Embed Size (px)

Citation preview

Macro Update Bank Indonesia cuts benchmark by 25 bps; will it be enough?

Bank Indonesia cuts benchmark by 25 bps

Yesterday (19 March), Bank Indonesia (BI) announced its latest monetary policy

decision, after finalizing a two-day board of governors meeting. The announcement—

conducted via video conference—was that the central bank had decided to lower its

policy rate—the 7-day reverse repo rate—to 4.5%, in line with Bloomberg consensus,

but different from our forecast for a 50-bps cut. Currently, the 7-day reverse repo rate of

4.5% marks its lowest level since April 2018.

Financial market hits another low

Despite meeting expectations of a 25-bps policy rate cut, Indonesia’s financial market

remains under fire; the Jakarta Composite Index (JCI) plunged by 5.2% on Thursday

(19 March), while Indonesia’s government 10Y bond yield jumped by 41 bps (please

note that yield moves inversely with price). As a result, the rupiah continued its losing

streak, depreciating by 4.5% against the US dollar to IDR15,913/US$. The depreciation

of the rupiah was worse compared with before BI’s rate-cut announcement, when it was

trading at around IDR15,585/US$.

No outbreak in Indonesia…yet

Up until yesterday (19 March), the government had announced a total of 309 Covid-19-

positive cases in the country. However, while 309 out of Indonesia’s population of more

than 270mn is a very small number, those numbers were obtained by testing a mere

1,651 people, according to official data from the Ministry of Finance. Thus, simple math

shows us that 19% of people tested by the government so far have turned out to be

Covid-19-positive.

Obviously, such a high figure was driven by the fact that Indonesia’s Covid-19 testing

kits were so limited, forcing hospitals to only test those at high risk of being

contaminated. Nevertheless, many suspect the number of Covid-19 positive cases in

the country would skyrocket should the government ramp up testing, as Indonesia has

yet to adopt any form of lockdown to contain the spread of the virus.

History tells us the rupiah should remain under pressure

Going forward, we expect the rupiah to remain under pressure, as we forecast selling

pressure to keep hitting both the equity and bond markets. Currently, transparency

around the handling of Covid-19 by the government is the key variable that is being

monitored by investors. On the other hand, as mentioned above, there have still been

no significant policy measures taken by the central bank, let alone the government.

If history is any reference, further pressure on the rupiah should come from the arrival

of dividend-payment season in April–June, or simply the second quarter. Over the past

10 years (2010–2019), the rupiah weakened six out ten times against the US dollar

during the second quarter (in QoQ terms).

Downside risk is materializing

Currently, we are keeping our macroeconomic projections unchanged for all of the

scenarios that we have set (base-case, bull-case, and bear-case), as we think it would

be wiser to give some time for Covid-19 developments to unfold, before revising our

model.

Macro update

March 20, 2020

PT.Mirae Asset Sekuritas Indonesia

Anthony Kevin

Economist

+62-21-5088-7000

Macro Update

2

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

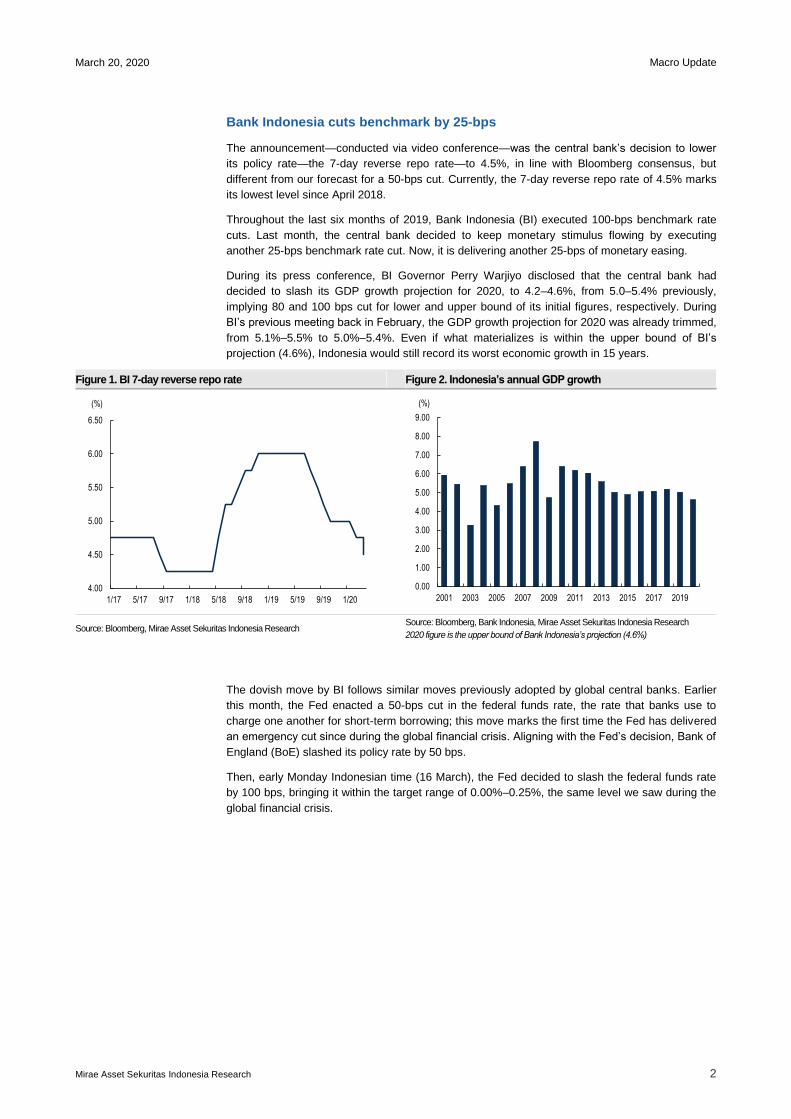

Bank Indonesia cuts benchmark by 25-bps

The announcement—conducted via video conference—was the central bank’s decision to lower

its policy rate—the 7-day reverse repo rate—to 4.5%, in line with Bloomberg consensus, but

different from our forecast for a 50-bps cut. Currently, the 7-day reverse repo rate of 4.5% marks

its lowest level since April 2018.

Throughout the last six months of 2019, Bank Indonesia (BI) executed 100-bps benchmark rate

cuts. Last month, the central bank decided to keep monetary stimulus flowing by executing

another 25-bps benchmark rate cut. Now, it is delivering another 25-bps of monetary easing.

During its press conference, BI Governor Perry Warjiyo disclosed that the central bank had

decided to slash its GDP growth projection for 2020, to 4.2–4.6%, from 5.0–5.4% previously,

implying 80 and 100 bps cut for lower and upper bound of its initial figures, respectively. During

BI’s previous meeting back in February, the GDP growth projection for 2020 was already trimmed,

from 5.1%–5.5% to 5.0%–5.4%. Even if what materializes is within the upper bound of BI’s

projection (4.6%), Indonesia would still record its worst economic growth in 15 years.

Figure 1. BI 7-day reverse repo rate Figure 2. Indonesia’s annual GDP growth

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Bank Indonesia, Mirae Asset Sekuritas Indonesia Research

2020 figure is the upper bound of Bank Indonesia’s projection (4.6%)

The dovish move by BI follows similar moves previously adopted by global central banks. Earlier

this month, the Fed enacted a 50-bps cut in the federal funds rate, the rate that banks use to

charge one another for short-term borrowing; this move marks the first time the Fed has delivered

an emergency cut since during the global financial crisis. Aligning with the Fed’s decision, Bank of

England (BoE) slashed its policy rate by 50 bps.

Then, early Monday Indonesian time (16 March), the Fed decided to slash the federal funds rate

by 100 bps, bringing it within the target range of 0.00%–0.25%, the same level we saw during the

global financial crisis.

4.00

4.50

5.00

5.50

6.00

6.50

1/17 5/17 9/17 1/18 5/18 9/18 1/19 5/19 9/19 1/20

(%)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

(%)

Macro Update

3

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Figure 3. Federal funds rate – upper bound Figure 4. Bank of England policy rate

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

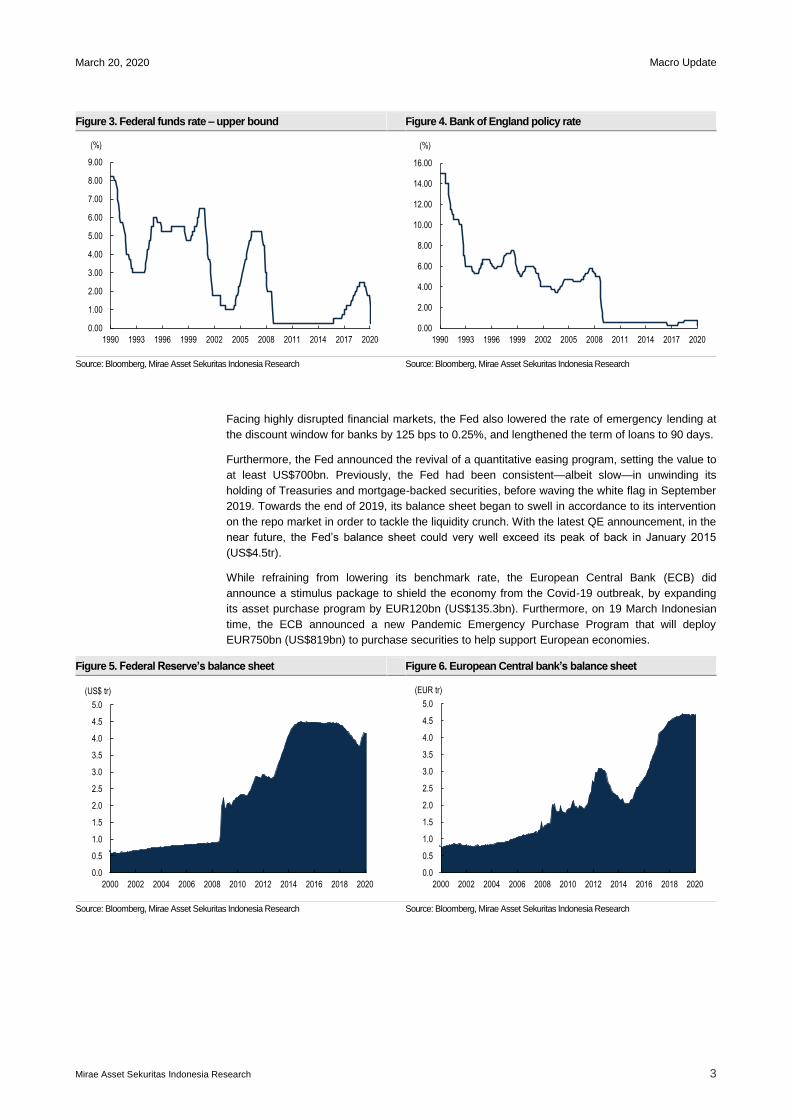

Facing highly disrupted financial markets, the Fed also lowered the rate of emergency lending at

the discount window for banks by 125 bps to 0.25%, and lengthened the term of loans to 90 days.

Furthermore, the Fed announced the revival of a quantitative easing program, setting the value to

at least US$700bn. Previously, the Fed had been consistent—albeit slow—in unwinding its

holding of Treasuries and mortgage-backed securities, before waving the white flag in September

2019. Towards the end of 2019, its balance sheet began to swell in accordance to its intervention

on the repo market in order to tackle the liquidity crunch. With the latest QE announcement, in the

near future, the Fed’s balance sheet could very well exceed its peak of back in January 2015

(US$4.5tr).

While refraining from lowering its benchmark rate, the European Central Bank (ECB) did

announce a stimulus package to shield the economy from the Covid-19 outbreak, by expanding

its asset purchase program by EUR120bn (US$135.3bn). Furthermore, on 19 March Indonesian

time, the ECB announced a new Pandemic Emergency Purchase Program that will deploy

EUR750bn (US$819bn) to purchase securities to help support European economies.

Figure 5. Federal Reserve’s balance sheet Figure 6. European Central bank’s balance sheet

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

(%)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

(%)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

(US$ tr)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

(EUR tr)

Macro Update

4

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Financial market hits another low

Despite meeting expectation of a 25-bps policy rate cut, Indonesia’s financial market remains

under fire; the Jakarta Composite Index (JCI) plunged by 5.2% on Thursday, while the Indonesian

government’s 10Y bond yield jumped by 41 bps (please note that yields move inversely with

price). As a result, the rupiah continued its losing streak, depreciating by 4.5% against the US

dollar to IDR15,913/US$. The depreciation of the rupiah was worse compared with before BI

announced its decision, when it was trading at around IDR15,585/US$.

Figure 7. Jakarta Composite Index Figure 8. Indonesia’s 10Y bond yield Figure 9. US$/IDR – spot market

Source: Bloomberg, Mirae Asset Sekuritas Indonesia

Research Source: Bloomberg, Mirae Asset Sekuritas Indonesia

Research Source: Bloomberg, Mirae Asset Sekuritas Indonesia

Research

In our view, BI should have executed a more aggressive easing in order to inject confidence into

the market, as the rupiah has been depreciating to way below its fundamental value. After a

depreciation of more than 4% yesterday, the rupiah has thus recorded a depreciation of 12.9%

throughout 2020, affirming its position as the worst currency in Asia, despite having been seen as

the best back in January. The additional easing measures by BI were badly needed, as the

government has yet to deliver any significant fiscal measures to boost the economy once the

number of new Covid-19 cases flatten.

Fundamentally speaking, there was more-than-ample room for BI to lower its benchmark rate by

another 25 bps, in our view. First, in FY19 and thus far in 2020, BI has only executed benchmark

rate cuts of 125 bps (before delivering yesterday’s 25-bps cut), way below the Fed’s 225-bps cuts.

Second, we expect inflation to remain manageable throughout the year, projecting it at 3.3%. In

February 2020, Statistics Indonesia recorded inflation at 2.98% YoY. Entering March, foodstuff

prices, the one constituent that often sends inflation soaring, were relatively tame.

Third, room for a 50-bps benchmark rate cut will come from a relatively wide spread between the

government bond yield and inflation. As of 18 March, the spread between Indonesia’s 10Y

government bond yield and inflation stands at 464.1 bps, higher than 2019’s average of 446.5

bps.

6.00

6.50

7.00

7.50

8.00

8.50

1/19 3/19 5/19 7/19 9/19 11/19 1/20 3/20

(%)

13,500

14,000

14,500

15,000

15,500

16,000

16,500

1/19 3/19 5/19 7/19 9/19 11/19 1/20 3/204,000

4,500

5,000

5,500

6,000

6,500

7,000

1/19 3/19 5/19 7/19 9/19 11/19 1/20 3/20

Macro Update

5

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Figure 10. Indonesia’s inflation Figure 11. Indonesia’s foodstuff prices

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

No outbreak in Indonesia…yet

Up until yesterday (19 March), the government had announced a total of 309 Covid-19 positive

cases in the country. However, while 309 out of Indonesia’s population of more than 270mn is a

very small number, those numbers were obtained by testing a mere 1,651 people, according to

official data from the Ministry of Finance. Thus, simple math shows us that 19% of people tested

by the government so far have turned out to be Covid-19-positive.

Figure 12. Cumulative Covid-19 cases in Indonesia Figure 13. New Covid-19 cases in Indonesia

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Obviously, such a high figure was driven by the fact that Indonesia’s Covid-19 testing kits were so

limited, forcing hospitals to only tests ones that are at the higher risk of being contaminated.

Nevertheless, many suspect the number of Covid-19-positive cases in the country would

skyrocket should the government ramp up testing, as Indonesia has yet to adopt any form of

lockdown to contain the spread of the virus.

In short, what has been happening lately in Indonesia is the inability of government officials, both

from the central and regional governments, to sit down together and discuss the issue. Earlier this

week, the governor of DKI Jakarta, Anies Baswedan, imposed strong measures aimed at limiting

the movement of people by significantly reducing the amount of public transportation available;

the policy–which was rescinded after only one day—resulted in massive crowds in MRT stations

and in the trains and buses themselves.

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2015 2016 2017 2018 2019 2020

(% YoY)

80

90

100

110

120

130

2/28 3/1 3/3 3/5 3/7 3/9 3/11 3/13 3/15 3/17

(Feb 28,2020 = 100) Rice Chicken

Beef Chicken egg

Onion Garlic

Red chili pepper Bird's eye chili

Cooking oil Sugar

0

50

100

150

200

250

300

350

3/01 3/04 3/07 3/10 3/13 3/16 3/19

(Person)

0

10

20

30

40

50

60

70

80

90

3/01 3/03 3/05 3/07 3/09 3/11 3/13 3/15 3/17 3/19

(Person)

Macro Update

6

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Figure 14. Long queue lines at MRT station Figure 15. Long queue lines at MRT station

Source: CNBC Indonesia, Mirae Asset Sekuritas Indonesia Research

Source: CNBC Indonesia, Mirae Asset Sekuritas Indonesia Research

Indonesia’s commander in chief, President Joko ―Jokowi‖ Widodo, recently issued a bold

statement stating that the decision on whether to lock down a region or the whole nation is in his

hands. However, according to the former Mayor of Solo, at this point, the option to lock down a

region or the whole nation is not even on the table.

History tells us the rupiah should remain under pressure

Going forward, we expect the rupiah to remain under pressure, as we forecast selling pressure to

keep hitting both the equity and bond markets. Currently, transparency around the handling of

Covid-19 by the government is the key variable that is being monitored by investors. On the other

hand, as mentioned above, there have still been no significant policy measures taken by the

central bank, let alone the government.

Investors in Indonesia’s financial market might be on the edge of witnessing an impending

outbreak in the world’s fourth most populous nation. Throughout the first quarter of 2020,

US$660.5mn of foreign funds were pulled from Indonesia’s equity market (as of 19 February),

while the figure on the bond market has reached US$6bn (as of 18 February), putting us on track

to see the biggest-ever quarterly capital outflow from the bond market.

Figure 16. Quarterly foreign funds flow to Indonesia’s equity

market

Figure 17. Quarterly foreign funds flow to Indonesia’s bond

market

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

-5,000

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

1/10 1/12 1/14 1/16 1/18 1/20

(US$ mn)

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1/10 1/12 1/14 1/16 1/18 1/20

(US$ mn)

Macro Update

7

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

The outbreak could very well be confirmed once the government conducts large-scale testing; PT

Rajawali Nusantara Indonesia (RNI), a state-owned enterprise, has ordered 500,000 rapid test

devices from China that could obtain tests result within only 15 minutes–three hours. An official

from the Ministry of State Owned Enterprises even said that the devices have begun arriving in

the country, albeit gradually.

If history is any reference, further pressure on the rupiah should come from the arrival of dividend-

payment season in April–June, or simply the second quarter. Over the past 10 years (2010–

2019), the rupiah weakened six out ten times against the US dollar during the second quarter (in

QoQ terms). On average during the 2010–2019 period, the rupiah recorded a 1.4% QoQ

depreciation against the US dollar in the second quarter. Taking into account all the

circumstances we have mentioned, we believe there is room for the rupiah to further depreciate to

IDR16,500/US$–IDR16,800/US$.

Figure 18. US$/IDR performance during the second quarter Figure 19. Average QoQ performance of US$/IDR

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research

Downside risk is materializing

In our economic outlook, titled ―Flat outlook amid COVID-19 outbreak‖ (published on 14 March),

we forecast the base-case scenario for Indonesia’s economy to record 5.02% growth in 2020, the

same level as last year’s; our base-case scenario was for the number of new Covid-19 cases in

China to remain at 80 per day or even less, new cases outside China to drop to around 2,000

nearing the end of March, and no outbreak in Indonesia.

Meanwhile, our bear-case scenario is that the outbreak extends way beyond March and occurs in

Indonesia. Under this scenario, Indonesia would not be able to greatly monetize the festive

season in April and May. Then, we predict economic growth to fall below the psychological level

of 5%, at 4.85%.

Recent developments have pointed more to our bear-case scenario than the base-case, i.e. the

downside risk is materializing. Currently, we are maintaining our macroeconomic projections

unchanged for all of the scenarios that we have set (base-case, bull-case, and bear-case), as we

think it would be wiser to give some time for Covid-19 developments to unfold, before revising our

model.

-1.2

1.4

3.4

0.6

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

1Q 2Q 3Q 4Q

(% QoQ)

-0.3

-1.5

3.12.8

4.5

2.0

-0.2

0.2

4.4

-0.8

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(% QoQ)

Macro Update

8

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Table 1. 2020 macroeconomic projection

2019 2020E (Base Case) 2020E (Bull Case) 2020E (Bear Case)

GDP Growth (%) 5.02 5.02 5.10 4.85

Household consumption (%) 5.04 5.05 5.10 4.90

Investment (%) 4.45 4.63 6.00 3.00

Government spending (%) 3.25 3.45 4.85 3.00

Exports (%) -0.87 1.35 3.00 -2.50

Imports (%) -7.69 2.06 4.50 -4.00

Inflation (%) 2.72 3.3 3.5 2.8

US$/IDR (average) 14,142 13,950 13,850 14,350

US$/IDR (year-end) 13,866 13,900 13,800 14,500

BI 7-Day Reverse Repo Rate

(%) 5.00 4.25 4.50 4.00

Source: Statistics Indonesia, Bloomberg, Mirae Asset Sekuritas Indonesia Research

Table 2. 2020 quarterly macroeconomic projection (base scenario)

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20

GDP Growth (% YoY) 5.07 5.05 5.02 4.97 4.92 5.08 5.05 5.05

Household consumption (%) 5.02 5.18 5.01 4.97 4.98 5.15 5.02 5.05

Investment (%) 5.03 4.55 4.21 4.06 2.50 3.25 6.00 6.50

Government spending (%) 5.22 8.23 0.98 0.48 5.00 3.00 2.00 4.00

Exports (%) -1.58 -1.73 0.10 -0.39 -4.00 1.50 4.00 3.50

Imports (%) -7.47 -6.84 -8.30 -8.05 -2.00 3.50 3.00 3.50

Source: Statistics Indonesia, Mirae Asset Sekuritas Indonesia Research

Macro Update

9

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

APPENDIX 1

Important Disclosures & Disclaimers

Stock Ratings Industry Ratings

Buy Relative performance of 20% or greater Overweight Fundamentals are favorable or improving

Trading Buy Relative performance of 10% or greater, but with volatility Neutral Fundamentals are steady without any material changes

Hold Relative performance of -10% and 10% Underweight Fundamentals are unfavorable or worsening

Sell Relative performance of -10%

* Ratings and Target Price History (Share price (----), Target price (----), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆))

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at PT Mirae Asset Sekuritas Indonesia, we may call a trading opportunity in case there is a technical or short-

term material development.

* The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of

future earnings.

The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic

conditions.

Equity Ratings Distribution

Buy Trading Buy Hold Sell

Equity Ratings Distribution 41% 18% 36% 5%

*Based on recommendations in the last 12-months (as of December 31, 2019)

Disclosures

As of the publication date, PT Mirae Asset Sekuritas Indonesia, and/or its affiliates do not have any special interest with the subject company and do not

own 1% or more of the subject company's shares outstanding.

Analyst Certification

Opinions expressed in this publication about the subject securities and companies accurately reflect the personal views of the Analysts primarily

responsible for this report. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject

companies in the past 12 months and have not been promised the same in connection with this report. No part of the compensation of the Analysts was, is,

or will be directly or indirectly related to the specific recommendations or views contained in this report but, like all employees of PT Mirae Asset Sekuritas

Indonesia, the Analysts receive compensation that is impacted by overall firm profitability, which includes revenues from, among other business units, the

institutional equities, investment banking, proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or

have reason to know of any actual, material conflict of interest of the Analyst or PT Mirae Asset Sekuritas Indonesia except as otherwise stated herein.

Disclaimers

This report is published by PT Mirae Asset Sekuritas Indonesia (―Mirae Asset‖), a broker-dealer registered in the Republic of Indonesia and a member of

the Indonesia Exchange. Information and opinions contained herein have been compiled from sources believed to be reliable and in good faith, but such

information has not been independently verified and Mirae Asset makes no guarantee, representation or warranty, express or implied, as to the fairness,

accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Bahasa Indonesia. If this

report is an English translation of a report prepared in the Indonesian language, the original Indonesian language report may have been made available to

investors in advance of this report. Mirae Asset, its affiliates and their directors, officers, employees and agents do not accept any liability for any loss

arising from the use hereof. This report is for general information purposes only and it is not and should not be construed as an offer or a solicitation of an

offer to effect transactions in any securities or other financial instruments. The intended recipients of this report are sophisticated institutional investors who

have substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use

of this report would violate any laws and regulations or subject Mirae Asset and its affiliates to registration or licensing requirements in any jurisdiction

should receive or make any use hereof. Information and opinions contained herein are subject to change without notice and no part of this document may

be copied or reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Mirae Asset. Mirae

Asset, its affiliates and their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may

make a purchase or sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or

otherwise, in each case either as principals or agents. Mirae Asset and its affiliates may have had, or may be expecting to enter into, business relationships

with the subject companies to provide investment banking, market-making or other financial services as are permitted under applicable laws and

regulations. The price and value of the investments referred to in this report and the income from them may go down as well as up, and investors may

realize losses on any investments. Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital

may occur.

Distribution

United Kingdom: This report is being distributed by Mirae Asset Securities (Europe) Ltd. in the United Kingdom only to (i) investment professionals falling

within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the ―Order‖), and (ii) high net worth companies and

other persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as

―Relevant Persons‖). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any

of its contents.

United States: This report is distributed in the U.S. by Mirae Asset Securities (America) Inc., a member of FINRA/SIPC, and is only intended for major

institutional investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their

acceptance thereof represent and warrant that they are a major institutional investor and have not received this report under any express or implied

understanding that they will direct commission income to Mirae Asset or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in

any securities discussed herein should contact and place orders with Mirae Asset Securities (America) Inc., which accepts responsibility for the contents of

this report in the U.S. The securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such

case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements.

Macro Update

10

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Hong Kong: This document has been approved for distribution in Hong Kong by Mirae Asset Securities (Hong Kong) Ltd., which is regulated by the Hong

Kong Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for

distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws

of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Mirae

Asset or its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Mirae

Asset and its affiliates to any registration or licensing requirement within such jurisdiction.

Macro Update

11

March 20, 2020

Mirae Asset Sekuritas Indonesia Research

Mirae Asset Daewoo International Network

Mirae Asset Daewoo Co., Ltd. (Seoul) Mirae Asset Securities (HK) Ltd. Mirae Asset Securities (UK) Ltd.

Global Equity Sales Team

Mirae Asset Center 1 Building

26 Eulji-ro 5-gil, Jung-gu, Seoul 04539

Korea

Suites 1109-1114, 11th Floor

Two International Finance Centre

8 Finance Street, Central

Hong Kong

China

41st Floor, Tower 42

25 Old Broad Street,

London EC2N 1HQ

United Kingdom

Tel: 82-2-3774-2124 Tel: 852-2845-6332 Tel: 44-20-7982-8000

Mirae Asset Securities (USA) Inc. Mirae Asset Wealth Management (USA) Inc. Mirae Asset Wealth Management (Brazil) CCTVM

810 Seventh Avenue, 37th Floor

New York, NY 10019

USA

555 S. Flower Street, Suite 4410,

Los Angeles, California 90071

USA

Rua Funchal, 418, 18th Floor, E-Tower Building

Vila Olimpia

Sao Paulo - SP

04551-060

Brasil

Tel: 1-212-407-1000 Tel: 1-213-262-3807 Tel: 55-11-2789-2100

PT. Mirae Asset Sekuritas Indonesia Mirae Asset Securities (Singapore) Pte. Ltd. Mirae Asset Securities (Vietnam) LLC

District 8, Treasury Tower Building Lt. 50

Sudirman Central Business District

Jl. Jend. Sudirman, Kav. 52-54 Jakarta Selatan

12190

Indonesia

6 Battery Road, #11-01

Singapore 049909

Republic of Singapore

7F, Saigon Royal Building

91 Pasteur St.

District 1, Ben Nghe Ward, Ho Chi Minh City

Vietnam

Tel: 62-21-5088-7000 Tel: 65-6671-9845 Tel: 84-8-3911-0633 (ext.110)

Mirae Asset Securities Mongolia UTsK LLC Mirae Asset Investment Advisory (Beijing) Co., Ltd Beijing Representative Office

#406, Blue Sky Tower, Peace Avenue 17

1 Khoroo, Sukhbaatar District

Ulaanbaatar 14240

Mongolia

2401B, 24th Floor, East Tower, Twin Towers

B12 Jianguomenwai Avenue, Chaoyang District

Beijing 100022

China

2401A, 24th Floor, East Tower, Twin Towers

B12 Jianguomenwai Avenue, Chaoyang District

Beijing 100022

China

Tel: 976-7011-0806 Tel: 86-10-6567-9699 Tel: 86-10-6567-9699 (ext. 3300)

Shanghai Representative Office Ho Chi Minh Representative Office

38T31, 38F, Shanghai World Financial Center

100 Century Avenue, Pudong New Area Shanghai

200120

China

7F, Saigon Royal Building

91 Pasteur St.

District 1, Ben Nghe Ward, Ho Chi Minh City

Vietnam

Tel: 86-21-5013-6392 Tel: 84-8-3910-7715