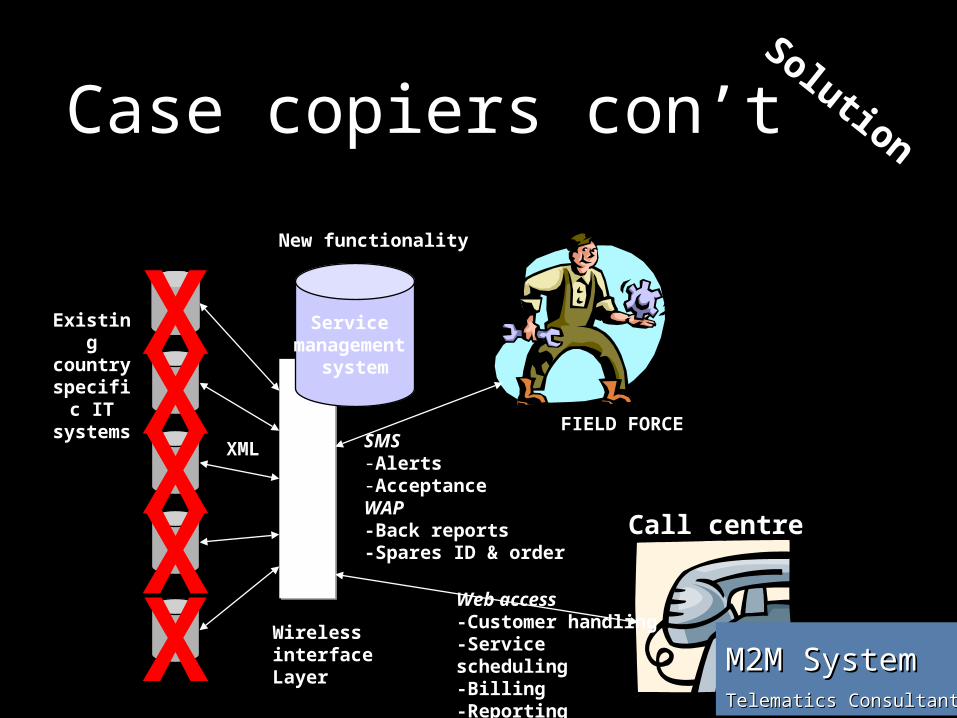

Case copiers con’tSolution

X

Existing country specific

IT systems

ASPASP

Wireless interface Layer

XML SMS -Alerts-AcceptanceWAP-Back reports-Spares ID & order

Service management

system

New functionality

XX

Call centre

Web access -Customer handling-Service scheduling-Billing-Reporting

XX FIELD FORCE

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

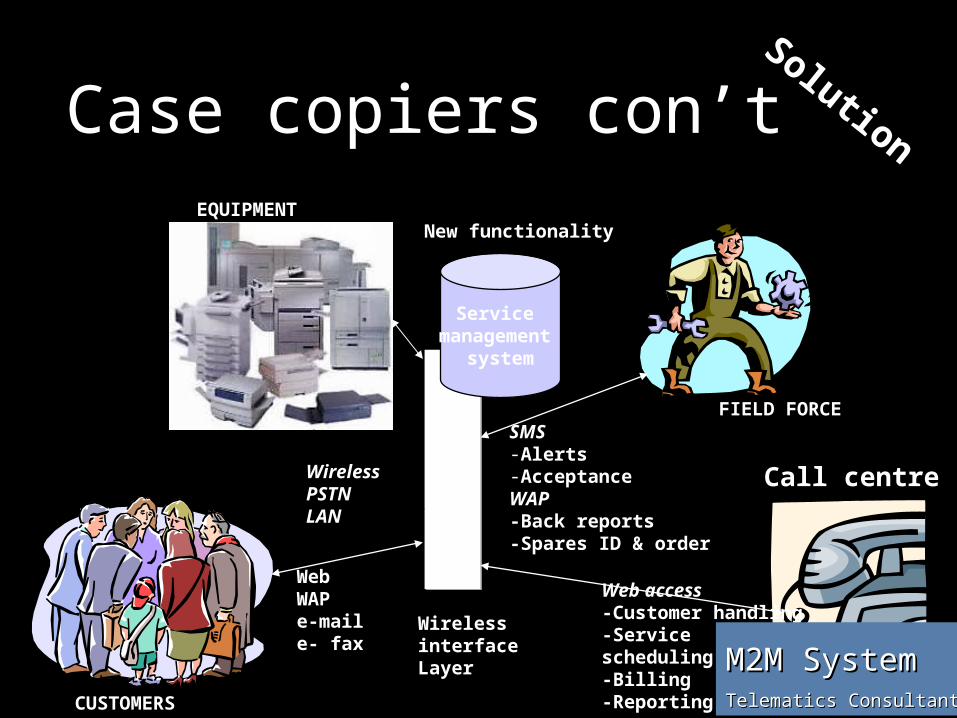

Case copiers con’tSolution

ASPASP

Wireless interface Layer

SMS -Alerts-AcceptanceWAP-Back reports-Spares ID & order

Service management

system

New functionality

Call centre

Web access -Customer handling-Service scheduling-Billing-Reporting

WirelessPSTNLAN

WebWAPe-maile- fax

CUSTOMERS

EQUIPMENT

FIELD FORCE

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

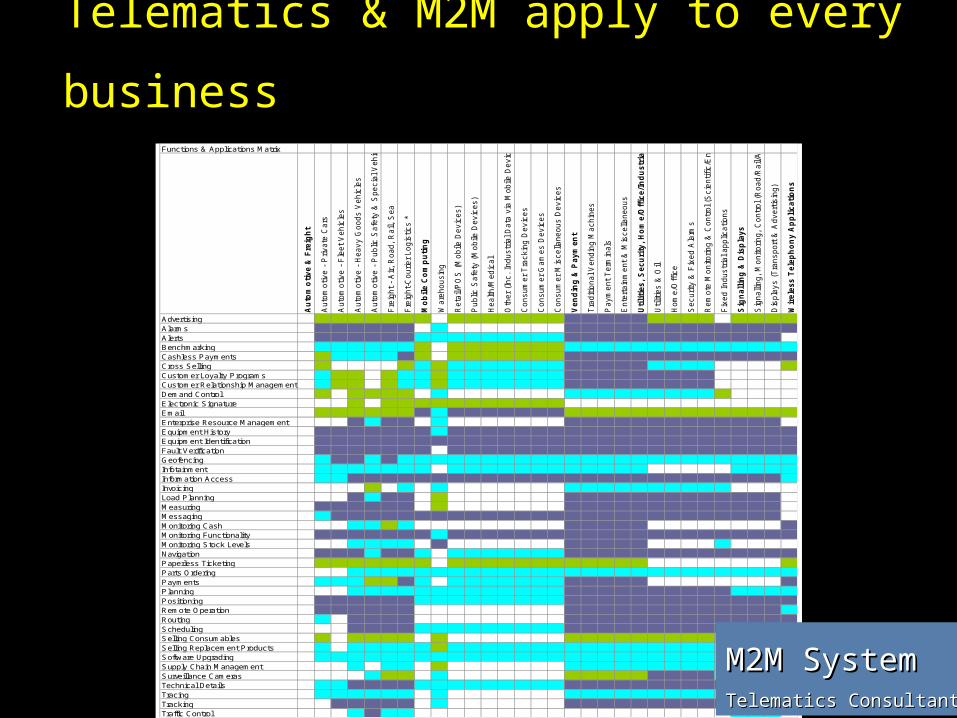

Telematics & M2M apply to every

businessFunctions & Applications Matrix

Au

tom

oti

ve &

Fre

igh

t

Au

tom

oti

ve

- P

riv

ate

Cars

Au

tom

oti

ve

- F

leet

Ve

hic

les

Au

tom

oti

ve

- H

ea

vy

Go

od

s V

eh

icle

s

Au

tom

oti

ve

- P

ub

lic S

afe

ty &

Sp

ec

ial

Veh

icle

s

Fre

ight

- A

ir,

Ro

ad

, R

ail,

Sea

Fre

ight-

Co

uri

er

Log

isti

cs

*

Mo

bil

e C

om

pu

tin

g

Wa

reho

usin

g

Re

tail/

PO

S (

Mo

bile

De

vic

es

)

Pu

blic

Sa

fety

(M

obile

De

vic

es

)

He

alt

h/M

ed

ica

l

Oth

er

(In

c.

Ind

ustr

ial

Data

via

Mo

bile

De

vic

es

)

Co

ns

um

er

Tra

ck

ing

Dev

ice

s

Co

ns

um

er

Gam

es

Dev

ice

s

Co

ns

um

er

Mis

cella

neo

us

De

vic

es

Ve

nd

ing

& P

ay

men

t

Tra

ditio

na

l V

en

din

g M

ac

hin

es

Pa

ym

en

t T

erm

inals

En

tert

ain

me

nt

& M

isc

ella

neo

us

Uti

liti

es

, S

ec

uri

ty,

Ho

me

/Off

ice

/In

du

str

ial

Uti

litie

s &

Oil

Ho

me

/Off

ice

Se

cu

rity

& F

ixed

Ala

rms

Re

mo

te M

on

ito

ring

& C

on

trol

(Scie

nti

fic

/En

vir

on

.)

Fix

ed I

nd

ustr

ial

app

licati

ons

Sig

nall

ing

& D

isp

lay

s

Sig

nalli

ng

, M

onit

ori

ng,

Co

ntr

ol (R

oad

/Rail/

Air/S

ea)

Dis

pla

ys (

Tra

ns

po

rt &

Ad

vert

isin

g)

Wir

ele

ss

Tele

ph

on

y A

pp

lic

ati

on

s

AdvertisingAlarmsAlertsBenchmarkingCashless PaymentsCross SellingCustomer Loyalty ProgramsCustomer Relationship ManagementDemand ControlElectronic SignatureEmailEnterprise Resource ManagementEquipment HistoryEquipment IdentificationFault VerificationGeofencingInfotainmentInformation AccessInvoicingLoad PlanningMeasuringMessagingMonitoring CashMonitoring FunctionalityMonitoring Stock LevelsNavigationPaperless TicketingParts OrderingPaymentsPlanningPositioningRemote OperationRoutingSchedulingSelling ConsumablesSelling Replacement ProductsSoftware UpgradingSupply Chain ManagementSurveillance CamerasTechnical DetailsTracingTrackingTraffic Control

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

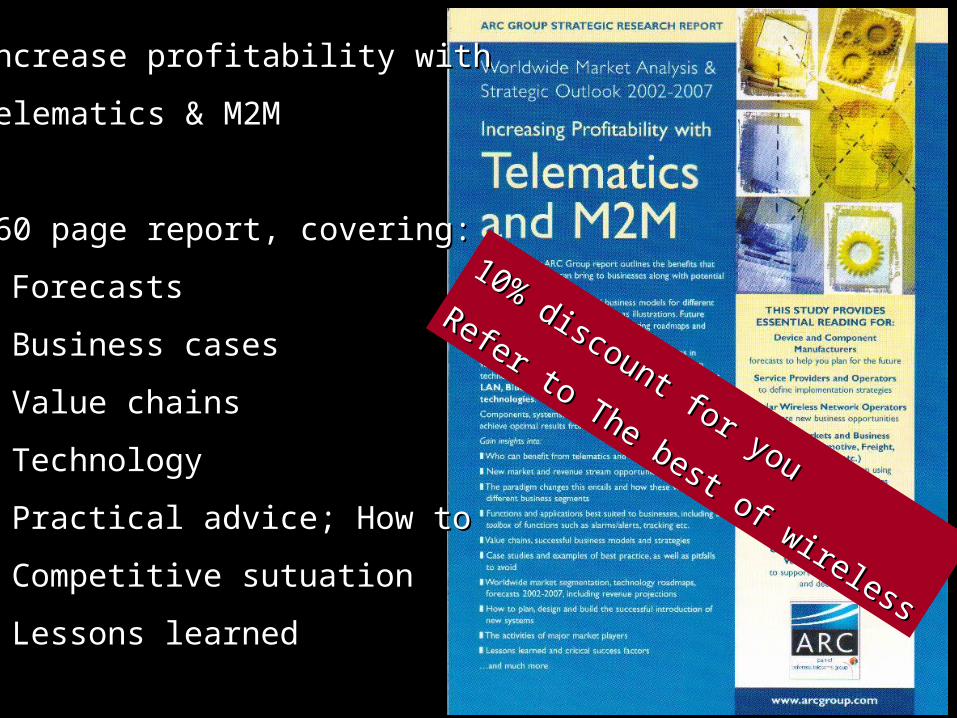

Increase profitability with Increase profitability with

Telematics & M2MTelematics & M2M

260 page report, covering:260 page report, covering:

ForecastsForecasts

Business casesBusiness cases

Value chainsValue chains

TechnologyTechnology

Practical advice; How toPractical advice; How to

Competitive sutuationCompetitive sutuation

Lessons learnedLessons learned

10% discount for you

10% discount for you

Refer to The best of wireless

Refer to The best of wireless

questions

M2M SystemM2M SystemTelematics ConsultantsTelematics Consultants

Thank you for listening

M2M SystemM2M SystemAdvisors to Industry LeadersAdvisors to Industry Leaders