Embed Size (px)

Citation preview

Major challenges for the Russian gas export

strategy

Groningen, 23 November, 2010

Tatiana Mitrova, Ph. D.Gubkin UniversityEnergy Research Institute of the RAS

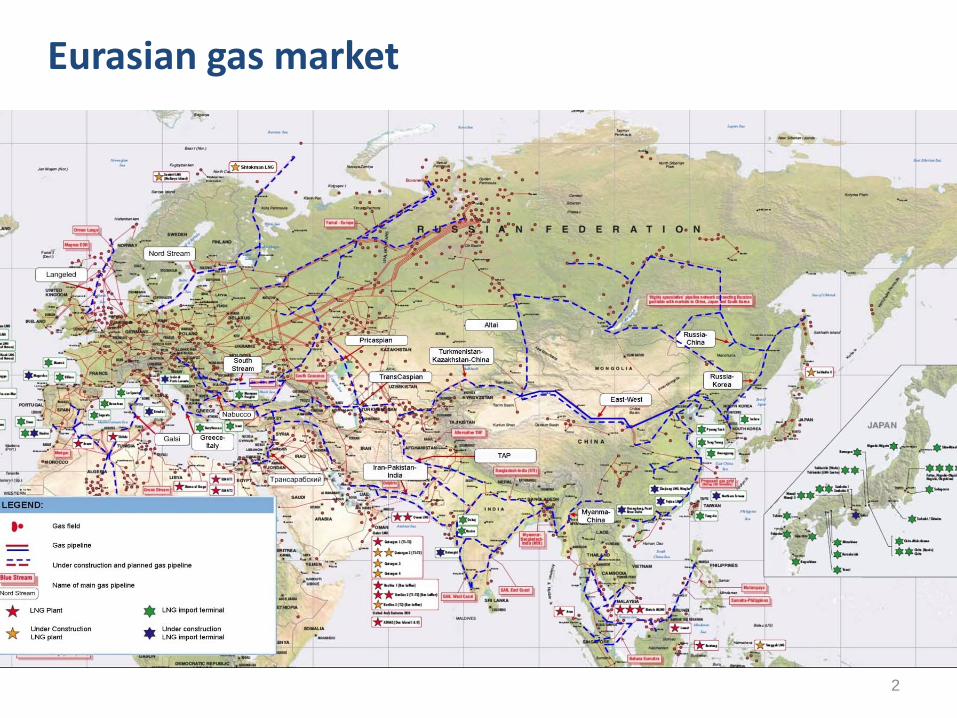

Eurasian gas market

2

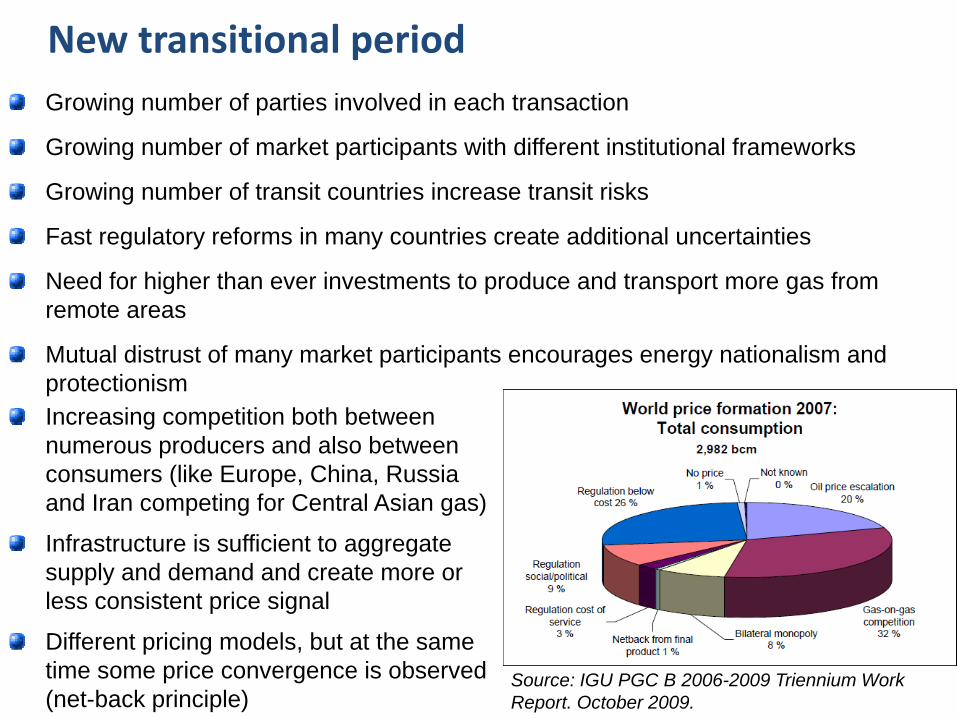

New transitional periodGrowing number of parties involved in each transaction

Growing number of market participants with different institutional frameworks

Growing number of transit countries increase transit risks

Fast regulatory reforms in many countries create additional uncertainties

Need for higher than ever investments to produce and transport more gas from remote areas

Mutual distrust of many market participants encourages energy nationalism and protectionism

Source: IGU PGC B 2006-2009 Triennium Work Report. October 2009.

Increasing competition both between numerous producers and also between consumers (like Europe, China, Russia and Iran competing for Central Asian gas)

Infrastructure is sufficient to aggregate supply and demand and create more or less consistent price signal

Different pricing models, but at the same time some price convergence is observed (net-back principle)

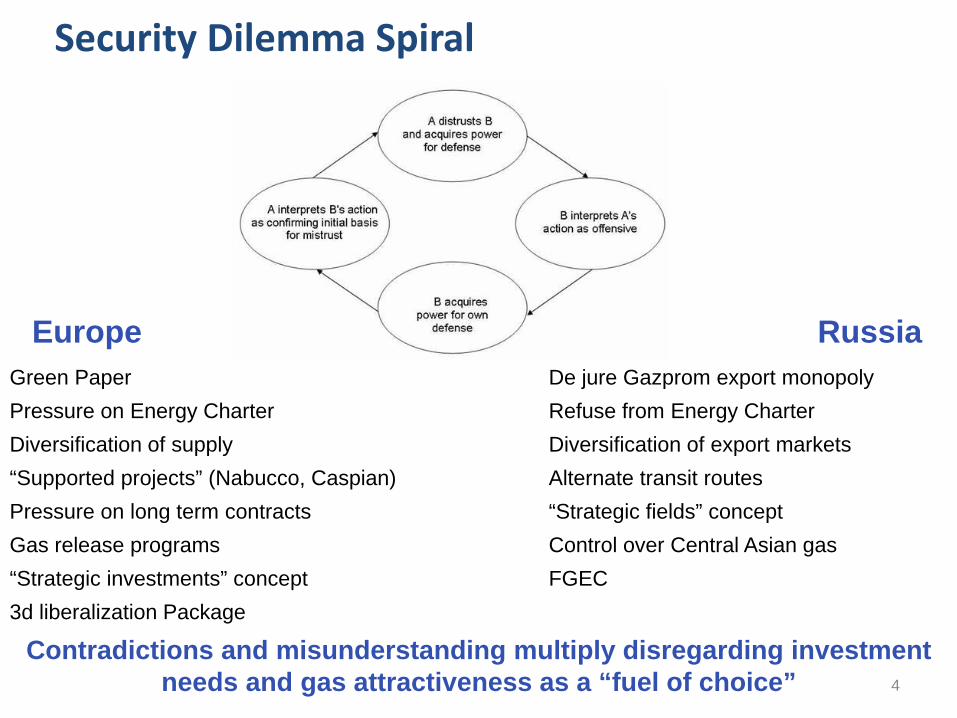

Security Dilemma Spiral

Europe RussiaGreen PaperPressure on Energy CharterDiversification of supply“Supported projects” (Nabucco, Caspian)Pressure on long term contractsGas release programs“Strategic investments” concept3d liberalization Package

De jure Gazprom export monopolyRefuse from Energy CharterDiversification of export marketsAlternate transit routes“Strategic fields” conceptControl over Central Asian gasFGEC

Contradictions and misunderstanding multiply disregarding investment needs and gas attractiveness as a “fuel of choice” 4

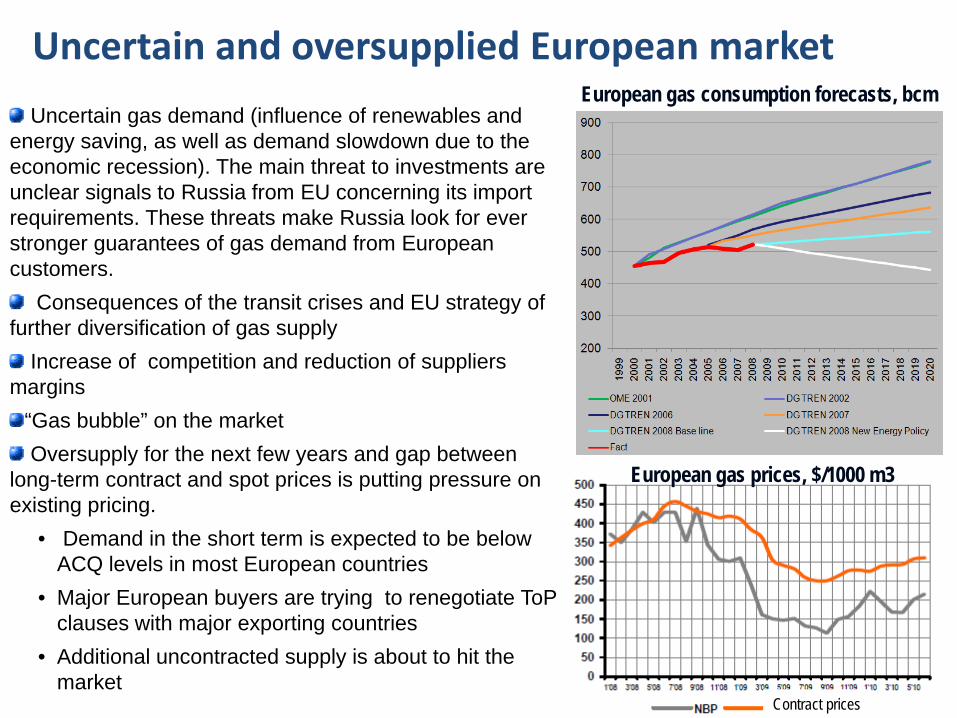

Uncertain gas demand (influence of renewables and energy saving, as well as demand slowdown due to the economic recession). The main threat to investments are unclear signals to Russia from EU concerning its import requirements. These threats make Russia look for ever stronger guarantees of gas demand from European customers.

Consequences of the transit crises and EU strategy of further diversification of gas supply

Increase of competition and reduction of suppliers margins

“Gas bubble” on the marketOversupply for the next few years and gap between

long-term contract and spot prices is putting pressure on existing pricing.

• Demand in the short term is expected to be below ACQ levels in most European countries

• Major European buyers are trying to renegotiate ToP clauses with major exporting countries

• Additional uncontracted supply is about to hit the market

European gas consumption forecasts, bcm

Uncertain and oversupplied European market

European gas prices, $/1000 m3

Contract prices

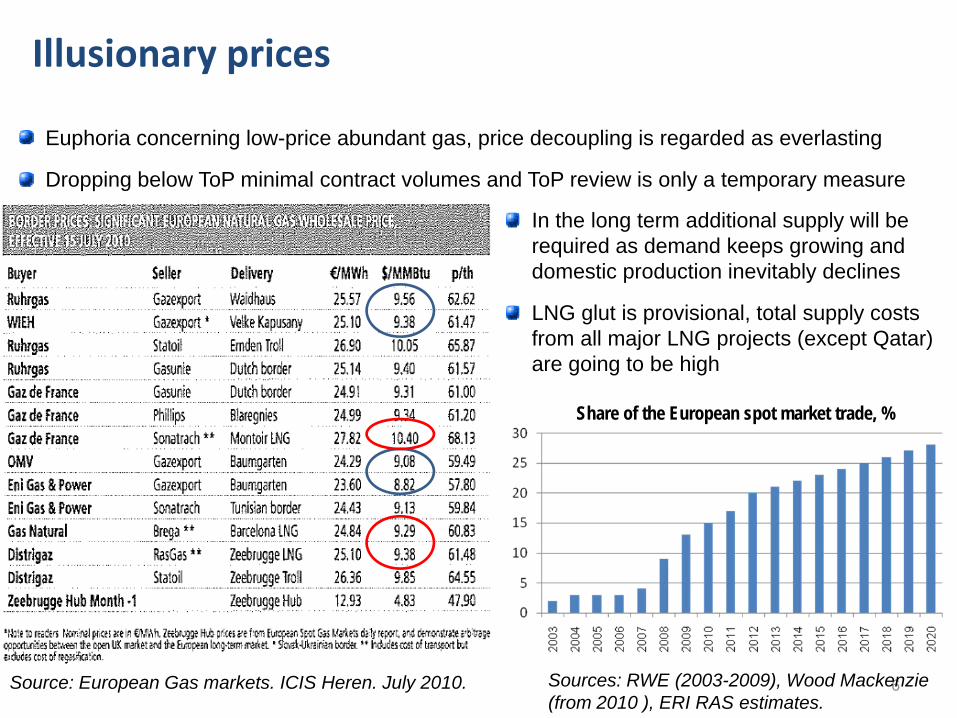

6Source: European Gas markets. ICIS Heren. July 2010.

In the long term additional supply will be required as demand keeps growing and domestic production inevitably declines

LNG glut is provisional, total supply costs from all major LNG projects (except Qatar) are going to be high

Illusionary prices

Share of the European spot market trade, %

Sources: RWE (2003-2009), Wood Mackenzie(from 2010 ), ERI RAS estimates.

Euphoria concerning low-price abundant gas, price decoupling is regarded as everlasting

Dropping below ToP minimal contract volumes and ToP review is only a temporary measure

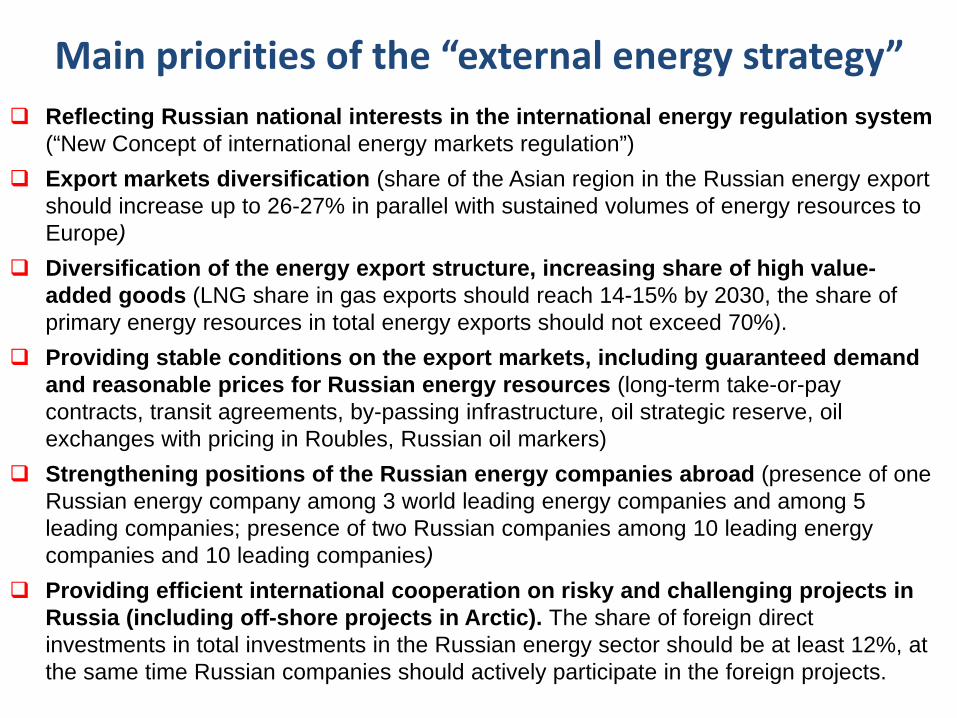

Main priorities of the “external energy strategy”Reflecting Russian national interests in the international energy regulation system (“New Concept of international energy markets regulation”)Export markets diversification (share of the Asian region in the Russian energy export should increase up to 26-27% in parallel with sustained volumes of energy resources to Europe)Diversification of the energy export structure, increasing share of high value-added goods (LNG share in gas exports should reach 14-15% by 2030, the share of primary energy resources in total energy exports should not exceed 70%).Providing stable conditions on the export markets, including guaranteed demand and reasonable prices for Russian energy resources (long-term take-or-pay contracts, transit agreements, by-passing infrastructure, oil strategic reserve, oil exchanges with pricing in Roubles, Russian oil markers)Strengthening positions of the Russian energy companies abroad (presence of one Russian energy company among 3 world leading energy companies and among 5 leading companies; presence of two Russian companies among 10 leading energy companies and 10 leading companies)Providing efficient international cooperation on risky and challenging projects in Russia (including off-shore projects in Arctic). The share of foreign direct investments in total investments in the Russian energy sector should be at least 12%, at the same time Russian companies should actively participate in the foreign projects.

Russian gas strategy on the European marketEurope is a highly solvable and well placed natural market for Russian

gas: all existing export pipelines go to Europe.Minimum Annual Quantities of gas in Gazprom’s portfolio of signed long

term contracts ensure deliveries of more than 3 tcm of gas to Europe in 2010-2035.

Europe is already a mature market approaching plateau demand in the foreseeable future. Russian goal is to maintain the existing market share, not to conquer an additional one.

Downstream strategy in order to secure demand and to get additional margins:

Development of marketing and trading activities (GMT: Gazprom Marketing & Trading). Swap operations with WINGAS, DONG, Statoil and other companies in order to reach attractive North European markets, especially UK.

Swaps of assets with the European companies (like WINGAS, EON, Gasunieetc.) in order to strengthen downstream positions.

Power generation and direct access to the final consumers to guarantee security of demand and get additional margins.

Underground storages to cover seasonal demand and increase margins.

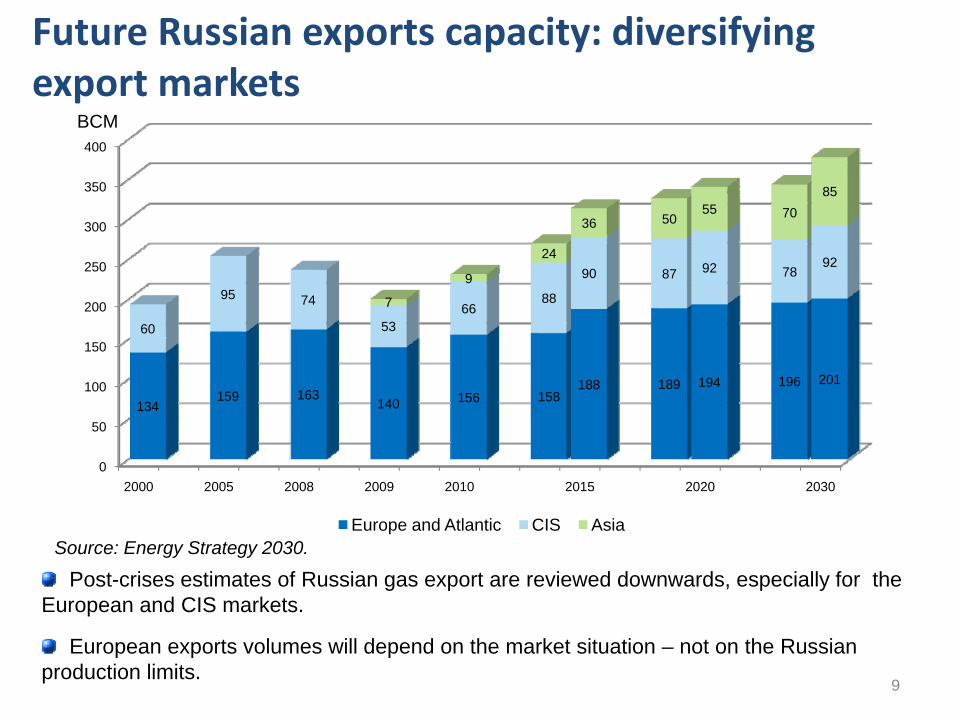

Future Russian exports capacity: diversifying export markets

Post-crises estimates of Russian gas export are reviewed downwards, especially for the European and CIS markets.

European exports volumes will depend on the market situation – not on the Russian production limits.

0

50

100

150

200

250

300

350

400

2000 2005 2008 2009 2010 2015 2020 2030

134159 163

140 156 158188 189 194 196 201

60

95 74

5366

88

90 87 92 7892

7

9

24

36 5055 70

85

Europe and Atlantic CIS Asia

9

Source: Energy Strategy 2030.

BCM

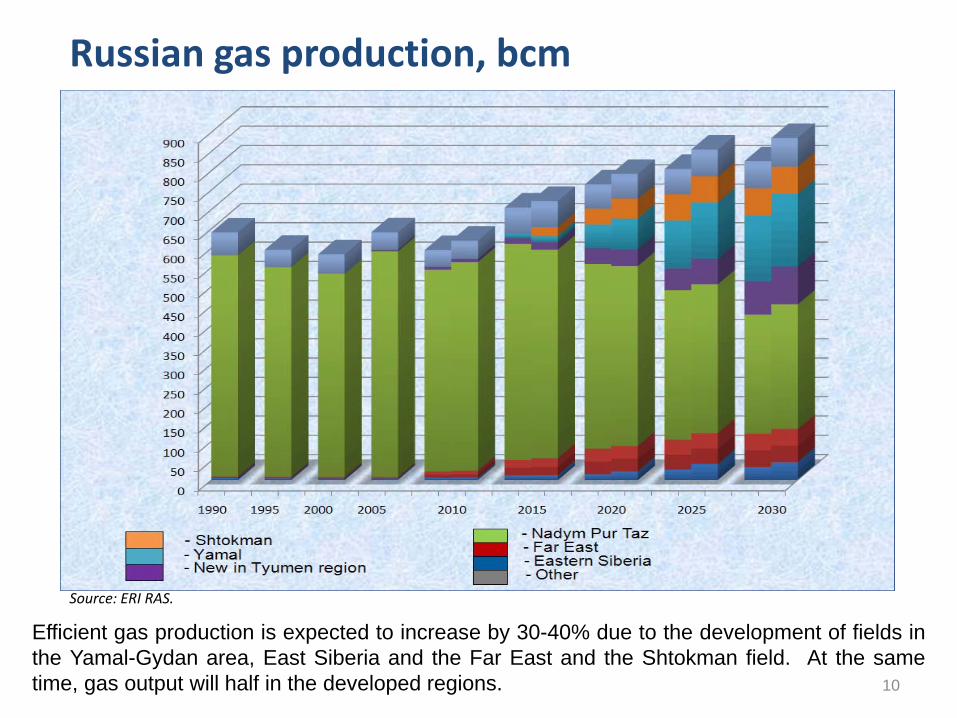

Russian gas production, bcm

Efficient gas production is expected to increase by 30-40% due to the development of fields inthe Yamal-Gydan area, East Siberia and the Far East and the Shtokman field. At the sametime, gas output will half in the developed regions.

37

Source: ERI RAS.

10

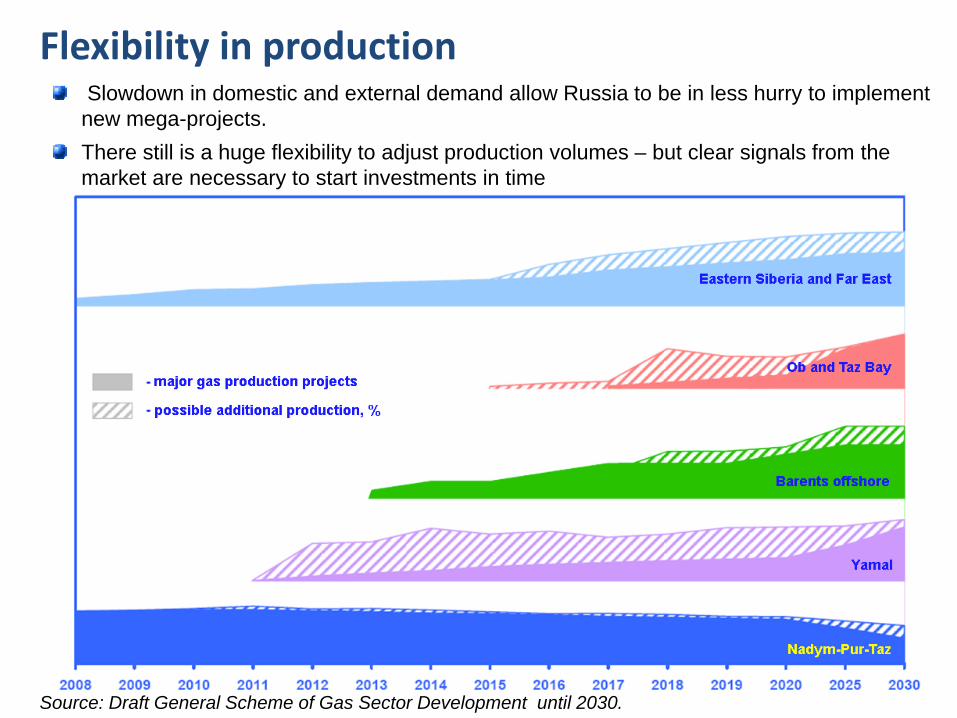

Flexibility in production

Source: Draft General Scheme of Gas Sector Development until 2030. 14

Slowdown in domestic and external demand allow Russia to be in less hurry to implement new mega-projects.There still is a huge flexibility to adjust production volumes – but clear signals from the market are necessary to start investments in time

Russian strategy on the CIS markets

Narrowing the gap between European and FSU export prices. Divergence between European and FSU export prices decreased from 30% in 2009 to 16% in 2010. In 2011 European and FSU export prices will reach parity for Custom Union non-members.

The main goal of the Russian strategy towards Caspian states is to sustain influence over the gas flows. Russia understands very well the risks of Central Asia and therefore even in the high gas demand environment, Russian projections of import volumes never exceeded 50-70 bcm. Contracts:

December 2009 – agreement with Uztransgaz and Lukoil on deliveries in 2010 up to 17.2 bcm of gas from Uzbekistan.

December 2009 – amendment to long-term contract with Turkmengas to resume in January 2010 purchases of 10-30 bcm of Turkmen gas annually in 2010-2012.

October 2009 – agreement with Azerbaijan for purchasing annually 0.5 bcm of gas in 2010-2015.

May 2007 – 15 year contract for purchasing gas from Kazakhstan. Volume in 2010 – 12.6 bcm. 18

Russian gas strategy on the Asia‐Pacific market

Asia Pacific gas demand is expected to more than double by 2030. There are forecasts of Chinese gas demand growth of 300% by 2030 up to 330 bcm. Russian gas is an attractive long term solution.

Most attractive markets – Japan and S.Korea – are LNG-focused. Sakhalin transforms in a major gas-producing region with “Sakhalin-2”.

The decision of the Chinese government to increase domestic prices and to link gas import prices to oil makes the projects profitable.

Gazprom and CNPC are in intensive negotiations over the contract for volumes comparable to current China consumption.

In October 2009 Gazprom and CNPC signed basic Heads of Agreement for gas deliveries to start supplies in 2014-2015 and in 2010 further negotiations were lead to additional MOU on 30 bcma deal.

1913

Transit – the most crucial for SoS

Russian gas is delivered to Europe through a grid of transit pipelines (Brotherhood, Blue Stream, Soyuz, trans-Balkan line, Northern Lights and the Yamal-Europe pipeline). 80% of Russian gas supplies to Europe come via Ukraine and cannot be replaced even by maximum loading of alternative routes. Belarus is delivering about 20% of Russia’s gas exports to Europe (45bcm). The issue of reliability of this transit route became acute after the 2004 Russo-Belorussian conflict.Transit network chronically lacks investments, assets are deteriorating. In addition to technological insecurity, political risks are still very high.

21

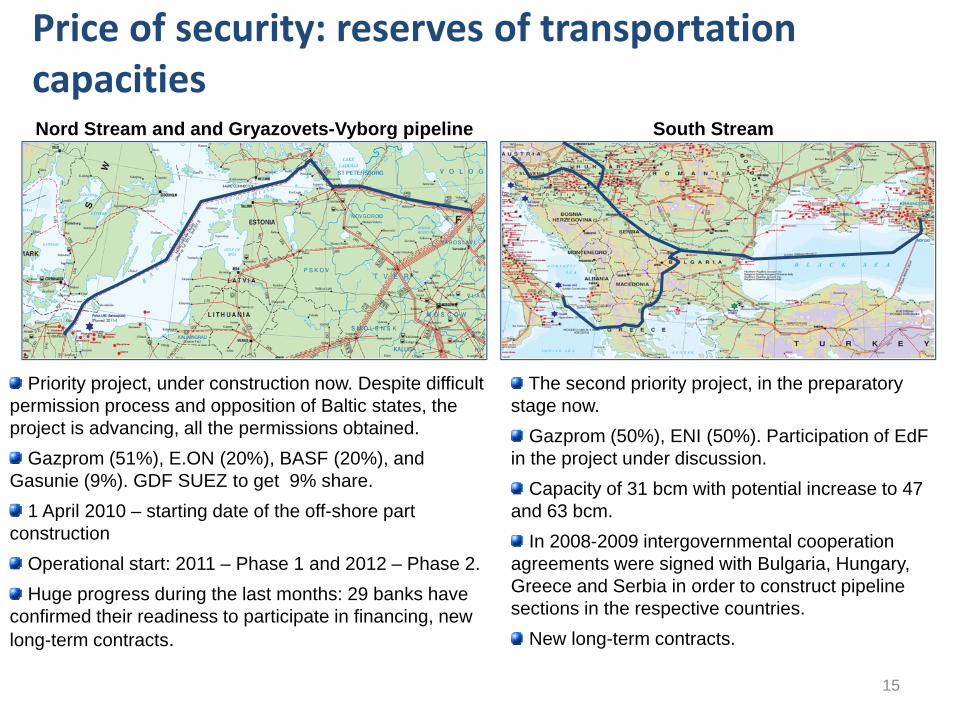

Price of security: reserves of transportation capacitiesNord Stream and and Gryazovets-Vyborg pipeline South Stream

Priority project, under construction now. Despite difficult permission process and opposition of Baltic states, the project is advancing, all the permissions obtained.

Gazprom (51%), E.ON (20%), BASF (20%), and Gasunie (9%). GDF SUEZ to get 9% share.

1 April 2010 – starting date of the off-shore part construction

Operational start: 2011 – Phase 1 and 2012 – Phase 2.Huge progress during the last months: 29 banks have

confirmed their readiness to participate in financing, new long-term contracts.

The second priority project, in the preparatory stage now.

Gazprom (50%), ENI (50%). Participation of EdFin the project under discussion.

Capacity of 31 bcm with potential increase to 47 and 63 bcm.

In 2008-2009 intergovernmental cooperation agreements were signed with Bulgaria, Hungary, Greece and Serbia in order to construct pipeline sections in the respective countries.

New long-term contracts.

2215

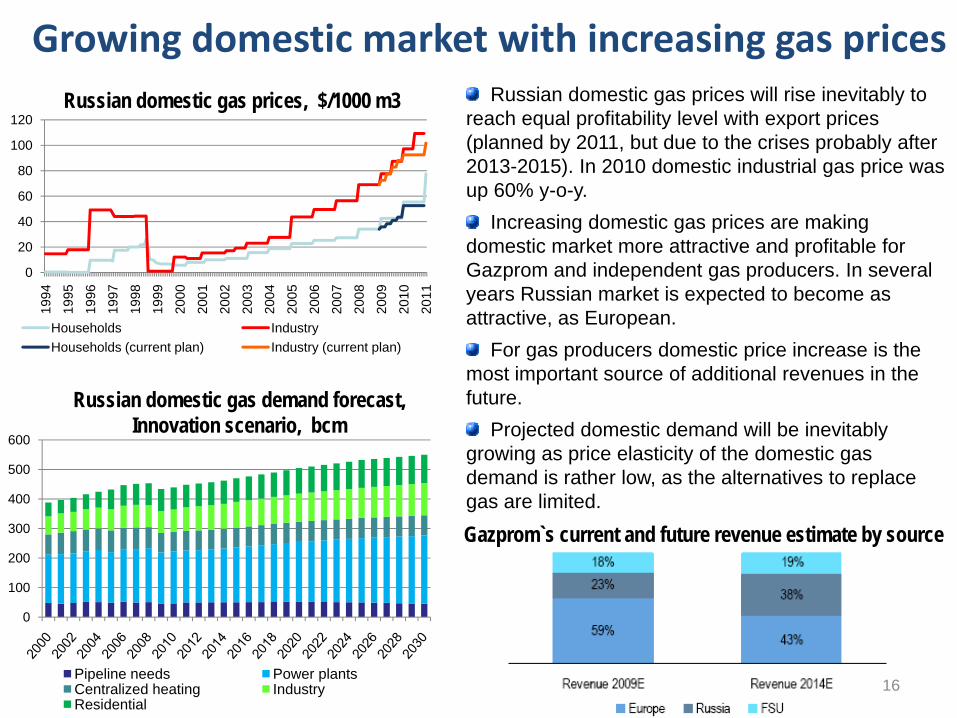

Growing domestic market with increasing gas pricesRussian domestic gas prices will rise inevitably to

reach equal profitability level with export prices (planned by 2011, but due to the crises probably after 2013-2015). In 2010 domestic industrial gas price was up 60% y-o-y.

Increasing domestic gas prices are making domestic market more attractive and profitable for Gazprom and independent gas producers. In several years Russian market is expected to become as attractive, as European.

For gas producers domestic price increase is the most important source of additional revenues in the future.

Projected domestic demand will be inevitably growing as price elasticity of the domestic gas demand is rather low, as the alternatives to replace gas are limited.

0

20

40

60

80

100

120

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Households IndustryHouseholds (current plan) Industry (current plan)

6

Gazprom`s current and future revenue estimate by source

Russian domestic gas demand forecast, Innovation scenario, bcm

0

100

200

300

400

500

600

Pipeline needs Power plantsCentralized heating IndustryResidential

Russian domestic gas prices, $/1000 m3

16

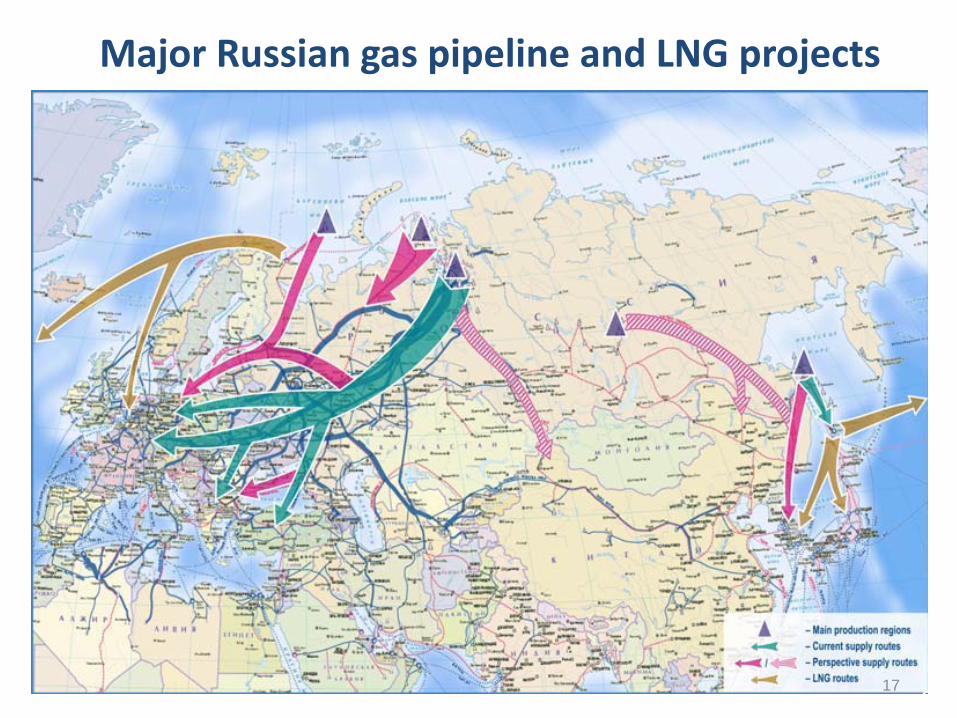

Major Russian gas pipeline and LNG projects

2017

ConclusionsInstitutional threat: imbalance between physical asset development and the old “patchwork” institutional framework leads to growing security threats

Market participants have developed several mechanisms of adaptation (vertical integration, mutual penetration of capital and long-term contracts) which should be regarded not as a market failure, but as an essential part of energy security system

Underinvestment threat: demand slowdown allows Russia to be in less hurry to implement new mega-projects. Depending on market conditions Russia has potential to supply more gas to the global market, but in order to avoid underinvestment timely signals from the market are necessary.

Volumes: post-crises estimates of Russian gas export are reviewed downwards, especially for the European and CIS markets. These export volumes will depend mainly on the market situation – not on the Russian production limits.

Prices: some temporary measures have been taken in order to adjust to an extraordinary demand drop, spot market indexation introduces for the next 3 years, but after gas glut disappears these clauses will hardly survive

Reserve margins: Excess transportation capacities are key to guarantee SoS to Europe

Market diversification: with increasing domestic prices and inevitably growing gas demand, domestic market will become much more important during the next decade and provide the bulk of sales and profits. Increasing export to the Asian markets is the main priority of ES-2030. 23

18