Embed Size (px)

Citation preview

Malardalen International Science ProgrammeWorkshop in Mathematics and Applied Mathematics -

ISPMAM 2017

dedicated to celebration ofprofessor Anatoliy Malyarenko’s 60th birthday

will take place inVasteras, Sweden, Wednesday 26 April 2017.

Organized by

• MAM Mathematics and Applied Mathematics research environmentDivision of Applied Mathematics, Malardalen University, Sweden

under auspices of• International Science Programme in Mathematics (Uppsala)

Program scope and goals

This workshop is aimed at bringing together PhD students and researchers and theirsupervisors at Swedish Universities taking part in International Science Programmein Mathematics and bilateral Sida projects for research capacity building in Mathe-matics between Sweden and other countries.

Topics

The main areas of the ISPMAM 2017 Workshop are

• Mathematics• Applied Mathematics• Engineering Mathematics• Industrial Mathematics• Applications of Mathematics in other subjects, industry and society

Organising and Programme Committee

Malardalen University

Sergei Silvestrov (chair), MAM Mathematics and Applied Mathematics researchenvironment, Division of Applied Mathematics, Malardalen University, Sweden

Milica Rancic (co-Chair), MAM Mathematics and Applied Mathematics researchenvironment, Division of Applied Mathematics, Malardalen University, Sweden

Johan Richter, Division of Applied Mathematics, Malardalen University, Sweden

Karl Lundengard, Division of Applied Mathematics, Malardalen University, Swe-den

Christopher Engstrom, Division of Applied Mathematics, Malardalen University,Sweden

Alex Tumwesigye, Division of Applied Mathematics, Malardalen University, Swe-den and Makerere University, Uganda

Tin Nwe Aye, Division of Applied Mathematics, Malardalen University, Swedenand University of Mandalay, Myanmar

International Science Programme

Leif Abrahamsson (co-Chair), ISP - International Science Program, Uppsala Uni-versity, Director of International Science Programme in Mathematics

Bengt-Ove Thuresson (co-Chair), Department of Mathematics, Linkoping Univer-sity, coordinator of Sida bilateral programmes in Mathematics with Uganda, Tanza-nia, Rwanda and Mozambique

Venue & Contact

Venue Contact

room Kappa, House U Dr. Milica RancicMalardalen University e-mail: [email protected] 1 Professor Sergei Silvestrov721 23 Vasteras e-mail: [email protected]

Acknowledgements

ISPMAM 2017 would like to acknowledge the support by the

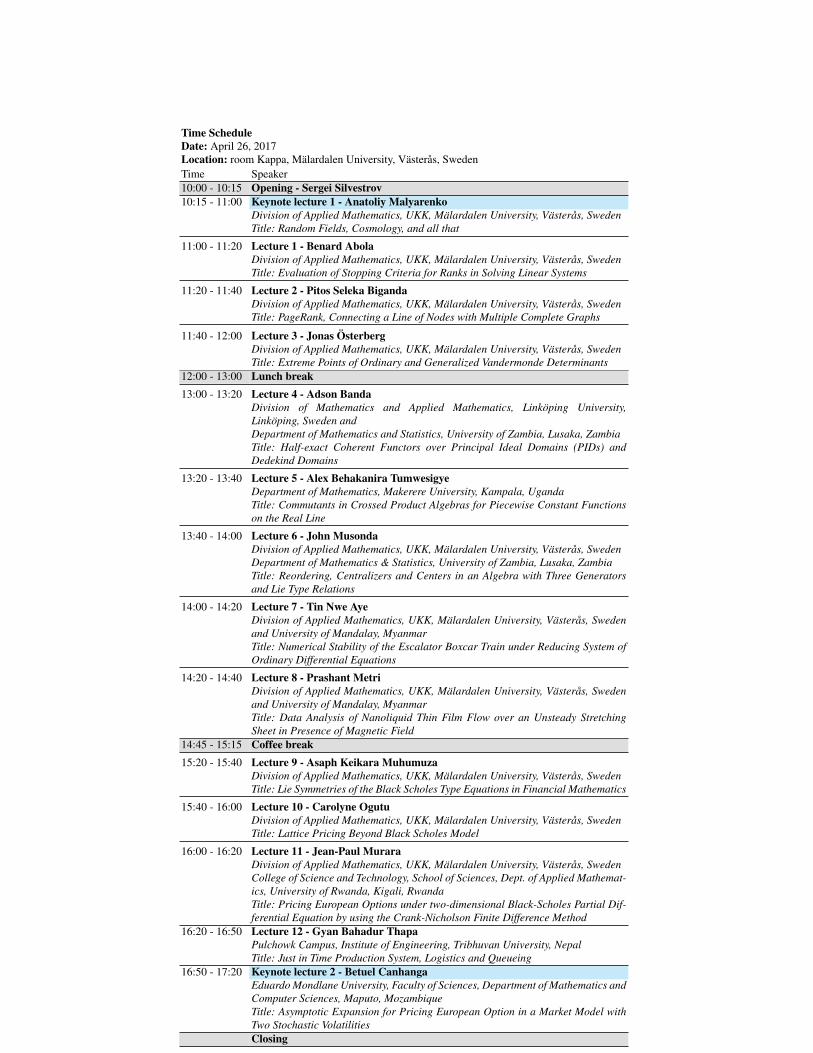

Time ScheduleDate: April 26, 2017Location: room Kappa, Malardalen University, Vasteras, SwedenTime Speaker10:00 - 10:15 Opening - Sergei Silvestrov10:15 - 11:00 Keynote lecture 1 - Anatoliy Malyarenko

Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenTitle: Random Fields, Cosmology, and all that

11:00 - 11:20 Lecture 1 - Benard AbolaDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenTitle: Evaluation of Stopping Criteria for Ranks in Solving Linear Systems

11:20 - 11:40 Lecture 2 - Pitos Seleka BigandaDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenTitle: PageRank, Connecting a Line of Nodes with Multiple Complete Graphs

11:40 - 12:00 Lecture 3 - Jonas OsterbergDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenTitle: Extreme Points of Ordinary and Generalized Vandermonde Determinants

12:00 - 13:00 Lunch break13:00 - 13:20 Lecture 4 - Adson Banda

Division of Mathematics and Applied Mathematics, Linkoping University,Linkoping, Sweden andDepartment of Mathematics and Statistics, University of Zambia, Lusaka, ZambiaTitle: Half-exact Coherent Functors over Principal Ideal Domains (PIDs) andDedekind Domains

13:20 - 13:40 Lecture 5 - Alex Behakanira TumwesigyeDepartment of Mathematics, Makerere University, Kampala, UgandaTitle: Commutants in Crossed Product Algebras for Piecewise Constant Functionson the Real Line

13:40 - 14:00 Lecture 6 - John MusondaDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenDepartment of Mathematics & Statistics, University of Zambia, Lusaka, ZambiaTitle: Reordering, Centralizers and Centers in an Algebra with Three Generatorsand Lie Type Relations

14:00 - 14:20 Lecture 7 - Tin Nwe AyeDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, Swedenand University of Mandalay, MyanmarTitle: Numerical Stability of the Escalator Boxcar Train under Reducing System ofOrdinary Differential Equations

14:20 - 14:40 Lecture 8 - Prashant MetriDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, Swedenand University of Mandalay, MyanmarTitle: Data Analysis of Nanoliquid Thin Film Flow over an Unsteady StretchingSheet in Presence of Magnetic Field

14:45 - 15:15 Coffee break15:20 - 15:40 Lecture 9 - Asaph Keikara Muhumuza

Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenTitle: Lie Symmetries of the Black Scholes Type Equations in Financial Mathematics

15:40 - 16:00 Lecture 10 - Carolyne OgutuDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenTitle: Lattice Pricing Beyond Black Scholes Model

16:00 - 16:20 Lecture 11 - Jean-Paul MuraraDivision of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCollege of Science and Technology, School of Sciences, Dept. of Applied Mathemat-ics, University of Rwanda, Kigali, RwandaTitle: Pricing European Options under two-dimensional Black-Scholes Partial Dif-ferential Equation by using the Crank-Nicholson Finite Difference Method

16:20 - 16:50 Lecture 12 - Gyan Bahadur ThapaPulchowk Campus, Institute of Engineering, Tribhuvan University, NepalTitle: Just in Time Production System, Logistics and Queueing

16:50 - 17:20 Keynote lecture 2 - Betuel CanhangaEduardo Mondlane University, Faculty of Sciences, Department of Mathematics andComputer Sciences, Maputo, MozambiqueTitle: Asymptotic Expansion for Pricing European Option in a Market Model withTwo Stochastic VolatilitiesClosing

Contents

Random Fields, Cosmology, and all that . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Anatoliy Malyarenko1*

Evaluation of Stopping Criteria for Ranks in Solving Linear Systems . . . . 3Benard Abola1*, Pitos Seleka Biganda1, Christopher Engstrom1, SergeiSilvestrov1

PageRank, Connecting a Line of Nodes with Multiple Complete Graphs . . 5Pitos Seleka Biganda1*, Benard Abola1, Christopher Engstrom1, SergeiSilvestrov1

Extreme Points of Ordinary and Generalized VandermondeDeterminants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Jonas Osterberg1, Sergei Silvestrov1, Karl Lundengard1

Half-exact Coherent Functors over Principal Ideal Domains (PIDs) andDedekind Domains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Adson Banda1*

Commutants in Crossed Product Algebras for Piecewise ConstantFunctions on the Real Line . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Alex Behakanira Tumwesigye2*, Johan Richter1, Sergei Silvestrov1

Reordering, Centralizers and Centers in an Algebra with ThreeGenerators and Lie Type Relations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13John Musonda 1,3*, Sergei Silvestrov 1, Sten Kaijser2

Numerical Stability of the Escalator Boxcar Train under ReducingSystem of Ordinary Differential Equations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Tin Nwe Aye1*, Linus Carlsson2, Sergei Silvestrov2

Contents

Data Analysis of Nanoliquid Thin Film Flow over an UnsteadyStretching Sheet in Presence of Magnetic Field . . . . . . . . . . . . . . . . . . . . . . . . 17Prashant G Metri1*, Sergei Silvestrov1

Lie Symmetries of the Black Scholes Type Equations in FinancialMathematics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Asaph Keikara Muhumuza1*, Anatoliy Malyarenko1, Sergei Silvestrov 1

Lattice Pricing Beyond Black Scholes Model . . . . . . . . . . . . . . . . . . . . . . . . . . 21Carolyne Ogutu1*, Karl Lundengard1, Ivivi Mwaniki2, Sergei Silvestrov1,Patrick Weke2

Pricing European Options under two-dimensional Black-Scholes PartialDifferential Equation by using the Crank-Nicholson Finite DifferenceMethod . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Jean-Paul Murara1, 3*, Betuel Canhanga2,3, Anatoliy Malyarenko3, YingNi3, Sergei Silvestrov3

Just in Time Production System, Logistics and Queueing . . . . . . . . . . . . . . . 25Gyan Bahadur Thapa 1*, Sushil Ghimire 1, Ram Prasad Ghimire 2, SergeiSilvestrov 3

Asymptotic Expansion for Pricing European Option in a Market Modelwith Two Stochastic Volatilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Betuel Canhanga1*, Anatoliy Malyarenko2, Ying Ni2, Sergei Silvestrov2,Milica Rancic2

Random Fields, Cosmology, and all that

Anatoliy Malyarenko1*

Abstract: A working mathematician has to know everything about something andsomething about everything. To illustrate this thesis, we present a pedagogical in-troduction into a research area lying somewhere between probability, differentialgeometry, group representations, special functions, and cosmology. Several exam-ples from astrophysics are included.

Keywords: Cosmic microwave background — Gravitational lensing — Randomfield

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: :[email protected]

1

2 Anatoliy Malyarenko1*

Biography

Anatoliy Malyarenko received the PhD degree in mathe-matics from Taras Shevchenko National University, Kyiv,Ukraine, in 1985.Between 1985 and 2000 he worked as a researcher at the Sta-tistical Research Centre of the above university and Interna-tional Mathematical Centre of the National Academy of Sci-ence of Ukraine. Since 2000 he is working at the MalardalenUniversity, Vasteras, Sweden, currently as a professor.His research interests include random functions of severalvariables, actuarial and financial mathematics, and computersimulation of real-world systems.

Evaluation of Stopping Criteria for Ranks inSolving Linear Systems

Benard Abola1*, Pitos Seleka Biganda1, Christopher Engstrom1, Sergei Silvestrov1

Abstract: Linear systems of algebraic equations arising from mathematical for-mulation of natural phenomena or technological processes are common. Many ofthese systems of equations are large, the matrices derived are mainly sparse andneed to be solved iteratively. Moreover, interpretation is crucial in making decision.Bioinformatics, internet search engines (webpages) and social networks are someof the examples with large and high sparsity matrices. For some of these systemsonly the actual ranks of the solution vector is interesting rather than the vector it-self. In this case, it is desirable that the stopping criterion reflects the error in ranksrather than the residual vector which might have a slower convergence. In this paper,we will evaluate stopping criteria on Jacobi, successive over relaxation and powerseries iterative schemes. We will focus on the following criteria: Infinity norm ofresidual, componentwise backward error, normwise backward error, Kendall τ rankcorrelation and top-k list. Numerical experiments will be performed to evaluate per-formance of each stopping criterion for ranks on the iterative methods.

Keywords: Stopping criterion — Networks — Ranks — Iterative methods

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

3

4 Benard Abola1*, Pitos Seleka Biganda1, Christopher Engstrom1, Sergei Silvestrov1

Biography

Benard Abola is a lecturer at the department of mathematics,Gulu University, Uganda with a master of science in mathe-matics, Makerere University, Kampala, Uganda.Currently, a doctoral student at Division of Applied Math-ematics, Malardalen University, Sweden under MakerereUniversity-SIDA bi-lateral Program. My research concernsmathematical statistics of big complex data. The researchlies in the field of ranking and classification of networks sys-tems such as webpages, biological and finance.

PageRank, Connecting a Line of Nodes withMultiple Complete Graphs

Pitos Seleka Biganda1*, Benard Abola1, Christopher Engstrom1, Sergei Silvestrov1

Abstract: PageRank was initially defined by S. Brin and L. Page for the purposeof ranking homepages (nodes) based on the structure of links between these pages.Studies has shown that PageRank of a graph changes with changes in the structureof the graph. In this article we will examine how the PageRank changes when two ormore complete graphs are connected to a line directed graph whose nodes are linkedbetween themselves in a number of ways. We will also look at the PageRank of agraph resulting from Kronecker products on adjacency matrices of two graphlets.We will develop explicit formulas for the PageRank in each consideration, and usethem to look at the behaviour of the ranking as the system changes.

Keywords: PageRank — Graph — Random walk — Kronecker product

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

5

6 Pitos Seleka Biganda1*, Benard Abola1, Christopher Engstrom1, Sergei Silvestrov1

Biography

Pitos Seleka Biganda is a PhD student in applied mathe-matics at Malardalen University under SIDA-Tanzania bi-lateral programme. He was born in Kigoma, Tanzania in1981. He received a Bachelor of Science with education de-gree, majoring in mathematics from University of Dar esSalaam, Tanzania in 2008 and a Master of Science in Tech-nomathematics from Lappeenranta University of Technol-ogy, Finland in 2009. He is working as an assistant lec-turer in mathematics at the University of Dar es Salaam, de-partment of mathematics since 2009. His research interestsinclude PageRank and complex networks analysis, matrixanalysis and mathematical statistics.

Extreme Points of Ordinary and GeneralizedVandermonde Determinants

Jonas Osterberg1, Sergei Silvestrov1, Karl Lundengard1

Abstract: The Vandermonde determinant has some interesting geometric and alge-braic properties as a multivariate function. Due to its symmetry, optimization oversymmetric surfaces in various dimensions will lead to symmetrically placed solu-tions, and in many cases these solutions are most easily constructed as the roots ofsome family of polynomials. In this paper we explore the ordinary and generalizedVandermonde determinant and these, often orthogonal, families of polynomials. Wealso consider the behavior of these determinants over other bounded and unboundedsurfaces of interest.

Keywords: Optimization — Orthogonal polynomials — Vandermonde determi-nant

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

7

8 Jonas Osterberg1, Sergei Silvestrov1, Karl Lundengard1

Biography

Jonas Daniel Osterberg was born in Vasteras-Sweden in1980. His first University studies were in engineeringphysics in 2002. From that he has studied computer sci-ence and aeronautical engineering at Malardalen Universityand Mid University in Sundsvall. Finally he graduated witha Bachelor in mathematics and a Master in mathematicsin 2014. He is currently a doctoral student and lecturer atMalardalen University.His current research interests are automated reasoning andthe use of numerical methods to attain analytical solutionsto problems, such as optimization over algebraic varieties.Also special matrices such as the Vandermonde matrix and related matrices andassociated numerical solution methods.

Half-exact Coherent Functors over PrincipalIdeal Domains (PIDs) and Dedekind Domains

Adson Banda1*

Abstract: We characterize half-exact coherent functors over PIDs and Dedekinddomains. We precisely show that every half-exact coherent functor over a PID andmore generally over a Dedekind domain is a direct sum of functors that arise from acomplex of projective modules. Now, given any covariant functor F over a noethe-rian ring A, there is an exact sequence

F(A)⊗− α−−−→ F −→ F0 −→ 0 (1)

where F0 = Coker α with the property F0(A) = 0. We show that if F is a half-exact coherent functor over a PID then F0 in (1) is left-exact. In this case, F0 ∼=HomA(N,−) for some finitely generated module N. We further show that over aPID, the sequence (1) splits, i.e F ∼= F(A)⊗−⊕F0. This shows that F arises froma complex since both F(A)⊗− and Hom(N,−) arise from a complex of projectivemodules. We prove the result over a Dedekind domain using localization by a primeideal ℘ of A. We show, similarly as in the PID case, that F0 is left-exact and that thesequence (1) splits.

Keywords: Coherent — Functors — Half-exact — Noetherian

1Division of Mathematics and Applied Mathematics, Linkoping University, Linkoping, Sweden ·Department of Mathematics and Statistics, University of Zambia, Lusaka, ZambiaCorresponding author: e-mail: [email protected]

9

10 Adson Banda1*

Biography

Adson Banda is a PhD student at Linkoping University un-der sandwich program. His studies are sponsored by ISPthrough Eastern Africa Universities Mathematics Program(EAUMP).He is also a lecturer in the department of Mathematics andStatistics at the University of Zambia. His research interestsinclude: commutative algebra, homological algebra and cat-egory theory.

Commutants in Crossed Product Algebras forPiecewise Constant Functions on the Real Line

Alex Behakanira Tumwesigye2*, Johan Richter1, Sergei Silvestrov1

Abstract: In this paper we consider commutants in crossed product algebras, foralgebras of piece-wise constant functions on the real line with Z. A description ofthe maximal commutative subalgebra (commutant) of the crossed product algebraof the said algebra with Z has already been given for the case where we have Nfixed jumps. Starting with an algebra A of piecewise constant functions with Nfixed jump points, we add a finite number of jumps, say m arbitrarily and considerthe algebra AS of piecewise constant functions with N + m jumps. We derive acondition for the algebras A and AS to be invariant under a bijection σ : R→ Rand compare the commutants A ′ and A ′

S .

Keywords: Crossed product — Piecewise constant — Algebras — Commutant

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, Sweden2Department of Mathematics, Makerere University, Kampala, UgandaCorresponding author: e-mail: [email protected]

11

12 Alex Behakanira Tumwesigye2*, Johan Richter1, Sergei Silvestrov1

Biography

Alex Behakanira Tumwesigye was born in Kampala,Uganda in 1982. I obtained a Bachelor of Science degreewith mathematics as a major and a master of mathematicsdegree from Makerere University, Kampala Uganda. I alsohave a postgraduate diploma from the International Centerfor Theoretical Physics (ICTP), Trieste, Italy and I am anAssistant Lecturer in the department of mathematics, Mak-erere University, Kampala.I am currently in the final stages of my PhD studies atMalardalen University, Sweden where I study commutingelements in noncommutative algebras in relation to one-dimensional dynamical systems. My research interests arein dynamical systems and operator algebras.

Reordering, Centralizers and Centers in anAlgebra with Three Generators and Lie TypeRelations

John Musonda 1,3*, Sergei Silvestrov 1, Sten Kaijser2

Abstract: We derive simple and explicit formulas for reordering elements in analgebra with three generators and Lie type relations. Centralizers and centers arecomputed as an example of an application of the formulas.

Keywords: Commutation relations — Operator algebra — Noncommutative alge-bra

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, Sweden2Department of Mathematics, Uppsala University, Uppsala, Sweden3Department of Mathematics & Statistics, University of Zambia, Lusaka, ZambiaCorresponding author: e-mail: [email protected]

13

14 John Musonda 1,3*, Sergei Silvestrov 1, Sten Kaijser2

Biography

John Musonda was born in Serenje, Zambia. He has a Bach-elor of Science in Mathematics from the University of Zam-bia, and a Master of Science in Mathematics from UppsalaUniversity in Sweden. Consequently, he has the experienceof having lived, worked and studied in both continents ofAfrica and Europe. He is currently a PhD student under thesandwich program between Malardalen University and theUniversity of Zambia under the sponsorship of the Interna-tional Science Program.His main topic of research is on orthogonal polynomials, op-erators and commutation relations, and these appear in manyareas of mathematics, physics and engineering where theyplay a vital role. For instance, orthogonal functions in general are central to thedevelopment of Fourier series and wavelets which are essential to signal process-ing. The -convergence of Fourier series is closely related to the -boundedness ofsingular integral operators. And many important relations in physical sciences arerepresented by operators satisfying various commutation relations. Such commuta-tion relations play key roles in such areas as quantum mechanics, wavelet analysis,spectral theory, representation theory, and many others.

Numerical Stability of the Escalator BoxcarTrain under Reducing System of OrdinaryDifferential Equations

Tin Nwe Aye1*, Linus Carlsson2, Sergei Silvestrov2

Abstract: The Escalator Boxcar Train(EBT) is one of the most popular numericalmethods to study the dynamics of physiologically structured population models. TheEBT-model can be adapted to numerically solve population dynamics of ecologicaland biological systems with continuous reproduction. The original EBT-model ac-cumulates a dynamic system of ODE’s to solve in each time step.In this project, we propose an EBT-solver to overcome some computational disad-vantageous of the EBT method which includes the automatic feature of mergingcohorts, in particular we apply the model to a colony of Daphnia pulex.

Keywords: Escalator boxcar train — Physiologically structured population models— Daphnia model

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, Sweden and Universityof Mandalay, Myanmar2Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

15

16 Tin Nwe Aye1*, Linus Carlsson2, Sergei Silvestrov2

Biography

Tin Nwe Aye was born in Mandalay, Myanmar in 1989. Shehas a Bachelor of Science degree with mathematics as a ma-jor from Yadanarbon University, Myanmar. She also has aMaster of Science degree with mathematics as a major anda Master of Research from Mandalay University, Myanmar.She was appointed as a tutor in the department of Mathe-matics, Sagaing University of Education in September 2012and has been working as an assistant lecturer in departmentof Mathematics, Mandalay University since 2016.She is now studying her PhD at Malardalen University, Swe-den, supported by International Science Programme (ISP) incollaboration with Cambodia, Laos and Myanmar. Her re-search interests are partial differential equations and func-tional analysis.

Data Analysis of Nanoliquid Thin Film Flowover an Unsteady Stretching Sheet in Presence ofMagnetic Field

Prashant G Metri1*, Sergei Silvestrov1

Abstract: A mathematical model is developed to analyze a nanoliquid film flowover an unsteady stretching sheet in presence of magnetic field. The flow prob-lem within a nanoliquid film of an unsteady stretching sheet, where the governingpartial differential equations with the auxiliary conditions are reduced to ordinarydifferential equations with the appropriate corresponding condition via similaritytransformations. The resulting non-linear ordinary differential equations are solvednumerically using the Runge-Kutta-Fehlberg and Newton-Raphson schemes basedon the shooting technique. A relationship between film thickness β and the un-steadiness parameter S is found. Furthermore, the effect of unsteadiness parameterS, the volume fraction of nanoliquid φ , Prandtl number Pr and the magnetic fieldparameter M on the temperature distributions are presented and discussed in detail.Presented data analysis shows that the combined effect of different types of nanoliq-uid, magnetic field and viscous dissipation has a significant influence in controllingthe dynamics of the considered problem.

Keywords: Boundary layer flow–Data analysis–Magnetic field–Nanoliquid–Thinfilm

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

17

18 Prashant G Metri1*, Sergei Silvestrov1

Biography

Prashant G Metri was born in Bijapur, India in 1987. Hereceived the B.Sc. and M.Sc. degrees in Applied Mathemat-ics from the Gulbarga University, India in 2009 and 2011,respectively. He is currently a doctoral student at the Divi-sion of Applied Mathematics, Malardalen University underthe Erasmus Mundus project FUSION (Featured Europe andSouth-East Asia mobility network).He has published a number of journal and conference papersin the field of applied mathematics, mathematical physics,heat and mass transfer and instability problems. As a re-searcher he has contributed one scientific project funded bythe Ministry of Human Resource Development, Governmentof India.

Lie Symmetries of the Black Scholes TypeEquations in Financial Mathematics

Asaph Keikara Muhumuza1*, Anatoliy Malyarenko1, Sergei Silvestrov 1

Abstract: Stochastic differential equations in financial mathematics are stronglylinked to partial differential equations. Lie groups and Lie algebras are a strong toolin analysis of global solutions of partial differential equations that occur in most ofmathematical models in finance. We give the the complete symmetry analysis of theBlack-Scholes type models.

Keywords: Partial differential equations in finance — Black-Scholes type models— Lie group classification — Lie symmetry analysis

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

19

20 Asaph Keikara Muhumuza1*, Anatoliy Malyarenko1, Sergei Silvestrov 1

Biography

Asaph Keikara Muhumuza was born in Mbarara WesternUganda in 1975. He holds a Bachelor of Science with Ed-ucation, BSc.Ed., degree with Mathematics as a major and aMaster of Science in Mathematics, MSc.Maths., from Mak-erere University, Kampala, Uganda.He is a full time lecture at the department of Mathematics,Busitema University and has been in the same department,since October 2007.He is currently pursuing PhD at Malardalen University, Swe-den on sandwich mode under the sponsorship of SIDA-Makerere Bilateral Program. His research interests are inLie symmetry and Wavelets solutions of partial differentialequations.

Lattice Pricing Beyond Black Scholes Model

Carolyne Ogutu1*, Karl Lundengard1, Ivivi Mwaniki2, Sergei Silvestrov1, PatrickWeke2

Abstract: Derivatives can be defined as an agreement based on an underlying assetor a non-tradeable asset. Options are derivatives that give the holder the right butnot obligation to exercise it before or at maturity. The seminal model by Black andScholes doesn’t reflect real asset dynamics due to its continuous trading and con-stant volatility assumptions. Cox et al first developed lattices binomial lattice - as anumerical scheme that discretizes the lifespan of the option by dividing it into timesteps of equal length. Dynamic programming is then used to obtain the option priceat inception. Other lattice schemes have been developed such as trinomial and pen-tanomial. In this paper, we undertake a comprehensive study of lattice models pre(Cox et al and family) and post (Amin and family) Black Scholes model. In addition,we develop an improved lattice-pricing model, which enhances the assumptions bypost-Black Scholes lattice models.

Keywords: Lattice models — moment-matching — multinomial — Vandermondematrix — option pricing

1Division of Applied Mathematics, UKK, Malardalen University, Vasteras, Sweden2School of Mathematics, University of Nairobi, KenyaCorresponding author: e-mail: [email protected]

21

22 Authors Suppressed Due to Excessive Length

Biography

Carolyne Ogutu is currently a PhD research fellow atMalardalen University in Sweden sponsored by Interna-tional Science Programme (ISP) in collaboration withthe East African Universities Mathematics Programme(EAUMP) and School of Mathematics, University ofNairobi.Her PhD focuses on mathematical finance. She is also alecturer at the Division of Actuarial Science and FinancialMathematics at the School of Mathematics, University ofNairobi with pedagogical interests in financial and actuar-ial mathematics and life contingencies.She was born in Kisumu, in western part of Kenya in 1980and has studied Mathematics in the undergraduate level andActuarial Science at the graduate level both at the Universityof Nairobi, Kenya. Her research interests span the areas offinancial modelling and actuarial risk analysis.

Pricing European Options undertwo-dimensional Black-Scholes PartialDifferential Equation by using theCrank-Nicholson Finite Difference Method

Jean-Paul Murara1, 3*, Betuel Canhanga2,3, Anatoliy Malyarenko3, Ying Ni3,Sergei Silvestrov3

Abstract: In the option pricing process, Black-Scholes in 1973 solved a partial dif-ferential equation and introduced a model to determine the price of European Op-tions. Many researchers improved Black-Scholes model afterwards. Christoffersenproved in 2009 that models with two stochastic volatilities capture better the skew-ness and the smiles of the volatilities, meaning that they can more accurately deter-mine the options prices. Canhanga et al. in 2014 and Chiarella and Ziveyi in 2013used the model introduced by Christoffersen to determine European and Americanoption prices respectively.While dealing with many problems in financial engineering, the application of Par-tial Differential Equations (PDEs) is fundamental to explain the changes that occurin the evolved systems. Some families of this type of equations are known to havethe so-called classical solutions. Others can be transformed into simple PDEs, forexample by using scaling methods, Laplace and Fourier transforms, afterwards onecan compute their solutions. Moreover, in many cases the PDEs that characterize thereal life problems do not have known forms of solutions. In this occasion, numericalmethods are considered in order to obtain the approximate solutions of the PDEs.In the present paper, we consider the option pricing problems that involves a two-dimensional Black-Scholes PDE as the one obtained by Canhanga et al. in 2014, andinstead of solving it by the approximation approach presented by Conze in 2010 weperform the Crank - Nicholson finite difference method. Comparing examples areincluded in the paper.

Keywords: Stochastic volatility — Two-dimensional Black-Scholes PDE — Crank-Nicholson finite difference method

1College of Science and Technology,School of Sciences, Department of Applied Mathematics, Uni-versity of Rwanda, Kigali, Rwanda2Faculty of Sciences, Department of Mathematics and Computer Sciences, Eduardo MondlaneUniversity, Box 257, Maputo, Mozambique3Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

23

24 Authors Suppressed Due to Excessive Length

Biography

Jean-Paul Murara is an assistant lecturer within the Depart-ment of Mathematics in the University of Rwanda. Since2013, he is a PhD student in the School of Education, Cul-ture and Communication at Malardalen University. His areaof interest is Financial Mathematics.

Just in Time Production System, Logistics andQueueing

Gyan Bahadur Thapa 1*, Sushil Ghimire 1, Ram Prasad Ghimire 2, SergeiSilvestrov 3

Abstract: In this talk, we present some ideas of just-in-time production systemwith mathematical models interlinking with supply chain logistics. We formulatea truck sequencing problem in mathematical form which is NP-hard. Further, wedeal with the transient analysis of multi-server queuing system subject to break-downs. The system does not accept the queue of the waiting customers. If the newcustomer upon its arrival finds n customers already present in the system, then it isrejected. Customers arrive to the system in Poisson fashion and are served exponen-tially. The main purpose is to find the proportion of lost customers, mean number ofcustomers in service, utilization factor of servers, mean number of broken serversand utilization of repair capacity, all at any instants. By varying different param-eters, the system behavior is examined with the help of numerical illustrations byusing computing software so as to show the model under study has ample practicalapplications.

Keywords: Just-in-time production system — Multi-server queuing system —Supply chain logistics

1Pulchowk Campus, Institute of Engineering, Tribhuvan University, Nepal2Department of Mathematical Sciences, School of Science, Kathmandu University, Nepal3Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

25

26 Gyan Bahadur Thapa 1*, Sushil Ghimire 1, Ram Prasad Ghimire 2, Sergei Silvestrov 3

Biography

Gyan Bahadur Thapa received his PhD in Mathematics fromTribhuvan University, Nepal in 2012 with sandwich researchvisits in Germany and UK. He received his second PhD inApplied Mathematics from Malardalen University, Swedenin 2015. Currently, he is working as post doctoral researchfellow under Erasmus Mundus Project in the Department ofMathematics, University of Evora, Portugal.He was lecturer of mathematics in Saraswati Campus, Kath-mandu during 1997-2000. Now, he is working in Instituteof Engineering, Tribhuvan University, Nepal as an Asso-ciate Professor. His research interests include Discrete Op-timization, Operations Research, Mathematical Modellingand Queueing System.

Asymptotic Expansion for Pricing EuropeanOption in a Market Model with Two StochasticVolatilities

Betuel Canhanga1*, Anatoliy Malyarenko2, Ying Ni2, Sergei Silvestrov2, MilicaRancic2

Abstract: The concept of stochastic volatility brought significant changes in thefield of Financial Mathematics. Attempting to construct models that represent closerthe real markets, Cox, Ross, Rubinstein, and Heston suggested a price dynamic us-ing single factor stochastic volatility. Later on in 2009, Christoffersen showed em-pirically ”why multi factor stochastic volatility models work so well”, droppingthe lightness of single factor stochastic volatility models. Four years late Chiarellaand Ziveyi considered the Christoffersen ideas and presented a model for an un-derlying asset whose price is governed by two factor stochastic volatilities of meanreversion. They derived an integral form solution of the boundary value problemassociated to the option price. Applying method of characteristics, Fourier trans-forms and Laplace transforms they computed an approximate formula for pricingAmerican options. The huge calculation involved in the Chiarella and Ziveyi papereven for computation of European Options Prices, motivated in 2014 the authors ofthis paper to investigate another approach to compute European Options prices on aChiarella and Ziveyi type model. Using the first and second order asymptotic expan-sion method we are going to present a close form solution for European options andprovided experimental and numerical studies on investigating the accuracy of theapproximation formulae given by the asymptotic expansion. The obtained resultsare compared to those obtained when considering Chiarella and Ziveyi approach.

Keywords: Option pricing model — Asymptotic expansion — Numerical studies

1Eduardo Mondlane University, Faculty of Sciences, Department of Mathematics and ComputerSciences, Maputo, Mozambique2Division of Applied Mathematics, UKK, Malardalen University, Vasteras, SwedenCorresponding author: e-mail: [email protected]

27

28 Authors Suppressed Due to Excessive Length

Biography

Betuel Canhanga was born in Quelimane, Mozambique.He received his Bachelor degree in Computer Sciences atEduardo Mondlane University in 2005, Master in AppliedMathematics at Lulea University of Technology in 2009, andDoctor degree in Applied Mathematics at Malrdalen Univer-sity in 2016.He works as a teacher at Eduardo Mondlane University,Mozambique.