Embed Size (px)

DESCRIPTION

£ www.stockporthomes.org Section 2 Universal Credit Page 8 Section 7 Basic bank accounts Page 34 Section 4 Managing money problems Page 20 Introduction Page 3 Contents Section 1 The cost of running your home Page 4 Section 5 Saving money on your energy bills Page 27 Stockport Homes - A guide to making the most of your money 2

Citation preview

A guide tomaking the mostof your money

£www.stockporthomes.org

2 Stockport Homes - A guide to making the most of your money

Contents

Introduction Page 3 Section 1The cost of running your home Page 4 Section 2Universal Credit Page 8 Section 3Borrowing money Page 15

Section 4Managing money problems Page 20

Section 5Saving money on your energy bills Page 27

Section 6Rent Page 31 Section 7Basic bank accounts Page 34

Section 8Home insurance Page 36

Section 9Useful contacts Page 38

3Stockport Homes - A guide to making the most of your money

Introduction

If the answer is yes to any of these questions, this booklet can help you!

The purpose of this booklet is:• to give you some basic information and advice to help you deal with your money; and• to provide details of agencies in Stockport who can help you with your finances.

Even if you do feel you can manage your money, this booklet has useful tips on how to save money and spend wisely.

If you have money worries it is important to deal with them as soon as possible. They will not go away and the longer you leave them the worse the situation will become. There is always someone who can help you.

4 Stockport Homes - A guide to making the most of your money

The cost of running your home

Section 1

Moving into your own home can be anexciting time – but also an expensive one.

If you have managed household bills before, you will know about the costs involved in running a home. However, if you are managing a household budget for the first time, you will need to think carefully about how much money you will need to set up your home and pay your regular bills. There are many ways of reducing the amount you pay.

How much money do you have coming in (income)?

Firstly, you need to know how much money you have coming in. This could include:

• Wages (including student loans);• Benefits and Tax Credits; and• Pension(s).

Now have a look at how much you need to spend each week or each month and check that you have enough money coming in to pay for your rent, bills (energy and water), food, travel, debt and savings. See pages 5-6 for more information.

5Stockport Homes - A guide to making the most of your money

The cost of running your home

What should I budget for?

There are several things you need to budget for, including:

Rent - Pay your rent in advance weekly or monthly, this will avoid getting into debt (or rent arrears). If you are a Stockport Homes customer your rent now includes water charges

which will not be covered by Housing Benefit. Go to page 31 for more information about paying your rent.

Energy - You need to pay for heat and light in your home. Go to page 27 for more information about saving money on your energy bills.

Food - On average you should allow £30 a week per person for food and other small household items (for example, cleaning products).

Debts and savings - If you have borrowed money, you need to pay it back regularly. It’s also important to plan and save for events like birthdays, Christmas and emergencies. By

putting small amounts aside regularly you will be able to cope with these events without getting into debt. Why not open a savings account with Stockport Credit Union? (please see pages 18-19 for more information)

6 Stockport Homes - A guide to making the most of your money

The cost of running your home

Section 1

Travel - If you have a car, you need to pay for insurance, tax, fuel and maintenance. If you use public transport and are 60 or over you will be entitled to free off-peak travel on

local buses anywhere in England. You may also get free bus travel if you are ‘eligible as disabled’. Please phone Greater Manchester Public Transport on 0161 244 1050 for details.

Council Tax - This pays for local Council services like policing and rubbish collection. If you receive housing benefit you could get Council Tax Benefit. Also, if you live alone, are

on a low wage or disabled, you may qualify for a reduction in your Council Tax bill. Please call 0161 217 6015 for more information.

What else should I budget for?

School meals - If your children have school meals, you will need to budget £10 a week for each child. Your child may receive free meals if you get income support, jobseekers allowance

or a high rate of child tax credit. Please call 0161 217 6015 for more information on free school meals and clothing grants.

Clothes - For families you should allow £30-£50 a month for each child, especially young children. As a guide, allow £20-£25 a month for each adult.

7Stockport Homes - A guide to making the most of your money

The cost of running your home

Where can I get help on budgeting?

Stockport Homes runs a ‘Making the Most of Your Money’ Skills for Life training (for all customers). Please contact the Customer Involvement Team on 0161 474 2862 for more information.

The Citizens Advice Bureau can give you advice on budgeting and debt, as well as many other subjects. There are three offices in Stockport: Central Stockport, Marple and Cheadle. For more information, please visit the Citizens Advice Bureau website www.citizensadvicebureau.org.uk or call 0844 826 9800 for advice and local opening times.

8 Stockport Homes - A guide to making the most of your money

Universal Credit

Section 2

Many people do not claim the benefits they are entitled to.

Even a small amount of extra money can make a big difference, so it pays to spend a little time finding out about what you can claim.

Where do I start?

You may be entitled to benefits if you or someone in your household is:

• over pension age;• unemployed;• off work due to illness or incapacity;• pregnant;• a parent or new parent;• sick or disabled;• working but on a low wage;• widowed;• recently bereaved;• caring for someone who is sick or disabled; or• a student.

9Stockport Homes - A guide to making the most of your money

Universal Credit

Housing Benefit and Council Tax Benefit

You may be able to get help with your rent (Housing Benefit) and Council Tax (Council Tax Benefit) even if you are working for an employer or are self-employed.

Stockport Council has a benefits calculator to help you find out if you are entitled to Housing Benefit and / or Council Tax Benefit. Visit http://interactive.stockport.gov.uk/hbcalculator/ to try it out or call Stockport Council Housing Benefit and Council Tax Team on 0161 217 6015 or email [email protected]

If you are eligible for Housing Benefit and / or Council Tax Benefit, you could also be able to get free school meals for your child / children and a clothing grant towards uniform for secondary pupils. You will need to fill in an application for free school meals and a clothing grant form. Call the Free School Meals and Clothing Grants Team on 0161 217 6015 or email [email protected]

Understanding benefits

There are different types of benefit for different circumstances. Some can only be claimed if you have paid enough National Insurance, while others are paid depending on your circumstances or the amount of money you already have. If your income is

10 Stockport Homes - A guide to making the most of your money

Universal Credit

Section 2

below a certain level you may be able to claim Income Support, Housing Benefit and Council Tax Benefit. You become liable to pay your rent from the date your tenancy agreement begins. If you have made a claim for Housing Benefit the earliest date your claim can start is the Monday after you move into the property. So, if you delay moving in, you could find yourself in rent arrears as your Housing Benefit will not begin until you move in.

If you lose your job it is important to start claiming benefits straight away to ensure your rent and Council Tax is covered. There are some exceptions to this rule – for more information see ‘Advice and support’ on page 11.

Some benefits can be claimed no matter how much money you have, for example, Child Benefit and Disability Living Allowance.

Tax and pension credits can be claimed depending on your income and situation. For example, if you work and have children you may be able to claim Working Tax Credit and Child Tax Credit. Older people may be able to claim Pension Credit depending on their income and savings.

11Stockport Homes - A guide to making the most of your money

Universal Credit

Advice and support

There are several agencies that can provide you with advice and support with your benefits, including:

Council Advice and Information Officers

The Council Advice and Information Officers can give you advice on benefits and tax credits as well as Council services, consumer problems, money matters, health issues, and housing problems. You can see them by calling in to one of the Stockport Direct Local Centres. There are Local Centres all over Stockport.

For their locations and opening hours, please go Stockport Council’s Stockport Direct page www.stockport.gov.uk/stockportdirect or call 0161 217 6009.

AdswoodNearest Advice Service is in Bridgehall (see page 12 for details).

Bramhall Advice ServiceBramhall Library, 70 Bramhall Lane South SK7 2DU

Bredbury Advice ServiceBredbury Library, George Lane SK6 1DJ

12 Stockport Homes - A guide to making the most of your money

Universal Credit

Section 2

Bridgehall Advice ServiceBridgehall Community Centre, Siddington Avenue SK3 8NR

Brinnington Advice ServiceFirst House, 367 Brinnington Road SK5 8EN

Cheadle Advice ServiceCheadle Library, Ashfield Road, Cheadle, Stockport SK8 1BB

Cheadle Hulme Advice Service6 Station Road, Cheadle Hulme SK8 5AE

Hazel Grove Advice ServiceHazel Grove Library, Beech Avenue, Hazel Grove SK7 4QP

Heald Green Advice ServiceHeald Green Library, Finney Lane, Heald Green SK8 3JB

Marple Advice ServiceMarple Library, Memorial Park, Marple SK6 6BA

Offerton Advice ServiceDialstone Library, Lisburne Lane, Offerton SK2 7LL

Reddish Advice ServiceStockport Direct, Houldsworth Centre, 2 Gorton Rd, Reddish SK5 7AF

Home visits can be arranged for people who are housebound.

13Stockport Homes - A guide to making the most of your money

Universal Credit Universal Credit

Welfare Rights Service

The Welfare Rights Service advises people on problems with social security benefits and tax credits, including representation at appeal tribunals. Welfare Rights Officers can be seen by appointment at:

• Regal House (4th Floor), Duke Street;• Stepping Hill Hospital; and • Local Centres in Reddish and Brinnington.

Home visits can be arranged for people who are housebound. Please see call Stockport Council Welfare Rights (to make an appointment or home visits) on 0161 474 3093.

Stockport Council Debtline 0161 474 3116 (Tuesday and Thursday afternoons only).

Stockport Council Benefits Advice Line 0161 474 6091 (Monday – Friday mornings only).

The Citizens Advice Bureau (CAB)

The Citizens Advice Bureau can give you advice on benefits and tax credits as well as many other subjects. There are three offices in Stockport: Central Stockport, Marple and Cheadle. For more information, please visit Stockport Citizens Advice Bureau’s website. Alternatively, you can call them on 0844 826 9800 for advice (the phone line is open 2pm Monday – Friday) and local opening times.

14 Stockport Homes - A guide to making the most of your money

Universal Credit

Section 2

Signpost Stockport for carers

A Carer is defined as ‘somebody who looks after a relative, partner or friend who is ill, disabled or confused’. Signpost Stockport for Carers is an independent charity which provides free, confidential information to all unpaid carers Stockport. You can visit the Signpost Stockport for Carers website for more information on local and national services www.signpostforcarers.org.uk

They can also be contacted at: Signpost for Carers, Torkington CentreTorkington Road,Hazel GroveStockport SK7 4PY

Tel: 0161 456 4276 Email: [email protected]: www.signpostforcarers.org.uk

15Stockport Homes - A guide to making the most of your money

Borrowing moneyUniversal Credit

Section 3

There are lots of ways to borrow money.

Some of these will cost you a lot more than others. It is very important to only borrow what you can afford to pay back. We all need to access some extra cash from time to time, but for some, access to affordable credit can be very difficult and many people turn to doorstop lenders for help.

Doorstep lenders (sometimes known as ‘home credit’)

Money lent to you by ‘doorstep lenders’ (such as salespeople who come and knock on your door) can be expensive. If you do consider taking out a loan from a doorstep lender you should:

• ask to see their lender’s licence or other authorisation. If they don’t have one, they are operating illegally, so don’t use them;

• be clear about the amount you are borrowing, how much you must repay and for how long you will be making repayments;

• ask how much in total the loan is going to cost you; and

• make sure you understand what will happen if you can’t keep up the repayments.

16 Stockport Homes - A guide to making the most of your money

Borrowing money

Section 3

If you borrow £100 over one year from a doorstop lender you may have to pay back £171.

The repayment on the same loan from a Credit Union would be just £107, that’s a saving of £64!

There are also other companies which will lend you money, but charge you a lot for doing so, or let you pay for things like a new television or fridge by weekly instalments. These are high cost credit providers. Sometimes you may not know how much you are paying back, often it is a lot more than you think.

Loan sharks

Loan sharks are unlicensed lenders. They operate illegally and will lend you money when nobody else will, but:

• their rates will be very high and you may find it difficult to keep up the repayments;

• you may be forced to get a second loan to pay off the first, causing your debts to get out of control; and

• they may use violence or intimidation to collect debts.

For confidential help and advice, please contact the Illegal Money Lending Team on 0300 555 2222.

17Stockport Homes - A guide to making the most of your money

Borrowing money

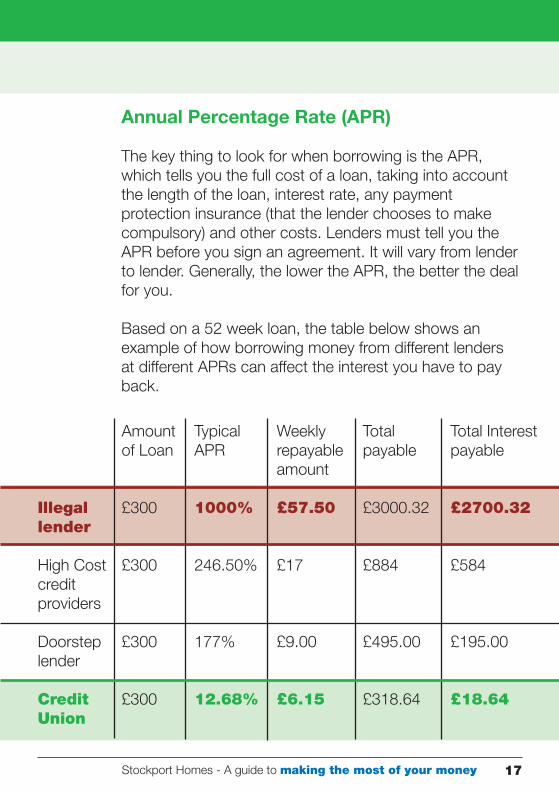

Annual Percentage Rate (APR)

The key thing to look for when borrowing is the APR, which tells you the full cost of a loan, taking into account the length of the loan, interest rate, any payment protection insurance (that the lender chooses to make compulsory) and other costs. Lenders must tell you the APR before you sign an agreement. It will vary from lender to lender. Generally, the lower the APR, the better the deal for you.

Based on a 52 week loan, the table below shows an example of how borrowing money from different lenders at different APRs can affect the interest you have to pay back.

Illegal lender

High Cost credit providers

Doorstep lender

Credit Union

Amount of Loan

£300

£300

£300

£300

Typical APR

1000%

246.50%

177%

12.68%

Weekly repayable amount

£57.50

£17

£9.00

£6.15

Totalpayable

£3000.32

£884

£495.00

£318.64

Total Interest payable

£2700.32

£584

£195.00

£18.64

18 Stockport Homes - A guide to making the most of your money

Borrowing money

Section 3

Credit Unions

Credit Unions are owned and managed by their members. They offer savings and affordable loans, especially when compared to doorstep lenders. Your money has the same protection as money in the bank.

Stockport Credit Union

Web: http://home.btconnect.com/stockportcu/Tel: 0161 430 5808Email: [email protected]

Stockport Credit Union was formed in December 2005 and offers a savings account to adults living or working in Stockport and their children can join too. Regular adult savers can also access low cost loans with a monthly interest rate of just 1%, this works out at 12.68% APR.

If you borrow £1,000 it will cost you less than £60 in interest to repay the loan within a year based on regular weekly or monthly payments). There are no arrangement fees and no penalty fee if you decide to repay your loan early.

19Stockport Homes - A guide to making the most of your money

Borrowing money

How do I join?

1. Complete an application form2. Go to a collection point3. Take with you your form, £1.20 joining fee and at least

£1 to open the account

Child members (aged 0 – 16 years old) do not have to pay a joining fee and can open their account with at least 10p. However, a child member needs to open their account with an adult member.

How do I pay money in?

There are collection points all over Stockport, visit http://home.btconnect.com/stockportcu/collecpoints.html or call Stockport Credit Union on 0161 430 5808 for more information.

You can also set up a standing order to pay money directly from your bank to your Stockport Credit Union account or even pay directly from your wage.

Useful contact details - Debt advice

Citizens Advice BureauTel: 0844 8269800Web: www.citizensadvice.org.uk

Consumer Credit Counselling ServiceTel: 0800 138 1111Web: www.cccs.co.uk

20 Stockport Homes - A guide to making the most of your money

Managing money problems

Section 4

Most people will borrow money at some time in their lives.

This debt only becomes a problem when you cannot pay it back.

People get into debt for all sorts of reasons, for example, losing a job, taking on a caring role, becoming pregnant, separating from a partner or becoming ill or disabled.

If you have borrowed more money than you can repay, or you have built up rent or fuel bills that you cannot afford to pay back, then you must take steps to sort things out.

It can be tempting to bury your head in the sand, but the longer you leave it, the worse it will get. Help and support is available and you will be able to take control of your finances again and look positively towards the future.

Which debts should I pay back first?

It is important to understand the difference between ‘priority’ and ‘non-priority’ debts. Your biggest debt will not necessarily be the most important one to pay back first.

21Stockport Homes - A guide to making the most of your money

Managing money problems

I can’t afford to pay my rent, what should I do?

If you are having problems paying your rent, you must contact Stockport Homes’ Customer Finance Team straight away for help and advice on 0161 474 2677 or0161 474 2668. If you stop paying your rent you could lose your home. Keeping a roof over your head is far more important than paying off loans.

Debt prioritisation

Which debts should I prioritise?

The following tables show the debts which are most important and which you should deal with first. It also states what may happen if you do not deal with them.

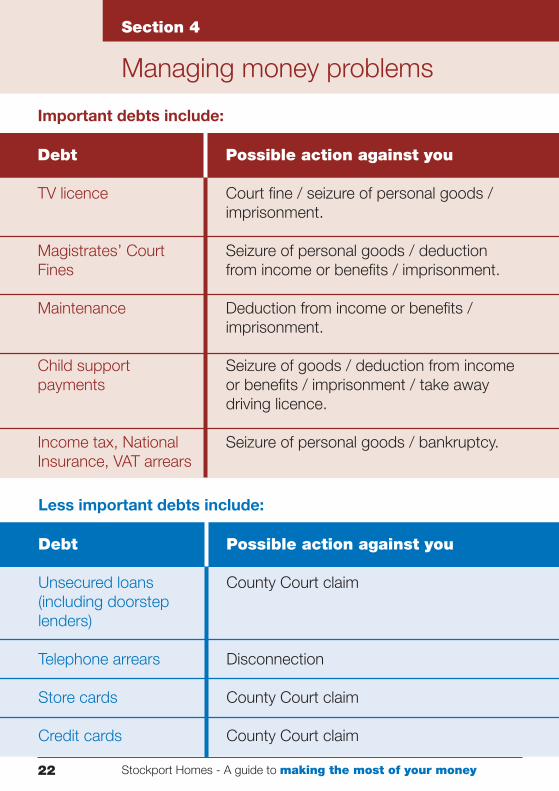

Important debts include:

Debt

Rent / water charges

Gas / Electricity

Council Tax

Possible action against you

Support to ensure payment / notice of possible Court action / Court action / Eviction from your home.

Supply cut off / pre-payment meter fitted.

Seizure of personal goods / deduction from income or benefits / imprisonment.

22 Stockport Homes - A guide to making the most of your money

Managing money problems

Section 4

Important debts include:

Debt

TV licence

Magistrates’ CourtFines

Maintenance

Child supportpayments

Income tax, National Insurance, VAT arrears

Possible action against you

Court fine / seizure of personal goods / imprisonment.

Seizure of personal goods / deduction from income or benefits / imprisonment.

Deduction from income or benefits / imprisonment.

Seizure of goods / deduction from income or benefits / imprisonment / take away driving licence.

Seizure of personal goods / bankruptcy.

Less important debts include:

Debt

Unsecured loans (including doorsteplenders)

Telephone arrears

Store cards

Credit cards

Possible action against you

County Court claim

Disconnection

County Court claim

County Court claim

23Stockport Homes - A guide to making the most of your money

Managing money problems

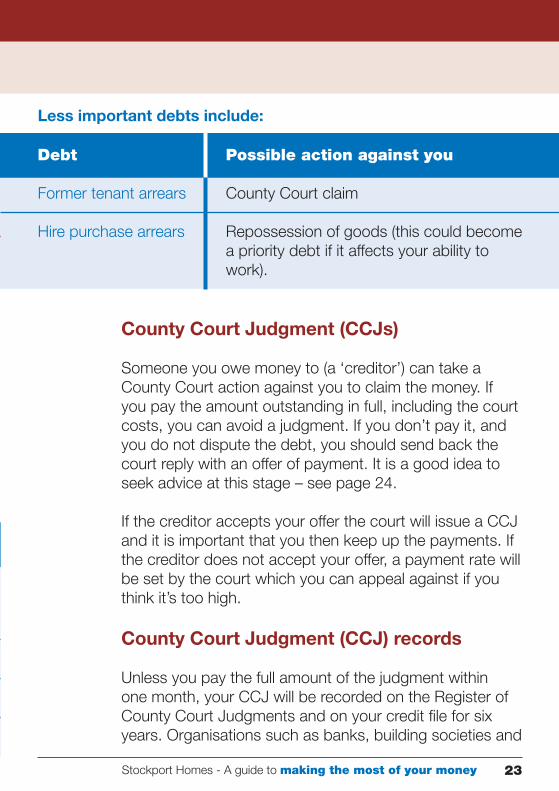

County Court Judgment (CCJs)

Someone you owe money to (a ‘creditor’) can take a County Court action against you to claim the money. If you pay the amount outstanding in full, including the court costs, you can avoid a judgment. If you don’t pay it, and you do not dispute the debt, you should send back the court reply with an offer of payment. It is a good idea to seek advice at this stage – see page 24.

If the creditor accepts your offer the court will issue a CCJ and it is important that you then keep up the payments. If the creditor does not accept your offer, a payment rate will be set by the court which you can appeal against if you think it’s too high.

County Court Judgment (CCJ) records

Unless you pay the full amount of the judgment within one month, your CCJ will be recorded on the Register of County Court Judgments and on your credit file for sixyears. Organisations such as banks, building societies and

Less important debts include:

Debt

Former tenant arrears

Hire purchase arrears

Possible action against you

County Court claim

Repossession of goods (this could become a priority debt if it affects your ability to work).

24 Stockport Homes - A guide to making the most of your money

Managing money problems

Section 4

loan companies use your credit file to help decide whether to give you credit or loans, like a mortgage.

Who can help me?

Stockport Debt Advice Service offers free independent advice, support and assistance with debt problems to Stockport residents. It is run by experienced debt advisers employed by Stockport Council with some funding from the Legal Services Commission.

Their team of specialist debt advisors can offer expert information, advice, negotiation, advocacy and professional representation on debt problems as well as giving advice on welfare benefits.

They can advise on:

• budgeting and maximising income;• basic bank accounts;• credit debts;• rent and Council Tax arrears;• fuel and water bills;• bankruptcy;• repossessions – including representation at Court;• Charging Orders – including representation at Court;• Administration Orders – including representation at

court;

25Stockport Homes - A guide to making the most of your money

Managing money problems

• bailiff’s action; and• individual voluntary arrangements.

To contact the Debt Advice Service, please phone 0161 474 3093 (weekdays 9.00am to 5.00pm, 4.30pm on Fridays). You will be asked for some brief details and may be referred for an appointment. You can also email [email protected]

The service is based at 4th Floor, Regal House, Duke Street, Stockport SK1 3DA.

The Council’s Debt Advice Service works closely with other local debt advice organisations offering specialist debt advice for Stockport residents.

It is important that you get advice about debts quickly, and so we strongly recommend that you seek help from the Debt Advice Service or one of the organisations listed below.

26 Stockport Homes - A guide to making the most of your money

Managing money problems

Section 4

National Debtline

Phone 0808 808 4000 (free from a landline) weekdays between 9.00am and 9.00pm and on Saturdays from 9.30am to 1.00pm. This free, independent charity can advise you about all personal debts. You can get more information online at www.nationaldebtline.co.uk

Other organisations who may be able to help you include:

• Stockport Citizens Advice Bureau: telephone 0844 826 9800 or go to www.stockportcab.org.uk

for the opening hours and addresses.• Stockport Direct Local Centres: ring 0161 217 6009,

email [email protected] or go to www.stockport.gov.uk/stockportdirect for the

opening hours and addresses.• Housing Options: if you are

homeless or need advice and help about housing

issues telephone 0161 474 4237 or go to www.stockporthomes.org

under ‘Our Sevices / Housing Options’.

27Stockport Homes - A guide to making the most of your money

Managing money problems Saving money on your energy bills

Section 5

Gas and Electricity There are two main ways in which you could reduce you energy bills:

1. Comparing gas and electricity to find the best deal

2. Making your home more energy efficient

Water

You could also save money by getting a water meter installed into your home or by changing your water tariff charges. Stockport Homes customers saved £12,000 during 2009 – 2010 on their Water bills. Call the Water Metering Project Officer on 0161 218 1669 for more information or to book a home visit.

Compare gas and electricity

Comparing gas and electricity prices on a regular basis is one way of paying as little as possible for gas and electricity. You could save up to £300 per year by comparing and switching suppliers.

You can compare and switch energy suppliers by visiting www.stockporthomesenergy.org.uk or calling0800 410 1245 (Free phone, Monday –Thursday 9.00am – 6.00pm, Friday 9.00am – 4.00pm, and Saturday 9.00am – 1.00pm)

28 Stockport Homes - A guide to making the most of your money

Saving money on your energy bills

Section 5

Remember the golden rules of using comparison services

1. Compare your actual usage over a long period of time, such as a year, to give a more accurate comparison result.

2. Opt for dual fuel – get your gas and electricity from the same supplier.

3. Pay by direct debit – most suppliers offers discounts to those using this method of payment.

This way you can be sure that you are getting the best deal. Please see the Stockport Homes leaflet ‘Save money on your gas and electricity bills with Stockport Homes Energy?’ for a step-by-step guide of how to switch and save using www.stockporthomesenergy.org.uk

Social Tariffs

All energy suppliers have to offer their most vulnerable customers cheaper tariffs. These are called social tariffs and offer cheaper energy deals and extra free services to certain customers. You may qualify for a social tariff if you are over 60, on means tested benefits or on a low income.

For more information on the eligibility criteria and how you could switch to this type of tariff visit http://www.consumerfocus.org.uk/energy-help-and-advice/households/energy-tariffs-explained/social-tariffs.

29Stockport Homes - A guide to making the most of your money

Saving money on your energy bills

Remember social tariffs may not be covered by searches on a comparison services website.

According to the Energy Saving Trust, the average household could save around £250 through energy efficiency measures.

Below are some energy saving tips that can help reduce your consumption and save money:

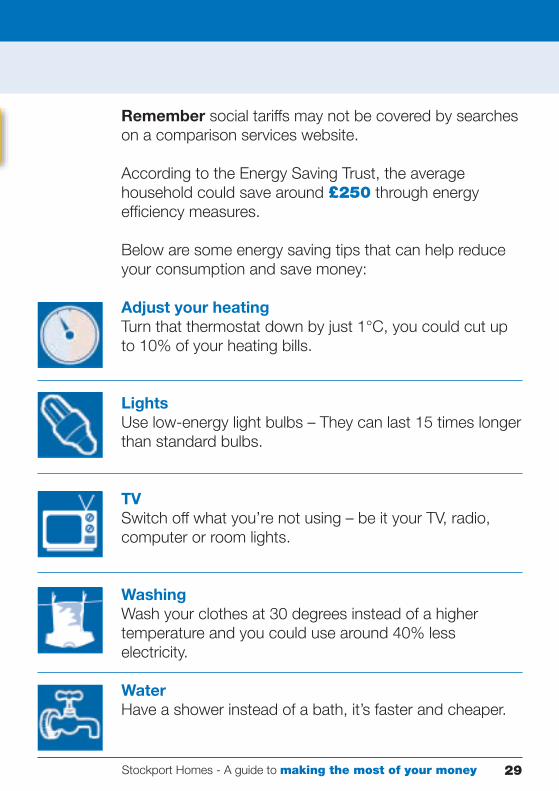

Adjust your heating Turn that thermostat down by just 1°C, you could cut up to 10% of your heating bills.

Lights Use low-energy light bulbs – They can last 15 times longer than standard bulbs.

TVSwitch off what you’re not using – be it your TV, radio, computer or room lights.

WashingWash your clothes at 30 degrees instead of a higher temperature and you could use around 40% less electricity.

Water Have a shower instead of a bath, it’s faster and cheaper.

30 Stockport Homes - A guide to making the most of your money

Saving money on your energy bills

Section 5

The following websites can also give you ideas on how to make your home more energy efficient:

http://www.consumerfocus.org.uk/energy-help-andadvice/households/reducing-bills

http://www.energysavingtrust.org.uk/

www.stockport.gov.uk/killthechill

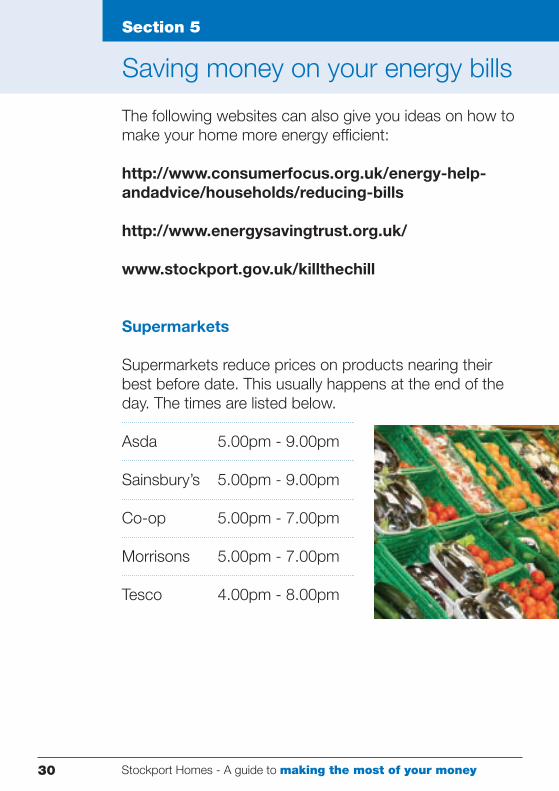

Supermarkets

Supermarkets reduce prices on products nearing their best before date. This usually happens at the end of the day. The times are listed below.

Asda 5.00pm - 9.00pm

Sainsbury’s 5.00pm - 9.00pm

Co-op 5.00pm - 7.00pm

Morrisons 5.00pm - 7.00pm

Tesco 4.00pm - 8.00pm

31Stockport Homes - A guide to making the most of your money

RentSaving money on your energy bills

Section 6

Paying your rent is a top priority

When you sign your tenancy agreement for your home, you make a legally binding agreement with us to pay your rent. Your rent now includes water charges which will not be covered by Housing Benefit. Your rent money is used to:• carry out repairs to your

home;• carry out improvements to• your home;• keep the estate tidy; and• other estate management services.

You can choose to pay your rent in various ways. Every rent week starts on a Monday. You can pay your rent weekly, fortnightly or monthly, but it should be paid in advance.

So, for example, if you pay monthly you should pay February’s rent at the end of January.

Anyone can fall behind with their payments at some time, only a small change in your circumstances can make a difference. If this happens, you must talk to us so that we can sort out the problem together. The problems will not go away, and the longer you leave them, the worse they will become. We will take action if you don’t pay your rent or you don’t try to work with us to solve your money problems.

32 Stockport Homes - A guide to making the most of your money

Rent

Section 6

If you owe a significant number of weeks rent, we will generally take court action against you. At this stage you are in serious danger of losing your home.

After we have served you with a notice, you will receive a summons to appear in Court for possession of your home and it is likely that you will have to pay all legal expenses we incur in taking you to Court.

Even at this stage you still have time to make reasonable arrangements with us to pay your arrears. If you do, we will ask for the possession order to be postponed. The Court will then make an order for you to pay an agreed amount on top of your weekly rent. As long as you maintain your Court order arrangement and your arrears do not increase, we will not enforce the possession order to repossess your home.

You can make payments to us as follows:

By Direct DebitYou can pay your rent and water charges by Direct Debit weekly or monthly (on 1st, 8th, 15th or 22nd) and receive an annual discount for doing so. Simply ring the Customer Finance Team on 0161 474 2668 (West) or0161 474 2677 (East) and ask for a Direct Debit Mandate.

By telephoneYou can pay using a debit or credit card by telephoning 0161 474 2677 (East) or 0161 474 2668 (West) during office hours or 0161 474 4050 during evenings and weekends. This service is available 24 hours a day.

33Stockport Homes - A guide to making the most of your money

Rent

On the internetYou can pay with a debit card or credit card at: www.stockport.gov.uk/payments

At a Post Office or Paypoint / Payzone outletYou can pay at any Post Office or any retail outlet displaying the Paypoint / Payzone logo using a swipe card. Post Offices are open on Saturday mornings and many Paypoint / Payzone outlets are open seven days a week and late nights.

To request a free payment swipe card, please telephone our Customer Finance Team on 0161 474 2677 (East) or 0161 474 2668 (West).

34 Stockport Homes - A guide to making the most of your money

Basic Bank Accounts

Section 7

Why do I need a bank account?

There are lots of good reasons to have a bank account, including:• you can have benefits paid

straight into your bank account;

• you can pay bills, for example, your rent, by direct debit;

• helping to give you a good credit record and you may be able to benefit from other banking services; and

• cashing cheques can be difficult and cost you money if you don’t have a bank account to pay your cheque into.

What is a basic bank account?

The government says that banks have to make basic bank accounts available to everyone, even people with a poor credit record.

How do I open a basic bank account?

You will need to:• visit the bank you would like to use and ask to open a

basic bank account; and• show them at least two proofs of your identity and

35Stockport Homes - A guide to making the most of your money

Basic Bank Accounts

where you live, for example, a passport, driving licence, utility bill or letter from a government department or local Council confirming your right to state benefits, for example, Job Seekers Allowance (JSA), Council Tax Benefit or Housing Benefit.

What can I use my basic bank account for?

You will be able to:• pay money into your account;• pay cheques into your account;• have benefits paid directly into your account; and• set up regular direct debits to pay bills.

Also, most basic bank accounts will offer a cash card so you can take out money free of charge at a cash machine or post office.

Will I have a cheque book and debit card?

Probably not, most basic bank accounts do not offer a cheque book or debit card.

Can I be overdrawn?

Most basic bank accounts will not allow you to have an overdraft. If you do not have enough money in your account to cover any payments going out (direct debits) you may be charged. It is really important to make sure you have enough money in your account to pay your bills.

36 Stockport Homes - A guide to making the most of your money

Basic Bank Accounts

Home insurance

Section 7

Section 8

How will I know how much is in my account?

You will receive regular statements from the bank and you will probably be able to check your balance at a post office, online or cash machine at any time.

You’re responsible for insuring the contents of your home from fire, theft and flood damage. Stockport Homes offer affordable home contents insurance. There is no excess to pay on your policy if you ever need to make a claim, and future premiums will notincrease as a result. For peace of mind at an affordable price, pick up an application pack from your Area Housing Office or ask for one to be sent to you.

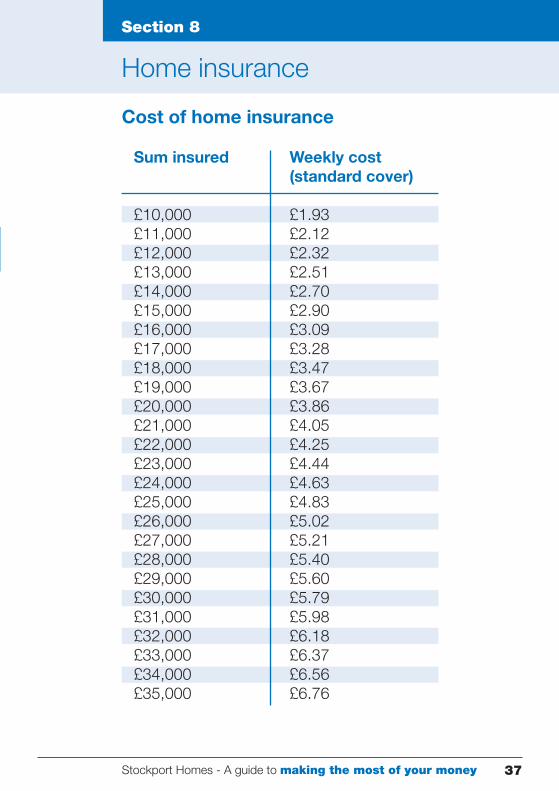

Cost of home insurance

Please see the table opposite and on the following page for a guide to the cost of home insurance. Please note: the premiums shown in the table are payable over 48 weeks. There are other home insurance providers such as Age Concern.

37Stockport Homes - A guide to making the most of your money

Basic Bank Accounts

Home insurance

Home insurance

Section 8

Cost of home insurance

Sum insured

£10,000£11,000£12,000£13,000£14,000£15,000£16,000£17,000£18,000£19,000£20,000£21,000£22,000£23,000£24,000£25,000£26,000£27,000£28,000£29,000£30,000£31,000£32,000£33,000£34,000£35,000

Weekly cost(standard cover)

£1.93£2.12£2.32£2.51£2.70£2.90£3.09£3.28£3.47£3.67£3.86£4.05£4.25£4.44£4.63£4.83£5.02£5.21£5.40£5.60£5.79£5.98£6.18£6.37£6.56£6.76

38 Stockport Homes - A guide to making the most of your money

Stockport Homes’ Contacts

Customer Finance TeamTel: 0161 474 2677 (East Area) 0161 474 2668 (West Area)Email: [email protected]

Customer Involvement TeamTel: 0161 474 2862Email: [email protected]

Debt Outreach WorkerTel: 0161 218 1304Email: [email protected]

Housing OptionsTel: 0161 474 4237Email: [email protected]

Other useful contacts

Stockport Credit UnionTel: 0161 430 5808Web: www.stockportcu.com

Consumer Credit Counselling ServiceTel: 0800 138 1111Web: www.cccs.co.uk

Debt Advice Service4th Floor, Regal House, Duke Street, Stockport SK1 3DATel: 0161 474 3093

Section 9

Useful contacts

39Stockport Homes - A guide to making the most of your money

DebtlineTel: 0161 474 3116 (Tuesday and Thursday afternoons)

Benefits Advice LineTel: 0161 474 6091 (Monday and Friday mornings)

Energy comparison websiteWeb: www.stockporthomesenergy.org.ukTel: 0800 410 1245

Greater Manchester Public TransportTel: 0161 244 1000

Signpost for CarersTorkington Centre, Torkington Road, Hazel Grove, Stockport SK7 4PYTel: 0161 456 4276Email: [email protected]

National DebtlineTel: 0808 808 4000Web: www.nationaldebtline.co.uk

Stockport Citizens Advice BureauTel: 0161 474 3090 / 0844 826 9800Web: www.stockportcab.org.uk or www.citizensadvice.org.uk

Stockport Direct Local CentresTel: 0161 217 6009Web: www.stockport.gov.uk/stockportdirect

Useful contacts

Accessing our services

This leaflet gives you information about managing your money. If you would like a copy in large print, Braille, on audio tape or CD, please contact the Service Improvement Team on 0161 474 2860 or email: [email protected]

Ref

: 773

/Feb

ruar

y 20

11