Embed Size (px)

Citation preview

1

Maker-Taker Fee, Liquidity Competition, and High Frequency Trading* Yiping Lina, Peter L. Swanb, and Frederick H. deB. Harrisc,†

This Draft: March 10, 2017

Abstract

This paper analyzes how a unilateral maker-taker fee reduction by Nasdaq affects market competition, liquidity, and high frequency trading. Holding the net exchange fee relatively constant, we find that: 1) contrary to much of the literature, the components of maker-taker fee change do matter; 2) the removal of the subsidy to ‘non-marketable orders’ causes the flight of informed market orders to the remaining highest tax-subsidy venues; and 3) the flight of informed orders reduced Nasdaq’s market share and pricing efficiency. By using the Nasdaq maker-taker fee experiment and difference-in-differences methodology, we find the reduced maker rebate lowers quote quality and the percentage of incoming orders routed to Nasdaq. However, in an only partially offsetting manner, it improves fill rate and speed of fill due to the reduced taker fee. Any improved relative position of a market in routing tables causes adverse selection costs to decline, together with information in the market orders, standard measures of market liquidity to increase, and liquidity supplier profits to decline. The maker-taker fee reduction did not result in a gain in share from off-exchange trading venues. As the fee and rebate decline, high frequency traders tend to switch from adding to removing liquidity.

Keywords: Maker-Taker Fee; Market Fragmentation; Market Quality; High Frequency Trading

JEL Classifications: G12, G14

* The views expressed herein are strictly those of the authors. Yiping Lin acknowledges the financial support from the CMCRC and Wake Forest University for facilitating his work in the United States. We thank Nasdaq, Inc. for providing data while Yiping Lin was visiting under an agreement between Nasdaq and the CMCRC. We also thank Avanidhar Subrahmanyam, Joakim Westerholm, Kumar Venkataraman and seminar participants at Australasian Finance & Banking Conference for helpful comments and suggestions. The views herein are not intended to represent the views of Nasdaq, Inc., its employees, or directors. Any errors or omissions are the responsibility of the authors alone. † a School of Banking and Finance, UNSW Business School, UNSW, Sydney NSW 2052 Australia; email: [email protected]. b School of Banking and Finance, UNSW Business School, UNSW, Sydney NSW 2052 Australia; email: [email protected]. c School of Business, Wake Forest University, Winston-Salem, NC 27106, United States; email: [email protected].

2

I. Introduction

The importance of the components of an exchange’s maker-taker fee remains unclear. Previous studies

such as Angel, Harris, and Spatt (2011), Colliard and Foucault (2012), and Malinova and Park (2015)

state that only the net fee change matters and that the maker-taker fee breakdown is irrelevant since the

explicit tax on market orders appears to offset the subsidy to limit orders. In fact, Foucault, Kadan, and

Kandel (2013) go one step further to claim that trading volume may increase or decrease (depending on

the model parameters), even in the absence of a change in the net total fee, because a fixed tick size

prevents prices from neutralizing the effect of the maker rebate. This potential cancelling out is in

appearance only, because maker-taker fees are normally mistakenly treated as an explicit tax on market

orders and offsetting subsidy to limit orders. Not so. The exchanges that devised maker-taker fees were

fully aware of potential offset. Hence they limit the subsidy to ‘non-marketable’ orders which means, in

effect, that only orders with delayed execution that increase the depth of the limit order market receive

the subsidy. If the tax and subsidy were fully offsetting, depth would be unaltered and this could only be

the case if marketable limit orders, as well as non-marketable limit orders, received the subsidy.

This ongoing debate on the exchange fee structure in U.S. markets led NASDAQ to experiment with

lowering both maker rebate and taker fee by an identical amount for a select group of securities. While

the Nasdaq3 experiment was motivated by competition from dark and off-exchange venues, the real

benefit of the experiment lies it its ability to reveal for the first time why maker-taker fees are of critical

importance for almost every aspect of market quality and why tax-subsidy schemes are fundamental

with no prospect of ever cancelling out.

One way to think about what really happens is that the best bid and ask are ideal for informationless

liquidity trades designed to minimize consumption volatility risk but these do not attract subsidy as these

are, in effect, ‘marketable’ orders. Orders in the limit order book queue further away that enhance depth

and facing either delay or non-execution risk are the both the target of the subsidy and provide limit

order places some element of protection from informed traders who move price substantially. It is clear

then that a subsidy to market depth can only benefit one class of trader, namely informed traders, and,

3 Over the past decade, hundreds of exchange-listed securities have traded more volume in off-exchange markets than on exchange markets. In response to claims that public markets are too expensive to trade, Nasdaq wanted to know whether access fees may be discouraging the use of public markets3 (Nasdaq’s SEC, 2014).

3

moreover, the same class of trader is the only one willing to pay the high explicit tax on market orders as

only they are effectively able to benefit from the greater depth of the limit order book.

Impatient limit order providers in the now much deeper book are now willing to become the

counterparty to the informed traders now dominating the taker market in the presence of a higher taker

fee. Hence the maker-taker fee structure is cleverly designed to cancel out for only one trader type – the

informed. In this paper, we show that the maker-taker fee structure employed by Nasdaq has highly

desirable features in that it improves price discovery and market efficiency while at the same time

maximizing Nasdaq’s trading volume and market share. By temporarily unwinding these highly

desirable features of the Nasdaq exchange for a limited number of stocks and a limited time-frame,

Nasdaq was able to reveal for the first time why its fee structure was so successful. It is hard for profit-

orientated exchanges to provide for what is essentially a public good – namely efficient price discovery

– but the taker-maker fee structure has evolved as a natural counterpart to competition in so-called

fragmented markets.

In this study, we use the difference-in-differences (DID) method to examine the impact of the NASDAQ

exchange access fee change on market competition, liquidity, and high frequency trading (HFT)

behavior. Specifically, we first test whether the components of maker-taker fee changes matter when the

net exchange fee remains relatively constant and find that they are of critical importance. Second, we

test whether reducing the exchange maker-taker fee attracts liquidity from off-exchange venues to find

that it does not. This is because of the public-good aspect of maker-taker fees alluded to above means

that alterations to subsidy-tax arrangements on price discovery do not affect off-lit market exchanges.

Third, we extend the purpose of the Nasdaq pilot to test how HFT behavior changes in response to the

maker-taker fee change. Since we show that HFT switches from adding to removing liquidity as the tax-

subsidy is removed, this novel finding indicates that HFT is a distinct trader-type, neither informed nor

uninformed, and has a substantial niche regardless of tax-subsidy schemes.

The Nasdaq access fee reduction pilot offers an informative natural experiment. Nasdaq charge taker fee

for removing liquidity by submitting marketable orders, and provide maker rebate for adding liquidity

by submitting non-marketable orders (i.e., limit orders which cannot be executed immediately). On

February 2, 2015, Nasdaq implemented a maker-taker fee pilot for 14 traded stocks on Nasdaq where the

4

taker fee was lowered to 5 cents per 100 shares (CPS) from 30 CPS to remove displayed liquidity; the

maker rebate for adding displayed liquidity was lowered to 4 CPS from an indicative4 29 CPS. For

simplicity, the indicative rebate for the PilotOff period is summarized in Table 1. The pilot ended on

May 31, 2015, when the fee reverted to its pre-pilot level.

<Insert Table 1 here>

The International Organization of Securities Commissions defines maker-taker fees as “a pricing model

whereby the maker of liquidity, or passive [limit] order, is paid a rebate and the taker of liquidity, or

aggressive [market] order, is charged a fee.” Maker-taker fees for protected quotes in the equities

markets are bound by Rule 610 of Regulation NMS5, which caps fees at 30 CPS traded. Maker rebates

aim to both improve liquidity, by rewarding its provision, and increase trading volume.

The maker-taker payment model originated with electronic trading venues in the late 1990s (Harris,

2013). In 1997, the Island electronic communication network (ECN) was among the first markets to

adopt maker-taker fees, which attract order flow through liquidity rebates. These rebates provide traders

with an additional source of income other than the bid-ask spread, incentivizing liquidity providers to

post more competitive quotes to attract order flows from other markets. As a result, Island’s market

share of reported Nasdaq trades increased from approximately 3% in 1997 to almost 13% in 1999

(Cardella, Hao, and Kalcheva, 2015). Other alternative trading systems (ATSs) soon followed Island’s

fee model to attract liquidity and order flows from lit exchanges (SEC, 2015a).

<Insert Table 2 here>

In response to the ATS competition, many exchanges adopted maker-taker fees of their own. Over the

past decade, the maker-taker pricing model has thus gained widespread adoption in the U.S. equities

4 The maker rebate scheme is much more complicated (see http://nasdaqtrader.com/Trader.aspx?id=PriceListTrading2). Further, see ITG Takeaways from the NASDAQ Pilot Program report, available at http://www.itg.com/marketing/ITG_Pearson_WP_20150602.pdf. 5 If the price of a protected quotation is less than $1, the fee cannot exceed 0.3% of the quotation price. See SEC Rule 610.

5

market (see Table 2), rewarding liquidity suppliers and charging liquidity demanders. Only three U.S.

exchanges (BATS-Y, EDGA, Nasdaq/BX) adopt the inverted fee (taker-maker) model, offering rebates

to take liquidity accompanied by a higher fee in order to add liquidity.

Angel, Harris, and Spatt (2011) argue that introducing a maker rebate financed by a taker fee should

have no effect, because prices in competitive markets adjust by the rebate amount. However, this

argument assumes that the information content in order flows is the same across venues and breaks

down when different venues have different fee structures. Colliard and Foucault (2012) formalize Angel,

Harris, and Spatt’s intuition and prove, without relying on perfect competition, that in the absence of

frictions only changes in the net total fee retained by the exchange affect liquidity and trading volume.

Foucault, Kadan, and Kandel (2013), by contrast, show that trading volume may increase or decrease

(depending on the model parameters), even in the absence of a change in the net total fee, because a

fixed tick size prevents prices from neutralizing the effect of the maker rebate. A problem, however,

with this extensive literature is that it does not take into account the switch in informed order flow away

from a high liquidity subsidy exchange to its closest competitors when the subsidy is lowered. This may

be caused by the change in the exchange’s relative position of the routing table.

From an empirical perspective, Malinova and Park (2015) analyze whether and why the breakdown of

trading fees between liquidity demanders and suppliers matters by using a change in trading fees on the

Toronto Stock Exchange (TSX), which is a monopoly exchange in their sample period. They find that

posted quotes adjust after the change in fee composition, but that the transaction costs for liquidity

demanders remain unaffected once fees are taken into account. In the absence of competition from

competing exchanges, one does not expect any change in the composition of the order flow. However,

we find that adverse selection costs decrease after the maker-taker fee reduces, holding the net exchange

fee relatively constant6.

Colliard and Foucault (2012) theorize that in the absence of frictions, changes in the breakdown of the

total fee between makers and takers should not affect trading behavior; only changes in the net exchange

fee are economically meaningful for participant welfare. However, the informed traders in a competitive

6 Because more than 90% of execution volume is displayed liquidity and more than 6% is non-displayed liquidity in our sample (Table 3), the overall net fee change remains relatively stable.

6

trading environment are not included in their model as patient and impatient traders are not informed

traders. If an exchange introduces a maker rebate and finances it by adopting an increased taker fee

without changing the total fee, then, ceteris paribus, placing a market order becomes relatively more

expensive than trading with a limit order. As some traders switch from market orders to limit orders,

each limit order’s execution probability declines and thus traders may improve quotes to attract matches

for their limit orders. Without frictions, the benefit from maker rebates could be exactly offset by the

narrowed bid-ask spread but only if the information content in the order flow is unaffected by the

introduction of the matching fee subsidy. However, the implicit assumption of an unchanged order flow

is implausible since informed trades with short-lived information need to be more aggressive to achieve

a higher executive probability.

Consequently, changes in the breakdown of the total fee between makers and takers should affect

trading behavior and raise the spread, as liquidity trades are the first to be shifted toward making

liquidity, while trades taking liquidity contain a higher proportion of asymmetric information. The

alternative prediction of an unchanged spread made by Angel, Harris, and Spatt (2011) arises since they

do not consider the altered order flow. While the Angel, Harris, and Spatt (2011) prediction is

empirically supported by Malinova and Park (2015), this concurrence is most likely because they study

the 2005 TSX fee change when it was a monopoly. In contrast, our study finds that when holding the

total exchange fee relatively constant, the change in the breakdown of the fee components does matter.

This difference may be driven by that our study examines the Nasdaq fee change in a competitive

trading environment with 11 competing stock exchanges, approximately 40 active ATSs, and numerous

broker-dealer platforms (Hatheway, Kwan, and Zheng, 2016). On a monopoly exchange, the variation in

order flow informativeness is likely to be exceedingly small.

Panayides, Rindi and Werner (2016) study the effects of BATS Europe maker-taker fee reduction on

market quality and market share in a fragmented market. Their model predicts, that a simultaneous

reduction in make and take fees results in a deterioration of market quality and a significant spillover

between venues following fee changes. However, they did not model the role of asymmetric

information. This is important because when the rebates are reduced, it may force away the informed

traders as the depth of the limit order book drops.

7

Lin, Swan, and Mollica (2017) find when U.S. tick size increased from one cent to five cents, the market

share of the inverted markets with significant high exchange access fee increased. Barclay, Kandel, and

Marx (1998) empirically study how changes in bid-ask spreads influence volume and prices, finding that

higher transaction costs reduce trading volume. Lutat (2010) argues that the Swiss Stock Exchange’s

removal of a maker fee (without changing the taker fee) has not affected the quoted spreads. Cardella,

Hao, and Kalcheva (2015) study a number of maker-taker fee changes in the United States from 2008 to

2010. They find that an exchange’s total fee relative to that of other exchanges affects its trading volume

and that a change in the taker fee has a stronger effect than a change in the maker rebate. They also show

that the breakdown of the total fee into maker rebates and taker fees does not affect the quoted spreads.

However, Malinova and Park (2015) argue that in Lutat (2010) and Cardella, Hao, and Kalcheva (2015),

changes in the maker-taker fees are in fact accompanied by changes in the total fee.

Foucault, Kadan, and Kandel (2013) examine the relative importance of the net fee and the levels of the

maker and taker fees. They show that the breakdown of the total fee between makers and takers only

becomes economically meaningful when the minimum tick size restricts adjustments to bid and ask

prices but do not consider how the competition between maker-taker business models affects the

information content of the order flow. Exchanges can maximize their trading volume by differentiating

their maker rebates and taker fees. If liquidity demand (supply) is insufficient, the venue can decrease

(increase) its taker fee and maker rebate.

We also examine how such a maker-taker fee reduction affects market efficiency, which is an important

aspect of market quality. The market efficiency hypothesis introduced by Fama (1970) emphasizes a

lack of return predictability as the criterion for efficiency. Lo and MacKinlay (1988) tests market

efficiency using variance ratio test which exploits the underlying property of the random walk process.

Chordia, Roll, and Subrahmanyam (2008) present return predictability from order flows can arise in at

least two ways. First, illiquidity raises implicit transaction costs (spreads) which squelch arbitrage

activity. Second, market makers may mis-react to the information content of the order flow. This

mispricing can create an incentive for outside agents to gather such information and trade on it. In this

case, market makers will face increased adverse selection, which raises the equilibrium spread and leads

to a less liquid market. Chordia, Roll, and Subrahmanyam (2008) find that liquidity enhances the

incorporation of private information into prices. When the maker-taker fee is reduced, we typically find

8

that the variance ratios increase, while first-order return autocorrelations decline in Nasdaq. This pattern

suggests that the observed increase in these variance ratios is caused by increased mispricing, with less

private information being reflected in prices. Moreover, compared with Nasdaq, the three other highest

rebate-paying exchanges (Arca, BATS Z, NYSE) experience a relatively low decline in market

efficiency.

Taker fees and maker rebates comprise a significant proportion of overall trading costs, given the typical

bid-ask spread in a liquid stock is tick constrained, which is 1 cent set by the SEC for stock prices above

$1. Although most retail investors do not have access to this information, all institutional investors and

market makers, which account for majority of trading activity, make use of such data. Brokers

commonly sell their marketable orders to wholesale dealers to capture the bid-ask spread and to avoid

access fees, and send their non-marketable orders to exchanges for executions to gain maker rebate

(Angel, Harris, and Spatt, 2015). In particular, they employ so-called “smart order routers” that take into

account real-time state information and formulate an order routing problem that considers various

execution metrics to decide whether to place a limit order or market order and accordingly to which

venue(s) to direct their order (Maglaras, Moallemi, and Zheng, 2012).

Because of its effect on execution probability in a fragmented market, we expect this liquidity impact of

an exchange’s fee-based net pricing to be increasingly important in the high frequency trading

environment and perhaps explain the shift from lit exchanges to off-exchange venues. Battalio, Corwin,

and Jennings (2015) examined the impact of differential exchange access fee schedules on broker

routing decisions and limit order execution quality. They find maker-taker may be a mismatch between

customer interest and broker incentive. Specifically, maker-taker may maximise liquidity rebate but

result in poor execution quality for some clients. For nonmarketable orders, brokers may be incentivized

to route customer orders to rest on a trading venue with the highest maker rebate. However, venues with

high maker rebates are necessarily financed with higher taker fees, meaning that they tend to be ranked

low on a broker’s routing tables for routing marketable orders that take liquidity. Since the SEC Order

Protection Rule does not specify who trades first when multiple trading venues have the best posted

price, all else being equal, a price-sensitive market participant is more likely to route an order to take

liquidity from an exchange with a lower taker fee. As a result, nonmarketable orders sent to rest on

9

trading venues with high taker fees may experience lower fill rates (Battalio, Corwin, and Jennings,

2015).

Brolley and Malinova (2012) argue that the effect of changes in the breakdown of the total fee into a

maker rebate and a taker fee is not neutral if some traders (e.g., retail traders) only pay them on average,

for example, through a flat commission to their brokers. In their model, only a fraction of traders receive

maker rebates for each executed limit order. As the maker rebate increases, these traders improve their

quotes and the raw bid-ask spread thus declines. Ceteris paribus, traders who pay the flat fee base their

order choices on the raw bid-ask spread rather than the cum fee bid-ask spread, thereby submitting

relatively more market orders as the raw bid-ask spread declines. The authors then predict that in the

presence of asymmetric information, the change in trader behavior causes market orders to become less

informative. Their prediction is driven by the monotonic equilibrium behavior of traders in their model

whereby, similar to Kaniel and Liu (2006) and Rosu (2012), traders with a sufficiently large

informational advantage use market orders and those with weaker information use limit orders. This is

due to privately informed traders facing a trade-off between the better price offered by a limit order and

the potential loss of their informational advantage if their limit order does not execute. Those with the

strongest informational advantage thus choose market orders and pay the bid-ask spread, whereas those

with a weaker advantage choose limit orders and (hope to) receive the spread.

However, HFT traders place either limit orders to gain rebates or market orders to pay a fee depending

on their degree of information. In the maker-taker pricing model, the liquidity supplier has two main

sources of revenue, namely bid-ask spreads and rebates, while liquidity takers profit from price

movement minus the taker fee. In electronic markets, large market orders consume the available

liquidity and widen the bid-ask spread. This drop in liquidity creates a profit opportunity for liquidity

suppliers, which react by posting new quotes (make liquidity phase), which in turn create a new trading

opportunity for liquidity demanders (take liquidity phase). Foucault, Kadan, and Kandel (2013) theorize

this “liquidity cycle” process appears repeatedly. Each trading opportunity is short-lived as it disappears

once a trader exploits it. Thus, HFT traders, who react faster than their competitors, gain the most from

the profit opportunity.

10

The SEC has requested comment on the HFT volume geared toward earning liquidity rebates and has

questioned whether “rebates [are] unfair to long-term investors because they necessarily will be paid

primarily to [high-frequency] proprietary firms engaging in passive market making strategies. Or do

they generally benefit long-term investors by promoting narrower spreads and more immediately

accessible liquidity?” (SEC, 2010). Angel, Harris, and Spatt (2011, p. 39) further argue that the maker-

taker model has “aggravated agency problems among brokers and their clients” because a typical broker

does not forward the exchange fees to its clients on a trade-by-trade basis and may have a conflict of

interests with its clients regarding the choice of trading venue.

The strength of our analysis lies in the structure of the Nasdaq fee pilot change. First, Nasdaq introduced

the maker-taker fee reduction only for a predefined subset of 14 securities, permitting the analysis of the

impact using a DID approach. Second, the pilot only lasted for four months in 2015, enabling us to

compare PilotOn with PilotOff events. Third, Nasdaq data allow us to analyze how HFT reacts to the

maker-taker fee reduction compared with non-HFT across different resting order types, giving us new

insights into the nature of HFT.

Our results show that when Nasdaq reduces the maker-taker fee unilaterally without the cooperation of

other exchanges, there are no significant changes in the market share of off-exchange trading venues (we

classify these into dark pools and non-dark pools). Instead, we observe a redistribution effect among

exchanges, whereby the reduced Nasdaq market share tends to shift to exchanges with higher maker

rebates. Hence, holding the exchange net fee relatively constant, when the maker rebate reduces, the

queue of Nasdaq limit orders shrinks, as evidenced by the drop in the percentage of time and depth at the

National Best Bid and Offer (NBBO).

Because the taker fee of removing liquidity declined (i.e., the explicit tax on buyer- and seller-initiated

trades fell), more market orders are submitted since they are less costly to trade. Moreover, the fill ratio

and speed of fill increased as a wider class of investors could now profit with the lowered taker fee.

Prior to the experimental pilot, the high taker fee discouraged all but relatively informed investors owing

to the relative position of a market in routing tables. Since the exchange access fee is a material portion

of the transaction cost given a stock is tick constrained, if one exchange’s taker fee is relatively high,

such a market tends to be ranked relatively low in the routing table. Thus, only the most informed orders

11

are likely to reach it. Recall that traders possessing relatively short-lived information require immediate

(liquidity taking) execution and hence are the most willing to pay the taker tax. With the lower access

fee, Nasdaq would have moved up in the tables. Hence, we predict that the information content of trade

will decline. The thinner limit order book deprived of its former subsidies becomes less attractive for

informed traders and these are likely to switch to other exchanges that have retained their high liquidity

subsidies in a competitive environment. Realized spreads should then increase to reflect the high but

falling proportion of informed traders, but the cum-rebate (i.e., the net realized spread) decreases

because of the smaller proportion of informed traders hitting limit orders. Hence, not only does the pilot

reduce the net realized spread, but also the effective spread and market impact costs lower, which are all

indicators of the switch in the informed order flow toward other high-rebate venues. As a net result, the

Nasdaq market share declines on average and is captured by the other high rebate-paying exchanges in

close competition with Nasdaq. This finding indicates that the components of the exchange access fee do

matter in a competitive trading environment.

Since the provision of liquidity to highly informed traders is specialized, we also find a more than

proportionate departure of HFT from the provision of liquidity but, more surprisingly, there is no net

loss in HFT, as there is a shift to the expanding sector engaged in removing liquidity (i.e., market

orders). One explanation, according to the SEC (2010) concept release, is the rebate capture by HFT;

however, more relevant is the contribution of the speed of execution when dealing with highly informed

order flows.

The rest of the paper is organized as follows. Section II discusses the institutional details. Section III

describes the data, sample selection, and research methodology. Section IV tests our empirical

predictions on trading volume, market liquidity, and HFT trading behavior. Section V presents the

results of our robustness tests and Section VI concludes.

II. Institutional Details

In this section, we describe the U.S. stock exchanges, off-exchange trading, and securities information

processor (SIP) data. The following 11 lit exchanges account for approximately 65% of the market share

12

in U.S. equities7: BATS Exchange (BATS), BATS Y Exchange (BATS Y), Chicago Stock Exchange

(CHX), EDGA Exchange (EDGA), EDGX Exchange (EDGX), NASDAQ BX (BX), NASDAQ PHLX

(PSX), Nasdaq Stock Market (NASDAQ), New York Stock Exchange (NYSE), NYSE MKT (AMEX),

and NYSE Arca (ARCA). Among these 11 lit exchanges, NASDAQ, BX, and PSX are within the

NASDAQ group (18.2% market share); NYSE, ARCA, and AMEX are within the Intercontinental

Exchange group (24.6%); and BATS, BATS Y, EDGA, and EDGX are within BATS Global Markets

(21.6% ) and Chicago Stock Exchange (0.6% of total market share)8. At the exchange level, NASDAQ

has the largest market share (approximately 15%) followed by NYSE and ARCA. NASDAQ follows the

price, display type, and time execution priority model.

Off-exchange trades for NMS stocks, which account for about 35% of total volume, need to be reported

to FINRA trade reporting facility (TRF) by members for which the Participant ID (Pid) is D in

centralized SIP data. FINRA has established two TRFs in conjunction with NASDAQ and NYSE9. U.S.

equities trade execution venues can be classified into three main categories: exchanges, dark pools, non-

dark pools off-exchange venues which consists of ECNs10, voice-brokered trades, and broker-dealer

internalization. Dark pools and ECNs are also called ATSs. The primary difference between an ATS

(typically operated by broker-dealers) and an exchange includes less regulatory scrutiny, fewer reporting

requirements, and restricted access.

III. Data, Sample Selection, and Methodology

A. Data source

Our analysis is based on trader-level data and U.S. SIP data. Our HFT data are identified by Nasdaq

based on the method described in Brogaard, Hendershott, and Riordan (2014). We analyze the effect of

Nasdaq’s fee pilot for an eight-month window (December 1, 2014 to July 31, 2015), which is two

7 The CBOE Stock Exchange and National Stock Exchange, Inc. ceased market operations on April 30, 2014 and May 30, 2014, respectively. 8 Nasdaq Trader website in December 2015: http://nasdaqtrader.com/trader.aspx?id=FullVolumeSummary. 9 FINRA Trade Reporting FAQ: http://www.finra.org/industry/trade-reporting-faq. 10 ECNs are prohibited from listing stocks and are not self-regulating organizations. The only remaining ECN in the United States, LavaFlow owned by Citi, ceased market operations on January 30, 2015.

13

months before to two months after the introduction of the maker-taker fee pilot, which ran from

February 2, 2015 to May 31, 2015. We exclude the half-day trading on Christmas Eve.

Our data include all information on order submission and trades, including price, volume, and a unique

identifier for the trader that submitted the order, which allow us to construct the HFT data. We restrict

our attention to transactions that occur in the limit order book and trades during regular trading hours.

For each limit order book transaction, the data contain identifiers for buyer- or seller-initiated trade,

adding or removing liquidity, and types of liquidity (such as displayed, non-displayed midpoint, and

non-displayed non-midpoint). Further, our ATS data are provided via www.FINRA.org/ATS,

copyrighted by FINRA 2015. ATS data is reported weekly. Our 38 dark pools list is taken from the SEC

report on the “Regulation of NMS Stock Alternative Trading Systems.”

B. Sample selection

Nasdaq introduced a maker-taker fee reduction only for 14 stocks (seven listed on Nasdaq—AAL, MU,

FEYE, GPRO, GPRN, SIRI, and ZNGA—and seven listed on the NYSE—BAC, GE, KMI, RAD, RIG,

S, and TWTR). We use the remaining companies on each corresponding listing exchange to find a one-

to-one control group without replacement to ensure that our results are not driven by market-wide,

exchange-wide, or industry-wide fluctuations. Moreover, we exclude securities that had stock splits,

switched listing exchange, or had days with a stock price below $1. In our sample, the minimum trade

count per stock per day is 450.

Our control sample matches listing exchange, closing price, market capitalization, and average daily

trading volume (ADV) based on one month prior our sample period data. Davies and Kim (2009) argue

that one-to-one matching without replacement based on closing price and market capitalization is the

most appropriate method to test for differences in trade execution costs. O’Hara and Ye (2011) followed

their approach and matched on closing price, market capitalization and listing exchange. We add ADV

as a matching criterion since this study focuses not only on trade execution costs but also on trader

behavior.

14

In addition, we randomize the matching order by sorting the stocks in the treatment group alphabetically

by ticker symbol. The match for each treatment group security i is then defined to be the control group

security j that minimizes the following matching error:

𝑚𝑚𝑚𝑚𝑚𝑚𝑚𝑚ℎ𝑒𝑒𝑒𝑒𝑒𝑒𝑒𝑒𝑒𝑒𝑖𝑖𝑖𝑖 = �𝐶𝐶𝐶𝐶𝑖𝑖−𝐶𝐶𝐶𝐶𝑗𝑗𝐶𝐶𝐶𝐶𝑖𝑖+𝐶𝐶𝐶𝐶𝑗𝑗

� + �𝑀𝑀𝐶𝐶𝑖𝑖−𝑀𝑀𝐶𝐶𝑗𝑗𝑀𝑀𝐶𝐶𝑖𝑖+𝑀𝑀𝐶𝐶𝑗𝑗

� + �𝐴𝐴𝐴𝐴𝐴𝐴𝑖𝑖−𝐴𝐴𝐴𝐴𝐴𝐴𝑗𝑗𝐴𝐴𝐴𝐴𝐴𝐴𝑖𝑖+𝐴𝐴𝐴𝐴𝐴𝐴𝑗𝑗

�,

where CP, MC, and ADV denote the security’s closing price, market capitalization as of the end of

November 2014, and average November 2014 ADV on its corresponding listing exchange (i.e., Nasdaq

or NYSE), respectively. Our panel regression analysis employs a DID approach to account for market-

wide fluctuations. The estimation is based on the following DID regression specification:

𝑌𝑌𝑖𝑖𝑖𝑖 = 𝛼𝛼0 + 𝛼𝛼1𝑇𝑇𝑒𝑒𝑒𝑒𝑚𝑚𝑚𝑚𝑖𝑖 + 𝛼𝛼2𝑃𝑃𝑃𝑃𝑃𝑃𝑒𝑒𝑚𝑚𝑃𝑃𝑃𝑃𝑖𝑖 + 𝛽𝛽1𝑇𝑇𝑒𝑒𝑒𝑒𝑚𝑚𝑚𝑚𝑖𝑖 ∗ 𝑃𝑃𝑃𝑃𝑃𝑃𝑒𝑒𝑚𝑚𝑃𝑃𝑃𝑃𝑖𝑖 + 𝛾𝛾𝑉𝑉𝑉𝑉𝑉𝑉𝑖𝑖 + 𝜑𝜑𝑉𝑉𝑖𝑖 + 𝜖𝜖𝑖𝑖𝑖𝑖 , (1)

where 𝑌𝑌𝑖𝑖𝑖𝑖 is the dependent variable; 𝛼𝛼0 is the intercept; 𝑇𝑇𝑒𝑒𝑒𝑒𝑚𝑚𝑚𝑚𝑖𝑖 is the dummy variable if security i is a

pilot stock; PilotOn is the dummy variable that is one if date t is during the pilot period and zero

otherwise; 𝑉𝑉𝑉𝑉𝑉𝑉𝑖𝑖 is the closing value of CBOE’s volatility index for day t; and 𝑉𝑉𝑖𝑖 is the vector of

security-level control variables including the log of the average closing price during the sample period,

the log of the average market capitalization during the sample period, and average volatility, measured

by daily high price minus daily low price over closing price, during the sample period. We estimate the

specification with and without stock fixed effects.

Table 3 reports the summary statistics across U.S. equity trading venues for our sample of 28 stocks

between December 1, 2014 and July 31, 2015. The sample period is divided into two parts: (i) the pilot

period between February 2, 2015 and May 31, 2015 and (ii) the two months before and after the pilot

from December 1, 2014 to February 1, 2015 and June 1, 2015 to July 31, 2015. The Nasdaq market

share dropped by 1.45% on average during the pilot period, while the average price and market

capitalization remained relatively stable. The Nasdaq depth at the NBBO and depth share declined,

while the fill ratio and speed of fill improved. The raw effective spread increased, while the realized

spread decreased, and the price impact decreased. By using Nasdaq data, we found that HFT changed

trading behavior from adding liquidity (dropped by 10.04%) to taking liquidity (increased by 9.94%)

after the reduction of the maker rebate and taker fee. The decline in HFT adding liquidity mainly came

from the displayed liquidity type.

15

<Insert Table 3 here>

IV. Empirical Results

A. Market quality and the information content of trades

A1. How does the Nasdaq percentage of time at the NBBO, market depth, and fill rate change?

Prediction: When Nasdaq reduces the rebate, the incentive to post liquidity is reduced, resulting in less

quoting on Nasdaq at the NBBO. Thus, the Nasdaq percentage of time at the NBBO and corresponding

depth and depth share will drop. After the taker fee is reduced, the fill rate and speed of fill is expected

to increase.

Result: After the maker rebate was reduced, the Nasdaq queue in the limit order book lowered. Table 4

shows that the Nasdaq percentage time and depth at the NBBO declined. The drop in the depth share at

the NBBO (coefficient of -4.010*** in Table 4) is much larger compared with the slightly decrease in

market share (coefficient of -1.451*** in Table 7). This finding indicates Nasdaq’s quote became

relatively more attractive and their routing table position may have risen. Further, when the taker fee

was reduced, the fill rate and speed of fill increased, since afterwards it was cheaper to remove liquidity

by using market orders.

<Insert Table 4 here>

A2. How do the quoted spread, effective spread, realized spread, and price impact change?

Prediction: Malinova and Park (2015) find that prices adjust as the maker rebate changes, using the TSX

pricing change in 2005. In particular, holding the total fee constant, the raw bid-ask spread declines as

the maker rebate increases. In addition, they show that the effective spread declines as the taker fee

increases, consistent with the finding of Colliard and Foucault (2012). As the quoted spread declines,

market orders become relatively cheap for these traders and more thus prefer market orders to limit

16

orders. Brolley and Malinova (2012) show that this behavior is an equilibrium outcome, with the

increased use of market orders causes a decline in adverse selection.

The quoted spread is the difference between the ask price and bid price. Specifically,

𝑞𝑞𝑞𝑞𝑞𝑞𝑒𝑒𝑒𝑒𝑚𝑚𝑞𝑞𝑖𝑖,𝑖𝑖 = 𝑚𝑚𝑖𝑖,𝑖𝑖 − 𝑏𝑏𝑖𝑖,𝑖𝑖, (2)

The effective spread is twice the signed difference between the transaction price and the midpoint of the

bid and offer quotes at the time of the transaction. Specifically,

𝑒𝑒𝑞𝑞𝑞𝑞𝑒𝑒𝑒𝑒𝑚𝑚𝑞𝑞𝑖𝑖,𝑖𝑖 = 2 ∗ 𝑞𝑞𝑖𝑖,𝑖𝑖 ∗ (𝑞𝑞𝑖𝑖,𝑖𝑖 − 𝑚𝑚𝑖𝑖,𝑖𝑖), (3)

The realized spread is a measure of profit to market makers. Previous studies have set τ to five minutes

after the trade. The choice of this time horizon should be sufficiently long to incorporate the permanent

impact of the trade and thus to ensure that quotes are subsequently stabilized, temporary effects are

dissipated, and there is a sufficiently long period for liquidity providers to close their positions (Conrad,

Wahal, and Xiang, 2015). In today’s ultra-high frequency trading environment that has upgraded trading

systems with an accuracy of mere nanoseconds, five minutes is excessively long. Similar to Conrad,

Wahal, and Xiang (2015), we estimate realized spreads from one second to five seconds after each trade.

The realized spread is then calculated as twice the signed difference between the transaction price and

the midpoint of the bid and offer quotes one second and five seconds after the transaction. Specifically,

𝑒𝑒𝑞𝑞𝑞𝑞𝑒𝑒𝑒𝑒𝑚𝑚𝑞𝑞𝑖𝑖,𝑥𝑥𝑖𝑖 = 2 ∗ 𝑞𝑞𝑖𝑖,𝑖𝑖 ∗ (𝑞𝑞𝑖𝑖,𝑖𝑖 − 𝑚𝑚𝑖𝑖,𝑖𝑖+𝜏𝜏), (4)

Price impact is defined as the signed change between the midpoint of the quote one second and five

seconds after the trade and the midpoint of the prevailing quote at the time of the trade. It captures the

information that is revealed by the trade. A decline in the price impact indicates a decline in adverse

selection costs. Specifically,

𝑞𝑞𝑒𝑒𝑃𝑃𝑚𝑚𝑒𝑒 𝑃𝑃𝑚𝑚𝑞𝑞𝑚𝑚𝑚𝑚𝑚𝑚𝑖𝑖,𝑖𝑖 = 2 ∗ 𝑞𝑞𝑖𝑖,𝑖𝑖 ∗ (𝑚𝑚𝑖𝑖,𝑖𝑖+𝜏𝜏 − 𝑚𝑚𝑖𝑖,𝑖𝑖), (5)

To test whether the fee change truly matters, we also compute the cum fee quoted spread, cum fee

effective spread, and cum rebate realized spread as follows:

𝑚𝑚𝑐𝑐𝑚𝑚 𝑓𝑓𝑒𝑒𝑒𝑒 𝑞𝑞𝑞𝑞𝑞𝑞𝑒𝑒𝑒𝑒𝑚𝑚𝑞𝑞𝑖𝑖,𝑖𝑖 = �𝑚𝑚𝑖𝑖,𝑖𝑖 − 𝑏𝑏𝑖𝑖,𝑖𝑖� + 2 ∗ 𝑓𝑓𝑖𝑖,𝑖𝑖, (6)

17

𝑚𝑚𝑐𝑐𝑚𝑚 𝑓𝑓𝑒𝑒𝑒𝑒 𝑒𝑒𝑞𝑞𝑞𝑞𝑒𝑒𝑒𝑒𝑚𝑚𝑞𝑞𝑖𝑖,𝑖𝑖 = 2 ∗ 𝑞𝑞𝑖𝑖,𝑖𝑖 ∗ �𝑞𝑞𝑖𝑖,𝑖𝑖 − 𝑚𝑚𝑖𝑖,𝑖𝑖� + 2 ∗ 𝑓𝑓𝑖𝑖,𝑖𝑖, (7)

𝑚𝑚𝑐𝑐𝑚𝑚 𝑒𝑒𝑒𝑒𝑏𝑏𝑚𝑚𝑚𝑚𝑒𝑒 𝑒𝑒𝑞𝑞𝑞𝑞𝑒𝑒𝑒𝑒𝑚𝑚𝑞𝑞𝑖𝑖,𝑥𝑥𝑖𝑖 = 2 ∗ 𝑞𝑞𝑖𝑖,𝑖𝑖 ∗ �𝑚𝑚𝑖𝑖,𝑖𝑖+𝜏𝜏 − 𝑚𝑚𝑖𝑖,𝑖𝑖� + 2 ∗ 𝑒𝑒𝑖𝑖,𝑖𝑖, (8)

where 𝑓𝑓𝑖𝑖,𝑖𝑖 is the taker fee for security i at time t, 𝑒𝑒𝑖𝑖,𝑖𝑖 is the maker rebate for security i at time t, 𝑚𝑚𝑖𝑖,𝑖𝑖 is the

ask price of the quote, where 𝑏𝑏𝑖𝑖,𝑖𝑖 is the bid price of the quote, 𝑞𝑞𝑖𝑖,𝑖𝑖 is the transaction price for security i

at time t, 𝑚𝑚𝑖𝑖,𝑖𝑖 is the midpoint of the prevailing quote at the time of the trade, 𝑚𝑚𝑖𝑖,𝑖𝑖+𝜏𝜏 is the midpoint of

the one second and five seconds after the trade, and 𝑞𝑞𝑖𝑖,𝑖𝑖 is an indicator variable that equals one if the

trade is buyer-initiated and minus one if the trade is seller-initiated. Our data report the prevailing quotes

as well as contain a marker that signs each trade as buyer- or seller-initiated.

Result: Tables 5a and 5b shows the cum fee quoted spread and cum fee effective spread decrease

(coefficients of -0.215*** and -0.438***, respectively), which is inconsistent with the findings of

Malinova and Park (2015). The cum fee quoted and effective spreads are adjusted by the taker fee, while

the cum rebate realized spread is adjusted by the maker rebate. However, we find that the price impact

declined (-0.232*** for the one second price impact and -0.304*** for the five second price impact)

after the maker-taker fee reduction. This decrease may have been caused by the relative position of a

market in routing tables. In other words, if a market is ranked low in the routing table, only the most

informed orders are likely to reach it. With a lower access fee, Nasdaq would have risen in the tables

and depth reduced, resulting in a reduction in the price impact. Further, owing to the less competition in

the limit order flow, the realized spread increases, while after taking into account the rebate reduction,

the cum rebate spread decreases.

Discussion

The inconsistency between our spread and price impact findings and those of Malinova and Park

(2015)11 may be driven by the different trading environments analyzed. In 2005, TSX was the only stock

exchange in Canada; however, our study of U.S. markets comprised 11 competing lit exchanges and

many more off-exchange trading venues. In addition, liquidity suppliers have two main sources of 11 The liquidity supplier does not necessarily need to adjust the realized spread since the trader has only the one trading venue to trade; hence, the realized spread does not change and the cum rebate realized spread increases.

18

revenue: the bid ask spread and rebate. Since traders had limited choices about where to trade in Canada

in 2005, the impact rebate increase accompanied with increased fee had to be adjusted within TSX.

Colliard and Foucault (2012) predict that the effective spread declines as the taker fee increases.

Because the cost of market orders increases if the taker fee increase, traders switch to limit orders and

the spread decreases.

By contrast, in our competitive trading environment, when Nasdaq decreases the maker rebate, traders

may post liquidity on other exchanges with a higher rebate. Hence, although the effective spread

increases, we find a decreased cum fee effective spread because of the lower amount of information (i.e.,

lower toxicity) in the order flow as a result of the change in order routing. To compensate the liquidity

supplier for the rebate loss, the realized spread must be widened for a given order flow type. After the

rebate reduction is adjusted, the cum rebate realized spread decreases, indicating that the order flow is

likely to be less informed. The high maker rebate financed with the high taker fee may attract informed

traders given the other cheaper venues for removing liquidity, because the high rebate attracts a thick

limit order book, which is particularly beneficial for informed traders. When the rebate is reduced, the

limit order book gets thinner, which is less attractive to informed traders, although it is less costly to

remove liquidity via a market order. As a net effect, we find that the information content of the order

flow declines.

<Insert Tables 5a and 5b here>

A3. How does market efficiency change?

Prediction: To test the informational efficiency of prices, we use variance ratio tests of the random walk

hypothesis (Lo and MacKinlay, 1988) and autocorrelation, which are identified as the two information-

associated measures in Chordia, Roll, and Subrahmanyam (2008), in multiple time intervals:

𝑉𝑉𝑚𝑚𝑒𝑒𝑃𝑃𝑚𝑚𝑃𝑃𝑚𝑚𝑒𝑒 𝑒𝑒𝑚𝑚𝑚𝑚𝑃𝑃𝑒𝑒 = 𝑣𝑣𝑚𝑚𝑒𝑒�𝑒𝑒𝑖𝑖,𝑖𝑖� ∗ 𝑥𝑥/𝑣𝑣𝑚𝑚𝑒𝑒(𝑒𝑒𝑖𝑖,𝑥𝑥∗𝑖𝑖), (9)

𝐴𝐴𝑐𝑐𝑚𝑚𝑒𝑒𝑚𝑚𝑒𝑒𝑒𝑒𝑒𝑒𝑒𝑒𝑃𝑃𝑚𝑚𝑚𝑚𝑃𝑃𝑒𝑒𝑃𝑃 = 𝐶𝐶𝑒𝑒𝑒𝑒𝑒𝑒(𝑒𝑒𝑖𝑖,𝑖𝑖, 𝑒𝑒𝑖𝑖,𝑖𝑖−1), (10)

19

where 𝑣𝑣𝑚𝑚𝑒𝑒�𝑒𝑒𝑖𝑖,𝑖𝑖� refers to the variance of the return during the 𝑚𝑚𝑖𝑖ℎ time interval for i, 𝑣𝑣𝑚𝑚𝑒𝑒(𝑒𝑒𝑖𝑖,𝑥𝑥∗𝑖𝑖) refers to

the variance of the return during the x*t time interval for i and 𝐶𝐶𝑒𝑒𝑒𝑒𝑒𝑒(𝑒𝑒𝑖𝑖,𝑖𝑖, 𝑒𝑒𝑖𝑖,𝑖𝑖−1) refers to the

autocorrelation of the midpoint return during the 𝑚𝑚𝑖𝑖ℎ time period for i. Specifically, when a stock’s price

follows a random walk, the variance of its returns is a linear function of the measurement frequency, i.e.

𝑣𝑣𝑚𝑚𝑒𝑒(𝑒𝑒𝑖𝑖,𝑥𝑥∗𝑖𝑖) is k times larger than 𝑣𝑣𝑚𝑚𝑒𝑒�𝑒𝑒𝑖𝑖,𝑖𝑖�.

When the maker-taker fee is reduced, we find that liquidity worsens (see the results presented above)

and there is less information in the order flow. Thus, we expect the informational efficiency of prices to

decrease.

Result: Table 6 shows that in response to the maker-taker fee reduction, the variance ratios in Nasdaq

generally increased, while first-order return autocorrelations declined. This pattern suggests that the

variance ratios rise because of increased mispricing, with less private information being reflected in

prices following the maker-taker fee reduction. Compared with Nasdaq, the market efficiency of the

three other highest rebate-paying exchanges (Arca, BATS Z, NYSE) become less bad than Nasdaq given

overall market efficiency declines.

<Insert Table 6 here>

B. Trading volume and market share

B1. Does a reduced exchange access fee attract trading volume from off-exchange venues?

Prediction: The Nasdaq access fee pilot aimed to test whether a lower exchange access fee can raise the

market share of off-exchange venues. In this regard, the SEC (2014) filing states the following: “Off-

exchange orders do not generate quotes on public markets, do not interact with orders on public

markets and consequently do not promote or contribute to price discovery to the same extent as do

orders posted and executed on exchanges. Economic studies from markets spanning the world conclude

that as more orders migrate away from exchanges, the price discovery process weakens, trading spreads

widen, and overall investor trading costs increase… Nasdaq believes that proposed changes may

improve price discovery in the select securities.” Kwan, Masulis, and McInish (2015) find that the U.S.

20

minimum tick constrains some stock spreads, causing large limit order queues, and that dark pools allow

traders to bypass existing limit order queues with minimal price improvement. Moreover, Foley and

Putniņš (2014) find that when Canada and Australia implemented minimum price improvement, the

level of dark trading decreased. We expect no change in dark pools trading volume after the maker-taker

fee reduction since their ability to circumvent the time priority of displayed limit orders is not affected

and nor are they required to provide price improvement.

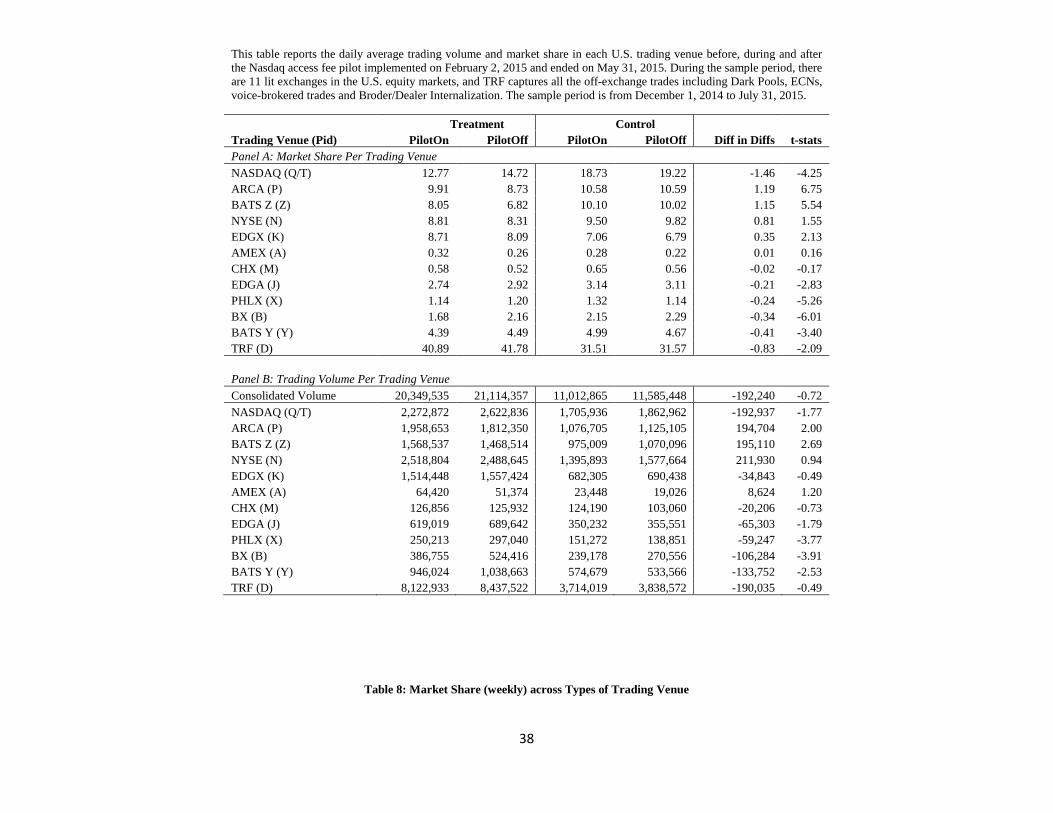

Result: Table 7 shows that after the Nasdaq fee reduction, the Nasdaq market share declined on average

(see also Hatheway, 2015a, 2015b), while the consolidated trading volume remained stable and the share

losses was captured by the other three highest rebate-paying stock exchanges (ARCA, BATS Z, NYSE).

Table 8 shows that when Nasdaq reduced the maker rebate and taker fee, there was no significant market

share drop from the off-exchange trading venues of dark pools and other non-dark pools. Instead, we

observe a redistribution of market share among lit exchanges (i.e., the lost market share shifted to those

lit exchanges with the highest liquidity provision rebate). One argument could be that only Nasdaq

reduce the access fee unilaterally during the pilot during the competitive trading environment. Dark

pools rely on mid-point prices and are protected by the inability of lit exchanges to reduce the minimum

tick size because of the SEC’s regulations. Instead, we observe a redistribution effect among existing lit

exchanges. Even with a uniform fee reduction across the entire lit market, a movement toward the lit

market is unlikely as dark pools can still undercut the 1 cent tick rule and there is still no requirement to

provide the minimum price improvement which, in any case, could be illusory.

<Insert Table 7 here>

<Insert Table 8 here>

B2. How does the lit exchange trading volume and market share change in response to the maker-taker

fee reduction?

Prediction: In traditional maker-taker markets, the liquidity rebate, which is financed by a taker fee, is

initially designed to increase liquidity. If the liquidity rebate is reduced, the trading volume and market

share tends to decline. More specifically, when the rebate is reduced, the incentive to post limit orders

21

on Nasdaq is reduced, the queue of limit orders declines, and the limit orders tend to flow to other

exchanges with higher rebate payments. However, this effect is offset by the reduced taker fee since it is

cheaper to remove liquidity as well. Overall, the Nasdaq market share declines since trade only occurs

when there is liquidity supply, and the reduced volume goes to other exchanges with higher incentives.

Result: Cardella, Hao, and Kalcheva (2015) find that reductions in relative taker fees in U.S. equity

markets are associated with increased market share. Malinova and Park (2015) argue that the change in

the maker-taker fees in Cardella, Hao, and Kalcheva (2015) are accompanied by changes in the total fee.

Indeed, Malinova and Park (2015) find that holding the total exchange fee constant, TSX’s trading

volume in 2005 was unaffected by the component change.

However, the DID regression model in Table 9 shows that the Nasdaq market share decreases in

response to the maker-taker fee reduction. To verify whether this reduced market share is caused by a

reduction in liquidity supply, we compare the Nasdaq depth at the NBBO change with the Nasdaq

trading volume change. We find that the Nasdaq depth at the NBBO (coefficient of -0.337*** in Table

4) dropped about three times more than the Nasdaq trading volume drop (coefficient of -0.131*** in

Table 9). We also did further statistical test and find statistically significant relationship between Nasdaq

market share and depth at the NBBO. This finding indicates that the reduced Nasdaq market share is

also associated with the drop in the depth at the NBBO.

<Insert Table 9 here>

B3. How do the Nasdaq routing dynamics change?

Prediction: Reg NMS Rule 61112, also known as the “Order Protection Rule” or “Trade-through” rule,

restricts trading, either as agent or principal, on one venue at prices inferior to the displayed quotations

at another trading venue during regular trading hours (9:30 am to 4:00 pm ET). Thus, if one exchange

does not have the NBBO when it receives incoming orders and if it is eligible for immediate electronic 12 “Rule 611 does not affirmatively require the routing of orders to trading venues displaying the best prices. Rather, it only restricts trades at prices worse than a protected quotation. Any trading venue is free to execute trades at prices equal to or better than a protected quotation, regardless of whether such a trading center is currently quoting at that price or is a dark venue that never displays quotations.” (SEC, 2015b).

22

execution, it is obligated to route the incoming order to another trading venue with the NBBO. After the

Nasdaq rebate is reduced, the incentive to submit nonmarketable orders on Nasdaq decreases. Thus, the

Nasdaq percentage of time at the NBBO is likely to decline and outbound routing is likely to increase.

Result: Table 9 shows that the Nasdaq incoming orders routed to Nasdaq declined and that the

proportion routed away to other exchanges increased. Moreover, the percentage of volume routed to off-

exchange trading venues remained stable.

C. HFT vs. non-HFT trading behavior

C1: HFT vs. non-HFT adding/taking liquidity_volume

Prediction: SEC (2010) summarizes that one HFT strategy is passive market making to earn the

liquidity rebate, which primarily involves the submission of nonmarketable resting orders (limit bids and

offers) that provide liquidity to the marketplace at specified prices. This is not a discerning observation

since all liquidity providers aim to gain rebates, especially when realized spreads are negative; however,

HFT arguably has a speed advantage.

In Rosu’s (2015) model, the trader who sees a signal containing information before a slower trader will

take liquidity as he is informed. Nevertheless, as holding inventory is expensive, a risk-averse trader

reverses part of his order to make money supplying liquidity to slower traders who receive a delayed

signal. The fast trader could even post some of these reversed trades as limit orders. Hence, HFT traders

are likely to have information and thus take liquidity but can also make liquidity. As both the rebate and

the tax on liquidity makers fall, HFT traders are likely to shift from making to taking liquidity.

Result: Table 10 shows that in response to the maker-taker fee reduction, HFT traders switched trading

behavior on Nasdaq from posting liquidity (coefficient of -10.043***) to taking liquidity (coefficient of

9.936***), as predicted, while the overall Nasdaq HFT volume remained stable (coefficient of -0.054

with no statistical significance).

<Insert Table 10 here>

23

C2: HFT vs. non-HFT adding and taking liquidity_spreads and price impact

Prediction: Carrion (2013) finds that spreads are wider (tighter) when HFT traders provide (take)

liquidity, which suggests HFTs provide liquidity when it is scarce and consume liquidity when it is

plentiful. Because of their effective real-time forecasting of the state of the market, HFT traders face

lower adverse selection costs than non-HFT traders when supplying liquidity in larger trades, suggesting

they have an informational advantage when demanding liquidity and avoiding the supply of liquidity to

informed traders. SEC (2010) thus questions whether “rebates generally benefit long-term investors by

promoting narrower spreads and more immediately accessible liquidity?”

Result: Focusing on the cum fee/rebate column in Table 11, we analyze the net effect of the participation

of the two trader types after taking into account the tax/subsidy alteration, the effective spread for HFT

is lower compared with non-HFT when placing market orders, with the spread sizably reduced for both

types because of the removal of the tax on market orders. This is because HFT market orders are less

informed than non-HFT market orders as the market impact over both the one-second and the-five

second intervals falls by a larger amount than that for non-HFT, such that the fall in the realized spread

is less for HFT market orders.

HFT is therefore more inclined to add to liquidity relative to non-HFT when the effective spread is

narrower because of its relatively less informed order flow, as shown by both the one-second and the

five-second delay price impacts being relatively low. As a consequence, the realized spread is higher

when HFT traders provide liquidity relative to non-HFT traders. These findings imply that HFT is more

likely to take liquidity when it is relatively plentiful (spreads are narrow and consistent with Carrion

(2013)) and provide liquidity when it is relatively cheap (the effective spread is relatively narrow), as it

uses its informational advantage to supply liquidity to less informed counterparts.

Discussion

Subsidized limit orders and taxed market orders benefit relatively informed short-term traders, as can be

seen when Nasdaq’s unilateral withdrawal of the subsidy and tax during the pilot led to the movement of

such traders to exchange with higher subsidy/tax regimes. Insofar as long-term investors are also

informed, high subsidy/tax regimes might also benefit them; however, but if they are not informed then

24

they may be better off without the subsidy/tax regime as their trades are infrequent and thus they gain

little from a subsidized spread.

<Insert Table 11 here>

D. Adding liquidity by submitting different types of resting orders

Prediction: In lowering the taker fee to remove liquidity to 5 CPS traded, Nasdaq reduced the rebate by

varying levels for different order types (displayed, non-displayed midpoint, non-displayed non-

midpoint), We predict that, trading volume and percentage of HFT adding liquidity will differ across

order types. For non-displayed non-midpoint liquidity (which accounts for about 3% of total volume),

unlike the other two types of liquidity, the net fee reduced significantly. Hence, we predict that trading

volume and the percentage of HFT adding liquidity increases.

Result: Table 12 shows that the overall percentage of displayed and non-displayed midpoint volume

reduced (coefficients of -0.316 and -0.194, respectively) but that the fall is not statistically significant;

moreover, the percentage of non-displayed non-midpoint volume increase (coefficient of 0.615***). In

terms of HFT in different liquidity types, the percentage of HFT adding displayed liquidity and HFT

non-displayed midpoint volume decreased (coefficients of -9.357*** and -0.756***, respectively)

significantly. The percentage of HFT non-displayed non-midpoint volume increased (coefficient of

0.175***). In sum, the major HFT liquidity enhancing comes from displayed liquidity, as predicted.

<Insert Table 12 here>

V. Robustness Test

To explore the robustness of our strikingly different results to those presented by previous studies, we

change the matching variable used to identify the control sample. An obvious alternative was to

25

construct the control sample by using only the price and ADV selection criteria in line with the sample

in the Nasdaq fee pilot report. The results are qualitatively consistent.

A second robustness test involved normalizing our dependent variables. We compute the quote spread,

effective spread, realized spread, and price impact (both one second and five second) in bps rather than

cents (see Table 13). Again, the results are generally consistent.

<Insert Table 13 here>

VI. Conclusion

This study analyzes how a reduction in the maker-taker fee affects market competition, liquidity, and

HFT. The current literature holds that only changes in the net exchange fee matter for market quality and

transaction cost efficiency. Our findings show that holding the net fee relatively constant, the change in

component fees and rebates does matter, but not for competition between market and non-market

venues. When Nasdaq’s fee pilot reduced both the fee and the rebate, its market share declined and the

reduced amount was shared by the other high rebate-paying exchanges. We find that the equivalently

reduced fee and rebate lowers quote quality and routed volume to Nasdaq. However, it improves the fill

rate and speed of fill because of the reduced taker fee. When Nasdaq’s relative routing position

improves, adverse selection costs decline and liquidity supplier profit increases (but the cum rebate

realized spread decreases). In addition, the decline in informed order flows on Nasdaq owing to the fall

in liquidity leads to a decline in market efficiency. The fall in Nasdaq’s market share indicates the strong

benefit of its existing strategy of providing the highest possible subsidy to liquidity takers funded by its

tax on liquidity makers and this also encourages better price discovery and higher market efficiency.

Whether high exchange access fees cause trading to shift away from public markets, using the Nasdaq

access fee pilot as a natural experiment. We find no evidence for such a shift, perhaps because only one

exchange reduced its access fee unilaterally in a competitive trading environment. However, even if all

lit exchanges had participated, the outcome may have remained the same, as the net fee does not

substantially alter and nothing fundamental changes in the competition between market and off-market

venues.

26

Further, we have shown that as exchange access fees and rebates decrease, HFT traders tend to switch

from adding to removing liquidity. While standard quality measures such as the effective spread,

realized spread, and market impact costs all appear to improve on a cum rebate basis, these apparent

improvements reflect the lower information content in Nasdaq’s order flow during the experiment as

informed order flows shift to exchanges that maintain high rebates. Even when HFT increases liquidity

taking as it retreats from making liquidity, it does so with a less informative order flow.

27

References

Angel, James, Lawrence Harris, and Chester S. Spatt, 2011, Equity trading in the 21st century, Quarterly

Journal of Finance 1, 1–53.

Angel, James, Lawrence Harris and Chester S. Spatt, 2015, Equity trading in the 21st century: An

Update, Quarterly Journal of Finance 5, 1-39.

Barclay, Michael J., Eugene Kandel, and Leslie M. Marx, 1998, The effects of transaction costs on stock

prices and trading volume, Journal of Financial Intermediation 7, 130–150.

Battalio, Robert H., Shane A. Corwin and Robert Jennings, 2016, Can brokers have it all? On the

relation between make-take fees and limit order execution quality, Journal of Finance, forthcoming.

Brogaard, Jonathan, Terrence Hendershott, and Ryan Riordan, 2014, High-frequency trading and price

discovery, Review of Financial Studies 27, 2267–2306.

Brolley, Michael, and Katya Malinova, 2012, Informed trading and maker-taker fees in a low latency

limit order market, Working Paper, University of Toronto.

Cardella, Laura, Jia Hao, and Ivalina Kalcheva, 2015, Make and Take Fees in the U.S. Equity Market,

Working Paper, Texas Tech University.

Carrion, Allen, 2013, Very fast money: High-frequency trading on the NASDAQ, Journal of Financial

Markets 16, 680–771.

Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam, 2008, Liquidity and market efficiency,

Journal of Financial Economics 87, 249–268.

Colliard, Jean-Edouard, and Thierry Foucault, 2012, Trading fees and efficiency in limit order markets,

Review of Financial Studies 25, 3389–3421.

28

Conrad, Jennifer, Sunil Wahal, and Jin Xiang, 2015, High-frequency quoting, trading, and the efficiency

of prices, Journal of Financial Economics 116, 271–291.

Davies, Ryan J., and Sang Soo Kim, 2009, Using matched samples to test for differences in trade

execution costs, Journal of Financial Markets 12, 173–202.

Foley, Sean, and Talis Putniņš, 2014, Regulatory efforts to reduce dark trading in Canada and Australia:

How have they worked? Report prepared for the CFA Institute.

Fama, Eugene, 1970, Efficient capital markets: A review of theory and empirical work, Journal of

Finance 25, 383–417.

Foucault, Thierry, Ohad Kadan, and Eugene Kandel, 2013, Liquidity cycles and make/take fees in

electronic markets, Journal of Finance 68, 299–341.

Hatheway, Frank, Amy Kwan and Hui Zheng, 2016, An empirical analysis of market segmentation on

U.S. equities markets, Journal of Financial and Quantitative Analysis, forthcoming.

Hatheway, Frank, 2015a, Nasdaq Access Fee Experiment: Report I, Nasdaq Report.

Hatheway, Frank, 2015b, Nasdaq Access Fee Experiment: Report II, Nasdaq Report.

Kaniel, Ron and Hong Liu, 2006, So what orders do informed traders use? Journal of Business 79,

1867–1913.

Kwan, Amy, Ronald Masulis, and Thomas H. McInish, 2015, Trading rules, competition for order flow

and market fragmentation, Journal of Financial Economics 115, 330–348.

Harris, Larry 2013, Maker-taker pricing effects on market quotations, Working Paper, University of

Southern California.

29

Lin, Yiping, Peter Swan, and Vito Mollica, 2017, Tick Size, Exchange Access Fee and Market Quality,

Working paper.

Lo, Andrew, W. and Craig MacKinlay, 1988, Stock market prices do not follow random walks:

Evidence from a simple specification test, Review of Financial Studies 1, 41–66.

Lutat, Marco, 2010, The effect of maker-taker pricing on market liquidity in electronic trading

systems—Empirical evidence from European equity trading, Working Paper, University of Frankfurt.

Maglaras, Costis, Ciamac C. Moallemi, and Hua Zheng, 2012, Optimal order routing in a fragmented

market, Working Paper, Columbia University.

Malinova, Katya, and Andreas Park, 2015, Subsidizing liquidity: The impact of make/take fees on

market quality, Journal of Finance 70, 509–536.

O’Hara, Maureen, and Mao Ye, 2011, Is market fragmentation harming market quality?, Journal of

Financial Economics 100, 459-474.

Panayides, Marios, Rindi, Barbara and Ingrid M. Werner, 2016, Trading Fees and Intermarket

Competition, Working Paper.

Rosu, Ioanid, 2012, Liquidity and information in order driven markets, Working Paper, HEC Paris.

Rosu, Ioanid, 2015, Fast and slow informed trading, Working Paper, HEC Paris.

SEC, 2010, Concept release on market structure, Release No. 34-61358, File No. S7-02-10, Discussion

paper.

SEC, 2014, Nasdaq Form 19b-4 filing on proposed access fee pilot, available at

http://nasdaq.cchwallstreet.com/NASDAQ/pdf/nasdaq-filings/2014/SR-NASDAQ-2014-128.pdf.

30

SEC, 2015a, Memo on maker-taker fees on equities exchange, available at

https://www.sec.gov/spotlight/emsac/memo-maker-taker-fees-on-equities-exchanges.pdf.

SEC, 2015b, Memo on Rule 611 of Regulation NMS, available at

https://www.sec.gov/spotlight/emsac/memo-rule-611-regulation-nms.pdf.

31

Table 1: Nasdaq Maker-Taker Fee Structure This table reports the Nasdaq pricing measured in cents per 100 shares (CPS) traded during (PilotOn) and pre/post (PilotOff) the Nasdaq access fee pilot implemented on February 2, 2015 and ended on May 31, 2015. The sample period is from December 1, 2014 to July 31, 2015. Net fee is defined as the sum of the taker fee and the maker rebate, which is the exchange revenue per 100 shares traded. The taker fee is the highest rate Nasdaq can charge and maker rebate is the most indicative rate Nasdaq provides in the Nasdaq pricing table.

Fee/ Rebate PilotOn (CPS) PilotOff (CPS) Difference

Taker Fee to Remove Liquidity: 5 30 -25 Maker Rebate to Add Liquidity:

Displayed Liquidity 4 29 -25 Non-Displayed Midpoint 2 25 -23

Other Non-Displayed Liquidity 0 10 -10 Net Fee:

Displayed Liquidity 1 1 0 Non-Displayed Midpoint 3 5 -2

Other Non-Displayed Liquidity 5 20 -15

Table 2: Indicative U.S. Exchange Fee Structure

32

This table reports the U.S. stock exchanges pricing, measured in cents per 100 shares (CPS) traded. Fee is the exchange charge (pay) in the maker-taker (taker-maker) market. Rebate is the exchange pay (charge) in the maker-taker (taker-maker) market. Net fee is defined as the sum of the taker fee and the maker rebate, which is the exchange revenue per 100 shares traded. For simplicity, the fee is the highest rate the exchange can charge and rebate is the highest rate below the fee given its pre-determined fee structure in their pricing table. Exchange Fee Model Fee (CPS) Rebate (CPS) Net Fee (CPS) NASDAQ Maker-Taker 30 -29 1 ARCA Maker-Taker 30 -29 1 BATS Z Maker-Taker 30 -29 1 NYSE Maker-Taker 27.5 -26 1.5 AMEX Maker-Taker 30 -25 5 PHLX Maker-Taker 29 -23 6 EDGX Maker-Taker 29 -20 9 CHX Maker-Taker 30 -20 10 EDGA Taker-Maker -2 5 3 BATS Y Taker-Maker -15 18 3 BX Taker-Maker -17 19 2

33

Table 3: Summary Statistics The table reports summary statistics for the selected variables for Nasdaq fee pilot stocks and its matching stocks. Nasdaq access fee pilot is implemented on February 2, 2015 and ended on May 31, 2015. The sample period is from December 1, 2014 to July 31, 2015. PilotOn is the period when Nasdaq implemented the fee pilot; and PilotOff refers to two months prior and post the fee pilot. Treatment Control PilotOn PilotOff PilotOn PilotOff Diff in Diffs Number of Daily Obs. 1148 1190 1148 1190 Mean Median Std Mean Median Std Mean Median Std Mean Median Std Diff t-stats Panel A: Trading Stats and Market Share Closing Price 24.21 22.78 17.28 23.78 18.79 17.93 31.08 33.99 18.66 30.11 33.01 18.70 -0.54 -0.44 Market Cap (millions) 47.63 20.70 73.32 46.78 18.78 74.40 43.56 18.44 63.50 42.84 18.46 62.93 0.13 0.03 Nasdaq Volume (millions) 2.27 1.57 2.29 2.62 1.97 2.11 1.71 1.33 1.36 1.86 1.57 1.56 -0.19 -1.77 Nasdaq MarketShare (%) 12.77 12.01 4.72 14.72 13.95 5.77 18.73 18.59 6.07 19.22 19.04 6.69 -1.46 -4.25 Panel B: Quote Quality and Fill Ratio Nasdaq Time at NBBO (%) 88.25 95.71 13.19 94.00 98.82 9.30 93.02 98.00 10.64 93.80 98.12 9.80 -4.98 -6.86 Nasdaq Depth at NBBO (millions) 1.69 0.38 3.51 2.33 0.72 5.26 0.41 0.26 0.47 0.41 0.26 0.46 -0.64 -3.67 Nasdaq Depth Share 15.68 15.57 5.88 19.31 18.50 7.29 21.64 19.27 6.58 21.25 19.66 7.58 -4.02 -10.15 Fill Rate (%) 3.91 3.59 1.46 3.65 3.50 1.48 2.99 2.91 1.27 2.96 2.83 1.14 0.24 3.02 Fill Time (seconds) 189 110 197 236 118 265 134 93 119 123 83 127 -58 -5.59 Panel C: Transaction Cost_cents Quoted Spread (cents) 1.35 1.01 0.83 1.59 1.02 1.28 1.63 1.01 1.86 2.15 1.03 3.23 0.28 2.33 Effective Spread (cents) 1.14 0.97 0.58 1.18 0.96 0.70 1.30 0.97 1.13 1.40 0.96 1.34 0.06 1.02 Realised Spread 1s (cents) -0.12 -0.07 0.48 -0.38 -0.42 0.35 -0.39 -0.43 0.51 -0.36 -0.44 0.68 0.29 9.97 Realised Spread 5s (cents) -0.30 -0.20 0.59 -0.62 -0.54 0.50 -0.56 -0.51 0.66 -0.51 -0.52 0.68 0.37 10.18 Price Impact 1s (cents) 1.26 1.06 0.74 1.56 1.42 0.70 1.69 1.45 1.09 1.77 1.46 1.13 -0.22 -3.95 Price Impact 5s (cents) 1.44 1.16 0.89 1.81 1.51 1.08 1.86 1.52 1.45 1.92 1.51 1.41 -0.31 -3.95 Panel D: HFT vs Non-HFT Trading Behaviour HFT Volume (millions) 1.69 1.07 1.71 1.96 1.49 1.59 1.26 1.08 0.98 1.40 1.23 1.11 -0.13 -1.59 Non-HFT Volume (millions) 2.86 2.04 2.96 3.29 2.44 2.74 2.15 1.70 1.81 2.33 1.89 2.11 -0.25 -1.78 HFT Adding Liquidity (%) 22.91 23.20 7.67 33.59 33.18 10.15 33.15 32.63 13.12 33.80 33.08 12.18 -10.04 -13.60 HFT Taking Liquidity (%) 50.68 51.50 9.88 41.05 41.61 8.80 41.18 39.91 9.83 41.48 40.09 10.09 9.94 17.20 Non-HFT Adding Liquidity (%) 77.09 76.80 7.67 66.41 66.82 10.15 66.85 67.37 13.12 66.20 66.92 12.18 10.04 13.60 Non-HFT Taking Liquidity (%) 49.32 48.50 9.88 58.95 58.39 8.80 58.82 60.09 9.83 58.52 59.91 10.09 -9.94 -17.20 Panel E: Liquidity Adding Types and HFT Displayed Liquidity (%) 88.99 90.10 5.37 89.01 90.56 5.65 91.48 92.32 4.05 91.18 92.16 4.45 -0.32 -1.17 Non-displayed Midpoint Liquidity (%) 7.78 6.23 5.66 8.12 6.51 5.98 5.77 5.31 2.88 5.92 5.33 3.29 -0.19 -0.73 Non-displayed Non-Midpoint Liquidity (%) 3.23 2.12 3.30 2.78 1.56 3.36 2.65 1.47 3.63 2.81 1.69 3.64 0.61 2.81 HFT Displayed Liquidity (%) 18.37 18.31 6.14 28.43 28.57 9.27 29.35 29.15 12.07 30.05 29.37 11.71 -9.36 -13.79 HFT Non-displayed Midpoint Liquidity (%) 3.87 2.27 4.19 4.51 3.23 4.31 3.21 2.71 2.70 3.10 2.49 2.73 -0.76 -3.51 HFT Non-displayed Non-Midpoint Liquidity (%) 0.67 0.16 1.39 0.56 0.04 1.63 0.49 0.06 1.36 0.56 0.05 1.56 0.17 1.92

34

Table 4: Quote and Execution Quality Regression The table tests the impact of trading fee change on the percentage of time and market depth when Nasdaq at national best bid or offer (NBBO), as well as the fill rate and speed. Time% NQ at NBBO is the average percentage time Nasdaq bid at NBB and Nasdaq ask at NBO. NQ Depth at NBBO is the average quote size when Nasdaq bid at NBB and Nasdaq ask at NBO. NQ Depth Share at NBBO is the average percentage of quote size when Nasdaq bid at NBB and Nasdaq ask at NBO. Fill rate is the ratio of volume of executed orders to the volume of resting orders. Fill time represents the average time (measured in seconds) that it takes executed to receive their first (and perhaps only) execution. All the variables are measured on a daily basis per security. Nasdaq access fee pilot is implemented on February 2, 2015 and ended on May 31, 2015. The sample period is from December 1, 2014 to July 31, 2015. Standard errors are in parentheses and are robust to both heteroscedasticity and correlation within stocks. * indicates significance at the 10% level, ** at the 5% level, and *** at the 1% level.

Dependent Variable Time% NQ at NBBO NQ Depth at NBBO

NQ Depth Share at NBBO Fill Rate Log(Fill Time)

Stock Fixed Effect No Yes No Yes No Yes No Yes No Yes Intercept 70.375*** 63.922*** 10.392*** 13.492*** 107.689*** 75.317*** 7.352*** 9.663*** 8.469*** 11.026*** (2.907) (3.987) (0.226) (0.267) (2.929) (3.689) (0.603) (1.056) (0.239) (0.360) Treat -3.064*** -2.870*** 0.194*** -0.281*** -1.034*** 1.944*** 0.843*** 0.415*** 0.203*** -0.180*** (0.261) (0.357) (0.020) (0.024) (0.263) (0.330) (0.054) (0.094) (0.022) (0.032) PilotOn -0.962*** -0.962*** -0.047** -0.047*** 0.262 0.262 -0.002 -0.002 0.038* 0.038** (0.265) (0.180) (0.021) (0.012) (0.267) (0.167) (0.055) (0.048) (0.022) (0.016) Treat*PilotOn -4.977*** -4.977*** -0.337*** -0.337*** -4.010*** -4.010*** 0.237*** 0.237*** -0.261*** -0.261*** (0.365) (0.248) (0.028) (0.017) (0.368) (0.229) (0.076) (0.066) (0.030) (0.022) VIX -0.115*** -0.115*** -0.032*** -0.032*** -0.077** -0.077*** -0.015** -0.015** -0.063*** -0.063*** (0.038) (0.026) (0.003) (0.002) (0.038) (0.024) (0.008) (0.007) (0.003) (0.002) Log(Price) -9.495*** -10.259*** -1.729*** -1.628*** 0.206* -0.399*** 0.373*** 0.273*** -0.822*** -0.712*** (0.108) (0.131) (0.008) (0.009) (0.109) (0.122) (0.022) (0.035) (0.009) (0.012) Log(Mkt Cap) 2.656*** 3.596*** 0.372*** 0.236*** -3.271*** -1.196*** -0.223*** -0.199*** -0.009 -0.137*** -0.11 -0.146 -0.009 -0.01 -0.11 -0.135 -0.023 -0.039 -0.009 -0.013 Volatility -249.743*** -661.217*** -31.073*** -27.563*** -311.181*** -701.937*** -2.274 -59.183*** -7.885*** 1.084 (13.732) (23.146) (1.068) (1.548) (13.836) (21.416) (2.849) (6.127) (1.130) (2.092) Adjusted R^2 0.682 0.853 0.911 0.970 0.251 0.708 0.152 0.362 0.693 0.829 Observations 4,676 4,676 4,676 4,676 4,676 4,676 4,676 4,676 4,676 4,676

Table 5a: Bid-Ask Spread and Price Impact Regression_Cents

35