Embed Size (px)

Citation preview

THE EFFECT OF CAPITAL STRUCTURE ON PERFORMANCE OF BANKS IN GHANA

KWAME NKRUMAH UNIVERSITY OF SCIENCE AND TECHNOLOGY, KUMASI.

SCHOOL OF BUSINESS

By

ANAMAN MARGARET DANSOA

A Thesis Submitted to the School of Business,

Kwame Nkrumah University of Science and Technology in Partial Fulfillment of the Requirements for

the Degree

Of

MASTER OF BUSINESS ADMINISTRATION

June, 2011

i

ABSTRACT

This study aims to find the impact of the capital structure on performance of banks in Ghana.

Existing literatures conclude that, capital structure of a firm has impact on the performance of the

firm. The study uses ROE as performance indicator; the researcher employs the uses of

correlation analysis by using the Pearson correlation coefficient to find the multicollinearity

among the variables used. Regression analysis was use to find the impact or the contribution of

each of the variables used. It was found that banks in Ghana uses leverage in its financing and

was noted that, banks in Ghana operates above its minimum requirements stated by the bank. It

became evidently known through the analysis that, short term debt contributes higher to the

performance of banks. the higher the short term debt of the bank, the higher its performance.

However long term debt financing was also recorded to have a positive impact on the

profitability of the bank even though it is minimal. Moreover, the findings show that, assets held

by banks increase its profitability if managed efficiently. The research is aimed to be added to

the existing literature on the capital structure and performance.

ii

DECLARATION

I hereby declare that this submission is my own work towards the award of master of Business

Administration and that to the best of my knowledge it contains no material previously published

by another person nor material which has been accepted for the award of any other degree of the

University except where due acknowledgement has been made in the text.

ANAMAN MARGARET DANSOA ------------------------------ ----------------

Signature Date

MR, NEWLOVE G. ASAMOAH ------------------------------ ----------------

(Supervisor) Signature Date

------------------------------- ------------------------------ ----------------

Head of Department Signature Date

iii

DEDICATION

This project is dedicated to my parents, siblings and friends for their love and care throughout

this course.

iv

ACKNOWLEDGEMENT

I express my profound gratitude to the Almighty God for seeing me through this course. I would

also like express special appreciation to my supervisor, Mr. Newlove G. Asamoah for his

penetrating criticism, guidance, and unceasing assistance in every aspect of my work.

Recognition is given to all the academic facilitators who taught me during the two years master’s

program.

I also thank Price water house coopers for their help in gathering my data for this project.

v

Table of Contents

ABSTRACT………………………………………………………………………………………………………………...iiDECLARATION........................................................................................................................iii

DEDICATION............................................................................................................................iv

ACKNOWLEDGEMENT...........................................................................................................v

Table of Contents........................................................................................................................vi

LIST OF TABLES......................................................................................................................ix

CHAPTER ONE INTRODUCTION.......................................................................................1

1.2 Problem Statement.................................................................................................................3

1.3 Objectives of the Study..........................................................................................................4

1.4. Research Questions...............................................................................................................5

1.5 Justification of the Study........................................................................................................5

1.6 Scope of the study..................................................................................................................6

1.7 Overview of the Research Methodology...............................................................................7

1.8 Organisation of the Study......................................................................................................7

1.9 Limitations of the Study.........................................................................................................8

CHAPTER TWO LITERATURE REVIEW..........................................................................9

Introduction..................................................................................................................................9

2.1 Performance Theory...............................................................................................................9

2.2 Capital structure theory........................................................................................................11

2.2.1 Static Trade-Off Theory....................................................................................................11

2.2.2 Agency Cost Theory.........................................................................................................14

2.2.3 Information Asymmetry Theory.......................................................................................15

2.2.4 Capital Structure Life Stage Theory and Performance.....................................................16

2.2.5 Pecking Order Theory.......................................................................................................17

2.3 Strategic Management Research and Capital Structure.......................................................18

vi

2.4 Overview of the banking industry in Ghana........................................................................21

2.4.1 Recent Developments, Structure and Regulation............................................................24

CHAPTER THREE METHODOLOGY...............................................................................26

Introduction................................................................................................................................26

3.1 The Research Paradigm.......................................................................................................26

3.2 The Research Method..........................................................................................................27

3.2.1 The Study Population........................................................................................................27

3.2.2 Sampling Techniques........................................................................................................27

3.2.3 Sample Size.......................................................................................................................27

3.2.4 Data Source and Collection Method.................................................................................28

3.3 Data Analysis.......................................................................................................................28

3.4 Proposed Model Used for the Study....................................................................................29

3.4.1 The proposed model is outlined below.............................................................................29

3.4.2 Research Variables............................................................................................................30

3.4.3 Variables Rationalization..................................................................................................31

3.4.4 Predictor or Explanatory Variables...................................................................................31

3.4.5 Control Variables..............................................................................................................32

3.5 Hausman Specification Test.................................................................................................34

3.6 Pearson Correlation Coefficients.........................................................................................35

CHAPTER FOUR DATA PRESENTATION, ANALYSIS AND DICUSSIONS..............36

Introduction................................................................................................................................36

4.1 Descriptive Statistics............................................................................................................36

4.2 Pearson Correlation Analysis...............................................................................................38

4.3 Regression Results from Stata 10 Output............................................................................41

4.3.1 Discussions from Model One on Bank Performance, Bank Capital and the Control Variables....................................................................................................................................43

4.3.2 Discussions on Model Two on Bank Performance, Short – term Debt and Control Variables....................................................................................................................................47

4.3.3 Discussions of Mode Three on Bank Performance, Long-term Debt and the Control Variables....................................................................................................................................50

vii

4.3.3 Discussions of Model Four on Bank Performance, Total Debt and the Control Variables....................................................................................................................................................53

CHAPTER FIVE FINDINGS, CONCLUSIONS AND RECOMMENDATIONS............54

Introduction................................................................................................................................54

5.1 Findings................................................................................................................................54

5.1.1 Key findings......................................................................................................................54

5.2 Conclusions..........................................................................................................................56

5.3 Recommendations................................................................................................................56

References..................................................................................................................................58

viii

LIST OF TABLES

Table 4.1 Descriptive Statistics of Variables …………………………………………………38

Table 4.2: Pearson Correlation Coefficients ………………………………………………….39

Table 4.3A: Regression Result for Model One, with Total Assets …………………………..41

Table 4.3B: Regression Result for Model One, with Loans and Investments ……………….42

Table 4.4A: Regression Result for Model Two, with Total Assets ………………………….45

Table 4.4B: Regression Result for Model Two, with Loans and Investments ………………46

Table 4.5A: Regression Result for Model Three, with Total Assets ………………………..48

Table 4.5B: Regression Result for Model One, with Loans and Investments ………………49

Table 4.6A: Regression Result for Model Four, with Total Assets …………………………51

Table 4.6B: Regression Result for Model Four, with Loans and Investments ……………..52

ix

CHAPTER ONE

INTRODUCTION

1.1 Background Study

A firm’s performance is very important for different groups of people. All agents that have made

financial decisions about companies were concerned with its financial position and its

performance. Thus, owners, managers, potential investors, banks, other financial institutions,

creditors, business partners, employees, and government had been interested in the capital

structure of the company in order to analyse and predict its performance. Much of the ground-

breaking work in the field of corporate finance focused on why firms chose differing proportions

of debt and equity to finance their operations. Perhaps the most famous work in this field was the

arbitrage argument of Modigliani and Miller (1958) which spawned a flood of research in the

area of capital structure.

Most capital structure researches have been concentrated on the search for an optimal capital

structure. Three main theories have been subsequently advanced: Pecking Order (POH), Agency

Cost (ATF) and Static Trade-off (tax based). Pecking order theory ( information asymmetry

theory) states that firms prefer to finance new investment, first from internally with retained

earnings , then with debt , and finally with an issue of new equity (Myers,1984). The agency cost

of capital structure states that an optimal capital structure will be determined by minimizing the

cost arising from conflict between the parties involved. Even in the absence of agency problems

the presence of asymmetric information may cause firms to under invest – which in itself is a

source of inefficiency (Myers and Majluf 1984). The existence of asymmetric information is the

root cause of these inefficiencies (Brooks and Davidson, 2003).

1

Five major sub-theories within capital structure theory which attempt to explain why capital

structure matters and how it contributed to the overall value of the firm have emerged, however,

none of the researches had proved conclusive (Myers, 2001). One of the five sub-theories

proposed that capital structure may be influenced by the organisational life stage of a firm, as

financing needs change with the changing circumstances of the firm (Damodaran, 2001; Bender

& Ward, 1993). However, capital structure theory and performance theory are generally

approached in isolation. Capital structure research has typically been carried out by researchers

with a background in corporate finance or economics, while performance has evolved out of

research in the field of strategic management.

While the link between capital structure and performance has been suggested by researchers on

the periphery of both fields, it appears never to have been directly tested.

Lizal (2002) states three reasons of firm’s failure: wrong asset and capital structure, wrong

financial structure, corporate governance problems. According to the neoclassical approach

liquidation is an instrument for reallocation of resources from inefficient to efficient use. By

going liquidation a firm frees the wrongly allocated resources for their more efficient use within

the same or even another industry. These come as a result of low performances of the firms.

Another reason for firm’s liquidation may be wrong financial structure, even if the asset structure

is appropriate. This means that firm goes bankrupt in the short run, even though it would

survive in the long run the quality of the capital markets is important in this case as

they could provide some support for temporarily financially constrained firms. There is also

a corporate governance problem, which often leads to liquidation, but changing the management

of the firm would be a better solution in such case. Creditors (banks, different financial

2

institutions, business partners, suppliers) are interested in predicting performance of the

company as a means of risk management. They should be able to evaluate the credit quality of

the company in order to adjust the contracts and create the appropriate reserves.

1.2 Problem Statement

The argument pertaining to the relationship of firms performance and capital structure has been

a subject of discussion of late among professionals in the financial markets since the work of

Miller (1958). Locally, various research have been made towards the finding of the optimal

capital structure and its determinants (Amidu, 2007, Boateng 2004 and Abor and Biekpe, 2004),

role of debt in Balance sheets (Aboagye, 1996), capital structure and firm’s performance (Abor,

2005 and Kyereboa-Coleman, 2007) of which these also capitalized on the optimal capital

structure. Of all these researchers only Kyereboa (2007) took into consideration the performance

of banks, yet this study takes a different look from that of Kyereboa-Coleman.

Kyereboah-Coleman (2007) sought to investigate the impact of capital structure on the

performance of microfinance institutions in Ghana and Amidu (2007) who was interested in the

determinants of capital structure of Banks in Ghana. Abor (2005) whose work actually

investigated the relationship between capital structure and profitability of listed firms on the

Ghana Stock Exchange (GSE) and;. The difference that this study sought to brings is on the basis

of the objectives as Kyereboah-Coleman (2007), limited the study to only micro-finance

institutions in Ghana and therefore did not include banks whereas this study looks at banks only,

moreover, Abor (2005), study was too broad to be applicable to the unique

3

characteristics of banks and also did not include unlisted banks. However, Amidu (2007) did not

look at the relationship between capital structure and bank performance but rather the

determinants of bank capital structure

Issues such as corporate governance, agency cost, and capital structure also play important role

because of the crucial roles played by banks in providing credit to non-financial firms, in

transmitting the effects of monetary policy, and in providing stability to the economy as a whole

( Pratomo and Ismail, 2006). These have placed strong emphasis on the need to study the

relationship between capital structure and bank performance. The researcher’s attention,

however, shall be concentrated on differences across banks and not between banks and other

firms, since banks in the proposed sample are subject to essentially equal regulatory capital and

other constraints.

1.3 Objectives of the Study

This general objective of the study is to find the correlation between capital structure and

performance of banks in Ghana, with the specific objectives being:

1. To find the leverage of Banks in Ghana, and to know whether they use more short term debt as

long term debt financing.

2. To know whether the banks operate above or below the required minimum capital adequacy

ratio

3. To examine the nature of capital structure of Banks in Ghana;

4. To examine the effect of debt financing on the performance of banks in Ghana

5. To find the effect of the total value of the bank assets to profitability

6. The association between the bank’s risk and performance

4

Hypothesis

Ho: Profitability of banks has no relationship with its capital structure.

Ha: Profitability of banks has a relationship with its capital structure

.

1.4. Research Questions

This study sought to answer the following questions to achieve the goal and objectives of the

study.

1. What is the leverage mainly used by Banks in Ghana, and does the banks use short term debt

as long term debt financing?

2. Does banks in Ghana operate below or above the required minimum capital adequacy ratio set

by the central bank?

3. What is the nature of capital structure of banks in Ghana?

4. What effects does debt financing have on performance of banks in Ghana?

5. What effect does the total value of the bank assets have on profitability?

6. Is there an association between the bank’s risk and performance?

1.5 Justification of the Study

This research provide in depth information about the behavior of capital structure and

performance of a firm as it exists today on some selected banks in the banking industry in Ghana.

As a result of the discoveries of crude oil in Ghana, it is becoming imperative that, the sector

needs huge financial inflows to invest in these areas, however, the participation of a financial

5

companies depend on the capital structure and agency cost associated with the firms and its

influences on the performance of the firm. Internal funds plays a major role in financing the

sector, nevertheless, most investors assess the performance and the capital structure of the bank

in order to assigned a contract to it due to the fact that these areas needs a huge financial capital

In addition to the above, these banks as a result of increasing their financial base to place itself in

a strategic level in order to attract foreign and local investors, capital structure and performance

have become the tool use to assess these banks as it serves as the bench mark one will used to

asses the bank to draw conclusion whether the bank has a strong capital base to support such

huge investment or not.. Thus, assessment can be based on the firms debt financing method and

its eventual effects on the performance, capital structure plays a major role for most investors

and the general banking industry to asses its performance and to know if these have a

relationship.

Capital structure and performance of a firm will play an important role to determine the healthy

of a firm that will help investors and financial educators to know the trend and stand of a

particular firm in order to attract investors. This will have an impact on the local economy if

local banks will have the needed capital to invest in this major sector of the economy of which

banks capital structure and its performance will be the sole indicator to choose which entity and

medium will be appropriate for financing.

1.6 Scope of the study

The study was conducted within the framework of the effect of capital structure on performance

of banks in Ghana. The study was carried out on selected banks who have been in operation as at

2004 and having annual report from 2004-2010, within the commercial banking license of the

6

central bank for operation. This study is not a case study approach of one particular bank;

however, it covers all other players in the banking industry to reflect in the entire industry

response to the effect of capital structure on their performance. Hence the result would be

generalized and placed in the relevant context of the performance of banks in Ghana.

1.7 Summary of Methodology

The study concentrates on the performance of some selected banks in Ghana by considering their

capital The research looks at the activities of the selected banks performances over the past five

years because it is listed on the Ghanaian stock exchange, privately owned and some have

operated for over eight years, which makes it unique. Secondary data were gathered from the

banks website as well as the Price Water-coopers to aid as a check up of figures and to ensure the

validity of these data, since the data are numeric in value, quantitative techniques were applied.

Descriptive statistics were employed to make inferences and scientific judgment on data.

Statistical analysis such as the correlation matrix and the multi variable regression models were

applied to obtained the needed results as being extensively explained in chapter three.

1.8 Organisation of the Study

The study has five chapters. Chapter one deals with the introduction of the study area. Which

comprises the background of the study, problem statement, significance. Goal and objectives,

research questions methodology, limitations and organization of the study.

7

Chapter two captures the review of relevant literature to the study. The third chapter of the study

presents detailed methodology that was used in this study.

Chapter four contains data presentation, analysis and discussion whilst the final chapter

concludes the summary of major findings, recommendations and conclusion.

1.9 Limitations of the Study

The researcher was constrained by time and financial resources and could not therefore apply

other methods of data collection aside the information on the internet and from the banks. Most

of the staff and senior managers these companies were always busy attending to customers which

make it very difficult to solicit information from them. Some of these information were sourced

from branch offices in Kumasi and their head office in Accra as well as the firm’s websites this

brought additional cost to the researcher as the researcher travelled up and down to Accra for

information.

8

CHAPTER TWO

LITERATURE REVIEW

Introduction

There has been a great deal of research into both organizational performance and capital

structure theory, but relatively little into how the two theories may relate to one another. In order

to lay a theoretical framework for our study, we review performance theory and capital structure

theory literature independently. We also explore how and why existing research suggests that

there might be a link between the two ideas.

2.1 Performance Theory

The pioneer modern theory of capital structure of a company and its relation to performance

began with the paper of Modigliani and Miller (1958). They prove that the choice of between

debt and equity financing in order to increase performance had no material effects on the value

of firm or on the cost of availability. Since, then, various studies have been directed to explore

the optimal capital structure in the absence of Modigliani-Miller’s assumption. Jensen and

Meckling (1976), for example, argue that an optimal capital structure can be obtained by trading

off the agency cost of debt against the benefit of debt to raise performance. The implication of

this argument is that firms, which have fewer opportunities for asset substitution such as banks

and mature firms, will have higher debt levels and eventually will affects its performances,

ceteris paribus. Moreover, firms which have plenty of cash inflows but have a slow growth

should have more debt. Large cash inflows without investment prospects create the resources to

consume perquisites, build empires, overpay subordinates, etc. Increasing debt reduces amount

9

of cash flows and increases manager fractional ownership of the residual claim. Jensen (1989)

predicts that the firms that have optimal capital structure should be characterized by high

leverage to aid it to perform creditably.

Previous study by Myers (1977) finds that higher leverage can mitigate conflict between

shareholders and manager concerning the choice of investment and the eventual performance of

the company. For firms that need to finance a new investment, Myers (1984) recommends using

a low risk debt than increasing equity. The reason is that if there is an asymmetric information

where investor is less well-informed than current firm insiders about the value of firm’s assets,

then it leads to a mis-priced of equity in the market. Investors do not believe on the new

profitable project and make the security is so severely undervalued.

Berger (2002) supports Myer’s argument. He argues that increasing the leverage ratio should

result in lower agency costs of outside equity and improve firm performance, all else held

constant. He suggests that under the efficiency risk hypothesis, more efficient firms choose lower

equity ratio than other firms, because higher efficiency reduce the expected costs of liquidation

and the financial distress. Higher profit efficiency may create a higher expected return for a

certain capital structure and a corresponding higher performance, and this condition does not

protect firms against future crises. Profit efficiency is strongly positively correlated with

expected return and higher expected return is substituted for equity capital to manage risks.

The empirical studies on those relationship have been conducted, among others are Titman and

Wessel (1988), Mester (1993), Pi and Timme (1993), Gorton and Rosen (1995), Mehran (1995),

McConnell and Servaes (1995) DeYoung, Spong and Sullivan (2001). Although these empirical

literatures have been successful in the sense that many of the capital structure plus some control

variables are correlated with firms’ performance.

10

Banks in the sample are subject to essentially equal regulatory constraints, and we focus on

differences across banks, not between banks and other firms. Most banks are well above the

regulatory capital minimums, and our results are based primarily on differences at the margin,

rather than the effects of regulation.

2.2 Capital structure theory

‘One of the most contentious issues in the theory of finance during the past quarter century has

been the theory of capital structure’ (Bradley et al, 1984). Even Stewart Myers, one of the

foremost researchers in the field, concluded, as recently as 2001, that ‘there is no universal

theory of the debt-equity choice, and no reason to expect one’ (Myers, 2001).

While there may be a lack of consensus on exactly what drives the capital structure decision,

there is no lack of alternative hypotheses. One of these theories, capital structure performance

theory, is conspicuously underdeveloped. Although mentioned in text-books (Damodaran, 2001),

mentioned obliquely in some research (Morgan & Abetti, 2004), and even referred to in the

development of some of the other major theories (Myers, 2001), the idea that the capital structure

of a firm may be related to its performance, appears to have received very little direct theoretical

or empirical examination. We now briefly review the capital structure theories.

2.2.1 Static Trade-Off Theory

The debate about how and why firms choose their capital structure began in 1958 (Myers, 2001),

when Modigliani and Miller (1958) published their famous arbitrage argument showing that ‘the

market value of any firm is independent of its capital structure’. Based on Modigliani and

11

Miller’s value invariance theory, we would not expect capital structure to vary from firm to firm,

or over the performance of a single firm. But the theory was developed under a ‘deliberately

artificial set of conditions’ (Barclay et al, 1995) of no information costs, no personal or corporate

taxes, no contracting or transaction costs, and a fixed investment policy. Unravelling Modigliani

and Miller’s assumptions introduce us to the other major capital structure theories. The

introduction of taxation effects implies that firms should, theoretically, seek to increase their debt

levels in order to increase performance as far as possible (Miller, 1988). However other theorists

(Stiglitz, 1974) added limitations to the optimal level of firm debt by arguing that liquidation

costs increase as the firm’s level of debt increases, and this places an upper limit on the amount

of debt that should be present in a firm’s capital structure. This evolved into the static trade-off

theory, which proposes that firms attempt to achieve an optimal capital structure that maximises

the value of the firm by balancing the tax benefits, with the liquidation costs, associated with

increasing levels of debt (Myers, 1984). Some researchers have identified problem areas in the

ability of static trade-off theory to explain actual firm behavior and its performance. Myers

(2001) argued that static trade-off theory implies that highly performed profitable firms should

have high debt ratios in order to shield their large profits from taxation, whereas in reality, highly

profitable firms tend to have less debt than less profitable firms.

Warner (1977) suggested that liquidation costs are much lower than the tax advantages of debt,

implying much higher debt levels than predicted by the theory. There is, however, also some

empirical evidence and theoretical support for the idea that firms – at least in part –construct

their capital structure to take advantage of the interest tax shield (net of the interest tax burden to

investors), while ensuring that they avoid incurring excessively high financial distress costs for

the sake of performance. Kayhan and Titman (2004) found that, over the long term, firms do

12

tend to move towards target debt ratios consistent with the theory to build a formidable capital

structure and to improve performance. Static trade-off theory therefore offers one possible

explanation of how firms choose their capital structure. It also provides some important support

for capital structure theory and performance.

Warner (1977) found that the ratio of ‘the value of direct liquidation costs to the market value of

the firm appears to fall as the value of the firm increases due to a higher performance, a view that

has also found support from Esperenca (Esperenca et al, 2003). We might expect, therefore, to

see liquidation costs reducing in importance as firms grow and develop, resulting in higher

optimal debt ratios and higher levels of debt in larger, more mature firms and higher

performance.

Opler and Titman’s (1994) study of indirect performances of banks using liquidation costs

among retailers suggested that firms in the infancy, and adolescence life stages should have

lower debt levels than firms in later life stages, as their liquidation costs are higher due to lower

performances associated with them. It has also been argued that ‘optimal firm leverage is related

inversely to the variability of firm earnings’ (Bradley et al., 1984), which suggests that prime and

stable firms, with more predictable earnings streams, should have higher debt ratios than

younger, less predictable firms. Graham (2000) found that firms with unique products, low asset

collateral or large future growth opportunities – in other words, firms at early stages of

development (infancy to adolescence) – tend to have lower levels of debt than firms in the stable

or aristocracy life stages.

In summary, static trade-off theory suggests that firms in infancy, go-go and adolescence cannot

afford debt as their liquidation costs are high, and their earnings are too low to use the tax benefit

of increasing interest payments. In the prime and stable stages, the larger, more predictable

13

earnings makes the tax shield advantage of debt more beneficial. Liquidation costs are also

smaller in the prime and stable life stages. In the stages from aristocracy to death, firms are likely

to experience a decrease in earnings (and hence a decrease in the tax shield benefit of debt) and

as a result might be inclined to use less debt.

Static trade-off theory thus suggests that the proportion of debt in a firm’s capital structure

should follow a low-high-low pattern over the firm’s life stages to enhance performance over the

various stages.

2.2.2 Agency Cost Theory

There is also another argument for how capital structure may be predisposed by symmetries

between managers and investors. Not only do managers have diverse information about the

prospects of the firm than shareholders do, but managers also have interests that diverge from

those of shareholders. Agency costs are a good reason for firms to increase the amount of debt in

their capital structure since it has a direct relationship with the performance of a company, as

debt ‘enables managers to bond their promise to pay out future cash flows’ (Jensen, 1986).

According to agency cost theory, firms use more debt in their capital structure when investors

seek to pressure management to use funds efficiently. Fosberg (2004) found that the debt ratio

decreases as agency costs decrease because of an increasing proportion of ownership by

management, and that those firms with fewer shareholders have more debt than firms with many

shareholders. The link between fewer shareholders and more debt suggests that shareholders,

who are able to influence capital structure in their favour, do so in a way that increases the level

of debt.

14

Jensen (1986) argued that agency costs are especially severe ‘when the organisation generates

substantial free cash flow’, and that the control function of debt is most important in old,

declining organisations that actually need to shrink. In the context of the Adizes life stage model

this suggests that firms in the prime, stable, aristocracy, recrimination and bureaucracy life stages

should take on more debt to control agency costs which will ultimately leads to higher

performance.

Jensen also argued that debt is less effective in reducing agency costs in rapidly growing

organisations with ‘large and highly profitable investment projects but no free cash flow’ . The

firm with the lowest agency costs is, by definition, the one that is run by its owner (Ang et al,

2000) and therefore one would expect start-up firms (the infancy, go-go and adolescence life

stages) that are run by the entrepreneur to have the least debt and higher performance.

The agency cost argument therefore also offers support for capital structure theory. This time,

however, the pattern of the relationship pattern is low-high-high. In terms of agency cost theory,

we would expect young owner managed firms to have the least debt, and that debt levels will

gradually increase as the firm develops and acquires a greater number of shareholders and more

professional managers.

2.2.3 Information Asymmetry Theory

Stephen Ross developed the information asymmetry theory of capital structure by removing

another assumption underlying Modigliani and Miller’s value invariance theory, namely that ‘the

market possesses full information about the its performance and funding activities of firms’

(Ross, 1977). If instead we assume that managers possess information about the firm’s future

15

prospects that the market does not have, then managers’ choice of a capital structure may signal

some of this information to the market (Ross, 1977). Increasing leverage, he reasoned, would

signal to the market that the firm’s managers are confident about being able to pay interest in

future, and hence are confident about future earnings prospects and performance. Increasing

leverage would, therefore, increase the value of the firm by signalling to investors the size and

stability of future cash flows (Ross, 1977). Fama and French (1988), on the other hand,

countered by pointing to the fact that more profitable firms which are associated with higher

performances tend to have lower levels of debt. They argued that increasing debt actually signals

poor prospects for future earnings and cash flow as there will be less internal financing available

to fund development. Therefore, while it has been argued that information asymmetries decrease

over the lifetime of a firm (Baeyens & Manigaart, 2003), there is insufficient clarity on exactly

how signalling, within the context of information asymmetries, affects capital structure

decisions. We cannot, therefore, look directly to information asymmetries, and how they change

over time, as an explanation of why capital structure might change over a firm’s periods of

operation to increase performance.

2.2.4 Capital Structure Life Stage Theory and Performance

Some theorists have approached the problem of how organisational life stage relates to capital

structure. Bender and Ward (1993) focused on the trade-off between business risk and financial

risk, positing that business risk reduces and performance increases over the life stages of a firm,

allowing financial risk to increase. (Opler et al, 2001) offered a similar view, stating that ‘firms

should use relatively more debt to finance assets in place and relatively more equity to finance

growth opportunities’, and should, therefore, use progressively more debt in their financing mix

16

as they mature. This is supported by Damodaran (2001) who proposed that expanding and high-

growth firms would finance themselves primarily with equity, while mature firms would replace

equity with debt. Capital structure life stage theory would seem to suggest, therefore, that debt

ratios should increase as the firm progress and performance through the early life stages. From

an empirical point of view, however, little work has been done to support or refute this idea.

Most of the evidence for and against appears in the context of other arguments. In their analysis

of the venture-capital financing of biotech ventures, for example, Morgan and Abetti (2004)

argued that high technology ventures are so risky that they can only be financed by ‘venture

capital and private equity sources’, a view that supports the theory that riskier firms in the

infancy, adolescence and go-go life stages should use more equity. There has been little research

focusing directly on capital structure life stage theory and its performance, but the little there is

suggests, in line with static trade-off theory, that debt ratios should follow a low-high- low

pattern over the firm’s life. Firms in infancy, go-go and adolescence have a high business risk

and cannot afford financial risk, while firms in prime and stable can afford the extra risk that

accompanies debt financing. Firms in the declining life stages would again experience a growth

in business risk and would need to decrease their exposure to debt.

2.2.5 Pecking Order Theory

Myers observed how firms actually structure their balance sheets, and found that firms tend to

follow a ‘pecking order’ in financing their projects: first they use internal equity, then debt, and

only then do they use external equity (Myers, 1984). In contrast to Ross (1977), who argued that

firms use more debt to overcome information asymmetries and signal better prospects, Myers

(2001) used information asymmetries to argue that managers are unlikely to issue equity because

17

they fear it will signal that the stock price is overvalued. In addition to the evidence presented by

Myers, several other studies have lent support to pecking order theory. For example Allen

(1993), like Fama and French (1988 ), found that leverage is inversely related to profitability and

performance, which supports the pecking order theory view that debt is only issued when there is

insufficient retained income to finance investment.

According to the pecking order theory, we might expect firms in infancy, adolescence and go-go,

with little retained earnings, to seek the maximum available debt funding before resorting to

external equity. Prime and stable firms, in contrast, generate substantial retained earnings and

therefore need less debt than they did in their high-growth phase. As they move into the stages of

decline, retained earnings will decrease and firms again will increase their debt levels to finance

acquisitions of young firms. Pecking order theory, therefore, also suggests a strong relationship

between life stage performance and capital structure. In contrast to static trade-off theory,

however, pecking order theory suggests a high-low-high pattern of debt ratio over time.

2.3 Strategic Management Research and Capital Structure

A firm’s capital structure refers to the mix of its financial liabilities. As financial capital is an

uncertain but critical resource for all firms, suppliers of finance are able to exert control over

firms . Debt and equity are the two major classes of liabilities, with debt holders and equity

holders representing the two types of investors in the firm. Each of these is associated with

different levels of risk, benefits, control and performance. While debt holders exert lower

control, they earn a fixed rate of return and are protected by contractual obligations with respect

18

to their investment. Equity holders are the residual claimants, bearing most of the risk, and,

correspondingly, have greater control over decisions.

Questions related to the choice of financing have increasingly gained importance in management

research as it has a bare relationship with performance. Traditionally examined in the discipline

of finance, these issues have gained relevance in the past few years, with researchers examining

linkages to strategy and strategic outcomes. Bettis (1983) argued that modern capital structure

theory and strategic management are based on very different paradigms, resulting in opposing

conclusions. He called for more integrative research to resolve the controversies. Strategic

management scholars exhibit disparate opinions regarding the possibility of such integration into

capital structure. Oviatt (1984) suggested that a theoretical integration between the two

disciplines is indeed possible as more and more re structuring of capital within a firm has a

significant impact on performance. In contrast, Bromiley (1990) believed that the scope for

integration is limited, if at all possible. According to him, capital structure strategy should

neither import empirical results from finance, nor should they work towards integration of

strategic and financial research. Therefore, while strategy should expand its domain to study

areas traditionally considered in finance to increase performance, researchers should be careful

to maintain a strategic Perspective on how capital structure should be integrated.

Some management researchers have viewed capital structure decisions as arising from the

preferences of various stakeholders such as managers (Barton et al, 1987,88), board of directors (Stearns

et al 1993) and institutional investors (Chaganti et al, 1999). Other researchers have viewed capital

structure as an antecedent to firm strategy, such as diversification into new businesses with

19

prime issue on performance (Chatterjee,1990, 91). While these studies have definitely

contributed to some understanding of the linkages between performance and capital structure,

Does it matter how firms finance their assets? and do different modes of financing make a

difference?

While anecdotal evidence suggests that the amount and type of financing should be closely tied

to a firm’s strategy and its previous performance (Gupta et al, 1995) few researchers have looked

at the strategy/financing interaction (Sandberg et al, 1987). A firm consists of a bundle of

resources, some of them able to contribute to sustainable competitive advantage (Penrose, 1959).

The financial management function of a firm - including its capital structure decision - deals with

the management of the sources and uses of finances. Firms enter into transactions with suppliers

of finance raising capital for strategic assets.

The different types of financing, however, are also associated with different levels of costs as

these affects capital structure.

This paper suggests that the efficient set of transactions, as indicated by an optimal debt-to-

equity ratio, is determined by the nature of strategic assets in the firm. Therefore, those firms that

succeed in setting up the efficient set of transactions will be able to realize the full value of these

assets. On the other hand, firms that are not able to determine and/or organize their transactions

efficiently (as per asset requirements) will suffer a decline in performance. This decline arises

from a decrease in the net benefits available from strategic assets. Consequently, superior

financial management matching capital structure to resources can provide a firm added benefit

over its competitors.

20

2.4 Overview of the banking industry in Ghana

Banking in Ghana started in 1896. In that year, a branch of the Bank of British West Africa

(BBWA) was opened in Accra and in the Gold Coast (now known as Ghana). Shortly after the

Bank was established, it was able to acquire the business of maintaining the Government

accounts. In addition, it was able to introduce the use of cheques in settlement of Government

accounts which helped to advertise the usefulness of the Bank to the public (Buckle et al (1999).

Buckle stated that, by 1918, the operations of BBWA in the Gold Coast had been so successful

that another expatriate bank, the Colonial Bank decided to commence banking. In 1925 the

Colonial Bank merged with the Anglo-Egyptian Bank, the National Bank of South Africa and

Barclays Bank under the leadership and name of Barclays Bank (Dominion Colonial and

Overseas). Barclays soon developed into a strong competitor of BBWA. From the late 1920s

until the early 1950s, banking services in the Gold Coast continued to be exclusively provided by

these two expatriate banks. Branches were opened in many of the provincial capital towns and in

the main trading centres in the Gold Coast Colony, and, subsequently, in Ashanti and the

Northern Territories of the Gold Coast.

The Bank of Gold Coast Ordinance was passed by the legislature in October 1952. Sir Cecil

Trevor’s report (1952) outlines the business that the bank may be authorised to carry, generally

in line with any typical commercial bank as follows:

The accepting of money on deposit, either with or without interest, from and the

collection of money for the Government, local authorities, banks and any other persons;

purchase and sale of foreign exchange;

21

the making of loans and advances payable on demand or on expiry of fixed period not

exceeding six months against certain specified securities (i.e. stocks, gold, silver etc);

the issue of demand drafts made payable at its own offices or agencies;

the purchase and sale of securities;

the purchase, sale and rediscount of bills of exchange and promissory notes bearing two

or more good signatures and maturing within six months from the date of such purchase

of rediscount; or within nine months in the case of bills for the purpose of financing

seasonal agricultural operations or the marketing of crops;

the acting as agent for the Government and local authorities or any other persons and;

the acting as agent or correspondent of a bank incorporated in any country outside the

Gold Coast.

In 1953 the Bank of the Gold Coast was set up by the Government and Alfred Engleston,

formerly of the Bank of England. Eventually the Bank was split into two: the Bank of Ghana,

operating as a bank of issue, to be developed into a complete central bank; and the Ghana

Commercial Bank, to be developed into the largest commercial bank with a monopoly on the

accounts of public corporations. In July 1957, Alfred Engleston was appointed as the first

Governor of the Bank of Ghana (Buckle et al, 1999). Sowa (2005) indicated that after

independence, a number of banks were established to fulfill certain developmental goals of the

new State. Thus, the National Investment Bank (NIB) which started operations in 1964 was

charged with the main object of assisting Ghanaian entrepreneurs in the establishment and

expansion of their enterprises. The Agricultural Development Bank (ADB) which originally was

part of the Bank of Ghana Rural Credit Unit was formed in 1965 with the aim of reaching

smallscale farmers. The third development, the Bank for Housing and Construction (BHC), was

22

established by the state in 1972 to cater for the building and construction industry. It is important

to note that the period of the establishment of these banks coincided with the “controlled regime”

when the State arrogated to itself the power to make all economic decisions and allocations, to

the exclusion of the private sector.

By the late 1980s, the banks had suffered substantial losses from a number of bad loans in their

portfolios. In addition, cedi depreciation had raised the banks' external liabilities. In order to

strengthen the banking sector, the government in 1988 initiated comprehensive reforms. In

regulatory framework, and gradually improved resource mobilization and credit allocation. In

1992 the Government began to privatise, what has for some time been regarded as the flagship in

banking, the Ghana Commercial Bank; and in 1994 took steps to divest itself of most of its

interests in the Social Security Bank.

The liquidation of Bank for Housing and Construction and Ghana Co-operative Bank in January

2000 and the collapse of Bank for Credit and Commerce in June 2000 called for pragmatic

approaches in capital adequacy, including holding a capital buffer of sufficient size, enough

liquid assets, and engaging in efficient risk management (Amidu, 2007). A critical analysis of

some selected banks revealed that Bank for Housing and Construction (BHC) and the Ghana

Cooperative Bank (COOP) showed signs of liquidity crunch before their liquidation. On

profitability, these banks showed abysmally poor performance while their capital structure ratios

did not favour these banks either (BoG, Financial Markets Department, 2000). These led to the

enactment of the following Acts: Bank of Ghana Act 2002, Act 612; Banking Act 2004, Act 673

and its subsequent amendments in 2007.

23

2.4.1 Recent Developments, Structure and Regulation

Some of the significant changes in banking regulations in Ghana in the past two years include the

Banking (Amendment) Act 2007, Act 738 which was enacted, introducing three types of banking

licenses; General Banking License (for universal and off-shore banking ),Class 1 Banking

License (for universal banking ) and class 2 Banking License ( for off-shore banking). The Credit

Reporting Act 2007 (Act 746) and Anti-Money Laundering Act, 2007 (Act 749). BoG also

proposed to increase the minimum capital requirement of banks from GHC 7 million to a range

of between GHC 50-60 million (BoG, 2007). This is to propel economic growth for the country

particular, the amended banking law of August 1989 required banks to maintain a minimum

capital base equivalent to 6 percent of net assets adjusted for risk and to establish uniform

accounting and auditing standards. The law also introduced limits on risk exposure to single

borrowers and sectors. These measures strengthened central bank supervision, improved them to

achieve a middle income status.

Time table for full compliance is given by BoG as follows:

End of 2009 for banks with majority foreign shareholdings (foreign banks); and

End of 2012 for banks with majority Ghanaian shareholdings (local banks).

The abolition of the 15% secondary reserve ( in August , 2006) requirements of banks and the

reduction of governments overall domestic debt-to-GDP from 29% (2002) to 10.1% (2006) and

reduction in the prime rate 24.5% (2002) to 12.5% (2006) also allowed banks to have more

money for private sector freed up significant liquidity for lending to businesses. The National

reconstruction Levy, which ranged between 2.5% to 5% of profit before tax was abolished at the

end of 2006 (The Ghana Banking survey, 2007). Total Domestic Credit for the period under

review rose from GHC635.40 million (in 1999) to GHC 7,290.3 million (in 2008) (ISSER,

24

2009). Some other recent improvements in the Banking industry include the introduction of the

e-zwitch, Automated Cheque codeline clearing system and the supervision of the redenomination

of the cedi.

The total number of major banks as at 2007 stood at 23. All of these banks were in compliance

with the minimum capital requirements of GHC 7 million for universal banking business under

class 1Banking license. All but one bank complied with the minimum capital adequacy ratio of

10.00 percent, with an industry ratio of 14.8 per cent (BoG, 2007).

25

CHAPTER THREE

METHODOLOGY

Introduction

This chapter brings to bear the research method adopted for this study; the study actually

involves association between performance and capital structure. In view of this, the researcher

sought to used data from the secondary source, since data on capital structure and performance of

corporate institutions are available both online and other data management consults, these

include the financial statements of the banks selected for the study. The chapter outline the

regression method adopted for the study as well as the Pearson correlation coefficient to find the

strength of association the exist between variables chosen for the study.

3.1 The Research Paradigm.

Research always adopt either one or both paradigm for study, i.e either inductive or deduction.

When data is first collected and then, after analyzing the data a theory is developed consequently, the

approach is of inductive nature which is quantitative. On the other hand, if a theory or hypothesis is first

developed and then, later a research strategy is designed to test the hypothesis, the approach is of

deductive nature Saunders et al. (2007). In this study, empirical findings were based on the use of

quantitative nature of the research. Therefore, quantitative approach was applied to this study.

26

3.2 The Research Method

3.2.1 The Study Population

The study population comprises all banks licensed by the central bank thus Bank of Ghana (BoG),

however, banks under certain categories are not considered to be part for this study, such banks classified

as rural bank and licensed by the central Bank of Ghana are not part of the study and does not constitute

to be part of the population. Financial services licensed by the central bank also do not constitute to be

part of the population for the study. Only banks or commercial banks form the population for the study.

The researcher chose this population due to the ever increasing number of merchant and commercial

banks operating around the shores of the nation.

3.2.2 Sampling Techniques

The researcher uses a convenience sampling method which is a non probability techniques for

the selection of the sample size for the study, the study initially was to include all commercial

banks in the country licensed by the central bank and fulfill the study population requirements, as

well as having its financial statement available from 2004-2010. Since not all the banks qualify

under this category, then the researcher selected the banks that meet the prerequisite for her own

convenience. Thus the reason for the convenience sampling method used for the selection of

selected banks.

3.2.3 Sample Size

27

Data were gathered from the Annual Reports of all banks selected for the study in Ghana from

2004 – 2010. The method of sampling was to include all registered commercial banks of the

Bank of Ghana with financial statements from within the stated period. In all 24 banks qualified

to be included in the sample. Since the study was purposely on the banking sector, commercial

banks being licensed by the central bank were all forms part of the study population.

3.2.4 Data Source and Collection Method

Data for this study was secondary taken from the annual financial statements of the selected

banks for the stipulated period. Price Waterhouse Coopers’ Ghana Annual Banking survey and

also from the respective published site of the selected banks website repository.

3.3 Data Analysis

Since the research paradigm was quantitative in nature, the researcher used a combination of

both descriptive statistics and inferential statistics to analysed her data gathered. Data was

analysed by using multiple regression analysis to find the cause and effect of the explanatory

variables or the predictor variables on the response or dependent variables, ratios, percentage,

mean and standard deviation were outline in a descriptive tables.

The panel disposition of the data allows for the use of panel data methodology. Panel data

involves the pooling of observations on a cross-section of units over several time periods and

provides results that are simply not detectable in pure cross-section studies. Of late, the structure

conduct- performance relationship is tested by the panel data method because its results take into

28

consideration structural change as well as cyclical fluctuations (Domowitz et al, 1986). in the

analysis of the data, the researcher employ the help of statistical and econometric software tools

such as RGui, Microsoft Excel and E-view software’s to aid her to come up with the results

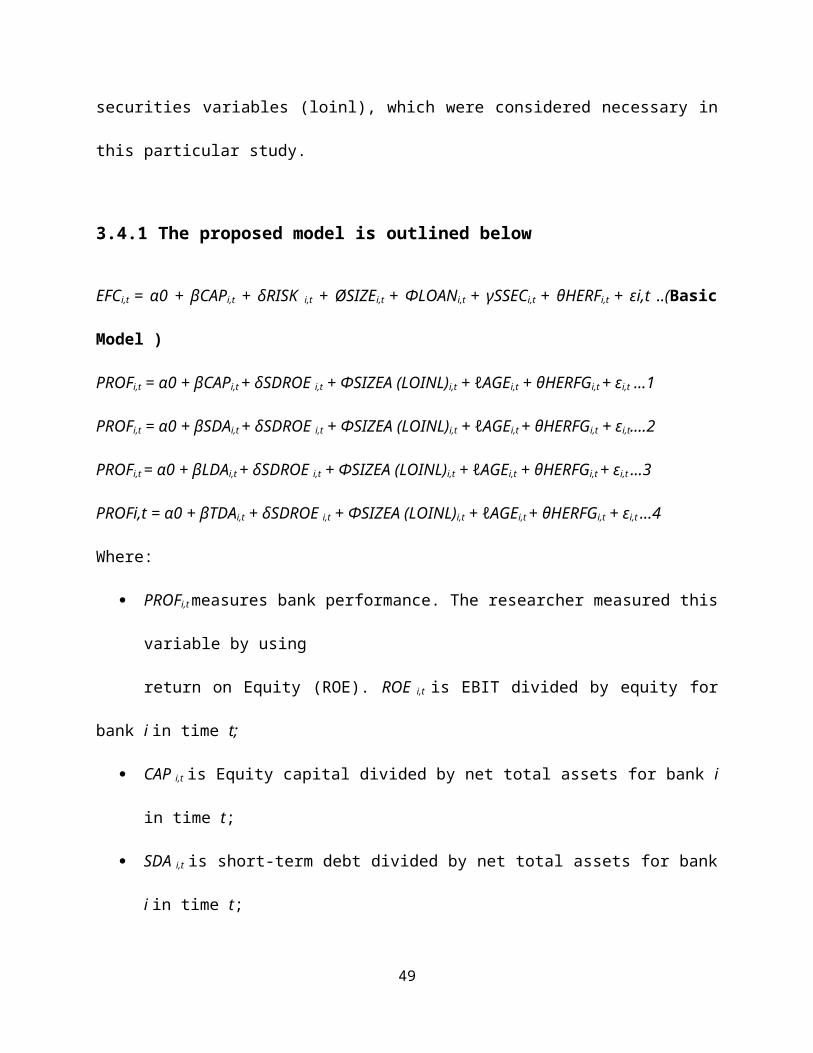

3.4 Proposed Model Used for the Study

The researcher used a model proposed by Berger and di Patti (2002) and latter adopted by

Pratomo and Ismail (2006) that shows the correlation of bank’s profit and capital structure. The

basic model is used by Pratomo and Ismail was altered slightly to suit the needs for this study

and to allow for a detach testing of the effect of capital, short-term debt, long-term debt and total

debt on profitability. It also allows for inclusion of the age, total assets (sizea) variables and the

combination of the loans and investment in securities variables (loinl), which were considered

necessary in this particular study.

3.4.1 The proposed model is outlined below

EFCi,t = α0 + βCAPi,t + δRISK i,t + ØSIZEi,t + ΦLOANi,t + γSSECi,t + θHERFi,t + εi,t ..(Basic

Model )

PROFi,t = α0 + βCAPi,t + δSDROE i,t + ΦSIZEA (LOINL)i,t + ℓAGEi,t + θHERFGi,t + εi,t ...1

PROFi,t = α0 + βSDAi,t + δSDROE i,t + ΦSIZEA (LOINL)i,t + ℓAGEi,t + θHERFGi,t + εi,t....2

PROFi,t = α0 + βLDAi,t + δSDROE i,t + ΦSIZEA (LOINL)i,t + ℓAGEi,t + θHERFGi,t + εi,t ...3

PROFi,t = α0 + βTDAi,t + δSDROE i,t + ΦSIZEA (LOINL)i,t + ℓAGEi,t + θHERFGi,t + εi,t ...4

Where:

PROFi,t measures bank performance. The researcher measured this variable by using

29

return on Equity (ROE). ROE i,t is EBIT divided by equity for bank i in time t;

CAP i,t is Equity capital divided by net total assets for bank i in time t;

SDA i,t is short-term debt divided by net total assets for bank i in time t;

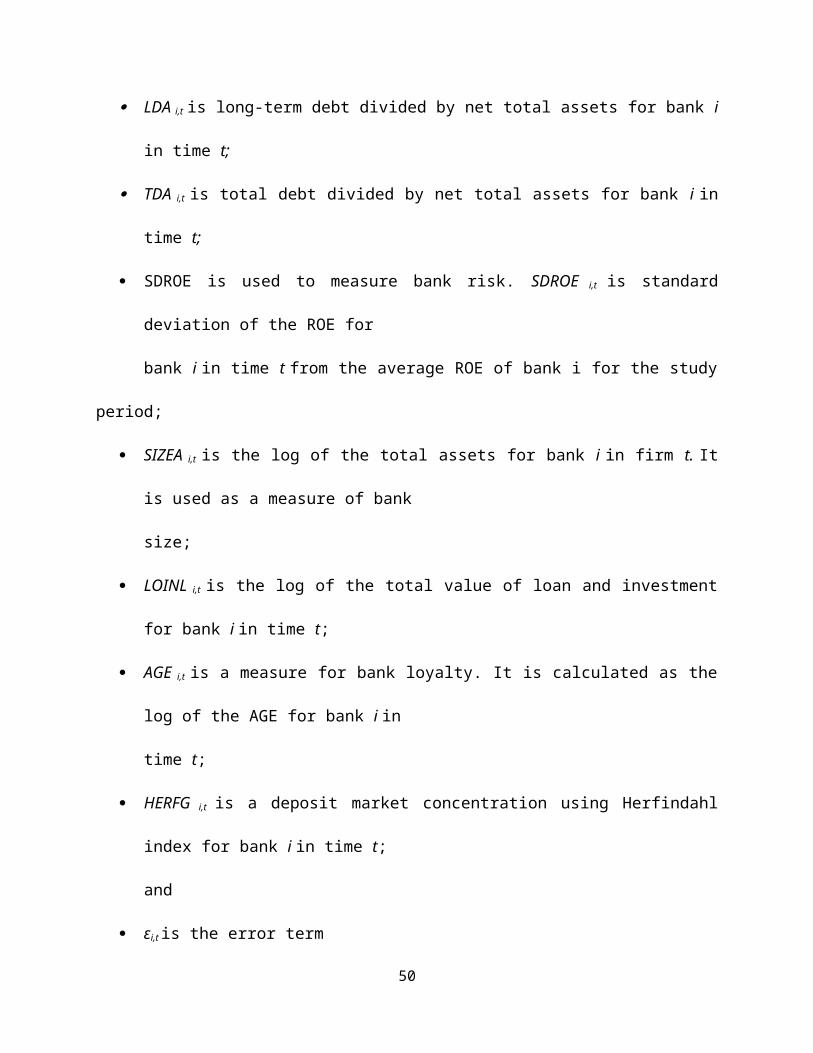

LDA i,t is long-term debt divided by net total assets for bank i in time t;

TDA i,t is total debt divided by net total assets for bank i in time t;

SDROE is used to measure bank risk. SDROE i,t is standard deviation of the ROE for

bank i in time t from the average ROE of bank i for the study period;

SIZEA i,t is the log of the total assets for bank i in firm t. It is used as a measure of bank

size;

LOINL i,t is the log of the total value of loan and investment for bank i in time t;

AGE i,t is a measure for bank loyalty. It is calculated as the log of the AGE for bank i in

time t;

HERFG i,t is a deposit market concentration using Herfindahl index for bank i in time t;

and

εi,t is the error term

3.4.2 Research Variables

The researcher used the accounting measure of performance such as the Return on Equity (ROE)

to operationalized profitability. The response or dependent variable in this study is Return on

Equity (ROE) whereas the explanatory variables include total asset ratio , short-term debt to net

total asset ratio ,capital to net total asset ratio , long-term debt to net and total debt to net total

asset ratio.

30

Equation 1 was used to find the correlation between bank efficiency as measured by Return on

Equity (ROE) and capital ratio (CAP).

Equation 2 was used to assess the relationship between ROE and short-term debt ratio whiles

Equation 3 was used to investigate the relationship between ROE and long-term debt

ratio and

Finally, equation 4 was used to ascertain the relationship between ROE and total debt.

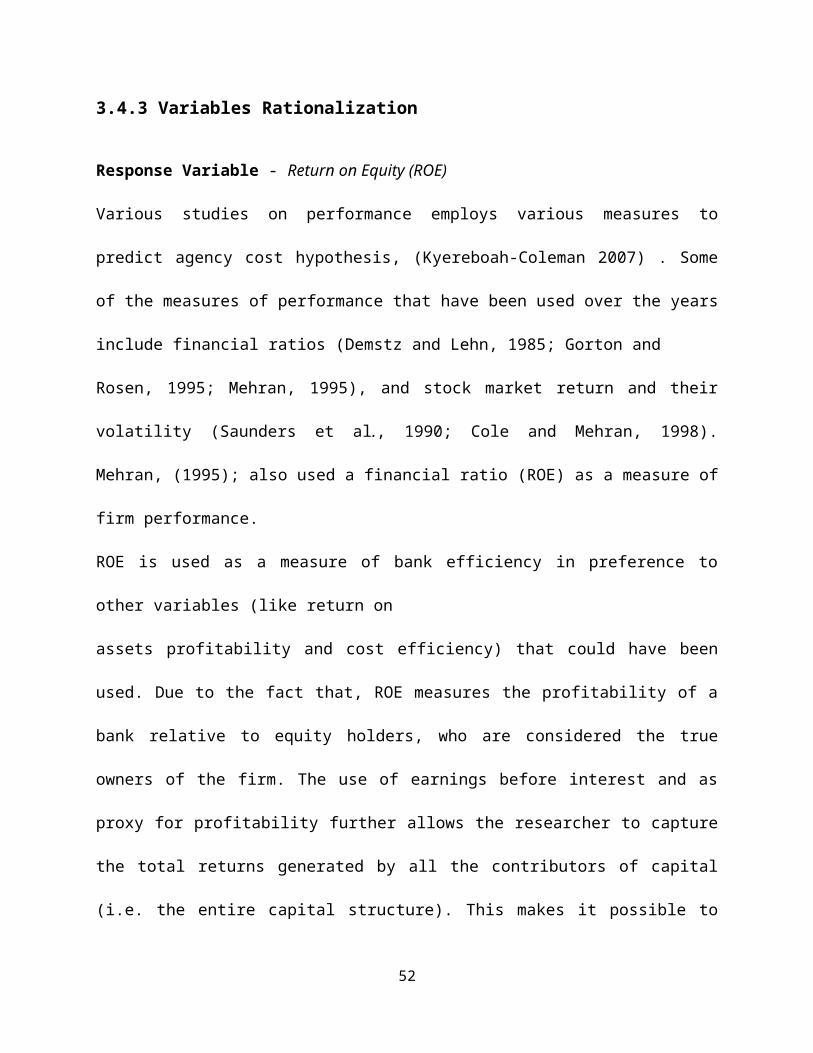

3.4.3 Variables Rationalization

Response Variable - Return on Equity (ROE)

Various studies on performance employs various measures to predict agency cost hypothesis,

(Kyereboah-Coleman 2007) . Some of the measures of performance that have been used over the

years include financial ratios (Demstz and Lehn, 1985; Gorton and

Rosen, 1995; Mehran, 1995), and stock market return and their volatility (Saunders et al., 1990;

Cole and Mehran, 1998). Mehran, (1995); also used a financial ratio (ROE) as a measure of firm

performance.

ROE is used as a measure of bank efficiency in preference to other variables (like return on

assets profitability and cost efficiency) that could have been used. Due to the fact that, ROE

measures the profitability of a bank relative to equity holders, who are considered the true

owners of the firm. The use of earnings before interest and as proxy for profitability further

allows the researcher to capture the total returns generated by all the contributors of capital (i.e.

the entire capital structure). This makes it possible to also assess the impact of both debt and

equity on the performance of banks, Abor (2005).

31

3.4.4 Predictor or Explanatory Variables

Long-term debt to Net Total Assets (LDA)

LDA measures the relationship between long-term debt (all debts of a bank with a lifespan of

more than 1 year) and net total assets. It shows the value per cedi of net total assets contributed

by long-term loans. This relationship enables the researcher to test the impact of long-term loans

on bank efficiency.

Short-term debt to Net Total Assets (SDA)

SDA is used to measure the relationship between short-term debt (all Owings by a bank which

fall due within a year) and net total assets. It is used to ascertain the portion of net total assets

financed by short-term debt. It shows the stake that short-term debt holders have in the business

and it is used to assess their impact on bank efficiency.

Capital Ratio (CAP)

CAP is the standard measure of leverage in banking research (Pratomo and Ismail, 2006). It

allows the researcher to ascertain the portion of net total assets contributed by equity holders.

This is then used as proxy to assess the impact of equity capital on bank profitability.

3.4.5 Control VariablesSIZEA

This is the proxy for bank size. It is taken to be the total bank assets as against other measures

like sales or number of employees. The reason is as a result of the fact that assets are the

32

economic resources controlled by an entity as a result of past transactions from which the entity

expects to gain future economic benefits. It follows therefore that the size of a firm’s assets

influences the sales that it can generate or the number of employees to be employed. This proxy

allows the researcher to assess the impact that assets in general have on performance. It is

expected that total assets will impact positively on the performance of the bank.

AGE

Age is calculated as the log of the number of years of existence for a bank since incorporation (or

since commencement of business, where the date for incorporation cannot be ascertained with a

degree of precision). Age is chosen as one of the control variables because, all other things being

equal, the length of time that a bank has been in existence will not only enable the bank to gain

experience in banking in Ghana but also improve its reputation and enhance customer loyalty.

These are expected to translate to bank efficiency if the bank can use its experience to gain

competitive advantage. This is not measured by the other variables, hence its inclusion in the

model.

Standard deviation of Return on Equity (SDROE)

SDROE is used to measure the uncertainty of returns to the true owners of the banks. It is a

standard measure for risk in investments. In investment, as the risk of an investment increases,

return is also expected to be high enough to cover the additional risk being taken by the

investors. In other words, as banks engage in risky adventures, the volatility of the earnings

33

should be compensated by higher rewards. Consequently, it is expected that the relationship

between SDROE and ROE would be positive.

Total Loans and Investment (LOINL)

LOINL is considered as a control variable because banks get a lot of operating income from

loans and investments. The granting of loans and credit is the principal activity of banks. It is

calculated as the total of all loans and advances irrespective of their life spans. Banks major

source of revenue comes from this source. Consequently the relationship between loans and ROE

is expected to be positive. Another operating activity of banks is the undertaking of investments.

Banks earn operating income from this source in the form of discounts, dividend etc and they can

have significant impact on the profitability of a bank. It is expected that the higher the amount of

a banks investment the higher its return. Therefore it is expected that total loans and investments

would have a positive impact on bank profitability.

Herfindahl Index (HERFG)

HERFG is the square of the deposit market share for a bank for a particular year. The resultant

figure is then multiplied by 10,000. Deposit is selected as the basis for calculating HERFG

because it is expected that a customer’s loyalty to a particular bank can be best reflected in the

amount he/she is willing to deposit with that bank. Deposits therefore give a justifiable indication

of the proportion of the entire market controlled by a bank. Thus banks with larger market share

are expected to have higher ROEs signaling a positive association between HERFG and ROE.

34

3.5 Hausman Specification TestTo determine the use of either random effect mode or the fixed effect model, the researcher

employed the used of the Hausman (1978) specification test. The use of Hausman specification

test is due to its characteristics which is normaly and commonly used to make the comparison of

random and fixed effect model estimates of coefficients. In the random effect model, the

intercept is assumed to be random drawing from a much larger population with a constant mean

value. The implication of this statement is that the Random effect Model is used when the

sample is so large and the data is randomly selected to represent the analysis, Pratomo and Ismail

(2006). As this research uses data from selected banks in Ghana, the researcher prefers Fixed

Effect Model as a representative model. Moreover, to strengthen the result, the researcher

analyzed the result of the estimated regression using Hausman Test. The different estimation

methods were used to run the multiple regression models.

3.6 Pearson Correlation Coefficients

Person correlation coefficient is a statistical/mathematical tool use to measure the degree or

strength of association between two variables or more variables; it always yields a value between

-1≤ r ≤1 inclusive. When the value r = 1 it shows that there is a perfect positive correlation,

whiles r = -1 means that there is a perfect inverse correlation. A value r near zero means there is

no clear relationship exists between the two variables, moreover, the measure also assumes an

assumption of values of 0.7 (absolute) and above is considered to be more correlated or have a

strong degree of association between the two variables involved, values from 0.5 -0.699

(absolute) is also considered to have an association either positive or inverse depending on the

sign associated with the value.

35

36

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND DICUSSIONS

Introduction

This chapter deals with the descriptive statistics of the various predictor various and its

association with the performance indicator, correlation analysis have also been discussed to find

the strength of relationship between the variables used. Regression analysis have also be

employed in this chapter of the various models to find the impact of the various predictors

variables contribution to the performance of banks in Ghana.

4.1 Descriptive Statistics

Table 4.1 Descriptive Statistics

Descriptive statistics gives the means and equips the researcher to have a fair view of the values

from the data processed. Form table 4.1, it gives information about the descriptive statistics of

the dependent/response variable, the independent/predictor variables as well as the control

variables used in the collection of the data for the entire discussions. From the table, it is evident

that, a greater percentage of the capital structure of banks in Ghana is made up of debt

accounting for about 81.68 percent of the bank’s capital. Short term debt was also revealed to

accounts for about 79.34 percent of total capital whiles long term debt accounts constitute for

6.56 percent. Apparently short term debt accounts for a higher source of funding for most banks

in Ghana with a greater portion coming from customer deposits. Nevertheless, long term debt

financing proves otherwise, as it does not seem to be a major source of funding for the banks in

Ghana. These findings are noted to be in agreement to existing literature, (Abor, 2005; Amidu,

37

2007). Amidu (2007) reveals that more than 87% of the banks in Ghana are financed by debt and

that average long-term debt represents around 8.2%.

Evidently, it has also shown that the banks in the industry operate above the minimum required

capital adequacy ratio of 10percent as it was found that, the mean capital ratio of banks in

Ghana is 13.86 percent. The low standard deviations of 3.75 percent (equity capital) and 12.77

percent (total debt) attest to the fact that almost all the banks in Ghana sources of funding are

similar and do not vary. The performance indicator (ROE) has a mean of 82.57 percent and a

standard deviation of 54.65 percent, which shows that, clearly, the banking industry performed

extremely well in the period under review but it is also obvious since the standard deviation is

quite large it indicates that not all the banks are benefiting from this high industry performance ,

some are actually not doing their best. The average risk level in the industry was 0.3476 with a

deviation of 38.54 percent. Which shows a fairly stable risk among banks. The mean of total

assets (log) was 6.24 (standard deviation of 70.24 percent) whiles that of total loans and

investments (log) was 6.59 (with a standard deviation of 63.82 percent). The extremely high

level of standard deviation of firm-level deposit-herfindahl Index suggests that the banking

industry is concentrated with only few banks in Ghana control the total deposits in the industry.

This may offer support for the high disparity in ROE, total assets and total loans and

investments. Probably these disparities are as a result of the fact that some of the banks have

been in existence for far more years than others (the standard deviation of the log of age is 58.72

percent whiles the average age (log) is 2.0586).

38

Table 4.1 Descriptive Statistics of Variables

Variable Observation Mean Value Std. Dev

ROE 24 .8256876 .54659

CAP 24 .1385680 .03752

SDA 24 .7934057 .13363

LDA 24 .0655987 .14036

TDA 24 .8167868 .12774

SDROE 24 .3476450 .38549

SIZEA 24 6.239879 .70236

LOINL 24 6.589452 .63821

AGE 24 2.058645 .58724

HERFG 24 57.81113 133.271

4.2 Pearson Correlation Analysis

Pearson correlation matrix was found to enable the researcher to find, it there exist

multicollinearity among the predictor variables. As explained in chapter three. Person

Correlation coefficient is a statistical/mathematical tool use to measure the degree or strength of

association between two variables or more variables; which always leads to yield a value

between -1≤ r ≤1 inclusive. The value r = 1 shows a perfect positive correlation or strength of

association, whiles r = -1 means a perfect inverse correlation or strength of association. A value r

near zero indicates no clear relationship existences between the two variables, moreover, the