Embed Size (px)

Citation preview

Making the Case for CRA Eligibility

MODERATOR PANELISTS

Renee Beaver Novogradac & Company LLP

Brad Calloway First NBC Bank

Sharon Canavan Office of the Comptroller of Currency

Kandi Jackson NTCIC

Tim Karp JP Morgan Chase

Historic Tax Credits

• Specific statutory banking authorities permit banks to provide

financing for a certified historic property rehabilitation project and gain

the related tax credits by taking interests in entities that hold such

properties for rehabilitation

• May be eligible for CRA consideration under certain circumstances

National Bank Legal Authority

• HTC investments permitted under national banking authorities:

– 12 U.S.C. § 24(Eleventh)

– 12 U.S.C. § 24(Seventh)

• A national bank can acquire an interest in an entity that holds HTC

properties for rehabilitation.

– Property owner/developer creates a limited partnership (LP) or limited

liability company (LLC)

– Bank typically holds substantial (e.g., 99%) interest

– Property owner/developer holds de minimis (e.g., 1%) interest

• Using this structure, national banks can provide the equity funding for

HTC projects in return for the associated tax credits

National Bank Legal Authority

• 12 U.S.C. § 24(Eleventh)— authorizes national banks to make loans

and investments designed primarily to promote the public welfare,

including the welfare of LMI communities or families (such as by

providing housing, service, or jobs).

– 12 CFR Part 24 (Part 24)

• Depending on safety and soundness profile, CRA performance, and

the nature of the project financing, the bank must either:

– Request prior OCC approval, or

– Submit an after-the-fact notice to the OCC

National Bank Legal Authority

• 12 U.S.C. § 24(Seventh)—Depending on the specifics of the

transaction, under § 24(Seventh), national banks may be authorized to

finance an HTC project by acquiring an interest in the entities that hold

the properties for rehabilitation.

• The substance of the transaction must remain the provision of

financing for the rehabilitation of historic property.

• National banks and federal thrifts should consult their supervisory

office contacts concerning investments that intend to use this

authority.

Federal Savings Associations (FSA)

Legal Authority

• FSA authorities to make community development investments:

– De Minimis Investments—12 CFR 160.36

– Community Development related equity investments in real estate—HOLA

5(c)(3)(A), 12 CFR 160.30, and May 10, 1995 letter

– Investments in Service Corporations and Lower-tier Entities for community

development investments—12 CFR 159

CRA Consideration For HTC

• HTC-related loan or investment must meet—

– Definition of community development

• Affordable housing for low- or moderate- income (LMI)

individuals

• Community services targeted to LMI individuals

• Economic development by financing small businesses or

small farms

• Revitalization or stabilization of underserved or distressed

nonmetropolitan middle-income areas, LMI areas, or

designated disaster areas

– Geographic restriction—must be located in:

• Bank’s Assessment Area or

• Broader Statewide or Regional Area

CRA Q&As

§ __.12(g) – 1

§ __.12(g)(2) – 1

§ __.12(g)(4) – 2

§ __.12(g)(4)(i) –

1, and

§ __.12(g)(4)(ii)

– 2 through – 4.

Greater weight on HTC-related activities that are most responsive to community

credit needs, including needs of LMI individuals or geographies

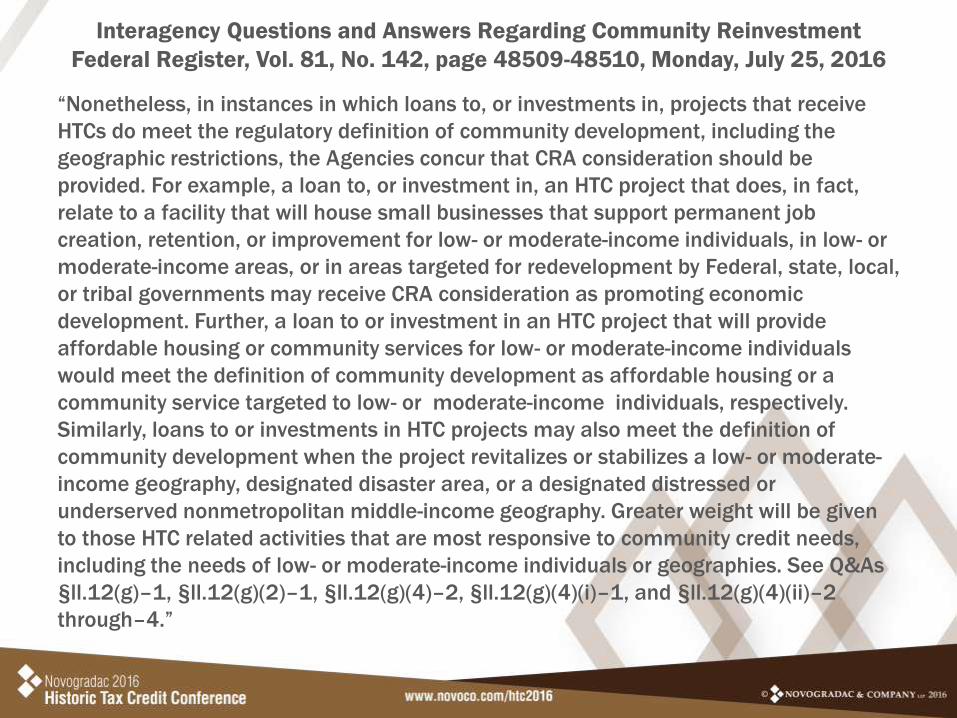

Interagency Questions and Answers Regarding Community Reinvestment

Federal Register, Vol. 81, No. 142, page 48509-48510, Monday, July 25, 2016

“Nonetheless, in instances in which loans to, or investments in, projects that receive

HTCs do meet the regulatory definition of community development, including the

geographic restrictions, the Agencies concur that CRA consideration should be

provided. For example, a loan to, or investment in, an HTC project that does, in fact,

relate to a facility that will house small businesses that support permanent job

creation, retention, or improvement for low- or moderate-income individuals, in low- or

moderate-income areas, or in areas targeted for redevelopment by Federal, state, local,

or tribal governments may receive CRA consideration as promoting economic

development. Further, a loan to or investment in an HTC project that will provide

affordable housing or community services for low- or moderate-income individuals

would meet the definition of community development as affordable housing or a

community service targeted to low- or moderate-income individuals, respectively.

Similarly, loans to or investments in HTC projects may also meet the definition of

community development when the project revitalizes or stabilizes a low- or moderate-

income geography, designated disaster area, or a designated distressed or

underserved nonmetropolitan middle-income geography. Greater weight will be given

to those HTC related activities that are most responsive to community credit needs,

including the needs of low- or moderate-income individuals or geographies. See Q&As

§ll.12(g)–1, §ll.12(g)(2)–1, §ll.12(g)(4)–2, §ll.12(g)(4)(i)–1, and §ll.12(g)(4)(ii)–2

through–4.”

CRA Consideration For HTC

HTC Investment in:

Affordable Housing for LMI individuals

Community Facility that targets services to

LMI individuals

Economic Development

• Economic development by financing small businesses or small farms

– Size test—Project must involve financing a business(es) with gross annual

revenues of $1 million or less, or meet the size eligibility requirements for

Small Business Administration Development Companies

– Purpose test—Must support permanent job creation, retention, and/or

improvement:

• For LMI individuals,

• In a low- or moderate-income census tract, or

• In an area targeted for redevelopment by federal, state, local, or tribal

government

Economic Development

Examples: Restoration of historic structure:

Occupied by small businesses with gross annual revenue of $1 million or less, which will provide 100 new permanent jobs for LMI individuals.

In LMI census tract and renovation will attract small businesses that meet size eligibility requirements for SBA Development Companies that will provide permanent jobs that improve employment opportunities.

In area targeted by federal, state, local, or tribal government and renovated structure will be occupied by existing small businesses with gross annual revenue of $1 million or less, and will retain permanent jobs.

HTC investment revitalizes or stabilizes area:

List of distressed or underserved nonmetropolitan middle-income areas

at www.ffiec.gov

Underserved nonmetropolitan middle-income areas

Activity must address essential community needs

• Distressed nonmetropolitan middle-income areas

• LMI areas, or

• Designated disaster areas

Activity must help retain existing or attract new businesses

or residents

HTC Investment Revitalizes or Stabilizes

Examples: Renovation of historic structure will:

• Provide community health center (meeting

essential community needs) in underserved

nonmetropolitan middle-income geography.

• Create mixed commercial/residential space

that will attract new residents and

businesses in distressed nonmetropolitan

middle-income geography.

• Provide commercial space in low- or

moderate- income area and will retain

existing businesses.

• Restore historic homes in a designated

disaster area, will retain residents, and is

related to disaster recovery.

Presumption

that activity

revitalizes or

stabilizes if in

government-

designated

area and

consistent with

plan

CD Activities—Broader Statewide or Regional Area

Q&A § __.12(h)–6

Always Considered

Direct benefit

to AAs Activities that do not

serve and will not

benefit the AA(s)

If the bank has been

responsive to needs

and opportunities in

its AA(s)

May Be Considered

Purpose, mandate

or function to serve

the AAs

OR

Broader Geographic Consideration

• CD activity with the purpose, mandate, or function to serve a bank’s AAs will be considered

• CD activities that do not serve and will not benefit the AA(s)—may be considered if the

bank has been responsive to needs and opportunities in its AA(s)

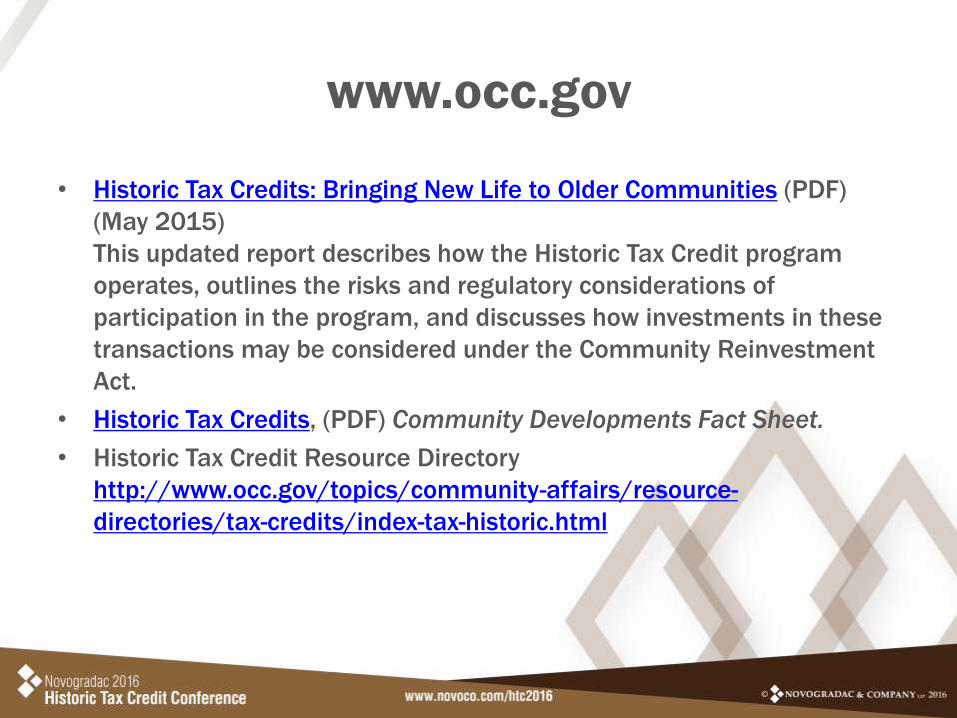

www.occ.gov

• Historic Tax Credits: Bringing New Life to Older Communities (PDF)

(May 2015)

This updated report describes how the Historic Tax Credit program

operates, outlines the risks and regulatory considerations of

participation in the program, and discusses how investments in these

transactions may be considered under the Community Reinvestment

Act.

• Historic Tax Credits, (PDF) Community Developments Fact Sheet.

• Historic Tax Credit Resource Directory

http://www.occ.gov/topics/community-affairs/resource-

directories/tax-credits/index-tax-historic.html

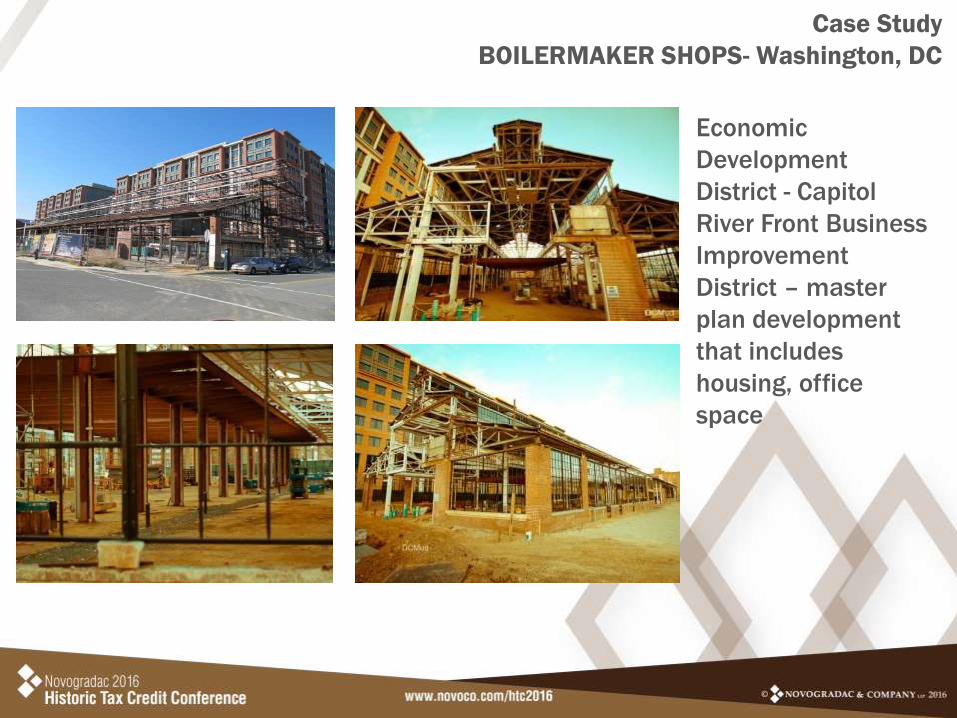

• Building history – former

46,000 sf navy ship boiler

manufacturing plant in

Washington Navy Yard

• Uses – restaurants, bars, retail

• Cost – $21.6 million

• Credits - $3.9 million

• LMI census tract data – 62.1%

AMI, unemployment 5.4x

national average

Case Study

BOILERMAKER SHOPS- Washington, DC

Economic

Development

District - Capitol

River Front Business

Improvement

District – master

plan development

that includes

housing, office

space

Case Study

BOILERMAKER SHOPS- Washington, DC

• Job creation - 217 total jobs, 92 FTEs 95% newly create jobs

– average wage $12/hour, 50% provide professional development

opportunities and 64% pay benefits.

– 90% of jobs taken by District of Columbia residents, 60% did not

require a college degree.

– Highly accessible via public transit (workers don’t need a car)

Case Study

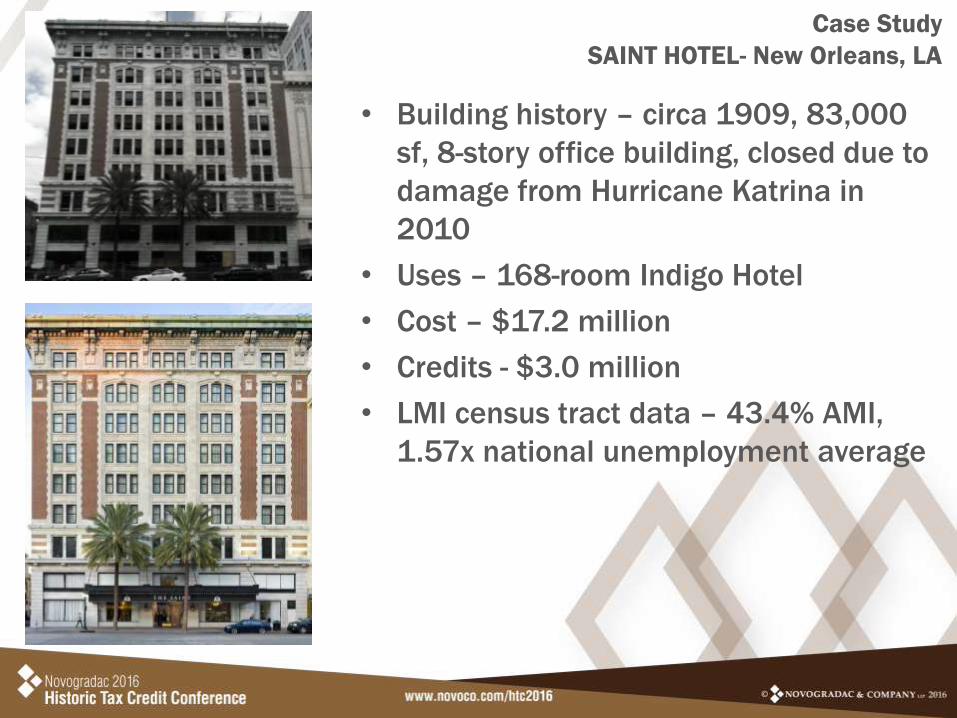

BOILERMAKER SHOPS- Washington, DC

• Building history – circa 1909, 83,000

sf, 8-story office building, closed due to

damage from Hurricane Katrina in

2010

• Uses – 168-room Indigo Hotel

• Cost – $17.2 million

• Credits - $3.0 million

• LMI census tract data – 43.4% AMI,

1.57x national unemployment average

Case Study

SAINT HOTEL- New Orleans, LA

• Economic Districts - SBA HUB Zone, State and City

Economic Distress Zone, federal disaster area,

Downtown Development District

• Job creation – 38 new full and part-time positions

(hotel management, front office, housekeeping,

maintenance, food service), 3rd-party vendor

employs 15 housekeepers

• Professional development opportunities – bar

manager started as a cocktail waitress, 2 former

desk clerks are now front office managers

Case Study

SAINT HOTEL- New Orleans, LA

Case Study

SAINT HOTEL- New Orleans, LA

• Full-time positions - pay $35,000-55,000, part-time $10-15/hr

– 90-239% of local livable wage

– no job requires a college degree

– owner hires for personality, work ethic and intelligence

– will hire people with misdemeanor record, no high school degree

– does extensive on-the-job-training

Coalitions Efforts

LIHTC & HTC EXAMPLES

NMTC & HTC EXAMPLES

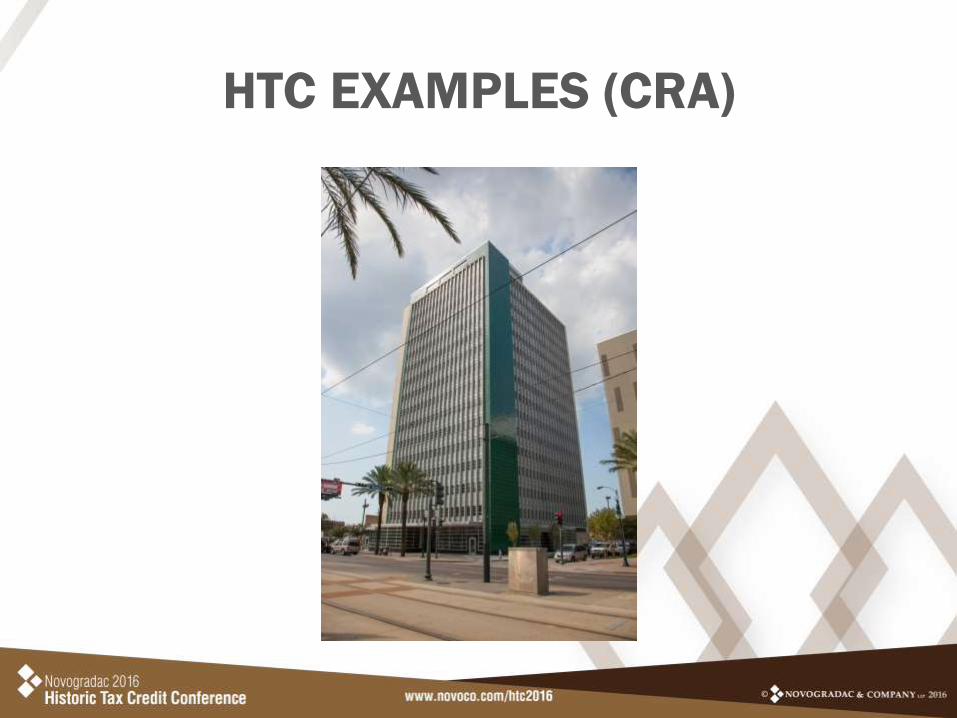

HTC EXAMPLES (CRA)

HTC EXAMPLES (CRA)

• Marais Apartments - 1501 Canal Street New Orleans, LA

• Developed by HRI Properties

• Formerly known as the Texaco Building

• Designed in 1951 by the architect Claude H. Hooton

• Building is an early example of the "International" style of architecture

found in Louisiana.

• Features a steel structure and an enamel-coated steel curtain wall

exterior which allowed for open, flexible interior space with minimal

interior columns. The renovation of 1501 Canal Street is an initial

phase in the redevelopment of the Iberville Housing Project, which is

the last remaining traditional public housing project in the City of New

Orleans.

HTC EXAMPLES (CRA)

HTC EXAMPLES (CRA)

• Capital Sources:

– 4% tax credit equity

– Permanent loan (Chase tax exempt bond)

– Federal Historic Tax Credits

– State Historic Tax Credits

– Choice Neighborhood Funds from City of New Orleans

– Deferred developer fee

HTC EXAMPLES (CRA)

• CRA Qualification/Community Impacts:

– Financed the adaptive reuse of the historic former Texaco office

– 17-story, dilapidated and leaky building in deplorable condition, renovated

into a 112-unit, 4% LIHTC, senior apartment project in downtown New

Orleans.

– All units are subject to a Section 8 Project Based HAP contract for 15

years, and will primarily accommodate low-income senior citizens,

especially those who might be moved by the retooling of the nearby

Iberville Housing Development.

– Six (5%) units will be at 20% AMI and will be Permanent Supportive

Housing (PSH) units

– The remaining 106 (95%) units are at 60% AMI.

– The project has 12 (10%) efficiency units (632 sf) and 100 (90%)

1BED/1BATH units (650 sf).

HTC EXAMPLES (CRA)

• CRA Qualification/Community Impacts continued:

– The project will also have approximately 1,980 sf of commercial space on

the first floor to be used for small retailer or café to complement the

ongoing revitalization of Canal Street.

– The Louisiana Housing Corporation was established in 1980 pursuant to

the Louisiana Housing Finance Act contained in Chapter 3-A of Title 40 of

the Louisiana Revised Statutes of 1950, as amended. The enacting

legislation grants the Agency the authority to undertake various programs

to assist in the financing of housing needs in the state of Louisiana for

persons of low and moderate incomes.

HTC EXAMPLES (CRA)

HTC EXAMPLES (CRA)

HTC EXAMPLES (CRA)

HTC EXAMPLES (NON-CRA)

• Discuss why it couldn’t qualify to stress why changes are needed?

www.occ.gov

• Historic Tax Credits: Bringing New Life to Older Communities (PDF)

(May 2015)

This updated report describes how the Historic Tax Credit program

operates, outlines the risks and regulatory considerations of

participation in the program, and discusses how investments in these

transactions may be considered under the Community Reinvestment

Act.

• Historic Tax Credits, (PDF) Community Developments Fact Sheet.

• Historic Tax Credit Resource Directory

http://www.occ.gov/topics/community-affairs/resource-

directories/tax-credits/index-tax-historic.html

Making the Case for CRA Eligibility

MODERATOR PANELISTS

Renee Beaver Novogradac & Company LLP

Brad Calloway First NBC Bank

Sharon Canavan Office of the Comptroller of Currency

Kandi Jackson NTCIC

Tim Karp JP Morgan Chase