Embed Size (px)

Citation preview

Making the Transition FromRecovery to ExpansionAUGUSTINE FAUCHER, DIRECTOR OF MACROECONOMICS

FROM MOODY’S ECONOMY.COM

2FROM MOODY’S ECONOMY.COM

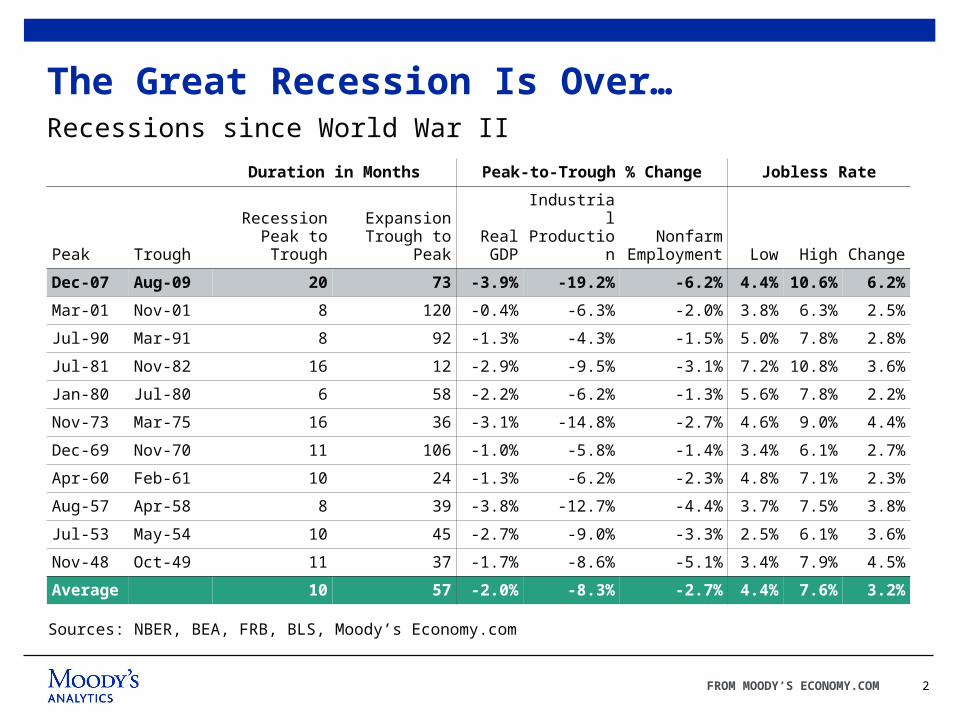

The Great Recession Is Over…Recessions since World War II

Sources: NBER, BEA, FRB, BLS, Moody’s Economy.com

Duration in Months Peak-to-Trough % Change Jobless Rate

Peak TroughRecession

Peak to TroughExpansion

Trough to PeakReal GDP

Industrial Production

Nonfarm Employment Low High Change

Dec-07 Aug-09 20 73 -3.9% -19.2% -6.2% 4.4% 10.6% 6.2%

Mar-01 Nov-01 8 120 -0.4% -6.3% -2.0% 3.8% 6.3% 2.5%

Jul-90 Mar-91 8 92 -1.3% -4.3% -1.5% 5.0% 7.8% 2.8%

Jul-81 Nov-82 16 12 -2.9% -9.5% -3.1% 7.2% 10.8% 3.6%

Jan-80 Jul-80 6 58 -2.2% -6.2% -1.3% 5.6% 7.8% 2.2%

Nov-73 Mar-75 16 36 -3.1% -14.8% -2.7% 4.6% 9.0% 4.4%

Dec-69 Nov-70 11 106 -1.0% -5.8% -1.4% 3.4% 6.1% 2.7%

Apr-60 Feb-61 10 24 -1.3% -6.2% -2.3% 4.8% 7.1% 2.3%

Aug-57 Apr-58 8 39 -3.8% -12.7% -4.4% 3.7% 7.5% 3.8%

Jul-53 May-54 10 45 -2.7% -9.0% -3.3% 2.5% 6.1% 3.6%

Nov-48 Oct-49 11 37 -1.7% -8.6% -5.1% 3.4% 7.9% 4.5%

Average 10 57 -2.0% -8.3% -2.7% 4.4% 7.6% 3.2%

3FROM MOODY’S ECONOMY.COM

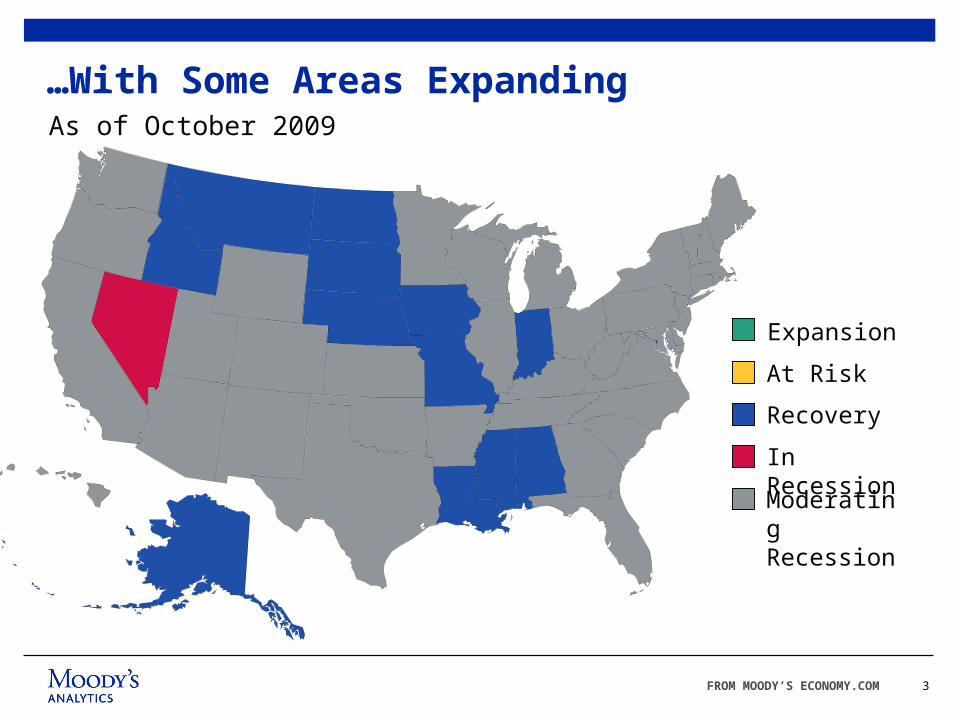

…With Some Areas ExpandingAs of October 2009

Expansion

At Risk

Recovery

In Recession

Moderating Recession

4FROM MOODY’S ECONOMY.COM

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

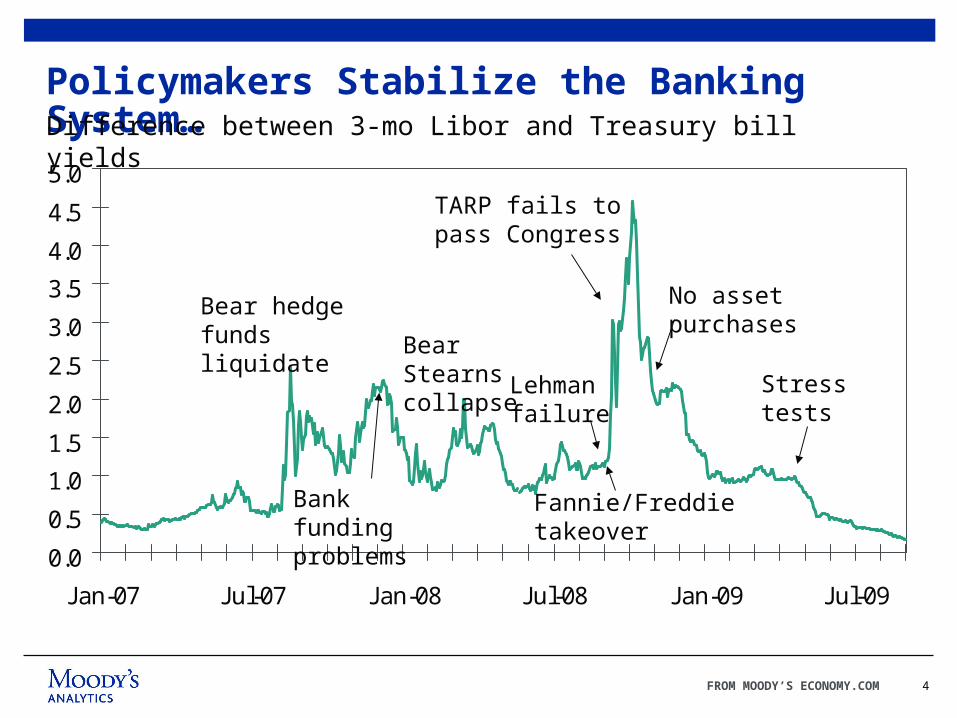

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09

Policymakers Stabilize the Banking System…

Bear hedgefunds liquidate

Bank fundingproblems

Difference between 3-mo Libor and Treasury bill yields

Bear Stearnscollapse Lehman

failure

Fannie/Freddietakeover

TARP fails topass Congress

No assetpurchases

Stresstests

5FROM MOODY’S ECONOMY.COM

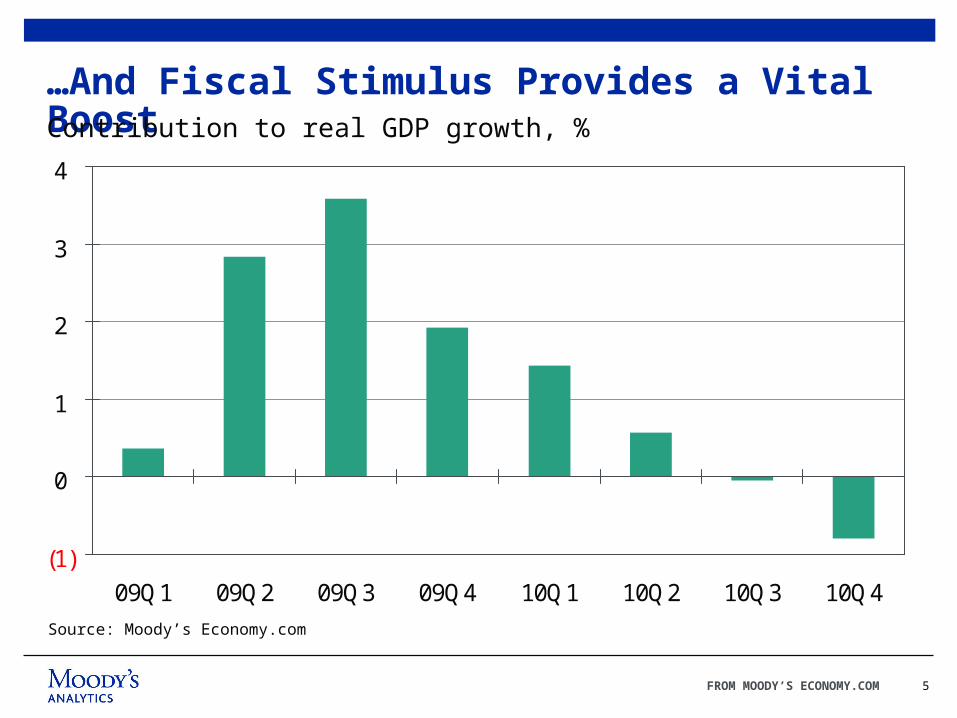

(1)

0

1

2

3

4

09Q1 09Q2 09Q3 09Q4 10Q1 10Q2 10Q3 10Q4

…And Fiscal Stimulus Provides a Vital Boost

Source: Moody’s Economy.com

Contribution to real GDP growth, %

6FROM MOODY’S ECONOMY.COM

5

6

7

8

9

92 94 96 98 00 02 04 06 08

Job Creation Craters…Rate of job creation and destruction, %

Job Creation

Source: BLS

Job Destruction

7FROM MOODY’S ECONOMY.COM

0

1

2

3

4

5

6

-3 -2 -1 0 1 2 3 4 5

Difference between actual and natural unemployment rate

Com

pens

atio

n gr

owth

Source: BLS

y = -0.48x + 3.40R2 = 0.32

2009Q3Unemployment rate=9.6%

Natural rate=5.4%Compensation growth=1.5%

…Threatening to Undermine Compensation…1985Q1-2009Q3

8FROM MOODY’S ECONOMY.COM

…But Fiscal Policymakers Are Responding

» Recently passed: $45 billion in more aid to unemployed workers, extension and expansion of homebuyer tax credit, extended higher conforming loans limits, and NOL.

» High odds of passage: $100 billion in aid for workers losing jobs in 2010.

» Better than even odds of passage: $50 billion in more SBA lending, job tax credit, weatherization program.

» Even odds of passage: $50 billion in another round of help to financially stressed state and local government for FMAP.

9FROM MOODY’S ECONOMY.COM

100

120

140

160

180

200

00 01 02 03 04 05 06 07 08 09 10 11 12

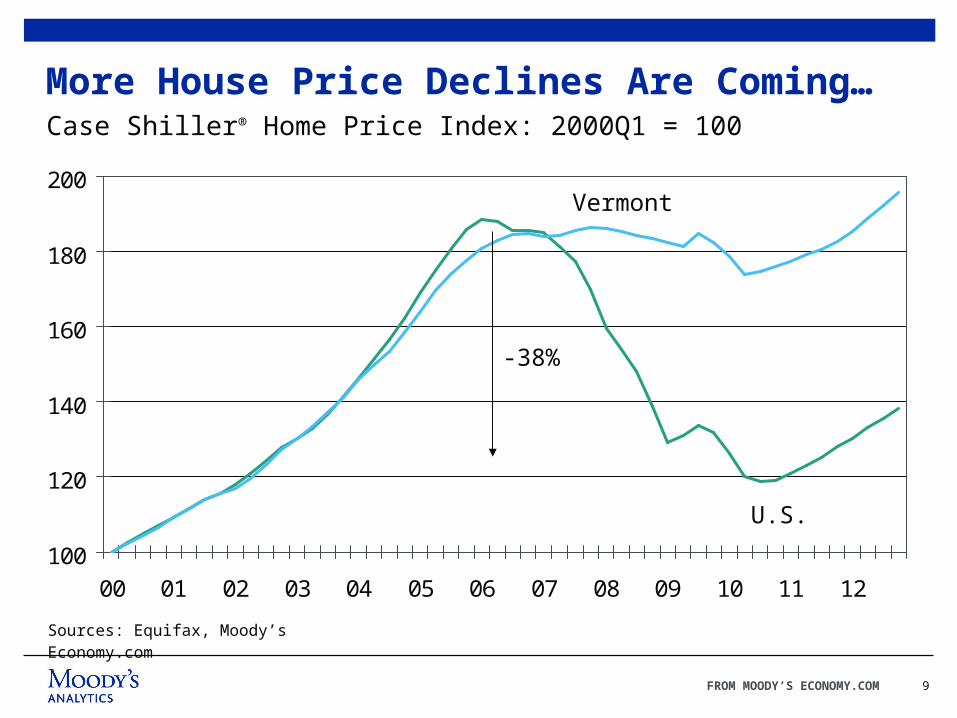

More House Price Declines Are Coming…

Case Shiller® Home Price Index: 2000Q1 = 100

Sources: Equifax, Moody’s Economy.com

-38%

U.S.

Vermont

10FROM MOODY’S ECONOMY.COM

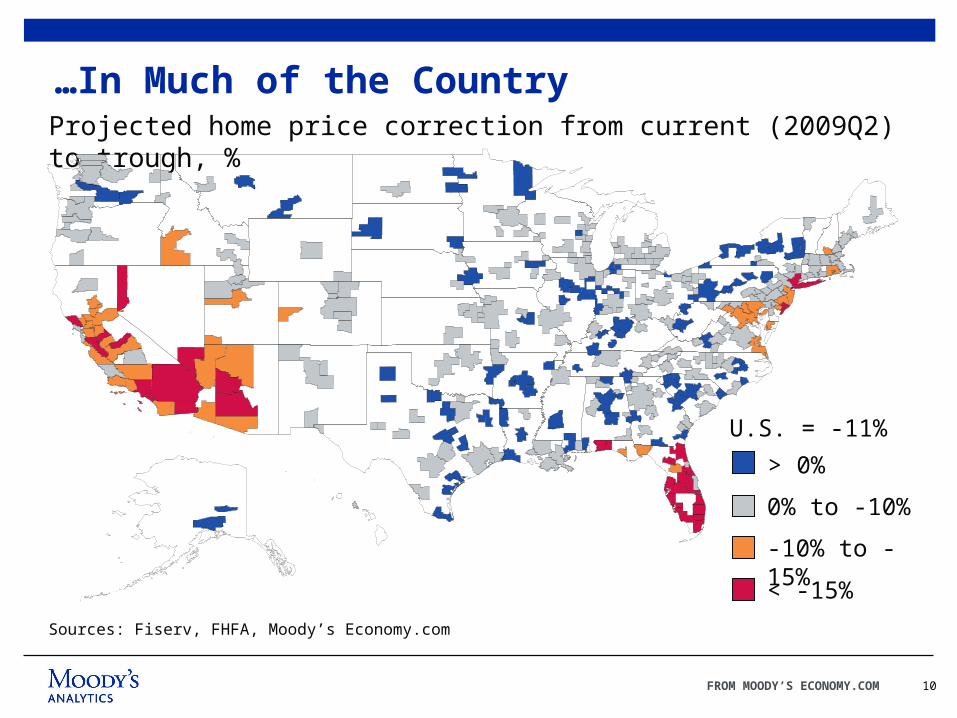

…In Much of the CountryProjected home price correction from current (2009Q2) to trough, %

Sources: Fiserv, FHFA, Moody’s Economy.com

> 0%

0% to -10%

-10% to -15%

< -15%

U.S. = -11%

11FROM MOODY’S ECONOMY.COM

0

5

10

15

20

25

30

35

40

45

50

05 06 07 08 09

-25

-20

-15

-10

-5

0

5

10

15

20

25

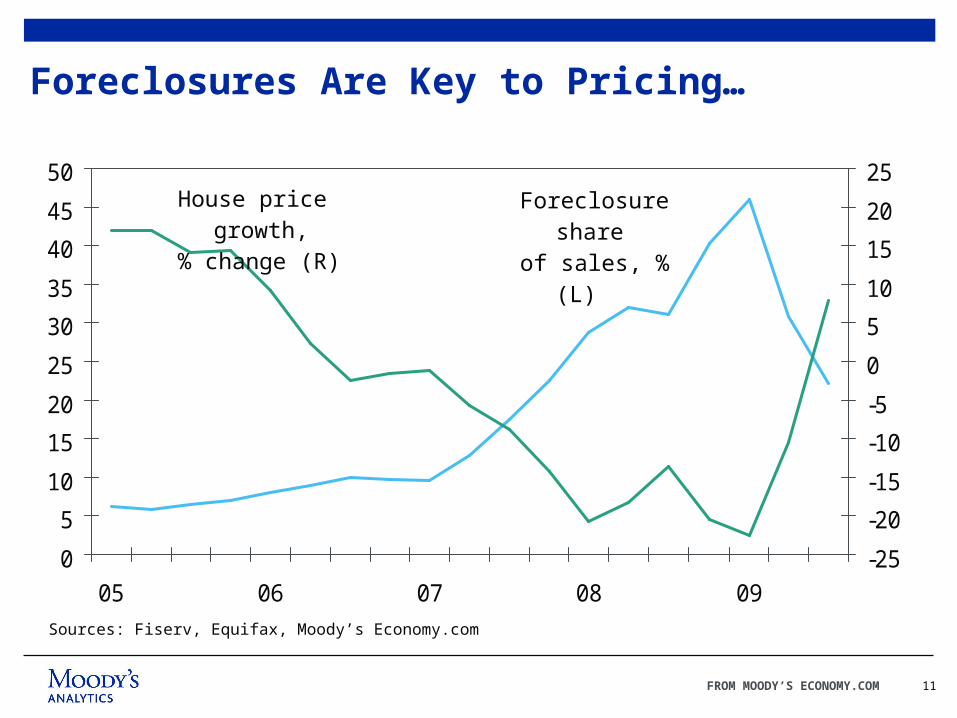

Foreclosures Are Key to Pricing…

Sources: Fiserv, Equifax, Moody’s Economy.com

House price growth, % change (R)

Foreclosure share

of sales, % (L)

12FROM MOODY’S ECONOMY.COM

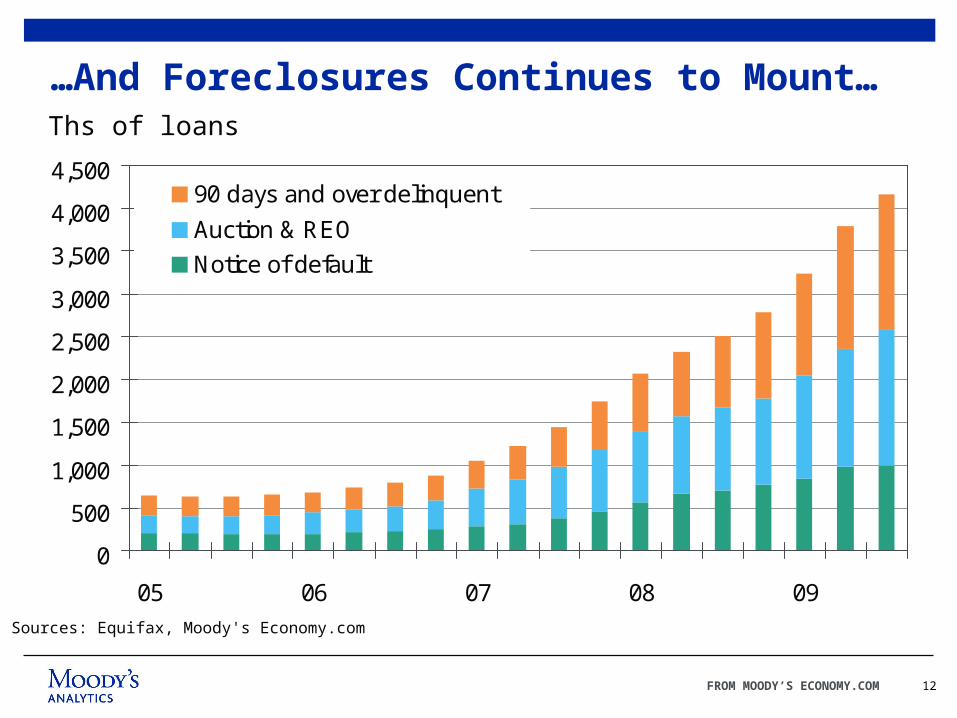

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

05 06 07 08 09

90 days and over delinquent

Auction & REO

Notice of default

Sources: Equifax, Moody's Economy.com

…And Foreclosures Continues to Mount…Ths of loans

13FROM MOODY’S ECONOMY.COM

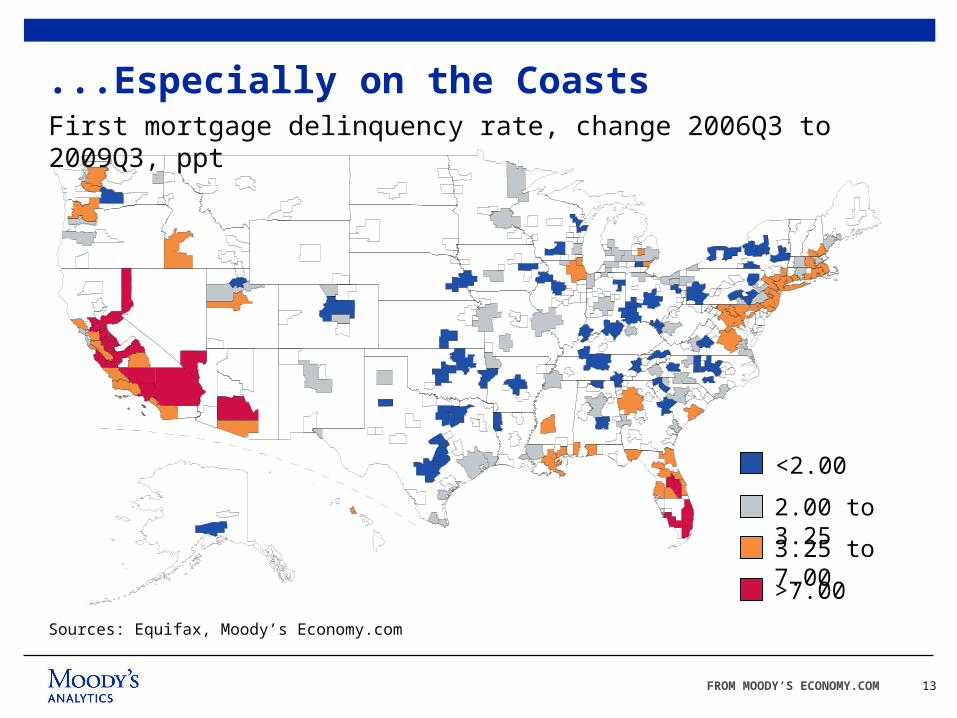

...Especially on the CoastsFirst mortgage delinquency rate, change 2006Q3 to 2009Q3, ppt

Sources: Equifax, Moody’s Economy.com

<2.00

2.00 to 3.25

3.25 to 7.00

>7.00

14FROM MOODY’S ECONOMY.COM

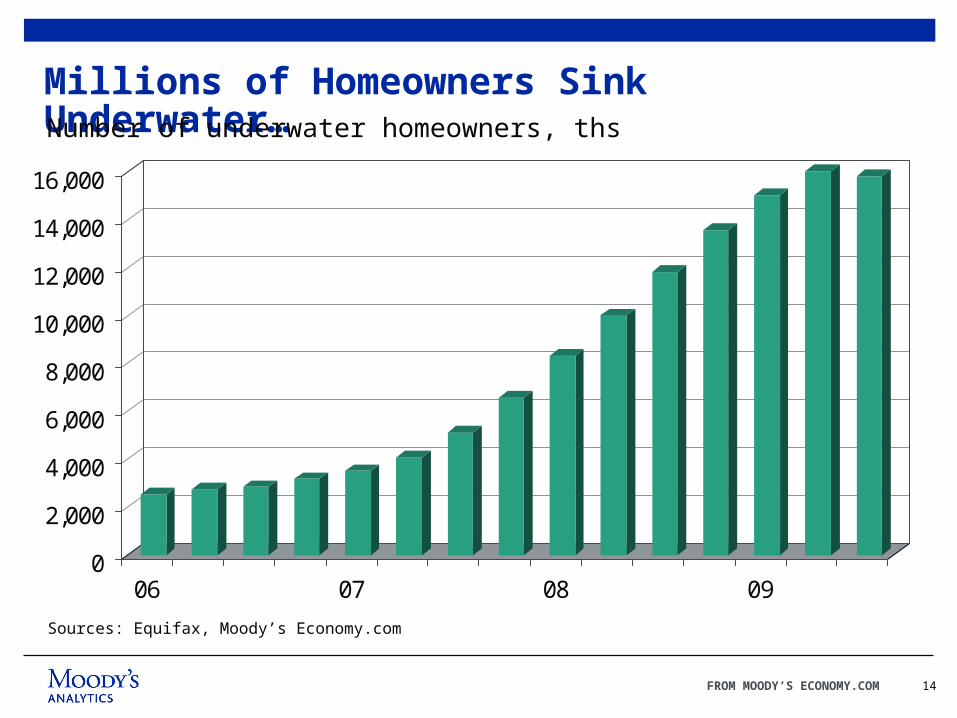

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

06 07 08 09

Millions of Homeowners Sink Underwater…Number of underwater homeowners, ths

Sources: Equifax, Moody’s Economy.com

15FROM MOODY’S ECONOMY.COM

2 3 4 5 6 7 8 9 10

< 6060-6565-7070-7575-8080-8585-9090-95

95-100100-105105-110110-115115-120

> 120

…And Strategic Defaults Are on the Rise90 Days and Over Delinquency Rate, % of #, by CLTV, 30-35% DTI

Sources: Equifax, Moody’s Economy.com

16FROM MOODY’S ECONOMY.COM

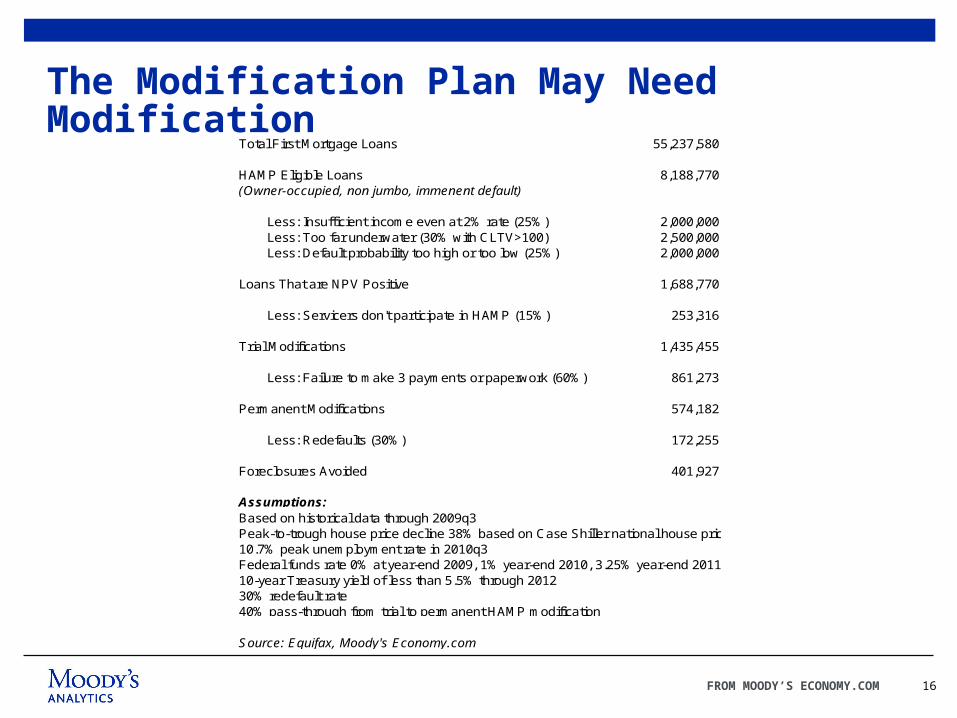

The Modification Plan May Need Modification

Total First Mortgage Loans 55,237,580

HAMP Eligible Loans 8,188,770(Owner-occupied, non jumbo, immenent default)

Less: Insufficient income even at 2% rate (25%) 2,000,000Less: Too far underwater (30% with CLTV>100) 2,500,000Less: Default probability too high or too low (25%) 2,000,000

Loans That are NPV Positive 1,688,770

Less: Servicers don't participate in HAMP (15%) 253,316

Trial Modifications 1,435,455

Less: Failure to make 3 payments or paperwork (60%) 861,273

Permanent Modifications 574,182

Less: Redefaults (30%) 172,255

Foreclosures Avoided 401,927

Assumptions:Based on historical data through 2009q3Peak-to-trough house price decline 38% based on Case Shiller national house price index; trough in 1010q310.7% peak unemployment rate in 2010q3Federal funds rate 0% at year-end 2009, 1% year-end 2010, 3.25% year-end 2011, 4.5% by year-end 201210-year Treasury yield of less than 5.5% through 201230% redefault rate40% pass-through from trial to permanent HAMP modification

Source: Equifax, Moody's Economy.com

17FROM MOODY’S ECONOMY.COM

0

500

1,000

1,500

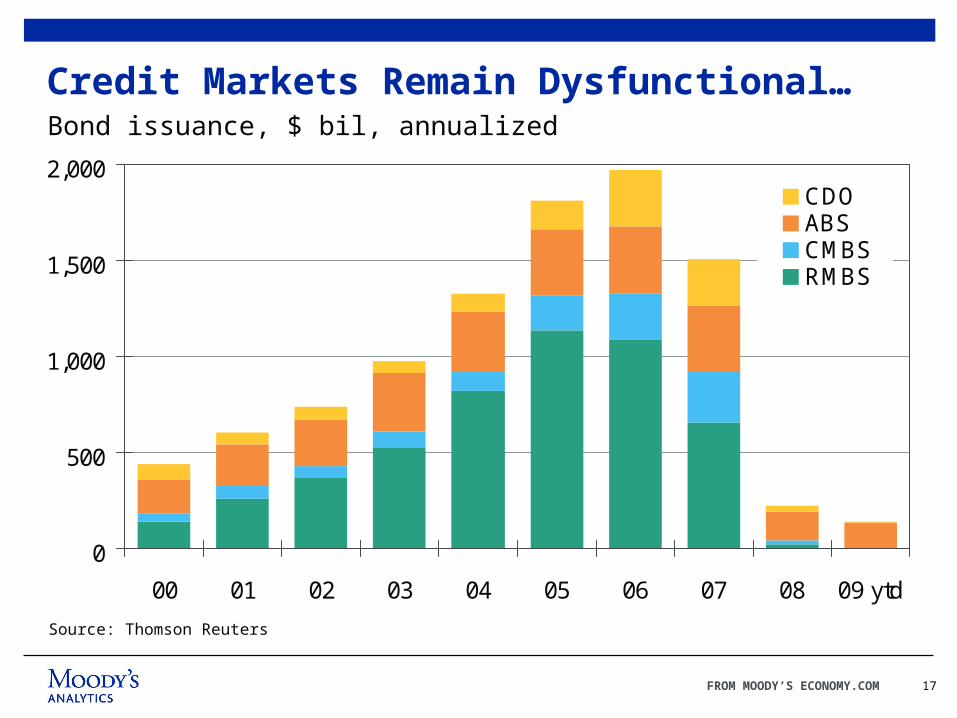

2,000

00 01 02 03 04 05 06 07 08 09 ytd

CDOABSCMBSRMBS

Credit Markets Remain Dysfunctional…Bond issuance, $ bil, annualized

Source: Thomson Reuters

18FROM MOODY’S ECONOMY.COM

-1

0

1

2

3

4

5

6

7

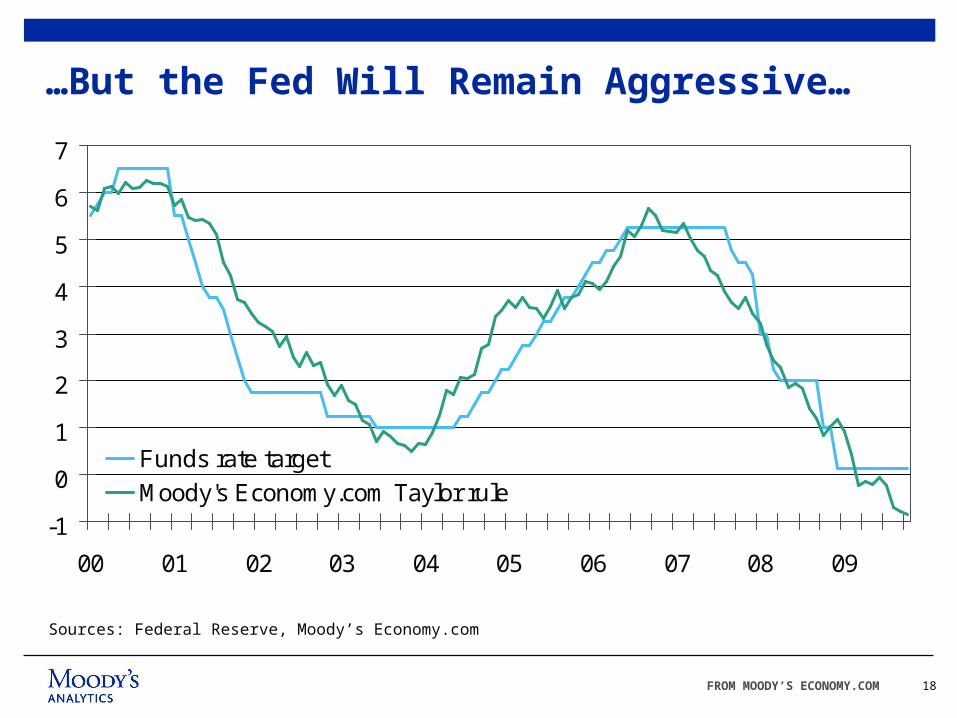

00 01 02 03 04 05 06 07 08 09

Funds rate target

Moody's Economy.com Taylor rule

…But the Fed Will Remain Aggressive…

Sources: Federal Reserve, Moody’s Economy.com

19FROM MOODY’S ECONOMY.COM

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

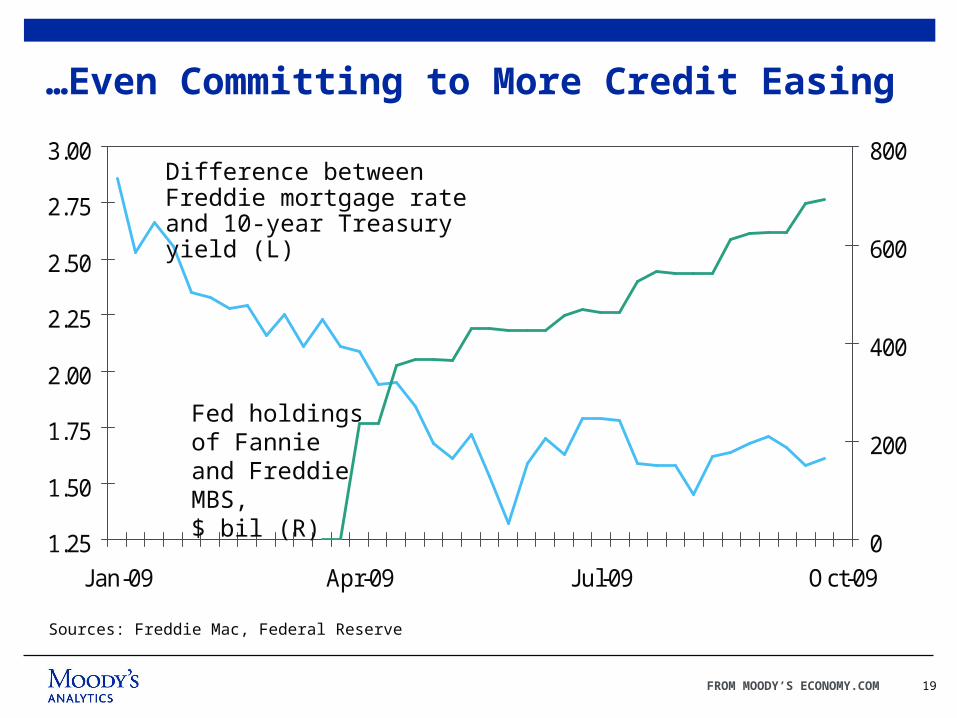

Jan-09 Apr-09 Jul-09 Oct-09

0

200

400

600

800

…Even Committing to More Credit Easing

Sources: Freddie Mac, Federal Reserve

Fed holdings of Fannie and Freddie MBS, $ bil (R)

Difference between Freddie mortgage rate and 10-year Treasury yield (L)

20FROM MOODY’S ECONOMY.COM

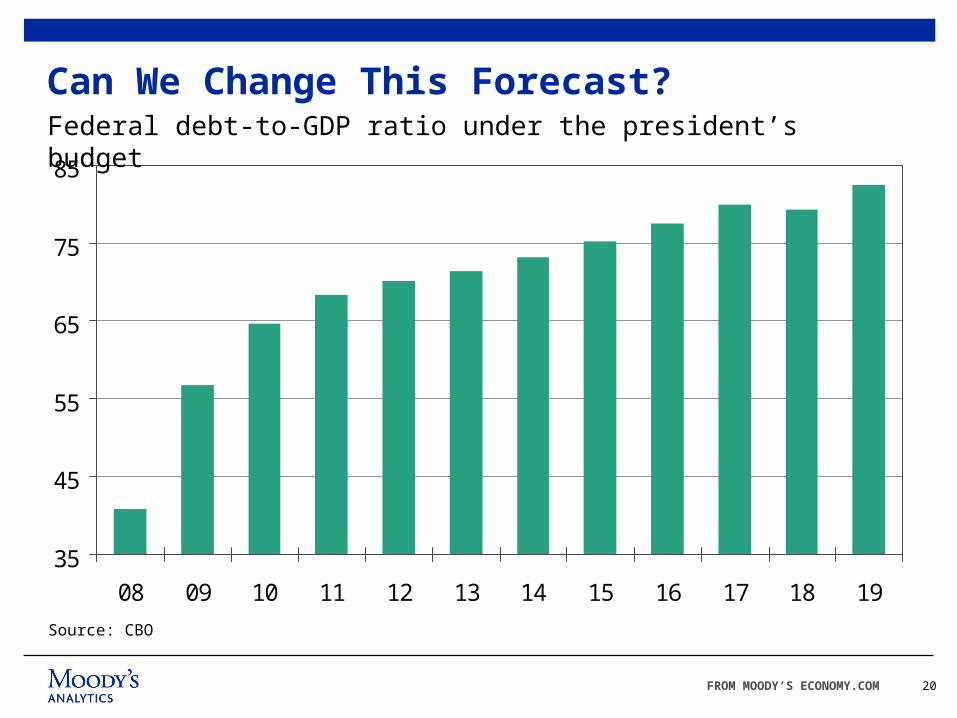

35

45

55

65

75

85

08 09 10 11 12 13 14 15 16 17 18 19

Can We Change This Forecast?Federal debt-to-GDP ratio under the president’s budget

Source: CBO

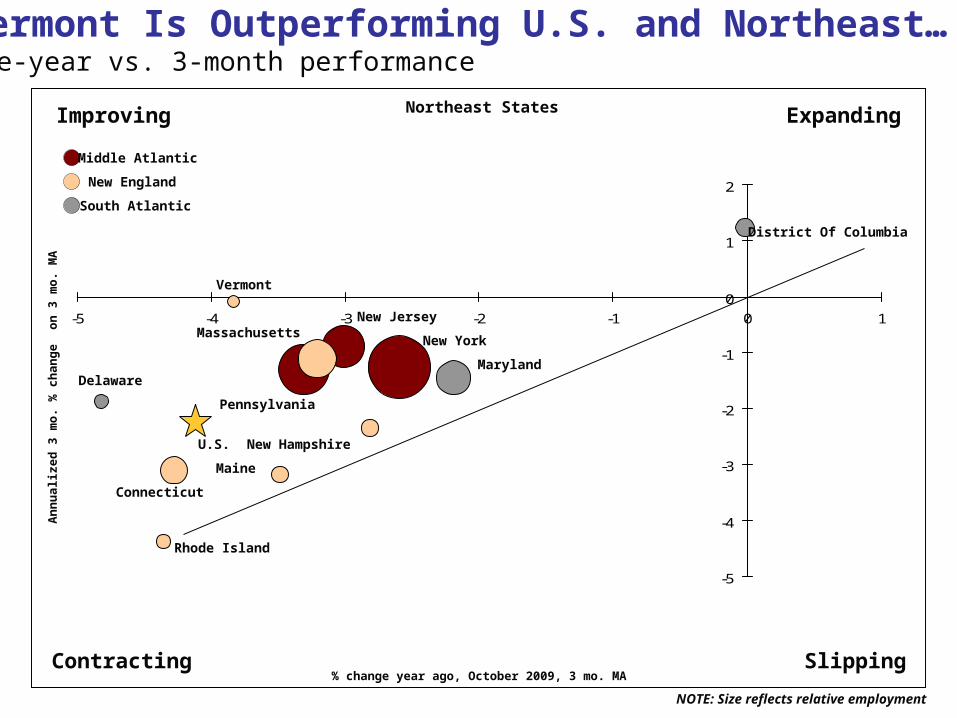

Improving Expanding

SlippingContracting

An

nu

aliz

ed

3 m

o.

% c

han

ge

o

n 3

mo

. M

A

NOTE: Size reflects relative employment

% change year ago, October 2009, 3 mo. MA

Middle Atlantic

New England

South Atlantic

Vermont Is Outperforming U.S. and Northeast…One-year vs. 3-month performance

Northeast States

-5

-4

-3

-2

-1

0

1

2

-5 -4 -3 -2 -1 0 1

New York

Pennsylvania

New JerseyMassachusetts

Connecticut

New Hampshire

Maine

Rhode Island

Vermont

Maryland

District Of Columbia

Delaware

U.S.

22FROM MOODY’S ECONOMY.COM

-5

-4

-3

-2

-1

0

1

2

3

4

08 09 10 11 12

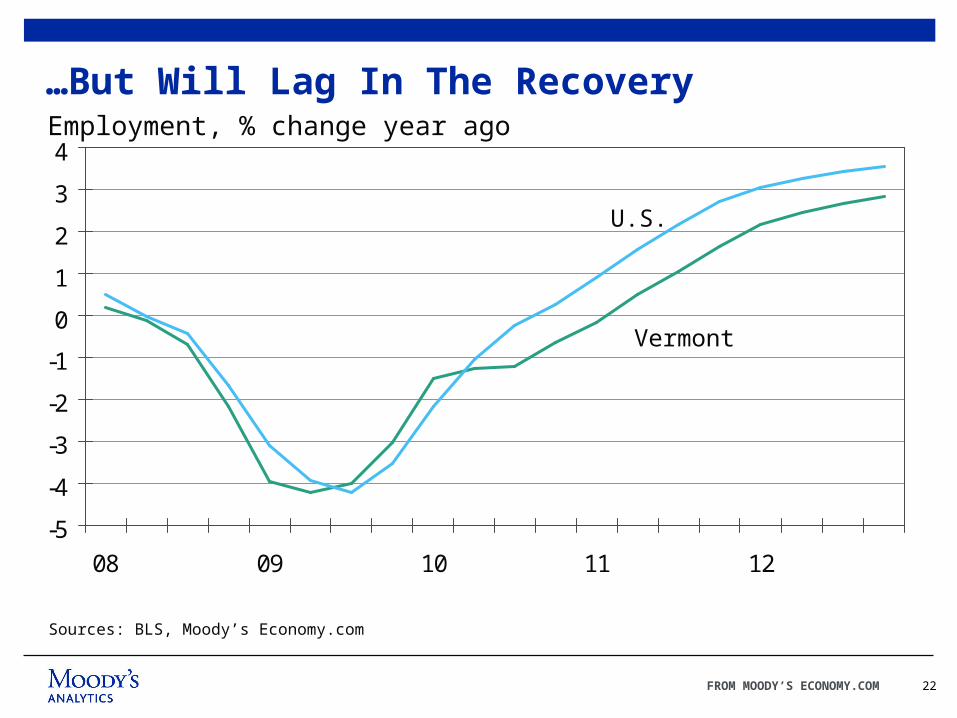

…But Will Lag In The Recovery

Sources: BLS, Moody’s Economy.com

Employment, % change year ago

U.S.

Vermont

23FROM MOODY’S ECONOMY.COM

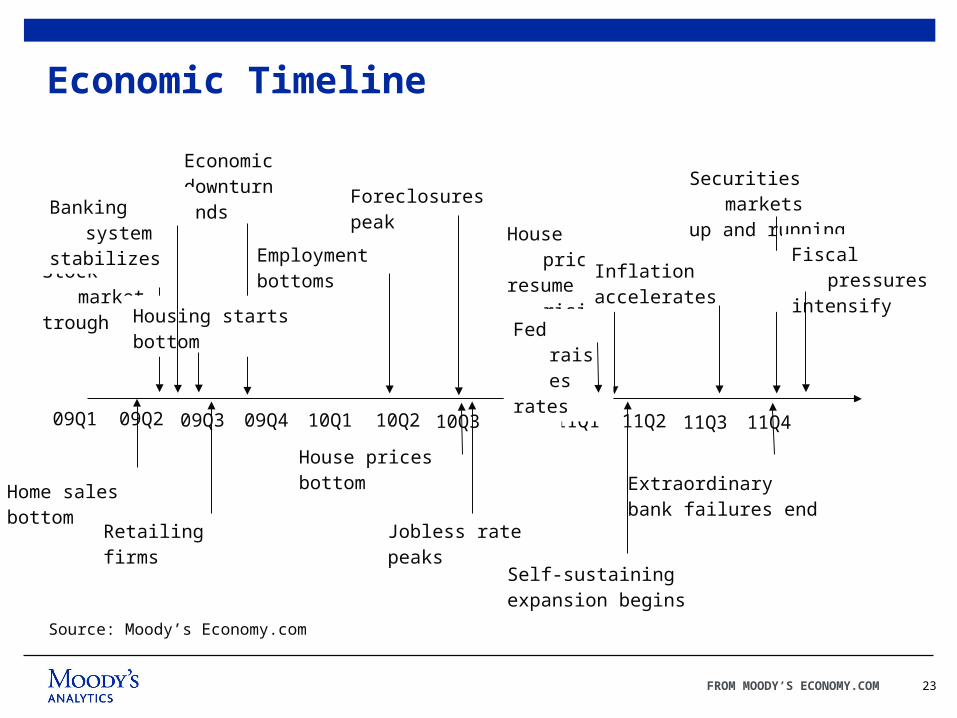

Economic Timeline

Source: Moody’s Economy.com

09Q1 09Q2 09Q3 09Q4 10Q1 10Q2 10Q4 11Q1 11Q2 11Q3 11Q4

Stock markettrough

Extraordinarybank failures end

Home salesbottom

Housing startsbottom

Employmentbottoms

House pricesbottom

Foreclosurespeak

Jobless ratepeaks

House pricesresume rising

Economicdownturnends

Self-sustainingexpansion begins

Banking systemstabilizes

Retailingfirms

10Q3

Securities marketsup and running

Fed raisesrates

Inflationaccelerates

Fiscal pressuresintensify

24FROM MOODY’S ECONOMY.COM

www.economy.com

25FROM MOODY’S ECONOMY.COM

© 2009 Moody’s Analytics, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding, or selling.

![Index [genealogiestemarie.ca] de décès/Marie dfts... · 2018. 4. 26. · Faucher, Gérard 03/04/2016 Faucher, Madeleine 25/02/2016 Faucher, Noëlla 06/05/2016 Faucher, Yolande 10/04/2016](https://img.pdfslide.net/doc/110x75/5ff505a3753e9e028708a834/index-de-dcsmarie-dfts-2018-4-26-faucher-grard-03042016.jpg)