Embed Size (px)

Citation preview

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

Hong Kong Telecoms Summit

M&A OPPORTUNITIES FOR TELCOS

TAYLOR LAM

JULY 2016

Strategy Consulting

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

CONTENTS A SLOWDOWN FROM RECENT FRENZIES: OPPORTUNITIES FOR TELCOS?

TELCO M&A HOTSPOTS: ENTERPRISE ICT AND CONSUMER DIGITAL

CONSIDERATIONS FOR M&A IN NEW FRONTIERS

KEY TAKEAWAYS

2

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

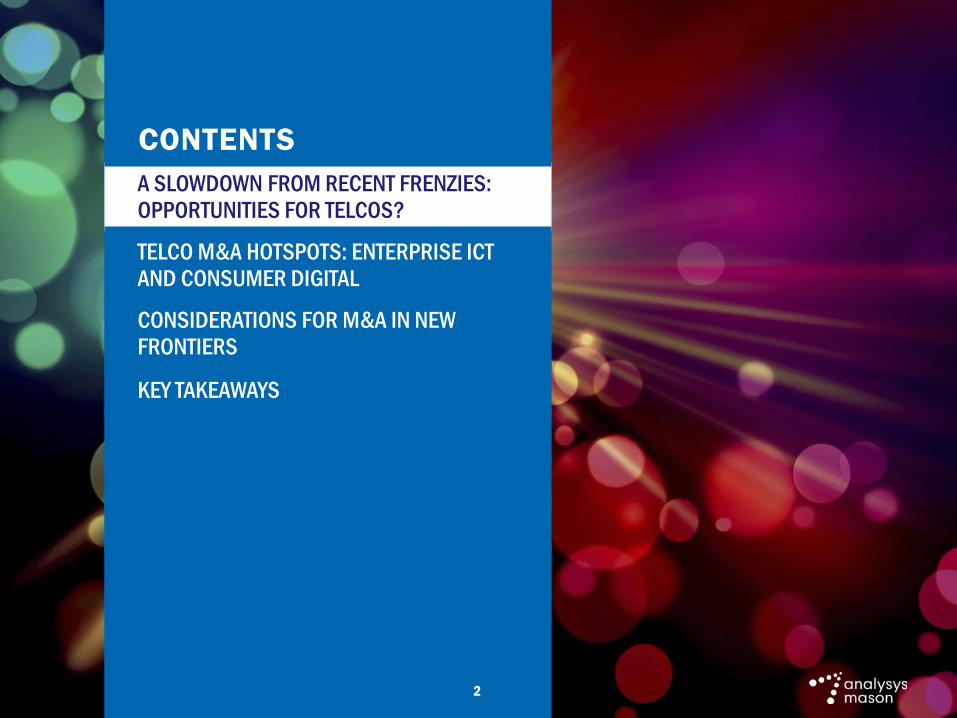

M&A activities in the TMT sector have slowed in 2016 – is it time for strategic investors to step in?

185 176 153

254 223 260

153

45

60

34

4473

7677

8594

81

100 161137

224

423

20

172172

500

600

800

300

0

100

200

700

400

14

51

Q1 2016

Tota

l val

ue o

f dea

ls (U

SD b

illio

n)

511 525

768

307

2008

286

2007

501

85

222

315 333

2014 2015

123

2009

81

2010 2013

102

2011 2012

Asia-Pac

Media Telecoms

Technology

Global value of disclosed deals in the TMT industry

Source: MergerMarket

3

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

CONTENTS A SLOWDOWN FROM RECENT FRENZIES: OPPORTUNITIES FOR TELCOS?

TELCO M&A HOTSPOTS: ENTERPRISE ICT AND CONSUMER DIGITAL

CONSIDERATIONS FOR M&A IN NEW FRONTIERS

KEY TAKEAWAYS

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

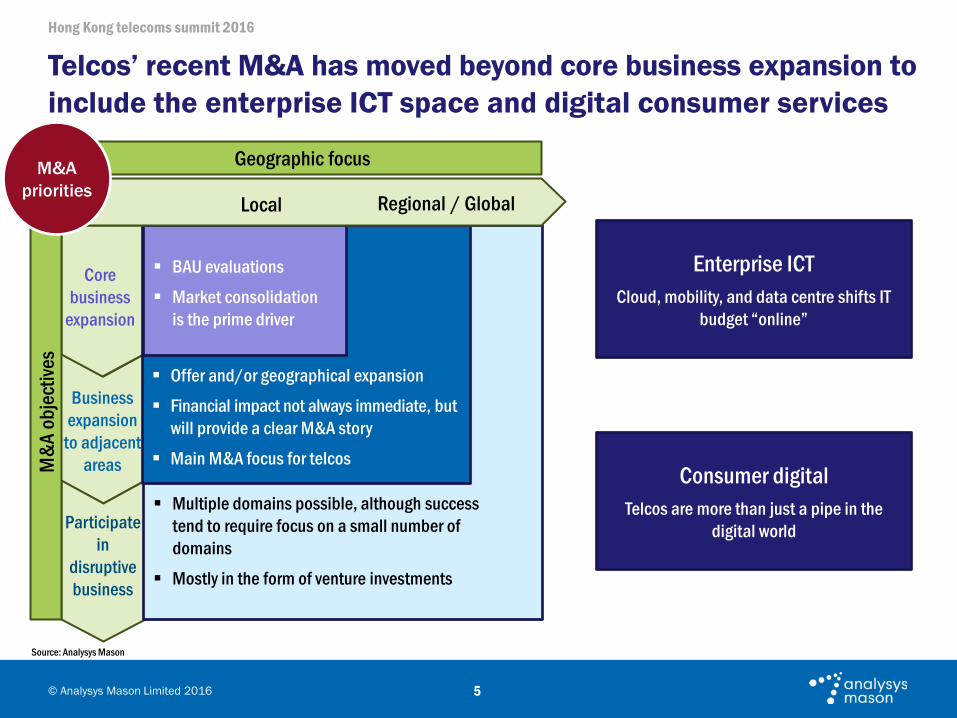

Telcos’ recent M&A has moved beyond core business expansion to include the enterprise ICT space and digital consumer services

5

M&A

obj

ectiv

es

Core business

expansion

Business expansion

to adjacent areas

Participate in

disruptive business

Geographic focus M&A priorities

Local Regional / Global

Offer and/or geographical expansion

Financial impact not always immediate, but will provide a clear M&A story

Main M&A focus for telcos

Multiple domains possible, although success tend to require focus on a small number of domains

Mostly in the form of venture investments

BAU evaluations

Market consolidation is the prime driver

Enterprise ICT Cloud, mobility, and data centre shifts IT

budget “online”

Consumer digital Telcos are more than just a pipe in the

digital world

Source: Analysys Mason

5

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

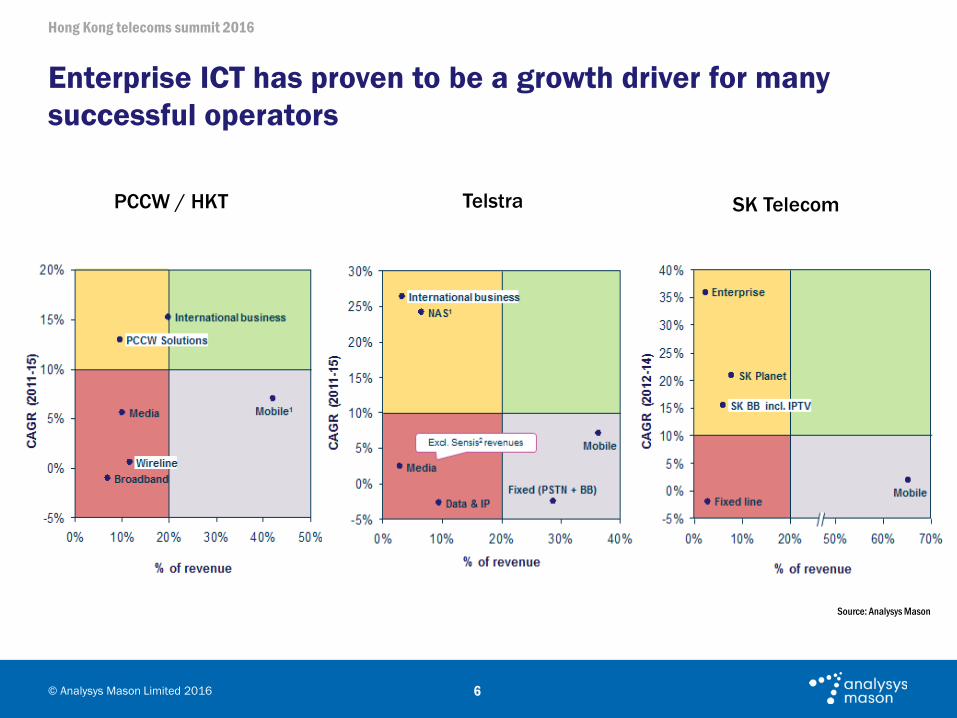

Enterprise ICT has proven to be a growth driver for many successful operators

PCCW / HKT Telstra SK Telecom

Source: Analysys Mason

6

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

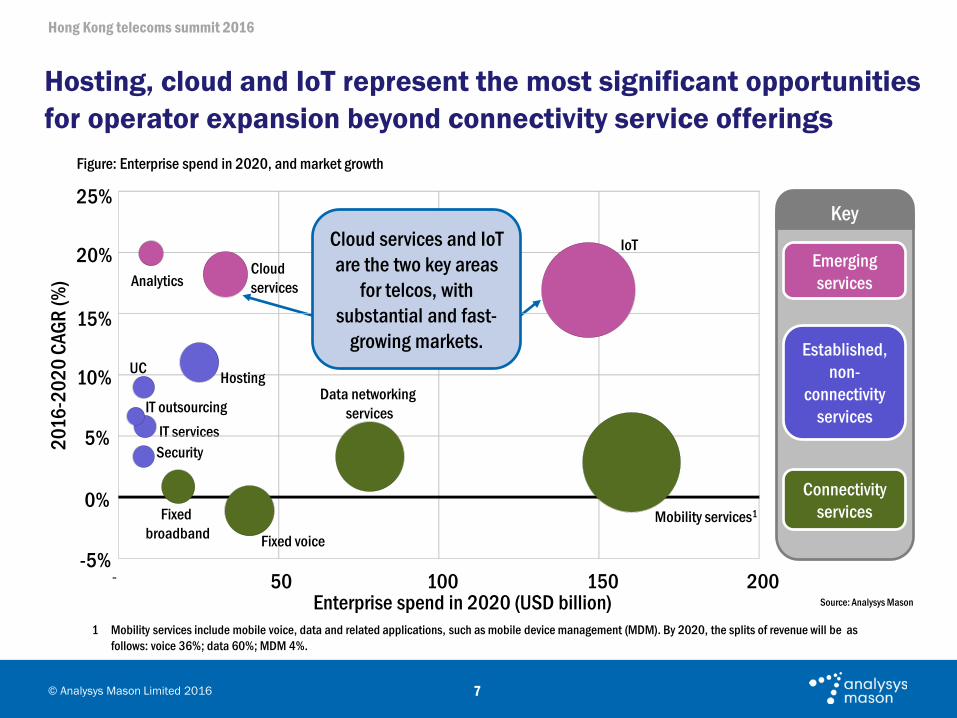

Hosting, cloud and IoT represent the most significant opportunities for operator expansion beyond connectivity service offerings

Figure: Enterprise spend in 2020, and market growth

Connectivity services

Established, non-

connectivity services

Emerging services

1 Mobility services include mobile voice, data and related applications, such as mobile device management (MDM). By 2020, the splits of revenue will be as follows: voice 36%; data 60%; MDM 4%.

Mobility services1

Data networking services

Cloud services

Fixed voice

Analytics

UC

Fixed broadband

IT services IT outsourcing

Security

IoT

-5%

0%

5%

10%

15%

20%

25%

- 50 100 150 200 Enterprise spend in 2020 (USD billion)

Cloud services and IoT are the two key areas

for telcos, with substantial and fast-

growing markets.

Hosting

Key

2016

-202

0 CA

GR (%

)

Source: Analysys Mason

7

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

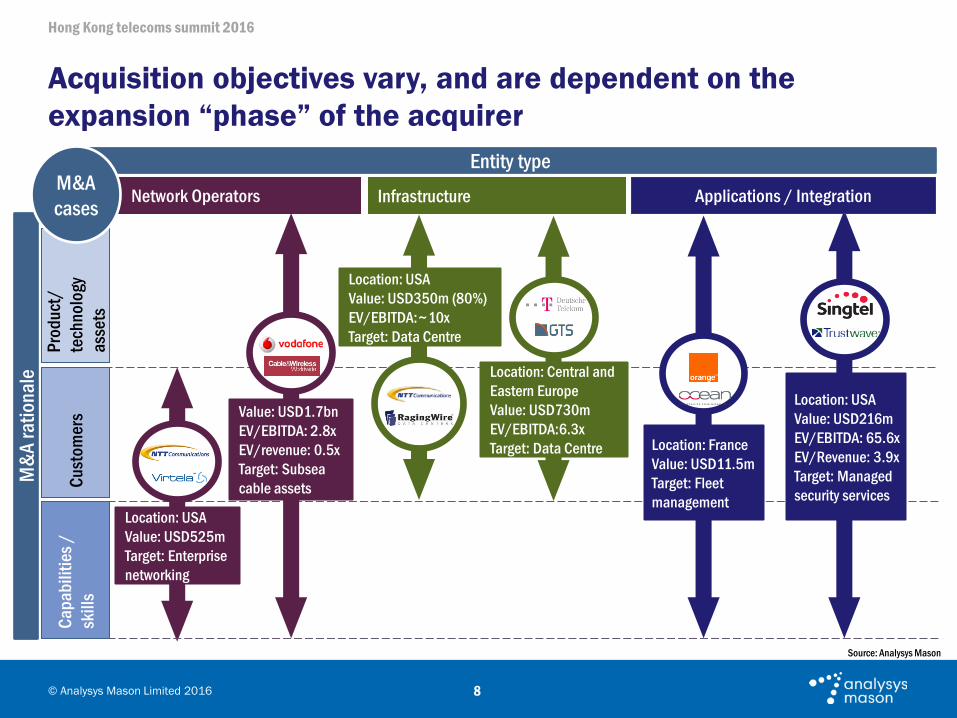

Network Operators

Prod

uct/

te

chno

logy

as

sets

M&A

ratio

nale

Entity type

Acquisition objectives vary, and are dependent on the expansion “phase” of the acquirer

8

M&A cases Infrastructure Applications / Integration

Capa

bilit

ies /

sk

ills

Cust

omer

s

Location: USA Value: USD525m Target: Enterprise networking

Value: USD1.7bn EV/EBITDA: 2.8x EV/revenue: 0.5x Target: Subsea cable assets

Location: USA Value: USD350m (80%) EV/EBITDA:~10x Target: Data Centre

Location: Central and Eastern Europe Value: USD730m EV/EBITDA:6.3x Target: Data Centre Location: France

Value: USD11.5m Target: Fleet management

Location: USA Value: USD216m EV/EBITDA: 65.6x EV/Revenue: 3.9x Target: Managed security services

Source: Analysys Mason

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

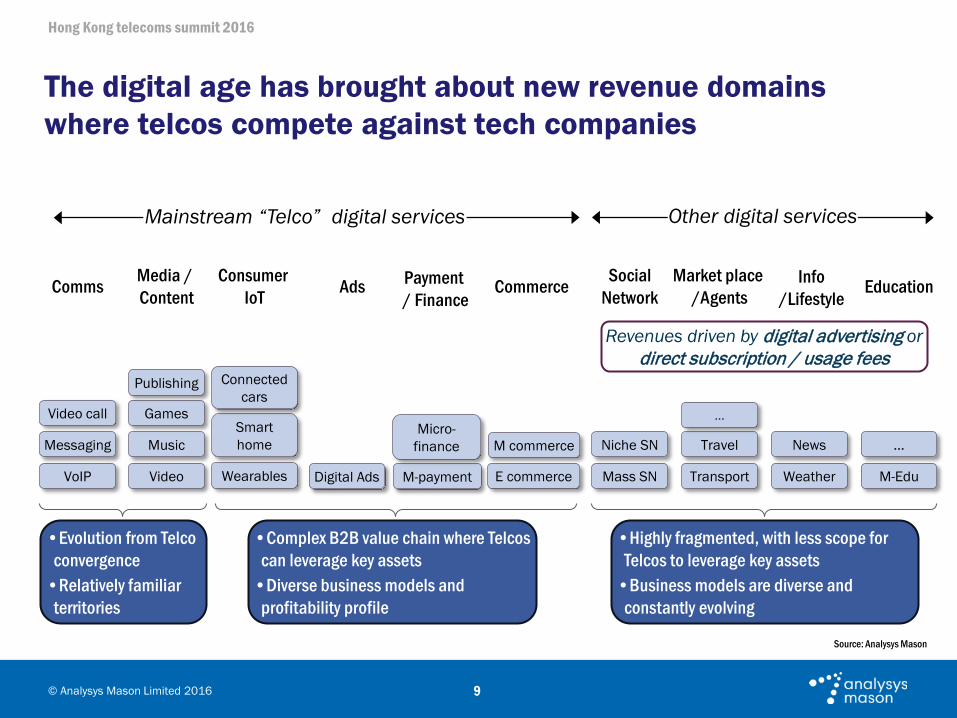

VoIP

Messaging

Video call

Video

Music

Games

Publishing

Digital Ads E commerce M-payment Mass SN

Niche SN

Transport

Travel

Weather

News

M-Edu

…

Comms Media / Content Ads Consumer

IoT Payment / Finance

Social Network

Market place /Agents

Info /Lifestyle

Education Commerce

Mainstream “Telco” digital services Other digital services

Revenues driven by digital advertising or direct subscription / usage fees

•Evolution from Telco convergence

•Relatively familiar territories

•Complex B2B value chain where Telcos can leverage key assets

•Diverse business models and profitability profile

•Highly fragmented, with less scope for Telcos to leverage key assets

•Business models are diverse and constantly evolving

The digital age has brought about new revenue domains where telcos compete against tech companies

Wearables

Smart home

Connected cars

…

M commerce Micro-

finance

Source: Analysys Mason

9

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

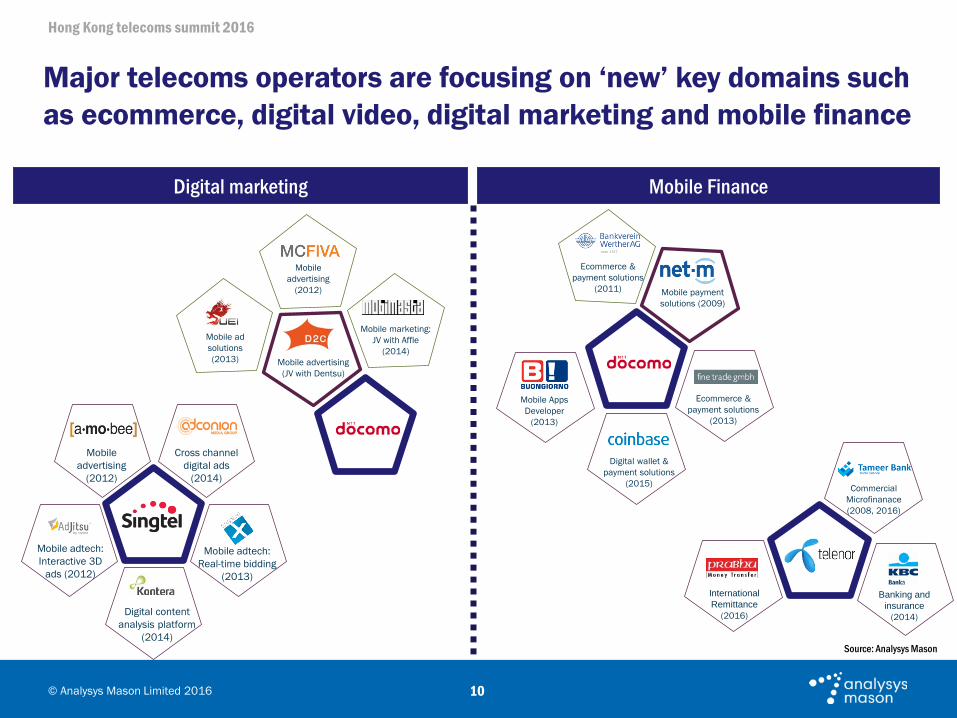

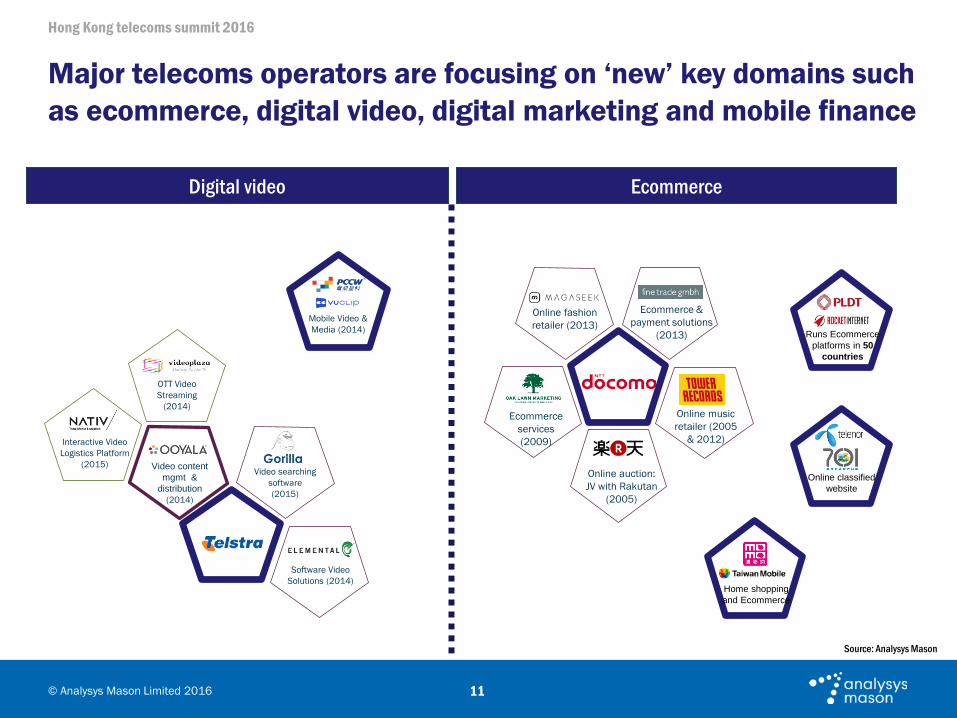

Major telecoms operators are focusing on ‘new’ key domains such as ecommerce, digital video, digital marketing and mobile finance

Digital marketing Mobile Finance

Mobile advertising

(2012)

Mobile adtech: Real-time bidding

(2013)

Mobile adtech: Interactive 3D

ads (2012)

Cross channel digital ads

(2014)

Digital content analysis platform

(2014)

International Remittance

(2016)

Commercial Microfinanace (2008, 2016)

Banking and insurance

(2014)

Mobile advertising (JV with Dentsu)

Mobile advertising

(2012)

Mobile ad solutions (2013)

Mobile marketing: JV with Affle

(2014)

Mobile Apps Developer

(2013)

Mobile payment solutions (2009)

Ecommerce & payment solutions

(2013)

Digital wallet & payment solutions

(2015)

Ecommerce & payment solutions

(2011)

Source: Analysys Mason

10

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

Major telecoms operators are focusing on ‘new’ key domains such as ecommerce, digital video, digital marketing and mobile finance

Mobile Video & Media (2014) Runs Ecommerce

platforms in 50 countries

Online classified website

Ecommerce & payment solutions

(2013)

Online fashion retailer (2013)

Ecommerce services (2009)

Online music retailer (2005

& 2012)

Online auction: JV with Rakutan

(2005)

Ecommerce Digital video

Video content mgmt &

distribution (2014)

Video searching software (2015)

Software Video Solutions (2014)

OTT Video Streaming

(2014)

Interactive Video Logistics Platform

(2015)

Home shopping and Ecommerce

Source: Analysys Mason

11

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

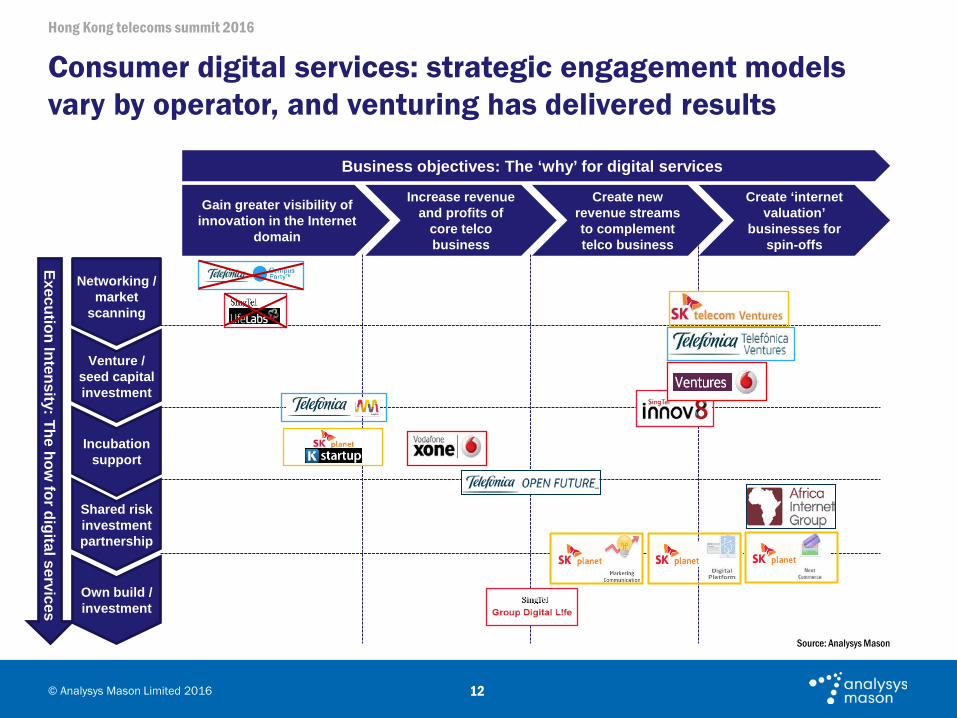

Consumer digital services: strategic engagement models vary by operator, and venturing has delivered results

12

Gain greater visibility of innovation in the Internet

domain

Increase revenue and profits of

core telco business

Create new revenue streams to complement telco business

Business objectives: The ‘why’ for digital services

Execution Intensity: The how for digital services

Create ‘internet valuation’

businesses for spin-offs

Networking / market

scanning

Venture / seed capital investment

Incubation support

Shared risk investment partnership

Own build / investment

Source: Analysys Mason

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

CONTENTS A SLOWDOWN FROM RECENT FRENZIES: OPPORTUNITIES FOR TELCOS?

TELCO M&A HOTSPOTS: ENTERPRISE ICT AND CONSUMER DIGITAL

CONSIDERATIONS FOR M&A IN NEW FRONTIERS

KEY TAKEAWAYS

13

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

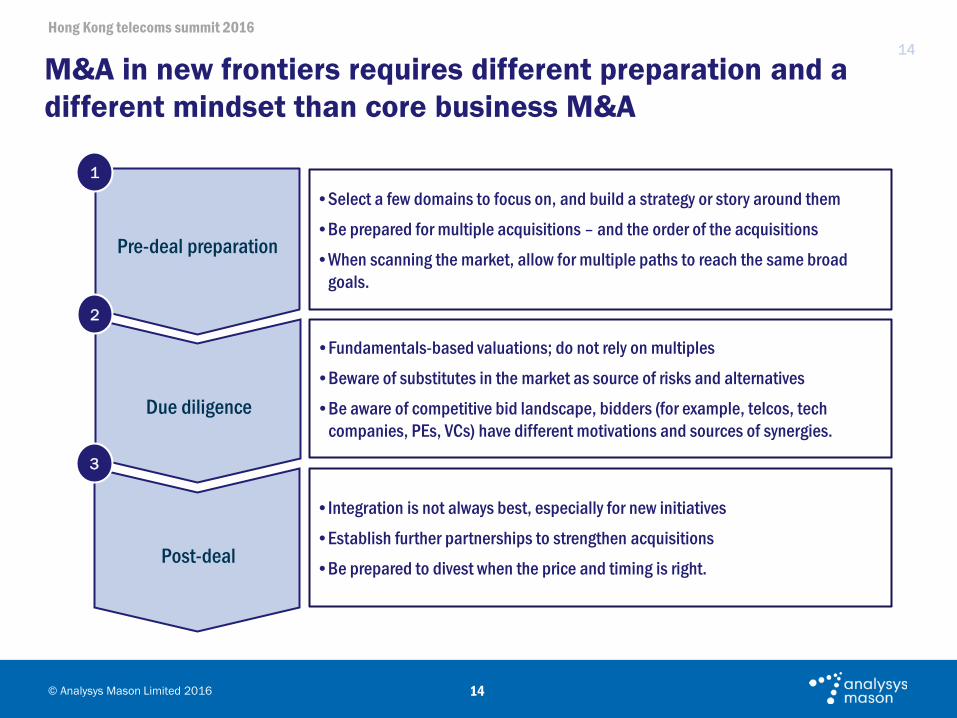

M&A in new frontiers requires different preparation and a different mindset than core business M&A

14

Post-deal

Pre-deal preparation

1

• Select a few domains to focus on, and build a strategy or story around them

• Be prepared for multiple acquisitions – and the order of the acquisitions

• When scanning the market, allow for multiple paths to reach the same broad goals.

• Integration is not always best, especially for new initiatives

• Establish further partnerships to strengthen acquisitions

• Be prepared to divest when the price and timing is right.

Due diligence

2

• Fundamentals-based valuations; do not rely on multiples

• Beware of substitutes in the market as source of risks and alternatives

• Be aware of competitive bid landscape, bidders (for example, telcos, tech companies, PEs, VCs) have different motivations and sources of synergies.

3

14

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

CONTENTS A SLOWDOWN FROM RECENT FRENZIES: OPPORTUNITIES FOR TELCOS?

TELCO M&A HOTSPOTS: ENTERPRISE ICT AND CONSUMER DIGITAL

CONSIDERATIONS FOR M&A IN NEW FRONTIERS

KEY TAKEAWAYS

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016 16

Key Takeaways

1 Enterprise ICT provides a solid growth area for telcos. Cloud, IoT and data centres are the prime drivers, but acquisitions should be consistent with a strategy that expands wallet share / breaking into enterprise customers’ ICT spend, by geographies.

2 Digital consumer services provide opportunities for fast growth business. Focus on a small set of domains, and be prepared to make multiple acquisitions to build scale in these fast expanding markets. Execution approaches could range from pure investment to buy-and-build of an entirely new business.

3 A different mindset / preparation from traditional M&A is required. Focused, but flexible, underlying strategy is needed, given that the M&A space is much more complex in these domains.

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

Contact details

17

Cambridge Tel: +44 (0)1223 460600 [email protected]

Milan Tel: +39 02 76 31 88 34 [email protected]

Dubai Tel: +971 (0)4 446 7473 [email protected]

New Delhi Tel: +91 124 4501860 [email protected]

Dublin Tel: +353 (0)1 602 4755 [email protected]

Paris Tel: +33 (0)1 72 71 96 96 [email protected]

London Tel: +44 (0)20 7395 9000 [email protected]

Singapore Tel: +65 6493 6038 [email protected]

Madrid Tel: +34 91 399 5016 [email protected]

Manchester Tel: +44 (0)161 877 7808 [email protected]

@AnalysysMason linkedin.com/company/analysys-mason youtube.com/AnalysysMason analysysmason.com/RSS

Taylor Lam Principal [email protected]

https://hk.linkedin.com/in/taylor-lam-5300b120

Boston Tel: +1 202 331 3080 [email protected]

Hong Kong Tel: +852 3669 7090 [email protected]

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

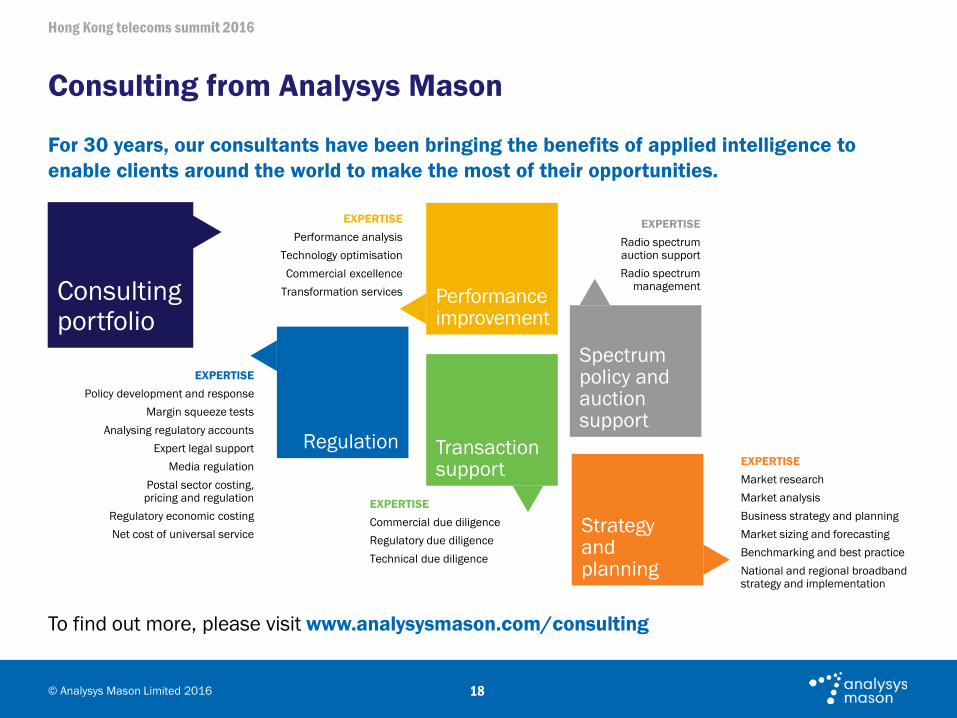

Consulting from Analysys Mason

18

For 30 years, our consultants have been bringing the benefits of applied intelligence to enable clients around the world to make the most of their opportunities.

To find out more, please visit www.analysysmason.com/consulting

Consulting portfolio

Strategy and planning

Transaction support

EXPERTISE Commercial due diligence Regulatory due diligence Technical due diligence

Regulation

EXPERTISE Policy development and response

Margin squeeze tests Analysing regulatory accounts

Expert legal support Media regulation

Postal sector costing, pricing and regulation

Regulatory economic costing Net cost of universal service

Performance improvement

EXPERTISE Market research Market analysis Business strategy and planning Market sizing and forecasting Benchmarking and best practice National and regional broadband strategy and implementation

EXPERTISE Performance analysis

Technology optimisation Commercial excellence

Transformation services

EXPERTISE Radio spectrum auction support Radio spectrum

management

Spectrum policy and auction support

Hong Kong telecoms summit 2016

© Analysys Mason Limited 2016

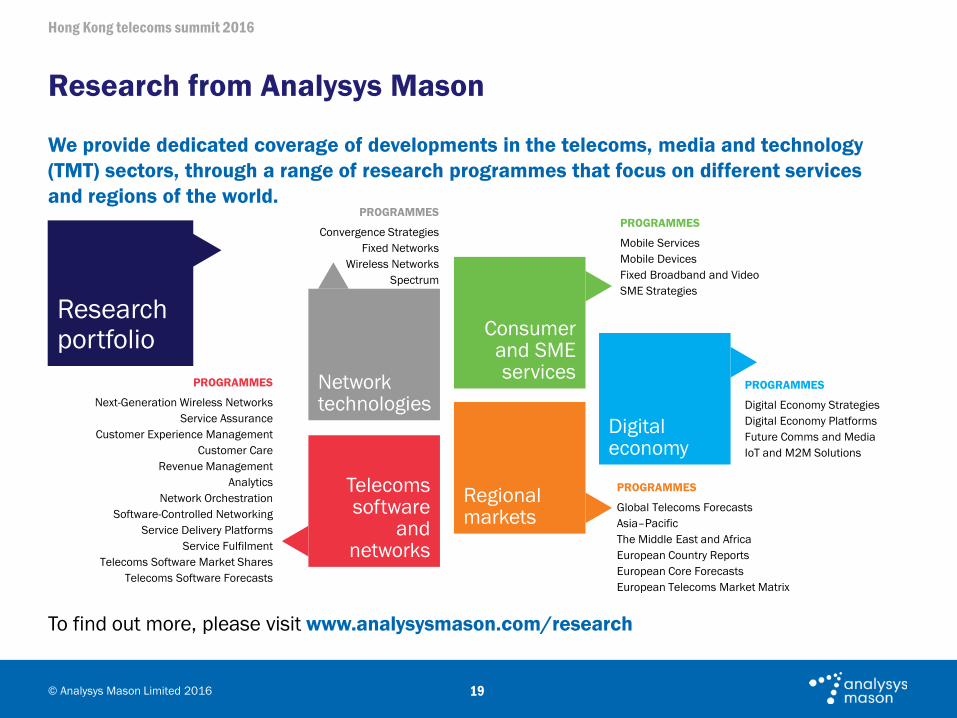

Research from Analysys Mason

19

We provide dedicated coverage of developments in the telecoms, media and technology (TMT) sectors, through a range of research programmes that focus on different services and regions of the world.

To find out more, please visit www.analysysmason.com/research

PROGRAMMES

Next-Generation Wireless Networks Service Assurance

Customer Experience Management Customer Care

Revenue Management Analytics

Network Orchestration Software-Controlled Networking

Service Delivery Platforms Service Fulfilment

Telecoms Software Market Shares Telecoms Software Forecasts

PROGRAMMES

Digital Economy Strategies Digital Economy Platforms Future Comms and Media IoT and M2M Solutions

PROGRAMMES

Mobile Services Mobile Devices Fixed Broadband and Video SME Strategies

PROGRAMMES

Convergence Strategies Fixed Networks

Wireless Networks Spectrum

Consumer and SME services

Digital economy

Regional markets

Telecoms software

and networks

Network technologies

PROGRAMMES

Global Telecoms Forecasts Asia–Pacific The Middle East and Africa European Country Reports European Core Forecasts European Telecoms Market Matrix

Research portfolio