Embed Size (px)

Citation preview

Macroeconomic Policy in the Eurozone: Are There

Alternatives to Slow Growth and High Unemployment?

Mark Weisbrot, Co-DirectorCenter for Economic and Policy Research

September 24, 2011

• Europe’s crisis, stagnation, and unemployment are not the result of unsustainable borrowing

• It is the result of bad macroeconomic policies from the European authorities:

• The “Troika” – European Central Bank, European Commission, IMF

• Three most important macroeconomic policies: Fiscal, monetary, and exchange rate

• Not helping, or actively causing damage, in troubled eurozone economies (Greece, Ireland, Portugal, Spain, Italy)

• Troika, especially ECB has played game of brinksmanship with troubled economies since early 2010

• Repeatedly pushing Europe, and now much of the world economy, to the edge of serious crisis

• Why?

What policy failure looks like

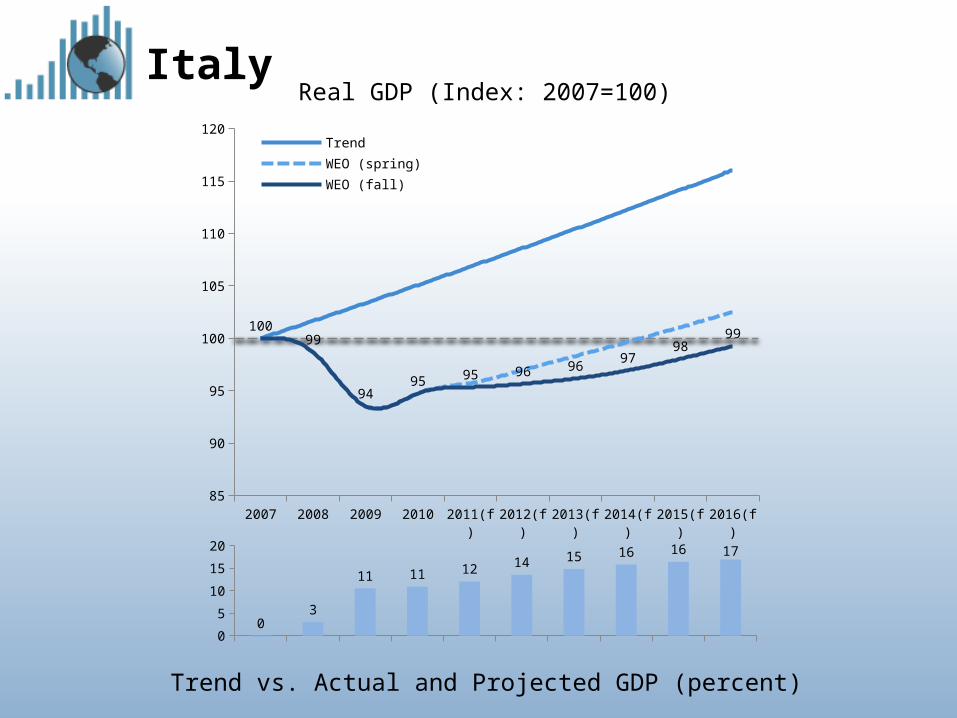

ItalyReal GDP (Index: 2007=100)

Trend vs. Actual and Projected GDP (percent)

0

5

10

15

20

03

11 11 12 14 15 16 16 17

2007 2008 2009 2010 2011(f) 2012(f) 2013(f) 2014(f) 2015(f) 2016(f)85

90

95

100

105

110

115

120

10099

9495 95 96 96

9798

99

Trend

WEO (spring)

WEO (fall)

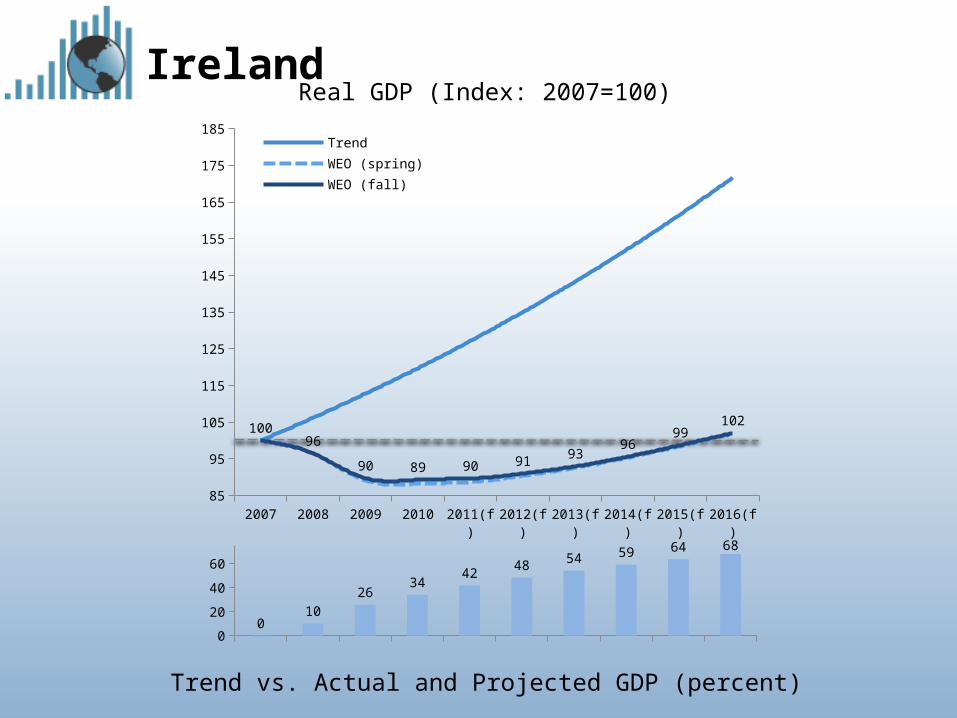

IrelandReal GDP (Index: 2007=100)

0

20

40

60

010

2634

4248 54 59 64 68

Trend vs. Actual and Projected GDP (percent)

2007 2008 2009 2010 2011(f) 2012(f) 2013(f) 2014(f) 2015(f) 2016(f)85

95

105

115

125

135

145

155

165

175

185

10096

90 89 90 91 9396

99102

Trend

WEO (spring)

WEO (fall)

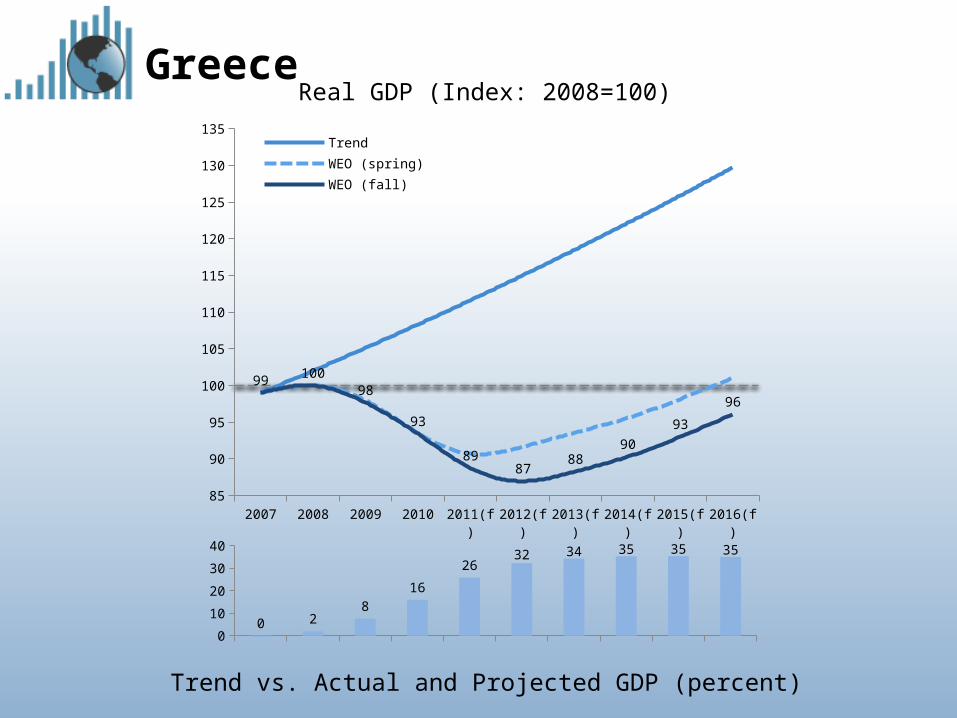

GreeceReal GDP (Index: 2008=100)

0

10

20

30

40

0 28

16

2632 34 35 35 35

Trend vs. Actual and Projected GDP (percent)

2007 2008 2009 2010 2011(f) 2012(f) 2013(f) 2014(f) 2015(f) 2016(f)85

90

95

100

105

110

115

120

125

130

135

99 10098

93

8987

8890

93

96

Trend

WEO (spring)

WEO (fall)

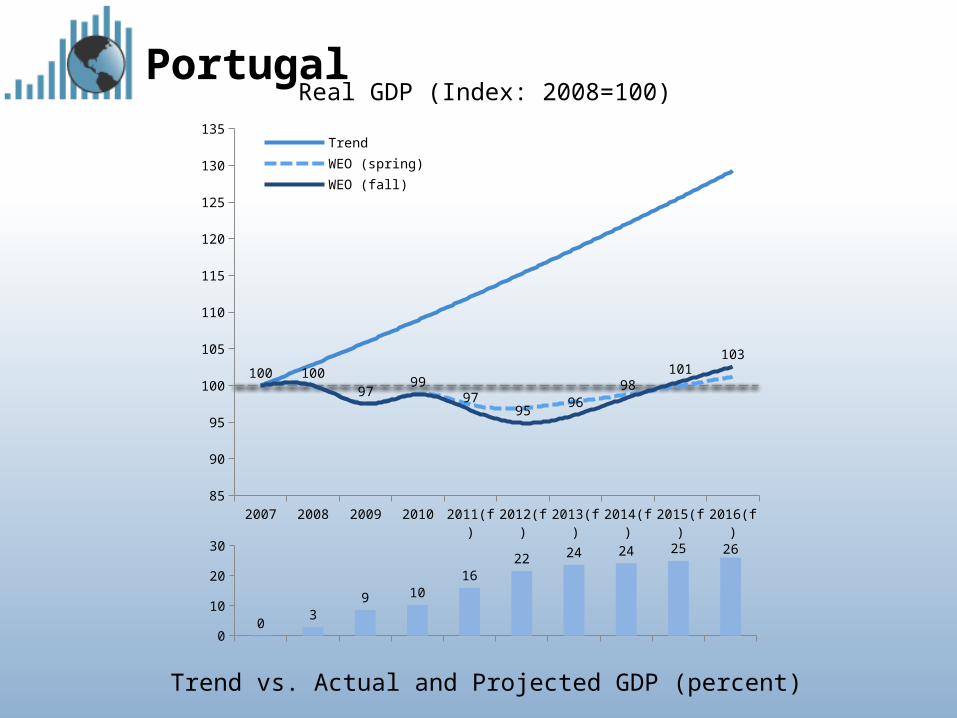

PortugalReal GDP (Index: 2008=100)

0

10

20

30

03

9 1016

22 24 24 25 26

Trend vs. Actual and Projected GDP (percent)

2007 2008 2009 2010 2011(f) 2012(f) 2013(f) 2014(f) 2015(f) 2016(f)85

90

95

100

105

110

115

120

125

130

135

100 10097

9997

9596

98101

103

Trend

WEO (spring)

WEO (fall)

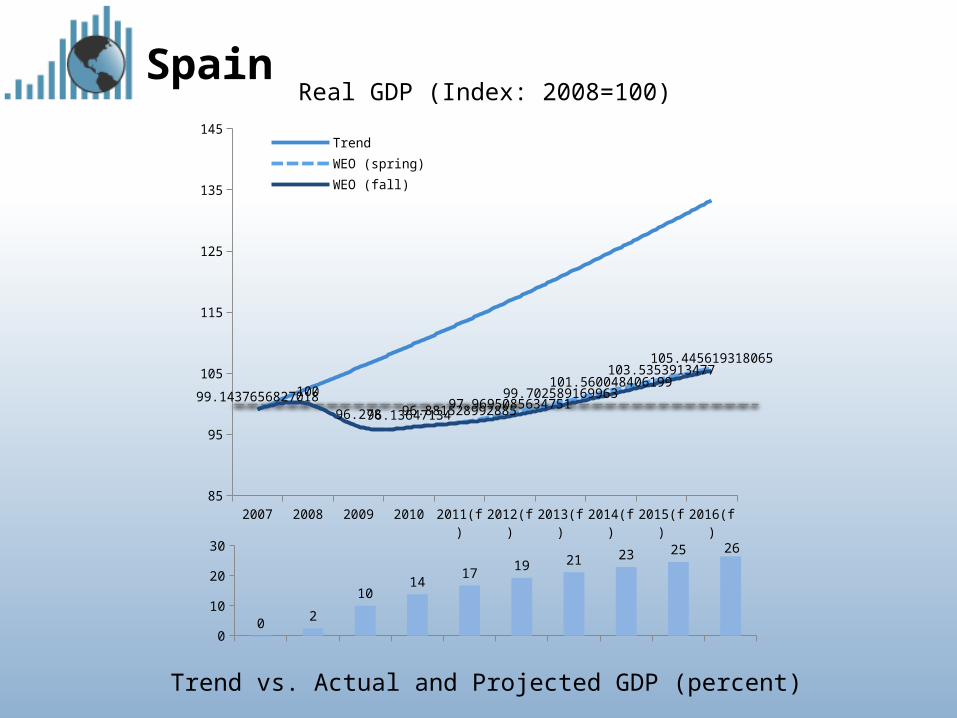

SpainReal GDP (Index: 2008=100)

0

10

20

30

0 2

1014

17 19 21 23 25 26

Trend vs. Actual and Projected GDP (percent)

2007 2008 2009 2010 2011(f) 2012(f) 2013(f) 2014(f) 2015(f) 2016(f)85

95

105

115

125

135

145

99.1437656827018100

96.27896.1364713496.88152899288597.969508563475199.702589169963

101.560048406199103.5353913477

105.445619318065

Trend

WEO (spring)

WEO (fall)

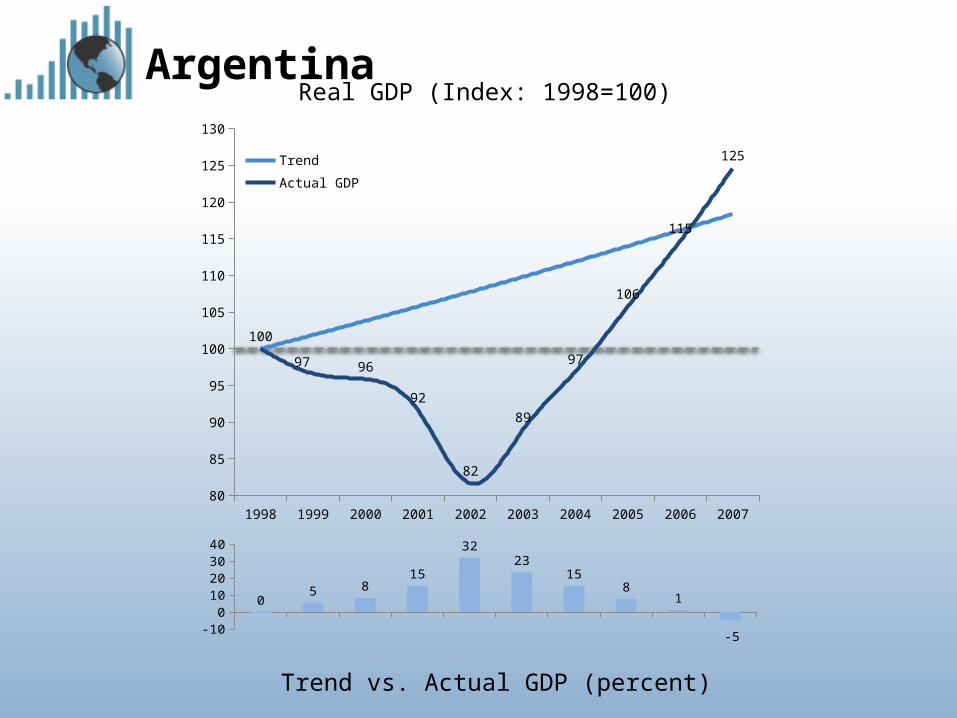

ArgentinaReal GDP (Index: 1998=100)

Trend vs. Actual GDP (percent)

-100

10203040

05 8

15

3223

158

1

-5

1998 1999 2000 2001 2002 2003 2004 2005 2006 200780

85

90

95

100

105

110

115

120

125

130

100

97 96

92

82

89

97

106

115

125Trend

Actual GDP

Lessons from Argentina:• Despite chaotic default, financial

collapse, and no outside help, Argentine economy begins to recover just one quarter after default

• Argentina reaches pre-recession GDP within 3 years, despite much deeper recession – compare to more than a decade in Greece.

• Passes trend GDP in 2006 (compare to eurozone – when?)

• Real GDP growth more than 90 percent 2002-2011

• There are ALWAYS alternatives to the years of recession, stagnation, and high unemployment that the Troika is offering to the troubled eurozone economies

The human cost of economic mismanagement

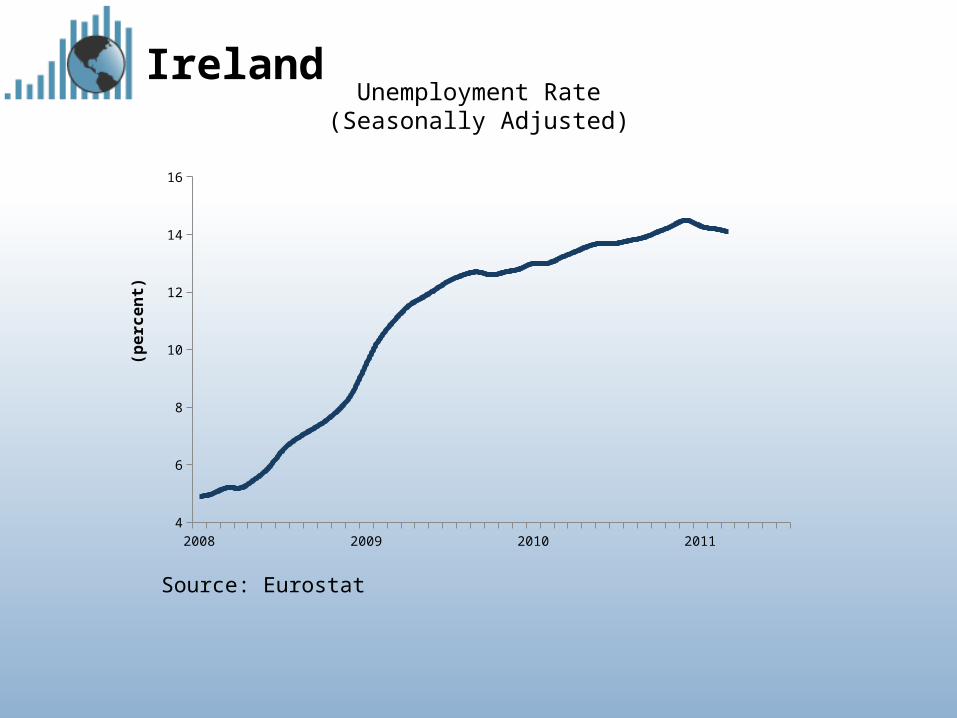

IrelandUnemployment Rate(Seasonally Adjusted)

Source: Eurostat

2008 2009 2010 20114

6

8

10

12

14

16

(pe

rce

nt)

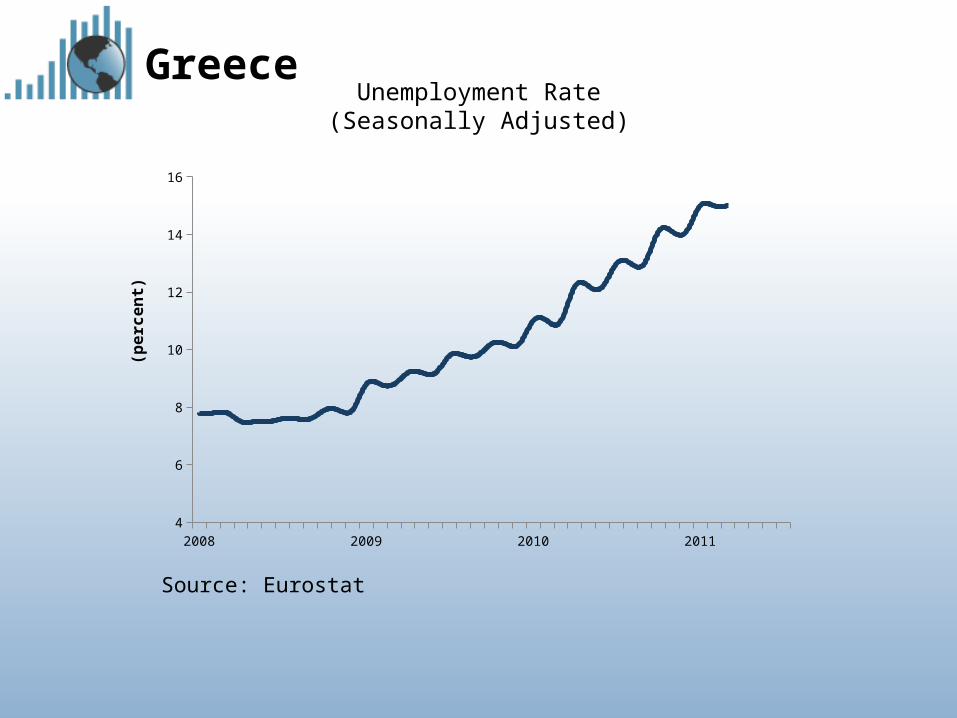

GreeceUnemployment Rate(Seasonally Adjusted)

Source: Eurostat

2008 2009 2010 20114

6

8

10

12

14

16

(pe

rce

nt)

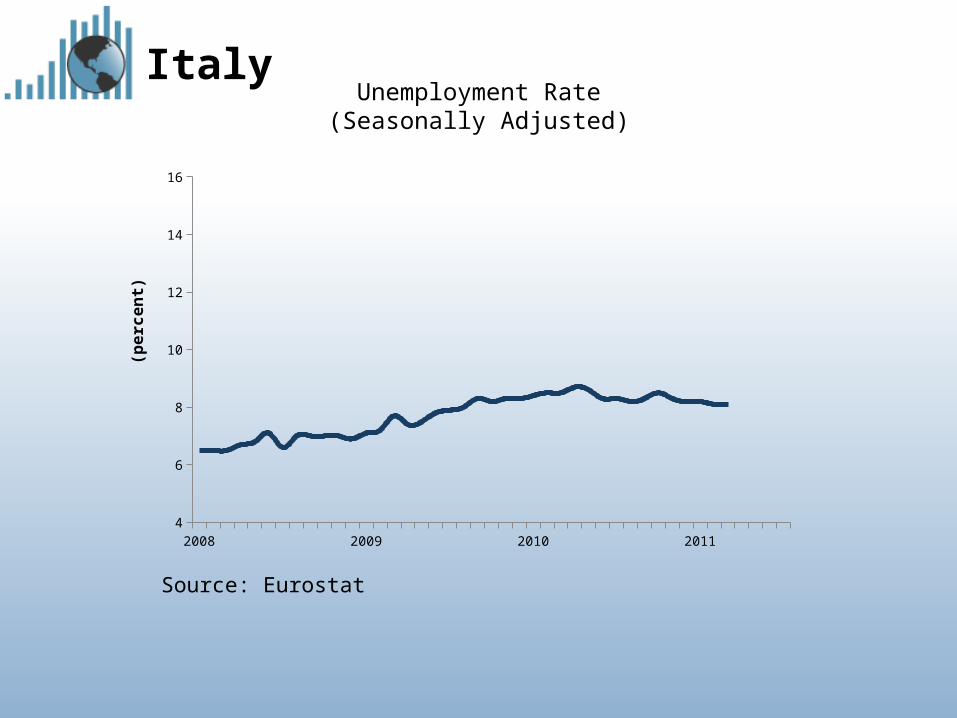

ItalyUnemployment Rate(Seasonally Adjusted)

Source: Eurostat

2008 2009 2010 20114

6

8

10

12

14

16

(pe

rce

nt)

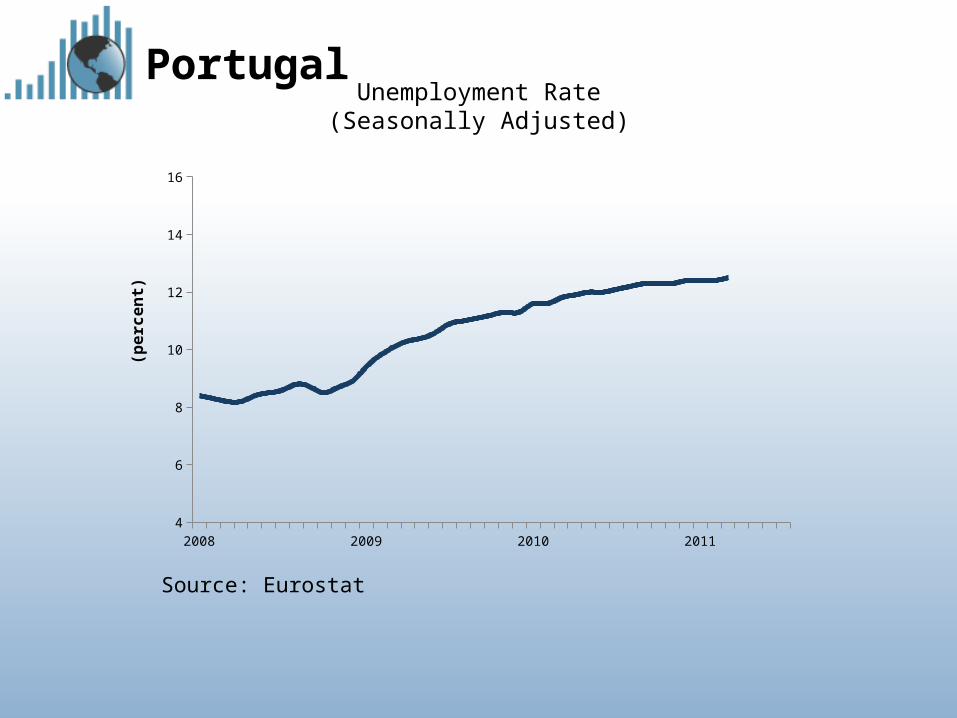

PortugalUnemployment Rate(Seasonally Adjusted)

Source: Eurostat

2008 2009 2010 20114

6

8

10

12

14

16

(pe

rce

nt)

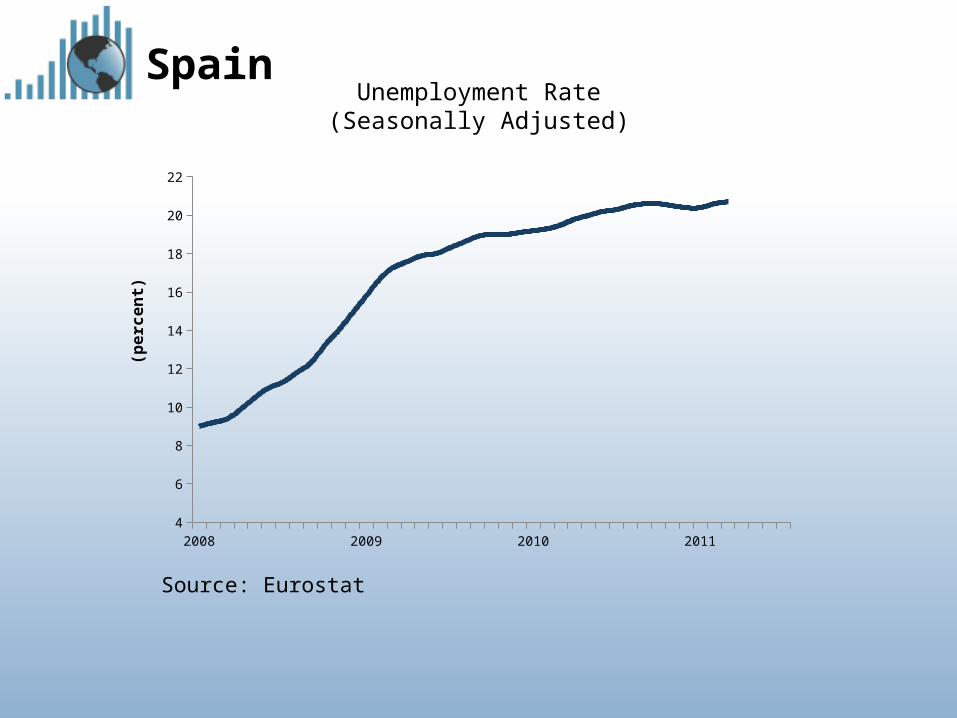

SpainUnemployment Rate(Seasonally Adjusted)

Source: Eurostat

2008 2009 2010 20114

6

8

10

12

14

16

18

20

22

(pe

rce

nt)

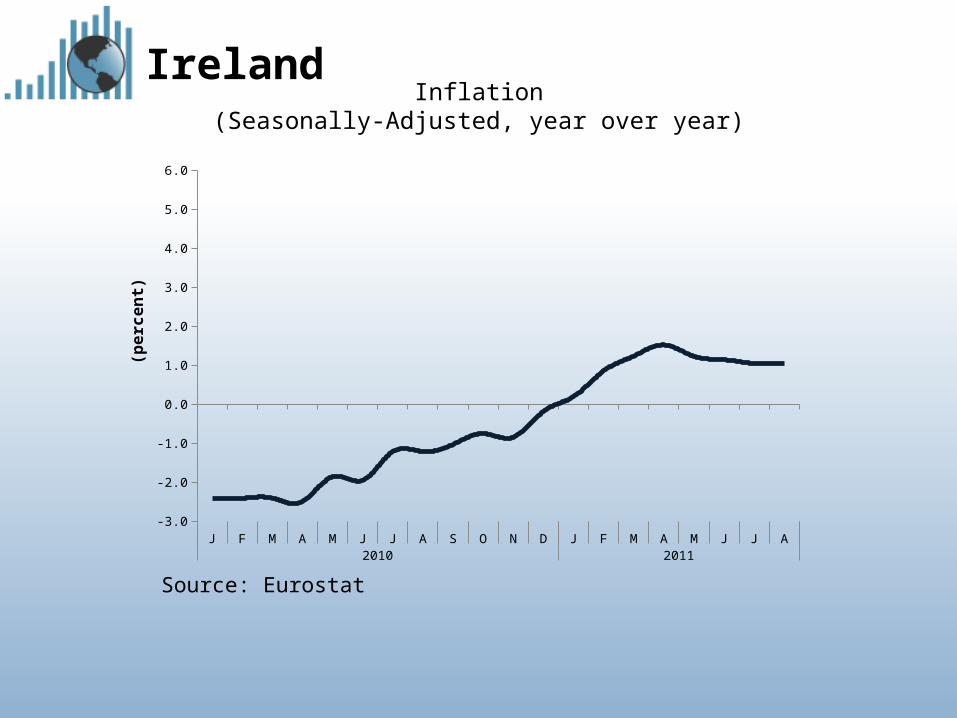

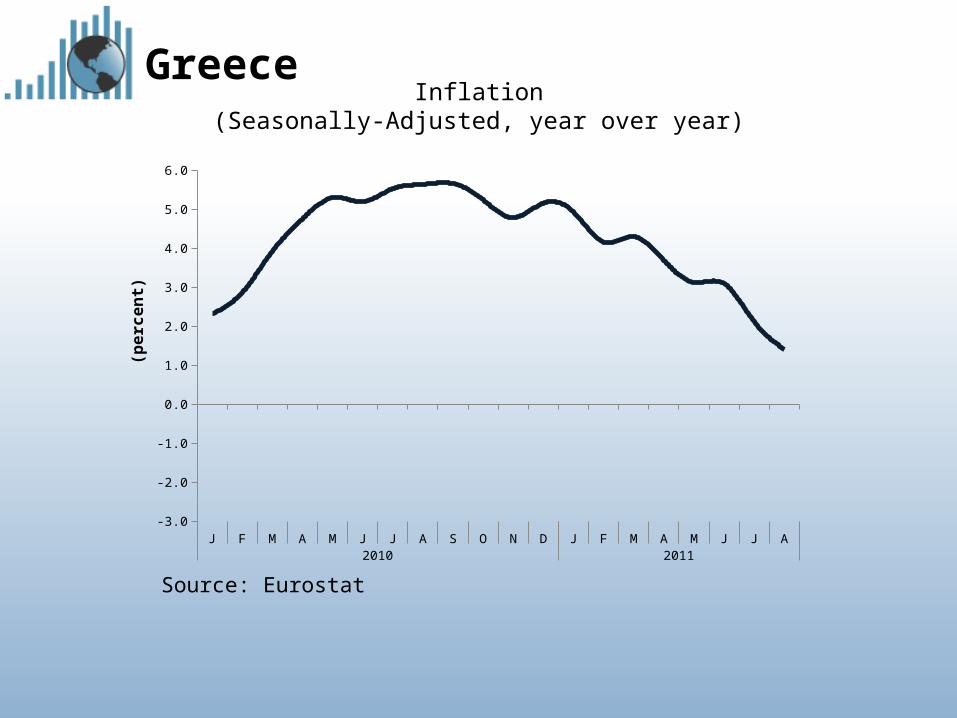

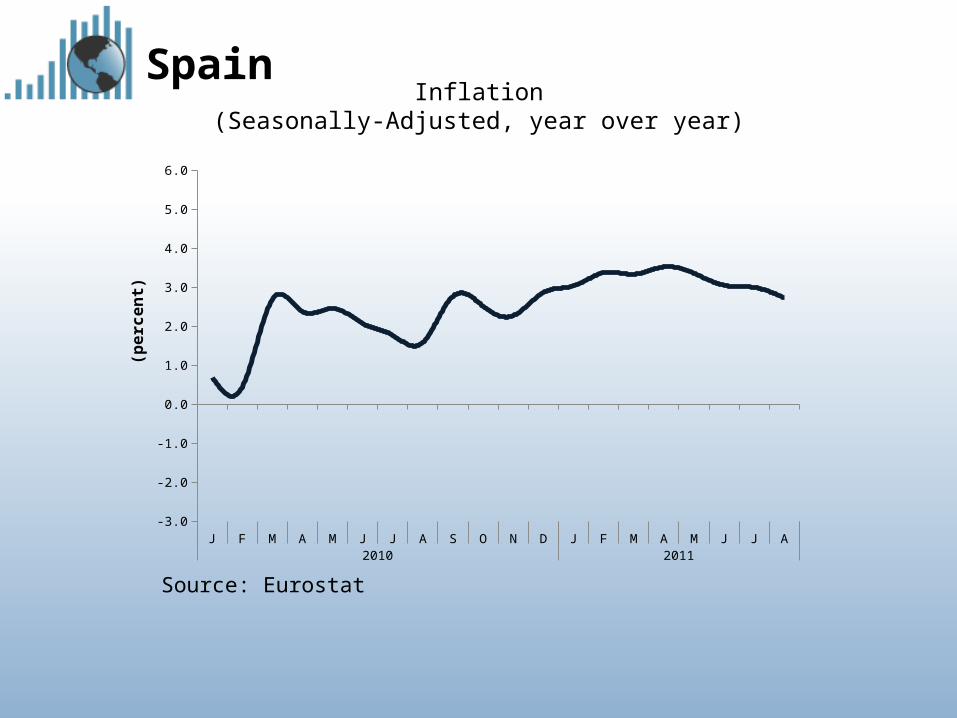

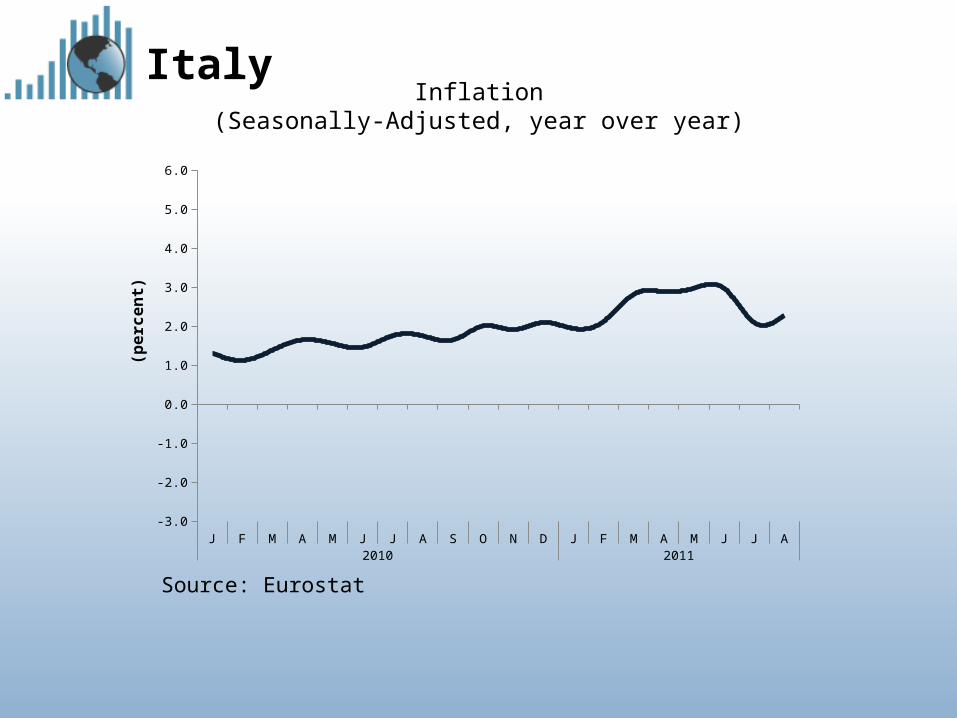

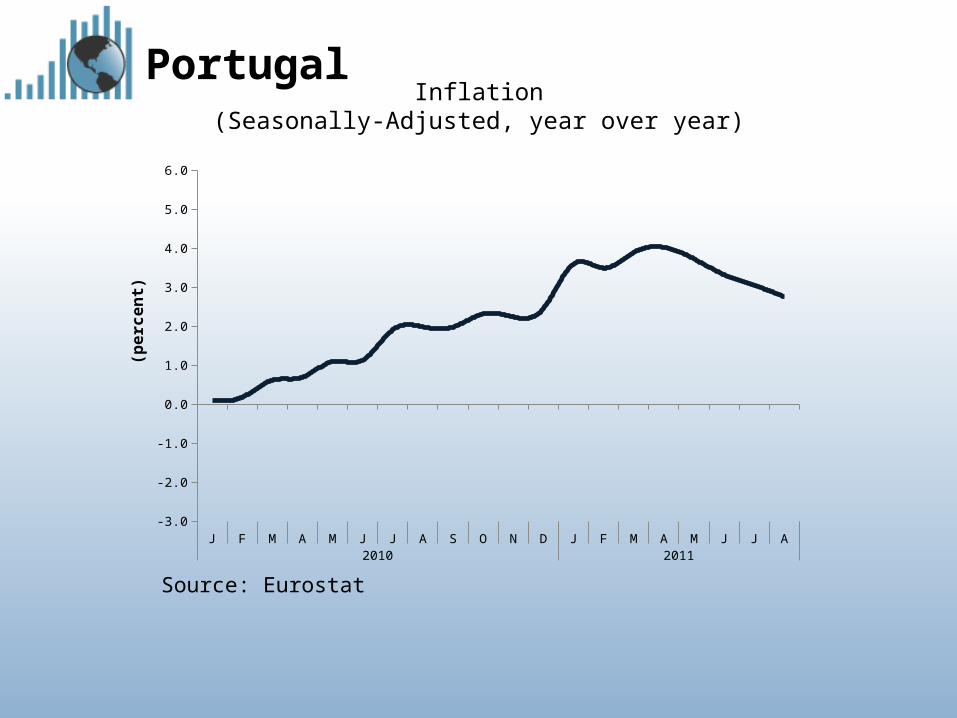

• Low inflation implies there is plenty of room for expansionary monetary and fiscal policies – but eurozone countries that need it can’t implement these policies

IrelandInflation

(Seasonally-Adjusted, year over year)

Source: Eurostat

J F M A M J J A S O N D J F M A M J J A2010 2011

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(pe

rce

nt)

Greece

Source: Eurostat

J F M A M J J A S O N D J F M A M J J A2010 2011

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(pe

rce

nt)

Inflation(Seasonally-Adjusted, year over year)

Spain

Source: Eurostat

J F M A M J J A S O N D J F M A M J J A2010 2011

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(pe

rce

nt)

Inflation(Seasonally-Adjusted, year over year)

Italy

Source: Eurostat

J F M A M J J A S O N D J F M A M J J A2010 2011

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(pe

rce

nt)

Inflation(Seasonally-Adjusted, year over year)

Portugal

Source: Eurostat

J F M A M J J A S O N D J F M A M J J A2010 2011

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(pe

rce

nt)

Inflation(Seasonally-Adjusted, year over year)

“Internal Devaluation” doesn’t work

Real Effective Exchange Rate(Based on Unit Labor Costs of 27 Trading Partners)

Source: Eurostat

I II III IV I II III IV I II III IV2008 2009 2010

90

95

100

105

Spain Ireland

Portugal Greece

Italy

(In

de

x:

20

08

QI=

10

0)

More fiscal consolidation

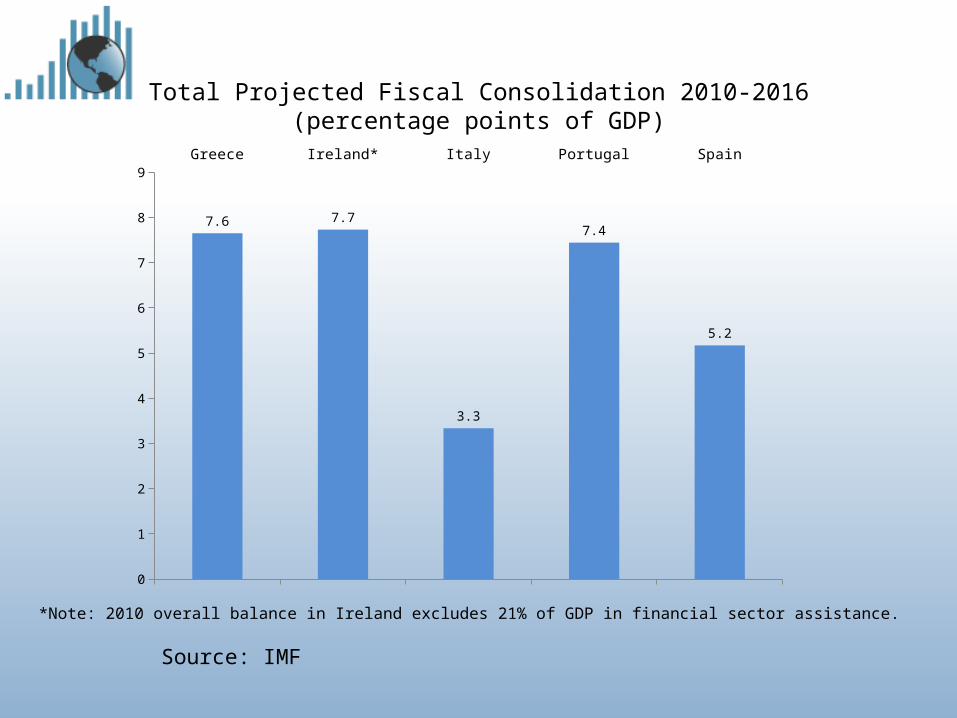

Total Projected Fiscal Consolidation 2010-2016(percentage points of GDP)

Source: IMF

Greece Ireland* Italy Portugal Spain

0

1

2

3

4

5

6

7

8

9

7.6 7.7

3.3

7.4

5.2

*Note: 2010 overall balance in Ireland excludes 21% of GDP in financial sector assistance.

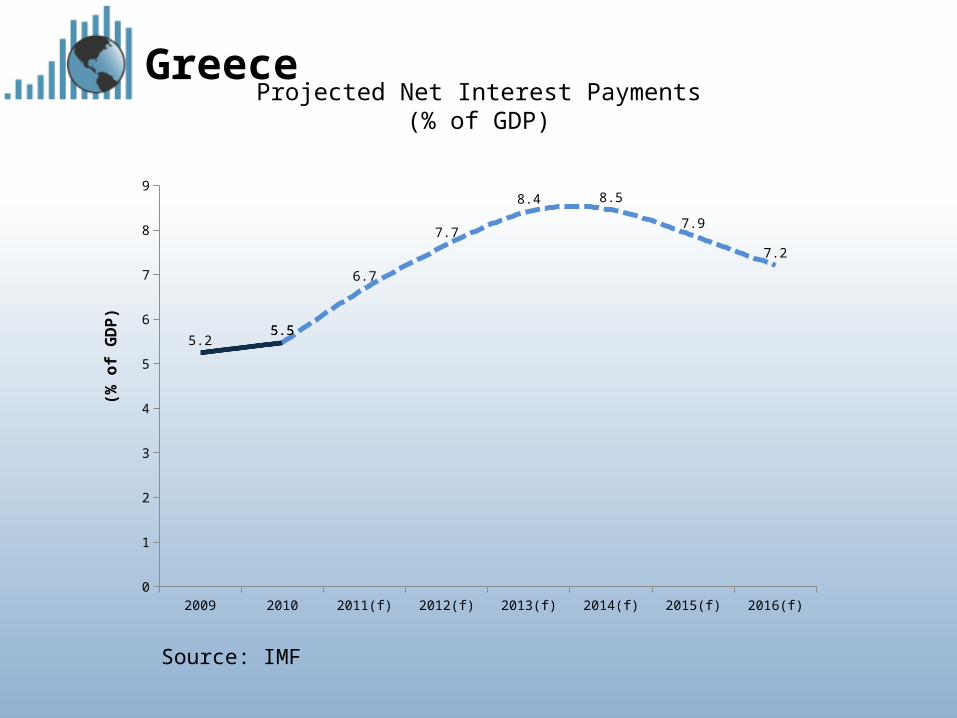

Projected Net Interest Payments(% of GDP)

Source: IMF

Greece

2009 2010 2011(f) 2012(f) 2013(f) 2014(f) 2015(f) 2016(f)0

1

2

3

4

5

6

7

8

9

5.25.55.5

6.7

7.7

8.4 8.5

7.9

7.2

(% o

f G

DP

)

• Euro zone crisis primarily a result of wrong macroeconomic policies

• European authorities will probably resolve current crisis with bigger EFSF or other rescue mechanisms, interventions in bond markets, bank bailouts, even Greek debt restructuring

Conclusion

• But continued wrong macroeconomic policies will cause unnecessary unemployment and suffering; cuts to health care, pensions, education; trillions of dollars in lost output, and possibly more crises

Conclusion